pbctpbct 1 economic environment: has connecticut joined the recovery? southern new england economic...

TRANSCRIPT

PBCT

1

Economic Environment: Economic Environment:

Has Connecticut Joined the Recovery?Has Connecticut Joined the Recovery?

Southern New England Southern New England Economic Summit & Outlook 2004Economic Summit & Outlook 2004

May 14, 2004

Todd P. MartinEconomic AdvisorPeople’s Bank203.218-9825 [email protected]

PBCT

2

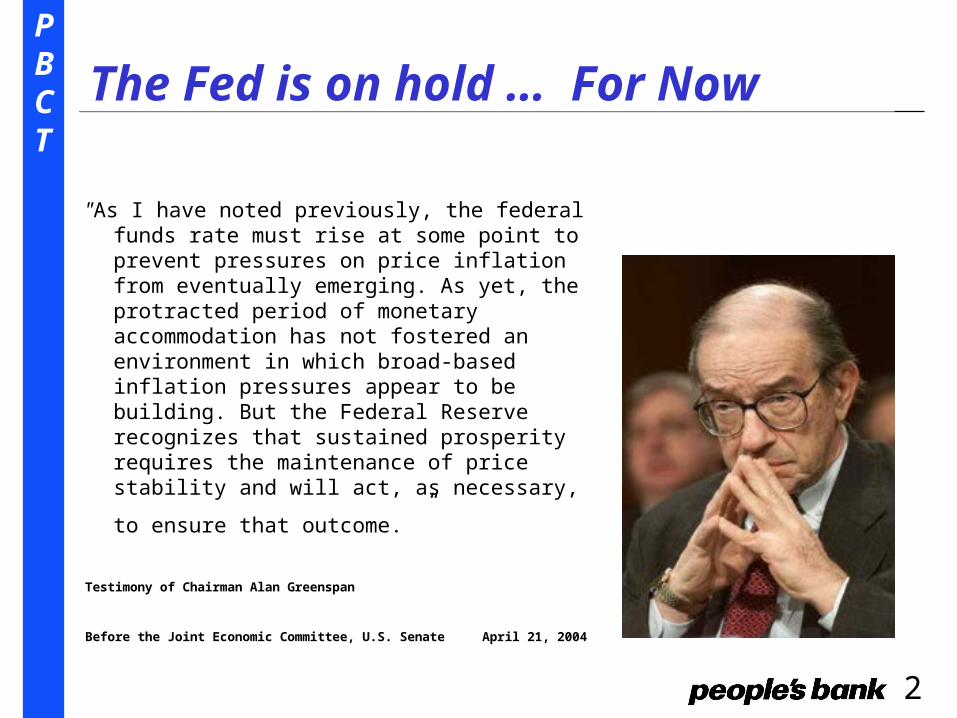

The Fed is on hold … For Now

"As I have noted previously, the federal funds rate must rise at some point to prevent pressures on price inflation from eventually emerging. As yet, the protracted period of monetary accommodation has not fostered an environment in which broad-based inflation pressures appear to be building. But the Federal Reserve recognizes that sustained prosperity requires the maintenance of price stability and will act, as necessary, to ensure

that outcome. ”

Testimony of Chairman Alan Greenspan

Before the Joint Economic Committee, U.S. Senate April 21, 2004

PBCT

3

US Economic Backdrop US Economic Backdrop

• The economic momentum that began in the second half of 2003 is carrying through into 2004. The combination of low interest rates, stimulative fiscal policy, outstanding productivity, and stronger corporate profits should result in real GDP growth of approximately 4%+ this year.

• The Fed has begun to set the stage for higher rates. The fed funds rate should remain at a 46-year low of 1.0% until at least the June or August 2004 FOMC meeting and move towards 1.5% by year-end. 10-year T-note yields should trend slightly higher (5%) by the end of 2004.

• Inflation is well contained, but concerns about the future are increasing.

