perfect competition *made by rachel stand* :). i. perfect competition: a model a. basic definitions...

TRANSCRIPT

Perfect Competition

*MADE BY RACHEL STAND* :)

I. Perfect Competition: A Model

A. Basic Definitions1. Perfect Competition: a model of the market based primarily on the assumption that a large number of firms produce identical goods consumed by a large number of buyers. 2. Other assumptions include ease of entry and exit from the market and complete information for buyers and sellers in the market. A. Assumptions of the Modela. No one buyer or seller has any influence over the market price. Individuals who must take the market price as given are called price takers. • Identical goods

• One unit of the good or service cannot be differentiated from any other on any basis. • The goods and services in a perfectly competitive market are sometime called homogeneous.• Since the goods are identical, there is no brand loyalty. You don’t know or care the brand of the good (ex: apples, lettuce)

• A large number of buyers and sellers• A “large number” is not a specific number of buyers and sellers.• A “large number” is however many there must be to assure that no one of them can influence the market price.

I. Perfect Competition: A Model

• Ease of entry and exit (in the long run)4. Because of this assumption, firms must deal not only with current competitors but also with potential competitors. 5. Because of this assumption, firms are free to exit one market and enter another. Ease of exit is necessary to assume ease of entry.6. Example: farming (switching from growing one crop to another is easy).

• Complete information• All sellers have complete information about prices, technology, and all other information relevant to the operation of the market.• All buyers know the prices offered by every seller.• The assumption of complete information implies that acquiring information is low cost.

• Perfect Competition and the Real World• The strong assumptions of the perfectly competitive market may appear unrealistic.• The of demand and supply presented in previous chapters is based on the perfectly competitive market.• Even though the actual markets of the world seldom meet all the assumptions of the perfectly competitive model, the model is strong enough to explain many real- world phenomena.

II. Output Determination in the Short Run

A. Price and Revenue1. As price takers, competitive firms expect that market price to prevail whether they produce large amounts or small amounts.2.Total Revenue:

a. Total revenue for a perfectly competitive firm: the market price times the quantity that the firm produces.b. The total revenue curve is a linear upward- sloping line. If the market price changes, the total revenue curve pivots around the origin.

3.Price, marginal revenue, and average revenuea. Marginal Revenue: the change in total revenue generated by selling an additional unit of output. b. Marginal revenue= the slope of the total revenue curve (the marginal revenue curve is the derivative of the total revenue curve). c. Since market price is fixed for the perfectly competitive firm, marginal revenue equals the price.

II. Output Determination in the Short Run

d. Average Revenue: the total revenue divided by quantity. Since all units sell for the same price, the average revenue must equal price. 1. The marginal revenue curve is a horizontal line at the market price. The average revenue curve is the same horizontal line at the market price.

1.Marginal revenue, price, and demand for the perfectly competitive firm.

1. Marginal revenue= average revenue= price• The demand curve for an individual perfectly competitive firm is horizontal at the price. The AR and MR curves coincide with the individual firm’s demand curve. Marginal revenue= firm’s demand curve.

• Revenue, Cost, and Economic Profit• A firm’s economic profit= total revenue minus total opportunity cost of its operations. • Marginal cost= firm’s supply curve. • The total revenue curve of a perfectly competitive firm has a constant slope. The total cost curve becomes ever steeper as diminishing returns set in. •The maximum profit is found where the slopes of the total revenue curve and the total cost curve are equal.• Applying the Marginal Decision Rule• Because marginal revenue and marginal cost are the slopes of the total revenue and total cost curves respectively, profit is maximized where marginal revenue equals marginal cost. • A producer makes $0 economic profit

• If a worker makes $80,000 at job A but could have made $80,000 at job B, the worker has made $0 economic profit because they did not do any better at job A than at the next best alternative.

