paper eiasm conference 2014 - def

TRANSCRIPT

1

10th workshop on family firm management research:

innovation, family firms and economic development

Bergamo, Italy, 23-24 May 2014

Informal governance: the advisory board

A qualitative study in a family business setting

- “The future of the business does not happen to you,

but is something that you should build together” -

Authors:

Judith van Helvert

Windesheim University of Applied Sciences

Affiliated to Jönköping International Business School (PhD candidate)

PO Box 10090

8000GB Zwolle

The Netherlands

T +31 88 469 7189

Ilse Matser

Windesheim University of Applied Sciences

PO Box 10090

8000GB Zwolle

The Netherlands

T + 31 88 469 8828

Work in progress; please do not quote!

2

ABSTRACT

Board literature addressed the different roles and tasks of the board by which they presumably create

value for the firm. Yet this assumption has not been verified yet and the advisory role of the board is not

well understood. This study aims to provide insight into why and how Dutch family businesses set up an

advisory board by using longitudinal in-depth methodologies. Drawing from the practice perspective

(Feldman & Orlikowski, 2011) and building on the insights developed on qualitative board research, a

multiple case study approach was chosen in order to find out what the advisory task of the board entails.

Linking the practice perspective to the resource based view, the study reveals that privately held Dutch

FBs set up an AB because they want to have a sounding board, they want to professionalize the FB, they

want support and guidance in the succession process, they want to have a controlling mechanism, and

they want to bring in specific resources. The setting up process consists of six subsequent steps which

was similar for the eight participating FBs in the study. The pace by which the FBs go through the process

however differs to a large extent and is dependent on a number of contextual factors.

Keywords: Advisory board, longitudinal observation study, family business

1. INTRODUCTION

Whereas the literature on board contribution has been dominated by a focus on the monitoring and

control task of the board for a long time, since the 1990s a growing interest in the advice task of the

board in privately-held businesses has become visible. In studying the advice or strategic task of boards

scholars implicitly assume that board involvement in strategy leads to more effective organizational

performance (Hendry, Kiel, & Nicholson, 2010; Levrau, 2007) and the creation of value (Huse, 2007). For

family businesses (FBs), the predominant form of business organizations among privately-held firms,

more effective organizational performance and the creation of value implies survival and sustainability of

the FB. Over the years, research on board contribution to strategy has evolved from normative and

structural approaches (from the seventies until the nineties) to more behavioral and cognitive studies

(since 2000) (Pugliese et al., 2009). However, most studies still build on economic-related perspectives

(mostly agency theory) and adopt approaches characterized by deductively testing theoretical

perspectives (Zattoni & Van Ees, 2012). Moreover, even though research has shown that it is very

important to understand the context in which governance issues are studied (Huse, Hoskisson, Zattoni, &

Viganò, 2011) the large majority of board contribution to strategy research continues using samples of

large, public firms (Zahra & Pearce, 1989; Uhlaner, Wright, & Huse, 2007). Most of the contemporary

knowledge on boards’ contribution to strategy therefore originates from a limited set of empirical

contexts, largely ignoring the accuracy and contextual nature of governance issues (Pugliese et al., 2009)

and having little relevance to the situation of privately-held firms. This is confirmed by the findings of

Forbes and Milliken (1999), who identified that firm size is an antecedent for the perceived importance

of the advice task. Small and medium-sized firms (SMEs), with revenue of $25 million or less, find the

advice task more important than the control task. This implies that the ownership structure of the firm is

relevant to board contribution, because in SMEs the owner and the CEO is most of the time one and the

3

same person. Whereas it is clear that boards have a definite advisory role to play, there is debate on the

nature of that role (Hendry & Kiel, 2004). It seems fair to conclude that the literature does not provide

clarity on what the advisory role of the board actually implies. Moreover, it is not clear to what extent

boards actually contribute to strategy and if they do, how they do it. One explanation for this may be

that researchers have a hard time getting access to board meetings over longer periods of time and

identifying the variables, processes and actors that have an impact on strategy.

