part c risk - mit - massachusetts institute of technologyweb.mit.edu/astomper/www/univie/pof/chapter...

TRANSCRIPT

Lecture Notes ©2008 Jiang Wang

15.401

Part C RiskPart C Risk

TexPoint fonts used in EMF.Read the TexPoint manual before you delete this box.: AAAAAAAAAAAAAAAAAAAAAAAA

Chapter 7: Introduction to Risk and Return

Chapter 8: Portfolio Choice

Chapter 9: Capital Asset Pricing Model

Lecture Notes

15.401 Part C Risk

Premise in Previous Discussions

1. A rich set of traded securities allow us to price a particular CF(asset) by arbitrage– Time and risk

2. Pricing of risky CFs has the following properties:– CFs with “same risk” are discounted at the same rate

– “Riskier” CFs are discounted at higher rates

Unanswered Questions

1. How do we measure risk?

2. How do financial markets determine the price of risk?

Introduction to Part CIntroduction to Part C

Lecture Notes

15.401 Part C Risk

Goals for Part C

1. Quantifying risk (Chapter 7)

2. Portfolio choice (Chapter 8):– Diversifiable risk versus non-diversifiable risk

– Optimal risk/return trade-off

3. Capital Asset Pricing Model (CAPM) (Chapter 9):– How to determine price of risk (risk adjusted discount rate)

Introduction to Part CIntroduction to Part C

Lecture Notes

15.401

15.401 Finance Theory I15.401 Finance Theory I

AlexAlex Stomper StomperMIT Sloan School of ManagementMIT Sloan School of Management

Lecture Lecture 77: Introduction to Risk and Return: Introduction to Risk and Return

Lecture Notes

15.401 Lecture 7: Intro to risk and return

_ Asset returns_ Measuring risk_ Investor preferences_ Estimating risk and return_ Historic asset returns and risks

Readings:

_ Brealy, Myers and Allen, Chapter 8.1

_ Bodie, Kane and Markus, Chapters 5.2 ‒ 5.4

5

Key conceptsKey concepts

TexPoint fonts used in EMF.Read the TexPoint manual before you delete this box.: AAAAAAAAAAAA

Lecture Notes

15.401 Lecture 6: Intro to risk and return

_ is the price at the beginning of period

_ is the price at the end of period ‒ uncertain (random variable)

_ is the dividend at the end of period ‒ uncertain

Asset returnsAsset returns

P̃1

~D1

P0

6

Lecture Notes

15.401 Lecture 6: Intro to risk and return

Monthly returns - IBM (1990 -- 2000)

Asset returnsAsset returns

7

Lecture Notes

15.401 Lecture 6: Intro to risk and return

Annual returns - S&P 500 Index (1926 -- 2004)

Asset returnsAsset returns

8

Lecture Notes

15.401 Lecture 6: Intro to risk and returnAsset returnsAsset returns

Basic statistics

_ Mean, variance, standard deviation:

_ Sample estimators:

9

Lecture Notes

15.401 Lecture 6: Intro to risk and returnAsset returnsAsset returns

Other statistics

_ Median: 50th percentile (probability of 1/2 that rt < median)

_ Skewness: Is the distribution symmetric?– Negative: big losses are more likely than big gains

– Positive: big gains are more likely than big losses

_ Kurtosis: Does the distribution have fat tails?

_ Correlation: How closely do two variables move together?

10

Lecture Notes

15.401 Lecture 6: Intro to risk and returnAsset returnsAsset returns

Negatively skewed distribution

11

Lecture Notes

15.401 Lecture 6: Intro to risk and returnAsset returnsAsset returns

0.00

0.07

0.14

0.21

-21% -15% -9% -3% 3% 9% 15% 21%

GM Monthly Returns

12

Lecture Notes

15.401 Lecture 6: Intro to risk and returnAsset returnsAsset returns

-4

-3

-2

-1

0

1

2

3

4

-4 -3 -2 -1 0 1 2 3 4

-4

-3

-2

-1

0

1

2

3

-4 -3 -2 -1 0 1 2 3 4

-4

-3

-2

-1

0

1

2

3

4

-4 -3 -2 -1 0 1 2 3 4

-4

-3

-2

-1

0

1

2

3

-4 -3 -2 -1 0 1 2 3 4

ρ = 0 ρ = .5

ρ = .8 ρ = –.5

Correlation between two random variables

13

(Slope of the scattered plot gives the beta.)

Lecture Notes

15.401 Lecture 6: Intro to risk and return

Example. Moments of return distribution. Consider three assets:

_ Between Asset 0 and 1, which one would you choose?

_ Between Asset 1 and 2, which one would you choose?

Investors care about expected return and risk.

Measuring riskMeasuring risk

Mean StDr̃0 (%) 10.0 0.00r̃1 (%) 10.0 10.00r̃2 (%) 10.0 20.00

14

Lecture Notes

15.401 Lecture 6: Intro to risk and returnMeasuring riskMeasuring risk

15

Lecture Notes

15.401 Lecture 6: Intro to risk and return

Assumptions on investor preferences for 15.401

1. Higher mean in return is preferred:

2. Higher standard deviation (StD) in return is disliked:

3. Investors care only about mean and StD (or variance)

Under 1-3, standard deviation (StD) gives a measure of risk.

