perception and attitude towards the mutual fund investors...

TRANSCRIPT

CHAPTER IV

4.1 INTRODUCTION

4.2 RELIABILITY ANALYSIS

4.3 INVESTORS PERCEPTION OF MUTUAL FUND INVESTMENT

4.4 INVESTORS ATTITUDES OF MUTUAL FUND INVESTMENT

4.5 REASON FOR PREFERRING MUTUAL FUND INVESTMENT

4.6 SOCIO-ECONOMIC CONDITION OF MUTUAL FUND INVESTMENT

4.7 MOTIVATION FACTOR OF MUTUAL FUND INVESTMENT

4.8 PURPOSE OF MUTUAL FUND INVESTMENT

4.9 AWARENESS OF THE SCHEMES OF MUTUAL FUND INVESTMENT

PERCEPTION AND ATTITUDE TOWARDS THE MUTUAL

FUND INVESTORS IN NAMAKKAL DISTRICT

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

89

CHAPTER IV

PERCEPTION AND ATTITUDE TOWARDS MUTUAL FUND

INVESTORS IN NAMAKKAL DISTRICT

4.1 INTRODUCTION

The Fourth chapter of the present study gives the analysis of perceptions

and attitude of the Mutual Fund Investors in the study area. Before perception, the

investors must have a knowledge of sources of Mutual fund Investment, various

schemes of mutual fund investment, various schemes of mutual funds, purposes

and facilities. This chapter analyses the perception of mutual fund investors by

using data related to the Gender of the Respondent, their Marital Status, Age,

Educational Qualification, Occupations and Income.

The Second part of this chapter analyses the attitude of the Mutual Fund

Investors. The Garrett Ranking Technique was employed to analyze the preference

given by the mutual fund Investors towards the mutual fund investment. After that,

the inter-correlation and multiple regression model have been fitted to analyse the

determinants of mutual fund Investors to invest their fund in the mutual funds.

The association between the economic conditions and the various factors related to

the mutual fund Investors has been analysed.

4.2 RELIABILITY ANALYSIS

The reliability of scales used in this study was calculated by Cronbach's

coefficient alpha. Cronbach‟s alpha reliability coefficient normally ranges between

0 and 1. However, there is actually no lower limit to the coefficient. The closer

Cronbach‟s alpha coefficient is 1.0 the greater the internal consistency of the items

in the scale. The coefficient alpha values exceeded the minimum standard of .70.

It has provided good estimates of internal consistency reliability.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

90

• The formula is as follows:

• K is the number of items in the scale.

• R is the average correlation pairs of items.

• As the number of items in the scale (k) increases, the value of alpha

becomes larger.

• If the inter-correlation between items is large, the corresponding alpha will

also be larger.

Table 4.1 Presents Reliability scales -opinion factors related to level of

satisfaction towards Mutual fund Investment.

Table 4.1

Reliability Scales - Opinion Factors Related to Level of Satisfaction towards

Mutual Fund Investment

S. No. Opinion (Items)

Scale

Mean If

Item

Deleted

Cronbach's

Alpha If

Item

Deleted

1 Schemes 64.42 .710

2 Risk and Return 63.92 .713

3 Services 64.42 .700

4 Relationship 65.22 .751

5 Claim 64.55 .762

6 Grievances 64.41 .730

7 Fund management 64.22 .729

8 NAV Updating 64.79 .703

9 Security 64.63 .727

10 Entry Load 64.51 .716

11 Exit Load 64.79 .700

rk

kr

)1(1

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

91

S. No. Opinion (Items)

Scale

Mean If

Item

Deleted

Cronbach's

Alpha If

Item

Deleted

12 New Fund Scheme (or) offer based on

Return 64.41 .701

13 Existing Fund based on return 64.51 .700

14 Asset management company service

(AMCS) 64.76 .700

15 Promptness in information giving 64.49 .707

16 Clarification towards technical doubts 64.62 .700

17 Reminding of premium payment 64.49 .709

18 Informing time about default payment 64.22 .700

19 Satisfied with remedial measures

(Redressal)

64.82 .700

Mean 68.12

Variance 76.55

Std. Deviation 8.75

Cronbach's Alpha Based On Standardized Items 0.700

Cronbach's Alpha 0.719

No. Of Items 19

It is inferred from table 4.1 that the reliability scales used for this study was

calculated by the closer Cronbach‟s alpha coefficient is 1.0 the greater the internal

consistency of the items in the scale. Based upon the formula a= rk / [1 + (k -1) r]

where k is the number of items considered and r is the mean of the inter-item

correlations the size of alpha is determined by both the number of items in the

scale and the mean inter-item correlations. The coefficient alpha values exceeded

the minimum standard of 0.70. It has provided good estimates of internal

consistency reliability. As shown in Table 4.1, all constructs obtained an

acceptable level of a coefficient alpha above 0.70, indicating that the scales used

in this study were reliable. It provides the following rules of thumb: “_ > .9 –

Excellent, _ > .8 – Good, _ > .7 – Acceptable, _ > .6 – Questionable, _ > .5 – Poor

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

92

and _ < .5 – Unacceptable”. While increasing the value of alpha is partially

dependent upon the number of items in the scale, it should be noted that this has

diminishing returns. It should also be noted that an alpha of 0.719 is probably a

reasonable goal. It should also be noted that while a high value for Cronbach‟s

alpha indicates good internal consistency of the items in the scale, it does not

mean that the scale is unidimensional. Factor analysis is a method to determine the

dimensionality of a scale.

Table 4.2 is Shows the Reliability Scales-Factors Related to Sources of

Information for Selecting the Schemes.

Table 4.2

Reliability Scales -Factors Related to Sources of Information

for Selecting the Schemes

S. No. Sources (Items)

Scale Mean

If Item

Deleted

Cronbach's

Alpha If

Item

Deleted

1 Funds/scheme's performance record 88.30 .870

2 Funds/scheme's reputation or brand name 88.50 .873

3 Scheme's expense ratio 88.90 .857

4 Scheme's portfolio of investment 88.90 .868

5 Reputation of scheme(s),portfolio

manager(s) 88.50 .866

6 Withdrawal facilities 88.50 .872

7 Favorable rating by a rating agency 88.90 .866

8 Innovativeness of the scheme 89.20 .870

9 Products with tax benefits 88.60 .874

10 Entry and Exit load 88.70 .860

11 Reputation of a sponsoring firm 88.60 .870

12 Sponsor offers a wide range of schemes

with different investment objectives 88.40 .854

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

93

S. No. Sources (Items)

Scale Mean

If Item

Deleted

Cronbach's

Alpha If

Item

Deleted

13 Sponsor has a recognized brand name 88.80 .847

14 Sponsor has a well developed Agency

Network / Infrastructure 88.50 .861

15 Sponsor has an efficient research wing 88.70 .869

16 Sponsor's expertise in managing money 88.50 .859

17

Disclosure of investment objectives,

method and periodicity of valuation in

advertisement

88.50 .864

18

Disclosure of the method and periodicity

of the scheme's sales and repurchase in

the offer documents

88.30 .855

19 Disclosure of NAV on every trading day 88.60 .870

20 Disclosure of deviation of the

investments from the original pattern 88.40 .876

21 Disclosure of scheme's investments on

every trading days 88.80 .853

22 Mutual Fund Investor's grievance

redressal machinery 89.00 .855

23

Fringe benefit like free insurance, free

credit card, loans on collateral, tax

benefits etc.

89.30 .863

Mean 92.7

Variance 188.68

Std. Deviation 13.74

Cronbach's Alpha Based On Standardized Items 0.872

Cronbach's Alpha 0.869

No. Of Items 23

Table 4.2 reveals that all the twenty-three measurement scale items are

reliable as the Cronbach alpha coefficient of 0.869. It is greater than the threshold

level of 0.70. It‟s provided good estimates of internal consistency reliability and

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

94

also coefficient alpha values ranged from 0.847 to 0.876 for all the constructs. It is

indicating that the scales used in this study were reliable. It clearly indicates that

the above scale items are consistent with each other and they are the reliable

measures of sources of information for selection of scheme.

Table 4.3 shows Reliability scales - factors related to extent of awareness

on the schemes of mutual fund.

Table 4.3

Reliability Scales- Factors Related to Extent of Awareness on the

Schemes of Mutual Fund

S. No. Schemes (Items)

Scale Mean

If Item

Deleted

Cronbach's

Alpha If Item

Deleted

1 Income fund scheme 29.50 .806

2 Growth fund Scheme 29.60 .812

3 Conservative fund scheme 30.10 .801

4 Equity fund 29.40 .841

5 Bond fund 30.20 .836

6 Balanced fund 29.90 .805

7 Sectoral fund 30.20 .842

8 Fund of funds 30.00 .823

9 Leverage fund 29.90 .777

10 Index fund 29.80 .787

11 Tax savings schemes 29.60 .812

12 Gold exchange traded fund 29.80 .843

13 Real estate fund 29.90 .789

14 Other schemes 30.70 .833

Mean 32.2

Variance 28.83

Std. Deviation 5.37

Cronbach's Alpha Based On Standardized Items 0.812

Cronbach's Alpha 0.828

No. Of Items 14

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

95

It is observed from table 4.3 that all the fourteen measurement scale items

are reliable as the Cronbach alpha coefficient of 0.828. It is greater than the

threshold level of 0.70. It has provided good estimates of internal consistency

reliability and also the coefficient alpha values ranged from 0.777 to 0.843 for all

the constructs. It is indicating that the scales used in this study were reliable. It clearly

indicates that the above scale items are consistent with each other and they are the

reliable measures of the extent of awareness on the schemes of mutual fund.

