pengumuman equity research pt multipolar tbk. (mlpl

TRANSCRIPT

PENGUMUMAN

Equity Research PT Multipolar Tbk. (MLPL)

(Tercatat Di Papan : Pengembangan) No.Peng-ER-00011/BEI.PPJ/03-2012

(dapat dilihat di laman: http://www.idx.co.id) PT Bursa Efek Indonesia pada tanggal 21 Maret 2012 telah menerima surat melalui email dari PT Pemeringkat Efek Indonesia dengan No. 485/PEF-DIR/IiI/2012 tanggal 19 Maret 2012 mengenai Publikasi Laporan Penilaian Target Harga Referensi Saham PT Multipolar Tbk. sebagaimana terlampir (32 lembar). Demikian untuk diketahui.

21 Maret 2012

Umi Kulsum Andre P.J. Toelle Kepala Divisi Penilaian Perusahaan Sektor Jasa Kepala Divisi Perdagangan Saham Tembusan: 1. Yth. Ketua Badan Pengawas Pasar Modal dan LK; 2. Yth. Kepala Biro Transaksi dan Lembaga Efek Bapepam dan LK; 3. Yth. Kepala Biro PKP Sektor Jasa Bapepam dan LK; 4. Yth. Pengurus Pusat Referensi Pasar Modal; 5. Yth. Direksi PT Multipolar Tbk.

psu_MLPL_er_20120321_11

'"PEFINDO CREDIT RATING INDONESIA

485 /PEF-DIR/III/ 2012

Jakarta, 19 Maret 2012

Kepada Yth.1. PT Multipolar Tbk

Menara Matahari - Lippo life Lt. 16Boulevard Palem Raya 7Karawaci 1100Tangerang 15811

u.p. Bapak Reynold Ong , DirekturBapak Chrys R.N. Sinulingga, Corporate Secretary

2. PT Bursa Efek IndonesiaGedung Bursa Efek IndonesiaJI. Jend. Sudirman Kav 52-53Jakarta Selatan, 12190

u.p. Bapak Ito Warsito, Direktur UtamaBapak Eddy Sugito, Direktur Penilaian Perusahaan

Perihal: Publikasi Laporan Penilaian Target Harga Referensi Saham PT Multipolar Tbk.

Dengan hormat,

Sehubungan dengan penugasan yang kami peroleh untuk melakukan Penilaian Target HargaReferensi Saham, dengan ini kami sampaikan hasil penilaian kami atas saham PT Multipolar Tbk(MLPL) dalam versi Bahasa Indonesia dan Bahasa Inggris.

Apabila masih ada hal-hal yang memerlukan penjelasan lebih lanjut, mohon agar menghubungi kami.Atas perhatian dan kerjasamanya, kami ucapkan terima kasih.

Hormat kami,

"

se Rizalirektur

Ronald T. Andi Kasim, CFADirektur Utama

Tembusan : Ibu Umi Kulsum, Kepala Divisi Pencatatan Sektor Jasa, PT Bursa Efek Indonesia

/ww

PT. Pemeringkat Efek IndonesiaPanin Tower Senayan City, 17th FloorJI. Asia Afrika Lot. 19, Jakarta 10270, INDONESIAPhone: (62-21) 7278 2380 • Fax: (62-21) 7278 2370

Halaman 1 dari 16 halaman

Kontak: Equity & Index Valuation Division Phone: (6221) 7278 2380 [email protected] “Pernyataan disclaimer pada halaman akhir

merupakan bagian yang tidak terpisahkan dari

dokumen ini”

www.pefindo.com

Multipolar, Tbk Laporan Utama

Equity Valuation

19 Maret 2012

Target Harga

Terendah Tertinggi 360 385

Grup Retail & IT

Property

Kinerja Saham

Source : Bloomberg

Informasi Saham Rp

Kode Saham MLPL

Harga saham per 16 Maret 2012 136

Harga Tertinggi 52 Minggu Terakhir 275

Harga Terendah 52 Minggu Terakhir 124

Kapitalisasi Pasar Tertinggi 52 Minggu

(miliar) 2.396

Kapitalisasi Pasar Terendah 52 Minggu

(miliar) 958

Market Value Added & Market Risk

Source : Bloomberg, Pefindo Equity & Index Valuation Division

Pemegang Saham * (%)

Cyport Limited 26,95

Grandhill Asia Limited 5,05

HSBC-Fund Services 5,38

Public (each below 5%) 62,62

Catt: Per 31 Desember 2011

Menjanjikan untuk Menjadi Pemain Terbesar dalam

Industri Ritel

PT Multipolar Tbk (“MLPL”) didirikan pada tahun 1975 sebagai peritel elektronik yang berubah menjadi penyedia solusi informasi dan teknologi (IT). Di tahun 1986, MLPL menjadi mitra usaha IBM yang pertama di Indonesia. Walaupun MLPL memulai usahanya sebagai peritel elektronik,

saat ini MLPL juga fokus dalam mengembangkan bisnisnya untuk menjadi

pemain besar dalam industri ritel melalui kepemilikannya pada PT Matahari Putra Prima Tbk (MPPA) dan Robbinz Department Store (“RDS”) di Cina. Saat ini, MLPL memiliki jaringan ritel yang sangat luas yang tersebar di Indonesia dan Cina. Di Indonesia, MLPL melalui MPPA mengoperasikan 63 Hypermart, 24 Foodmart dan 63 Boston HBC’s.

Sedangkan di Cina, MLPL telah membuka 6 toko ritel yang terdiri dari 2 Hypermart di Tianjin dan Suzhou dan 4 Department Store di Tianjin, Chengdu, Yangzhou, dan Suzhou. Selain itu, MLPL masih akan terus melakukan pengembangan pada lini bisnis IT dan Multimedianya dan terus mencari peluang investasi lainnya untuk mencapai portfolio bisnis yang lebih strategis.

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 2 dari 16 halaman

Perkembangan Perekonomian Indonesia dan Cina: Permintaan Domestik Masih Akan Mendukung Pertumbuhan Ekonomi

Pertumbuhan perekonomian dunia di tahun 2012 masih akan diperkuat oleh pertumbuhan yang dinamis di negara-negara berkembang dan negara maju yang didukung oleh permintan domestik mereka. Perekonomian

negara berkembang diperkirakan akan tumbuh sebesar 5,1% YoY di tahun 2011, lebih rendah dari 6,4% YoY di tahun 2010, sedangkan perekonomian Indonesia di tahun 2012 diperkirakan akan tumbuh sebesar 6,2% YoY sedikit lebih rendah dari pertumbuhan tahun 2011 yaitu sebesar 6,5% YoY. Pertumbuhan ekonomi Cina masih akan tinggi karena masih kuatnya permintaan konsumen. Perekonomian Cina diperkirakan akan tumbuh sebesar 8,7% YoY di tahun 2012, lebih rendah dari pertumbuhan tahun

2011 yaitu sebesar 9,5% YoY. Masih tingginya proyeksi pertumbuhan perekonomian kedua negara juga tergambar pada outlook industri ritel yang memiliki kaitan yang sangat erat dengan permintaan konsumen, pendapatan per kapita dan daya beli masyarakat. Industri ritel pada kedua negara diestimasikan akan tumbuh masing-masing sebesar 20% dan 13,2% di Indonesia dan Cina.

Kinerja yang Lebih Baik selama 9M2011 Selain rugi bersih dari perusahaan asosiasi pada sembilan bulan pertama 2011, MLPL menunjukkan kinerja yang lebih baik dibandingkan dengan periode yang sama tahun 2010. Pada lini atas, pendapatan konsolidasi MLPL meningkat 7,3% YoY menjadi Rp 7,6 triliun dari Rp 7,0 triliun di 9M2010. Peningkatan pendapatan pada periode ini berasal dari unit usaha ritel dan distribusi yang didukung oleh pendapatan MPPA. Selama 9M2011,

pendapatan dari unit bisnis ritel meningkat sebesar 0,63% YoY menjadi Rp 6,6 triliun dan memberikan kontribusi sekitar 88% terhadap pendapatan konsolidasi MLPL. Sementara, pendapatan MLPL dari bisnis TI tumbuh secara signifikan sebesar 115% YoY menjadi Rp 833 miliar dari Rp 388 miliar di 9M2010. Sedangkan, pada tingkat operasi, MLPL berhasil membukukan laba usaha positif sebesar Rp 843 juta, meningkat 102% YoY dari minus Rp 41 miliar di 9M2010.

Berekspansi Untuk Pertumbuhan Berkelanjutan

Untuk tahun 2012, MLPL telah menganggarkan dana sebesar USD 90 juta untuk pengembangan usaha. Sebagai kontributor utama pendapatannya, MLPL terus mengembangakan bisnis ritel dengan membuka beberapa toko baru. Selain toko ritel MPPA di Indonesia yang telah membuka 12 toko ritel

baru di tahun 2011, pada waktu yang sama, MLPL juga membuka 3 toko ritel di Cina yang terdiri atas 2 Hypermart di Tianjin dan Suzhou dan 1 gerai Robbinz di Suzhou. Sementara itu, di tahun 2012, MLPL berencana untuk membuka sekitar 10 toko baru di Cina yang diproyeksikan akan membutuhkan dana sekitar USD 60 juta, sedangkan di Indonesia anak perusahaannya (MPPA) juga akan membuka sekitar 15 gerai Hypermart selama tahun 2012. Di sisi lain, lini bisnis IT sedang mengembangkan

program cloud computing (komputasi awan) yang direncanakan akan diluncurkan pada tahun 2013. Di tahun ini, MLPL akan membangun pusat data untuk mendukung program cloud computing tersebut dan diperkirakan akan menghabiskan belanja modal sekitar USD 30 juta. Dengan belanja modal tersebut, kami memproyeksikan pendapatan MLPL akan tumbuh dengan rata-rata CAGR sebesar 23,0% selama periode 2010-2014.

Prospek Usaha

Sejalan dengan pertumbuhan industri ritel di Indonesia dan Cina yang diperkirakan akan terus tumbuh masing-masing sebesar 20% dan 13,2%, prospek bisnis ritel yang merupakan kontributor pendapatan utama MLPL akan tetap aman, didukung oleh jaringan ritel yang luas dan tersebar dihampir semua provinsi di Indonesia dan di beberapa kota-kota besar di Cina. Kami memproyeksikan pendapatan MLPL dari bisnis ritel akan tumbuh

sebesar 17,5%YoY di tahun 2012 dan tumbuh dengan rata-rata CAGR sebesar 27,1% selama tahun 2011-2015. Pada sisi lain, tahun 2012 akan menjadi tahun yang penting bagi industri teknologi, informasi dan komunikasi (TIK) baik secara global maupun di Asia. Khusus di Indonesia, Business Monitor International (BMI) memprediksikan industri TIK akan tumbuh sebesar 18% per tahun dalam empat tahun ke depan. Berbagai

PARAMETER INVESTASI

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 3 dari 16 halaman

tren yang menunjukkan daya tarik industri ini dalam beberapa tahun terakhir yang telah teruji dan akan menjadi fitur utama dari industri TIK dimasa yang akan datang, sebagai contoh komputasi awan. Sejalan dengan ekspansi dalam program komputasi awan, MLPL akan merasakan manisnya

bisnis ini pada tahun 2013. Namun demikian, industri TIK di Indonesia masih dihadapkan pada minimnya infrastruktur dan kesenjangan digital

