part iv adding - textbook media · capital budgeting chapter 12 investing in permanent working...

TRANSCRIPT

Chapter 11Capital Budgeting

Chapter 12Investing in PermanentWorking Capital Assets

Chapter 13Improving Financial Processes

Chapter 14Selecting the Best

Debt-Equity Mix

Chapter 15Managing Risk

261

In Part IV we look at how financial managers can add value to their firms.

Chapter 11 examines capital budgeting, selecting value-adding invest-ments in long-term assets. We identify the data that should enter theanalysis and then demonstrate how to organize and analyze the data.

Chapter 12 shows how the techniques of capital budgeting can beadapted to the analysis of investments in permanent current assets, thebase level of a firm’s current resources. We illustrate this process withdecisions involving the firm’s balances of cash and accounts receivable.

Chapter 13 explores financial processes, the day-to-day work of financialmanaging. We define and identify the nature and functioning of theseprocesses and show how their performance is measured. Then we dis-cuss how financial processes can be improved and give examples of sig-nificant financial process improvement.

Chapter 14 discusses leverage and the optimal mix of debt vs. equity fi-nancing. We review why a firm’s financing choice might affect its value.We describe four theories that attempt to explain the optimal debt-equitymix and look at practical approaches to the financing mix decision.

Chapter 15 is devoted to risk management. After introducing hedging andshowing how it can be used to reduce financial risks, we describe thefour-step sequence of making working capital decisions and apply hedg-ing to two of the four steps.

PART IV

ADDING

VALUE

CHAPTER 11

CAPITAL

BUDGETING

Rick Daniel stared at the computer screen and shook his head. Thenumbers did not seem to make sense. How could an investment with

such obvious potential have such a low value?

Rick was an analyst in the corporate finance group of a large corporation. Hehad been assigned the task of evaluating the proposed purchase of a new kindof machinery which promised to reduce dramatically the cost of producing thecompany’s highest-volume product. From his classes in finance, Rick knew thatthe proper method of analysis began with a complete summary of the incre-mental cash flows from accepting the project. But when he put the numbersinto his spreadsheet program, the resulting calculations did not seem to be atall correct.

Puzzled, Rick printed out his spreadsheet and took the page to one of thegroup’s senior analysts for advice. The analyst first looked at Rick’s mathemat-ics. Next, the analyst questioned Rick about his assumptions: where the num-bers came from and how Rick had decided which numbers to include in theanalysis. Rick took notes as he answered each question.

When he returned to his desk, Rick reviewed his notes. He had written a list ofleads to follow up—leads that could improve his numbers and analysis. As hebegan to prioritize his follow-up actions, Rick thought back to his introductory fi-

nance course and realized that it was time to do a thorough review of the ba-sics of capital budgeting.

A key part of the job of financial managing is to advise senior management ofthe value of potential uses of the firm’s money. One important use is invest-ment in long-term plant and equipment, the resources economists call a firm’s“capital.” As Rick Daniel is rediscovering, understanding whether a proposedcapital expenditure is wise requires careful attention to researching and analyz-ing every consequence of the proposed change.

Finance as a discipline has been a pioneer in developing techniques for theanalysis of long-term investment alternatives. Yet financial people have beenwidely blamed for many companies’ lack of attention to long-term investment.While this may seem contradictory, there is much truth to both observations.Poor application of finance theory can easily lead to poor managerial judg-ments. In this chapter we will explore the methodology of evaluating invest-ment projects as well as the pitfalls that can lead to myopic, short-term decisionmaking.

Key Points You Should Learn from This Chapter

After reading this chapter you should be able to:�� Discuss the importance of capital budgeting to business success.�� Identify the data used in capital budgeting.�� Organize cash flow data for capital budgeting analysis.�� Use the techniques of net present value (NPV) and internal rate of return (IRR)

to judge the worth of a capital project.

263

Introductory Concepts—The Importance of Capital Budgeting

Capital budgeting is the widely used term for the process of evaluating poten-tial investments in long-term assets. The cash budget (presented in Web Appen-dix 5B) is the projection of the firm’s day-to-day—or at least month-to-month—cash flow needs for the next year. Here we look at the capital budget, the paral-lel plan for spending money to acquire long-term resources.

Capital budgeting is important to any firm that makes significant use of plant andequipment, land, and other long-term assets. For one thing, long-term assets maymake up 50% or more of the total assets of a company. Thus, capital budgetingmay be the technique used to qualify the acquisition of a large amount of the firm’s resources. Second, the decision to acquire—or not to acquire—capital re-sources has a major impact on the financing of the firm. Expenditures on assetsrequire the company to make parallel and integrated decisions about where andin what form to raise funds. In addition, the effects of capital budgeting decisionsstay with the firm for a long time. The wise acquisition of long-term assets canoften be the difference between a business that is competitively strong, with op-portunities for growth and market penetration, and a business that is weak anduncompetitive.

Even for the financial manager of a firm with little investment in capital assets,capital budgeting is an important technique to know and use well. As we will seein subsequent chapters, the techniques of capital budgeting are not only applica-ble to long-term asset decisions, they can be easily extended to deal with many

264 Part IV Adding Value

capital budgeting—theprocess of discovering,evaluating, and decidingwhether to pursueinvestments in long-termassets

capital budget—a financialplan showing a firm’sintended outlays for long-term assets

ManufacturingReturns to theUnited States

In May 2011, Yamaha Motor Corporation, the large Japanese manufacturer of musi-cal instruments, audio products, semiconductors, and sports vehicles, announced thatit would be shifting production of some all terrain vehicles (ATVs) from Japan to aplant in Georgia, the first step in eventually transferring the majority of the company’sworldwide ATV manufacturing to the United States by 2013.

Throughout the 1990s and 2000s, the United States lost manufacturing jobs as manycompanies outsourced production to countries where labor was much cheaper than inthe U.S., particularly China. However, China’s rapid emergence as a developing na-tion has led to elevated living standards and increased wages making manufacturingthere more expensive. China’s growing purchasing power is also increasing the valueof its currency, the Yuan, further adding to the cost of doing business there. And, atthe same time, the recent recession has resulted in greater labor flexibility and lowerwage rates in the United States.

“If the trend plays out, I think you’ll see manufacturing growing and expanding in theU.S.,” says Michael Zinser, one of the authors of a 2011 Boston Consulting Groupstudy of international manufacturing. “China is no longer expected to be the defaultlow-cost manufacturing location for those companies who are looking to supply theU.S. market. As a result of the changing economics, you’re going to see a lot moreproducts ‘Made in th USA’ in the next five years.”

Reference : PRN/Newswire, Yamaha Motor Corp., U.S.A. press release, May 18,2011; BenForer, “Manufacturing in America: US Set for a ‘Manufacturing Renaissance’,” ABC News/Money, May 13, 2011.

FINANCE IN PRACTICE

choices affecting current assets as well. In addition, the logic we develop in thischapter is of considerable use in other, nontraditional, areas where finance-trainedpeople are becoming more frequently involved. Often, when working with a teamdrawn from throughout the organization, the incremental thinking of this chap-ter is the finance person’s greatest contribution.

�� Identification of Data

To make sound capital budgeting decisions, it is necessary to keep eight data rulesin mind. The first seven identify numbers to include in the analysis and the lastspecifies what to exclude: (1) Use cash flow numbers only. (2) Use incrementalnumbers only. (3) Include changes in every functional area of the business. (4) In-clude changes across the full life cycle of the product or service. (5) Include fore-casted inflation in the cash flow estimates. (6) Consider the impact of the decisionon quality and sustainability. (7) Consider the options implicit in the decision.(8) Do not contaminate the numbers with the firm’s financing flows.

1. Use Cash Flow Numbers Only

Since financial value comes from cash flows, it is important to measure the im-pact of a decision in cash flow terms. In particular, we avoid accounting revenueand expense numbers. The amount and timing of these figures are highly de-pendent on financial accounting rules which are made by people and change fromtime to time. There are alternative treatments for a single event within financialaccounting; as a result, the same economic event can be described in several dif-ferent ways. By concentrating on cash flows, we avoid the risk of distorting busi-ness decisions because of the selection among accounting alternatives.

Financial accounting might require the business to recognize income at one pointin time, even though the associated cash flows take place over a much longer pe-riod. Alternatively, the financial statements might spread revenues or expensesover several time periods even though the cash flow was received or paid in onelump sum. Perhaps the most common example is depreciation expense:

Chapter 11 Capital Budgeting 265

Using Cash Flow and Not Depreciation ExpenseExample

Three companies are considering the purchase of the identical machine for$100,000. All three would depreciate it over five years to zero salvage value ontheir financial statements; but Company A would use straight-line deprecia-tion, Company B would use sum-of-the-years-digits depreciation, and Com-pany C would use double-declining-balance depreciation.

Question: What figure should each firm use in its capital budgeting analysisfor the cost of the machine?

Answer: All three should use the same number: $100,000 at the date of pur-chase. This is the cash they must give up to acquire the machine. The dif-ferences between the three depreciation conventions are arbitrary and havenothing to do with the cost of the asset.

Using Activity-Based and Not Local NumbersExample

A firm is considering a change to its product which would reduce productioncosts by $0.50 per unit but add $0.75 per unit to warranty service costs.

Question: Which figure should the firm use in its capital budgeting analysisfor the per-unit cash flow change?

Answer: �$0.25 per unit ($0.50 � 0.75). While the impact on warranty ser-vice costs may not be immediately visible to those who attempt to lowerproduction costs, its impact is real. It doesn’t pay to save $0.50 in the fac-tory only to lose $0.75 in the service department.

2. Use Incremental Numbers Only

As we discussed in the opening pages to this part of the book, incremental deci-sions are made by ignoring cash flows that do not change with the decision. Onetype of cash flow that cannot change with the decision, and therefore is a goodexample of a number that should not be included in capital budgeting analysis,is a sunk cost—a cash flow that took place in the past.

