“past, present & future developments in the rare earth...

TRANSCRIPT

byDudley J Kingsnorth

Industrial Minerals Company of Australia Pty Ltd

BBY Rare Earths ConferenceApril 2011

“Rare Earth Opportunities - Real or Imaginary?”

IMCOA

DISCLAIMER

2

The statements in this presentation represent the considered views of theIndustrial Minerals Company of Australia Pty Ltd (IMCOA). It includes certainstatements that may be deemed "forward-looking statements." All statements inthis presentation, other than statements of historical facts, that address futuremarket developments, government actions and events, are forward-lookingstatements. Although IMCOA believes the outcomes expressed in such forward-looking statements are based on reasonable assumptions, such statements arenot guarantees of future performance and actual results or developments maydiffer materially from those in forward-looking statements. Factors that couldcause actual results to differ materially from those in forward-looking statementsinclude new rare earth applications, the development of economic rare earthsubstitutes and general economic, market or business conditions.While, IMCOA has made every reasonable effort to ensure the veracity of theinformation presented it cannot expressly guarantee the accuracy and reliability ofthe estimates, forecasts and conclusions contained herein. Accordingly, thestatements in the presentation should be used for general guidance only.

IMCOA

DisclosureDudley J. Kingsnorth, through the Industrial Minerals Company of Australia Pty Ltd (“IMCOA”) provides rare earths market and project development advice to Molycorp Minerals, LLC (owners of the Mountain Pass Project), Alkane Resources Ltd (owners of the Dubbo Zirconia Project), Rare Element Resources (owners of the Bear Lodge Project) and Northern Minerals Ltd (owners of the John Galt Project and the Browns Range Project). He consults to other rare earths companies on an occasional basis. This advice is provided on a fee for service basis; with no success or promotional fees or obligations. The are Confidentiality Agreements in place with these companies, but this does not preclude comment on public information.

Dudley J. Kingsnorth is a Non-Executive Director of Northern Minerals Ltd.

IMCOA owns securities in Alkane Resources Ltd and Northern Minerals Ltd.

3

IMCOA

Summary of Presentation

4

The “Line in the Sand”The rare earths industry todayThe last 12-18 monthsChinaPresent and future demand and supply

4

IMCOA

The Line in the SandIn September 2010 when China ‘temporarily suspended shipments’ of rare earths to Japan –to support a territorial dispute - it marked the drawing of a line in the sand.The ROW now recognises that it can no longer depend on China as a long term reliable supplier of rare earths.By 2020 the ROW could be self-sufficient in the supply of rare earths – if adequate sources of ‘heavy rare’ earths can be developed.

5

IMCOA

The OpportunitiesBetween 2010 and 2014 Rest-of-World (ROW) rare earths production will increase tenfold – from 4-6,000tpa REO to 40-60,000tpa REO.Between 2010 and 2015 ROW demand will grow from 52,500tpa REO to 75,000tpa REO.Forecast global demand in 2020 is 250-300,000 tpa REOForecast ROW demand in 2020 is 100-130,000tpa REO; so, there is an opportunity for ROW producers to triple production between 2014 and 2020 to meet ROW demand

6

IMCOA

The Rare Earths Market Today

7

Estimated demand in 2010: 125,000t REO

Prices: Early 2010 US$11-13/kg; Now US$80-120/kg REO

China is dominant (supplying 95% and consuming 60% of global supply/demand)

Constraints on Chinese production and exports are creating opportunities for non-Chinese projects

Two major non-Chinese rare earths projects are under construction

Many non-Chinese projects (~200) are being evaluated

7

IMCOA

Rare Earths – Development Concepts

8

Each orebody is different; so the process route is project specificAll rare earths orebodies have U and Th associated with them; requiring safe disposalPilot plant studies (for non-Chinese projects) essential to:

Demonstrate technical viabilityGenerate samples for customer approval as basis for sales contractsProvide data for bankable feasibility studyGenerate data for environmental impact statement

From Resource to BFS can take 5-12 years

IMCOA

China: RE Export Transition

9

1970s: Rare earth mineral concentrates.