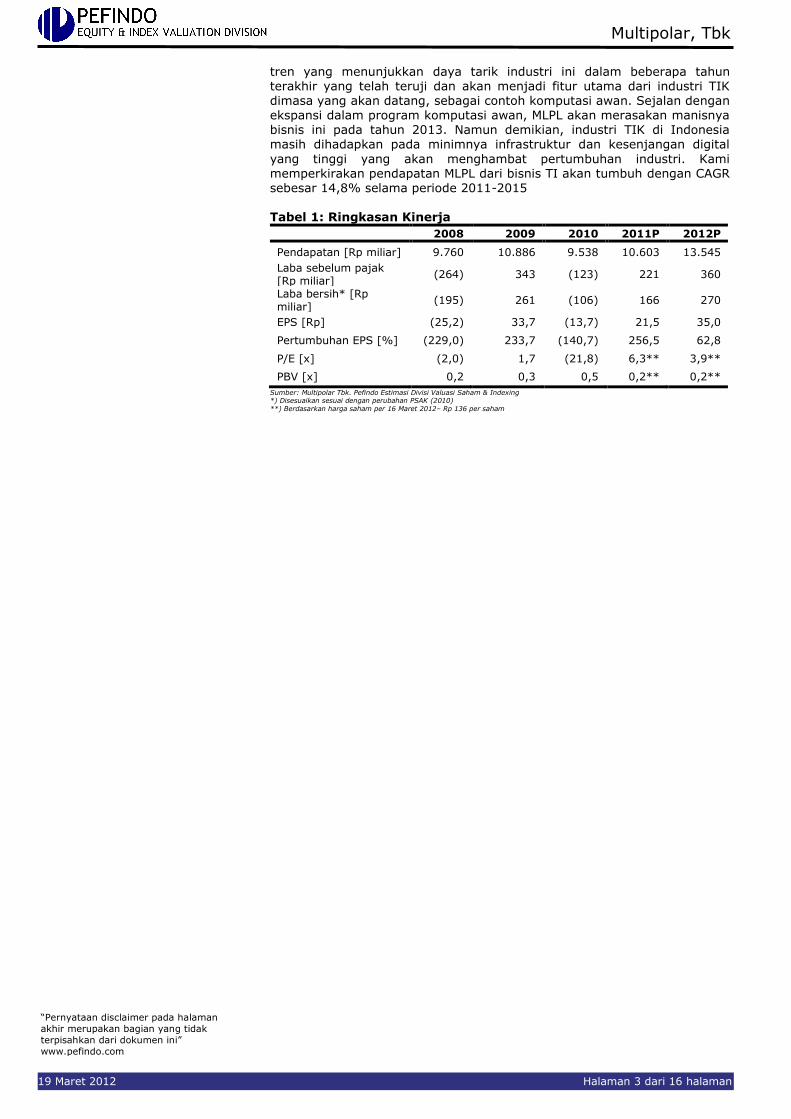

yang tinggi yang akan menghambat pertumbuhan industri. Kami memperkirakan pendapatan MLPL dari bisnis TI akan tumbuh dengan CAGR sebesar 14,8% selama periode 2011-2015 Tabel 1: Ringkasan Kinerja

2008 2009 2010 2011P 2012P

Pendapatan [Rp miliar] 9.760 10.886 9.538 10.603 13.545

Laba sebelum pajak [Rp miliar]

(264) 343 (123) 221 360

Laba bersih* [Rp miliar]

(195) 261 (106) 166 270

EPS [Rp] (25,2) 33,7 (13,7) 21,5 35,0

Pertumbuhan EPS [%] (229,0) 233,7 (140,7) 256,5 62,8

P/E [x] (2,0) 1,7 (21,8) 6,3** 3,9**

PBV [x] 0,2 0,3 0,5 0,2** 0,2**

Sumber: Multipolar Tbk. Pefindo Estimasi Divisi Valuasi Saham & Indexing *) Disesuaikan sesuai dengan perubahan PSAK (2010) **) Berdasarkan harga saham per 16 Maret 2012– Rp 136 per saham

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 4 dari 16 halaman

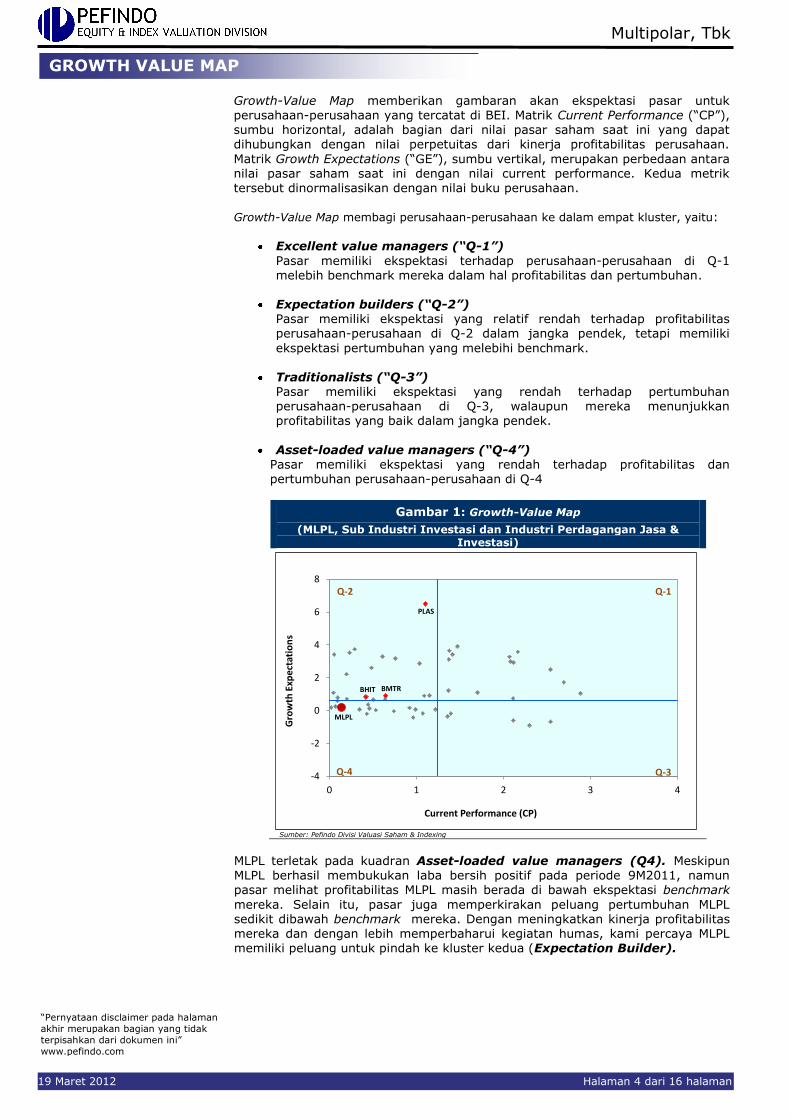

Growth-Value Map memberikan gambaran akan ekspektasi pasar untuk perusahaan-perusahaan yang tercatat di BEI. Matrik Current Performance (“CP”),

sumbu horizontal, adalah bagian dari nilai pasar saham saat ini yang dapat dihubungkan dengan nilai perpetuitas dari kinerja profitabilitas perusahaan.

Matrik Growth Expectations (“GE”), sumbu vertikal, merupakan perbedaan antara nilai pasar saham saat ini dengan nilai current performance. Kedua metrik tersebut dinormalisasikan dengan nilai buku perusahaan. Growth-Value Map membagi perusahaan-perusahaan ke dalam empat kluster, yaitu:

Excellent value managers (“Q-1”)

Pasar memiliki ekspektasi terhadap perusahaan-perusahaan di Q-1 melebih benchmark mereka dalam hal profitabilitas dan pertumbuhan.

Expectation builders (“Q-2”) Pasar memiliki ekspektasi yang relatif rendah terhadap profitabilitas perusahaan-perusahaan di Q-2 dalam jangka pendek, tetapi memiliki

ekspektasi pertumbuhan yang melebihi benchmark.

Traditionalists (“Q-3”)

Pasar memiliki ekspektasi yang rendah terhadap pertumbuhan perusahaan-perusahaan di Q-3, walaupun mereka menunjukkan profitabilitas yang baik dalam jangka pendek.

Asset-loaded value managers (“Q-4”) Pasar memiliki ekspektasi yang rendah terhadap profitabilitas dan pertumbuhan perusahaan-perusahaan di Q-4

Gambar 1: Growth-Value Map

(MLPL, Sub Industri Investasi dan Industri Perdagangan Jasa & Investasi)

-4

-2

0

2

4

6

8

0 1 2 3 4

Gro

wth

Exp

ecta

tio

ns

Current Performance (CP)

BMTR

PLAS

Q-1

Q-3

Q-2

Q-4

BHIT

MLPL

Sumber: Pefindo Divisi Valuasi Saham & Indexing

MLPL terletak pada kuadran Asset-loaded value managers (Q4). Meskipun MLPL berhasil membukukan laba bersih positif pada periode 9M2011, namun pasar melihat profitabilitas MLPL masih berada di bawah ekspektasi benchmark

mereka. Selain itu, pasar juga memperkirakan peluang pertumbuhan MLPL sedikit dibawah benchmark mereka. Dengan meningkatkan kinerja profitabilitas mereka dan dengan lebih memperbaharui kegiatan humas, kami percaya MLPL memiliki peluang untuk pindah ke kluster kedua (Expectation Builder).

GROWTH VALUE MAP

Multipolar, Tbk

February 23rd, 2012 Page 5 of 15 pages

Outlook Perekonomian Dunia: Masih Akan Didukung oleh Pertumbuhan yang Lebih Kuat di Negara-Negara Berkembang

Berdasarkan riset yang dilakukan oleh The Conference Board, perekonomian global diprediksikan akan tumbuh sebesar 3,2% YoY di tahun 2012, melemah dari pertumbuhan di tahun sebelumnya yaitu 3,9% YoY, tapi pertumbuhan ekonomi tersebut diperkirakan akan berakselerasi hingga 3,5% YoY selama periode 2013-2016. Tingginya tingkat pengangguran dan melemahnya tingkat konsumsi di negara-negara maju adalah penyebab turunnya revisi proyeksi pertumbuhan perekonomian dunia dari proyeksi sebelumnya. Meskipun

mengalami penurunan, pertumbuhan perekonomian di tahun 2012, masih akan didukung oleh pertumbuhan yang lebih kuat di negara-negara berkembang walaupun momentumnya berkurang sebagai imbas dari krisis di Eropa dan Amerika.

Negara-negara maju akan menghadapi penurunan permintaan eksternal di tahun 2012, tapi pada sebagian besar negara-negara berkembang, mereka bisa

bergantung kepada permintaan domestik untuk mendorong pertumbuhan ekonomi mereka hingga perkonomian dunia menjadi lebih sehat. Tapi bagi negara-negara berkembang yang bergantung terhadap permintaan eksternal,

akan merasakan dampak dari penurunan pasar global. Sejalan dengan penurunan perekonomian secara keseluruhan, perekonomian negara-negara berkembang diperkirakan hanya akan tumbuh sebesar 5,1% YoY di tahun 2012 turun dari 6,4% YoY di tahun 2011. Penyusutan ini merupakan akibat dari negara

berkembang yang akan mengalami pertumbuhan ekspor yang lebih lambat, dan beberapa karena mungkin sudah tumbuh di atas tren. Namun, mereka umumnya memiliki lebih banyak fleksibilitas dalam kebijakan fiskal dari sebagian besar negara-negara maju yang mungkin menguntungkan mereka dalam bentuk pertumbuhan yang lebih stabil.

Tabel 2: Pertumbuhan Perekonomian Global

Negara 2011E 2012F

US

EU-15

Jepang

Negara Maju Lainnya

Negara Ekonomi Maju

1,5

1,5

-0,5

3,3

1,6

1,1

1,1

0,7

2,5

1,3

Cina India

Negara berkembang Asia lainnya

Amerika Latin

Timur Tengah

Afrika

Eropa Tengah & Timur

Rusia dan negara-negara CIS

Emerging Market and Developing Economies

9,5 7,8

5,1

4,5

4,3

4,4

4,0

4,6

6,4

8,7 7,4

2,8

2,9

2,3

2,4

2,1

2,8

5,1

Dunia 3,9 3,2 Sumber: The Conference Board Economic Outlook, November 2011; Pefindo Divisi Valuasi Saham & Indexing

Permintaan Domestik Masih Menjadi Mesin Utama Pertumbuhan Ekonomi Indonesia dan Cina di Tahun 2012 Memburuknya perekonomian global mungkin akan menghambat pertumbuhan

perekonomian Cina dan Indonesia pada tahun 2012. Pemerintah Cina terus mengambil langkah-langkah untuk mencegah overheating dan untuk mengarahkan perekonomian menuju soft landing, sementara perpaduan antara langkah-langkah moneter dan kehati-hatian makro memperlambat pertumbuhan PDB, meskipun pertumbuhan PDB masih tetap kuat karena kuatnya permintaan konsumen.