• Risks: Jobs (insecurity & outsourcing) - Iraq - terrorism - oil prices - divisive election year - growing budget & trade deficits - stocks vulnerable?

PBCT

4

The economy is on track to grow at 4%+ in 2004The economy is on track to grow at 4%+ in 2004

Source: Conference Board,BEA, People’s Bank

Gross Domestic Product (CW$)

Transformation: %Chg, AR Source: Bureau of Economic Analysis

-2

-4

0

2

4

6

8

10

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

PBCT

5

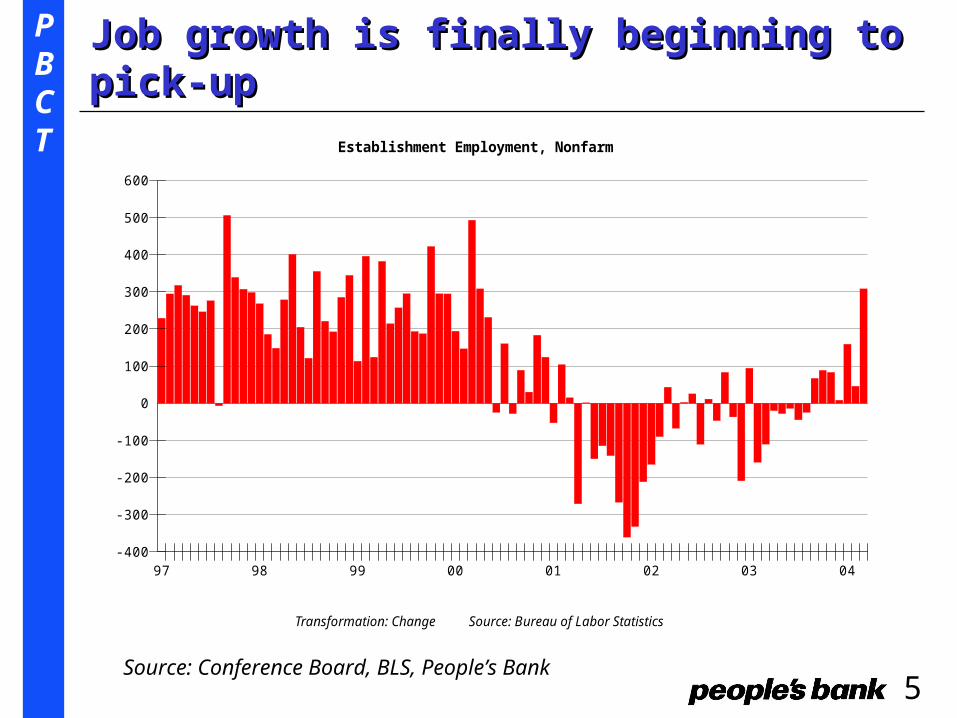

Job growth is finally beginning to pick-upJob growth is finally beginning to pick-up