266 Part IV Adding Value

3. Include Changes in Every Functional Areaof the Business

Capital budgeting projects can change cash flows throughout the business. Whilesome changes will be obvious, others may be quite subtle and not immediatelyvisible. Traditional cost accounting—grouping costs by functional area, cost cen-ter, profit center, etc.—is often inadequate to point out the financial interconnec-tions throughout the organization. The analyst must adopt an activity-based ap-proach, searching across all functional areas of the firm for cash flows that willchange. Not to do so would be to miss some of the incremental cash flows fromaccepting the proposal.

Using Incremental Numbers and Not Sunk CostsExample

A firm has spent $10 million over the years to purchase plant and equipment.It is presently considering a proposal to spend $100,000 for another machine.

Question: Which figure should the firm use in its capital budgeting analysisfor the cost of the machine?

Answer: $100,000. The decision to purchase the new machine involves thisamount only. The $10 million is a sunk cost and cannot be changed by say-ing yes or no to the purchase of the new machine.

4. Include Changes Across the Full Life Cycleof the Product or Service

Just as financial analysts must search across all functional areas of the firm, so toomust they examine the entire life span of the activity for which a change is pro-posed. Traditional cost accounting often fails to provide sufficient information due

to its focus on period-by-period reporting. The analyst must adopt a life-cycleapproach considering all changes which might occur during the life span of theactivity to be altered. Not to do so would be to miss some of the incremental cashflows from accepting the proposal.

Chapter 11 Capital Budgeting 267

5. Include Forecasted Inflation in the CashFlow Estimates

Inflation can create a tangible change to cash flows. If left out, future cash flowestimates will tend to be understated.

While the example below illustrates including inflation in revenue forecasts, it islikely that the company’s costs for the new product will increase as well due tothe same inflationary forces. The impact of inflation must be included in all cashflow projections, whether they are forecasts of inflows or outflows.

Using Life-Cycle and Not Single-Period NumbersExample

A firm is considering a change that would reduce production costs by $2.00per unit but result in production machinery wearing out faster: new machin-ery would have to be purchased in three years instead of five.

Question: Which figure should the firm use in its capital budgeting analysisfor the cash flow change?

Answer: A figure that includes both the $2.00 and the cost to replace the ma-chinery earlier. While the replacement of machinery is still in the future, theearlier replacement date translates into a more costly expenditure when timevalue of money is taken into account. The two effects must be balancedagainst one another.

"It may not be the best investment decision, but hey, we won't know for three years and I just got promoted to the L.A. office."

life-cycle numbers—numbers which cover thefull life-span of someactivity and which are notlimited to any time period

© 2006 by Eric Werner. All rights reserved.

6. Consider the Impact of the Decision onQuality and Sustainability

Capital budgeting proposals that affect the quality of a firm’s products and ser-vices or the risks and/or opportunities from sustainability, will typically result inchanges to cash flows well beyond what is immediately apparent. These quality-and sustainability-related cash flows can easily be large and far outweigh the ob-vious cash flow changes. An estimate of them must be included in the analysis.

268 Part IV Adding Value

Using Nominal and Not Real NumbersExample

A firm is considering whether to market a new product. It expects to sell 500units of the product in each of the next three years. It would price the productat $1,000 per unit in the coming year. Inflation is forecasted to be 8% per yearfor each succeeding year, and management believes it could increase its priceswith the general level of prices over that period.

Question: Which figures should the firm use in its capital budgeting analy-sis for receipts from the sale of the new product?

Solution steps: Year 1: Receipts � 500 units � $1,000 � $500,000Year 2: Price � $1,000 (1.08) � $1,080Year 1: Receipts � 500 units � $1,080 � $540,000Year 3: Price � $1,080 (1.08) � $1,166Year 1: Receipts � 500 units � $1,166 � $583,000

Answer: $500,000 for the first year, then $540,000, then $583,000. The eco-nomic environment will allow the firm to increase its prices which will bringin additional cash flow. Ignoring inflation and using $500,000 for each year’sreceipts would understate the benefits from this product.

Including Quality- and Sustainability-Related Cash FlowsExample

A firm is considering the installation of new energy-efficient lighting in its re-tail stores. The team working on the project has researched the cost of instal-lation and savings from the more efficient bulbs. Beyond the hard numbers,there is a shared feeling among the team members that the new lighting willbetter show off the merchandise and communicate the firm’s commitment tosustainability, and this will lead to increased customer satisfaction, hence gen-erate more repeat sales and attract new customers.

Question: Which figures should be used in the capital budgeting analysis?

Answer: The analysis must include an estimate of the quality- and sustain-ability-related benefits as well as the cost of the lighting. Increased saleswould produce new cash inflows which should not be ignored. Further, ifthe system were not installed, the firm might lose customers; a second in-cremental benefit of the new system is retaining the business of those cus-tomers who might otherwise go elsewhere. To estimate the value of newsales and existing customers retained, the analysts might interview mem-bers of the company’s sales and marketing staff. They might also interviewmembers of other companies that have installed similar lighting systems.

Chapter 11 Capital Budgeting 269

7. Consider the Options You Get if You Makethe Decision

Capital budgeting proposals are often rejected because the future benefits fromthe investment are not easily quantifiable. This is especially true in research anddevelopment, where it is difficult to know what products or services will emergefrom the R&D or what the marketplace will look like in the future. Yet if a firmrejects all such R&D efforts while its competitors push ahead, it could find itselfat a severe disadvantage in the future.

One way to deal with this dilemma is to view accepting investments whose re-turns are speculative as the equivalent of purchasing a call option.1 The firmspends some amount today (the option premium) to develop its knowledge, tech-nology, expertise, etc., in return for the right (capability) to enter the market atsome future date.

8. Do Not Contaminate the Numbers of AnyOne Project with the Firm’s FinancingFlows

The techniques for evaluating capital budgeting projects (discussed later in thischapter) test each potential investment against the firm’s cost of capital. Since therole of the cost of capital is to bring the company’s financing cash flows into thedecision, we exclude financing flows from the description of the investment pro-ject itself. Otherwise we would be “double-counting,” incorporating the financ-ing flows twice.

FINANCE IN PRACTICE

Real Options andClimate Change

One of the difficulties of reacting to climate change is the uncertainty surrounding theway it will affect any particular ecosystem. In 2010, a team of analysts from theWorld Bank evaluating development efforts in Vietnam found that the incorporation ofreal options analysis into local investment decisions could lead to significantly betterchoices.

The team looked at investments in houses, dykes, and community shelters in areassubject to floods and cyclones, weather events whose frequency and severity are af-fected by climate change. They discovered that each investment contained real op-tions since the structures could be adapted to meet future climate conditions. By in-corporating the value of these options into their analyses, the team was able torecommend more flexible designs that could be constructed initially at a lower costthan originally planned and could be modified at a later date should future weatherconditions warrant.

Reference: Leo Dobes, “Notes on applying ‘real options’ to climate change adaptation mea-sures, with examples from Vietnam,” Centre for Climate Economics & Policy working paper,The Australian National University, November 2010.

1 Cross-reference: Options are discussed in Web Appendixes 6D and 9B. The option valuation modelcan be used in capital budgeting to calculate the present value of future benefits where managementexpects at some future date to have the choice to proceed or terminate the investment.

270 Part IV Adding Value

Omitting Financing Flows from the Description of theInvestment Project

Example

A firm is considering an investment project which would cost $100 today andreturn $115 in exactly one year. It will finance the project with capital costing10% (it will cost $10, due in one year, to finance the $100 investment).

Question: Should the $10 financing cost be included in the project’s cashflows?

Answer: No! The cost of capital does not enter the analysis at this stage. Donot deduct the $10 financing cost from the $115 to produce a $105 net re-turn. Since the next step in evaluating the project will be to test its cash flowsagainst the firm’s 10% cost of capital, deducting the $10 would result in us-ing the 10% number twice in the analysis.

�� Organizing the Data

In the remainder of this chapter we will use cash flow spreadsheets to organizethe data for each capital budgeting problem. This is the same approach we usedwhen we calculated the cost of each source of capital in Chapter 10. Recall thatour spreadsheet summarizes cash flows by the date they are forecasted to occur,making it easy to do the required time value of money calculations.

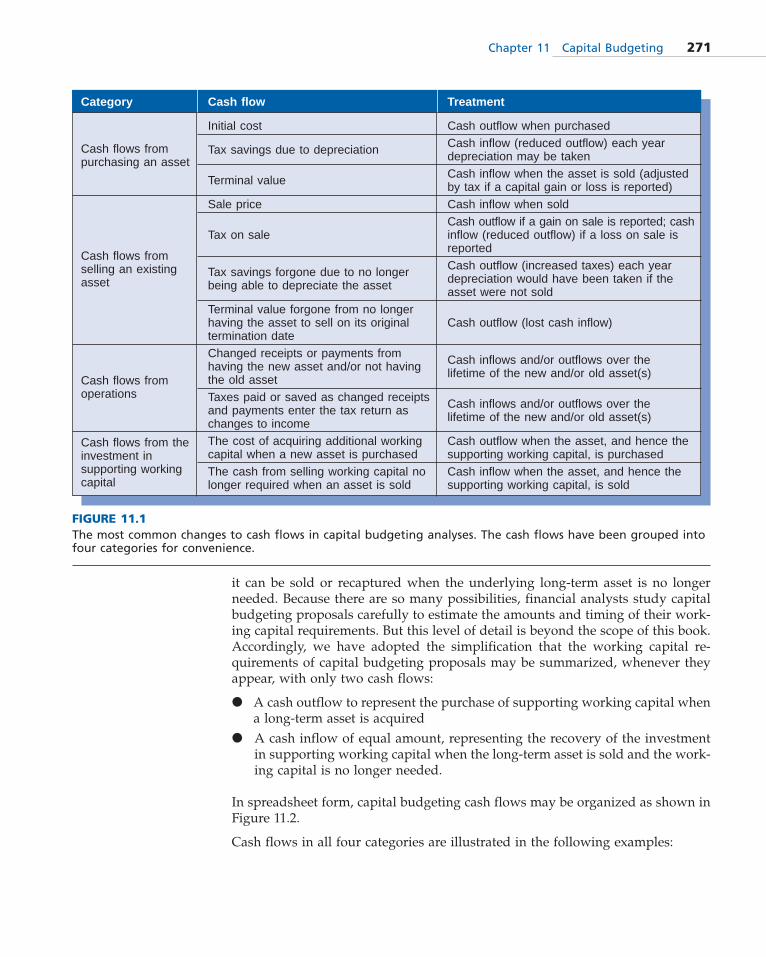

The cash flows most often changed by capital budgeting decisions can be conve-niently grouped into four categories: cash flows from (1) purchasing a new asset,(2) selling an existing asset, (3) changes in operations resulting from the asset pur-chase and/or sale, and (4) changes in the working capital required to support anew asset or no longer required when an asset is sold. These categories are sum-marized in Figure 11.1.