1980s: Mixed rare earth chemical concentrates.

Early 1990s: Separated rare earth oxides and metals.

Late 1990s: Magnets, phosphors, polishing powders.

2000s: Electric motors, computers, batteries, LCDs, mobile phones.

9

IMCOA

China: Export Quota History

10

Chinese Export Quota History 2005-2011 (Tonnes Product)

YearRare Earth Quotas ROW

DemandDomestic

CompaniesForeign

CompaniesTotal Change

2005 48,040t 17,659t 65,609t 0% 46,000t

2006 45,752t 16,069t 61,821t -6% 50,000t

2007 43,574t 16,069t 59,643t -4% 50,000t

2008 Actual: 34,156tAdjusted: 40,987t*

Actual:13,293tAdjusted: 15,834t*

Actual: 47,449tAdjusted: 56,939t* -5½%* 50,000t

2009 33,300t 16,845t 50,145t -12% 25,000t

2010 22,512t 7,746t 30,258t -40% 55,000t

1H2011 10,762t 3,648t 14,446t -5% 60,000tNote: * Quotas adjusted to an equivalent 12 month quota as there was a change in the dates for which they were issued; so that now they are for a calendar year

IMCOA

China: Industry Constraints

11

Export quotas – recent reduction of 40%

Production quotas – HREE reserves limited

Export taxes: 15-25%

VAT rebate on exports withdrawn

“Co-ordinated pricing”

Industry consolidation

Environmental legislation enforced

Lack of Transparency

11

IMCOA

China has Adequate Rare Earths Resources to Meet its Own NeedsReserves of 30-50 million tonnes REO.Processing capacity of 200-250,000 tpa REO, of which 50-55% is idle for either environmental and/or economic reasons, but ‘available’ for purchase.The SOEs charged with consolidating the industry have all announced large capital investments.Fujian has announced a US$920M investment.China’s priority is maintaining employment.The focus should be: ROW suppliers to meet ROW demand – lots of opportunity.

12

IMCOA

The Last 18-24 Months

13

The ‘Line in the Sand’.Chinese export quotas reduced significantlyGlobal financial crisis (Growth set back 2 years)

China declares ‘heavy’ rare earths resources are finite (approximately 15 years)

Chinese rare earths industry consolidationMt Weld & Mountain Pass to rapidly move to 20,000tpa & 40,000tpa REO respectively.The earthquake and tsunami to hit Japan

13

IMCOA

Rare Earths Supply & Demand

14

Source: IMCOA, Roskill, CREIC, Discussions with Rare Earths Industry Stakeholders

14

IMCOA

The Issue of ‘Balance’ in 2015

Forecast Supply and Demand for Selected Rare Earths in 2015

Rare Earth OxideDemand @

180-190,000tpa REOSupply @

195-210,000tpa REO

Cerium 65-70,000t REO 75-80,000t REO

Lanthanum 45-50,000t REO 50-55,000t REO

Neodymium 35-40,000t REO 30-35,000t REO

Terbium 450-500t REO 400-450t REO

Dysprosium 2,750-3,000t REO 1,750-2,000t REO

15

IMCOA

Rare Earths Prices 1Q2008 - 11Comparison of Selected Rare Earths Prices US$/kg REO 2005-10

(Notes: 1.Source is metal pages© 2. Prices have been rounded 3. US$1.00 = C¥6.65 to 6.85)