Source: Conference Board, BLS, People’s Bank

Establishment Employment, Nonfarm

Transformation: Change Source: Bureau of Labor Statistics

-100

-200

-300

-400

0

100

200

300

400

500

600

97 98 99 00 01 02 03 04

monthly change (thousands) SA

PBCT

6

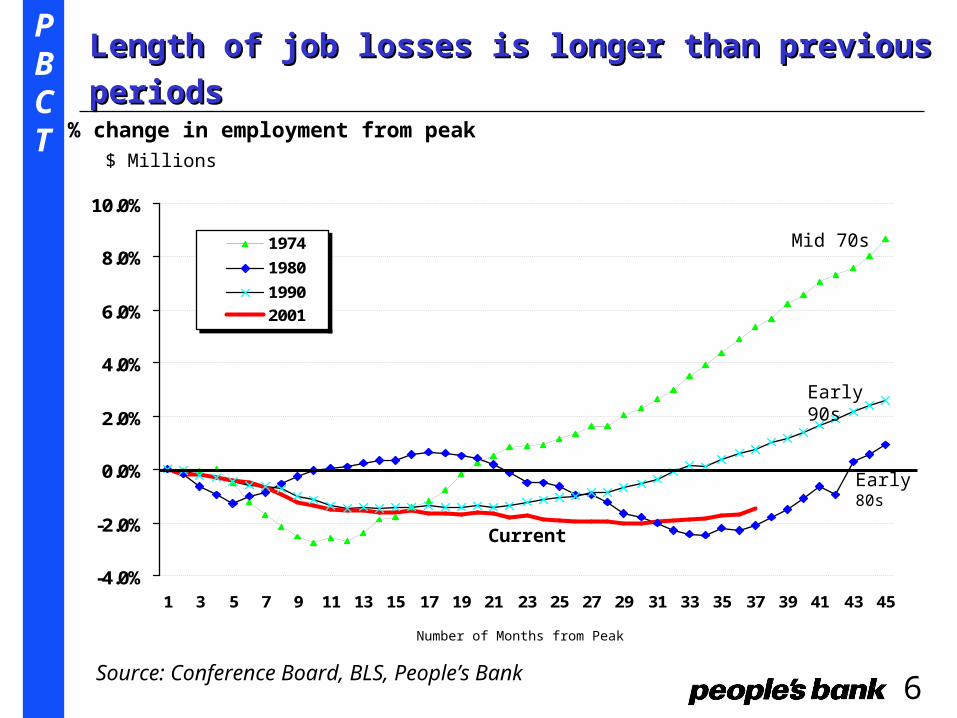

Length of job losses is longer than previous periodsLength of job losses is longer than previous periods

Source: Conference Board, BLS, People’s Bank

% change in employment from peak

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45

1974

1980

1990

2001

$ Millions

Current

Early 90s

Early 80s

Mid 70s

Number of Months from Peak

PBCT

7

Major discrepancies between labor surveysMajor discrepancies between labor surveys

Source: The Conference Board, BLS, People’s Bank

Household vs. Establishment Survey Change (000's) since 11/01 (SA)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

2,500

3,000

Household Survey

Establishment Survey

- 323,000

+ 2.1million

PBCT

8

Jobless Claims at the lowest level since Jan. 2001Jobless Claims at the lowest level since Jan. 2001

Source: Bloomberg, BLS, People’s Bank

US Weekly Initial Jobless Claims - 4 week MA

200.0

250.0

300.0

350.0

400.0

450.0

500.0

550.0Ja

n-89

Jul-8

9Ja

n-90

Jul-9

0Ja

n-91

Jul-9

1Ja

n-92

Jul-9

2Ja

n-93

Jul-9

3Ja

n-94

Jul-9

4Ja

n-95

Jul-9

5Ja

n-96

Jul-9

6Ja

n-97

Jul-9

7Ja

n-98

Jul-9

8Ja

n-99

Jul-9

9De

c-99

Jun-

00De

c-00

Jun-

01De

c-01

Jun-

02De

c-02

Jun-

03De

c-03

Below 400,000 for 5-months

Similar Pattern to early 1990s?

PBCT

9

The US creates - and destroys - more jobsThe US creates - and destroys - more jobs

Source: Tom Peters “Re-Imagine”

Total jobs lost & created – 1980 – 1998 – US vs. Europe (millions)

-44

73

29

04 4

-60

-40

-20

0

20

40

60

80

Job Losses Job Gains Net Gain

US Europe

PBCT

10

Outsourcing will continue Outsourcing will continue

Quotes:

“We will never again be as dominant as we are today. But we can remain in the top spot as long as we obsess on five things: Research-Innovation, Entrepreneurship, Education, Free Trade-Open Society, Self-Reliance”

[Tom Peters: Off-shoring" Manifesto/Rant: Twenty Hard Truths about Inevitabilities, Pitfalls, and Matchless Opportunities ]

“The Americans’ self-image that this tech thing was their private preserve is over. This is a wake-up call to U.S. workers to redouble their efforts at education and research. If they do that it will spur a whole new cycle of innovation, and we’ll both win. If we each pull down our shutters, we will both lose."