Tabel 3: Indikator Perekonomian Indonesia

2008 2009 2010 2011

Pertumbuhan PDB (%, YoY)

Tingkat Inflasi (%, YoY)

Nilai tukar * (Rp/USD)

Tingkat SBI (%)

6,1

11,06

9.136

9,25

4,5

2,78

9.680

6,50

6,1

6,96

10.398

6,5

6,5

3,79

8.779

6,0 * Rata-rata nilai tengah Bank Indonesia Sumber: BPS, Bank Indonesia, diolah oleh Pefindo Divisi Valuasi Saham & Indexing

Sedangkan fundamental perekonomian Indonesia akan tetap kuat meskipun efek dari krisis global saat ini diprediksikan akan dapat memperlambat perekonomian global. Pefindo memperkirakan bahwa pertumbuhan ekonomi Indonesia akan sedikit turun ke 6,2% YoY pada tahun 2012, sementara di tahun 2011,

pertumbuhan ekonomi Indonesia tercatat sebesar 6,5% YoY. Penggerak utama perekonomian masih akan berasal dari kontribusi konsumsi swasta dengan

INFORMASI USAHA

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 6 dari 16 halaman

didukung oleh masih berlanjutnya optimisme konsumen, terjaganya tingkat inflasi, rendahnya tingkat suku bunga dan meningkatnya pendapatan per kapita. Pendapatan per kapita Indonesia mencapai USD 3.543 pada 2011, dan mungkin bisa mencapai USD 4.000 pada tahun 2012, dibandingkan dengan USD 3.000

pada tahun 2010. Sementara itu, realisasi investasi tahun 2011 mencapai Rp 251,3 triliun atau naik 20,5% dibandingkan dengan tahun 2010. Dengan

komposisi penduduk yang didominasi oleh penduduk usia produktif (sekitar 60%) dan meningkatnya persepsi internasional terhadap perkembangan perekonomian Indonesia yang tercermin dari masuknya Indonesia menjadi investment grade dari Fitch pada Desember 2011 dan oleh Moody`s pada Januari 2012, maka kami percaya bahwa Indonesia akan mampu mempertahankan pertumbuhan yang menguntungkan di tahun mendatang

Industri TIK akan Berkembang di Tahun 2012

Tahun 2012 akan menjadi tahun yang penting bagi Industri Teknologi, Informasi dan komunikasi (TIK) baik secara global maupun di Asia. Khusus di Indonesia, Business Monitor International (BMI) memprediksikan industri TIK akan tumbuh sebesar 18% per tahun dalam 4 tahun yang akan datang. Berbagai tren yang meningkatkan daya tarik industri ini dalam beberapa tahun terakhir telah diadaptasi dan akan menjadi fitur utama dalam industri TIK yang terus tumbuh,

seperti cloud computing (komputasi awan). Sementara itu, nilai industri TIK berdasarkan data dari Kementerian Komunikasi dan Informatika (Kemkominfo) telah mencapai Rp 350 triliun, meningkat 17% YoY dari Rp 300 triliun di tahun 2010. Pertumbuhan tersebut didorong oleh beberapa hal, antara lain penyebaran industri teknologi informasi, pasar yang semakin kompetitif, peningkatan penjualan hardware dan software dan penyebaran jasa teknologi informasi. Penjualan hardware seperti Telepon Seluler (Ponsel) dan komputer tumbuh

dengan rata-rata CAGR masing-masing sebesar 37,3% dan 27,9% selama periode 2008-2011, sedangkan penjualan software mencapai USD 599 juta di tahun 2011 dan diperkirakan akan tumbuh dengan CAGR sebesar 22% dalam lima tahun yang akan datang. Selain itu, industri TIK juga didongkrak oleh meningkatnya belanja pemerintah untuk teknologi informasi seperti program e-learning, e-KTP dan e-passport.

Namun demikian, industri TIK di Indonesia masih dihadapkan dengan masalah

masih kurangnya infrastruktur dan tingginya digital gap yang akan menekan pertumbuhan industri tersebut. Untuk mengatasi masalah tersebut, pemerintah

Indonesia di tahun 2012 telah menganggarkan sekitar Rp 3,2 triliun dalam draft anggaran pendapatan dan belanja Kementerian Komunikasi dan Informatika Republik Indonesia (Kemkominfo). Kemkominfo akan menggunakan dana tersebut untuk fokus dalam pembangunan infrastruktur telekomunikasi seperti

Palapa Ring sesuai dengan target pemerintah untuk meningkatkan penetrasi internet hingga 30% di tahun 2014.

Berawal sebagai Pengecer Elektronik dan Saat ini Telah Memiliki Beragam Portofolio Strategis PT Multipolar Tbk (“MLPL”) didirikan pada tahun 1975 sebagai sebuah perusahaan peritel elektronik dan saat ini MLPL telah bertransformasi menjadi sebuah penyedia solusi IT dan perusahaan investasi yang strategis. Per September 2011,

hampir 90% dari pendapatannya adalah berasal dari investasinya dalam berbagai industri seperti ritel, multimedia dan jasa. Pada industri ritel, MLPL merupakan pemegang saham mayoritas PT Matahari Putra Prima Tbk (MPPA) – operator hipermarket terbesar kedua di Indonesia- dan Congrex Limited – operator Robbinz Departement Store (RDS), sebuah Departement store yang terkenal di

Cina. Di dalam industri multimedia, MLPL melalui anak perusahaannya PT Reksa Puspita Karya memiliki sekitar 33,8% saham PT First Media Tbk (KLBV) –

pencetus pertama jasa broadband. MLPL juga merupakan pionir dalam industri jasa administrasi dan outsourcing melalui anak perusahaannya PT Multifiling Mitra Indonesia Tbk (MFMI) dan PT Visionet International.

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 7 dari 16 halaman

Gambar 2: Portfolio MLPL

Multipolar Tbk

Teknologi Informasi Ritel Jasa Multimedia

PT Matahari Putra Prima Tbk

Congrex Limited

PT Sharestar Indonesia

PT Surya Cipta Investama

PT Multifiling Mitra Indonesia Tbk

PT Visonet International

PT Reksa Puspita Karya

PT First Media Tbk

Sumber: PT Multipolar Tbk, Pefindo Divisi Valuasi Saham & Indexing

Pertumbuhan yang Kuat Pada Sektor Keuangan dan Telekomunikasi Menguntungkan Pendapatan Bisnis IT MLPL Secara sektoral, sumber pertumbuhan perekonomian Indonesia mulai seimbang sejalan dengan pertumbuhan sektor tradable yang menyumbangkan sekitar 46,5% dari total PDB naik 4,5% selama tahun 2011, sedangkan sektor non-

tradable tumbuh 8,3% YoY dibandingkan periode yang sama 8,2% YoY pada tahun lalu. Pertumbuhan sektor non-tradable, antara lain didukung oleh sektor keuangan dan sektor komunikasi. Selama tahun 2011, sektor keuangan tumbuh sebesar 6,8% YoY sementara sektor pengangkutan dan telekomunikasi tumbuh sebesar 10,7% YoY. Prospek industri keuangan akan tetap positif karena diuntungkan oleh meningkatnya rating Indonesia.

Kondisi ini merupakan indikasi positif bagi divisi bisnis IT MLPL, karena sebagian besar pendapatan divisi ini berasal dari kedua industri tersebut. Selama 9M2011, sektor perbankan/institusi keuangan berkontribusi sebesar 64% dari total pendapatan divisi IT, sedangkan sektor telekomunikasi masih merupakan

kontributor terbesar kedua pendapatan divisi IT yaitu sebesar 23%.

Gambar 3: Kontributor Pendapatan Divisi Usaha IT

Sumber: PT Multipolar Tbk, Pefindo Divisi Valuasi Saham & Indexing

Jaringan Distribusi Ritel yang Luas di Dalam Negeri dan di Luar Negeri Dipercayai Akan Mendongkrak Pendapatan MLPL dari Unit Usaha Ritel Salah satu investasi strategis MLPL adalah dalam industri ritel. Pada industri ini, MLPL memiliki mayoritas saham MPPA dan Congrex Limited. MPPA merupakan operator Hypermart, hipermaket terbesar kedua di Indonesia. Dalam 6 tahun

terakhir, jumlah outlet Hypermart telah tumbuh dengan rata-rata sebesar 23,0% per tahun. Di tahun 2005, jumlah outlet Hypermart adalah sebanyak 17 unit dan meningkat menjadi 59 unit di tahun 2011. Jaringan ritel ini tersebar di 32 kota di Indonesia. Hypermart didukung oleh 3 pusat distribusi (distribution center) yang memiliki peranan penting dalam mendistribusikan barang-barang ke Hypermart dan Foodmart. Gudang-gudang pusat distribusi ini berlokasi di Surabaya,

Balaraja dan Cibitung. Di tahun 2011, MPPA telah membuka sekitar 12 toko baru

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 8 dari 16 halaman

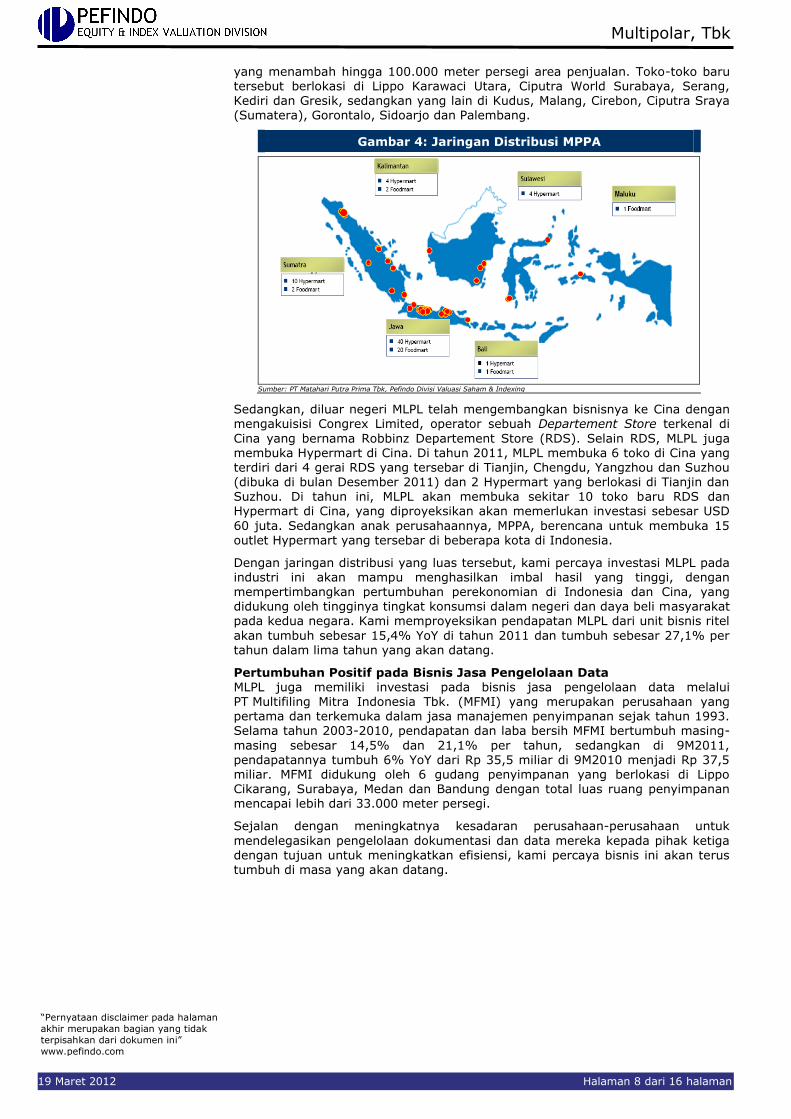

yang menambah hingga 100.000 meter persegi area penjualan. Toko-toko baru tersebut berlokasi di Lippo Karawaci Utara, Ciputra World Surabaya, Serang, Kediri dan Gresik, sedangkan yang lain di Kudus, Malang, Cirebon, Ciputra Sraya (Sumatera), Gorontalo, Sidoarjo dan Palembang.

