pental limited 53 weeks ended 2 july 2017 for personal use ...name of entity financial year...

TRANSCRIPT

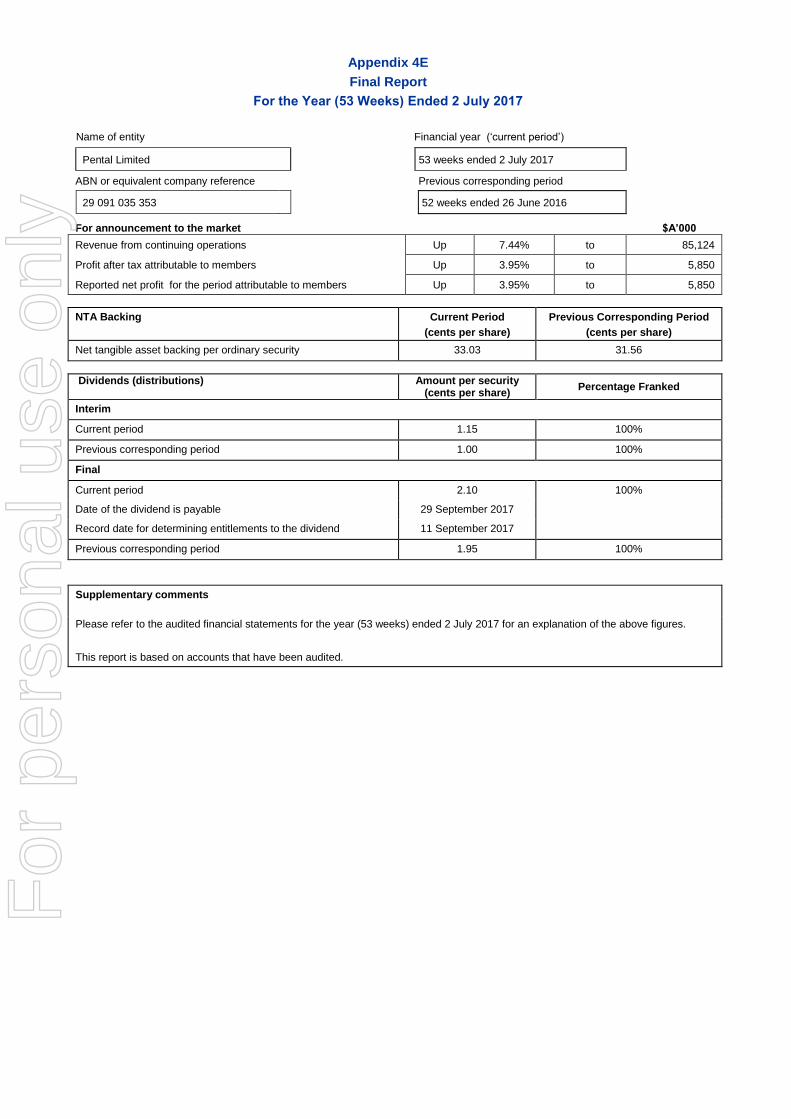

Appendix 4E

Final Report

For the Year (53 Weeks) Ended 2 July 2017

Name of entity Financial year (‘current period’)

Pental Limited 53 weeks ended 2 July 2017

ABN or equivalent company reference Previous corresponding period

29 091 035 353 52 weeks ended 26 June 2016

For announcement to the market $A’000

Revenue from continuing operations Up 7.44% to 85,124

Profit after tax attributable to members Up 3.95% to 5,850

Reported net profit for the period attributable to members Up 3.95% to 5,850

NTA Backing Current Period

(cents per share)

Previous Corresponding Period

(cents per share)

Net tangible asset backing per ordinary security 33.03 31.56

Dividends (distributions) Amount per security (cents per share)

Percentage Franked

Interim

Current period 1.15 100%

Previous corresponding period 1.00 100%

Final

Current period 2.10 100%

Date of the dividend is payable 29 September 2017

Record date for determining entitlements to the dividend 11 September 2017

Previous corresponding period 1.95 100%

Supplementary comments

Please refer to the audited financial statements for the year (53 weeks) ended 2 July 2017 for an explanation of the above figures.

This report is based on accounts that have been audited.

For

per

sona

l use

onl

y

Pental Limited

ABN: 29 091 035 353

Financial Report

for the year (53 weeks) ended 2 July 2017

For

per

sona

l use

onl

y

2

Contents

Description Page

Chairman’s Review 3

Corporate Governance Statement 5

Directors’ Report 11

Auditor’s Independence Declaration 28

Independent Auditors’ Report 29

Directors’ Declaration 33

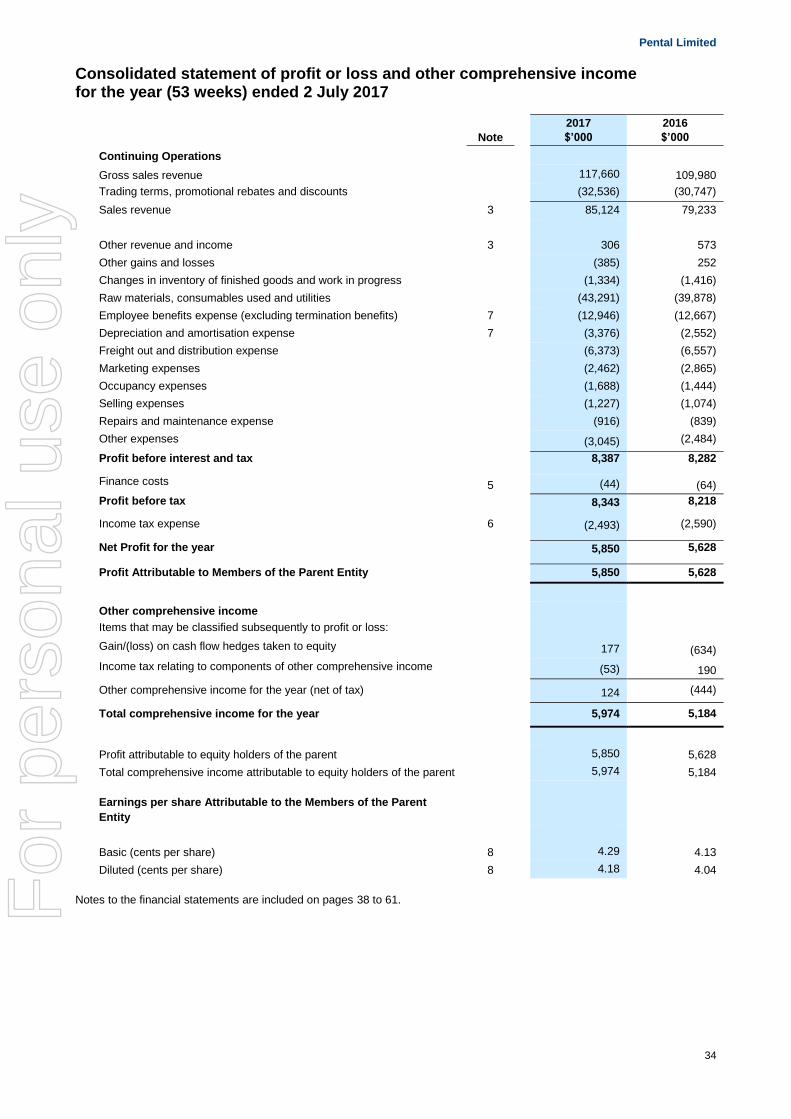

Consolidated Statement of Profit or Loss and Other Comprehensive Income

34

Consolidated Statement of Financial Position 35

Consolidated Statement of Changes in Equity 36

Consolidated Statement of Cash Flows 37

Notes to the Financial Statements 38

ASX Additional Information 62

For

per

sona

l use

onl

y

3

(i) Unaudited non-IFRS table

9,618 9,69010,287

10,834

11,923

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

FY 13 FY 14 FY 15 FY 16 FY17

$'0

00

Underlying EBITDA(i)

Chairman’s Review

On behalf of the Directors of Pental Limited, I am pleased to present the 2017 Annual Report. Looking back at 2017 financial year, we consolidated our position in a number of areas and continued with our growth strategy. Our net sales were up 7.4% (or 5.4% on a like-for-like 52 week year basis) supported by the manufacturing plants’ efficiency continuing to improve following recent years of capital investment.