[Indian software exec to Tom Friedman/New York Times]

"The notion that God intended Americans to be permanently wealthier than the rest of the world, that gets less and less likely as time goes on."

[Robert Solow, Nobel Laureate in Economics]

PBCT

11

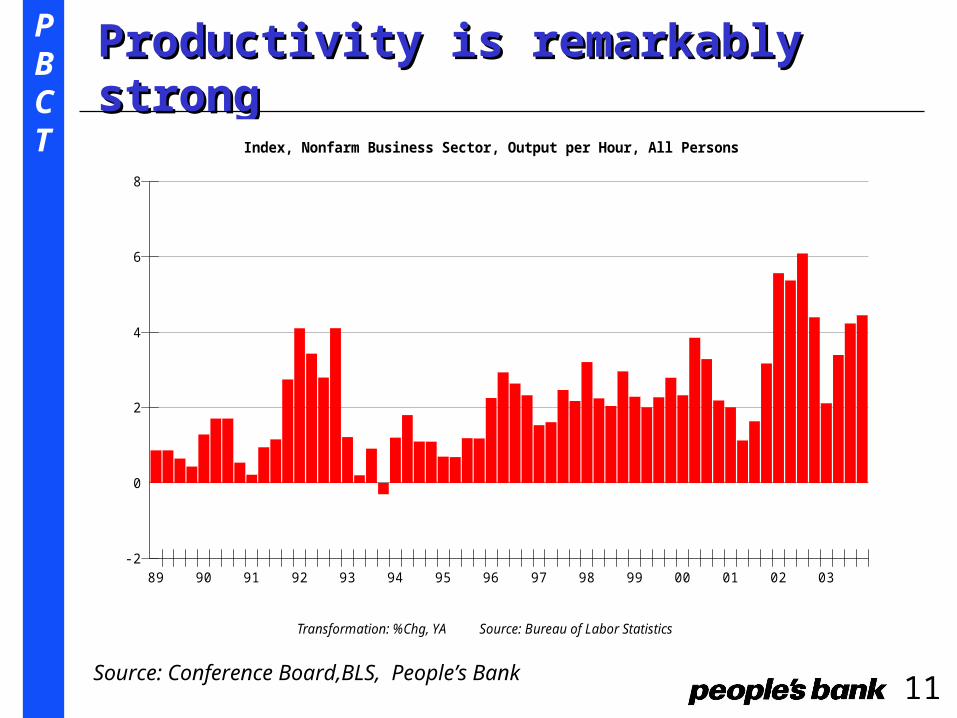

Productivity is remarkably strongProductivity is remarkably strong

Source: Conference Board,BLS, People’s Bank

Index, Nonfarm Business Sector, Output per Hour, All Persons

Transformation: %Chg, YA Source: Bureau of Labor Statistics

-2

0

2

4

6

8

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

PBCT

12

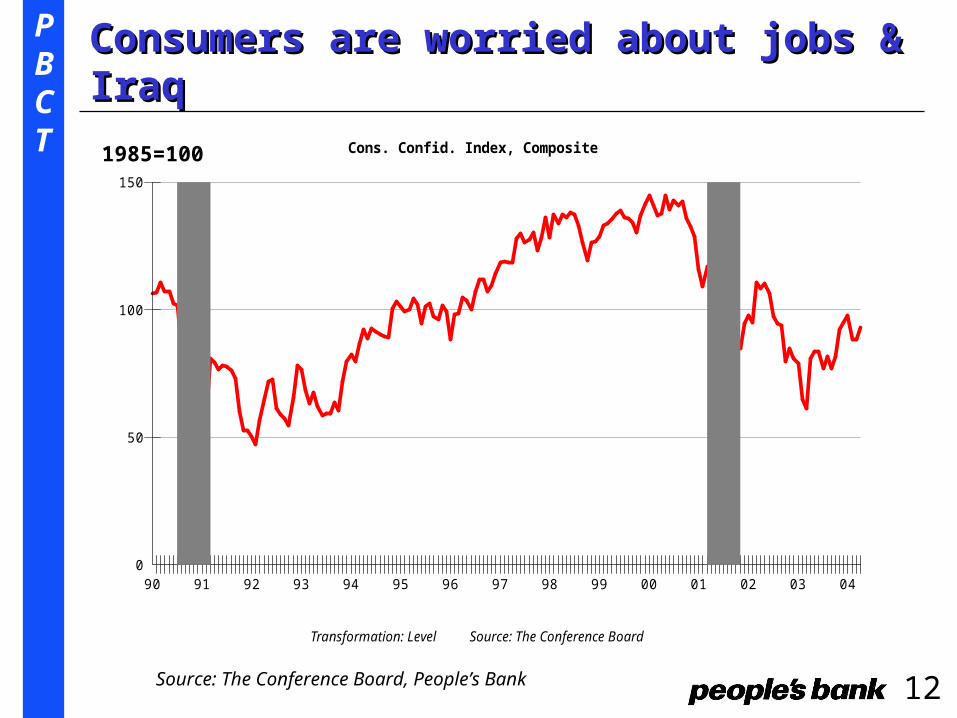

Consumers are worried about jobs & IraqConsumers are worried about jobs & Iraq

Source: The Conference Board, People’s Bank

Cons. Confid. Index, Composite

Transformation: Level Source: The Conference Board

0

50

100

150

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

1985=100

PBCT

13

Capital Spending has rebounded nicelyCapital Spending has rebounded nicely

Source: Conference Board,BEA, People’s Bank

Investment, Equipment and Software (CW$)