Gambar 4: Jaringan Distribusi MPPA

Sumber: PT Matahari Putra Prima Tbk, Pefindo Divisi Valuasi Saham & Indexing

Sedangkan, diluar negeri MLPL telah mengembangkan bisnisnya ke Cina dengan mengakuisisi Congrex Limited, operator sebuah Departement Store terkenal di

Cina yang bernama Robbinz Departement Store (RDS). Selain RDS, MLPL juga membuka Hypermart di Cina. Di tahun 2011, MLPL membuka 6 toko di Cina yang terdiri dari 4 gerai RDS yang tersebar di Tianjin, Chengdu, Yangzhou dan Suzhou (dibuka di bulan Desember 2011) dan 2 Hypermart yang berlokasi di Tianjin dan Suzhou. Di tahun ini, MLPL akan membuka sekitar 10 toko baru RDS dan Hypermart di Cina, yang diproyeksikan akan memerlukan investasi sebesar USD

60 juta. Sedangkan anak perusahaannya, MPPA, berencana untuk membuka 15 outlet Hypermart yang tersebar di beberapa kota di Indonesia.

Dengan jaringan distribusi yang luas tersebut, kami percaya investasi MLPL pada industri ini akan mampu menghasilkan imbal hasil yang tinggi, dengan mempertimbangkan pertumbuhan perekonomian di Indonesia dan Cina, yang

didukung oleh tingginya tingkat konsumsi dalam negeri dan daya beli masyarakat pada kedua negara. Kami memproyeksikan pendapatan MLPL dari unit bisnis ritel

akan tumbuh sebesar 15,4% YoY di tahun 2011 dan tumbuh sebesar 27,1% per tahun dalam lima tahun yang akan datang.

Pertumbuhan Positif pada Bisnis Jasa Pengelolaan Data MLPL juga memiliki investasi pada bisnis jasa pengelolaan data melalui PT Multifiling Mitra Indonesia Tbk. (MFMI) yang merupakan perusahaan yang pertama dan terkemuka dalam jasa manajemen penyimpanan sejak tahun 1993. Selama tahun 2003-2010, pendapatan dan laba bersih MFMI bertumbuh masing-

masing sebesar 14,5% dan 21,1% per tahun, sedangkan di 9M2011, pendapatannya tumbuh 6% YoY dari Rp 35,5 miliar di 9M2010 menjadi Rp 37,5 miliar. MFMI didukung oleh 6 gudang penyimpanan yang berlokasi di Lippo Cikarang, Surabaya, Medan dan Bandung dengan total luas ruang penyimpanan mencapai lebih dari 33.000 meter persegi.

Sejalan dengan meningkatnya kesadaran perusahaan-perusahaan untuk

mendelegasikan pengelolaan dokumentasi dan data mereka kepada pihak ketiga

dengan tujuan untuk meningkatkan efisiensi, kami percaya bisnis ini akan terus tumbuh di masa yang akan datang.

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 9 dari 16 halaman

Gambar 5: Pusat Penyimpanan Pengelolaan Data

Sumber: Multipolar Tbk, Pefindo Divisi Valuasi Saham & Indexing

Pendapatan MLPL Bertumbuh Sejalan dengan Pertumbuhan Perekonomian Indonesia

MLPL menunjukkan kinerja yang lebih baik dalam 9 bulan pertama 2011 dibandingkan dengan periode yang sama pada tahun sebelumnya. Berdasarkan pertumbuhan tahunan, pendapatan MLPL meningkat 7,3% YoY dari Rp 7,0 triliun pada 9M2010 menjadi Rp 7,6 triliun di 9M2011. Peningkatan pendapatan MLPL selama periode ini merupakan satu dari sekian banyak dampak positif pertumbuhan perekonomian Indonesia selama tahun 2011 yang mencapai 6,5% YoY. Meningkatnya pendapatan perkapita yang mendukung daya beli

masyarakat telah meningkatkan pendapatan bisnis ritel (khususnya di Indonesia) yang merupakan kontributor terbesar pendapatan MLPL. Secara triwulanan,

pendapatan MLPL pada 3Q2011 tumbuh signifikan yaitu sebesar 14% q-o-q dari 2Q2011 menjadi Rp 2,8 triliun. Tingginya pendapatan ini dikarenakan meningkatnya pengeluaran masyarakat selama bulan Ramadhan dan sebelum hari Lebaran yang jatuh pada triwulan ini. Sedangkan untuk 4Q2011, kami memproyeksikan pendapatan MLPL akan tumbuh menjadi Rp 3,0 triliun, atau

naik 8,3% q-o-q atau tumbuh 17,7% YoY dari Rp 2,6 triliun pada 4Q2010. Selain dari unit usaha ritel, pendapatan MLPL pada periode ini juga didorong oleh pendapatan dari bisnis IT khususnya dari penjualan hardware seperti Ponsel dan komputer (PC).

Gambar 6 : Penjualan, Laba Kotor dan Pertumbuhan Penjualan (QoQ)

Sumber :PT Multipolar Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

KEUANGAN

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 10 dari 16 halaman

Pendapatan Bertumbuh di Semua Lini Bisnis Sebagai perusahaan investasi, MLPL menggantungkan pendapatannya kepada anak perusahaan yang mayoritas sahamnya dimiliki oleh MLPL, yang dikelompokkan berdasarkan kegiatan operasionalnya kedalam beberapa unit

usaha yaitu unit usaha ritel, unit usaha Informasi dan Teknologi (IT), unit usaha jasa dan multimedia (lain-lain). Setelah melepaskan Matahari Department Store

(MDS) di awal tahun 2010, unit usaha ritel masih mengalami pertumbuhan yang signifikan yang didukung oleh ekspansi agresif selama tahun 2011, seperti terlihat pada pendapatan di 9M2011, meningkat sebesar 58,2% menjadi Rp 6,7 triliun dari Rp Rp 4,2 triliun di 6M2011, atau secara tahunan tumbuh sebesar 0,63% YoY dari Rp 6,6 triliun di 9M2010. Selain bisnis ritel, divisi IT juga mencatatkan kinerja yang memuaskan dan tumbuh sebesar 115% YoY dari Rp 387,8 miliar di 9M2010 menjadi Rp Rp 833,4 miliar di 9M2011. Secara

kuartalan, bisnis IT tumbuh 14,5% q-o-q menjadi Rp 336 miliar dari Rp 293 miliar pada kuartal sebelumnya.

Gambar 7 : Penjualan MLPL Per Unit Usaha

Sumber: PT Multipolar Tbk, Pefindo Divisi Valuasi Saham & Indexing

Semakin Efisien dalam Kegiatan Operasional Pada lini operasi, MLPL mampu meningkatkan efisiensi dalam kegiatan operasionalnya dan membukukan laba operasi sebesar Rp 834 juta, naik 102% YoY dari minus Rp 41 miliar di 9M2010. Efisiensi biaya operasi khususnya

terjadi pada beban pemasaran yang turun menjadi Rp 381 juta, lebih rendah 34% YoY dari Rp 578 juta di 9M2010. Sedangkan beban umum dan administrasi

turun 12% YoY menjadi Rp 1,3 triliun dari beban umum dan administrasi pada 9M2010.

Gambar 8 : Laba Operasi MLPL

524,4545,1

15,9

-41,3

0,8

-100

0

100

200

300

400

500

600

2008 2009 2010 9M2010 9M2011

Dalam Rp miliar

Tumbuh Sebesar

102% YoY

Sumber: PT Multipolar Tbk, Pefindo Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 11 dari 16 halaman

Menargetkan Belanja Modal sebesar USD 90 juta untuk Pengembangan Usaha Saat ini, MLPL sedang mengerjakan 2 proyek ekspansi yaitu bisnis komputasi awan (cloud computing) dan bisnis ritel di Cina. Dengan berkerja sama dengan

HCL Industries, MLPL berencana untuk memasuki pasar komputasi awan sejak tahun 2010. Saat ini, MLPL masih dalam proses pengkajian untuk menentukan

lokasi terbaik untuk data center yang direncanakan akan dibangun di tengah tahun kedua tahun 2012 dan mulai beroperasi di tahun 2013. Untuk proyek ini, MLPL menganggarkan dana sebesar USD 30 juta atau setara dengan Rp 263,0 miliar (dengan asumsi nilai tukar Rupiah USD 1 = Rp 8.768 – rata-rata nilai tukar Rupiah selama tahun 2011-).

Selain itu, pengembangan usaha yang dilakukan MPPA di Indonesia selama tahun 2011, MLPL juga menginvestasikan belanja modal sekitar USD 60 juta atau sama

dengan Rp 526,1 miliar untuk membuka 3 outlet ritel di Cina yang diperkirakan akan menghasilkan return sebesar Rp 2 juta per meter persegi. Sedangkan di tahun 2012, MLPL berencana untuk membukan sekitar 10 outlet RDS dan Hypermart yang diproyeksikan juga akan menghabiskan dana sekitar USD 60 juta.

Gambar 9: Belanja Modal MLPL dan Perkembangan Toko Bisnis Ritelnya di

Indonesia dan Cina

Sumber: PT Multipolar Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

Dengan mempertimbangkan perkembangan komputasi awan di Indonesia yang diperkirakan akan tumbuh sebesar 54% di tahun 2014 dan masih kuatnya

permintaan domestik di Indonesia dan Cina yang akan mendukung industri ritel,

kami percaya rencana ekspansi MLPL ini akan menghasilkan laba dan meningkatkan pendapatan MLPL. Untuk periode 2010-2014, kami memproyeksikan pendapatan MLPL akan tumbuh dengan rata-rata CAGR sebesar 23,0%

Likuiditas yang Memadai Untuk Pelunasan Pinjaman Per 9M2011, kewajiban MLPL adalah sebanyak Rp 5,55 triliun, naik 0,6% dari

kewajiban pada bulan Desember 2010. Sekitar 30% dari total kewajiban tersebut adalah merupakan kewajiban jangka panjang yaitu berupa obligasi yang diterbitkan oleh anak perusahaannya (MPPA) di tahun 2009 dan akan jatuh tempo pada tahun 2012 dan 2014 dan pinjaman bank yang digunakan untuk modal kerja. Sedangkan 70%-nya merupakan pinjaman jangka pendek yaitu modal kerja anak-anak perusahaannya. Dengan jumlah kewajiban tersebut dibagi dengan total ekuitas MLPL sebesar Rp 8,1 triliun, maka rasio kewajiban terhadap

ekuitas adalah 0,7x. Sedangkan dengan total aset yang mencapai Rp 13,7 triliun, rasio total kewajiban terhadap aset adalah sebesar 0,41x. Kondisi ini menunjukkan bahwa MLPL memiliki dana yang memadai untuk membayar

seluruh kewajibannya kepada kreditor.

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 12 dari 16 halaman

Gambar 10 : Aset, Kewajiban dan Ekuitas MLPL

Sumber: PT Multipolar Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

Prospek Usaha MLPL

Kuatnya permintaan konsumen masih menjadi mesin utama untuk pertumbuhan

perekonomian di Cina dan Indonesia pada tahun 2012, meskipun diperkirakan pertumbuhannya akan lebih rendah dari tahun sebelumnya yaitu masing-masing sebesar 8,7% dan 6,2%. Industri ritel di Indonesia dan Cina diperkirakan akan tumbuh masing-masing sebesar 20% YoY dan 13,2 YoY pada periode yang sama. Ritel modern masih memiliki potensi untuk tumbuh di Indonesia karena, saat ini penetrasi pasar ritel modern baru menjangkau sekitar 40% dari total pasar, lebih kecil dari negara-negara Asia lainnya, sementara normalisasi harga properti di

Cina diperkirakan akan meningkatkan konsumsi pada sektor lainnya termasuk sektor ritel.

Di sisi lain, tahun 2012 akan menjadi tahun yang penting bagi industri TIK global dan di Asia. Khusus di Indonesia, Business Monitor International (BMI) memperkirakan industri TIK akan tumbuh sebesar 18% per tahun dalam empat tahun yang akan datang. Berbagai tren yang meningkatkan daya tarik industri ini

dalam beberapa tahun terakhir telah diadaptasi dan akan menjadi fitur utama dalam industri TIK yang terus tumbuh, seperti komputasi awan (cloud

computing). BMI juga memperkirakan bahwa nilai belanja TIK di Indonesia pada 2011 akan mencapai Rp 5,4 miliar, naik 14,9% YoY dari 2010. Pertumbuhan ini didorong beberapa hal, antara lain penyebaran industri informasi teknologi, pasar yang semakin kompetitif, peningkatan penjualan hardware dan penjualan perangkat lunak dan penyebaran layanan teknologi informasi. Pertumbuhan

industri ini juga didorong oleh meningkatnya pengeluaran pemerintah untuk teknologi dan informasi, seperti program e-learning, e-KTP dan e-paspor. Namun, industri TIK masih menghadapi kurangnya infrastruktur dan kesenjangan digital yang tinggi yang bisa menghambat pertumbuhan industri ini.