II. Output Determination in the Short Run2. Marginal revenue and marginal cost are the marginal benefit

and marginal cost of selling an additional unita. The marginal decision rule says to expand production if MR exceeds MC, to decrease production if MC exceeds MR, and to retain the present output if MR= MC.b. Economic profit can be demonstrated numerically or graphically by multiplying economic profit per unit by the number of units produced.• Economic Losses in the Short Run• Background information

• In the short run, the firm cannot leave the industry because one or more of its inputs are fixed.• As a result, even if a firm shuts down, it must pay fixed costs.• Thus in the short run, a firm may run an economic loss, the amount by which its total cost exceeds its total revenue.

•Producing to minimize economic losses• In the short run, a perfectly competitive firm will continue to produce and sell even at an economic loss if the price is above the firm’s average variable cost. • The minimum level of average variable cost, which occurs at the intersection of the marginal cost curve and the average variable cost curve, is the shutdown point.

II. Output Determination in the Short Run

• Marginal Cost and SupplyE. A supply curve tells us the quantity that will be produced at each price, which is what the marginal cost curve tells us.F.The marginal cost curve is the firm’s supply curve in the short run for prices above the minimum value of average variable cost. At prices below average variable cost, the firm’s output is zero.

III. Perfect Competition in the Long RunA. Economic Profit and Economic Loss

1. Economic versus accounting concepts of profit and lossa. Explicit costs: include charges that must be paid for factors of production such as labor and capital, together with an estimate of depreciation. b. Profit computed using explicit costs is accounting profit.• A cost that is included in the economic concept of opportunity cost but that is not an explicit cost is called an implicit cost.• Profit computed using explicit and implicit costs is economic profit.