Our focus on organic growth, coupled with ongoing emphasis on innovation, resulted in solid sales growth both in the Australian and New Zealand markets.

Market share of the White King Brand grew 6.3% and has allowed us to expand into new categories, such as the launch of the White King Blue range of non-bleach cleaning products.

Little Lucifer and Jiffy firelighters outperformed category growth, cementing Pental’s strong locally made credentials as the one and only firelighter manufacturer in Australia.

In the personal care category, sales growth was achieved through driving a strong promotional programme, which also supported the launch of various new products.

In our new Asian export channel, we are happy with the steady progress being made. Sales grew to $1.848 million, predominantly into China where we have increased our geographical reach and have teamed up with two of the more popular e-commence platforms in China. Furthermore, in June 2017 we also made our initial shipment into Vietnam. Whilst Asia opens new exciting growth opportunities, it will take time for Pental to establish its power brands in these new and competitive markets that are keen to embrace quality Australian-made goods.

The second new sales channel being developed is in the commercial/industrial sector. In the first half, the new bulk plant was successfully commissioned and a new range of five litre sized products were produced and launched under the White King, Sunlight and Huggie brands. We have developed and produced a portfolio of Commercial Products that will set up Pental’s entry into this channel to achieve the longer-term objective of becoming a significant recognised quality producer and supplier of Commercial Grade products.

Pleasingly, underlying Earnings Before Interest and Tax (EBIT) increased by 3.2%. However, in achieving a positive result, the company encountered operational challenges.

An unforeseen break down of Pental’s newly installed bleach filling line (which is under warranty) in January 2017 caused a shortage of stocks, impacting the result in the second half. Management was able to realign sales plans and change promotional activities in response, but these actions impacted gross margins in the second half. Margins have now returned to historical levels but Pental estimates the impact was $500,000 in lost earnings.

The next 12 months, Pental will focus on the soap factory infrastructure upgrade and soap packaging automation, as well as increasing plant capability to manufacture non-bleach products from the existing bleach liquid lines. This will be progressively undertaken to support future growth plans and strategy.

Financial performance

Net Profit After Tax was $5.850 million (up 3.8% on last year) and underlying EBITDA was $11.9 million (up 10.1% on last year, excluding $0.160 million in one-off ACCC legal costs - refer to the “Proceedings Against the Company” section of the Directors’ Report for further details.

The latest financial performance was also impacted by an unfavourable foreign currency exchange rate movement – causing a year-on-year impact of $0.637 million, even though Pental maintains a robust rolling 12 month foreign currency hedge book. Excluding the foreign exchange impact, year-on-year underlying EBIT increased 11.2%.

In achieving another solid result, the Board has recommended payment of a fully franked final year dividend of 2.10 cents per ordinary share. This brings the total dividend for the financial year to 3.25 cents per share (a 10.2% increase from FY16’s 2.95 cents per share), representing a payout ratio of 75.7% (2016: 71.4%).

Following approval by shareholders at the November 2016 Annual General Meeting, Pental exercised its option to buy back the Shepparton manufacturing site on 3 July 2017. The estimated acquisition cost (including stamp duty and related costs) is $7.345 million, with settlement of the property completed on 2 August 2017. This will be funded from Pental’s year-end cash position of $11.660 million.

For

per

sona

l use

onl

y

4

Looking forward

Pental continues to reinforce its operational foundations enabling it to focus on delivering significant and sustainable improvements, using the latest technology to increase efficiency and relentlessly drive costs down.

Understanding the market dynamics and consumer needs will help us to deliver new and innovative products that reinforce the superior performance and efficacy of our products. Through supporting our power brands, this will allow us to keep growing in Australia, New Zealand and Asia, and expand into new segments and channels.

The directors would like to thank all of our employees for their commitment and contribution during the year, and shareholders, suppliers and customers for their ongoing loyalty and support.

Peter Robinson

Chairman

For

per

sona

l use

onl

y

Pental Limited

Corporate governance statement

5

Corporate Governance Statement

This Corporate Governance Statement sets out the Company’s current compliance with the ASX Corporate Governance Council’s Principles of Good Corporate Governance and Best Practice Recommendations (Best Practice Recommendations).

The Company's website www.pental.com.au contains an Investor Section, which details the Company's Corporate Governance policies and procedures. This provides public access to all the information relevant to the Company meeting its corporate governance obligations.

BEST PRACTICE RECOMMENDATION COMMENT

1. Lay solid foundations for management and oversight

1.1 A listed entity should disclose:

(a) the respective roles and responsibilities of its board and management; and

(b) those matters expressly reserved to the board and those delegated to management.

The Corporate Governance Policies include a Board Charter, which discloses the specific responsibilities of the Board and provides that the Board shall delegate responsibility for the day-to-day operations and administration of the Company to the Chief Executive Officer.

The responsibilities of the Board, which are reserved for the Board and not delegated to management, include:

Oversight of the business and affairs of the Company;

Establishment of control and accountability systems;

Establishment with management of a strategic direction, supporting strategies and operating performance objectives;

Appointing the Chief Executive Officer (CEO) and any Executive Director; and

Reviewing and ratifying systems of risk management and internal compliance and control, codes of conduct and legal compliance.

The Board Charter is available on the Company’s website.

1.2 A listed entity should:

(a) undertake appropriate checks before appointing a person, or putting forward to security holders a candidate for election, as a director; and

(b) provide security holders with all material

information in its possession relevant to a

decision on whether or not to elect or re-elect

a director.

The Board has not established a Nominations Committee given the size of the Board and the Company’s operations. The Board as a whole performs the role of selection of potential new directors, and appropriate checks are made before an appointment occurs.

The Company provides security holders with all material information in its possession concerning the appointment or re-appointment of a director in the Notice of Shareholder Meeting concerning that appointment or re-appointment. A recommendation of the Directors concerning that appointment or re-appointment is also given.

1.3 A listed entity should have a written agreement with each director and senior executive setting out the terms of their appointment.

The Company has a written agreement with each director and senior executive setting out the terms of their appointment.

1.4 The company secretary of a listed entity should be accountable directly to the board, through the chair, on all matters to do with the proper functioning of the board.

The company secretary is accountable directly to the board, through the chair, on all matters to do with the proper functioning of the board. The current company secretary is a long-standing appointee and has direct contact with all directors as and when required.

1.5 A listed entity should:

(a) have a diversity policy which includes requirements for the board or a relevant committee of the board to set measurable objectives for achieving gender diversity and to assess annually both the objectives and the entity’s progress in achieving them;

The Company does not have a specific policy or measurable objectives for achieving gender diversity. The Board believes the existing Code of Conduct anti-discrimination provisions provides for this. The Company does not believe it is appropriate to establish a quota system for measuring gender diversity, and indeed such a quota system could itself lead to discrimination.

For

per

sona

l use

onl

y

Pental Limited

Corporate governance statement

6

BEST PRACTICE RECOMMENDATION COMMENT

(b) disclose that policy or a summary of it; and

(c) disclose as at the end of each reporting period the measurable objectives for achieving gender diversity set by the board or a relevant committee of the board in accordance with the entity’s diversity policy and its progress towards achieving them and either:

(1) the respective proportions of men and women on the board, in senior executive positions and across the whole organisation (including how the entity has defined “senior executive” for these purposes); or

(2) if the entity is a “relevant employer” under the Workplace Gender Equality Act, the entity’s most recent “Gender Equality Indicators”, as defined in and published under that Act.

The Company has instead required management to monitor gender diversity in line with the Corporate Governance Council Recommendations and intends to take appropriate action should it be of the view that there is insufficient gender diversity within the business.

As at 2 July 2017, there were 29 women employed representing 21.82% of total employees. There was one woman on the Board of Directors.

1.6 A listed entity should:

(a) have and disclose a process for periodically evaluating the performance of the board, its committees and individual directors; and

(b) disclose, in relation to each reporting period, whether a performance evaluation was undertaken in the reporting period in accordance with that process.

