pension systems during the financial and economic crisis edward whitehouse social policy division,...

Post on 22-Dec-2015

215 views

TRANSCRIPT

Pension systems during thefinancial and economic crisis

Edward WhitehouseSocial Policy division, OECD

Pension funds’ real returns

-30 -25 -20 -15 -10 -5 0

Czech Republic

Germany

Slovak Republic

Sweden

Poland

United Kingdom

Finland

Netherlands

Hungary

United States

Lithuania

Bulgaria

Real investment return, 2008

Source: OECD

-40 -30 -20 -10 0

0

25

50

75

Real investmentreturn in 2008 (%)

Equities,% of total portfolio

United States

Mexico

Czech RSlovak R

Hungary

Iceland

Australia

Spain

Germany

Netherlands

Poland

Norway

Portugal Switzerland

Denmark, Sweden

Austria

United Kingdom

Japan

Explaining differences in 2008 returnsIreland

Canada

Economic crisis

-5

-4

-3

-2

-1

0

1

2008 2009 2010

Falling output

Change in GDP(%)

OECD 30

Economic crisis

-5

-4

-3

-2

-1

0

1

2008 2009 20100

2.5

5

7.5

10

12.5

2009 2010 2011

Euro zone

OECD 30

Falling output

Change in GDP(%)

Unemployment(% of labour force)

Rising unemployment

-

-

OECD 30

Economic crisis

-5

-4

-3

-2

-1

0

1

2008 2009 20100

2.5

5

7.5

10

12.5

2009 2010 2011

Euro zone

OECD 30

Falling output

Change in GDP(%)

Unemployment(% of labour force)

Rising unemployment

Growing budget deficits

-10

-7.5

-5

-2.5

0

2007 2008 2009 2010

Budget balance(% of GDP)

Source: OECD

OECD 30 OECD 30

Impact on pensions

• Financial crisis– Defined-contribution plans– Private, defined-benefit plans– Public pension reserves

• Economic crisis– Countries with automatic adjustments

• But no country or pension scheme is immune

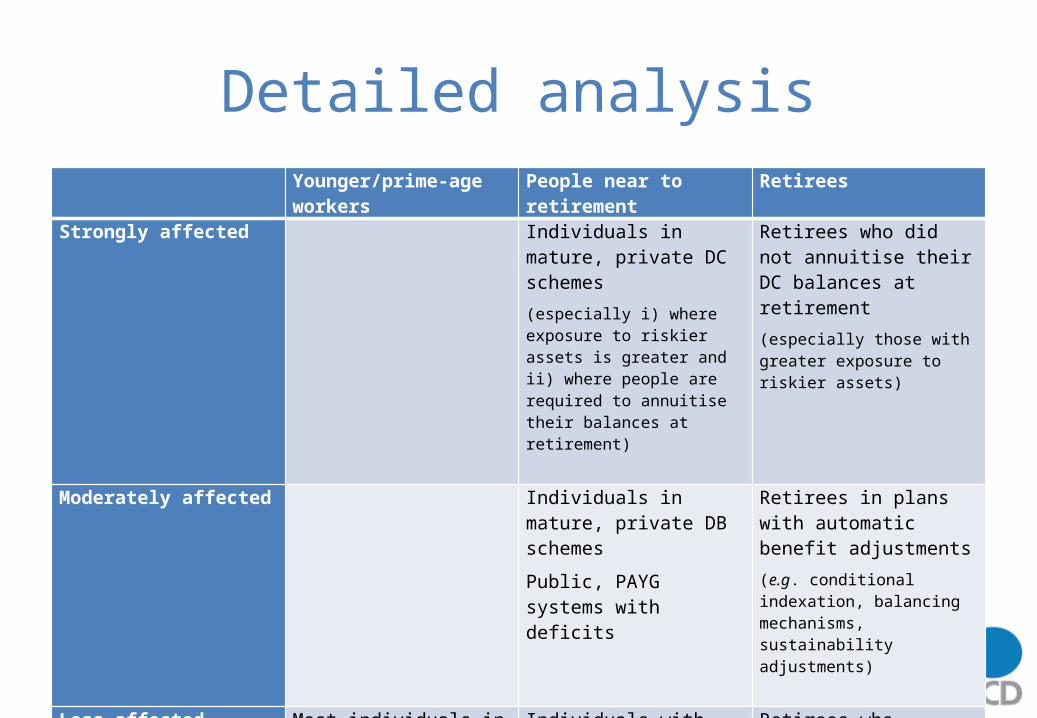

Detailed analysisYounger/prime-age workers People near to retirement Retirees

Strongly affected Individuals in mature, private DC schemes (especially i) where exposure to riskier assets is greater and ii) where people are required to annuitise their balances at retirement)