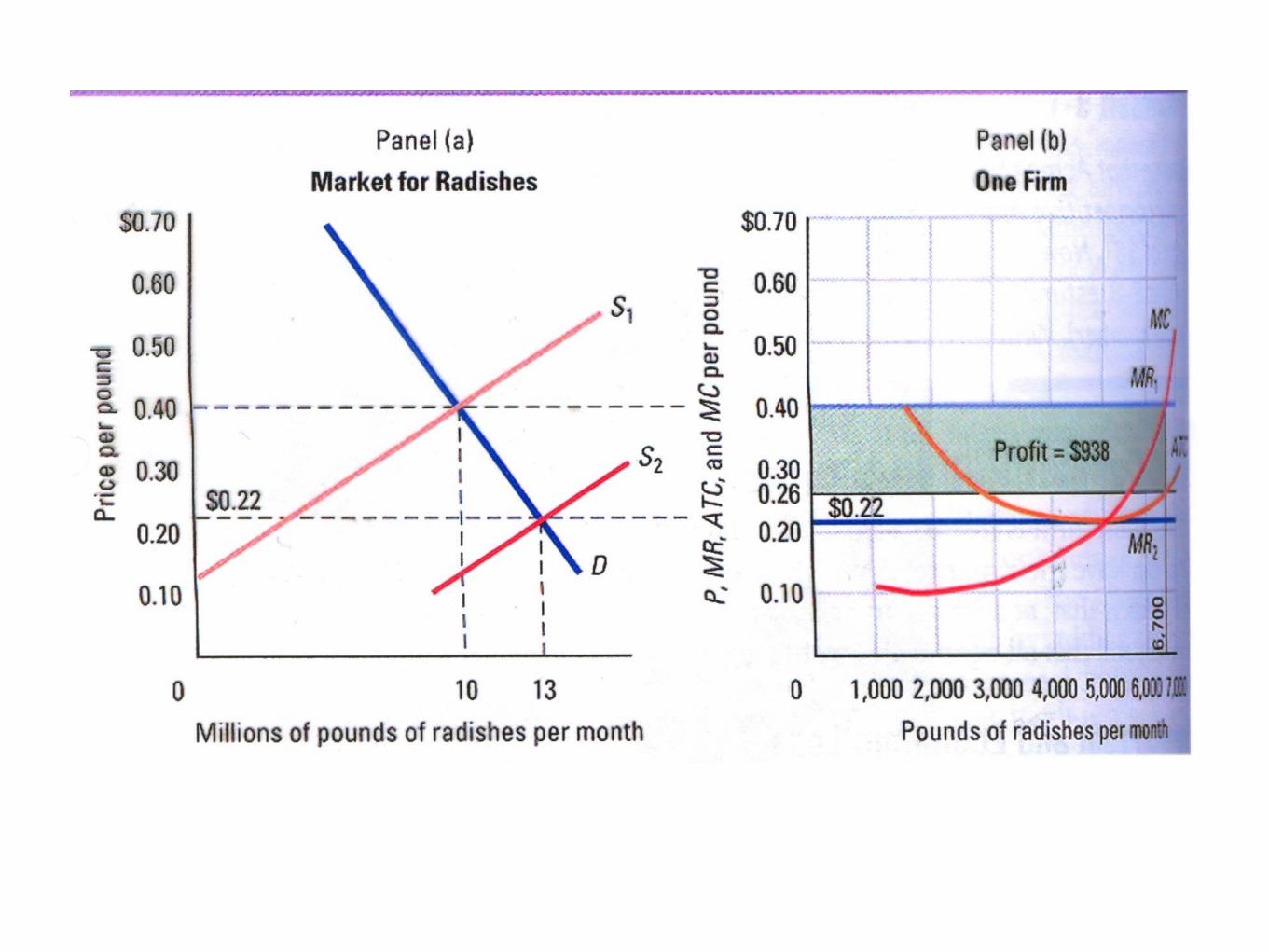

• The long run and zero economic profits- economic profits in a system of perfectly competitive markets will, in the long run, be driven to zero in all industries.

III. Perfect Competition in the Long Run

3. Eliminating economic profit: the role of entrya. Economic profits encourage new firms to enter the market thereby increasing the market supply and reducing the market price.b. The reduction in the market price continues until the economic profit is eliminated.

4. Eliminating losses: the role of exit:a. Economic losses encourage some firms to exit the market, thereby decreasing the market supply and increasing the market price. b. The increase in the market price continues until the economic losses are eliminated.

5. Entry, exit, and production costs.a. When expansion of an industry does not affect the prices of factors of production, it is a constant- cost industry. b. An industry in which the entry of new firms bids up the prices of factors of production and thus increases production costs is an increasing- cost industry. c. An industry in which production costs fall as new firms enter in the long run, is a decreasing- cost industry.• In a constant- cost industry, exit will not affect the input prices of remaining firms. In an increasing- cost industry, exit will reduce the input prices of remaining firms. In a decreasing- cost industry, input prices may rise with the exit of existing firms.

III. Perfect Competition in the Long Run

i. The long- run industry supply curve is a curve that relates the price of a good or service to the quantity produced after all long- run adjustments to a price change have been completed. ii. Every point on a long- run industry supply curve in a perfectly competitive industry therefore shows a price and quantity supplied at which firms in the industry are earning zero economic profit.