Table 4.4 Reliability shows scales-factors related to purpose of Mutual fund

investment.

Table 4.4

Reliability Scales - Factors Related to Purpose of Mutual Fund Investment

S. No. Purpose(Items) Scale Mean If

Item Deleted

Cronbach's

Alpha If Item

Deleted

1 Savings 28.90 .700

2 Better investments 28.90 .694

3 Tax Benefit 29.60 .713

4 Children's Education 28.70 .717

5 Marriage 29.20 .783

6 Medical Expenses 29.40 .639

7 Low Risk 28.00 .758

8 Switching Facility 29.10 .713

9 Other purpose 29.00 .688

Mean 32.6

Variance 44.75

Std. Deviation 6.69

Cronbach's Alpha Based On Standardized Items 0.717

Cronbach's Alpha 0.736

No. Of Items 9

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

96

Table 4.4 shows that all the nine measurement scale items are reliable as

the Cronbach alpha coefficient is 0.736. It is greater than the threshold level of

0.70. It has provided good estimates of internal consistency reliability and also the

coefficient alpha values ranged from 0.688 to 0.758 for all the constructs. It is

indicating that the scales used in this study were reliable. It clearly indicates that

the above scale items are consistent with each other and they are the reliable

measures of the purpose of mutual fund investment and opinion.

Table 4.5 presents Reliability scales - factors related to facilities provided

by the mutual fund companies.

Table 4.5

Reliability Scales - Factors Related to Facilities Provided by the

Mutual Fund Companies in India

S. No. Facilities (Items)

Scale

Mean If

Item

Deleted

Cronbach's

Alpha If

Item

Deleted

1 Message services 28.20 .927

2 Online Services 28.00 .934

3 Computer Age Management Services (CAMS) 28.40 .925

4 Information directly by mutual fund

companies

28.20 .930

5 Information through mutual fund agent 28.40 .936

6 Information about mutual fund through

specialized journals

28.20 .933

7 Switching facilities 28.00 .933

8 Systematic Investment Plan (SIP) 28.10 .934

9 Direct Investment 28.10 .926

Mean 31.7

Variance 82.62

Std. Deviation 9.09

Cronbach's Alpha Based On Standardized Items 0.939

Cronbach's Alpha 0.938

No. Of Items 9

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

97

Table 4.5 reveals that all the nine measurement scale items are reliable as

the Cronbach alpha coefficient of 0.938. It is greater than the threshold level of

0.70. It has provided good estimates is internal consistency reliability and also the

coefficient alpha values ranged from 0.925 to 0.934 for all the constructs. It is

indicating that the scales used in this study were reliable. It clearly indicates that

the above scale items are consistent with each other and they are the reliable measures

of the factors related to facilities provided by the mutual fund companies.

4.3 INVESTORS‟ PERCEPTION OF MUTUAL FUND INVESTMENT

Perception is a significant concept in understanding and studying the

behavior of mutual fund Investors towards mutual fund Investment. Under this

part, the perception of mutual fund investors have been analyzed in terms of

Gender, Age Marital Status, Occupation, Educational Qualification, Income

earned with suitable statistical tools.

4.3.1 Gender

Gender may have an influence in the investors‟ perception. Mobility and

Contact of male members may be higher than female. So male investors‟ may

have high level of perception.

Table 4.6

Gender of the Respondents

Gender Freq % Mean S.D Range

MIN MAX

Male 280 70.0 96.62 11.71 69.00 112.00

Female 120 30.0 83.55 13.80 69.00 112.00

Total 400 100.0

Source: Primary Data

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

98

It is represented from the table 4.6 that 70 per cent of the respondents are

males and that investors perception of mutual fund investment on the male ranged

between 69 and 112 with an average of 96.62 and the remaining 30 per cent of the

respondents are females and that investors perception of mutual fund investment

on the females ranged between 69 and 112 with an average of 83.55. Thus the

table reveals a high perception on male respondents of mutual fund investment

than female respondents.

In order to find out the association between the gender and the level of

perception towards mutual fund investor, tables 4.7 and 4.8 were presented.

Table 4.7

Gender and Level of Investors Perception of Mutual Fund Investment

Gender Level of Perception

Total Low Medium High

Male Freq 45 133 102 280

% 11.3 33.3 25.5 70

Female Freq 75 27 18 120

% 18.8 6.8 4.5 30

Total Freq 120 160 120 400

% 30.0 40.0 30.0 100.0

Source: Primary Data

Table 4.7 depicts that out of 400 mutual fund investors, 280 (70 per cent)

are males and among them 45 (11.3%) investors have a low level perception;

133 (33.3%) investors have a medium level of perception and 102 (25.5%)

investors have a high level of perception on the mutual fund investment.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

99

Among 120 (30%) female investors, 75 (18.8%) investors have a low level

of perception, 27(6.8%) investors have a medium level of perception and 18(4.5%)

investors have a high level of perception on the mutual fund investment.

Regarding the investors perception of mutual fund investment, the lowest

level was found for the female investors than that of the male investors. As far as

the high level of perception is concerned, the male investors outnumbered the

female investors.

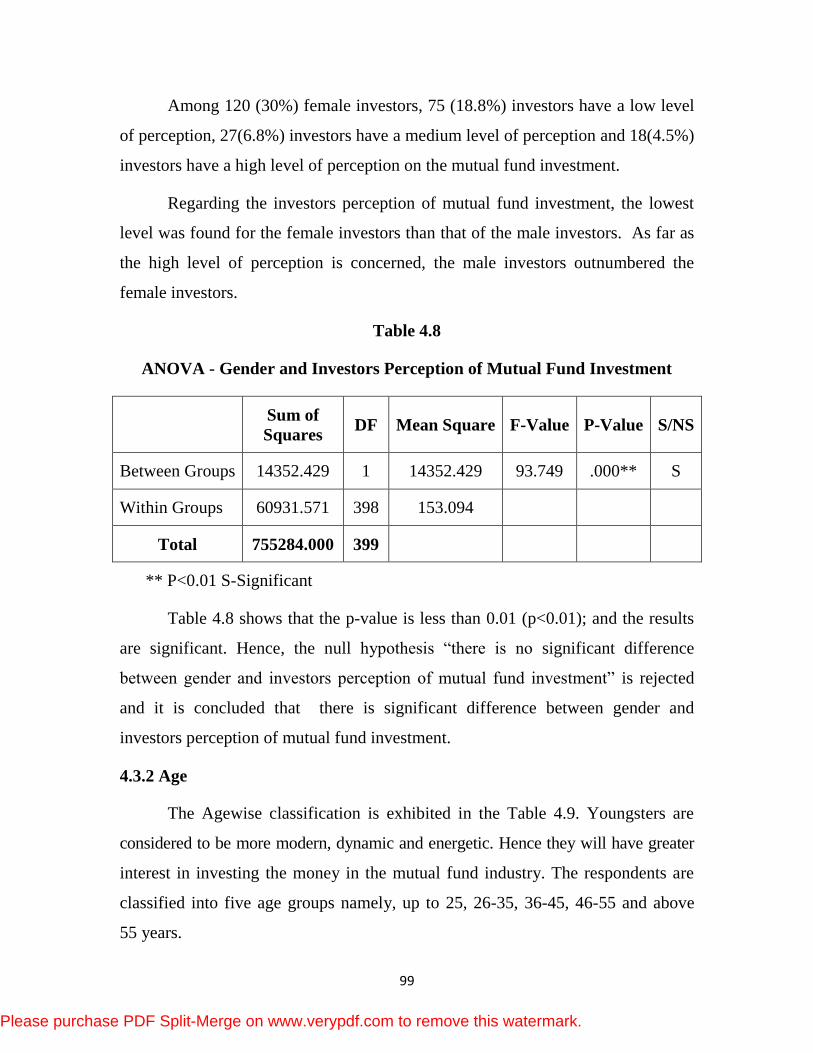

Table 4.8

ANOVA - Gender and Investors Perception of Mutual Fund Investment

Sum of

Squares DF Mean Square F-Value P-Value S/NS

Between Groups 14352.429 1 14352.429 93.749 .000** S

Within Groups 60931.571 398 153.094

Total 755284.000 399

** P<0.01 S-Significant

Table 4.8 shows that the p-value is less than 0.01 (p<0.01); and the results

are significant. Hence, the null hypothesis “there is no significant difference

between gender and investors perception of mutual fund investment” is rejected

and it is concluded that there is significant difference between gender and

investors perception of mutual fund investment.

4.3.2 Age

The Agewise classification is exhibited in the Table 4.9. Youngsters are

considered to be more modern, dynamic and energetic. Hence they will have greater

interest in investing the money in the mutual fund industry. The respondents are

classified into five age groups namely, up to 25, 26-35, 36-45, 46-55 and above

55 years.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

100

Table 4.9

Age of the Respondents

Age Freq % Mean S.D Range

Min Max

Up to 25 years 64 16.0 83.58 9.92 69.00 112.00

26-35 years 139 34.7 99.91 10.89 77.00 112.00

36-45 years 92 23.0 89.02 11.91 69.00 112.00

46-55 years 65 16.3 99.72 1.89 98.00 112.00

Above 55 years 40 10.0 75.83 15.24 69.00 112.00

Total 400 100.0

Source: Primary Data

Table 4.9 represents that 16 per cent of the respondents belong to age group

of up to 25 years and that investors perception of mutual fund investment on this

age group ranged between 69 and 112 with an average of 83.58; 34.7 per cent of

the respondents belong to 26 - 35 years age group and that investors perception of

mutual fund investment on this age group ranged between 77 and 112 with an

average of 99.91; 23 per cent of the respondents belong to 36-45 years of age and

that investors perception of mutual fund investment on this age group ranged

between 69 and 112 with an average of 89.2; 16.3 per cent of the respondents

belong to 46 - 55 years of age and that investors perception of mutual fund

investment on this age group ranged between 98 and 112 with an average of 99.72

and the remaining 10 per cent of the respondents belong to above 55 years of age

and that investors perception of mutual fund investment on this age group ranged

between 69 and 112 with an average of 75.83 per cent.