Diperkuat oleh rencana ekspansi usaha MLPL dan anak perusahaannya selama tahun 2011-2012 yang diproyeksikan akan memerlukan dana sekitar USD 60 juta sampai dengan USD 90 juta, kami memproyeksikan pendapatan MLPL dapat

tumbuh dengan rata-rata CAGR sebesar 23,0% selama periode 2010-2014.

Gambar 11 : Proyeksi Pendapatan MLPL

Sumber: PT Multipolar Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 13 dari 16 halaman

Tabel 4: Analisa SWOT

Kekuatan (Strengths) Kelemahan (Weakness)

Terkenal sebagai penyedia solusi

IT Memiliki jaringan distribusi yang

luas yang tersebar di Indonesia dan Cina

Memiliki hubungan yang baik dengan penyedia IT ternama di dunia

Rendahnya hambatan dalam

industri Tidak baiknya kinerja anak-anak

perusahaan, dimana MLPL memiliki saham minoritas bisa menurunkan

laba bersih MLPL

Kesempatan (Opportunities) Ancaman (Threats) Berkembangnya industri IT

seperti komputasi awan di

Indonesia Lebih baiknya prospek

perekonomian di Indonesia dan Cina, begitu juga dengan prospek industri ritel

Pemain baru dengan modal yang

lebih besar akan meningkatkan

persaingan Mundurnya penyelesaian beberapa

proyek properti dapat menghambat pengembangan toko

Kurangnya infrastruktur TIK di Indonesia

ANALISA SWOT

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 14 dari 16 halaman

Penilaian

Metodologi Penilaian

Kami mengaplikasikan metode discounted cash flow (DCF) sebagai metode penilaian utama dengan pertimbangan bahwa pertumbuhan pendapatan adalah merupakan faktor yang sangat mempengaruhi nilai (value driver) jika dibandingkan dengan pertumbuhan aset. Kami tidak mengkombinasikan perhitungan DCF ini dengan metode Guideline Company Method (GCM) di dalam valuasi ini, disebabkan tidak terdapat peers

yang benar-benar dapat diperbandingkan di Bursa Efek Indonesia. Penilaian ini berdasarkan pada harga 100% saham MLPL per 16 Maret 2012, dengan menggunakan laporan keuangan MLPL per 30 September 2011 sebagai dasar analisa fundamental.

Estimasi Nilai

Kami menggunakan Cost of Capital sebesar 13,4% dan Cost of Equity sebesar 14,8% berdasarkan asumsi-asumsi berikut:

Tabel 5: Asumsi

Risk free rate [%]* 5,9

Risk premium [%]* 9,3

Beta [x]* 0,9

Cost of Equity [%] 14,8

Marginal tax rate [%] 25,0

Debt to Equity Ratio 0,3

WACC [%] 13,4

Sumber: Bloomberg, Pefindo Divisi Valuasi Saham & Indexing Catt: * per 16 Maret 2012

Estimasi Target harga saham untuk 12 bulan berdasarkan posisi penilaian pada tanggal 16 Maret 2012 dengan menggunakan metode DCF dan asumsi

tingkat diskonto 13,4% adalah sebesar Rp 360-Rp 385.- per lembar saham Tabel 6: Ringkasan Penilaian Metode DCF

Konservatif Moderat Agresif

PV of Free Cash Flows [Rp miliar] 833 876 920

PV Terminal Value [Rp miliar] 957 1,007 1,057

Non-Operating Assets [Rp miliar] 3.649 3.649 3.649

Net Debt [Rp miliar] (2.669) (2.669) (2.669)

Total Equity Value [Rp miliar] 2.769 2.864 2.958

Number of Share [juta saham] 7.728 7.728 7.728

Fair Value per Share [Rp] 360 370 385 Sumber: Estimasi Pefindo Divisi Valuasi Saham & Indexing

TARGET HARGA

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 15 dari 16 halaman

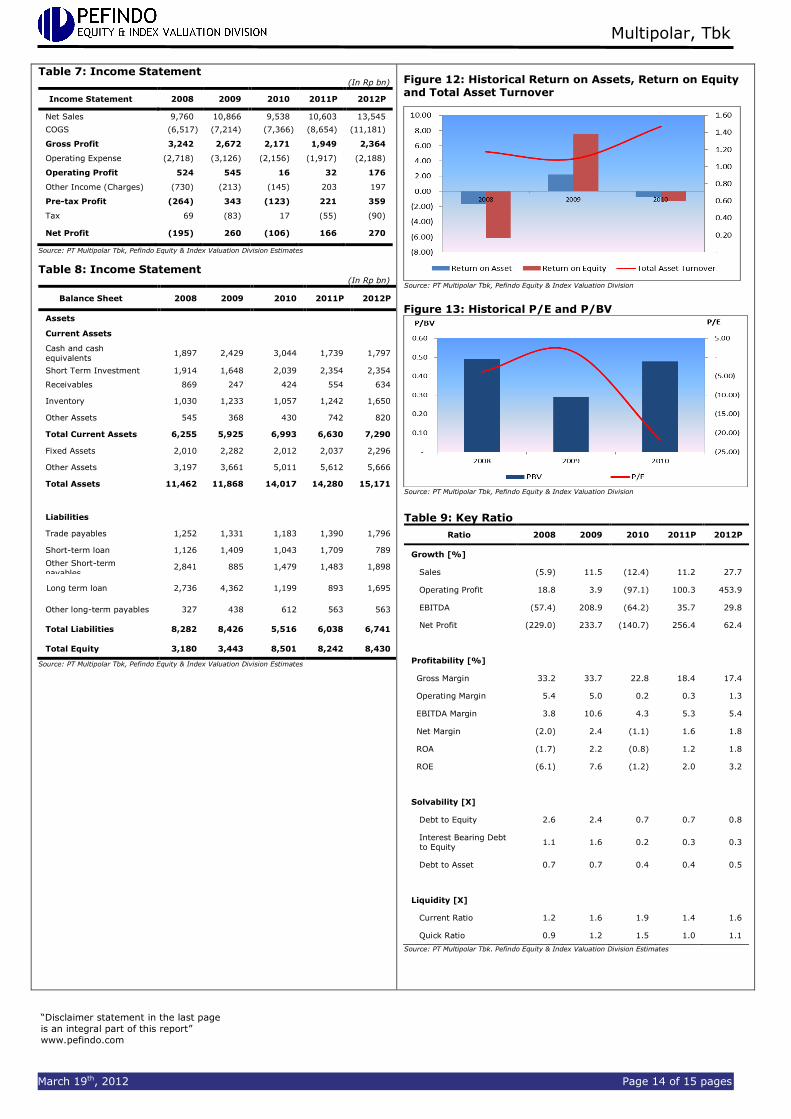

Tabel 7: Laporan Laba (Rugi) (Dalam Rp miliar)

Income Statement 2008 2009 2010 2011P 2012P

Penjualan 9.760 10.866 9.538 10.603 13.545

Harga Pokok Penjualan (6.517) (7.214) (7.366) (8.654) (11.181)

Laba Kotor 3.242 2.672 2.171 1.949 2.364

Beban Operasi (2.718) (3.126) (2.156) (1.917) (2.188)

Laba Operasi 524 545 16 32 176

Pendapatan (Beban) Lain-

lain (730) (213) (145) 203 197

Laba Sebelum Pajak (264) 343 (123) 221 359

Pajak 69 (83) 17 (55) (90)

Laba Bersih (195) 260 (106) 166 270

Sumber: PT Multipolar Tbk., Estimasi Pefindo Divisi Valuasi Saham & Indexing

Tabel 8: Neraca (Dalam Rp miliar)

Neraca 2008 2009 2010 2011P 2012P

Aset

Aset Lancar

Kas dan Setara Kas 1.897 2.429 3.044 1.739 1.797

Investasi Jk. Pendek 1.914 1.648 2.039 2.354 2.354

Piutang Usaha 869 247 424 554 634

Persediaan 1.030 1.233 1.057 1.242 1.650

Aset Lancar Lain-lain 545 368 430 742 820

Total Aset Lancar 6.255 5.925 6.993 6.630 7.290

Aset Tetap 2.010 2.282 2.012 2.037 2.296

Aset Lain-lain 3.197 3.661 5.011 5.612 5.666

Total Aset 11.462 11.868 14.017 14.280 15.171

Kewajiban

Hutang Usaha 1.252 1.331 1.183 1.390 1.796

Pinjaman Jk. Pendek 1.126 1.409 1.043 1.709 789

Pinjaman Jk. Pendek

lainnya 2.841 885 1.479 1.483 1.898

Pinjaman Jk. Panjang 2.736 4.362 1.199 893 1.695

Kewajiban Lain-lain 327 438 612 563 563

Total Kewajiban 8.282 8.426 5.516 6.038 6.741

Total Ekuitas 3.180 3.443 8.501 8.242 8.430

Sumber: PT Multipolar Tbk., Estimasi Pefindo Divisi Valuasi Saham & Indexing

Gambar 12: Return on Assets, Return on Equity dan Total Asset Turnover Historis

Sumber: PT Multipolar Tbk., Pefindo Divisi Valuasi Saham & Indexing

Gambar 13: P/E dan P/BV Historis

Sumber: PT Multipolar Tbk., Pefindo Divisi Valuasi Saham & Indexing

Tabel 9: Rasio-Rasio Kunci

Rasio 2008 2009 2010 2011P 2012P

Pertumbuhan [%]

Penjualan (5,9) 11,5 (12,4) 11,2 27,7

Laba Operasi 18,8 3,9 (97,1) 100,3 453,9

EBITDA (57,4) 208,9 (64,2) 35,7 29,8

Laba Bersih (229,0) 233,7 (140,7) 256,4 62,4

Profitabilitas [%]

Marjin Laba Kotor 33,2 33,7 22,8 18,4 17,4

Marjin Laba Operasi 5,4 5,0 0,2 0,3 1,3

Marjin EBITDA 3,8 10,6 4,3 5,3 5,4

Marjin Laba Bersih (2,0) 2,4 (1,1) 1,6 1,8

ROA (1,7) 2,2 (0,8) 1,2 1,8

ROE (6,1) 7,6 (1,2) 2,0 3,2

Solvabilitas [X]

Debt to Equity 2,6 2,4 0,7 0,7 0,8

Interest Bearing Debt to Equity

1,1 1,6 0,2 0,3 0,3

Debt to Asset 0,7 0,7 0,4 0,4 0,5

Likuiditas [X]

Rasio Lancar 1,2 1,6 1,9 1,4 1,6

Rasio Cepat 0,9 1,2 1,5 1,0 1,1

Sumber: PT Multipolar Tbk., Estimasi Pefindo Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada halaman

akhir merupakan bagian yang tidak

terpisahkan dari dokumen ini”

www.pefindo.com

Multipolar, Tbk

19 Maret 2012 Halaman 16 dari 16 halaman

DISCLAIMER

Laporan ini dibuat berdasarkan sumber-sumber yang kami anggap terpercaya dan dapat diandalkan. Namun kami tidak menjamin kelengkapan, keakuratan atau kecukupannya. Dengan demikian kami tidak bertanggung jawab atas segala keputusan investasi yang diambil berdasarkan laporan ini. Adapun asumsi, opini, dan perkiraan merupakan hasil dari pertimbangan internal kami per tanggal penilaian (cut off date), dan kami dapat mengubah pertimbangan diatas sewaktu-waktu tanpa pemberitahuan terlebih dahulu.

Kami tidak bertanggung jawab atas kekeliruan atau kelalaian yang terjadi akibat penggunaan laporan ini. Kinerja dimasa lalu tidak selalu dapat dijadikan acuan hasil masa depan. Laporan ini bukan merupakan rekomendasi penawaran, pembelian atau menahan suatu saham tertentu. Laporan ini mungkin tidak sesuai untuk beberapa investor. Seluruh opini dalam laporan ini telah disampaikan dengan itikad baik, namun sewaktu-waktu dapat berubah tanpa pemberitahuan terlebih dahulu, dan disajikan dengan benar per tanggal diterbitkan laporan ini. Harga, nilai, atau pendapatan dari setiap saham Perseroan yang disajikan dalam laporan ini kemungkinan dapat lebih rendah dari harapan pemodal, dan pemodal juga mungkin mendapatkan pengembalian yang lebih rendah dari nilai investasi yang ditanamkan. Investasi didefinisikan sebagai pendapatan yang kemungkinan besar diterima dimasa depan, namun nilai dari pendapatan yang akan diterima tersebut kemungkinan besar juga akan berfluktuasi. Untuk saham Perseroan yang penyajian laporan keuangannya didenominasi dalam mata uang selain Rupiah, perubahan nilai tukar mata uang

tersebut kemungkinan dapat menurunkan nilai, harga, atau pendapatan investasi pemodal. Informasi dalam laporan ini bukan merupakan pertimbangan pajak dalam mengambil suatu keputusan investasi.