Transformation: %Chg, YA Source: Bureau of Economic Analysis

-5

-10

0

5

10

15

20

91 92 93 94 95 96 97 98 99 00 01 02 03 04

PBCT

14

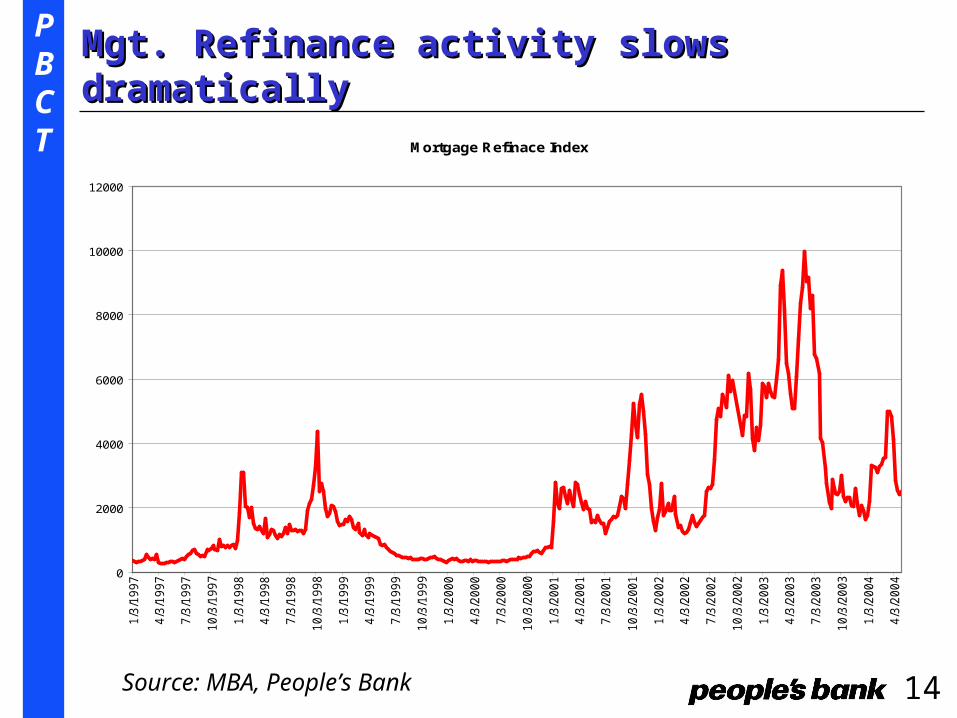

Mgt. Refinance activity slows dramaticallyMgt. Refinance activity slows dramatically

Source: MBA, People’s Bank

Mortgage Refinace Index

0

2000

4000

6000

8000

10000

12000

1/3

/19

97

4/3

/19

97

7/3

/19

97

10

/3/1

99

7

1/3

/19

98

4/3

/19

98

7/3

/19

98

10

/3/1

99

8

1/3

/19

99

4/3

/19

99

7/3

/19

99

10

/3/1

99

9

1/3

/20

00

4/3

/20

00

7/3

/20

00

10

/3/2

00

0

1/3

/20

01

4/3

/20

01

7/3

/20

01

10

/3/2

00

1

1/3

/20

02

4/3

/20

02

7/3

/20

02

10

/3/2

00

2

1/3

/20

03

4/3

/20

03

7/3

/20

03

10

/3/2

00

3

1/3

/20

04

4/3

/20

04

PBCT

15

Home sales are at record high levelsHome sales are at record high levels

Source: Conference Board, Bloomberg, People’s Bank

US New & Existing Home Sales - millions of units (SAAR)Housing Sales, New and Existing Homes

Transformation: Level Source: Bureau of the Census

3

4

5

6

7

8

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

PBCT

16

Housing affordability is still historically highHousing affordability is still historically high

Source: Conference Board, NAR, People’s Bank

Index, Housing Affordability

Transformation: Level Source: WEFA, NAR

100

110

120

130

140

150

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

PBCT

17

ISM index at a 20-year high - Strong orders ISM index at a 20-year high - Strong orders

Source: Conference Board, ISM, People’s Bank