The Company does not have a formal policy for the periodic evaluation of it Board. The Board does not consider that a formal policy is necessary given the size of the Board and operations of the Company. The Board did however conduct a performance evaluation during the financial period.

1.7 A listed entity should:

(a) have and disclose a process for periodically evaluating the performance of its senior executives; and

(b) disclose, in relation to each reporting period, whether a performance evaluation was undertaken in the reporting period in accordance with that process.

The Board is responsible for assessing the performance of the Chief Executive Officer. The Chief Executive Officer is responsible for assessing the performance of the key executives within the Company, in conjunction with the Board. Executive assessments are conducted annually.

Formal appraisals are conducted at least annually for other staff and key performance indicators are set.

A performance evaluation for senior executives has taken place during the year under the process disclosed.

2. Structure the board to add value

2.1 The board of a listed entity should:

(a) have a nomination committee which:

(1) has at least three members, a majority of whom are independent directors; and

(2) is chaired by an independent director,

and disclose:

(3) the charter of the committee;

(4) the members of the committee; and

(5) as at the end of each reporting period, the number of times the committee met throughout the period and the individual attendances of the members at those meetings; or

(b) if it does not have a nomination committee, disclose that fact and the processes it employs to address board succession issues and to ensure that the board has the appropriate balance of skills, knowledge, experience, independence and diversity to enable it to discharge its duties and responsibilities effectively.

The Board has not established a Nominations Committee. The Board as a whole carries out the functions of a Nominations Committee, and Pental believes this is appropriate for a Company of its size and business. The Board seeks to ensure that it has an appropriate mix of skills necessary to fulfil its obligations.

For

per

sona

l use

onl

y

Pental Limited

Corporate governance statement

7

BEST PRACTICE RECOMMENDATION COMMENT

2.2 A listed entity should have and disclose a board skills matrix setting out the mix of skills and diversity that the board currently has or is looking to achieve in its membership.

Pental does not have a board skills matrix. The names and details of Directors in office at the date of this Annual Report, including skills, experience, term of office and expertise, are included in the Directors' Report Section of this Annual Report.

2.3 A listed entity should disclose:

(a) the names of the directors considered by the board to be independent directors;

(b) if a director has an interest, position, association or relationship of the type described in Box 2.3 but the board is of the opinion that it does not compromise the independence of the director, the nature of the interest, position, association or relationship in question and an explanation of why the board is of that opinion; and

(c) the length of service of each director.

Directors of Pental are considered to be independent when they are independent of management and free from any business or other relationship that could materially interfere with the exercise of their independent judgment. The following Directors are considered to be Independent: Mr Peter Robinson, Mr John Rishworth, Ms Kimberlee Wells and Mr John Etherington. Mr Mel Sutton is not considered to meet the test of independence as he has provided consultancy services to the Group during the previous reporting period.

The date of appointment of each Director is set out in the Directors’ Report Section of this Annual Report.

2.4 A majority of the board of a listed entity should be independent directors.

At the date of this report and during the period a majority of directors were independent directors.

2.5 The chair of the board of a listed entity should be an independent director and, in particular, should not be the same person as the CEO of the entity.

The Chairman is an independent director. The Chief Executive Officer is not the Chairman.

2.6 A listed entity should have a program for inducting new directors and provide appropriate professional development opportunities for directors to develop and maintain the skills and knowledge needed to perform their role as directors effectively.

The Company has an induction program for new directors.

The Company does not provide professional development opportunities for Directors. Given the current skill sets of each Director the Board considers that this is unnecessary.

3. Promote ethical and responsible decision-making

3.1 A listed entity should:

(a) have a code of conduct for its directors, senior executives and employees; and

(b) disclose that code or a summary of it.

The Company has a formal Code of Conduct, which applies to all Pental directors, employees, and contractors. A summary of this policy is available on the Company website within the Corporate Governance Section.

The Company’s Corporate Governance Section includes the Securities Trading Policy, which regulates dealings by directors, officers and employees in securities issued by the Company.

For

per

sona

l use

onl

y

Pental Limited

Corporate governance statement

8

BEST PRACTICE RECOMMENDATION COMMENT

4. Safeguard integrity in financial reporting

4.1 The board of a listed entity should:

(a) have an audit committee which:

(1) has at least three members, all of whom are non-executive directors and a majority of whom are independent directors; and

(2) is chaired by an independent director, who is not the chair of the board,

and disclose:

(3) the charter of the committee;

(4) the relevant qualifications and experience of the members of the committee; and

(5) in relation to each reporting period, the number of times the committee met throughout the period and the individual attendances of the members at those meetings; or

(b) if it does not have an audit committee, disclose that fact and the processes it employs that independently verify and safeguard the integrity of its corporate reporting, including the processes for the appointment and removal of the external auditor and the rotation of the audit engagement partner.

The Board has established an Audit Committee. The Audit Committee consisted of four members, the majority of whom are independent directors.

The Chair of the Committee was and is not the Chair of the Board during the period.

The names of the members of the Committee, details of their qualifications and experience and details of the number of meetings held during the period, are contained in the Directors’ Report section of this Annual Report.

The Audit Committee operates under a Charter which is available on the Company website within the Corporate Governance Section.

4.2 (a) The board of a listed entity should, before it approves the entity’s financial statements for a financial period, receive from its CEO and CFO a declaration that, in their opinion, the financial records of the entity have been properly maintained and that the financial statements comply with the appropriate accounting standards and give a true and fair view of the financial position and performance of the entity and that the opinion has been formed on the basis of a sound system of risk management and internal control which is operating effectively.

The Board has obtained the relevant assurances from management.

4.3 A listed entity that has an AGM should ensure that its external auditor attends its AGM and is available to answer questions from security holders relevant to the audit.

The external auditor attends its AGM and is available to answer questions from security holders relevant to the audit.

5. Make timely and balanced disclosure

5.1 A listed entity should:

(a) have a written policy for complying with its continuous disclosure obligations under the Listing Rules; and

(b) disclose that policy or a summary of it.

The Company has in place a Continuous Disclosure Policy, which has been implemented across the Company. The Policy is available on the Corporate Governance section of the Company website.

For

per

sona

l use

onl

y

Pental Limited

Corporate governance statement

9

BEST PRACTICE RECOMMENDATIONS COMMENT

6. Respect the rights of shareholders

6.1 A listed entity should provide information about itself and its governance to investors via its website.

The Company provides information about itself and its governance on its website. All policies and charters concerning governance issues are located on a dedicated section headed Corporate Governance.

6.2 A listed entity should design and implement an investor relations program to facilitate effective two-way communication with investors.

The Company has in place a Shareholder Communication Policy, which promotes effective communication with shareholders. The Policy is available on the Corporate Governance section of the Company website.

6.3 A listed entity should disclose the policies and processes it has in place to facilitate and encourage participation at meetings of security holders.

The Company has in place a Shareholder Communication Policy, which promotes effective communication with shareholders. The Policy is available on the Corporate Governance section of the Company website.

6.4 A listed entity should give security holders the option to receive communications from, and send communications to, the entity and its security registry electronically.

The Company gives security holders the option to receive communications from, and send communications to, the entity and its security registry electronically.

7. Recognise and manage risk

7.1 The board of a listed entity should:

(a) have a committee or committees to oversee risk, each of which:

(1) has at least three members, a majority of whom are independent directors; and

(2) is chaired by an independent director,

and disclose:

(3) the charter of the committee;

(4) the members of the committee; and

(5) as at the end of each reporting period, the number of times the committee met throughout the period and the individual attendances of the members at those meetings; or

(b) if it does not have a risk committee or committees that satisfy (a) above, disclose that fact and the processes it employs for overseeing the entity’s risk management framework.

The Audit Committee referred to in section 4 also oversees risk as part of its Charter.

7.2 The board or a committee of the board should:

(a) review the entity’s risk management framework at least annually to satisfy itself that it continues to be sound; and

(b) disclose, in relation to each reporting period, whether such a review has taken place.

The Audit Committee reviews the Company’s risk management framework annually and specific risks at each meeting. Key risks are referred to the Board periodically, and management reports on whether risk is being effectively managed.