Table 4.10 and 4.11 present the degree of association between the age

groups and investors level of perception towards mutual fund investment.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

101

Table 4.10

Age and Level of Investor‟s Perception

Age Level of Perception

Total Low Medium High

Up to 25 years Freq 45 15 4 64

% 11.3 3.8 1.0 16.0

26-35 years Freq 3 42 94 139

% .8 10.5 23.5 34.8

36-45 years Freq 39 38 15 92

% 9.8 9.5 3.8 23.0

46-55 years Freq - 63 2 65

% - 15.8 .5 16.3

Above 55 years Freq 33 2 5 40

% 8.3 .5 1.3 10.0

Total Freq 120 160 120 400

% 30.0 40.0 30.0 100.0

Source: Primary Data

Table 4.10 represents that among 400 respondents 64 (16%) of the investors

belong to the age up to 25 years and of them 45 (11.3%) investors have a low level

of perception, 15 (3.8%) investors have a medium level of perception and 4 (1%)

have a high level of perception on mutual fund investment.

Out of 139 (34.8%) investors belong to the age group of 26 to 35 years and

among them three (0.8%) investors have a low level of perception, 42 (10.5%)

investors have a medium level of perception and 94 (23.5%) investors have a high

level of perception on mutual fund investment.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

102

Among 92 (23.0%) investors belong to the age group of 36 to 45 years and

among them 39 (9.8%) investors have a low level of perception, 38 (9.5%) investors

have a medium level of perception and 15 (3.8%) investors have a high level of

perception on mutual fund investment.

Out of 65 (16.3%) investors belong to the age group of 46-55 years. There

are no investors with low level of perception 63 (15.8%) investors have a medium

level of perception and 2 (0.5%) investors have a high level of perception on

mutual fund investment.

Among 40 (10%) investors belong to the age above 55 years. 33 (8.3%)

investors have a low level of perception, 2 (0.5%) investors have a medium level of

perception and 5 (1.3%) investors have a high level of perception on mutual fund

investment.

The level of perceptions has been analyzed for investors of different age

groups, a high percentage (11.3) is found in low level perception in the age group of

upto 25 years and a high percentage (23.5) in high level of perception in the age

group of 26-36 years.

Table 4.11

ANOVA - Age and Investor‟s Perception of Mutual Fund Investment

Sum Of

Squares DF Mean Square F-Value P-Value S/Ns

Between Groups 30527.860 4 7631.965 67.357 .000** S

Within Groups 44756.140 395 113.307

Total 75284.000 399

** P<0.01 S-Significant

Table 4.11 shows that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant difference between

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

103

age of the respondents and investors perception of mutual fund investment” is

rejected and it is concluded that there is a significant difference between age of the

respondents and investors perception of mutual fund investment.

4.3.3 Marital Status

In today‟s world both men and women are working to earn money, so risk

and returns are shared by them. But the unmarried category has a certain limit to

take risk because they can not share their risk. So, mainly married category people

invest more. Marital status of sample respondents are classified into groups

namely married and unmarried respectively.

Table 4.12

Marital Status of the Respondents

Marital Status Freq % Mean S.D Range

Min Max

Married 249 62.2 92.92 14.39 69.00 112.00

Unmarried 151 37.8 92.34 12.62 69.00 113.00

Total 400 100.0

Source: Primary Data

Table 4.12 reveals that the level of investor‟s perception of mutual fund

investment among the married respondents was ranged between 69 and 112 with

a percentage and average of 92.92. The level of investor‟s perception of mutual

fund investment among the unmarried respondents ranged between 69 and 113

with a percentage and average of 92.34. It is concluded that the married respondents

have more perception of mutual fund investment in the study area.

The degree of association between marital status and investor‟s level of

perception towards mutual fund investment were presented in table 4.13 and 4.14.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

104

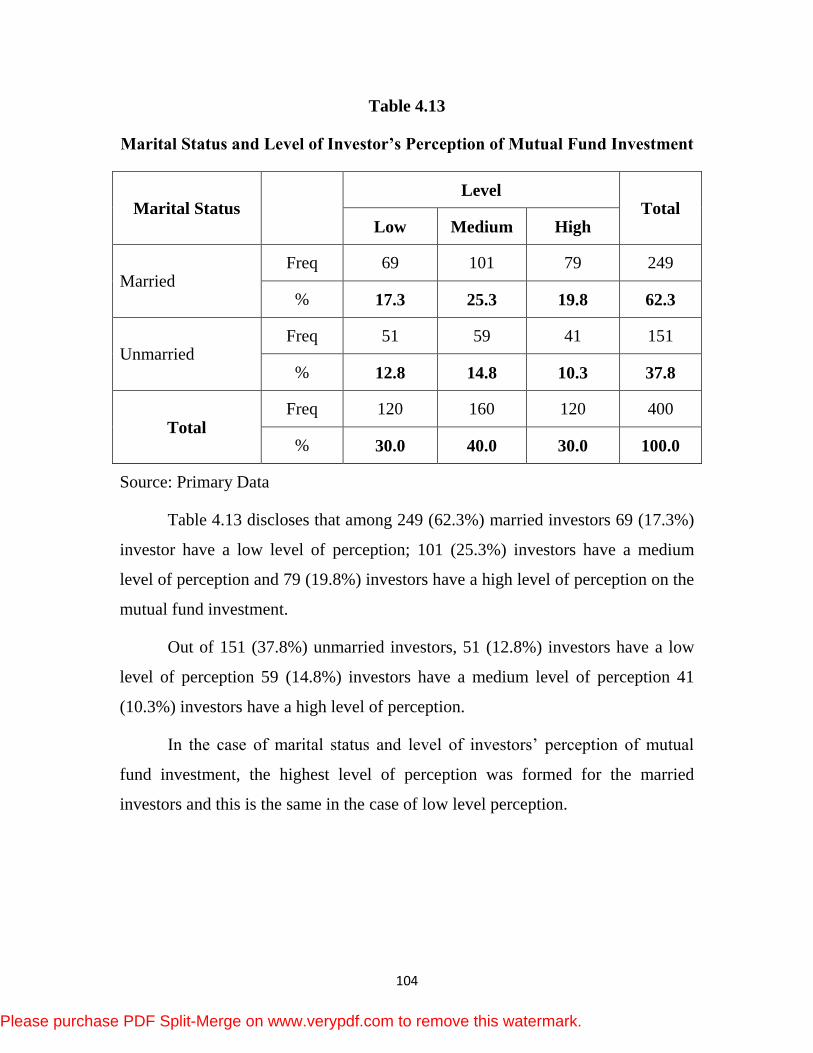

Table 4.13

Marital Status and Level of Investor‟s Perception of Mutual Fund Investment

Marital Status Level

Total Low Medium High

Married Freq 69 101 79 249

% 17.3 25.3 19.8 62.3

Unmarried Freq 51 59 41 151

% 12.8 14.8 10.3 37.8

Total Freq 120 160 120 400

% 30.0 40.0 30.0 100.0

Source: Primary Data

Table 4.13 discloses that among 249 (62.3%) married investors 69 (17.3%)

investor have a low level of perception; 101 (25.3%) investors have a medium

level of perception and 79 (19.8%) investors have a high level of perception on the

mutual fund investment.

Out of 151 (37.8%) unmarried investors, 51 (12.8%) investors have a low

level of perception 59 (14.8%) investors have a medium level of perception 41

(10.3%) investors have a high level of perception.

In the case of marital status and level of investors‟ perception of mutual

fund investment, the highest level of perception was formed for the married

investors and this is the same in the case of low level perception.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

105

Table 4.14

ANOVA - Marital Status and Investor‟s Perception of

Mutual Fund Investment

Sum of

Squares DF

Mean

Square F-Value P-Value S/Ns

Between Groups 30.678 1 30.678 .162 .687 NS

Within Groups 75253.322 398 189.079

Total 755284.000 399

NS- Not Significant

It is identified from the table 4.14 that the p-value is greater than 0.05; and the

results are not significant. Hence, the null hypothesis “there is no significant

difference between marital status of the respondents and investors perception of

mutual fund investment” is accepted and it is concluded that there is no significant

difference between marital status and investor‟s perception of mutual fund investment.

4.3.4 Educational Qualification

Education is very essential for all human beings. It is very important for

one in the modern electronic world to adapt himself to modern principles and

techniques. For this purpose the Educational levels of the respondents are classified

into four groups namely School Level, Graduation, Post-Graduation and Professional.