Institute of Supply Management Survey (formally NAPM)Purchasing Managers' Index

Transformation: Level Source: NAPM

30

40

50

60

70

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

PBCT

18

Fed funds usually track nominal GDP growthFed funds usually track nominal GDP growth

Source: Conference Board, Bloomberg, People’s Bank

Targeted Fed Funds vs. Nominal GDP Growth (YOY%)

Nominal GDP Targeted Fed Funds

1

3

5

7

9

11

86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

PBCT

19

Targeted fed funds rate less nominal GDP growthTargeted fed funds rate less nominal GDP growth

Source: Conference Board, Bloomberg, People’s Bank

Fed Funds less Nominal GDP

Transformation: Level Source: N/A

-1

-2

-3

-4

-5

0

1

2

3

4

86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

The Gap has never been wider

PBCT

20

Core Inflation rate beginning to move higher?Core Inflation rate beginning to move higher?

Source: Conference Board, Bloomberg, People’s Bank

CPI vs. CPI less Food & Energy

CPI CPI less F&E

0

5

10

15

66 73 80 87 94 01

YOY% change “core” inflation rate the lowest since early 1960s, up just 1.1% YOY

PBCT

21

CT Economic OutlookCT Economic Outlook

• Connecticut’s Economy appears to be stabilizing, but a sustainable recovery is not yet evident in labor market.

• According to NEEP, state should add 8,200 jobs in 2004 and 22,000 in 2005. Unemployment rate will remain below national average.

• State’s economy is more diversified and performed much better than early 1990’s downturn. Manufacturing continues to be the hardest hit sector.