Some of Figure 11.1 is self-explanatory—for example, the first line which identi-fies the cash outflow when a new asset is purchased. Other cash flow treatmentsrequire an understanding of basic accounting and tax rules—for example the cal-culation of the tax impact of changes to depreciation expense.2 The last category—changes to supporting working capital—might require a bit more explanation. Of-ten an investment in long-term assets triggers an accompanying change in relatedcurrent assets (different inventory levels, changed receivable levels if sales is pro-jected to change, etc.). These working capital changes involve cash flows and mustbe included in the capital budgeting analysis. However, there is no standard pat-tern for these flows. Sometimes the additional working capital must be acquiredalong with the long-term asset—for example, an inventory of spare parts for anew machine. At other times, working capital is added in increments over thelong-term asset’s life—for example, additional accounts receivable as a new plantproduces sales growth over time. On occasion, the new working capital becomesa permanent part of the company’s resources; while in other cases, some or all of

2 Cross-reference and recommendation: Depreciation for corporate tax returns is done using theMACRS (modified accelerated cost recovery system) as described in Web Appendix 2E. The samerules apply to business assets owned by proprietorships and partnerships. See your accounting text-book if you desire further review of depreciation or of other accounting calculations such as the gainor loss when an asset is sold.

Category Cash flow Treatment

Initial cost Cash outflow when purchased

Tax savings due to depreciation Cash inflow (reduced outflow) each yeardepreciation may be takenCash inflow when the asset is sold (adjustedTerminal value by tax if a capital gain or loss is reported)

Sale price Cash inflow when soldCash outflow if a gain on sale is reported; cash

Tax on sale inflow (reduced outflow) if a loss on sale isreportedCash outflow (increased taxes) each yearTax savings forgone due to no longer depreciation would have been taken if thebeing able to depreciate the asset asset were not sold

Terminal value forgone from no longerhaving the asset to sell on its original Cash outflow (lost cash inflow)termination dateChanged receipts or payments from Cash inflows and/or outflows over thehaving the new asset and/or not having lifetime of the new and/or old asset(s)the old assetTaxes paid or saved as changed receipts Cash inflows and/or outflows over theand payments enter the tax return as lifetime of the new and/or old asset(s)changes to incomeThe cost of acquiring additional working Cash outflow when the asset, and hence thecapital when a new asset is purchased supporting working capital, is purchasedThe cash from selling working capital no Cash inflow when the asset, and hence thelonger required when an asset is sold supporting working capital, is sold

it can be sold or recaptured when the underlying long-term asset is no longerneeded. Because there are so many possibilities, financial analysts study capitalbudgeting proposals carefully to estimate the amounts and timing of their work-ing capital requirements. But this level of detail is beyond the scope of this book.Accordingly, we have adopted the simplification that the working capital re-quirements of capital budgeting proposals may be summarized, whenever theyappear, with only two cash flows:

� A cash outflow to represent the purchase of supporting working capital whena long-term asset is acquired

� A cash inflow of equal amount, representing the recovery of the investmentin supporting working capital when the long-term asset is sold and the work-ing capital is no longer needed.

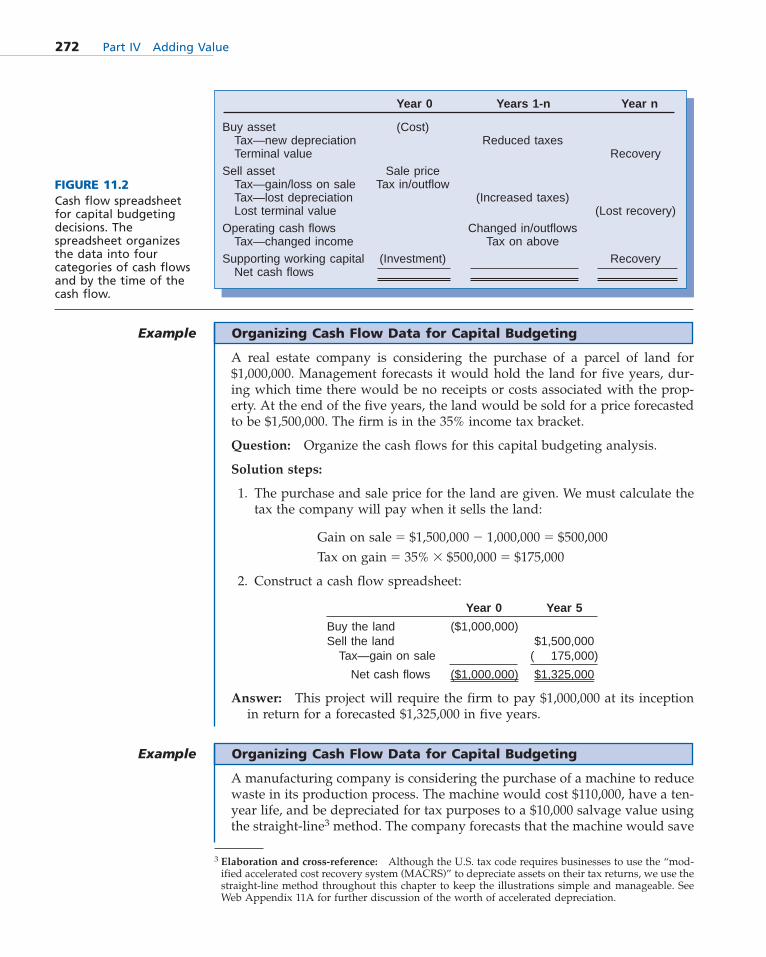

In spreadsheet form, capital budgeting cash flows may be organized as shown inFigure 11.2.

Cash flows in all four categories are illustrated in the following examples:

Chapter 11 Capital Budgeting 271

FIGURE 11.1The most common changes to cash flows in capital budgeting analyses. The cash flows have been grouped intofour categories for convenience.

Cash flows fromselling an existingasset

Cash flows fromoperations

Cash flows from theinvestment insupporting workingcapital

Cash flows frompurchasing an asset

272 Part IV Adding Value

FIGURE 11.2Cash flow spreadsheetfor capital budgetingdecisions. Thespreadsheet organizesthe data into fourcategories of cash flowsand by the time of thecash flow.

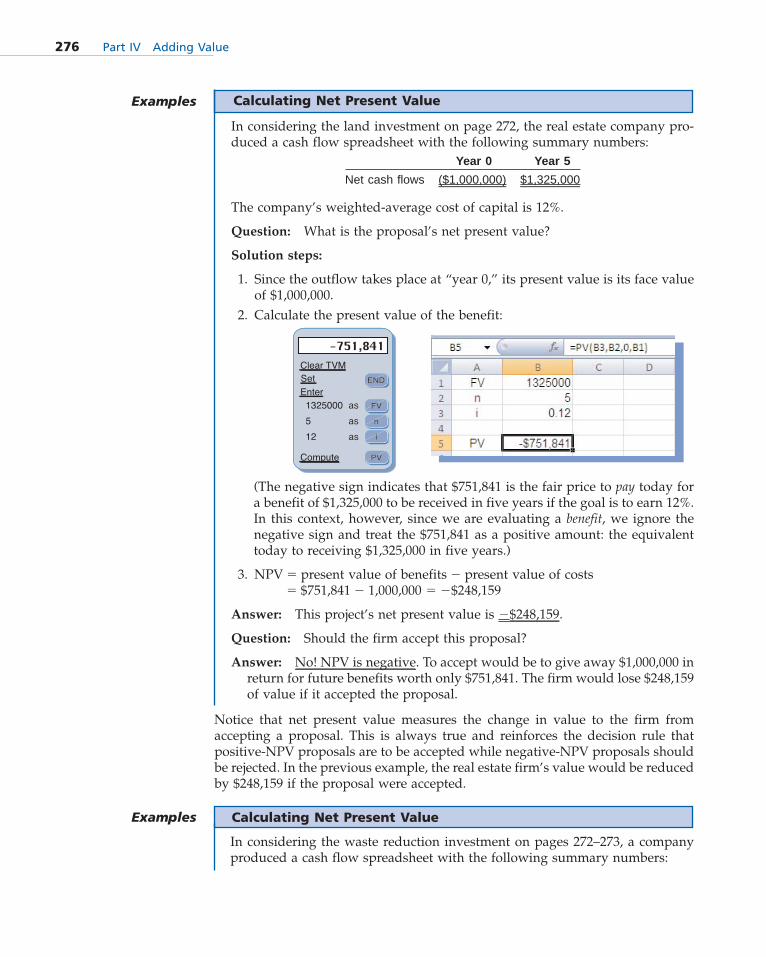

Organizing Cash Flow Data for Capital BudgetingExample

A real estate company is considering the purchase of a parcel of land for$1,000,000. Management forecasts it would hold the land for five years, dur-ing which time there would be no receipts or costs associated with the prop-erty. At the end of the five years, the land would be sold for a price forecastedto be $1,500,000. The firm is in the 35% income tax bracket.

Question: Organize the cash flows for this capital budgeting analysis.