B. Changes in Demand and in Production Cost1. Changes in demand

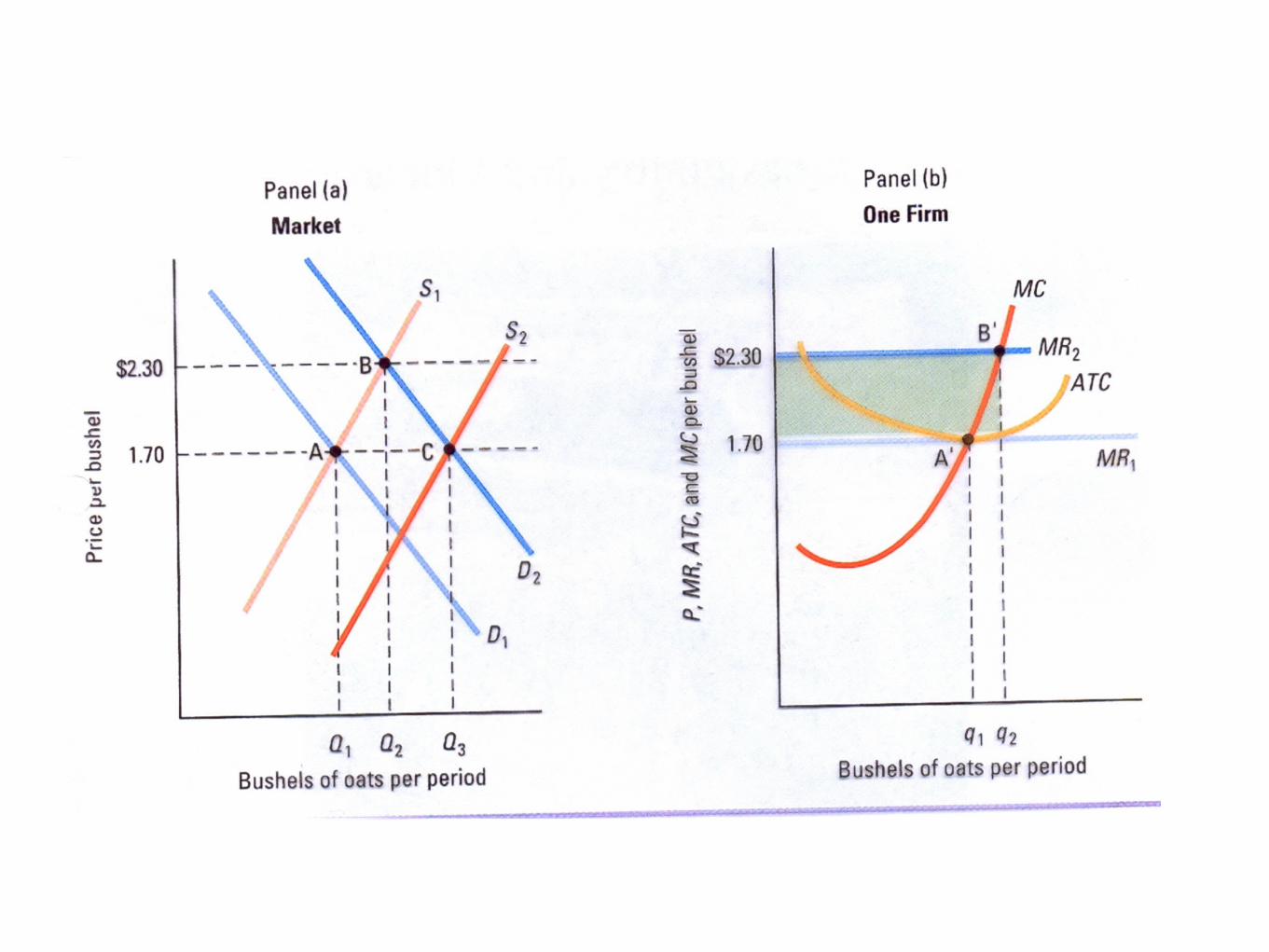

a. A change in demand for any reason causes a change in the market price, thus shifting the marginal revenue curves of firms in the industryb. An increase in demand generates short- term profits that attract other firms to the industry, thereby wiping out the economic profits for the enlarged number of firms. c. A decrease in demand generates short- term losses that cause some firms to exit the industry, thereby restoring the zero economic profit position for the remaining firms.

a. Changes in production costa. Changes in production cost shift the ATC curveb. If the changes in production cost affect variable costs, a firm’s marginal cost curves will shift in addition to the ATC curve.

c. Any change in marginal cost produces a similar change in industry supply.d. A reduction in production cost shifts the firm’s cost curves down, creating economic profit that is eliminated by the entry of new firms to the industry.e. An increase in production cost shifts the firm’s cost curves up creating economic loss that is eliminated by the exit of firms from the industry

III. Perfect Competition in the Long Run