Target harga saham dalam Laporan ini merupakan nilai fundamental, bukan merupakan Nilai Pasar Wajar, dan bukan merupakan harga acuan transaksi yang diwajibkan oleh peraturan perundang-undangan yang berlaku.

Laporan target harga saham yang diterbitkan oleh Pefindo Divisi Valuasi Saham dan Indexing bukan merupakan rekomendasi untuk membeli, menjual, atau menahan suatu saham tertentu, dan tidak dapat dianggap sebagai nasehat investasi oleh Pefindo Divisi Valuasi Saham dan Indexing yang behubungan dengan cakupan Jasa Pefindo kepada, atau kaitannya kepada, beberapa pihak, termasuk emiten, penasehat keuangan, pialang saham, investment banks, institusi keuangan dan perantara keuangan, dalam kaitannya menerima imbalan atau keuntungan lainnya dari pihak tersebut,

Laporan ini tidak ditujukan untuk pemodal tertentu dan tidak dapat dijadikan bagian dari tujuan investasi terhadap suatu saham dan juga bukan merupakan rekomendasi investasi terhadap suatu saham tertentu atau suatu strategi investasi. Sebelum melakukan tindakan dari hasil laporan ini, pemodal disarankan untuk mempertimbangkan terlebih dahulu kesesuaian situasi dan kondisi dan, jika dibutuhkan, mintalah bantuan penasehat keuangan.

PEFINDO memisahkan kegiatan Valuasi Saham dengan kegiatan Pemeringkatan untuk menjaga independensi dan objektivitas dari proses dan produk kegiatan analitis. PEFINDO telah menetapkan kebijakan dan prosedur untuk menjaga kerahasiaan informasi non-publik tertentu yang diterima sehubungan dengan proses analitis. Keseluruhan proses, metodologi dan database yang digunakan dalam penyusunan Laporan Target Harga Referensi Saham ini secara keseluruhan adalah berbeda dengan proses, metodologi dan database yang digunakan PEFINDO dalam melakukan pemeringkatan.

Laporan ini dibuat dan disiapkan Pefindo Divisi Valuasi Saham & Indexing dengan tujuan untuk meningkatkan transparansi harga saham yang tercatat di Bursa Efek Indonesia. Laporan ini juga bebas dari pengaruh tekanan atau paksaan dari Bursa maupun Perseroan yang dinilai. Pefindo Divisi Valuasi Saham & Indexing akan menerima imbalan sebesar Rp.40.000.000,- dari perusahaan yang dinilai untuk 2 (dua) kali pelaporan per tahun. Untuk keterangan lebih lanjut, dapat mengunjungi website kami di http://www.pefindo.com

Laporan ini dibuat dan disiapkan oleh Pefindo Divisi Valuasi Saham dan Indexing. Di Indonesia Laporan ini dipublikasikan pada website kami dan juga pada website Bursa Efek Indonesia.

Page 1 of 15 pages

Contact: Equity & Index Valuation Division Phone: (6221) 7278 2380 [email protected] “Disclaimer statement in the last page is an

integral part of this report”

www.pefindo.com

Multipolar, Tbk Primary Report

Equity Valuation

March 19th, 2012

Target Price

Low High 360 385

Retail & IT Group

Property

Historical Chart

Source : Bloomberg

Stock Information Rp

Ticker code MLPL

Market price as of March 16th, 2012 136

Market price – 52 week high 275

Market price – 52 week low 124

Market cap – 52 week high (bn) 2,396

Market cap – 52 week low (bn) 958

Market Value Added & Market Risk

Source : Bloomberg, Pefindo Equity & Index Valuation Division

Shareholders* (%)

Cyport Limited 26.95

Grandhill Asia Limited 5.05

HSBC-Fund Services 5.38

Public (each below 5%) 62.62

Notes: As of December 31st, 2011

Promising to Become the Biggest Player in Retail Industry

PT Multipolar Tbk (“MLPL”) was established in 1975 as an electronics retailer which transforms to Information & Technology (“IT”) solutions provider. In 1986, MLPL became the first IBM business partner in Indonesia. Even though MLPL started its business as an electronic retailer, nowadays MLPL also focus in developing its business to become a big player in retail industry through its ownership in PT Matahari Putra

Prima Tbk (“MPPA”) and Robbinz Department Store (“RDS”) in China. Currently MLPL has extensive retail network in Indonesia and China. In Indonesia, MLPL through MPPA operates 63 Hypermarts, 24 Foodmarts and 63 Boston HBC’s. While in China, MLPL has opened 6 retail stores in China, consist of 2 Hypermarts in Tianjin and Suzhou and 4 Department Stores in Tianjin, Chengdu, Yangzhou and Suzhou. Moreover, MLPL will

continue to develop it’s IT and Multimedia business unit and looking for another investment opportunity in order to achieve more strategic business portfolio.

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 2 of 15 pages

Indonesia and China Economic Development: Domestic Demand Will Continue Support the Economic Growth

World’s economy growth in 2012 will again be bolstered by the vibrant growth in emerging and developing market which supported by its domestic market. The emerging economy is estimated will grow by 5.1% YoY in

2011, lowering from 6.4% YoY growth in 2010. While Indonesia economy in 2012 will grow by 6.2% slightly down than 2011 figures of 6.5% YoY. The economic growth in China remains robust due to strong consumer demand. It is estimated will grow by 8.7% YoY in 2012, lower than 2011 growth of 9.5% YoY. Better economy outlook in both countries also reflected in the outlook of retail industry which very closely related to consumer demand, per capita income and people purchasing power. Retail

industry in both countries is estimated will grow by 20% and 13.2% in Indonesia and China, respectively.

Better Performance during 9M2011 Despite of net loss of associated companies in the first nine month 2011, MLPL showed better performance compared to the same period in 2010. In the top line, MLPL consolidated revenue increased by 7.3% YoY to

Rp 7.6 trillion from Rp 7.0 trillion in 9M2010. The revenue increases in this periods was from retail and distribution business unit that was driven by MPPA’s revenue. In 9M2011, the revenue of retail business unit increased by 0.63% YoY to Rp 6.6 trillion and contributes about 88% to MLPL’s consolidated revenue. While, MLPL’s revenue from IT business grew significantly by 115% YoY to Rp 833 billion from Rp 388 billion in 9M2010. Whereas, at operating level, MLPL managed to book positive operating

profit of Rp 843 million, up by 102% YoY from minus Rp 41 billion in 9M2010.

Expansion for Further Growth For 2012, MLPL has budgeted about USD 90 million for business expansion. As the main contributor to its revenue, MLPL continues expanding its retail business by opening new stores. In addition to MPPA’s retail store in Indonesia which opened about 12 stores in 2011, at the same periods,

MLPL also opened 3 retail stores in China, consisting of 2 Hypermart in Tianjin and Suzhou and 1 Robbinz in Suzhou. While for 2012, MLPL plans to

open about 10 retail stores in China in 2012 which estimated will spend about USD 60 million; while in Indonesia its subsidiary (MPPA) also plan to open 15 new stores during 2012. On the other hand, IT business unit is on working to develop cloud computing program which estimated will be

released in 2013. This year, MLPL will build a data center to support the cloud computing program which will spend about USD 30 million capital expenditures. With such expansion, we estimate MLPL’s revenue to grow at a CAGR of 23.0% during 2010-2014 periods

Business Prospects As the retail industry in Indonesia and china continue to grow by 20% and 13.2%, respectively, the prospect of retail business of which the biggest

contributor of MLPL’s revenue will remain conducive, bolstered up by extensive retail network which spread over almost all provinces in Indonesia and in several big cities in China. We estimate MLPL’s revenue from retail business will grow by 17.5% YoY in 2011 and growing at CAGR of 27.1% during 2011-2015. On the other hand, year 2012 will be the

momentous year for ICT industry globally and in Asia. Specifically in Indonesia, Business Monitor International (BMI) estimates ICT industry will

grow by 18% per year within the next four year. Many trends gaining traction in the last couple of years have crossed the chasm and will be a mainstream feature of the ICT industry moving forward, such as cloud computing. In line with its expansion in cloud computing program, MLPL will taste the sweetness of this business in 2013. Nevertheless, ICT industry in Indonesia is still faced with the lack of infrastructure and high digital gap

which will hamper ICT industry growth. We estimate MLPL’s revenue from IT business to grow at a CAGR of 14.8% during 2011-2015 periods.

INVESTMENT PARAMETER

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 3 of 15 pages

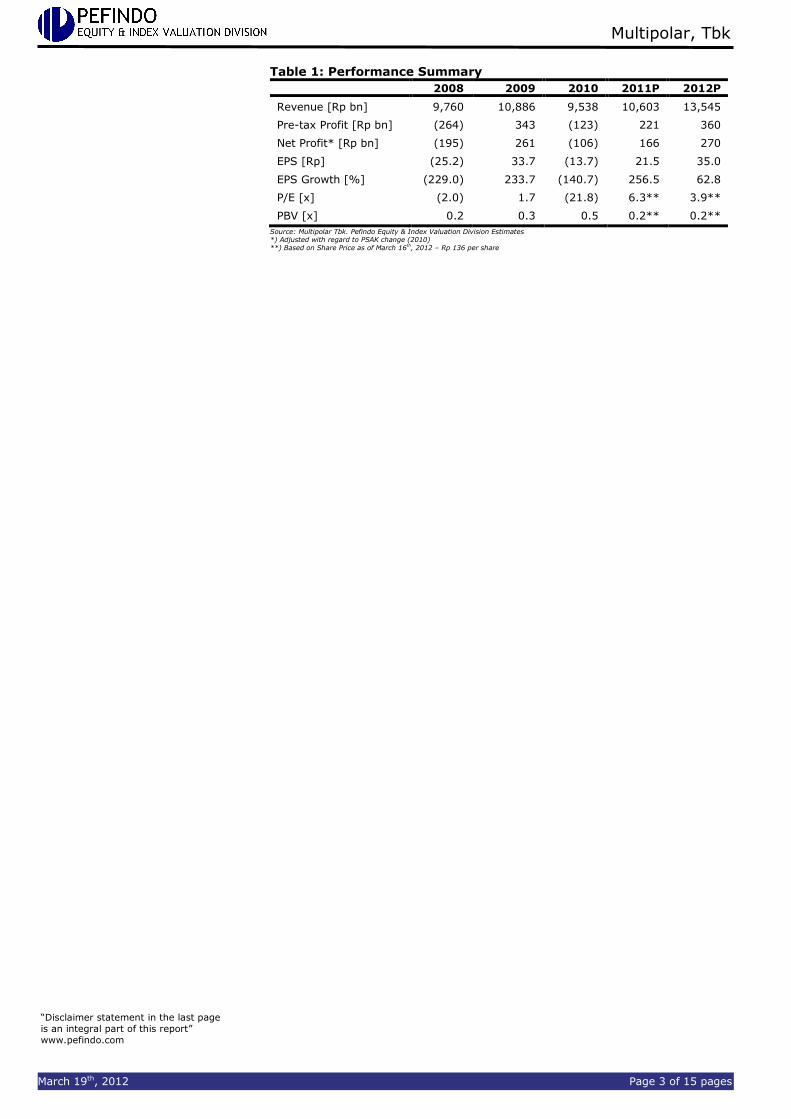

Table 1: Performance Summary

2008 2009 2010 2011P 2012P

Revenue [Rp bn] 9,760 10,886 9,538 10,603 13,545

Pre-tax Profit [Rp bn] (264) 343 (123) 221 360

Net Profit* [Rp bn] (195) 261 (106) 166 270

EPS [Rp] (25.2) 33.7 (13.7) 21.5 35.0

EPS Growth [%] (229.0) 233.7 (140.7) 256.5 62.8

P/E [x] (2.0) 1.7 (21.8) 6.3** 3.9**

PBV [x] 0.2 0.3 0.5 0.2** 0.2**

Source: Multipolar Tbk. Pefindo Equity & Index Valuation Division Estimates *) Adjusted with regard to PSAK change (2010) **) Based on Share Price as of March 16

th, 2012 – Rp 136 per share

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 4 of 15 pages

Growth-Value Map gives visualization of market expectations for the companies listed on IDX. Current Performance (“CP”) metric is a portion of current stock

market value that can be linked to the perpetuity of current company’s performance in profitability. Growth Expectations (“GE”) metric is the difference

between current stock market value and the value of current performance. Both metrics are normalized by the company’s book value. Growth-Value Map divides companies into four clusters, they are:

Excellent value managers (“Q-1”) Market expects companies in Q-1 to surpass their benchmark in

profitability and growth.