For

per

sona

l use

onl

y

Pental Limited

Corporate governance statement

10

BEST PRACTICE RECOMMENDATION COMMENT

7.3 A listed entity should disclose:

(a) if it has an internal audit function, how the function is structured and what role it performs; or

(b) if it does not have an internal audit function, that fact and the processes it employs for evaluating and continually improving the effectiveness of its risk management and internal control processes.

The Company does not have an internal audit function. The Board considers that this is unnecessary given the size of the Company’s operations.

The Audit Committee reviews the Company’s risk management framework and risks generally. Where desirable, the Company has requested its external auditors to review particular operations to ensure internal controls are effective.

7.4 A listed entity should disclose whether it has any material exposure to economic, environmental and social sustainability risks and, if it does, how it manages or intends to manage those risks.

The Company does not have any economic, environmental and social sustainability risks over and above those of every commercial organisation, and not already disclosed to security holders.

8. Remunerate fairly and responsibly

8.1 The board of a listed entity should:

(a) have a remuneration committee which:

(1) has at least three members, a majority of whom are independent directors; and

(2) is chaired by an independent director,

and disclose:

(3) the charter of the committee;

(4) the members of the committee; and

(5) as at the end of each reporting period, the number of times the committee met throughout the period and the individual attendances of the members at those meetings; or

(b) if it does not have a remuneration committee, disclose that fact and the processes it employs for setting the level and composition of remuneration for directors and senior executives and ensuring that such remuneration is appropriate and not excessive.

The Board has established a Remuneration Committee. The Remuneration Committee operates under a Charter, which is available on the Company’s website.

Memberships of the Committee, and details of meetings held during the period, are contained in the Directors’ Report section.

8.2 A listed entity should separately disclose its policies and practices regarding the remuneration of non-executive directors and the remuneration of executive directors and other senior executives.

Remuneration policies are set out in the Remuneration Report section of this Annual Report.

When thought desirable the Board utilises specialist third parties to benchmark executive and non-executive director remuneration.

8.3 A listed entity which has an equity-based remuneration scheme should:

(a) have a policy on whether participants are permitted to enter into transactions (whether through the use of derivatives or otherwise) which limit the economic risk of participating in the scheme; and

(b) disclose that policy or a summary of it.

The Company has established an Executive Performance Rights Plan that may result in the issue of securities to executives. As those securities will be ordinary shares there is no policy on permitting participants to enter into transactions limiting the risk of participation in the scheme.

For

per

sona

l use

onl

y

11

Directors’ report

The directors of Pental Limited submit herewith the annual financial report of the company for the year (52 weeks) ended

2 July 2017. In order to comply with the provisions of the Corporations Act 2001, the directors report as follows:

Information about the directors

The names and particulars of the directors of the company during or since the end of the financial year are:

Name & Qualifications Experience and Responsibilities

Mr Peter Robinson B.Eco (Mon) Non-Executive Independent Chairman

Peter has a wealth of experience in the manufacturing sector within Australia and internationally. He was the Chief Executive of ACI Packaging Group and Vice President of Owens-Illinois Inc, the parent company of ACI Packaging Group. Previous roles include Chief Operating Officer and Director of BTR Nylex Limited, and General Manager of Bowater Scott, where he held substantial marketing roles. Appointed Director on 29 November 2002. Appointed Chairman on 5 March 2009. Member of the Audit Committee and Chairman of Remuneration Committee.

Mr Mel Sutton B.Com

Non-Executive Vice-Chairman

Mel has extensive experience and a diverse background across a number of key sectors, including food-production, wholesale and retail; facility services; apparel and footwear - wholesale and retail; consumer goods - beverage; and sporting goods - wholesale and retail. Mel was CEO and a Managing Director of Nike Pacific, Globe International, Colorado Group and a Divisional Chief Executive of George Weston Foods Limited and Spotless Group. Previous roles also include senior executive positions with Lion Nathan and Foster’s. Mel, as a Director of ZABS Advisory & Consulting Pty Ltd, currently provides advisory services across a wide range of disciplines to clients, who operate in and across diverse sectors. Appointed Director 2 October 2013. Member of Audit Committee and Member of Remuneration Committee.

Mr John Rishworth Non-Executive Independent Director

John has worked in the Fast Moving Consumer Goods sector for over 30 years. He held significant senior positions within Woolworths before founding his own successful retail brokerage business in 1987. Since selling that business he has taken on a number of consultancy assignments within the retail sector. Appointed Director 9 September 2004. Member of Audit Committee and Member of Remuneration Committee

Mr John Etherington B.Ec, FCA, FAICD Non-Executive Independent Director

John is a former senior partner of Deloitte, where he held both senior leadership positions and provided audit and advisory services to public, private and not for profit organisations, with a particular specialisation on rapidly-growing Australian-listed entities. He is also currently a non-executive director on a range of public and private organisations. Appointed Director 2 April 2013. Chairman of Audit Committee and Member of Remuneration Committee.

Ms Kimberlee Wells Non-Executive Independent Director

Kimberlee has spent her career building the brands of large blue-chip organisations including ANZ, NAB, Medibank, Qantas and Myer. She has written countless digital transition strategies for her clients and works in almost daily partnership with the digital pioneers of our time including Google and Facebook. Kimberlee also lectures with RMIT University, the Australian Direct Marketing Institute and other industry bodies. Kimberlee is currently the CEO of Whybin\TBWA Group Melbourne - a tier one global advertising and digital agency. Previous roles included senior management positions with BBDO, Wunderman and M&C Saatchi. Appointed Director 19 November 2015. Member of Remuneration Committee.

The above named directors held office during the whole of the financial year and since the end of the financial year. Any directorships of other listed companies held by directors in the three years immediately before the end of the financial year are indicated above under “experience and responsibilities”.

For

per

sona

l use

onl

y

12

Directors’ shareholdings

The following table sets out each director’s relevant interest in shares, debentures, and rights or options in shares or

debentures of the company or a related body corporate as at the date of this report.

Directors Fully paid ordinary shares

Number

Share options

Number

Peter Robinson 3,972,926 -

Mel Sutton - -

John Rishworth 13,207 -

John Etherington 160,000 -

Kimberlee Wells - -

Share options granted to directors and senior management

During and since the end of the financial year no share options were granted to directors or senior management, however

senior management were issued Rights pursuant to the Executive Performance Rights Plan as detailed in the Remuneration

Report.

Company secretary

Name & qualifications

Mr Oliver Carton B Juris LL.B Company Secretary

Experience and Responsibilities

Oliver is a qualified lawyer with over 29 years’ experience in a variety of corporate roles. He currently runs his own consulting business, and was previously a Director of the Chartered Accounting firm KPMG where he managed its Corporate Secretarial Group. Prior to that, he was a senior legal officer with ASIC.

Oliver is an experienced company secretary and is currently company secretary of a number of listed and unlisted companies, ranging from Pental Limited to the not for profit Melbourne Symphony Orchestra Pty Ltd.

Principal activities

The principal activities of the Group during the course of the financial year were the manufacturing and distribution of personal care and home products.

Company Overview - Trusted brands that get the job done

From humble beginnings Pental Limited has grown to include a portfolio of leading brands, which have become household names in Australia and New Zealand. Today we are an innovative market leader and the largest local manufacturer of bar soaps, liquid bleach and cube firelighters.

For more than 60 years we’ve worked hard to stay true to our Australian heritage, maintaining 90% of manufacturing at our plant in Shepparton, Victoria, supplemented with third party contract manufacturing in New Zealand for the local market. There are four distinct production plants at the Shepparton site, comprising the Soap plant, Bleach plant, Liquids plant and Firelighters plant.

Pental has grown through an unrelenting dedication to innovation, efficiency and quality. This foundation has made Pental a trusted manufacturer of household and commercial products, taking our business across Australia and New Zealand, and now into new Asian markets.

Our Brands

Personal Care Household cleaning Laundry Fire Needs Kitchen

Pental’s products are seen in more than 4,000 supermarkets, 700 pharmacies and 300 petrol and convenience, corner and hardware stores in Australia and New Zealand and the Company is now establishing a presence in Asia (commencing with China) and expanding into the commercial/industrial channels. These products are distributed from Shepparton (Victoria), Christchurch and Auckland (New Zealand), and the Shanghai and Ningbo Free Trade Zones (China) warehouses.