Education plays an important role in improving knowledge, attitude, tendency and

temperament of the mutual fund investors.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

106

Table 4.15

Educational Qualification of the Respondents

Educational Qualification Freq % Mean S.D Range

Min Max

School Level 68 17.0 99.31 11.26 69 112

Under-Graduation 105 26.2 88.26 12.99 69 112

Post-Graduation 95 23.8 88.49 15.93 70 113

Professional 132 33.0 95.86 11.51 69 112

Total 400 100.0

Source: Primary Data

It is represented from the table 4.15 that the level of investors perception of

mutual fund investment among the School Level respondents was ranged between

69 and 112 with a percentage and an average of 17 and 99.31 respectively and the

level of investors perception of mutual fund investment among the Graduation

respondents was ranged between 69 and 112 with a percentage and an average of

26.3 and 88.26 respectively. The level of impact on corporate retailers among the

Post-Graduation level respondents was ranged between 1 and 3 with a percentage

and an average of 14.2 and 1.88 respectively. The level of investor‟s perception of

mutual fund investment among the HSc level respondents was ranged between

70 and 113 with a percentage and an average of 23.8 and 88.49 and the remaining

level of investor‟s perception of mutual fund investment among the professional

was ranged between 69 and 112 with a percentage and an average of 33 and 95.86

respectively.

To examine the association between educational qualification and investors‟

level of perception towards mutual fund investment, the table 4.16 and 4.17 were

presented.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

107

Table 4.16

Educational Qualification and Level of Investor‟s Perception of

Mutual Fund Investment

Educational Qualification Level of Perception

Total Low Medium High

School Level Freq 10 17 41 68

% 2.5 4.3 10.3 17.0

Under-Graduation Freq 46 42 17 105

% 11.5 10.5 4.3% 26.3

Post-Graduation Freq 32 38 25 95

% 8.0 9.5 6.3 23.8

Professional Freq 32 63 37 132

% 8.0 15.8 9.3 33.0

Total Freq 120 160 120 400

% 30.0 40.0 30.0 100.0

Source: Primary Data

Table 4.16 shows that among 400 respondents 68 (17%) of the investors‟

educational qualification is at school level and among them, 10 (2.5%) investors

have a low level of perception, 17 (4.3%) investors have a medium level of

perception and 41 (10.3%) investors have a high level of perception on the mutual

fund investment.

Out of 105 (26.3%) of the investors‟ educational qualification is under-

Graduation and among them, 46 (11.5%) investors have a low level of perception,

42 (10.5%) investors have a medium level of perception and 17 (4.3%) investors

have a high level of perception on the mutual fund.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

108

Among 95 (23.8%) of the investors educational qualification is post-

Graduation and among them, 32 (8.0%) investors have a low level of perception,

38 (9.5%) investors have a medium level of perception and 25 (6.3%) investors

have a high level of perception on the mutual fund.

Out of 132 (33.0%) of the investors are professionals and among them,

32 (8.0%) investors have a low level of perception, 63 (15.8%) investors have a

medium level of perception and 37 (9.3%) investors have a high level of

perception on the mutual fund.

The researcher has also analyzed the Level of Perception of Investors of mutual

fund investment among the investors of different educational qualifications. A high

percentage (11.5) is found in low level of perception in under-graduates category and a

high percentage (10.3) is found in high level of perception in school level educated

category.

Table 4.17

ANOVA - Educational Qualification and Investor‟s Perception of

Mutual Fund Investment

** P<0.01 S-Significant

Table 4.17 depicts that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant difference between

educational qualification of the respondents and investors perception of mutual

fund investment” is rejected and it is concluded that there is a significant

difference between educational qualification of the respondents and investors

perception of mutual fund investment.

Sum Of

Squares DF

Mean

Square F-Value P Value S/Ns

Between Groups 8037.416 3 2679.139 15.777 .000** S

Within Groups 67246.584 396 169.815

Total 75284.000 399

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

109

4.3.5 Occupation

Occupationwise distributions of sample respondents are classified according to

their employment position. Occupation is a status symbol in society. Hence the

respondents are classified into groups namely Agriculturists, Govt. Employees,

Private Employees, Businessmen / Professionals and others.

Table 4.18

Occupation of the Respondents

Occupation Freq % Mean S.D Range

Min Max

Agriculturists 77 19.3 94.86 13.56 69 112

Govt. Employees 105 26.3 92.23 16.21 69 112

Private Employees 95 23.7 89.19 11.26 69 112

Businessmen / Professionals 87 21.7 98.45 11.62 69 112

Others 36 9.0 84.83 10.38 77 107

Total 400 100.0

Source: Primary Data

Table 4.18 discloses that 19.3 per cent of the respondents are Agriculturists

and level of their perception of mutual fund investment ranged between 69 and

112 with an average of 94.86 and 26.3 per cent of the respondents are Govt.

Employees and level of their perception of mutual fund investment ranged

between 69 and 112 with an average of 92.23; 23.7 per cent of the respondents are

Private Employees and level of their perception of mutual fund investment ranged

between 69 and 112 with an average of 89.19 and 21.7 per cent of the respondents

are Businessmen / Professionals and their perception of mutual fund investment

ranged between 69 and 112 with an average of 98.45 and the remaining 9 per cent

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

110

of the respondents are others and the level of investors perception of mutual fund

investment ranged between 77 and 107 with an average of 84.83. Majority of the

respondents are Govt. Employees.

Table 4.19 and 4.20 shows the association between the occupational status

and the level of investor‟s perception towards mutual fund investment.

Table 4.19

Occupation and Level of Investor‟s Perception of Mutual Fund Investment

Occupation Level of Perception

Total Low Medium High

Agriculturists Freq 17 26 34 77

% 4.3 6.5 8.5 19.3

Govt. Employees Freq 37 33 35 105

% 9.3 8.3 8.8 26.3

Private Employees Freq 33 51 11 95

% 8.3 12.8 2.8 23.8

Businessmen / Professionals Freq 11 38 38 87

% 2.8 9.5 9.5 21.8

Others Freq 22 12 2 36

% 5.5 3.0 .5 9.0

Total Freq 120 160 120 400

% 30.0 40.0 30.0 100.0

Source: Primary Data

Table 4.19 depicts that among 400 respondents 77 (19.3%) of the investors‟

occupational status is agriculturists and among them, 17 (4.3%) investors have a

low level of perception 26 (6.5%) investors have a medium level of perception and

344 (8.5%) investors have a high level of perception on mutual fund investment.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

111

Out of 105 (26.3%) investors‟ occupational status is Govt. employees and

among them, 37 (9.3%) investors have a low level of perception, 33 (8.3%)

investors have a medium level of perception and 35 (8.8%) investors have a high

level of perception on mutual fund investment.

Among 95 (23.8%) investors occupational status is private employees and

among them, 33 (8.3%) investors have a low level of perception 51 (12.8%) investors

have a medium level of perception and 11 (2.8%) investors have medium level of

perception and 2 (0.5%) investors have a high level of perception on mutual fund

investment.

Out of 87 (21.8%) investors occupational status is businessmen/professionals

and among them, 11 (2.8%) investors have a low level of perception 38 (9.5%)

investors have a medium level of perception and 38 (9.5%) investors have a high

level of perception on mutual fund investment.

Among 36 (9%) investors cum under other occupational status and among

them, 22 (5.5%) investors have a low level of perception 12 (3%) investors have a

medium level of perception and 2 (0.5%) investors have a high level of perception

and 2 (0.5%) investors have high level of perception on mutual fund investment.

The researcher has also analyzed level of perception of investors of mutual

fund investment among the investors of different occupational status. A high

percentage (9.3) is found in low level of perception in Govt. Employees and a high

percentage (9.5) is found in high level of perception in businessmen /

professionals.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

112

Table 4.20

ANOVA - Occupation and Investor‟s Perception of Mutual Fund Investment

Sum Of

Squares DF

Mean

Square F-Value

P-

Value S/Ns

Between Groups 6654.950 4 1663.738 9.576 .000** S

Within Groups 68629.050 395 173.744

Total 75284.000 399

** P<0.01 S-Significant

It is revealed from table 4.20 that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant difference between

occupation of the respondents and investors perception of mutual fund

investment” is rejected and it is concluded that there is a significant difference

between occupation of the respondents and investors perception of mutual fund

investment.

4.3.6 Income Earned

Income is important for all human beings, because each and everything is

based on income. It induces individuals to spend their hard earned money on

different products and services. In this study, the income has been studied closely

to see its relationship with mutual funds investments. The respondent‟s income

was studied under four different categories. For this purpose the monthly income

level of the respondents are classified into five levels namely, (i) up to Rs.10,000,

(ii) between Rs.10,001 and Rs.20,000, (iii) between Rs.20,001 and Rs.30,000, (iv)

between Rs.30,001 and Rs.40,000, (v) above Rs.40,000.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

113

Table 4.21

Income Earned of the Respondents

Monthly Income Freq % Mean S.D Range

Min Max

Up to Rs.10,000 91 22.7 92.90 13.86 69 112

Rs.10,001 – Rs.20,000 109 27.3 92.59 13.46 69 112

Rs.20,001 – Rs.30,000 65 16.2 93.52 14.12 69 112

Rs.30,001 - Rs.40,000 68 17.0 92.54 14.05 69 112

Above Rs.40,000 67 16.8 91.97 13.69 69 112

Total 400 100.0

Source: Primary Data

Table 4.21 represents that 22.7 per cent of the respondents earn up to

Rs.10,000 income per month and their perception of mutual fund investment

ranged between 69 and 112 with an average of 92.9; 27.3 per cent of the

respondents earn between Rs.10,001 – Rs.20,000 income per month and the level

of their perception of mutual fund investment ranged between 69 and 112 with an

average of 92.59; 16.2 per cent of the respondents earn between Rs.20,001 –

Rs.30,000 income per month and the level of their perception of mutual fund

investment ranged between 69 and 112 with an average of 93.52; 17 per cent of the

respondents earn Rs.30,001 – Rs.40,000 income per month and the level of their

perception of mutual fund investment ranged between 69 and 112 with an average

of 92.54 and the remaining 16.8 per cent of the respondents earn above Rs.40,000

income per month and the level of their perception of mutual fund investment

ranged between 69 and 112 with an average of 91.97.