Expectation builders (“Q-2”) Market has relatively low expectations of profitability from companies in Q-2 in the short term, but has growth expectations exceed the benchmark.

Traditionalists (“Q-3”)

Market has low growth expectations of companies in the Q-3, although they showed a good profitability in the short term.

Asset-loaded value managers (“Q-4”) Market has low expectations in terms of profitability and growth for companies in Q-4

Figure 1: Growth-Value Map

(MLPL, Investment Sub Industry, and Trade, Services & Investment Industry)

-4

-2

0

2

4

6

8

0 1 2 3 4

Gro

wth

Exp

ecta

tio

ns

Current Performance (CP)

BMTR

PLAS

Q-1

Q-3

Q-2

Q-4

BHIT

MLPL

Source: Pefindo Equity & Index Valuation Division

MLPL is lying in Asset-loaded value managers (Q4). Although MLPL managed to book positive net income in 9M2011, but market view MLPL profitability below

their benchmark expectations. Moreover, market also expects MLPL’s growth opportunity slightly below their benchmark. By improving its profitability performance as well as rejuvenate its investor relation activity, we believe MLPL has opportunity to move to the second cluster (Expectation Builder).

GROWTH VALUE MAP

Multipolar, Tbk

February 23rd, 2012 Page 5 of 15 pages

World Economic Outlook: Will Again Be Bolstered By the Vibrant Growth in Emerging Markets

Based on The Conference Board research, global economy growth is projected to grow at 3.2% YoY in 2012, weakening from the previous year growth of 3.9% YoY, but then expected to accelerate somewhat to 3.5% YoY for the periods of 2013-2016. High unemployment and weak consumption in developed nations caused the downward revision in forecasts of world economic growth in 2012 from earlier projections. Despite the downturn, the world economy in 2012 will again be bolstered by the vibrant growth in emerging markets despite reduced

momentum due to the spillover effects of the crisis in Europe and the US.

Developing countries will face weakening external demand in 2012, but in most emerging economies they can rely on domestic demand to propel the growth until the world economy becomes healthier. But for developing countries that rely on external demand, will be impacted from the shrinking global market. In line with the downturn in overall economy, emerging economies are estimated to have

growth of only 5.1% YoY in 2012 lowering from 6.4% YoY growth in 2011. The downsize is resulting from emerging economies facing a slower export growth, after beating the trend for a while. However, they generally have more flexibility

in fiscal policy than most developed countries that may benefit them in term of more stable growth.

Table 2: Global Economic Growth

Country 2011E 2012F

US

EU-15

Japan

Other Advance Advance Economies

1.5

1.5

-0.5

3.3 1.6

1.1

1.1

0.7

2.5 1.3

China India

Other developing Asia

Latin America

Middle East

Africa

Central & Eastern Europe

Russia and Other CIS

Emerging Market and Developing Economies

9.5 7.8

5.1

4.5

4.3

4.4

4.0

4.6

6.4

8.7 7.4

2.8

2.9

2.3

2.4

2.1

2.8

5.1

World 3.9 3.2 Source: The Conference Board Economic Outlook, November 2011; Pefindo Equity & Index Valuation Division

Domestic Demand Remain the Main Engine for Indonesia and China Economic Growth in 2012 A deteriorating global economy is likely to impede growth in China and Indonesia in 2012. The Chinese government has continued taking steps to avert

overheating and to steer the economy toward a soft landing, while a mix of monetary and macro prudential measures has slowed GDP growth, although growth still remains robust due to strong consumer demand.

Table 3: Indonesia Economic Indicator

2008 2009 2010 2011

GDP Growth (%, YoY)

Inflation rate (%, YoY)

Exchange rate* (Rp/USD)

SBI rate (%)

6.1

11.06

9,136

9.25

4.5

2.78

9,680

6.50

6.1

6.96

10,398

6.5

6.5

3.79

8,779

6.0 * Bank Indonesia middle rate average Source: BPS, Bank Indonesia, Pefindo Equity & Index Valuation Division

Meanwhile Indonesia’s economic fundamentals will remain strong despite

expected effect of current global crisis that may cause world economic slowdown. Pefindo estimates that Indonesia’s economic growth will slightly down to 6.2% YoY in 2012, as in 2011, it was recorded of 6.5% YoY. The growth locomotive would be contributed from private consumption with the support of continued consumers’ optimism, manageable inflation, lower interest rate, and increasing per capita income. Indonesia’s per capita income reached USD 3,543 in 2011,

and may break USD 4,000 in 2012, compared to USD 3,000 in 2010. Meanwhile, investment realization in 2011 reached Rp 251.3 trillion or rose by 20.5% compared to 2010’s. With population composition is dominated by productive age population (around 60%) and increasing international perception of Indonesia’s economy development that reflected from the inclusion of Indonesia into investment grade by Fitch on December 2011 and by Moody’s on January 2012, then we believe that Indonesia will able to maintain its favorable growth in the

coming years.

BUSINESS INFORMATION

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 6 of 15 pages

ICT Industry Will be Flourished in 2012 Year 2012 will be the momentous year for ICT industry globally and in Asia. Specifically in Indonesia, Business Monitor International (BMI) estimates ICT industry will grow by 18% per year within the next four years. Many trends

gaining traction in the last couple of years have crossed the chasm and will be a mainstream feature of the ICT industry moving forward, such as cloud

computing. Meanwhile, the value of ICT industry based on the data from ministry of Communication and Information Technology (Kemkominfo) was reached Rp 350 trillion, up by 17% YoY from Rp 300 trillion in 2010. The growth was driven by a few things such as the spread of information technology industry, an increasingly competitive market, increase of hardware and software sales and the spread of information technology services. The sales of hardware, such as cell phone and computer grew at CAGR of 37.3% and 27.9% during 2008-2011

periods, while the sales of software reach USD 599 million in 2011 and estimated to grow at 22%CAGR in the next five years. Moreover, ICT industry is also boosted by the increase of government spending for technology and information, such as e-learning program, e-KTP and e-passport.

However, ICT industry is still facing lack of infrastructure and high digital gap which will hamper ICT industry growth. To solve this problem, Indonesia

government in 2012 has budgeted about Rp 3.2 trillion in the draft budget of

government’s revenue and expenditure for the Ministry of Communication and Information Technology. Kemkominfo will use these funds to focus on building telecommunication infrastructure such as Palapa Ring that relate to government targets to increase internet penetration up to 30% in 2014.

Starting as Electronic Retailer and Now Having a Wide Range of Strategic Portfolio

PT Multipolar Tbk (MLPL) was established in 1975 as an electronic retailer and now MLPL transforms to IT solution provider and strategic investment company. As of September 2011, almost 90% of its income was from its investment in various industry i.e. retail, multimedia and services. In retail industry, MLPL hold majority shares of ownership in PT Matahari Putra Prima Tbk (MPPA) - operator the second largest hypermarket in Indonesia- and Congrex Limited, operator of Robbinz Department Store (RDS), a well-known department store in China. In

Multimedia Industry, MLPL through its subsidiary PT Reksa Puspita Karya has about 33.8% shares of PT First Media Tbk (KBLV) - first mover in broadband services. MLPL is also a pioneer in the field of administrative services and

outsourcing industry through its subsidiaries PT Multifiling Mitra Indonesia Tbk (MFMI) and PT Visionet International.

Figure 2: MLPL’s Portfolios

Multipolar Tbk

Information Technology Retail Services Multimedia

PT Matahari Putra Prima Tbk

Congrex Limited

PT Sharestar Indonesia

PT Surya Cipta Investama

PT Multifiling Mitra Indonesia Tbk

PT Visonet International

PT Reksa Puspita Karya

PT First Media Tbk

Source: PT Multipolar Tbk, Pefindo Equity & Index Valuation Division

Strong Growth of Financial and Telecommunication Sectors Benefited MLPL IT Business’s revenue

On the sector basis, the source of Indonesian growth has started to be more balanced as the tradable sectors that accounted 46.5% of total GDP rose 4.5% YoY in the 2011, while non-tradable sectors grew 8.3% YoY in the same period vs. 8.2% YoY last year. The growth of non-tradable sector, among others, was supported by financial sector and communication sector. In 2011, financial sector grew by 6.8% YoY while transportation and telecommunication sector grew

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 7 of 15 pages

by 10.7% YoY. The outlook of financial industry will remain positive benefited by credit-rating upgrade.

This condition is a positive indication for MLPL’s IT business division, as majority

of its revenue is from these industries. During 9M2011, banking/financial institution contribute about 64% of total revenue of IT business unit, while telecommunication sectors still constitutes as the second biggest contributor by

23%.

Figure 3: IT Business Revenue Contributors

Source: PT Multipolar Tbk, Pefindo Equity & Index Valuation Division

Extensive Retail Distribution Network Nationwide and Abroad is Believed Will Boosted MLPL’s Revenue from Retail Business Unit One of MLPL strategic investments is in retail industry. In this industry, MLPL has majority shares of PT Matahari Putra Prima Tbk (MPPA) and Congrex Limited. MPPA is operator of Hypermart, the second largest hypermarket in Indonesia. In

the past six years, the number of Hypermart outlet has increased 23.0% a year on the average. In 2005, the number of Hypermart outlet was 17 units and increased to 59 units in 2011. This retail networks are spread over 32 cities in Indonesia. Hypermart is backed up with three distribution centers which have an important role in the distribution of goods to Hypermart and Foodmart. The warehouses of the three distribution centers are located in Surabaya, Balaraja

and Cibitung. In 2011, MPPA has opened 12 new stores of Hypermart which

increased up to 100,000 sqm sales area. The new stores are located in Lippo Karawaci Utara, Ciputra World Surabaya, Serang, Kediri and Gresik, while the rest is planned to be opened in Kudus, Malang, Cirebon, Ciputra Sraya (Sumatera), Gorontalo, Sidoarjo and Palembang.

Figure 4: MPPA’s Distribution Network

Source: PT Matahari Putra Prima Tbk, Pefindo Equity & Index Valuation Division

Meanwhile, abroad, MLPL succeed to expand its business to China by acquiring Congrex Limited, operator of a well-known Department Store in China, namely

Robbinz Department Store (RDS). In addition to RDS, MLPL also develop Hypermart in China. In 2011, MLPL has about 6 stores in China includes 4 RDS stores which spread over Tianjin, Chengdu, Yangzhou and Suzhou (open in December 2011) and 2 Hypermart which located in Tianjin and Suzhou. In this year, MLPL will open about 10 new stores of RDS and Hypermart in China, which

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 8 of 15 pages

we estimate will spend about USD 60 million investments. While, its subsidiary (MPPA) plans to open about 15 stores of Hypermart spread over several cities in Indonesia.

With such extensive retail distribution network we believe, MLPL investment in this industry will create high return, considering the economic growth in Indonesia and China, which supported by high domestic consumption and high

purchasing power. We estimate MLPL’s revenue from retail business unit will grow by 15.4% YoY in 2011 and grew by 27.1% per year in the next five years.

Positive Growth in Data Management Services MLPL also has investment in data management services industry, especially PT Multifiling Mitra Indonesia (“MFMI”) which is a pioneer and leader in Record Management Services since 1993. During 2007-2010, MFMI’s revenue and net income grew by 14.5% and 21.1% per year, respectively, while in 9M2011, its

revenue grew by 6% YoY from Rp 35.5 billion in 9M2010 to Rp 37.5 billion. MFMI is supported by 6 storages located in Lippo Cikarang, Surabaya, Medan, and Bandung which coverage more than 33,000 sqm storage area.