Solution steps:

1. The purchase and sale price for the land are given. We must calculate thetax the company will pay when it sells the land:

Gain on sale � $1,500,000 � 1,000,000 � $500,000Tax on gain � 35% � $500,000 � $175,000

2. Construct a cash flow spreadsheet:

Year 0 Year 5

Buy the land ($1,000,000)Sell the land ($1,500,000

Tax—gain on sale ($1,175,000)

Net cash flows ($1,000,000) $1,325,000

Answer: This project will require the firm to pay $1,000,000 at its inceptionin return for a forecasted $1,325,000 in five years.

Year 0 Years 1-n Year n

Buy asset (Cost)Tax—new depreciation Reduced taxesTerminal value Recovery

Sell asset Sale priceTax—gain/loss on sale Tax in/outflowTax—lost depreciation (Increased taxes)Lost terminal value (Lost recovery)

Operating cash flows Changed in/outflowsTax—changed income Tax on above

Supporting working capital (Investment) RecoveryNet cash flows

Organizing Cash Flow Data for Capital BudgetingExample

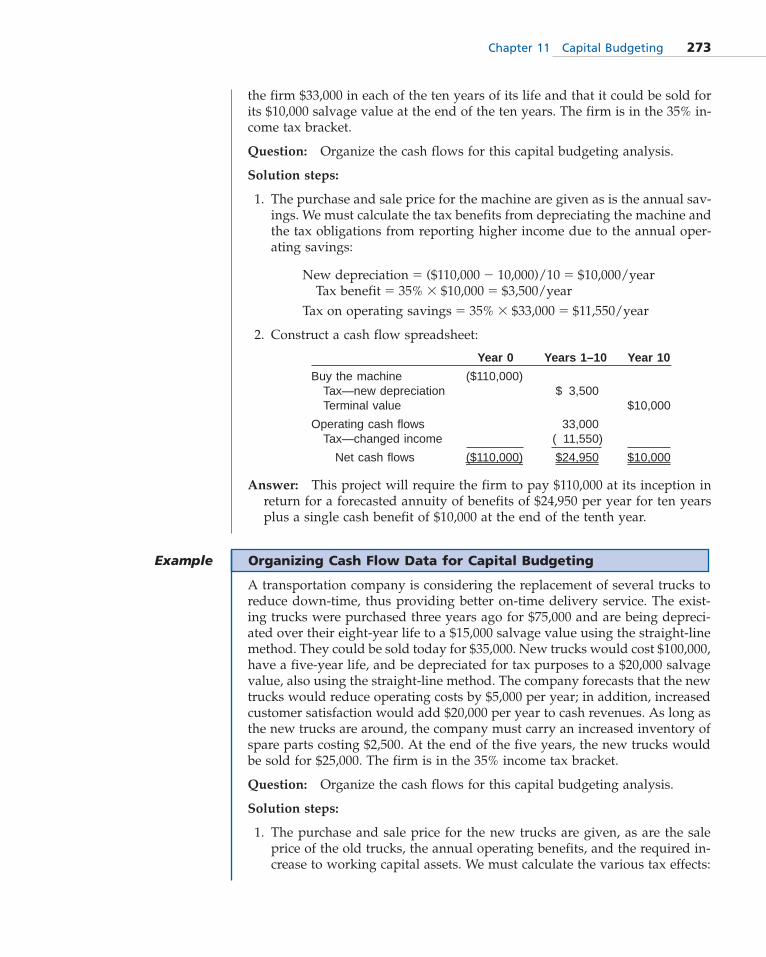

A manufacturing company is considering the purchase of a machine to reducewaste in its production process. The machine would cost $110,000, have a ten-year life, and be depreciated for tax purposes to a $10,000 salvage value usingthe straight-line3 method. The company forecasts that the machine would save

3 Elaboration and cross-reference: Although the U.S. tax code requires businesses to use the “mod-ified accelerated cost recovery system (MACRS)” to depreciate assets on their tax returns, we use thestraight-line method throughout this chapter to keep the illustrations simple and manageable. SeeWeb Appendix 11A for further discussion of the worth of accelerated depreciation.

the firm $33,000 in each of the ten years of its life and that it could be sold forits $10,000 salvage value at the end of the ten years. The firm is in the 35% in-come tax bracket.

Question: Organize the cash flows for this capital budgeting analysis.

Solution steps:

1. The purchase and sale price for the machine are given as is the annual sav-ings. We must calculate the tax benefits from depreciating the machine andthe tax obligations from reporting higher income due to the annual oper-ating savings:

New depreciation � ($110,000 � 10,000)/10 � $10,000/yearTax benefit � 35% � $10,000 � $3,500/year

Tax on operating savings � 35% � $33,000 � $11,550/year

2. Construct a cash flow spreadsheet:

Year 0 Years 1–10 Year 10

Buy the machine ($110,000)Tax—new depreciation $13,500Terminal value $10,000

Operating cash flows 33,000Tax—changed income ($11,550)

Net cash flows ($110,000) $24,950 $10,000

Answer: This project will require the firm to pay $110,000 at its inception inreturn for a forecasted annuity of benefits of $24,950 per year for ten yearsplus a single cash benefit of $10,000 at the end of the tenth year.

Chapter 11 Capital Budgeting 273

Organizing Cash Flow Data for Capital BudgetingExample

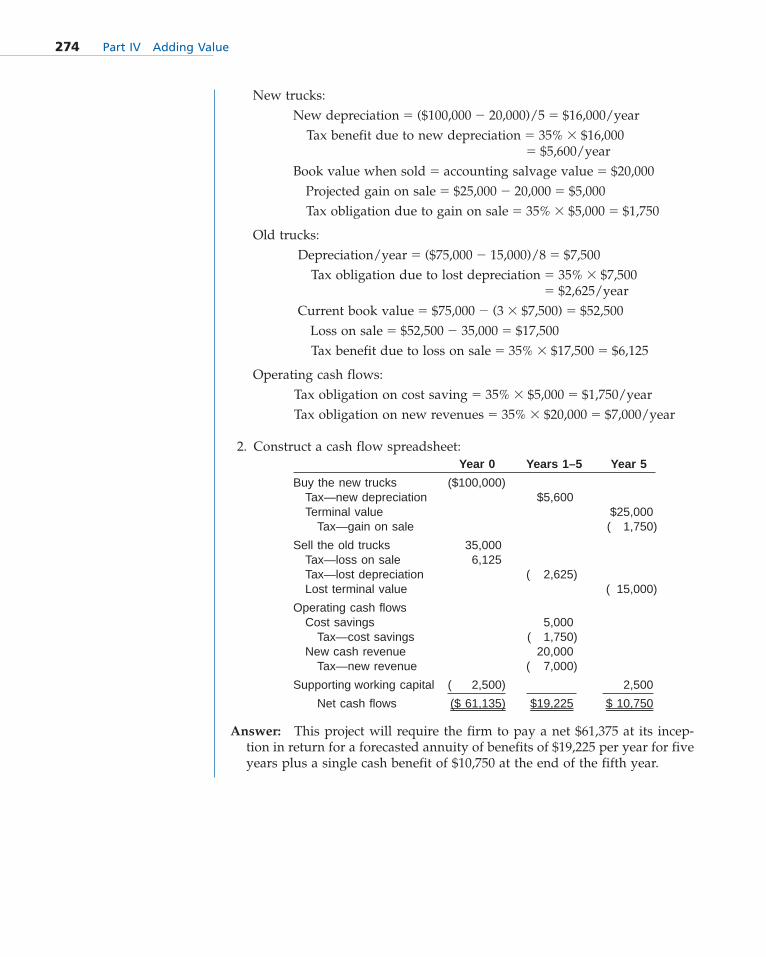

A transportation company is considering the replacement of several trucks toreduce down-time, thus providing better on-time delivery service. The exist-ing trucks were purchased three years ago for $75,000 and are being depreci-ated over their eight-year life to a $15,000 salvage value using the straight-linemethod. They could be sold today for $35,000. New trucks would cost $100,000,have a five-year life, and be depreciated for tax purposes to a $20,000 salvagevalue, also using the straight-line method. The company forecasts that the newtrucks would reduce operating costs by $5,000 per year; in addition, increasedcustomer satisfaction would add $20,000 per year to cash revenues. As long asthe new trucks are around, the company must carry an increased inventory ofspare parts costing $2,500. At the end of the five years, the new trucks wouldbe sold for $25,000. The firm is in the 35% income tax bracket.

Question: Organize the cash flows for this capital budgeting analysis.

Solution steps:

1. The purchase and sale price for the new trucks are given, as are the saleprice of the old trucks, the annual operating benefits, and the required in-crease to working capital assets. We must calculate the various tax effects:

274 Part IV Adding Value

New trucks:New depreciation � ($100,000 � 20,000)/5 � $16,000/year

Tax benefit due to new depreciation � 35% � $16,000� $5,600/year

Book value when sold � accounting salvage value � $20,000Projected gain on sale � $25,000 � 20,000 � $5,000Tax obligation due to gain on sale � 35% � $5,000 � $1,750

Old trucks:Depreciation/year � ($75,000 � 15,000)/8 � $7,500

Tax obligation due to lost depreciation � 35% � $7,500Tax obligation due to lost depreciation � $2,625/year

Current book value � $75,000 � (3 � $7,500) � $52,500Loss on sale � $52,500 � 35,000 � $17,500Tax benefit due to loss on sale � 35% � $17,500 � $6,125

Operating cash flows:Tax obligation on cost saving � 35% � $5,000 � $1,750/yearTax obligation on new revenues � 35% � $20,000 � $7,000/year

2. Construct a cash flow spreadsheet:Year 0 Years 1–5 Year 5

Buy the new trucks ($100,000)Tax—new depreciation $5,600Terminal value $25,000

Tax—gain on sale ($11,750)

Sell the old trucks 35,000Tax—loss on sale 6,125Tax—lost depreciation ($12,625)Lost terminal value ($15,000)

Operating cash flowsCost savings 5,000

Tax—cost savings ($11,750)New cash revenue 20,000

Tax—new revenue ($17,000)

Supporting working capital ($122,500) 2,500

Net cash flows ($ 61,135) $19,225 $ 10,750

Answer: This project will require the firm to pay a net $61,375 at its incep-tion in return for a forecasted annuity of benefits of $19,225 per year for fiveyears plus a single cash benefit of $10,750 at the end of the fifth year.