Table 4.22 and 4.23 present the association between the monthly income

and level of investors perception towards mutual fund investment,

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

114

Table 4.22

Income Earned and Level of Investor‟s Perception of

Mutual Fund Investment

Monthly Income Level of Perception

Total Low Medium High

Up to Rs. 10,000 Freq 26 37 28 91

% 6.4 9.3 7.0 22.7

Rs. 10,001 - Rs. 20,000 Freq 33 46 30 109

% 8.3 11.5 7.5 27.3

Rs. 20,001 - Rs. 30,000 Freq 18 25 22 65

% 4.4 6.3 5.5 16.2

Rs. 30,001 - Rs. 40,000 Freq 23 23 22 68

% 5.8 5.8 5.5 17.0

above Rs.40,000 Freq 20 29 18 67

% 5.0 7.3 4.5 16.8

Total Freq 120 160 120 400

% 30.0 40.0 30.0 100.0

Source: Primary Data

Table 4.22 shows that among 400 respondents, 91 (22.7%) investors whose

monthly income is up to Rs.10, 000 and among them, 26 (6.4%) investors have a

low level of perception, 37 (9.3%) investors have a medium level of perception

and 28 (7%) investors have a high level of perception on mutual fund investment.

Out of 109 (27.3%) investors whose monthly income is Rs 10,001-

Rs 20,000 and among them, 33 (8.3%) investors have a low level of perception, 46

(11.5%) investors have a medium level of perception and 30 (7.5%) investors have

a high level of perception on mutual fund investment.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

115

Out of 65 (16.2%) investors whose monthly income is Rs 20,001-

Rs 30,000 and among them, 18 (4.4%) investors have a low level of perception,

25 (6.3%) investors have a medium level of perception and 22 (5.5%) investors

have a high level of perception on mutual fund investment.

Out of 68 (17%) investors whose monthly income is Rs 30,001- Rs 40,000

and among them, 23 (5.8%) investors have a low level of perception, 23 (5.8%)

investors have a medium level of perception and 22 (5.5%) investors have a high

level of perception on mutual fund investment.

Out of 67 (16.8%) investors whose monthly income is above Rs 40,000 and

among them, 20 (5.0%) investors have a low level of perception, 29 (7.3%) investors

have a medium level of perception and 18 (4.5%) investors have a high level of

perception on mutual fund investment.

The Investors‟ who fall under the income category from Rs.10,001 to

Rs. 20,000 were found to be the highest perceivers in the low level of perception

and highest perceivers in the high level of perception.

Table 4.23

ANOVA - Income Earned and Investors‟ Perception of

Mutual Fund Investment

Sum Of

Squares DF

Mean

Square

F-

Value

P-

Value S/NS

Between Groups 86.445 4 21.611 .114 .978 NS

Within Groups 75197.555 395 190.374

Total 75284.000 399

NS-Not Significant

It is revealed from table 4.23 that the p-value is greater than 0.01; and the

results are not significant. Hence, the null hypothesis “there is no significant

difference between monthly income of the respondents and investors‟ perception

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

116

of mutual fund investment” is accepted and it is concluded that there is no

significant difference between monthly income of the respondents and investors

perception of mutual fund investment.

4.4 INVESTORS‟ ATTITUDES OF MUTUAL FUND INVESTMENT

Studying attitude of mutual fund investors‟ help to know in what way their

attitude prevails and how they opined about the mutual fund investment. In this

section, opinion of mutual fund investors has been studied by taking their opinion

in relation to Gender, Occupation and their monthly income.

Table 4.24 shows Chi-square test for Gender and Opinion about Investment

options of mutual fund.

Table 4.24

Gender and Opinion about Investment Options of Mutual Fund

Gender

Opinion About Investment Options Of Mutual Fund

Total Growth

option

Dividend

payout

option

Dividend re-

investment

option

Retirement

pension

option

Insurance

Option

Male Freq 40 134 58 40 8 280

% 10.0% 33.5% 14.5% 10.0% 2.0% 70.0%

Female Freq 40 23 22 0 35 120

% 10.0% 5.8% 5.5% .0% 8.8% 30.0%

Total Freq 80 157 80 40 43 400

% 20.0% 39.3% 20.0% 10.0% 10.8% 100.0%

Chi

square

calculated

value

104.323

DF 4

P-value 0.000** (s)

**P<0.01 S- Significant

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

117

Table 4.24 describes that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant relationship between

gender of the respondents and opinion about investment options of mutual fund” is

rejected and it is concluded that there is a significant relationship between gender

of the respondents and opinion about investment options of mutual fund.

Table 4.25 reveals the occupation and opinion about Investment options of

Mutual fund.

Table 4.25

Occupation and Opinion about Investment Options of Mutual Fund

Occupation

Opinion about investment options of mutual fund

Total Growth

option

Dividend

payout

option

Dividend

re-

investment

option

Retirement

pension

option

Insurance

Option

Agriculturists Freq 13 22 32 4 6 77

% 3.3% 5.5% 8.0% 1.0% 1.5% 19.3%

Govt.

Employees

Freq 14 46 33 6 6 105

% 3.5% 11.5% 8.3% 1.5% 1.5% 26.3%

Private

Employees

Freq 36 22 9 20 8 95

% 9.0% 5.5% 2.3% 5.0% 2.0% 23.8%

Businessmen/

Professionals

Freq 11 61 6 4 5 87

% 2.8% 15.3% 1.5% 1.0% 1.3% 21.8%

Others Freq 6 6 0 6 18 36

% 1.5% 1.5% .0% 1.5% 4.5% 9.0%

Total Freq 80 157 80 40 43 400

% 20.0% 39.3% 20.0% 10.0% 10.8% 100.0%

Chi square

calculated

value

176.660

DF 16

P-value 0.000** (s)

**P<0.01 S- Significant

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

118

It is identified from the table 4.25 that the p-value is less than 0.01; and the

results are significant. Hence, the null hypothesis “there is no significant relationship

between occupational status of the respondents and opinion about investment options

of mutual fund” is rejected and it is concluded that there is a significant relationship

between occupational status of the respondents and opinion about investment options

of mutual fund.

Income earned and opinion about Investment options of Mutual fund is

presented in table 4.26.

Table 4.26

Income Earned and Opinion about Investment Options of Mutual Fund

Monthly

Income

Opinion about investment options of mutual fund

Total Growth

option

Dividend

payout

option

Dividend

re-

investment

option

Retirement

pension

option

Insurance

Option

Up to

Rs. 10,000

Freq 21 35 22 6 7 91

% 5.3% 8.8% 5.5% 1.5% 1.8% 22.8%

Rs. 10,001

to

Rs. 20,000

Freq 18 49 17 11 14 109

% 4.5% 12.3% 4.3% 2.8% 3.5% 27.3%

Rs. 20,001

to

Rs. 30,000

Freq 15 26 13 7 4 65

% 3.8% 6.5% 3.3% 1.8% 1.0% 16.3%

Rs. 30,001

to

Rs. 40,000

Freq 12 22 14 11 9 68

% 3.0% 5.5% 3.5% 2.8% 2.3% 17.0%

Above

Rs. 40,000

Freq 14 25 14 5 9 67

% 3.5% 6.3% 3.5% 1.3% 2.3% 16.8%

Total Freq 80 157 80 40 43 400

% 20.0% 39.3% 20.0% 10.0% 10.8% 100.0%

Chi-square

calculated

value

12.794

DF 16

P-value 0.688 (NS)

NS- Not Significant

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

119

Table 4.26 shows that the p-value is greater than 0.05; and the results are not

significant. Hence, the null hypothesis “there is no significant relationship between

monthly income of the respondents and opinion about investment options of mutual

fund” is accepted and it is concluded that there is no significant relationship

between monthly income of the respondents and opinion about investment options

of mutual fund.

4.5 REASON FOR PREFERRING MUTUAL FUND INVESTMENT

Every Mutual fund investor has their own reason for investing their money

into the mutual fund investment. The mutual fund investment is preferred by the

investors for various reasons. A particular reason is attributed to a particular type

of investors therefore; the preference differs from investor to investor. In this

analytical part, Gannett ranking technique has been employed to rank the

preferences of the mutual fund investors.

Garret Ranking Technique

This technique was used to rank the preference of the respondents on

different aspects of the study. The order of merit given by the respondents was

converted into ranks by using the following formula2.

Percentage Position = 100(Rij-0.5)

Nj

Where Rij = Rank given for ith

factor by jth

individual.

Nj = Number of factors ranked by jth

individual.

The percentage position of each rank thus obtained is converted into scores

by referring to the table given by Henry E.Garret. Then for each factor the scores

of individual respondents are added together and divided by the total number of

respondents for whom the scores were added.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

120

These mean scores for all the factors were arranged in the descending order,

ranks given and most important aspects identified and presented in table 4.27.