Along with the increase of many companies awareness to delegate their documentation and data management to third party in order to increase their efficiency, we believe its business will continue to grow in subsequent periods.

Figure 5: Data Management-Storage Center

Source: Multipolar Tbk, Pefindo Equity & Index Valuation Division

MLPL’s Revenue Increase Along With the Indonesia Economic Growth MLPL showed a better performance in the first nine months of 2011 compared to the same period in the last year. In year on year basis, MLPL’s revenue grew by 7.3% YoY from Rp 7.0 trillion in 9M2010 to Rp 7.6 trillion in 9M2011. The increases of MLPL’s revenue during this period were one from many positive

effect of Indonesia economy growth during 2011 of 6.5% YoY. Rising per capita income that sustains people purchasing power has boosted retail business revenue (especially in Indonesia) which is the biggest contributor to MLPL’s

revenue. On quarterly basis, MLPL revenue in 3Q2011 grew significantly by 14% q-o-q from 2Q2011 to Rp 2.8 trillion. It was due to high public spending during Ramadhan and before Lebaran days which happen in this quarter. For 4Q2011, we estimate MLPL’s revenue will grow to Rp 3.0 trillion, up by 8.3% q-o-q or

17.7% YoY from Rp 2.6 trillion in 4Q2010. In addition to retail sales, MLPL’s revenue in this period also surge by the revenue from IT unit business especially the sales of hardware such as cellular phone and personal computer.

FINANCE

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 9 of 15 pages

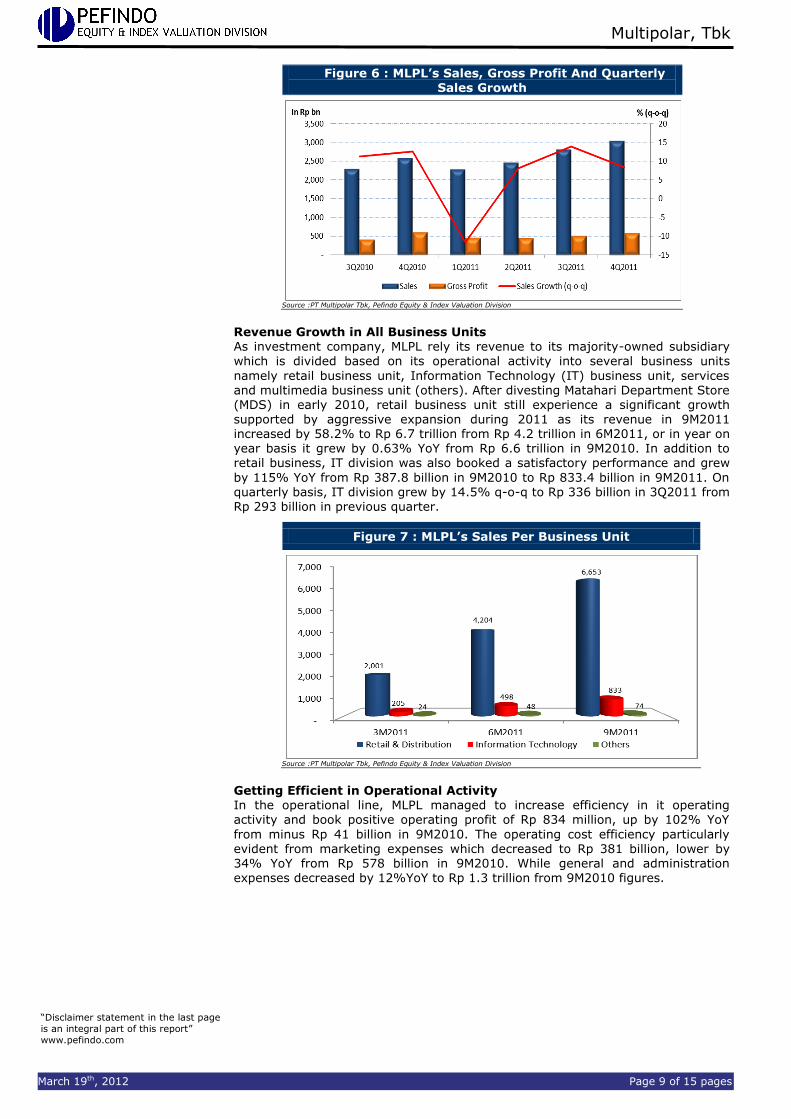

Figure 6 : MLPL’s Sales, Gross Profit And Quarterly Sales Growth

Source :PT Multipolar Tbk, Pefindo Equity & Index Valuation Division

Revenue Growth in All Business Units As investment company, MLPL rely its revenue to its majority-owned subsidiary

which is divided based on its operational activity into several business units

namely retail business unit, Information Technology (IT) business unit, services and multimedia business unit (others). After divesting Matahari Department Store (MDS) in early 2010, retail business unit still experience a significant growth supported by aggressive expansion during 2011 as its revenue in 9M2011 increased by 58.2% to Rp 6.7 trillion from Rp 4.2 trillion in 6M2011, or in year on year basis it grew by 0.63% YoY from Rp 6.6 trillion in 9M2010. In addition to retail business, IT division was also booked a satisfactory performance and grew

by 115% YoY from Rp 387.8 billion in 9M2010 to Rp 833.4 billion in 9M2011. On quarterly basis, IT division grew by 14.5% q-o-q to Rp 336 billion in 3Q2011 from Rp 293 billion in previous quarter.

Figure 7 : MLPL’s Sales Per Business Unit

Source :PT Multipolar Tbk, Pefindo Equity & Index Valuation Division

Getting Efficient in Operational Activity In the operational line, MLPL managed to increase efficiency in it operating activity and book positive operating profit of Rp 834 million, up by 102% YoY

from minus Rp 41 billion in 9M2010. The operating cost efficiency particularly

evident from marketing expenses which decreased to Rp 381 billion, lower by 34% YoY from Rp 578 billion in 9M2010. While general and administration expenses decreased by 12%YoY to Rp 1.3 trillion from 9M2010 figures.

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 10 of 15 pages

Figure 8 : MLPL’s Operating Income

Source :PT Multipolar Tbk, Pefindo Equity & Index Valuation Division

Targeting Capital Spending of USD 90 million for Business Expansion Currently, MLPL is developing two big expansion projects namely cloud computing business and retail business in China. In corporate with HCL Industries, MLPL

has planned to enter cloud computing market since 2010. Nowadays, MLPL is in

the assessment process to determine the best location for data center which is planned to be built in the second half of 2012 and begin to operate in 2013. For this project, MLPL has budgeted about USD 30 million (with assumption of Rp the exchange rate USD 1= Rp 8,768 –average Rupiah exchange rate in 2011- ) equal to Rp 263.0 billion.

In addition to MPPA’s expansion in Indonesia during 2011, MLPL also spent about USD 60 million or equal to Rp 526.1 billion million for capital expenditure to open

3 retail stores in China which we estimate will generate return of Rp 2 million per sqm. Meanwhile, in 2012, MLPL plans to open about 10 stores of RDS and Hypermart which is estimated will need about USD 60 million spending.

Figure 9: MLPL’s Capital Expenditure and The Development of Its Retail

Stores in Indonesia and China

Source :PT Multipolar Tbk, Pefindo Equity & Index Valuation Division Estimation

Considering the development of cloud computing in Indonesia which is estimated to grow by 54% in 2014 and strong domestic demand in Indonesia and China which will support retail industry, we believe the expansion plan will increase MLPL’s revenue. For 2010-2014 periods, we estimate MLPL’s revenue will grow at a CAGR of 23.0%.

Sufficient Liquidity for Debt Payment As of 9M2011, MLPL’ liabilities was amounted to Rp 5.55 trillion, up by 0.6% from December 2010. About 30% of total liabilities are long-term liabilities which formed of bond that issued by its subsidiary (MPPA) in 2009 and will mature in 2012 and in 2014 and in bank debt for working capital. About 70% are short-term liabilities which are for MLPL and subsidiaries working capital. With thus liabilities divided by total equity of Rp 8.1 trillion, we get total debt to equity ratio

at 0.7x. Meanwhile, with total asset reached Rp 13.7 trillion, total debt to asset is 0.41x. It indicates that MLPL has sufficient fund to pay off its entire obligation to creditor.

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 11 of 15 pages

Figure 10 : MLPL’s Assets, Liabilities and Equities

Source :PT Multipolar Tbk, Pefindo Equity & Index Valuation Division

MLPL Business Prospects

Strong consumer demand remain the main engine for economic growth in China

and Indonesia in 2012, although it is estimated will be lower than previous years of 8.7% and 6.2%, respectively. Retail industry in Indonesia and China is estimated to grow by 20% YoY and 13.2 YoY in the same periods. Modern retail still has potential grow in Indonesia as now it caters approximately 40% of total market, smaller than other Asian country, while normalization of property prices in China is estimated will boost consumption in other area include retail.

On the other hand, year 2012 will be the momentous year for ICT industry globally and in Asia. Specifically in Indonesia, Business Monitor International (BMI) estimates ICT industry will grow by 18% per year within the next four year. Many trends gaining traction in the last couple of years have crossed the chasm and will be a mainstream feature of the ICT industry moving forward, such as cloud computing. BMI also estimates that the value of Indonesia’s ICT

spending in 2011 will reach USD 5.4 billion, up by 14.9% YoY from 2010. The growth was driven by a few things, including the spread of information technology industry, an increasingly competitive market, increase of hardware and software sales and the spread of information technology services. It also

boosting by the increase of government spending for technology and information, such as e-learning program, e-KTP and e-passport. However, ICT industry is still faced with the lack of infrastructure and high digital gap that will hamper ICT

industry growth.

Augmented with MLPL and its subsidiaries expansion plan during 2011-2012, which will spent about USD 60 million - USD 90 million, we estimate MLPL’s revenue will grow at a CAGR of 23.0% during 2010-2014 period.

Figure 11 : MLPL’s Sales Projection

Source :PT Multipolar Tbk, Pefindo Equity & Index Valuation Division Estimates

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 12 of 15 pages

Table 4: SWOT Analysis

Strengths Weakness

Well-known as IT solution

partners Extensive retail store network

distribution in Indonesia and China

Good relationship with world class IT provider

Low entry barrier in the industry Underperformed of minority

interest in subsidiaries burden MLPL net income

Opportunities Threats The development of IT industries

such as cloud computing program in Indonesia

Positive outlook of Indonesia and China economy as well as retail

industry

Newcomer with big capital can

give more competition. The delayed of several property

projects hampered the store expansion

Lack of ICT infrastructure in Indonesia

SWOT ANALYSIS

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multipolar, Tbk

March 19th, 2012 Page 13 of 15 pages

VALUATION

Methodology

We apply Discounted Cash Flow (DCF) method as the main valuation approach considering the income growth is a value driver in MLPL instead of asset growth. We do not combine DCF method with Guideline Company Method (GCM) as there is no similar company eligible to be compared with MLPL in the IDX.

This valuation is based on 100% of MLPL’s shares price as of March 16th, 2012, using MLPL’s financial report as of September 30th, 2011 for our fundamental analysis.

Value Estimation

We use Cost of Capital of 13.4% and Cost of Equity of 14.8% based on the following assumptions: Table 5: Assumption

Risk free rate [%]* 5.9

Risk premium [%]* 9.3

Beta [x]* 0.9

Cost of Equity [%] 14.8

Marginal tax rate [%] 25.0

Debt to Equity Ratio 0.3

WACC [%] 13.4

Source: Bloomberg, Pefindo Equity & Index Valuation Division Estimates Notes: * As of March 16

th, 2012

Target price for 12 months based on valuation as per March 16th, 2012 using

DCF method with an assumption of 13.4% discount rate is Rp 360 – Rp 385 per share

Table 6: DCF Method

Conservative Moderate Aggressive

PV of Free Cash Flows [Rp bn] 833 876 920

PV Terminal Value [Rp bn] 957 1,007 1,057

Non-Operating Assets 3,649 3,649 3,649

Net Debt [Rp bn] (2,669) (2,669) (2,669)

Total Equity Value [Rp bn] 2,769 2,864 2,958

Number of Share [mn shares] 7,728 7,728 7,728

Fair Value per Share [Rp] 360 370 385 Source: Pefindo Equity & Index Valuation Division Estimates

TARGET PRICE

“Disclaimer statement in the last page

is an integral part of this report”