Investor preferencesInvestor preferences

�r = E[r̃]

=pE[(r̃ ¡ �r)2]

16

Lecture Notes

15.401 Lecture 6: Intro to risk and returnInvestor preferencesInvestor preferences

Investor Preference for Return and Risk

-

6

@@

@@

@@

@@

@@

@@

@@I 6

increasing return

decreasing risk

Risk ( )

Expected return (�r)

17

Lecture Notes

15.401 Lecture 6: Intro to risk and return

Return Indices of Investments in the US Capital Markets

Historical return and riskHistorical return and risk

Data R eturn (% per qtr)S&P Dell

1991-Q4 11.43 9.041992-Q1 -2.55 41.951992-Q2 1.97 -25.261992-Q3 3.10 57.931992-Q4 5.10 67.681993-Q1 4.28 -26.821993-Q2 0.51 -46.621993-Q3 2.56 -11.331993-Q4 2.31 36.091994-Q1 -3.81 11.601994-Q2 0.41 4.461994-Q3 4.92 41.941994-Q4 -0.03 9.521995-Q1 9.74 6.711995-Q2 9.49 37.431995-Q3 7.95 41.371995-Q4 5.96 -21.18

18

Lecture Notes

15.401 Lecture 6: Intro to risk and returnHistorical return and riskHistorical return and risk

Average Annual Total Returns from 1926 to 2005 (Nominal)Asset Mean (%) StD (%)T-bills 3.8 3.1Long term T-bonds 5.8 9.2Long term corp. bonds 6.2 8.5Large stocks 12.3 20.2Small stocks 17.4 32.9Inflation 3.1 4.3

Average Annual Total Returns from 1926 to 2005 (Real)Asset Mean (%) StD (%)T-bills 0.7 4.0Long term T-bonds 2.9 10.4Long term corp. bonds 3.2 9.7Large stocks 9.1 20.3Small stocks 13.9 32.3

19

Lecture Notes

15.401 Lecture 6: Intro to risk and returnHistorical return and riskHistorical return and risk

Average Annual Total Returns from 1926 to 2005 (Nominal)Asset Mean (%) StD (%)T-bills 3.8 3.1Long term T-bonds 5.8 9.2Long term corp. bonds 6.2 8.5Large stocks 12.3 20.2Small stocks 17.4 32.9Inflation 3.1 4.3

Average Annual Total Returns from 1926 to 2005 (Real)Asset Mean (%) StD (%)T-bills 0.7 4.0Long term T-bonds 2.9 10.4Long term corp. bonds 3.2 9.7Large stocks 9.1 20.3Small stocks 13.9 32.3

20

Lecture Notes

15.401 Lecture 6: Intro to risk and return

Returns on risky assets can be highly correlated with each other.

Estimating risk and returnEstimating risk and return

Sample moments for S&P 500 and Dell (1991.Q4 { 1995.Q4)

Sample Moments S&P 500 DellMean 0.0373 0.1379Variance 0.0018 0.1070StD 0.0428 0.3271Skewness 0.4930 -0.5112Covariance 0.0019Beta 1.06