For

per

sona

l use

onl

y

13

FY17 (i) FY16 (i)

$’000 $’000 % Change

Reported profit after tax 5,850 5,628 3.9%

Income tax expense 2,493 2,590

Finance costs 44 64

EBIT 8,387 8,282 1.3%

One off - ACCC legal costs 160 -

Underlying EBIT 8,547 8,282 3.2%

Depreciation and amortisation 3,376 2,552

Underlying EBITDA 11,923 10,834 10.1%(i)

Unaudited non-IFRS financial table

Review of operations

Financial Performance

Gross sales of $117,660 million were up 7.0% or $7.680 million on last year, or 5.0% excluding the 53rd trading week on like-for-like.

o Gross sales in the Australian market were up 7.7%, with strong growth with the White King cleaning range, the Little Lucifer and Jiffy firelighters range, Country Life and Pears personal care range, and private label.

o New Zealand market share in a number of categories such as Toilet, Household Cleaning and Dish Wash continues to be solid. The ongoing aggressive marketing by competitors, in particular in the Dish Wash category, caused gross sales to be 1.0% down (3.7% in New Zealand dollars). However, with an improved promotional tactical program and the launch of new products, net sales (after trade spend) was up 4.6% (2.1% in New Zealand dollars).

o Expansion into Asia continues to grow at a steady pace, albeit slower than initially anticipated. Sales increased by $1.157 million to $1.837 million (first half $0.664 million and 2nd half $1.173 million). Ranging of Pental’s personal care brands (Country Life and Velvet), and cleaning brands (White King and Softly) in retail stores and through online channels in China continues to grow, as has Pental’s contract manufacturing business, where Asian customers are seeking high-quality Australian made products. Furthermore, Pental’s first shipment to Vietnam commenced in June 2017 and the company is actively developing other new export opportunities in the Asian region.

Trade spend (trading terms, promotional activities and discounts) at 28.1% of Australian and New Zealand gross sales was largely in line with the previous corresponding period. The current period also including the promotional activities to launch the Country Life Liquids range in the Australian market and support for expansion of the White King range and other personal care ranges.

Net sales (after trade spend) of $85.124 million were up 7.4% or $5.891 million on last year, or 5.4% excluding the 53rd trading week on like for like.

For

per

sona

l use

onl

y

14

Underlying EBIT (Earnings Before Interest and Tax) of $8.547 million was $0.265 million (or 3.2%) up on last year, after excluding one-off ACCC legal costs - refer to the “Proceedings Against the Company” section of the Directors’ Report for further details.

Although a solid result, the financial performance was also impacted by:

o an unforeseen break down of Pental’s newly installed bleach filling line (which is under warranty) in January 2017 which caused a shortage of stocks, impacting the result in the second half. Management was able to realign sales plans and change promotional activities in response, but these actions impacted gross margins in the second half. Margins have now returned to historical levels but Pental estimates the impact was $500,000 in lost earnings; and

o the year-on-year impact of foreign currency changes of $0.937m arising from the deterioration of the Australian dollar against the United States and New Zealand currencies. Pental continues to actively hedge its currency exposures on a rolling 12 month basis; and

Excluding the foreign exchange loss the underlying EBIT was $8.932 million, up $0.902 million or 11.2% (after excluding the prior year’s foreign exchange gain).

While EBIT was impact by the breakdown of equipment, operational costs continued be driven down:

o Freight out costs to customers decreased further this year, through renegotiation of routes and optimisation of

container re-usage. Freight costs to gross sales decreased by 0.55% to 5.42%;

o Renegotiation of non-commodity based raw materials and services has led to $1.087 million in Profit Delivery

Project savings;

o Direct wages net of manufacturing recoveries improved by $0.671 million (or 28.7%) on last year, with a 9.1%

increase in the number of cartons produced arising from improved manufacturing efficiency driven from the

capital investment completed in the prior year and continuous improvement in manufacturing disciplines; and

o Refocused marketing to specific in-store promotional activities and catalogues (that is, trade spend).

However, these significant savings were offset by: o Significant increases in gas and electricity prices;

o The rise in some commodity based raw materials, such as tallow and coconut, used in Country Life soaps; and

o A depreciation increase of $0.824 million following the recent years of significant capital investment to modernise the manufacturing facilities.

Consolidated net profit after tax for the year (53 weeks) ended 2 July 2017 was $5.850 million (2016: $5.628 million).

The total dividend for the 2017 financial year is 3.25 cents per ordinary share, representing 75.7% (2016: 71.4%) of the full-year net profit after tax and consists of :

- Interim fully franked dividend of 1.15 cents per ordinary share, which was paid 24 March 2017; and

- Proposed final fully franked dividend of 2.10 cents per ordinary share, payable to shareholders on 29 September 2017, with a record date of 11 September 2017.

Basic earnings per share of 4.29 cents increased from 4.13 cents in 2016. Cash generation and capital management

Operating cash flow of $6.615 million decreased by $4.644 on last year, predominately due to the FY16 and FY17 taxes paid in the current year, whilst there was no tax payment due in the prior year.

Net working capital (receivables, inventories less trade and other payables) of $16.668 million was also higher than last year by $0.879 million as the business increased its safety stock levels. This was as the major retailers continue to seek to minimise their stock holdings whilst requiring suppliers to maintain a Delivery In Full and On Time (DIFOT) benchmark of 97%. Pental’s prior year investment in new warehousing facilities and a strong balance sheet, with cash at bank of $11.660 million, allowed the business to effectively execute this change.

The net debtors and creditors position improved on last year due to timing of the 53 week financial year that closed on 2 July 2017 compared to the prior year closure on 26 June 2016. This resulted in additional cash receipts in FY17. It is also pleasing to report that Pental’s debtors’ position continues to be solid, with minimal over dues.

As previously indicated, cash reserves have been maintained pending the acquisition of the Shepparton property, which was approved by shareholders at the November 2016 Annual General Meeting. Settlement of the property was completed on 2 August 2017, following Pental exercising its buy back option on 3 July 2017. The purchase price is $6.891 million plus estimated stamp duty and related costs of $0.454 million. The total estimated acquisition cost is $7.345 million.

Cash reserves will also be utilised to complete further major capital works to upgrade the manufacturing facilities, which is expected over the next two years before returning to a normalised level of capital expenditure. Major capital works in FY18 will include the commencement of the soap plant upgrade and increasing plant capacity in producing non bleach based products.

For

per

sona

l use

onl

y

15

Strategic objectives & activities - Five key pillars to drive growth

Pental’s vision is to be a leading supplier of shelf stable (non-food) products to its chosen markets built around a reputation of delivering quality, innovation and sustainability to the satisfaction of customer needs whilst enhancing shareholder value.

Pental remains focused on what we believe are the highest-value opportunities for driving long-term profitable growth and generating solid total shareholder returns. The five strategic pillars to drive growth have continued to guide our decisions. A review of FY17 outcomes and progress follows:

Strategic Objective Outcomes and progress in FY17

1. Creating a solid platform for growth;

Continuously improving on the basics: safety, people, engagement, environment, quality, customer service, preventative maintenance processes, logistics and information systems; and

Installing cost-effective, high-performance manufacturing capability, where importation of the product is not cost effective and/or not aligned with its Australia made, Australia-owned marketing positioning.

Our health and safety vision, ‘Safety must always come first”, means we will not compromise on workplace safety in the pursuit of other business goals. We care about the health and safety of our employees, contractors and visitors, and we are focused on eliminating work-related injury. We believe that all incidents are preventable. There is a continuing commitment to identify and eliminate risks with the prime objective being to prevent injuries from occurring.

Through a safety conscious work force supported by safety initiatives such as safety walks by managers, random safety reviews for sections of the plant and monthly safety meetings, we have not only protected our team, but Pental’s WorkCover continues to be below industry standard. However, as much as we aim for zero harm, one lost time injury was reported in FY17.

While our strategic direction is top of mind with our employees, this cannot be delivered without fostering a highly motivated team committed to Pental’s core values. Maintaining a strong company culture is a critical organisational enabler and in 2017 our people substantively reconfirmed Pental’s core values and have continued to positively drive continuous improvement disciplines throughout the operations.