Chapter 11 Capital Budgeting 275

�� Reaching a Decision

The cash flow spreadsheet for a capital budgeting project gives a summary of theproject’s projected cash flows organized by when they are expected to occur. Inthis form the data are perfectly arranged for evaluation using time value of moneytools. The use of time value analysis is necessary since long-term asset invest-ments, by their very nature, involve cash flow changes at a variety of points intime—from the project’s inception into the future—and, as we originally saw inChapter 3, it is impossible to compare cash flows unless they are adjusted for time.

There are two widely used methods of applying time value analysis to a table ofcash flows: (1) net present value and (2) internal rate of return. Both reduce thecash flow data to a single number. Both test that number against the firm’sweighted-average cost of capital to determine if the investment project returns anamount sufficient to give investors their required rate of return. If so, the com-pany should accept the proposed investment as it will add value for the firm’sstakeholders; if not, the proposed investment should be rejected since to accept itwould reduce the firm’s worth.4

In what follows, we look further at these two methods and apply them to the fourinvestments for which we developed cash flow spreadsheets on the previouspages.

1. Net Present Value (NPV)

The net present value of a series of cash flows is the difference, or net, betweenthe present value of all benefits and the present value of all costs. Alternatively,since cash inflows are written with a positive sign while cash outflows are treatedas negative, net present value is simply the sum of the signed present values ofall the cash flows. By combining the benefits and costs of a proposed project, NPVperforms a (time-value-of-money adjusted) cost-benefit analysis.

The interest rate used to calculate net present value must be the cost of capital ap-propriate for the investment project. By using the cost of capital to discount fu-ture cash flows to their present value, NPV tests those flows to see if they repre-sent a growth in value in excess of “the rate the firm must earn on new investmentsto return to investors their required rate of return.”

When net present value is positive, benefits exceed costs and the proposal shouldbe accepted. When net present value is negative, the reverse is true: costs aregreater than benefits and the proposal should be rejected.

4 Elaboration and observation: Net present value (NPV) is the theoretically correct method, calcu-lating the projected value added to the company from undertaking the proposed project. But inter-nal rate of return (IRR) is a perfect substitute for NPV in many cases. Where this is so, many financeprofessionals prefer IRR since they find it easier to communicate and understand (“The proposedinvestment earns a 30% rate of return”). IRR, a rate of interest, is easily compared to other interestrates in the economy, especially the company’s cost of capital. NPV on the other hand, a dollaramount, may seem like a more abstract concept (“The proposed investment would add $5,000 to thecompany’s value measured in today’s dollars”), and is more difficult to relate to the cost of financ-ing the proposed capital budgeting project. See Web Appendix 11C for a discussion of those caseswhere IRR breaks down.

net present value—thepresent value of all benefitsfrom a proposed investmentless the present value of all costs, using theweighted-average cost ofcapital as the discount rate

NNEETT PPrreesseenntt VVaalluuee(This time the subjectreally is “Net PresentValue”!) A website withfurther information onthe concept of NPV iswww.investopedia.com/terms/n/npv.asp

276 Part IV Adding Value

Calculating Net Present ValueExamples

In considering the land investment on page 272, the real estate company pro-duced a cash flow spreadsheet with the following summary numbers:

Year 0 Year 5

Net cash flows ($1,000,000) $1,325,000

The company’s weighted-average cost of capital is 12%.

Question: What is the proposal’s net present value?

Solution steps:

1. Since the outflow takes place at “year 0,” its present value is its face valueof $1,000,000.

2. Calculate the present value of the benefit:

(The negative sign indicates that $751,841 is the fair price to pay today fora benefit of $1,325,000 to be received in five years if the goal is to earn 12%.In this context, however, since we are evaluating a benefit, we ignore thenegative sign and treat the $751,841 as a positive amount: the equivalenttoday to receiving $1,325,000 in five years.)

3. NPV � present value of benefits � present value of costs� $751,841 � 1,000,000 � �$248,159

Answer: This project’s net present value is �$248,159.

Question: Should the firm accept this proposal?

Answer: No! NPV is negative. To accept would be to give away $1,000,000 inreturn for future benefits worth only $751,841. The firm would lose $248,159of value if it accepted the proposal.

Notice that net present value measures the change in value to the firm from accepting a proposal. This is always true and reinforces the decision rule that positive-NPV proposals are to be accepted while negative-NPV proposals shouldbe rejected. In the previous example, the real estate firm’s value would be reducedby $248,159 if the proposal were accepted.

Calculating Net Present ValueExamples

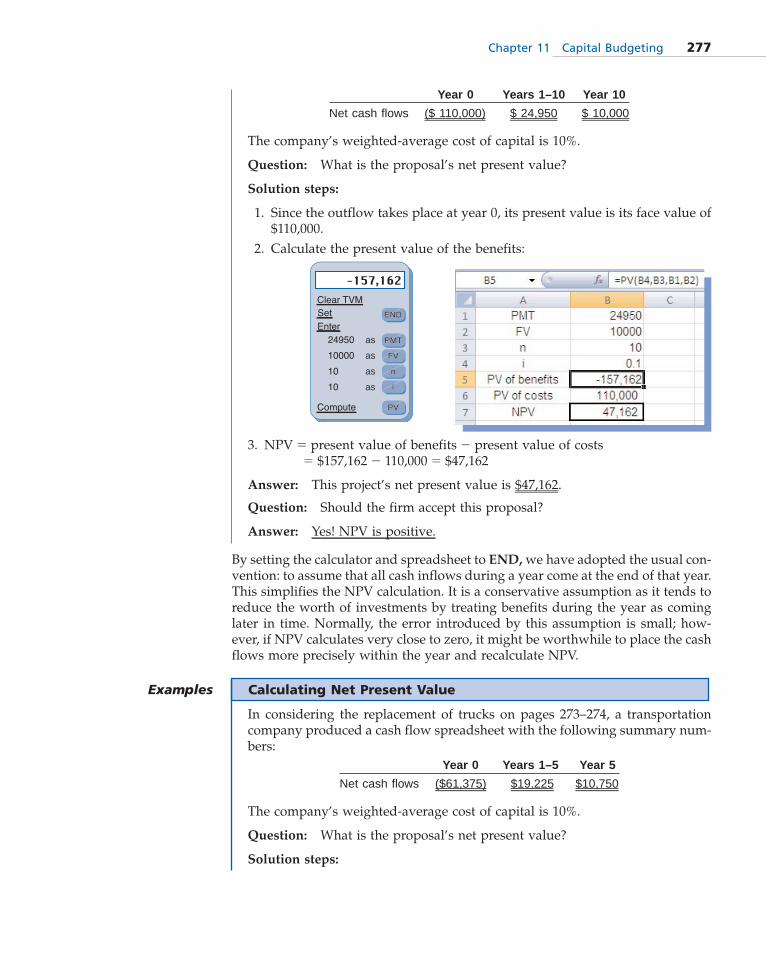

In considering the waste reduction investment on pages 272–273, a companyproduced a cash flow spreadsheet with the following summary numbers:

Year 0 Years 1–10 Year 10

Net cash flows ($ 110,000) $ 24,950 $ 10,000

The company’s weighted-average cost of capital is 10%.

Question: What is the proposal’s net present value?

Solution steps:

1. Since the outflow takes place at year 0, its present value is its face value of$110,000.

2. Calculate the present value of the benefits:

3. NPV � present value of benefits � present value of costs� $157,162 � 110,000 � $47,162

Answer: This project’s net present value is $47,162.

Question: Should the firm accept this proposal?

Answer: Yes! NPV is positive.

Chapter 11 Capital Budgeting 277

Calculating Net Present ValueExamples

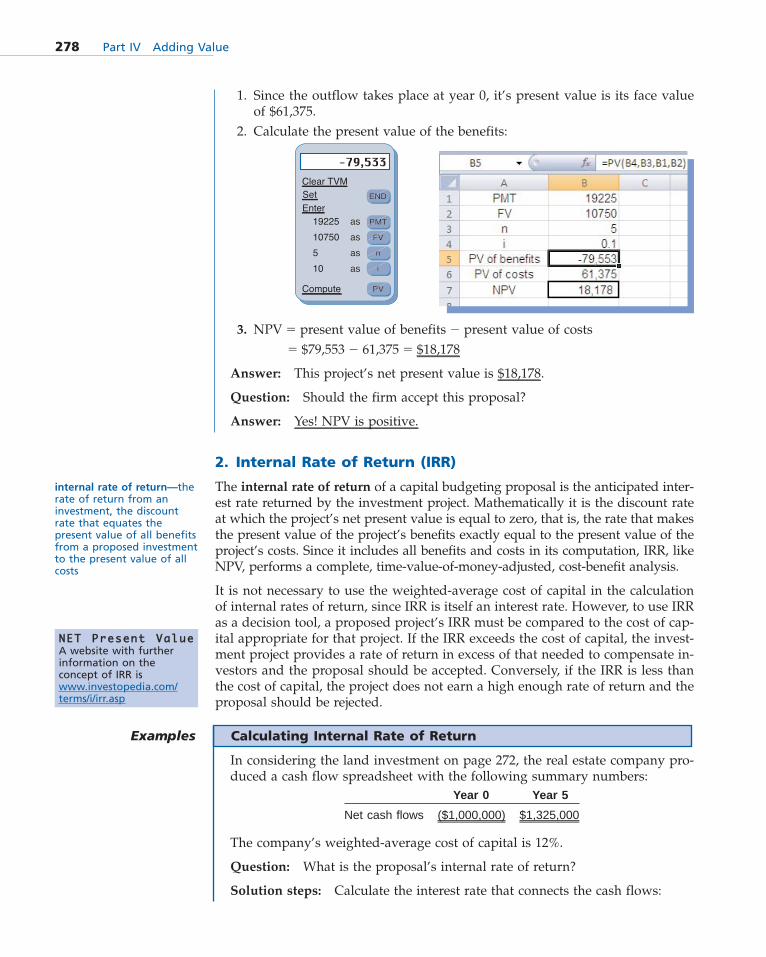

In considering the replacement of trucks on pages 273–274, a transportationcompany produced a cash flow spreadsheet with the following summary num-bers:

Year 0 Years 1–5 Year 5

Net cash flows ($61,375) $19,225 $10,750

The company’s weighted-average cost of capital is 10%.