• Housing permits totaled 9,985 in 2003 -- the strongest since 1999. Not overbuilt like the late 1980s.

• CT vulnerable to national (and global) economy, stock market, energy prices, and deteriorating state fiscal condition.

PBCT

22

CT unemployment rate is well below the US rateCT unemployment rate is well below the US rate

Source: CT Labor Department

Unemployment Rate CT vs. US

Unemployment Rate CT Unemployment Rate US

2

4

6

8

10

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

% of labor force (SA)

PBCT

23

CT Job growth lags the US and is still neg. YOYCT Job growth lags the US and is still neg. YOY

Source: CT Labor Department, the Conference Board

% of labor force (SA)

CT vs. US Employment Growth YOY% change

CT Non-Farm Employment US Non Farm Employment

-1

-2

-3

-4

-5

0

1

2

3

4

5

6

83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

PBCT

24

CT has lost 62,000 jobs since July 2000 peakCT has lost 62,000 jobs since July 2000 peak

Source: CT Labor Department, the Conference Board

% of labor force (SA)

CT Non-Farm Employment

Transformation: Level Source: CT Labor Dept., User

1500

1550

1600

1650

1700

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

[Thousands]

PBCT

25

CT construction employment levels-offCT construction employment levels-off

Source: CT Labor Department, the Conference Board

Connecticut, Employment, Construction

Transformation: Level Source: Bureau of Labor Statistics

40

50

60

70

80

90

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02

[Thousands]

PBCT

26

CT Manufacturing has been the hardest hit sectorCT Manufacturing has been the hardest hit sector

Source: CT Labor Department, the Conference Board

Connecticut, Employment, Manufacturing

Transformation: Level Source: Bureau of Labor Statistics

150

181

212

243

274

305

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

[Thousands]

PBCT

27

CT Manufacturing still shedding 8,000 jobs a yearCT Manufacturing still shedding 8,000 jobs a year

Source: CT Labor Department, the Conference Board

Connecticut, Employment, Manufacturing

Transformation: Chg, YA Source: Bureau of Labor Statistics

-5

-10

-15

-20

0

5

10

91 92 93 94 95 96 97 98 99 00 01 02 03 04

[Change - Thousands]

PBCT

28

CT Service sector is where job growth has beenCT Service sector is where job growth has been

Source: CT Labor Department, the Conference Board

Connecticut, Employment, Services

Transformation: Level Source: Bureau of Labor Statistics

400.00

450.00

500.00

550.00

89 90 91 92 93 94 95 96 97 98 99 00 01 02

[Thousands]

PBCT

29

CT Claims are moving in the right directionCT Claims are moving in the right direction

Source: CT Labor Department

CT Average Weekly Initial Unemployment Claims

Transformation: Level Source: Ct Dept. of Labor, U, User

3000.00

4000.00

5000.00

6000.00

7000.00

8000.00

9000.00

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

PBCT

30

Unemployment rates up sharply from 2000 Unemployment rates up sharply from 2000

CT Unemployment Rates % by Labor Market Area (NSA)

3.3

3.5

3.7

4.7

4.9

5.0

5.6

5.7

6.1

6.8

1.1

1.3

1.3

1.9

1.5

2.0

2.0

2.3

2.3

2.3

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0

Stamford

Danbury

Lower River

New London

Torrington

New Haven

Hartford

Danielson

Bridgeport

Waterbury

8/31/2000

3/31/2004

Source: CT Labor Dept.

PBCT

31

CT Job losses across the board YOYCT Job losses across the board YOY

-3,000

-2,700

-1,600

-1,300

-1,200

-1,000

-900

-900

-700

-700

-600

-500

-400

-400

-300

-200

-200

-200-200

-3,500 -3,000 -2,500 -2,000 -1,500 -1,000 -500 0

Professional & Business Services

State Gov.

Machinery

Computer & Electronic Product

Transportation Equipment

Other Non-Durable Goods

Fabricated Metal

Information

Chemicals

Federal Gov.