Table 4.27

Reason for Preferring Mutual Fund Investment

S. No. Factors Total Score Mean Score Rank

1 Owned by government 28200 70.5 I

2 Better investors relationship 16960 42.4 V

3 Prompt payment at maturity 20320 50.8 IV

4 Low premium & high return 25680 64.2 II

5 Better liquidity 20400 51.0 III

6 Diversified investment 12840 32.1 VI

Source: Primary Data

The above table 4.27 reveals the ranking of reason for preferring mutual

fund investment. “Owned by government” was ranked first by the select sample

respondents with the total score of 28200 and mean score of 70.5. “Low premium

& high return” was ranked second with the total score of 25680 and mean score of

64.2. “Better liquidity” occupied third position with the total score of 20400 mean

score of 51. “Prompt payment at maturity” was ranked fourth with the total score

of 20320 and mean score of 50.8. “Better investors‟ relationship” occupied fifth

position with the total score of 16960 and mean score of 42.4. “Diversified investment”

occupied last position with the total score of 12840 and mean score of 32.1. It is

evident that most of the respondents gave top priority to “Owned by government”

as the first rank for preferring mutual fund investment.

Exhibit 4.1 shows the reason for preferring mutual fund investment.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

121

Exhibit 4.1

REASON FOR PREFERRING MUTUAL FUND INVESTMENT

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

122

4.6 SOCIO-ECONOMIC CONDITION OF MUTUAL FUND INVESTMENT

The Socio-Economic Conditions of the people determine the mutual fund

investments. The investors, who are having sound financial position, prefer mutual

fund investment with their surplus funds. Apart from the Socio-Economic Conditions

of the mutual fund investors, there are some other factors from the market forces

which determine the mutual fund investment. In this part, the factors such as

product qualities, fund sponsor qualities and investors services have been taken into

account in relation to Age, Gender, Educational Qualifications and Occupation.

Chi-Square Analysis

Ho5: There is no association between Gender and the selection of mutual fund

scheme.

Table 4.28

Gender and the Selection of Mutual Fund Scheme - Product Qualities

Product Qualities Calculated

value DF P-value S/NS

Funds/scheme‟s performance record 89.320 3 .000** S

Funds/scheme‟s reputation or brand name 22.937 3 .000** S

Scheme‟s expense ratio 41.280 3 .000** S

Scheme‟s portfolio of investments 166.260 4 .000** S

Reputation of scheme(s),portfolio

manager(s) 29.302 3 .000** S

Withdrawal facilities 48.175 3 .000** S

Favorable rating by a rating agency 111.260 4 .000** S

Innovativeness of the scheme 82.054 4 .000** S

Products with tax benefits 26.333 2 .000** S

Entry and Exit load 129.667 3 .000** S

**P<0.01 S-Significant

Table 4.28 exposes that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant relationship between

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

123

Gender of the respondents and all Product Qualities factors related to selection of

mutual fund scheme” is rejected and it is concluded that there is a significant

relationship between Gender of the respondents and all Product Qualities factors

related to selection of mutual fund schemes.

Table 4.29 shows the Age and the Selection of Mutual Fund Schemes

Product Qualities.

Table 4.29

Age and the Selection of Mutual Fund Scheme - Product Qualities

Product Qualities Calculated

value DF

P-

value S/NS

Funds/scheme‟s performance record 450.746 12 .000** S

Funds/scheme‟s reputation or brand

name 435.016 12 .000** S

Scheme‟s expense ratio 570.263 12 .000** S

Scheme‟s portfolio of investments 588.486 16 .000** S

Reputation of scheme(s),portfolio

manager(s) 385.743 12 .000** S

Withdrawal facilities 474.871 12 .000** S

Favorable rating by a rating agency 586.690 16 .000** S

Innovativeness of the scheme 453.845 16 .000** S

Products with tax benefits 140.292 8 .000** S

Entry and Exit load 269.907 12 .000** S

**P<0.01 S-Significant

It is identified from the table 4.29 that the p-value is less than 0.01; and the

results are significant. Hence, the null hypothesis “there is no significant relationship

between age of the respondents and all Product Qualities factors related to selection of

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

124

mutual fund scheme” is rejected and it is concluded that there is a significant

relationship between age of the respondents and all Product Qualities factors related to

selection of mutual fund scheme.

Table 4.30 deals with the Educational Qualification and the Selection of

mutual Fund Scheme – Product Qualities.

Table 4.30

Educational Qualification and the Selection of Mutual Fund Scheme -

Product Qualities

Product Qualities Calculated

value DF

P-

value S/NS

Funds/scheme‟s performance record 96.168 9 .000** S

Funds/scheme‟s reputation or brand

name 102.106 9 .000** S

Scheme‟s expense ratio 173.867 9 .000** S

Scheme‟s portfolio of investments 250.513 12 .000** S

Reputation of scheme(s),portfolio

manager(s) 82.454 9 .000** S

Withdrawal facilities 114.080 9 .000** S

Favorable rating by a rating agency 148.489 12 .000** S

Innovativeness of the scheme 129.869 12 .000** S

Products with tax benefits 54.534 6 .000** S

Entry and Exit load 176.114 9 .000** S

**P<0.01 S-Significant

Table 4.30 shows that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant relationship between

educational qualification of the respondents and all Product Qualities factors

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

125

related to selection of mutual fund scheme” is rejected and it is concluded that

there is a significant relationship between educational qualification of the respondents

and all Product Qualities factors related to selection of mutual fund scheme.

Table 4.31 shows the Occupational Status and the Selection of Mutual Fund

Schemes – Product Qualities.

Table 4.31

Occupational Status and the Selection of Mutual Fund

Scheme - Product Qualities

Product Qualities Calculated

value DF

P-

value S/NS

Funds/scheme‟s performance record 125.392 12 .000** S

Funds/scheme‟s reputation or brand

name 95.832 12 .000** S

Scheme‟s expense ratio 127.623 12 .000** S

Scheme‟s portfolio of investments 142.814 16 .000** S

Reputation of scheme(s),portfolio

manager(s) 76.960 12 .000** S

Withdrawal facilities 103.344 12 .000** S

Favorable rating by a rating agency 158.573 16 .000** S

Innovativeness of the scheme 130.289 16 .000** S

Products with tax benefits 46.835 8 .000** S

Entry and Exit load 121.459 12 .000** S

**P<0.01 S-Significant

It is observed from the table 4.31 that the p-value is less than 0.01; and the

results are significant. Hence, the null hypothesis “there is no significant relationship

between occupational status of the respondents and all Product Qualities factors

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

126

related to selection of mutual fund scheme” is rejected and it is concluded that

there is a significant relationship between occupational status of the respondents

and all Product Qualities factors related to selection of mutual fund scheme.

Table 4.32 deals with Gender and the selection of Mutual Fund Scheme-Fund

Sponsor Qualities.

Table 4.32

Gender and the Selection of Mutual Fund Scheme - Fund Sponsor Qualities

Fund Sponsor qualities Calculated

value DF P-value S/NS

Reputation of a sponsoring firm 48.175 3 .000** S

Sponsor offers a wide range of schemes

with different investment objectives 121.508 3 .000** S

Sponsor has a recognized brand name 112.000 4 .000** S

Sponsor has a well developed Agency

Network / Infrastructure 66.286 3 .000** S

Sponsor has an efficient research wing 127.893 3 .000** S

Sponsor‟s expertise in managing money 95.258 3 .000** S

**P<0.01 S-Significant

Table 4.32 portrays that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant relationship between

Gender of the respondents and all Fund Sponsor qualities factors related to

selection of mutual fund scheme” is rejected and it is concluded that there is a

significant relationship between Gender of the respondents and all Fund Sponsor

qualities factors related to selection of mutual fund scheme.

Table 4.33 shows the Age and the Selection of Mutual Fund Scheme–Fund

Sponsor Qualities.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

127

Table 4.33

Age and the Selection of Mutual Fund Scheme - Fund Sponsor Qualities

Fund Sponsor qualities Calculated

value DF P-value S/NS

Reputation of a sponsoring firm 427.333 12 .000** S

Sponsor offers a wide range of schemes

with different investment objectives 460.578 12 .000** S

Sponsor has a recognized brand name 618.844 16 .000** S

Sponsor has a well developed Agency

Net Work / Infrastructure 389.710 12 .000** S

Sponsor has an efficient research wing 397.725 12 .000** S

Sponsor‟s expertise in managing money 507.980 12 .000** S

**P<0.01 S-Significant

Table 4.33 discloses that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant relationship between

age of the respondents and all fund sponsor qualities factors related to selection of

mutual fund scheme” is rejected and it is concluded that there is a significant

relationship between age of the respondents and all fund sponsor qualities factors

related to selection of mutual fund scheme.