As continuous improvement disciplines spread throughout the manufacturing operations, the business recognised that engineer skills and preventative maintenance disciplines remained below expectations and was one of the causes of not consistently achieving the efficiency targets. As a result two senior engineers were appointed in the first half of FY17 with the appropriate skills to manage the new state-of-the-art equipment and to enhance the preventative maintenance disciplines. A refocused manufacturing operations team has steadily increased efficiency levels, which resulted in direct wages net of manufacturing recoveries improving by 28.7% on last year with 9.1% more cartons produced.

Preventative maintenance, whilst improved, is still a key area of focus in FY18, as we continue to build robust and sustainable disciplines.

Though it was pleasing to see the production efficiency progress being made, an unforeseen breakdown of Pental’s newly installed bleach filling line in January 2017 caused a shortage of stocks, impacting the result in the second half. Management was able to realign sales plans and change promotional activities in response, but these actions impacted gross margins in the second half. Margins have now returned to historical levels. The breakdown also caused our service levels measured by “DIFOT” (Delivered in Full On Time) to fall below acceptable levels and in turn led to loss of higher margin sales.

For

per

sona

l use

onl

y

16

Strategic Objective Outcomes and progress in FY17

The poor DIFOT, not only had a direct impact on the White King and Janola business, but also delayed the roll out of new products, until Pental returned to acceptable DIFOT levels.

Whilst DIFOT has returned to industry acceptable levels, further works are underway to ensure raw materials are delivered in time and as specified, such as in supplier operational audits, and that the preventative maintenance program is further improved to minimise unplanned stoppages, thus increasing plant efficiency.

During the year $3.067 million of capital improvements were undertaken, which included numerous smaller plant upgrades and replacements, site improvements and the completion of projects initiated in the prior year such as soap cutting equipment, SWING plant and installation of the new bulk plant. Following the new bulk plant commissioning in September 2016, it delivered on the first objective to reduce the cost of bulk products previously outsourced. Furthermore, the new equipment successfully produced a new range of commercial and industrial cleaning products under the White King and Sunlight brands.

The next major phases of the manufacturing strategy involves:

o upgrading of the bar soap factory;,

o increasing the level of automation in soap packaging; and

o increasing plant capacity to produce non-bleach based products. This will involve using existing “bleach” filling and packaging equipment with new batching equipment and processes to produce both non–bleach and bleach products.

Business cases for these upgrades are being evaluated and will depend on branded and private label sales growth opportunities in Australasia and Asia.

2. Optimising value growth from the current portfolio;

Focus on and over invest in growth categories and our power brands;

Build strategic alliances with category leaders to access customer insights and innovation pipeline;

Optimise pack and price in the right channel; and

Drive innovation - build its new product pipelines and launch new products to the market.

Pental has operated a common brand management process for several years. The process involves the creation of brand plans, which outlines the actions to be undertaken to grow and strengthen the brand for the year and beyond. The key focus was to grow our Core Power brands - White King, Country Life, Janola and Sunlight and then support our other “maintain” brands such as Jiffy, Little Lucifer, Velvet, Pears and Softy.

We also reviewed our longer-term position on a number of smaller trading brands and we expect to transition the smaller brands under some of our core “maintain” brands in order to increase key brand presence on shelf and leverage our marketing program over fewer larger brands compared to doing the same over numerous smaller brands. These transitional plans will be rolled out over the next few years. On the back of these brand plans the marketing and research and development teams launched a number of new products into growth categories, some previously not tackled by Pental. The successes and learnings have varied, but our innovation and drive to become a product leader is a key priority Pental will continue to aggressively pursue. During the year, some of the key products were launched into the market and others were developed and accepted by retailers ready for FY18:

White King Blue Range was launched in March 2017. The kitchen and bathroom cleaners have a non-bleach formulation, with comparative product testing indicating a higher efficacy. Pental is targeting to expand into this growth category. The White King brand market share continues to grow strongly at 6.3%*, with some key areas to note:

o Toilet cleaners grew 11.9%* o Household cleaners grew 5.9%* o White King Oxy grew 24.3%* o Increased White King Toilet shelf presence with key retailers

Whilst the general liquid bleach category of $19.2 is not growing, it continues to provide significant base and value in positioning expansion into other categories - White King has 80% of the branded liquid bleach market and Pental also supplies the majority of private label in this category*.

For

per

sona

l use

onl

y

17

Strategic Objective Outcomes and progress in FY17

On the back of success of the White King range in Australia, five new Janola toilet cleaning (Toilet PowerGel and In Bowl Cleaners) and

household cleaning (Mould & Soap Scum and bleach Power Cleaners) products were launched into the New Zealand market in June 2017.

New Sunlight Automatic Dish Washing tablets were developed during the year and will be ranged with New Zealand retailers in FY18. This is an exciting opportunity that complements the Sunlight Manual Dish Washing range (Sunlight being the third largest manual dish wash brand in New Zealand). Furthermore, Pental developed a new range of 2 litre dish washing liquids to diversify its range from 500ml and 750ml offerings, where the smaller sizes continue to be aggressively priced. The 2 litre size is now ranked the third top selling product* based on sales.

In early FY17 the Australian Country Life brand (mainly known for bar soaps) was launched into the liquid wash categories - entry into these categories was new to Pental. We achieved $1.660 million in gross sales in FY17 and the launch was strongly supported with significant investment through in-house development, digital marketing and in-store promotional activities (trade spend). However, “sales rate” per store did not achieve the expected levels with a major Australian grocery retailer.

Country Life Liquids ranging will continue with other retailers and we are excited with interest expressed in the export channel. In the short term we will refocus on Country Life bar soaps where Pental is the only manufacturer to be able to claim that its bar soaps are 100% Australian Made – from raw materials to finished products. At a later time, we will relaunch into the Australian grocery personal care liquid wash categories.

Little Lucifer brand was repositioned as the “Foodie’s Choice” fire needs range. This not only helped promote the key features of the firelighters, such as not affecting flavours, non-toxic and odourless, but allowed the fire range to be extended. In July 2017, Little Lucifer Scented Wood Chips were launched with retailers.

Similarly the Jiffy brand, in the fire needs category, was repositioned as the “outdoor living” firelighter brand, where Jiffy is the Number 1 selling product in grocery firelighters*. Furthermore, in June 2017 Jiffy Fire Lighting Sticks was introduced into the range.

Pental is the only firelighter manufacture in Australia (making its Jiffy and Little Lucifer 24 cube firelighters) and in FY17 significantly outperformed category growth and holds 42% of the grocery accounts*.

Following commissioning of the bulk plant, Pental launched a five litre commercial range of cleaning products. These included White King Sanitiser & Disinfectant, White King Floor cleaner, White King Glass Cleaner, Sunlight Rinse Aid, Sunlight Laundry Liquid and Sunlight Hand Wash.

A new Huggie range of fabric conditioners was launched in June 2017 on the back of the strong credentials provided by the Choice consumer advocacy group review of fabric softeners, which rated Pental’s Huggie Ultra Concentrate Fabric conditioner the best in the market. The new Huggie Easy Iron, Huggie Quick Dry and Huggie Eco Wash Fabric Concentrate range demonstrates Pental’s commitment to providing high-quality Australian products.

* Based on Aztec data

For

per

sona

l use

onl

y

18

Strategic Objective Outcomes and progress in FY17

As evident from the extensive new range of products, this was the key focus of the marketing budget in FY17 supported by in store activation and ongoing instore promotional activities (trade spend).

Pental’s power brands remain strong and front-of-mind in the marketplace, however we can’t slow down, in fact we are accelerating our actions to deliver both short-term and long-term sustainable growth, with innovative and quality products to consumers. In last quarter of FY17, we’ve put additional resources behind our brands by refreshing key sales, R&D and marketing positions to focus on highlighting the superior value of our brands and to accelerate driving new products into market, to be supported by strong targeted marketing programs and promotional activities in FY18.