Within the FB research field, the topic of the board of directors has received a great deal of interest with

studies highlighting the board’s potential to contribute to performance and continuity (Bammens,

Voordeckers, & Van Gils, 2011). Research on FBs as a specific organizational setting is motivated by the

idea that the influence of the family on the firm has consequences for organizational processes and

policies, making them distinct from non-FBs from a theoretical perspective. Whereas many studies focus

on the control task of the board in the FB, Bammens et al. (2011) found that only a limited number of

studies has analyzed how family involvement in privately-held FBs affects the advice role of the board.

Those that do illustrate that family CEOs value the provision of board advice by outside board members

(e.g. Van Den Heuvel, Van Gils, & Voordeckers, 2006) and that provision of advice by the board increases

the quality of and commitment to strategic decisions (Mustakallio, Autio, & Zahra, 2002). Variables that

possibly have an influence on the advice role of the board in FBs include the affiliation of board members

to the family (Jaskiewicz & Klein, 2007) and the generational phase (Bammens, Voordeckers, & Gils,

2008).

To justify the research effort on the advisory role of the board, we should proceed by developing our

understanding of how and to what extent boards are involved in strategy, under which circumstances

and in which contexts. Only then we can start testing the assumption that board involvement indeed

leads to value creation and improved organizational performance. Several suggestions have been offered

to further develop our understanding of the advisory board role. For example, scholars should broaden

the themes studied in governance research (Daily, Dalton, & Cannella Jr, 2003; Huse et al., 2011), they

should try to gain access to and use process-oriented data (Forbes & Milliken, 1999; Daily et al., 2003),

broaden the research paradigms underlying the conceptualizations of corporate governance and use

complementary research methods (Zattoni, Douglas, & Judge, 2013; Daily et al., 2003; Huse et al., 2011),

and incorporate alternative theoretical perspectives to agency theory (e.g. Daily et al., 2003; Hambrick,

Werder, & Zajac, 2008; Huse et al., 2011). McNulty, Zattoni, and Douglas (2013) further argue that the

governance research field is in need of theoretical and empirical development through direct

engagement with the actors and settings involved in governance phenomena by using qualitative

research methods.

In this study, we have the unique opportunity to be involved in the set-up of advisory boards in privately-

held family businesses in the Netherlands. Boards and the way that they operate is dependent on the

specific (type of) organization, and on the national context. Different national legal systems and

consequently differences in company law lead to a huge variety in the definition of boards and their

functioning. In the Netherlands, privately-held firms are generally not legally obliged to have a formal

board. However, firms can deliberately choose to have a board, either a formal (supervisory) board or an

4

informal (advisory) board. Whereas formal supervisory boards at a minimum monitor and control

strategic decisions and thereby to a certain extent participate in strategic decision making and are

authorized to select and evaluate the CEO, advisory boards are an informal type of boards with a specific

focus on the resource function. This implies that they provide input on strategic issues, dilemmas and

problems, but are not involved in the actual decision making. Also, advisory boards are not authorized to

appoint and dismiss the CEO. This makes them an accessible instrument and an interesting alternative to

formal supervisory boards for owner-managers of family businesses who do want to have a sounding

board that critically evaluates proposals and plans and brings in critical resources such as expertise, skills

and a network, but at the same time want to remain in charge of strategic decision making themselves.

Dutch privately-held FBs that have an advisory board to create value provide an excellent context to

study the role of boards in strategy since these boards will not function as rubber stamp boards (Pearce

II & Zahra, 1991), but instead are expected to generate as much input as possible.

The purpose of this study is to address the gaps in our understanding of the advisory board role through

a longitudinal in-depth study of the set-up phase of eight Dutch advisory boards in FBs. Taking a practice

perspective, we provide insight into the main reasons to set up an advisory board, how the process of

setting up an advisory board evolves and the procedures and tasks ascribed to the advisory board. Our

findings identify that (1) the set-up of the advisory board is part of a more general professionalization

process of the firm, (2) the main intention to set up an advisory board is to guarantee the continuity of

the firm, (3) the direct cause to set up an advisory board is succession or the need for a sounding board,

and (4) the profile of the ideal member of the advisory board is very similar in the different cases. We

argue that understanding how FBs want and try to create value by setting up an advisory board offers a

new perspective to develop our insights on the strategic task of the board, and calls for extensions to

current theoretical frameworks underpinning FB board contribution. Moreover, by adopting a

longitudinal in-depth methodology which is different from the mainstream, we seek to contribute to the

small but growing group of studies (e.g. Machold & Farquhar, 2013) that are grounded in the field and

are relevant to both theory and practice.