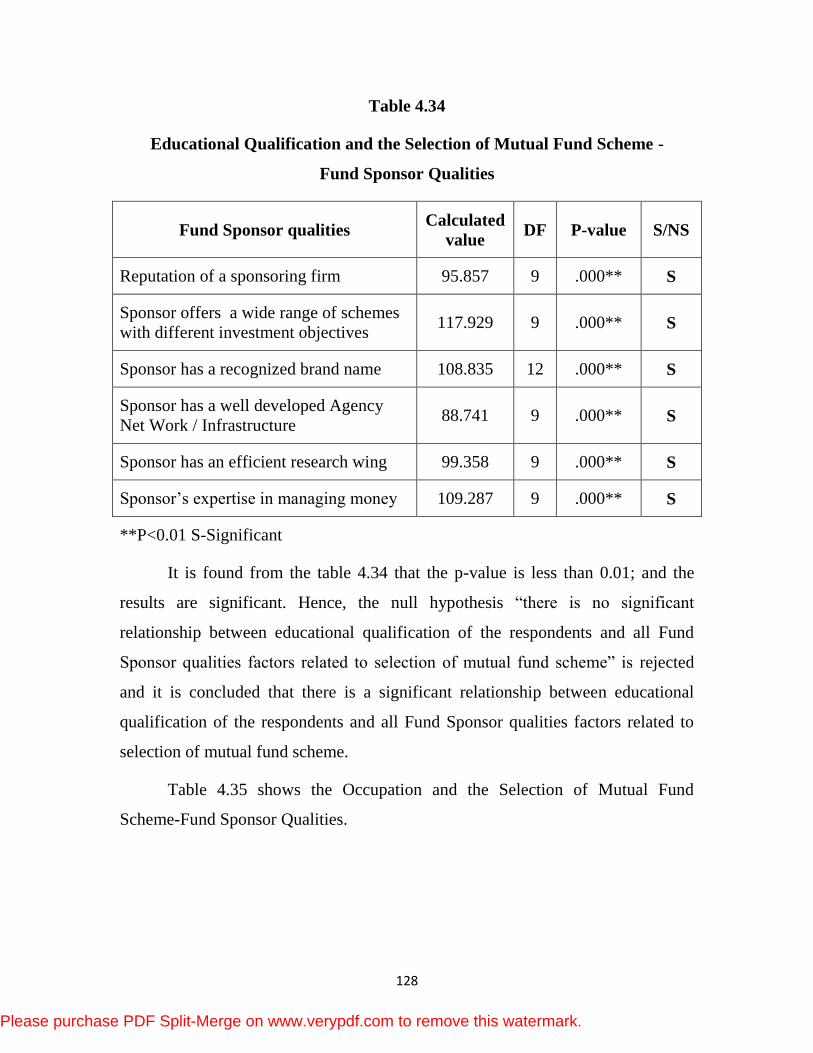

Table 4.34 deals with the Educational Qualification and the Selection of

Mutual Fund Scheme–Fund Sponsor Qualities.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

128

Table 4.34

Educational Qualification and the Selection of Mutual Fund Scheme -

Fund Sponsor Qualities

Fund Sponsor qualities Calculated

value DF P-value S/NS

Reputation of a sponsoring firm 95.857 9 .000** S

Sponsor offers a wide range of schemes

with different investment objectives 117.929 9 .000** S

Sponsor has a recognized brand name 108.835 12 .000** S

Sponsor has a well developed Agency

Net Work / Infrastructure 88.741 9 .000** S

Sponsor has an efficient research wing 99.358 9 .000** S

Sponsor‟s expertise in managing money 109.287 9 .000** S

**P<0.01 S-Significant

It is found from the table 4.34 that the p-value is less than 0.01; and the

results are significant. Hence, the null hypothesis “there is no significant

relationship between educational qualification of the respondents and all Fund

Sponsor qualities factors related to selection of mutual fund scheme” is rejected

and it is concluded that there is a significant relationship between educational

qualification of the respondents and all Fund Sponsor qualities factors related to

selection of mutual fund scheme.

Table 4.35 shows the Occupation and the Selection of Mutual Fund

Scheme-Fund Sponsor Qualities.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

129

Table 4.35

Occupation and the Selection of Mutual Fund Scheme -

Fund Sponsor Qualities

Fund Sponsor qualities Calculated

value DF P-value S/NS

Reputation of a sponsoring firm 78.812 12 .000** S

Sponsor offers a wide range of schemes

with different investment objectives 89.290 12 .000** S

Sponsor has a recognized brand name 128.509 16 .000** S

Sponsor has a well developed Agency

Network / Infrastructure 37.903 12 .000** S

Sponsor has an efficient research wing 77.987 12 .000** S

Sponsor‟s expertise in managing money 124.816 12 .000** S

**P<0.01 S-Significant

Table 4.35 describes that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant relationship between

occupational status of the respondents and all Fund Sponsor qualities factors

related to selection of mutual fund scheme” is rejected and it is concluded that

there is a significant relationship between occupational status of the respondents

and all Fund Sponsor qualities factors related to selection of mutual fund scheme.

Table 4.36 reveals the Gender and the Selection of Mutual Fund Scheme-

Investor Services.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

130

Table 4.36

Gender and the Selection of Mutual Fund Scheme - Investor Services

Investor services Calculated

value DF

P-

value S/NS

Disclosure of investment objectives,

method and periodicity of valuation in

advertisement

122.000 3 .000** S

Disclosure of the method and periodicity

of the scheme‟s sales and repurchase in the

offer documents

127.698 2 .000** S

Disclosure of NAV on every trading day 65.506 3 .000** S

Disclosure of deviation of the investments

from the original pattern 93.571 3 .000** S

Disclosure of scheme‟s investments on

every trading day 118.810 4 .000** S

Mutual Fund Investor‟s grievance

redressal machinery 159.702 4 .000** S

Fringe benefits like free insurance, free

credit card, loans on collateral, tax benefits

etc.

26.746 4 .000** S

**P<0.01 S-Significant

It is observed from the table 4.36 that the p-value is less than 0.01; and the

results are significant. Hence, the null hypothesis “there is no significant

relationship between Gender of the respondents and all Investor services factors

related to selection of mutual fund scheme” is rejected and it is concluded that

there is a significant relationship between Gender of the respondents and all

Investor services factors related to selection of mutual fund scheme.

Table 4.37 deals with the Age and the Selection of Mutual Scheme-Investor

Services.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

131

Table 4.37

Age and the Selection of Mutual Fund Scheme - Investor Services

Investor services Calculated

value DF P-value S/NS

Disclosure of investment objectives,

method and periodicity of valuation in

advertisement

461.226 12 .000** S

Disclosure of the method and periodicity of

the scheme‟s sales and repurchase in the

offer documents

292.575 8 .000** S

Disclosure of NAV on every trading day 390.548 12 .000** S

Disclosure of deviation of the investments

from the original pattern 268.585 12 .000** S

Disclosure of scheme‟s investments on

every trading day 612.326 16 .000** S

Mutual Fund Investor‟s grievance redressal

machinery 473.403 16 .000** S

Fringe benefits like free insurance, free

credit card, loans on collateral, tax benefits

etc.

521.991 16 .000** S

**P<0.01 S-Significant

Table 4.37 reveals that the p-value is less than 0.01; and the results are

significant. Hence, the hypothesis “there is no significant relationship between age

of the respondents and all investor services factors related to selection of mutual

fund scheme” is rejected and it is concluded that there is a significant relationship

between age of the respondents and all investor services factors related to selection

of mutual fund scheme.

Table 4.38 deals with the Educational Qualification and the Selection of

Mutual Fund Scheme-Investor Services.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

132

Table 4.38

Educational Qualification and the Selection of Mutual Fund Scheme -

Investor Services

Investor services Calculated

value DF

P-

value S/NS

Disclosure of investment objectives,

method and periodicity of valuation in

advertisement

74.709 9 .000** S

Disclosure of the method and

periodicity of the scheme‟s sales and

repurchase in the offer documents

53.729 6 .000** S

Disclosure of NAV on every trading day 81.559 9 .000** S

Disclosure of deviation of the

investments from the original pattern 181.161 9 .000** S

Disclosure of scheme‟s investments on

every trading day 130.238 12 .000** S

Mutual Fund Investor‟s grievance

redressal machinery 159.045 12 .000** S

Fringe benefits like free insurance,

free credit card, loans on collateral, tax

benefits etc.

145.155 12 .000** S

**P<0.01 S-Significant

It is revealed from table 4.38 that the p-value is less than 0.01; and the

results are significant. Hence, the hypothesis “there is no significant relationship

between educational qualification of the respondents and all Investor services

factors related to selection of mutual fund scheme” is rejected and it is concluded

that there is a significant relationship between educational qualification of the

respondents and all Investor services factors related to selection of mutual

fund scheme.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

133

Table 4.39 shows the Occupational Status and the Selection of Mutual Fund

Scheme-Investor Services.

Table 4.39

Occupational Status and the Selection of Mutual Fund Scheme -

Investor Services

Investor services Calculated

value DF P-value S/NS Remarks

Disclosure of investment objectives,

method and periodicity of valuation

in advertisement

94.921 12 .000** S Rejected

Disclosure of the method and

periodicity of the scheme‟s sales

and repurchase in the offer

documents

57.889 8 .000** S Rejected

Disclosure of NAV on every trading

day 66.722 12 .000** S Rejected

Disclosure of deviation of the

investments from the original

pattern

108.296 12 .000** S Rejected

Disclosure of scheme‟s investments

on every trading day 151.585 16 .000** S Rejected

Mutual Fund Investor‟s grievance

redressal machinery 129.982 16 .000** S Rejected

Fringe benefits like free insurance,

free credit card, loans on collateral,

tax benefits etc.

92.150 16 .000** S Rejected

**P<0.01 S-Significant

Table 4.39 depicts that the p-value is less than 0.01; and the results are

significant. Hence, the null hypothesis “there is no significant relationship between

occupational status of the respondents and all Investor services factors related to

selection of mutual fund scheme” is rejected and it is concluded that there is a

significant relationship between occupational status of the respondents and all

Investor services factors related to selection of mutual fund scheme.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

134

4.7 MOTIVATION FACTOR OF MUTUAL FUND INVESTMENT

There are certain motivational forces which pull the potential investors to

invest into the mutual fund investment. These motivational forces have been

analyzed so that their inter-relationship and multiple regression model has been

used to find the determinants of mutual fund investment. Under this section, the

significance of each motivational factor and their contribution in determining the

mutual investment have been given.