Printing & Related

Food & Beverage Stores

Insurance

Local Gov.

Utilities

Electrical Equipment

Wholesale Trade

General Merchandise

Utilities

Change in CT Non-Farm Employment March 2004 vs. March 2003 ( Not SA)

Source: CT Labor Department

PBCT

32

Fewer industries adding jobs in CT YOYFewer industries adding jobs in CT YOY

200

200

300

400

400

400

400

500

1,000

1,000

1,900

2,600

0 500 1,000 1,500 2,000 2,500 3,000 3,500

Motor Vehicle & Parts Dealers

Other Retail

Securities & Commodity

Transportation & Warehousing

Credit Intermediation

Real Estate & Rental & Leasing

Other Services

Educational Services

Construction & Mining

Arts, Ent. & Recreation

Health Care & Social Assistance

Accommodation & Food Services

Change in CT Non-Farm Employment March 2004 vs. March 2003 ( Not SA)

Source: CT Labor Department

PBCT

33

Housing permits very strong so far in 2004Housing permits very strong so far in 2004

Source: CT DECD

% Change in CT New Housing Permits Authorized YTD January - March 2004 vs. 2002 by LMA

-25.0%

0.0%

7.8%

12.5%

18.0%

21.4%

45.1%

70.5%

128.2%

29.3%

29.7%

-50.0% 0.0% 50.0% 100.0% 150.0%

Lower River

New Haven

Stamford

Torrington

Hartford

Danielson

New London

Waterbury

Danbury

Bridgeport

Connecticut

Permits totaled 9,985 last year, the strongest since 1999 and the 3rd strongest since 1989. Total 2,176 YTD in 2004 vs. 1,683 in 2003.

PBCT

34

Housing is not overbuild like the mid-1980sHousing is not overbuild like the mid-1980s

Source:CT DECD, New England Economic Project

Total housing permits authorized in CT in units

16,9

27 19,3

92

26,2

46

30,1

63

27,4

15

19,5

47

11,9

70

7,58

0

7,48

0

8,01

0

9,25

0

9,46

0

8,55

0

8,53

7

9,31

1 11,8

63

10,6

37

9,37

6

9,29

0

9,73

1

9,98

5

8,65

8

8,62

0

8,77

0

8,66

2

0.0

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

35,000.0

2004-2007 is forecast

PBCT

35

Auto registrations down 4.4% YTDAuto registrations down 4.4% YTD

Source: CT Labor Department

Connecticut New Auto Registrations Processed YTD - (January - March)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,0001

98

0

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

PBCT

36

Tax revenues up 6.9% this yearTax revenues up 6.9% this year

Source: State of CT Dept. of Revenue Services

Year-to-Date % change in CT Tax Revenues ( FY 03-04 vs. FY 02-03 July - March)

-13.9%

2.6%

5.5%

6.9%

4.7%

15.1%

22.2%

-40.0% -30.0% -20.0% -10.0% 0.0% 10.0% 20.0% 30.0%

Corp. Business

Sales & Use

Real Estate Conv.

Motor Fuel

Income

Cigarette

Total Up $419 million

PBCT

37

SummarySummary• Economic growth continues to improve in 2004 due to: low rates - fiscal stimulus -

productivity - corporate profits - capital spending - weaker dollar

• Fed’s “Patience” is coming to and end – tightening of monetary policy should begin by August 2004.

• Connecticut economic growth has lagged the US - meaningful job growth not likely until 2005 - Higher taxes, higher costs, impeachment hearings are not helping recovery

• Watch: Jobless Claims - employment - purchasing managers’ index - oil prices - home prices - consumer confidence

• Risks: Companies don’t hire - Iraq & Middle East - nasty election year - more terrorist attacks - higher oil prices - stock correction - deficits

PBCT

38

For more information...For more information...

Please visit our web site at www.peoples.com