Retirees who did not annuitise their DC balances at retirement (especially those with greater exposure to riskier assets)

Moderately affected Individuals in mature, private DB schemesPublic, PAYG systems with deficits

Retirees in plans with automatic benefit adjustments (e.g. conditional indexation, balancing mechanisms, sustainability adjustments)

Less affected Most individuals in this group

Individuals with recently established private DC schemes

Retirees who annuitised DC balances before the crisis Most retirees with DB private pensions or public, PAYG benefits

Role of private pensions for workers

0 25 50 75 100

Czech Republic

Norway

New Zealand

Germany

Belgium

Switzerland

Hungary

Canada

Ireland

Sweden

United States

Poland

Australia

United Kingdom

Slovak Republic

Netherlands

Denmark

Mexico

Iceland

Mandatory defined contribution

Voluntary defined contribution

Mandatory defined benefit

Private pensions

per cent of totalretirement-income package

Capital income of today’s pensioners

0 10 20 30 40 50

Czech RepublicSlovak Republic

PolandAustria

HungaryItaly

SpainPortugalBelgiumFrance

LuxembourgGreeceJapan

IcelandGermanySweden

New ZealandNorwayIreland

DenmarkUnited Kingdom

AustraliaUnited StatesNetherlands

Canada

Percentage of total non-workretirement income from capital

Pension for full-career low earner

0 5 10 15 20 25 30 35 40 45 50

Germany

United States

United Kingdom

Estonia

Latvia

Lithuania

Slovenia

Bulgaria

Finland

Sweden

Czech Republic

Romania

Netherlands

Pension level(% of economy-wide average earnings)

5 years’ unemployment/early retirement

Pension level(% of economy-wide average earnings)

0 5 10 15 20 25 30 35 40 45 50

Germany

United States

United Kingdom

Estonia

Latvia

Lithuania

Slovenia

Bulgaria

Finland

Sweden

Czech Republic

Romania

Netherlands

Policy responses: what to do

• Old-age payments as part of economic-stimulus packages (e.g. Australia, Greece, UK)

• Strengthen safety-nets (e.g. Finland, France, Spain)

• Ensure investment options for DC schemes with default switch to less risky assets with age (e.g. Poland)

• Temporarily relax regulations for private DB schemes (e.g. Netherlands)

• Flexible timing of annuity purchase (e.g. Ireland)

• Improve governance and risk-management of pension funds and focus on financial education

Investing for the long term

0

2.5

5

7.5

10

12.5

Bonds Conservative Balanced Risky Equities

90%

80%

70%

60%

Median

40%

30%

20%

10%

Simulated annual real rate of return(%)

Policy responses: to do or not to do?• Temporary access for individuals to DC accounts (e.g.

Australia, Iceland, US)– But risk of lack of resources in retirement

• Temporary reduction in contribution by employers or governments (e.g. US –corporate, Estonia, Lativa, Lithuania)– But again risk of lack of resources in retirement

• Bail out of DC accounts (e.g. Israel)– But problems of cost, equity, moral hazard

• Guarantees for DC accounts (e.g. Switzerland, Slovakia)– What level? Who pays?

• Use public pension reserves for crisis mitigation (e.g. Ireland, Norway)

Policy responses: what not to do

• Resort to early retirement or other benefits (disability, unemployment)– negative and persistent effect on labour market

• Indeed, workers may wish to work longer in countries with more mature DC schemes (e.g. Australia, US)

• And other countries proposing to increase pension ages in response to crisis (e.g. Finland, Hungary, Netherlands)

• Abandon long-term goals for short-term expediency (e.g. Argentina, Slovak Republic)

Conclusions

• Financial crisis focused attention on investment risk and pensions– But all pension systems subject to risks

• Financial and economic crisis highlights and exacerbates the problems of pension systems

• Long-term strategy should remain diversification and balanced old-age provision