Question: What is the proposal’s net present value?

Solution steps:

By setting the calculator and spreadsheet to END, we have adopted the usual con-vention: to assume that all cash inflows during a year come at the end of that year.This simplifies the NPV calculation. It is a conservative assumption as it tends toreduce the worth of investments by treating benefits during the year as cominglater in time. Normally, the error introduced by this assumption is small; how-ever, if NPV calculates very close to zero, it might be worthwhile to place the cashflows more precisely within the year and recalculate NPV.

1. Since the outflow takes place at year 0, it’s present value is its face valueof $61,375.

2. Calculate the present value of the benefits:

3. NPV � present value of benefits � present value of costs� $79,553 � 61,375 � $18,178

Answer: This project’s net present value is $18,178.

Question: Should the firm accept this proposal?

Answer: Yes! NPV is positive.

2. Internal Rate of Return (IRR)

The internal rate of return of a capital budgeting proposal is the anticipated inter-est rate returned by the investment project. Mathematically it is the discount rateat which the project’s net present value is equal to zero, that is, the rate that makesthe present value of the project’s benefits exactly equal to the present value of theproject’s costs. Since it includes all benefits and costs in its computation, IRR, likeNPV, performs a complete, time-value-of-money-adjusted, cost-benefit analysis.

It is not necessary to use the weighted-average cost of capital in the calculationof internal rates of return, since IRR is itself an interest rate. However, to use IRRas a decision tool, a proposed project’s IRR must be compared to the cost of cap-ital appropriate for that project. If the IRR exceeds the cost of capital, the invest-ment project provides a rate of return in excess of that needed to compensate in-vestors and the proposal should be accepted. Conversely, if the IRR is less thanthe cost of capital, the project does not earn a high enough rate of return and theproposal should be rejected.

internal rate of return—therate of return from aninvestment, the discountrate that equates thepresent value of all benefitsfrom a proposed investmentto the present value of allcosts

278 Part IV Adding Value

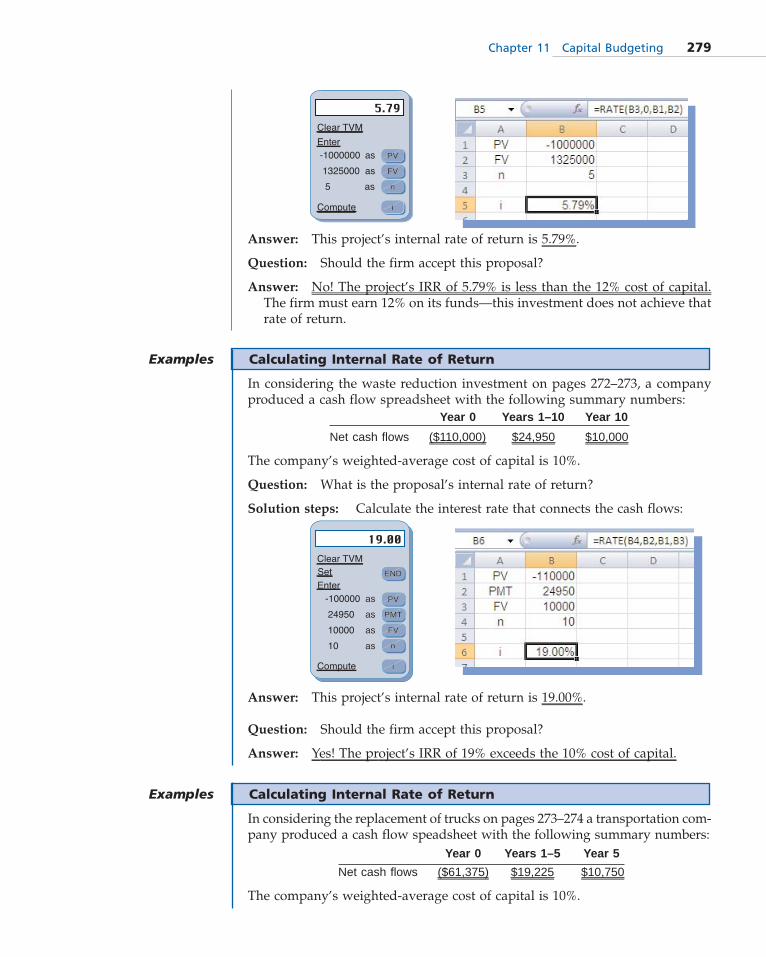

Calculating Internal Rate of ReturnExamples

In considering the land investment on page 272, the real estate company pro-duced a cash flow spreadsheet with the following summary numbers:

Year 0 Year 5

Net cash flows ($1,000,000) $1,325,000

The company’s weighted-average cost of capital is 12%.

Question: What is the proposal’s internal rate of return?

Solution steps: Calculate the interest rate that connects the cash flows:

NNEETT PPrreesseenntt VVaalluueeA website with furtherinformation on theconcept of IRR iswww.investopedia.com/terms/i/irr.asp

Answer: This project’s internal rate of return is 5.79%.

Question: Should the firm accept this proposal?

Answer: No! The project’s IRR of 5.79% is less than the 12% cost of capital.The firm must earn 12% on its funds—this investment does not achieve thatrate of return.

Chapter 11 Capital Budgeting 279

Calculating Internal Rate of ReturnExamples

In considering the waste reduction investment on pages 272–273, a companyproduced a cash flow spreadsheet with the following summary numbers:

Year 0 Years 1–10 Year 10

Net cash flows ($110,000) $24,950 $10,000

The company’s weighted-average cost of capital is 10%.

Question: What is the proposal’s internal rate of return?

Solution steps: Calculate the interest rate that connects the cash flows:

Answer: This project’s internal rate of return is 19.00%.

Question: Should the firm accept this proposal?

Answer: Yes! The project’s IRR of 19% exceeds the 10% cost of capital.

Calculating Internal Rate of ReturnExamples

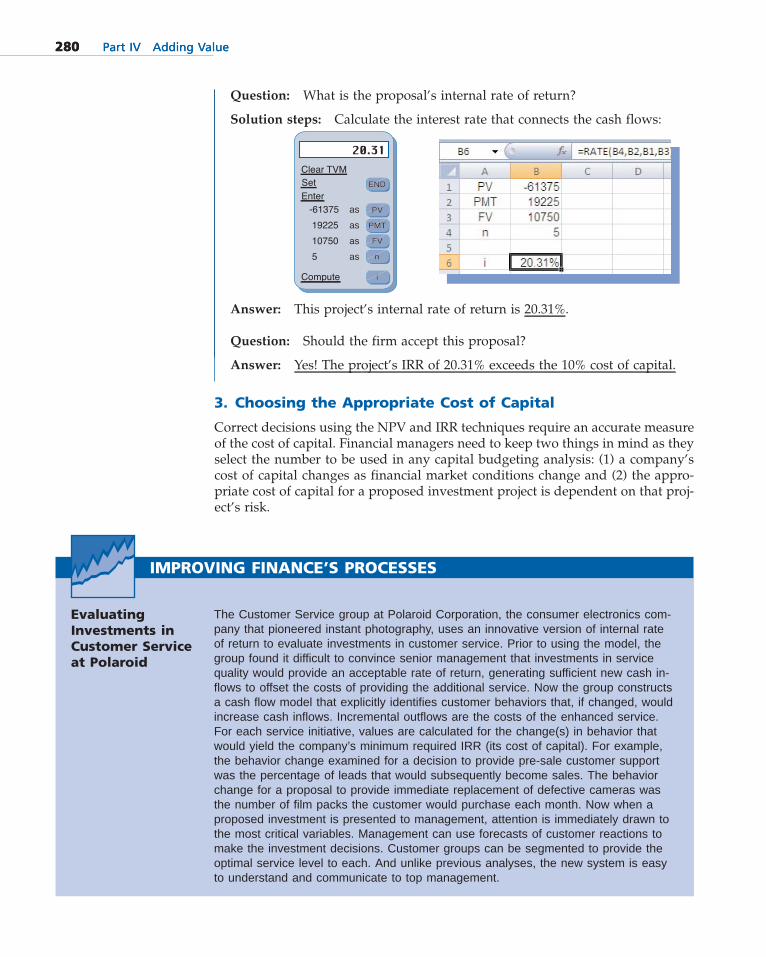

In considering the replacement of trucks on pages 273–274 a transportation com-pany produced a cash flow speadsheet with the following summary numbers:

Year 0 Years 1–5 Year 5

Net cash flows ($61,375) $19,225 $10,750

The company’s weighted-average cost of capital is 10%.

Question: What is the proposal’s internal rate of return?

Solution steps: Calculate the interest rate that connects the cash flows:

Answer: This project’s internal rate of return is 20.31%.

Question: Should the firm accept this proposal?

Answer: Yes! The project’s IRR of 20.31% exceeds the 10% cost of capital.

280 Part IV Adding Value280 Part IV Adding Value

3. Choosing the Appropriate Cost of Capital

Correct decisions using the NPV and IRR techniques require an accurate measureof the cost of capital. Financial managers need to keep two things in mind as theyselect the number to be used in any capital budgeting analysis: (1) a company’scost of capital changes as financial market conditions change and (2) the appro-priate cost of capital for a proposed investment project is dependent on that proj-ect’s risk.