3. Driving year-on-year real productivity savings;

Driving an agile business, eliminating low-value activities and reducing costs through product cost innovation and improved manufacturing techniques, supply chain optimisation and improved procurement, all lead to savings that can be reinvested to drive growth and improve profitability. Whilst the constant change of market conditions and ongoing price increase pressures from local and overseas suppliers has not subsided, Pental’s Continuous Improvement/Profit Delivery Projects process delivered significant savings of $1.087 million in FY17: For example:

o Renegotiation of pallet rates, changing from road to rail transport for certain destinations and container reusage.

o Improved buying of non-commodity based raw materials and services, and reduced wastage, such as fragrances, packaging, waste disposal costs;

o Minimising production changeover times;

o Reformulation of branded and private label of products; and

o Sourcing of finished products from new countries.

Furthermore, with the capital investment completed in prior years, and improved management of staffing and continuous improvement focused on increasing manufacturing efficiency, direct wages net of manufacturing recoveries improved by 28.7% on last year.

However, these significant savings were diluted by ongoing cost pressures from other areas, such as:

o Significant increases in gas and electricity prices. Although a number of initiatives have been introduced to minimise this impact,

utility price increases remain a challenge for the manufacturing sector; and

o The rise in some commodity-based raw materials, such as tallow and coconut, used in Country Life soaps. In FY17, the average

tallow was at a seven-year high. Pleasingly, in late May 2017 tallow prices improved. However, coconut prices remained very high,

due to the increased popularity of the ingredient.

Whilst year-on-year savings continues to be challenging, we are confident that the constant review of raw material and finished goods supply contracts, operational processes and other service costs will deliver ongoing savings and ensure Pental’s cost of goods remain competitive.

For

per

sona

l use

onl

y

19

Strategic Objective Outcomes and progress in FY17

4. Accelerating our capability to grow the export business and private label; and

We are excited with the steady progress being made to expand into new Asian markets; however it has proved to be challenging. In FY17 gross sales increased by $1.157 million, to $1.848 million. Geographically, we are widening our product reach from dotted cities along Eastern regions into wider regions and more provinces and cities into Central, Northern and Southern China, and in June 2017 a container also went to Vietnam. White King, Country Life, Velvet, Softly, Natural Selections sales have increased in a number of bricks and mortar stores and products were officially launched into two of the more popular e-commerce platforms in China - JD.com and Kaola.com.

Furthermore, on the back of increasing demand for Australian-made quality Pental branded products, which is our major focus, we also commenced contract manufacturing for multiple Chinese customers.

Whilst sales are slower than initially foreseen, it is worth remembering that Pental products and brands are totally new in this very competitive Chinese/Asian market. As a result, penetration into this new market will take some time for consumers to recognise our power brands and make their first and repeat purchases. Furthermore, during the year, progress was slowed as Chinese customs import regulations changed and Pental products required reverification, which was achieved without any concerns.

Bedding down the Chinese channel is the first step to building a sustainable Asian export business, which will continue to grow through enhancing Pental brand exposure in the Asian markets and the ongoing roll-out of new product development.

As we have innovated brand products, our private label sales growth of 6.0% on last year has being achieved by providing new formulas, fragrances and packaging formats to meet the progressive demands of today’s consumers. Private label represents 15% of gross sales and continues to be core element of the Pental business, and whilst sales growth is important, our key focus is on achieving commercially acceptable margins on the back of our manufacturing plant operating at optimum levels.

5. Driving growth through non-retail commercial and industrial channels.

The initial step of completing the commissioning of the new bulk plant was completed on target and on budget in September 2016. Concurrently, additional R&D and marketing resources were put in place, and we developed an exciting range of White King and Sunlight five litre products.

The launch of these commenced positively, with solid expression from a number of customers. However, due to staff turnover in the Pental commercial sales area, sales execution in these new channels was slower than initially anticipated. Initial ranging has been obtained in a number of new food, office and bulk good retailers and distributors. With further field development work to be undertaken in FY18, we expect this new channel to produce steady growth, whilst Pental establishes its new range of commercial cleaning products.

As the five pillars remain the cornerstone of our approach in organically growing the business, we also continue to search for new partnerships, distributorships and acquisitions that will complement the Company’s product range/expertise, and scope to leverage its infrastructure and/or provide the ability to expand into new channels.

For

per

sona

l use

onl

y

Pental Limited

Directors’ report

20

Operational risks

There are a number of operational risks, both specific to Pental and of a general nature, which may impact the future operating and financial performance of the Group. There can be no guarantee that Pental will achieve its objectives or that forward looking statements will be realised. The operating and financial performance is influenced by a variety of general economic and business conditions including levels of consumer spending, inflation, interest and exchange rates, and certain raw material prices such as tallow and/or sustainable palm noodles used in some soap products, and the price of resin affecting the cost of bottles. The specific material business risks faced by the Group and how the Group manages these risks are set out below:

Competition: the majority of Pental’s products are sold in supermarkets in Australia and New Zealand, which are dominated by two major participants in Australia. These retailers have been aggressively reviewing their product mix and also implementing a move towards their own or private label products. This has the potential to lead to delisting of Pental’s products by one or both of those retailers, which could cause a significant drop in sales of any product delisted. The two major participants have also been engaging in an aggressive campaign for market share, primarily through product price reductions. This has made it difficult for Pental to pass on price rises, despite rising production costs, thus impacting margins. This situation is not expected to change in the short to medium term. Pental believes it can continue to successfully operate in the Fast Moving Consumer Goods market through strong product innovation and managing its product sourcing and manufacturing costs;

Product sourcing: Pental relies on a range of parties for its product-sourcing strategy. Any change in existing relationships (including the termination of any key supply arrangements) or any change in terms or conditions of overseas/local suppliers and any change in the political or economic environment may lead to material adverse changes to Pental’s operational and financial performance. Pental is continually refining its sourcing arrangements and has in many instances dual sourcing arrangements that facilitates in reducing this risk;

Supply chain: Pental has established an extensive and reliable supply chain that allows it to procure and deliver products to customers in a timely and efficient manner. Disruption to any aspect of this supply chain could have a material adverse impact on Pental’s operational and financial performance. Pental’s ongoing review of supply chain costs and the corresponding change of supply chain arrangements with minimal disruption, shows that Pental is able to effectively manage this risk;

Loss of key personnel : Pental’s future success depends to a significant extent on the retention of key personnel, in particular its management team. These individuals have extensive experience in, and knowledge of the market Pental operates in and Pental's business. The loss of key personnel and the time taken to recruit suitable replacements or additional personnel could adversely affect the Company’s future financial performance. The Board has reviewed the organisational structure of the business and will continue to do so to ensure the best people are retained, whilst investing in developing other key people in the business; and

Damage to Pental's brands: the reputation and value associated with Pental’s brand names could be adversely impacted by a number of factors including failure to provide customers with the quality of products they expect and disputes with third parties such as suppliers or customers or adverse media coverage. Significant erosion in the reputation of, or value associated with, Pental's brands could have an adverse effect on Pental’s future financial performance. Pental believes that its processes and systems, and proactive tracking and management of any disputes, minimises this risk.

Outlook

The outlook for the Group is contained in the Chairman’s report.

Changes in the state of affairs During the financial year there were no significant changes in the state of affairs of the Group, other than as referred to in this Annual Report.

Future developments

Information regarding likely developments in the operations of the Group in future financial years is set out in the Review of

operations and elsewhere in the Annual Report.

Subsequent events

There has not been any matter or circumstance occurring subsequent to the end of financial year that has significantly

affected, or may affect, the operations of the Group, the results of those operations, or the state of affairs of the Group in

future financial years, except for:

Acquisition of Shepparton Property

Following the approval by shareholders at the November 2016 Annual General Meeting, Pental exercised its option to buy back the Shepparton property on 3 July 2017. The purchase price is $6.891 million plus estimated stamp duty and related costs of $0.454 million. Total estimated acquisition cost is $7.345 million. Settlement of the property was completed on 2 August 2017.

For

per

sona

l use

onl

y

Pental Limited

Directors’ report

21

Dividends

In respect of the year (53 weeks) ended 2 July 2017 an interim fully franked dividend of 1.15 cents per ordinary share was paid on 24 March 2017, and the directors have declared the payment of a final fully franked dividend of 2.10 cents per ordinary share, payable to shareholders on 29 September 2017, with a record date of 11 September 2017. The total dividend for the FY17 financial year of 3.25 cents per share represents a payout ratio of 75.7%.