21

Lecture Notes

15.401 Lecture 6: intro to risk and return

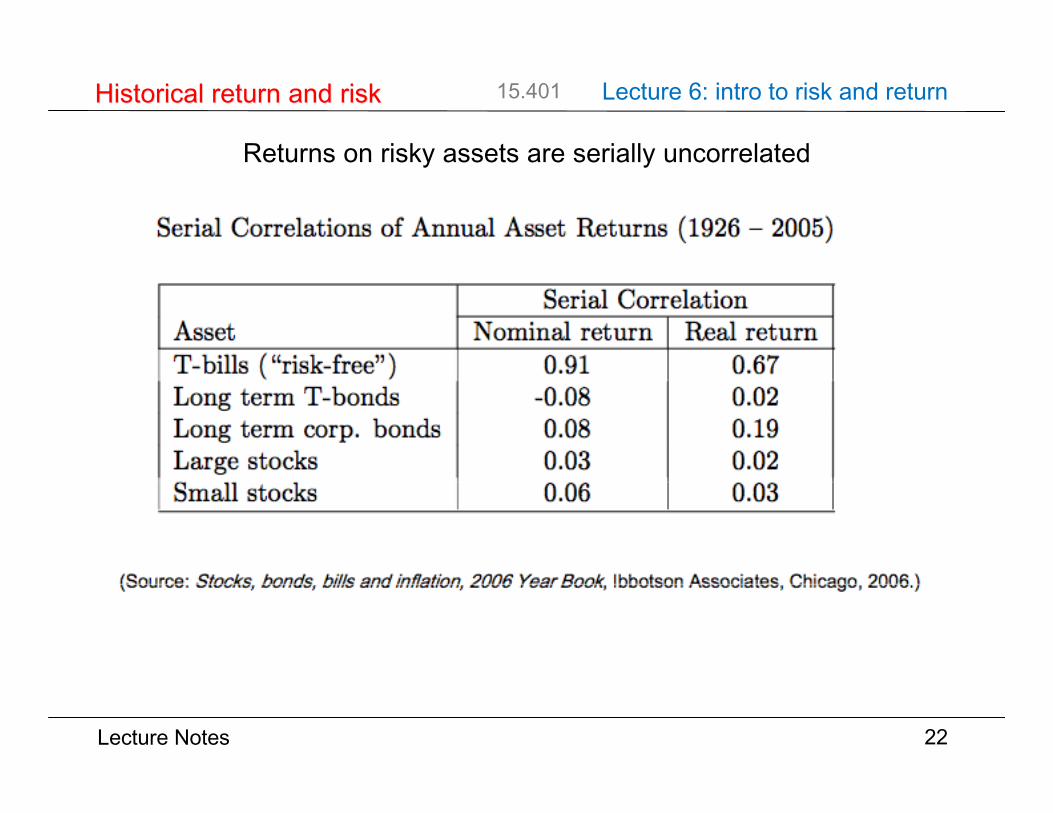

Returns on risky assets are serially uncorrelated

Historical return and riskHistorical return and risk

22

Lecture Notes

15.401 Lecture 6: intro to risk and returnHistorical return and riskHistorical return and risk

Total real returns from 1926 to 2005

Security Initial Total ReturnT-Bills $1.00 1.74Long Term T-Bonds $1.00 6.03Corporate Bonds $1.00 8.86Large Stocks $1.00 242.88Small Stocks $1.00 1,208.84

23

Lecture Notes

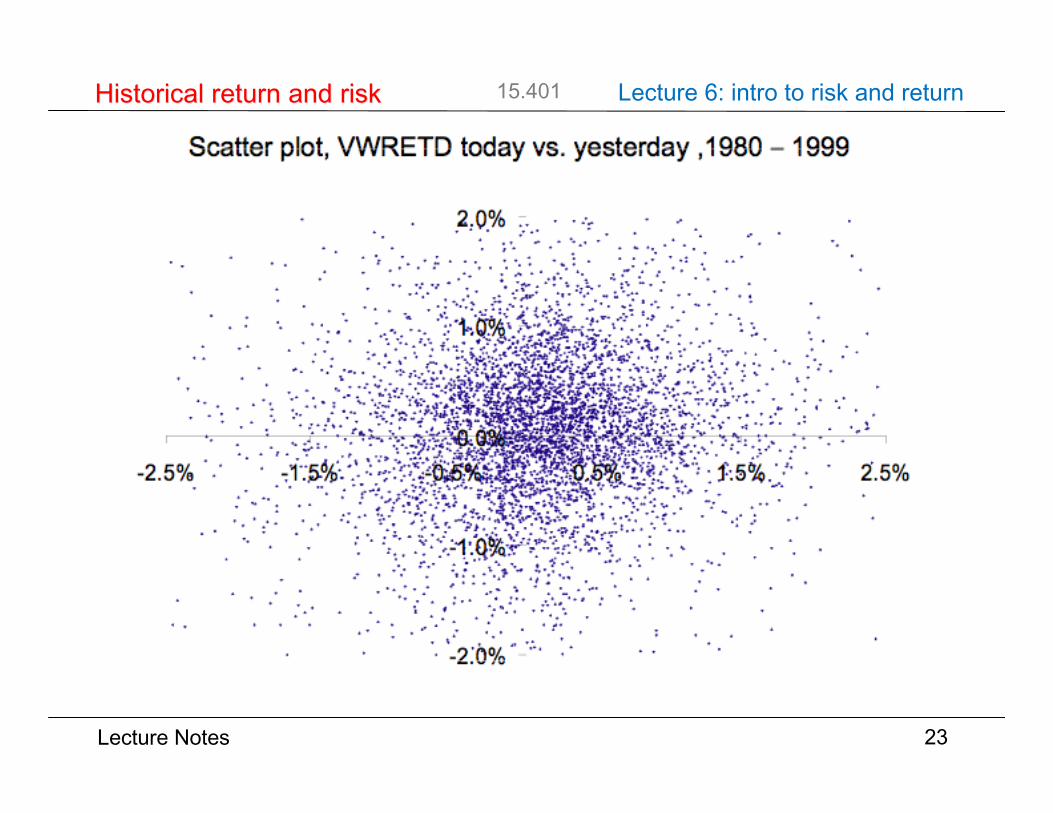

15.401 Lecture 6: Intro to risk and returnHistorical return and riskHistorical return and risk

-2.0%

-1.0%

0.0%

1.0%

2.0%

-2.5% -1.5% -0.5% 0.5% 1.5% 2.5%

Scatter plot, VWRETD today vs. yesterday ,1980 ‒ 1999

24

Lecture Notes

15.401 Lecture 7: Intro to risk and return

_ Asset returns_ Measuring risk_ Investor preferences_ Estimating risk and return_ Historic asset returns and risks

25

Key conceptsKey concepts

TexPoint fonts used in EMF.Read the TexPoint manual before you delete this box.: AAAAAAAAAAAA