IMPROVING FINANCE’S PROCESSES

Evaluating Investments inCustomer Serviceat Polaroid

The Customer Service group at Polaroid Corporation, the consumer electronics com-pany that pioneered instant photography, uses an innovative version of internal rateof return to evaluate investments in customer service. Prior to using the model, thegroup found it difficult to convince senior management that investments in servicequality would provide an acceptable rate of return, generating sufficient new cash in-flows to offset the costs of providing the additional service. Now the group constructsa cash flow model that explicitly identifies customer behaviors that, if changed, wouldincrease cash inflows. Incremental outflows are the costs of the enhanced service.For each service initiative, values are calculated for the change(s) in behavior thatwould yield the company’s minimum required IRR (its cost of capital). For example,the behavior change examined for a decision to provide pre-sale customer supportwas the percentage of leads that would subsequently become sales. The behaviorchange for a proposal to provide immediate replacement of defective cameras wasthe number of film packs the customer would purchase each month. Now when aproposed investment is presented to management, attention is immediately drawn tothe most critical variables. Management can use forecasts of customer reactions tomake the investment decisions. Customer groups can be segmented to provide theoptimal service level to each. And unlike previous analyses, the new system is easyto understand and communicate to top management.

Chapter 11 Capital Budgeting 281

Changing conditions A company’s cost of capital changes regularly. As wesaw in Chapter 10, the calculation of the cost of capital begins with the rates ofreturn required by the company’s suppliers of funds, each of which incorporatesthe general level of interest rates and a premium for risk as delineated by theFisher model we studied in Chapter 4. The cost of capital is then assembled byincorporating flotation costs, income tax effects, and the mix of financing used.As interest rates fluctuate, as risk perceptions shift, as flotation costs change, andas different tax rates affect the company, the cost of capital adjusts accordingly.

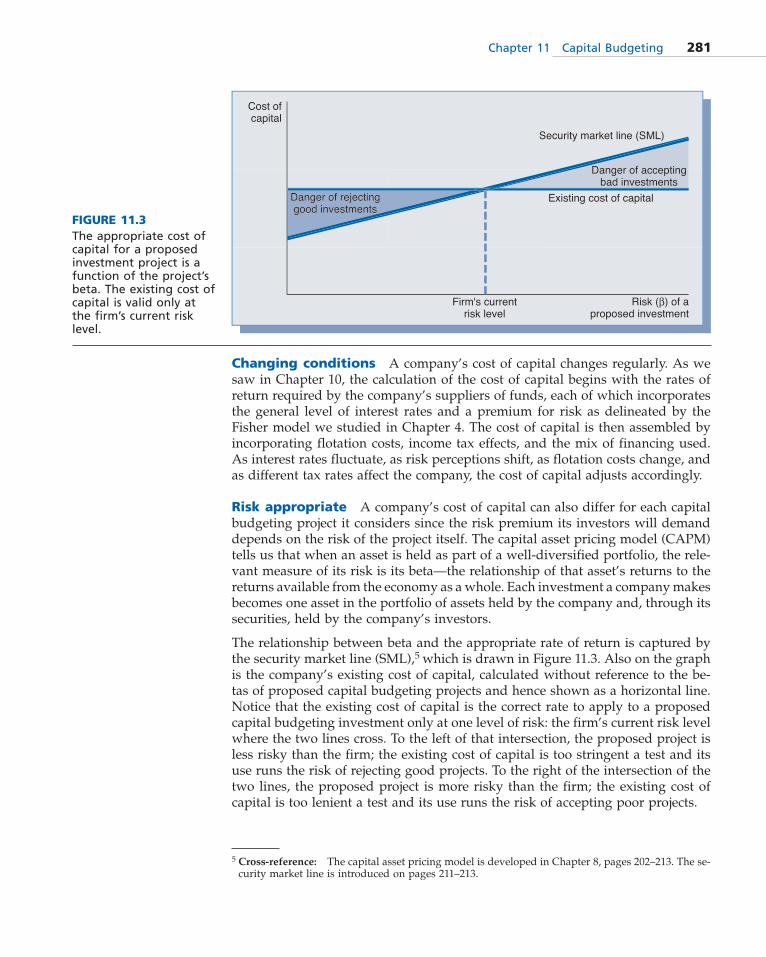

Risk appropriate A company’s cost of capital can also differ for each capitalbudgeting project it considers since the risk premium its investors will demanddepends on the risk of the project itself. The capital asset pricing model (CAPM)tells us that when an asset is held as part of a well-diversified portfolio, the rele-vant measure of its risk is its beta—the relationship of that asset’s returns to thereturns available from the economy as a whole. Each investment a company makesbecomes one asset in the portfolio of assets held by the company and, through itssecurities, held by the company’s investors.

The relationship between beta and the appropriate rate of return is captured bythe security market line (SML),5 which is drawn in Figure 11.3. Also on the graphis the company’s existing cost of capital, calculated without reference to the be-tas of proposed capital budgeting projects and hence shown as a horizontal line.Notice that the existing cost of capital is the correct rate to apply to a proposedcapital budgeting investment only at one level of risk: the firm’s current risk levelwhere the two lines cross. To the left of that intersection, the proposed project isless risky than the firm; the existing cost of capital is too stringent a test and itsuse runs the risk of rejecting good projects. To the right of the intersection of thetwo lines, the proposed project is more risky than the firm; the existing cost ofcapital is too lenient a test and its use runs the risk of accepting poor projects.

FIGURE 11.3The appropriate cost ofcapital for a proposedinvestment project is afunction of the project’sbeta. The existing cost ofcapital is valid only atthe firm’s current risklevel.

5 Cross-reference: The capital asset pricing model is developed in Chapter 8, pages 202–213. The se-curity market line is introduced on pages 211–213.

282 Part IV Adding Value

Rick Daniel put down the advanced finance text and turned back to hisspreadsheet. He had just finished rereading several chapters on capi-

tal budgeting. He was happy to discover that he had remembered most of it butwas equally happy that he had located several ideas that could be applied tohis current task. One chapter in particular, on how to search methodically forgood data, had confirmed some of the senior analyst’s suggestions.

The cash flow numbers had been entered into the appropriate columns of thespreadsheet, reflecting estimates of when those cash flows would occur. Thecost of capital was realistic. And the spreadsheet program was correctly calcu-lating the project’s net present value and internal rate of return. The problemseemed to be with the completeness of the data.

As he returned the text to his bookshelf, Rick thought back to his finance classon capital budgeting and remembered a statement his professor seemed toemphasize: “After a while, the NPV and IRR calculations become routine; get-ting good data is the difficult part of the job.” Rick smiled wryly as he realizedthat his current problem was teaching him just how true that statement was.

282 Part IV Adding Value

Summary of Key Points

�� Discuss the importance of capital budgeting tobusiness success. Capital budgeting is the processof evaluating potential long-term investments. Dueto their long-term nature, investments in these assetshave a major impact on the firm’s ability to compete.The techniques of capital budgeting are applicable toother incremental decisions and form an importantcomponent of the financial manager’s skills.

�� Identify the data used in capital budgeting. Thereare eight rules which specify the data that should andshould not enter into capital budgeting analysis: (1)use cash flow numbers only, (2) use incremental num-bers only, (3) include changes in all functional areas,(4) include changes across the life cycle, (5) includeforecasted inflation, (6) consider quality and sustain-ability impacts, (7) consider the options implicit inthe decision, and (8) leave the financing flows out.

�� Organize cash flow data for capital budgetinganalysis. It is useful to organize the data of a capi-tal budgeting decision with a cash flow spreadsheetthat summarizes cash flows by time of occurrence.This makes the data ready for analysis using time-value-of-money methods.

�� Use the techniques of net present value (NPV) andinternal rate of return (IRR) to judge the worth ofa capital project. Net present value (NPV) com-pares the present value of the proposal’s benefits tothe present value of its costs to determine which isgreater. The NPV number measures the value addedto (or subtracted from) the firm by going ahead with

the investment. When NPV is positive, benefits ex-ceed costs and the project should be accepted. WhenNPV is negative, costs exceed benefits and the projectshould be rejected. A project’s IRR is its anticipatedrate of return. When a project’s IRR exceeds the ap-propriate cost of capital, the project should be ac-cepted as it returns more than the minimum amountrequired to satisfy investors. When a project’s IRR isless than the cost of capital, the project should be re-jected as the return is insufficient to meet investors’needs. The cost of capital used to evaluate each pro-posed project must reflect current market conditionsand be adjusted to match the risk of the project.

Questions1. Why does capital budgeting analysis pay attention

only to cash flows?

2. What is a sunk cost? Why is it ignored in capital bud-geting?

3. What would happen to a capital budgeting analysisif inflation were omitted from the cash flow esti-mates?

4. What is meant by the “option” inherent in a capitalbudgeting decision?

5. A financial analyst included the interest cost of thedebt used to buy new machinery in the cash flowsfrom a capital budgeting project. Is this correct or in-correct? Why?

6. What function does a cash flow spreadsheet play incapital budgeting analysis?

Chapter 11 Capital Budgeting 283

Cost to build addition $ 500,000Book value of existing plant 7,000,000Cost for new machinery 200,000Cost of new electric wiring 30,000Amount spent on study to date 2,000Increase to working capital to

support machinery 60,000Interest on loan to finance the addition 40,000

a. Which of the above figures should enter the capi-tal budgeting analysis? Why?

b. Which of the above figures should not enter thecapital budgeting analysis? Why?

c. Suppose that $15,000 of working capital currentlyin use elsewhere within the company could per-form double duty by supporting this facility aswell. How would this change your answers toparts a and b?

d. Suppose the land under the plant would havebeen sold to a real estate developer for $1,500,000if the addition were not built. How would thischange your answers to parts a and b?