In the prior year ended 26 June 2016, the total dividend paid was 2.95 cents per ordinary share, representing a payout ratio of 71.4%.

Pental’s dividend policy is to distribute at least 60% of the Company’s net profit after tax to shareholders, subject to the

Board’s overall discretion on dividend payments.

Environmental regulations

The Shepparton manufacturing site is subject to various pieces of environmental legislation. Licences and Agreements relevant to the environmental performance of its operations are currently held with Goulbourn Valley.

Pental proactively monitors the amount of trade waste discharge from the site and in recent years significantly changed it manufacturing equipment and processes to minimise trade waste. Whilst there have been some minor trade waste non-compliances, Pental continues to be focussed on working with Goulburn Valley Water to implement sustainable solutions.

Environmental performance is reported to the Site Management Group and the Board as required.

Shares under option or issued on exercise of options

There were no unissued shares under options as at the date of this report.

Indemnification of officers and auditors

During the financial year, the company paid a premium in respect of a contract insuring the directors of the company (as

named above), the company secretary, Oliver Carton, and all executive officers of the company and of any related body

corporate against a liability incurred by such a director, secretary or executive officer to the extent permitted by the

Corporations Act 2001. The contract of insurance prohibits disclosure of the nature of the liability and the amount of the

premium.

The company has not otherwise, during or since the end of the financial year, except to the extent permitted by law,

indemnified or agreed to indemnify an officer or auditor of the company or of any related body corporate against a liability

incurred as such an officer or auditor.

Directors’ meetings

The following table sets out the number of directors’ meetings (including meetings of committees of directors) held during the

financial year and the number of meetings attended by each director (while they were a director or committee member).

During the financial year, 11 Board, 4 Audit Committee and 2 Remuneration Committee meetings were held.

Board of

Directors

Audit

Committee Remuneration

Committee

Directors Eligible to

Attend Attended Eligible to

Attend Attended Eligible to

Attend Attended

Peter Robinson 11 11 4 4 2 2

Mel Sutton 11 11 4 3 2 1

John Rishworth 11 11 4 3 2 2

John Etherington 11 11 4 4 2 2

Kimberlee Wells 11 10 - - 2 1

For

per

sona

l use

onl

y

Pental Limited

Directors’ report

22

Proceedings against the Company

On 13 December 2016 ACCC commenced proceedings concerning claims made by Pental on the packaging for its White King Bathroom Flushable Wipes and on its websites that the wipes were flushable and/or that they disintegrate like toilet paper, which the ACCC alleges to be false, misleading or deceptive conduct.

The product packaging was inherited by Pental from a major international company with a long history of selling consumer products. Accordingly, Pental held the belief that the labelling and packaging of the White King Bathroom Wipes were in conformity with all relevant legal requirements.

In September 2014, Pental undertook its own review of the White King Bathroom Flushable Wipes packaging and removed the claims relating to disintegration like toilet paper. This was approximately 18 months prior to any ACCC investigation or any controversy about 'flushability' claims.

Pental continued to sell the biodegradable White King Bathroom Wipes as 'flushable' products for a period of time. There is currently no legal standard for flushability and therefore there is an inherent degree of ambiguity about the meaning of that term, and that the product is biodegradable.

Nevertheless, in response to the ACCC's concerns, Pental took action to remove the word 'flushable' from the White King Bathroom Wipes packaging and its websites in or around July 2016.

Pental takes its obligations under the Competition and Consumer Act 2010 (Cth) seriously. Pental has co-operated with the ACCC since it commenced an investigation in February 2016.

Pental is therefore disappointed that the ACCC has decided to issue proceedings despite Pental's proactive approach in removing the claims of concern to the ACCC and the fact that other larger multinational companies continue to sell similar products labelled as ‘flushable’ but are not subject to the same proceedings.

There are no other proceedings being brought against the company.

Non-audit services

Details of amounts paid or payable to the auditor for non-audit services provided during the year by the auditor are outlined in

Note 30 to the financial statements.

The directors are satisfied that the provision of non-audit services during the year, by the auditor (or by another person or firm

on the auditor’s behalf) is compatible with the general standard of independence for auditors imposed by the Corporations Act

2001.

The directors are of the opinion that the services as disclosed in Note 30 to the financial statements do not compromise the

external auditor’s independence, based on advice received from the Audit Committee, for the following reasons:

all non-audit services have been reviewed and approved to ensure that they do not impact the integrity and

objectivity of the auditor, and

none of the services undermine the general principles relating to auditor independence as set out in Code of

Conduct APES 110 Code of Ethics for Professional Accountants issued by the Accounting Professional & Ethical

Standards Board, including reviewing or auditing the auditor’s own work, acting in a management or decision-

making capacity for the company, acting as advocate for the company or jointly sharing economic risks and rewards.

Auditor’s independence declaration

The auditor’s independence declaration is included on page 28 of the annual report.

Rounding off of amounts

The Company is a company of the kind referred to in ASIC Class Order 98/0100, dated 10 July 1998, and in accordance with that Class Order amounts in the directors’ report and the financial report are rounded off to the nearest thousand dollars, unless otherwise indicated.

For

per

sona

l use

onl

y

Pental Limited

Directors’ report

23

Remuneration report - audited

This remuneration report details the nature and amount of remuneration for each director and senior management personnel

of Pental Limited.

The directors and other members of key management personnel of the Group during the year were:

Peter Robinson Non-executive Independent Chairman

Mel Sutton Non-executive Vice-Chairman

John Rishworth Non-executive Independent Director

John Etherington Non-executive Independent Director

Kimberlee Wells Non-executive Independent Director

Charlie McLeish Chief Executive Officer

Albert Zago Chief Financial Officer

Remuneration Policy

The remuneration policy of Pental Limited has been designed to align director and executive objectives with shareholder and business objectives by providing a fixed remuneration component and offering specific short-term and long-term incentives based upon key performance areas affecting the Group’s financial results. The board of Pental Limited believes the remuneration policy to be appropriate and effective in its ability to attract and retain the best executives and directors to run and manage the Group, as well as create goal congruence between directors, executives and shareholders. The Board’s policy for determining the nature and amount of remuneration for board members and senior executives of the Group is as follows: The remuneration policy, setting the terms and conditions for the executive directors and other senior executives, was developed and approved by the Board. Executive packages are reviewed annually by reference to the Group’s performance, executive performance and comparable information from industry sectors and other listed companies in similar industries. The performance of executives is measured regularly against agreed criteria and is based predominantly on the forecast growth of the Group’s profits and shareholders’ value. All bonuses and incentives are linked to predetermined operational and financial performance criteria. Executives are also entitled to participate in a performance rights plan. The directors and executives receive a superannuation guarantee contribution required by the law, and do not receive any other retirement benefits. Some individuals, however, may choose to sacrifice part of their salary to increase payments towards superannuation. The Board policy is to remunerate non-executive directors at market rates for comparable companies for time, commitment and responsibilities. The Board determines payments to the non-executive directors and reviews their remuneration annually, based on market practice, duties and accountability. The maximum aggregate amount of fees that can be paid to non-executive directors is subject to approval by shareholders at the Annual General Meeting. The maximum aggregate amount of fees that can be paid to non-executive directors as per last approval is $0.750 million. Fees for non-executive directors are not linked to the performance of the Group. No shares or options have been issued to non-executive directors, under the performance rights plan or an option scheme, within the last five years.

Key terms of employment contracts

Mr Charlie McLeish is employed by the Group under an ongoing contract. The period of notice required by either party to terminate the contract is twelve months without cause. Mr McLeish is entitled to receive a maximum yearly bonus of 35 per cent of his base salary plus superannuation. He is also entitled to participate in the Executive Performance Rights Plan (Rights Plan) as a long-term incentive, which is aligned to the Company’s performance.

Mr Albert Zago is employed by the Group under an ongoing contract which may be terminated on three months’ notice by either the Company or the executive. Mr Zago is entitled to receive a maximum yearly bonus of 30 per cent of his base salary plus superannuation. Mr Zago is also entitled to participate in the executive Rights Plan.