Rare Earths Product

Rare Earths Price FOB China Rare Earths Price

FOB China 24/3/111Q2008 1Q2009 1Q2010 1Q2011

Lanthanum Oxide US$5.50 US$7.00 US$5.75 US$75 US$95

Cerium Oxide US$3.75 US$4.50 US$4.15 US$77 US$96

Praseodymium Oxide US$31.00 US$14.25 US$26.00 US$117 US$155

Neodymium Oxide US$31.00 US$14.25 US$26.50 US$125 US$170

Europium Oxide US$425 US$435 US$490 US$725 US$820

Dysprosium Oxide US$105 US$92½ US$140 US$405 US$520

Terbium Oxide US$700 US$360 US$405 US$690 US$830

Yttrium Oxide US$13.50 US$15.25 US$10.50 US$95 US$125

16

IMCOA

The Outlook to 2015

17

China will not directly deny rare earths to the ROW; but it will take whatever measures are necessary to maximise ‘value add’ manufacturing (job retention) in China.

Chinese constraints could constrain global growth.

Supply will be tight.

‘Balance’ will still be an issue; so prices for Nd, Eu, Dy, and Tb will remain strong..

First of new projects will be on-stream and looking to expand.

Next generation projects could be in early stages of start up.

17

IMCOA

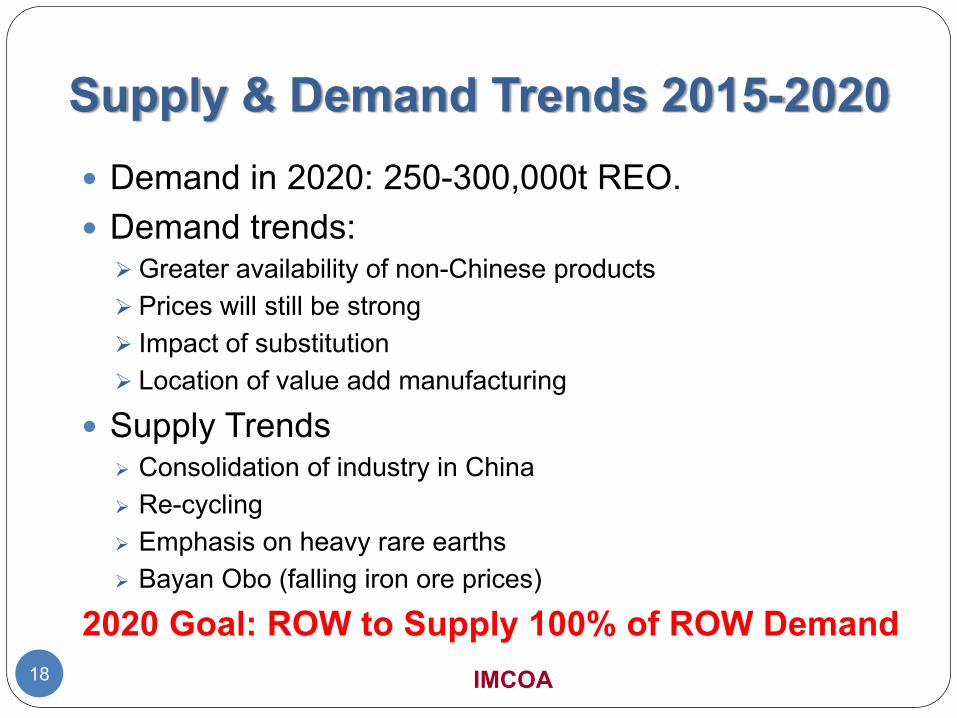

Supply & Demand Trends 2015-2020Demand in 2020: 250-300,000t REO.Demand trends:

Greater availability of non-Chinese productsPrices will still be strongImpact of substitutionLocation of value add manufacturing

Supply TrendsConsolidation of industry in ChinaRe-cyclingEmphasis on heavy rare earthsBayan Obo (falling iron ore prices)

2020 Goal: ROW to Supply 100% of ROW Demand18

IMCOA

Reality and Imagination

The opportunities to supply ROW rare earths demand through to 2020 are real.The project development schedules proposed by many prospective suppliers rely more upon imagination than reality

19

Dudley J Kingsnorth

Industrial Minerals Company of Australia Pty Ltd

Thank you