Multiple Regression Analysis

Multiple regression co-efficient measures the relationship between two

variables in such a way that the effects of other related variables are eliminated.

In other words, it measures the relation between a dependent variable and a

particular independent variable by holding all other variables constant. Thus, each

multiple regression co-efficient measures the effect of its independent variable on

the dependent variable. Multiple regression analysis of motivation factors for

investing in mutual fund (Y) was performed with variables and Risk and returns

(X1), Savings (X2), Tax benefit (X3), Scheme (X4), Occupational (X5) and Monthly

Income (X6) the following regression model is fitted for performance:

X16 = bo + b1X1 + b2 X2 +b3 X3 + ……….

Where b1, b2 …. and b6 are partial regression coefficients; bo-constant the results

are presented in table 4.40.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

135

Table 4.40

Inter-Correlation between Select Variables with the Motivation Factors for

Investing in Mutual Fund

S.

No. Factors 1 2 3 4 5 6

(Constant) 1.000

1 Risk and return .527** 1.000

2 Savings -.263** .136** 1.000

3 Tax Benefit -.433** .000 .240** 1.000

4 Scheme .164** .477** .006 .384** 1.000

5 Occupational -.012 -.182** -.242** -.230** -.145* 1.000

6 Monthly income .025 .002 .011 -.051 .000 .005 1.000

Source: Primary Data

Table 4.40 reveals that the correlation analysis that has been done on all the

data that have been collected through interview schedule. Motivation is correlated

with the rest of the variables. This analysis is done to show the existing relation

among the study variables namely risk and return, savings, tax, benefit, schemes

occupational and monthly income. It can be seen that one variable namely x1, risk

and return r.527 p<0.01 has significant positive correlation with the motivation

factors for investing in mutual fund. Other two variables namely x2 savings

r.-0.263, p<0.01 and x3 tax benefits r.-433 p<0.01 have significant but negative

correlation with motivation factors for investing in mutual fund. In this all of the

predictor variables were entered simultaneously because the predicator variables

and the enter method were used.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

136

Ho6: There is no significant difference between select variables like Risk and

return, Savings, Tax Benefit, Scheme, Occupational, Monthly income and

the motivation factors for investing in mutual fund.

Table 4.41

Multiple Regression Analysis of the Select Variables with the Motivation

Factors for Investing In Mutual Fund

S. No. Factors

Standardized

Coefficients

(β)

t-value p-value S/NS

(Constant) - 7.668 .000** S

1 Risk and return 0.518 12.370 .000** S

2 Savings -0.251 -6.725 .000** S

3 Tax Benefit -0.412 -10.050 .000** S

4 Scheme 0.067 1.497 0.135 NS

5 Occupational -0.063 -1.712 0.088 NS

6 Monthly

income

0.007 0.195 0.845 NS

R

R2

Adjusted R2

F Change

Sig in F change

0.728

0.530

0.523

73.771**

0.000***

**p <0.01, S-Significant NS- Not significant

The above table 4.41 represents the statistical significance of the model.

The R2 value at 0.530 states that all the six independent variables that is risk and

return, savings, tax benefit, scheme, occupational and a monthly income have 53%

influence on the dependent variable motivation.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

137

It is clear that out of the six independent variables risk and return, savings,

tax benefit have significant influence on the dependent variable motivation scheme

and the remaining do not have significant influence on the motivation.

Table 4.42

ANOVA-The Select Variables with the Motivation Factors for

Investing in Mutual Fund

Model Sum of

Squares DF Mean Square F-value P-value S/NS

Regression 230.946 6 38.491 73.771 .000** S

Residual 205.054 393 .522

Total 436.000 399

**p <0.01, S-Significant

Table 4.42 reveals the p-value which is less than 0.01 and the overall

ANOVA results which assess the overall significance [F.73.77]. This model is

statistically significant. This shows that there is a significant difference between

select variables and motivation for investing in mutual fund investment.

4.8 PURPOSE OF MUTUAL FUND INVESTMENT

There are so many purposes for which the mutual fund investors invest

their movies into the mutual investment. But, the weightage of each and every

purpose cannot be ranked with subjective mind. In order to rank the various

purposes, the Friedman rank test was used and its results were given.

Friedman Rank Test

In the Friedman rank test the scores in each row of the data file stands

independently of every other row. The Friedman chi-square tests the null hypothesis

that the ranks of the variables do not differ from their expected value. For a

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

138

constant sample size, the higher the value of this chi-square statistic, the larger the

difference between each variables rank sum and its expected value.

Table 4.43 shows the Purpose of Mutual Fund Investment.

Table 4.43

Purpose of Mutual Fund Investment and Opinion

S. No. Factors Mean Value Rank

1 Savings 6.80 I

2 Better investments 5.20 IV

3 Tax Benefit 5.50 II

4 Children‟s Education 5.25 III

5 Marriage 4.90 V

6 Medical Expenses 4.10 VIII

7 Low Risk 3.90 IX

8 Switching Facility 4.65 VII

9 Other purpose 4.70 VI

Source: Primary Data

Table 4.43 reveals the Purpose of Mutual fund Investment. The variable

“Savings” was ranked first by the select sample respondents with the mean score

of 6.80. “Tax Benefit” was ranked second with the mean score of 5.50. “Children‟s

Education” occupied third position with the mean score of 5.25. “Better investments”

was ranked fourth with the mean score of 5.20. “Marriage” occupied fifth position

with the mean score of 4.90. “Low risk” occupied last position with the mean

score of 3.90. It is evident that most of the respondents gave top priority to savings

as the first rank for preferring mutual fund investment. Exhibit 4.2 presents the

purpose of mutual fund investment and opinion.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

139

Exh

ibit

4.2

Pu

rpo

se o

f M

utu

al

Fu

nd

In

ves

tmen

t a

nd

Op

inio

n

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

140

Ho 7: There is no significant difference between mean ranks for respondent‟s

purpose and opinion of mutual fund investment.

Table 4.44 Friedman Test

**P<0.01 S-Significant

Table 4.44 presents the result of the Friedman test. For these rankings, the

chi-square value is 374.9; Degree of freedom is equal to the number of values

minus 1. As nine purpose and opinion of mutual fund investment are ranked, there

are 8 degrees of freedom. It is clear from the above table that significance level is

0.000 at 1 per cent level of significance. Hence the hypothesis is rejected.

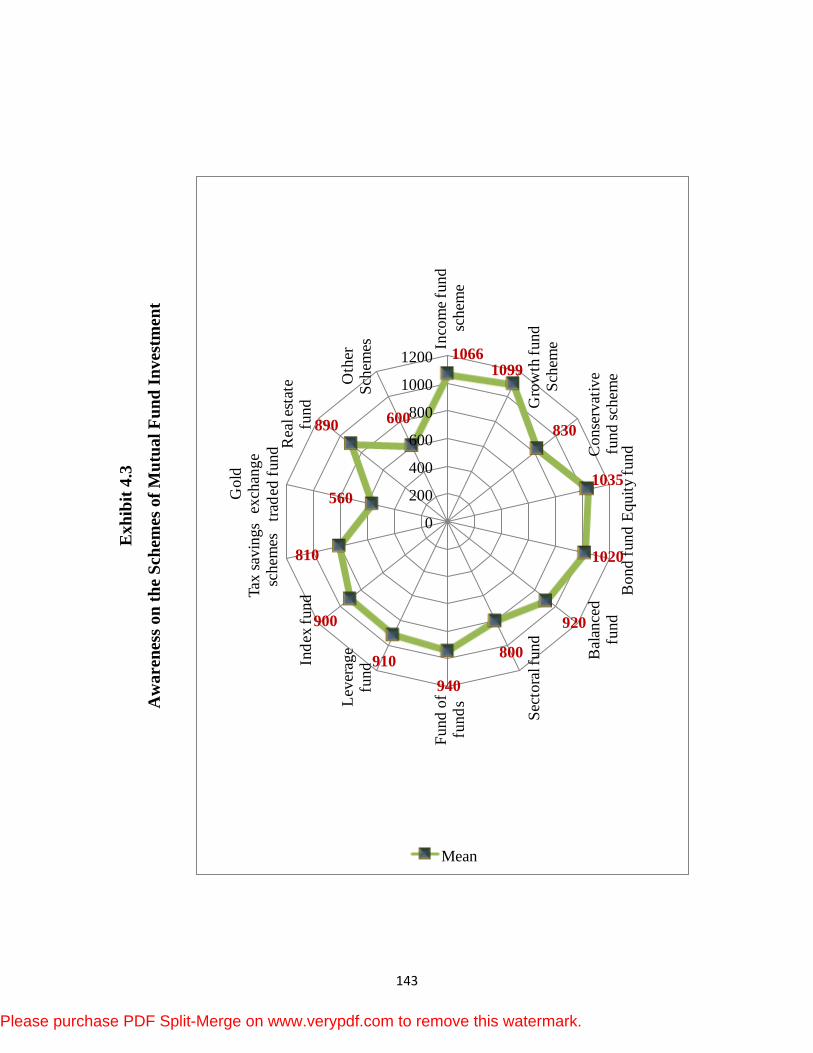

4.9 AWARENESS ON THE SCHEMES OF MUTUAL FUND INVESTMENT

The fund sponsoring companies offer various schemes to their investors

with special features. It is not easy to say that all the investors are aware of all the

schemes which are offered by the fund sponsoring companies. The levels of