4. (Identifying incremental cash flows) Last week,your firm bought a fleet of trucks for $200,000 to be-gin a delivery service business. Today, someone cameup with the idea to use the trucks to sell ice cream tosuburban children door to door. Converting thetrucks would cost $75,000. You have been asked towork on this capital budgeting project.

a. What is the role of the $200,000 in your analysis?b. What is the role of the $75,000 in your analysis?c. What other information would you need to know

about the trucks before making this decision?d. What information not about the trucks would you

need to know before making this decision?

5. (Identifying nominal numbers) A company is con-sidering an investment that would cost $25,000 andreturn a net after-tax cash flow of $8,000 per year ineach of the next five years.

a. Assume these figures include inflation forecasts. What numbers should enter the capital budgetinganalysis?

b. Now assume the above figures do not include in-flation, forecast to be 6% per year. What numbersshould enter the capital budgeting analysis?

c. Why must the cash flows used in capital budget-ing contain the impact of inflation?

d. What would be the bias if the impact of inflationwere left out?

6. (Identifying nominal numbers) A company is con-sidering an investment that would cost $70,000 andreturn a net after-tax cash flow of $10,000 per year ineach of the next seven years.

7. What is the meaning of:

a. Net present value?b. Internal rate of return?

In what ways are they the same; how do they differ?

8. Why is the net present value of a capital budgetingproject equal to zero when its internal rate of returnis used as the discount rate?

9. True or false (and why?): The NPV technique uses thefirm’s cost of capital in its calculation, but the IRRtechnique does not. Therefore, the cost of capital isrelevant only if capital budgeting projects are evalu-ated using NPV.

10. What is the danger of applying one cost of capital toall proposed capital budgeting projects?

Problems1. (Identifying cash flows) An analyst has prepared the

following data as part of a proposal to acquire a newmachine:

Cost to purchase machine $40,000Cost to install machine 1,000Cost of new electric wiring 2,000First-year depreciation of machine 4,000Sales tax on purchasing machine 3,000Economic salvage value of the machine 10,000Accounting salvage value of the machine 8,000

a. Which of the above figures should enter the capi-tal budgeting analysis?

b. What figure should enter the capital budgetinganalysis as the investment at year zero?

c. Which of the above figures should not enter thecapital budgeting analysis?

d. Will any of the items you list in part c have a laterimpact on the firm’s cash flows? If so, what?

2. (Identifying cash flows) A company is consideringswitching from accelerated to straight-line deprecia-tion on its GAAP financial statements to reduce itsdepreciation expense and boost income.

a. What effect will this change have on the firm’s re-ported income?

b. What is the financial value of this decision?c. Suppose the company made the same switch on its

tax returns. Now what is the financial value of thisdecision?

d. Given your answers to parts a–c, why do manycompanies make this change in choice of depreci-ation method?

3. (Identifying incremental cash flows) An analyst hasprepared the following data as part of a proposal foran addition to the firm’s plant:

284 Part IV Adding Value

a. Assume these figures include inflation forecasts.What numbers should enter the capital budgetinganalysis?

b. Now assume the above figures do not include in-flation, forecast to be 9% per year. What numbersshould enter the capital budgeting analysis?

c. Why does inflation affect only one of the numbersabove and not the other?

d. Does inflation appear anywhere else in the capitalbudgeting analysis? If so, where?

7. (Organizing cash flows) Judy Entrepreneur is con-sidering the purchase of a machine for $100,000; themachine would be depreciated to a $20,000 salvagevalue over an eight-year period using the straight-line method. During its life, the machine would im-prove Judy’s annual cash earnings by $25,000 peryear. The firm expects to sell the machine for its$20,000 salvage value at the end of the eight years.The firm’s federal tax rate on income is 35%. Calcu-late the incremental cash flows from:

a. The purchase of the machineb. The depreciation of the machinec. The operation of the machined. The sale of the machine

8. (Organizing cash flows) Joe Businessperson isconsidering the purchase of a machine for $650,000.The machine would be depreciated to a $50,000 sal-vage value over a nine-year period using thestraight-line method and would bring in incremen-tal cash income of $80,000 in each year. However, thefirm expects to sell the machine for $60,000 at the endof the nine years. The firm’s federal tax rate on in-come is 35%. Calculate the incremental cash flowsfrom:

a. The purchase of the machineb. The depreciation of the machinec. The operation of the machined. The sale of the machine

9. (NPV, IRR) A company can invest $200,000 in a cap-ital budgeting project that will generate the follow-ing forecasted cash flows:

Years Cash flow1–4 $75,000

The company has a 14% cost of capital.

a. Calculate the project’s net present value.b. Calculate the project’s internal rate of return.c. Should the firm accept or reject the project?d. At what cost of capital would the firm be indiffer-

ent to accepting or rejecting this proposal?

10. (NPV, IRR) A company can invest $3 million in acapital budgeting project that will generate the fol-lowing forecasted cash flows:

Years Cash flow1–16 $275,000

The company has an 8% cost of capital.

a. Calculate the project’s net present value.b. Calculate the project’s internal rate of return.c. Should the firm accept or reject the project?d. At what cost of capital would the firm be indiffer-

ent to accepting or rejecting this proposal?

11. (NPV, IRR) A company can invest $200,000 in a cap-ital budgeting project that will generate the follow-ing forecasted cash flows:

Year Cash flow1 $110,0002 150,0003 120,0004 200,000

The company has a 10% cost of capital.

a. Calculate the project’s net present value.b. Calculate the project’s internal rate of return.c. Should the firm accept or reject the project?d. What is the value added to the firm if it accepts

this proposed investment?

12. (NPV, IRR) A company can invest $1,600,000 in acapital budgeting project that will generate the fol-lowing forecasted cash flows:

Year Cash flow1 $500,0002 720,0003 300,0004 600,000

The company has a 13% cost of capital.

a. Calculate the project’s net present value.b. Calculate the project’s internal rate of return.c. Should the firm accept or reject the project?d. What is the value added to the firm if it accepts

this proposed investment?

13. (Organizing cash flows, NPV, IRR) A company isevaluating the purchase of Machine A. The new ma-chine would cost $120,000 and would be depreciatedfor tax purposes using the straight-line method overan estimated ten-year life to its expected salvagevalue of $20,000. The new machine would require anaddition of $30,000 to working capital. In each yearof Machine A’s life, the company would reduce itspre-tax costs by $40,000. The company has a 12% costof capital and is in the 35% marginal tax bracket.

a. Identify the incremental cash flows from investingin Machine A.

b. Calculate the investment’s net present value (NPV).c. Calculate the investment’s internal rate of return

(IRR).

Chapter 11 Capital Budgeting 285

d. Should the company purchase Machine A? Why orwhy not?

14. (Organizing cash flows, NPV, IRR) A company isevaluating the purchase of Machine X to improveproduct quality. The new machine would cost$1,000,000 and would be depreciated for tax purposesusing the straight-line method over an estimatedseven-year life to its expected salvage value of$125,000. The new machine would require an addi-tion of $100,000 to working capital. In each year ofMachine X’s life, the company would increase its pre-tax receipts by $400,000. The company has an 11% costof capital and is in the 35% marginal tax bracket.

a. Identify the incremental cash flows from investingin Machine X.

b. Calculate the investment’s net present value (NPV).c. Calculate the investment’s internal rate of return

(IRR).d. Should the company purchase Machine X? Why or

why not?

15. (Organizing cash flows, NPV, IRR) This problemfollows Problem 13. It is now five years later. Thecompany did buy Machine A, but just this week Ma-chine B came on the market; Machine B could be pur-chased to replace Machine A. If acquired, Machine Bwould cost $80,000 and would be depreciated for taxpurposes using the straight-line method over an esti-mated five-year life to its expected salvage value of$20,000. Machine B would also require $30,000 ofworking capital but would save an additional $20,000per year in pre-tax operating costs. Machine A’s sal-vage value remains $20,000, but it could be sold to-day for $40,000.

a. Identify the incremental cash flows from convert-ing to Machine B.

b. Calculate this investment’s net present value (NPV).c. Calculate this investment’s internal rate of return

(IRR).d. Should the company convert to Machine B? Why

or why not?

16. (Organizing cash flows, NPV, IRR) This problemfollows Problem 14. It is now four years later. Thecompany did buy Machine X, but just today MachineY came on the market; Machine Y could be purchasedto replace Machine X. If acquired, Machine Y wouldcost $750,000 and would be depreciated for tax pur-poses using the straight-line method over an esti-mated three-year life to its expected salvage value of$150,000. Machine Y would require $160,000 of work-ing capital but would add an additional $300,000 peryear to pre-tax receipts. Machine X’s salvage value re-

mains $125,000, but it could be sold today for$100,000.

a. Identify the incremental cash flows from convert-ing to Machine Y.

b. Calculate this investment’s net present value (NPV).c. Calculate this investment’s internal rate of return

(IRR).d. Should the company convert to Machine Y? Why

or why not?

17. (Adjusting the cost of capital for risk) A companywith a 13% cost of capital is evaluating four inde-pendent potential capital budgeting proposals withthe following forecasted internal rates of return (IRRs) and betas:

Proposal IRR BetaA 12% .85B 10 1.00C 16 1.10D 14 1.25

The market price of risk is 8.5%, and the risk-free rateof interest is currently 4%.

a. Write the equation of the security market line (SML).b. Calculate the required rate of return on each in-

vestment according to the SML.c. Which projects would be accepted by using the ex-

isting cost of capital?d. Which projects would be accepted by using a risk-

adjusted cost of capital for each project based onthe SML?

18. (Adjusting the cost of capital for risk) A companywith a 14% cost of capital is evaluating four inde-pendent potential capital budgeting proposals withthe following forecasted internal rates of return (IRRs)and betas:

Proposal IRR BetaW 15% 1.40X 19 1.15Y 11 .90Z 12 .65

The market price of risk is 8%, and the risk-free rateof interest is currently 5%.

a. Write the equation of the security market line(SML).

b. Calculate the required rate of return on each in-vestment according to the SML.

c. Which projects would be accepted by using the ex-isting cost of capital?

d. Which projects would be accepted by using a risk-adjusted cost of capital for each project based onthe SML?