2. GOVERNANCE IN THE NETHERLANDS

Differences between the practical implications of governance systems in different countries are

considerable. The working and composition of the board is dependent on the country history, the

culture, and the governance system (one tier versus two-tier). For example, the average board in the

United Kingdom consists of the CEO, three other executive directors, the chairman of the board and 4 or

5 outside directors. The average board of a company in the United States is composed of the CEO, who is

in most cases also the chairman of the board, and 7 to 8 outside, non-executive directors. Other

executive directors are not members of the board, but do in most cases attend the board meetings. Both

countries have a one-tier governance system but they enact on it in an entirely different way (Calkoen,

2012). The contribution and composition of the board is therefore strongly dependent on the context.

5

The two-tier system in the Netherlands as we know it today has existed since 1623, when the Dutch East

India Company created a supervisory board (Calkoen, 2012). The members of the supervisory board are

assigned by the owners of the company and they have a role in nominating the management board of

the firm, including the CEO (to ensure good management), they should monitor amongst others the

realization of objectives and the financial developments, and assist management with advice (Corporate

Governance Code, III.1.6). The supervisory board should be independent and consider the interests of all

of the stakeholders, including the shareholders (Dutch Civil Code, 1971; article 2.150/250 (934)). The

Dutch corporate governance code defines the task of the supervisory board as follows: “to supervise the

policies of the management board and the general affairs of the company and its affiliated enterprise, as

well as to assist the management board by providing advice” (2008, p. 19). The code sees the role of the

management board as “to manage the company, which means, among other things, that it is responsible

for achieving the company’s aims, the strategy and associated risk profile, the development of results

and corporate social responsibility issues that are relevant to the enterprise. The management board is

accountable for this to the supervisory board and to the general meeting’’ (Dutch corporate governance

code, 2008, p. 11). In comparison to the one-tier boards in the United Kingdom and the United States,

the supervisory boards in the Netherlands spend little time in discussing and developing long-term

strategies (Calkoen, 2012). Instead, they focus on the monitoring and control of the performance of the

company. Since 1 January 2012, Dutch companies have the possibility to have a one-tier board, similar to

the model of the United Kingdom and the United States. According to Bezemer, Peij, de Kruijs, and

Maassen (2014), the main underlying difference between the one-tier and the two-tier board model

relates to the question whether it is desirable to have independent monitors involved in decision-

management. Overall, it can be said that the Dutch corporate boardroom culture is characterized by

consultation and consensus, a plurality of interests, two-tier board system and the old boys network

(Calkoen, 2012). Listed companies in the Netherlands are obliged by law to have a supervisory board.

The law (book 2 of the Dutch Civil Code) is complemented with a governance code, the ‘Code

Tabaksblat’. This code sets a number of recommendations for good governance, and companies have to

indicate in their annual reports whether they comply with the code and if not, explain why.

For privately-held firms, the Dutch law distinguishes between three different company entities, which

have different implications for the control of the owners: the ‘normal’ private limited companies, the

structure regime companies and the enlighted structure regime companies. If privately-held firms fulfill

certain size criteria they enter a three year period and at the end of this period their entity changes from

a private limited company to a so-called structure regime. Firms with a structure regime entity are

obliged to have a supervisory board. The goal of this entity form is to limit the power of the owners and

to assign the responsibility of supervising the policy pursued by the management board to the

supervisory board. Supervisory boards have the authority to approve of certain management board

decisions and to assign and dismiss the management board director(s) of the company. There is also an

enlighted version of the structure regime for firms that do fulfill the size criteria, but in which the

ownership is concentrated in the hands of one or a few persons. In this situation, the supervisory board

does not have the authority to assign and dismiss the management board directors. Owner-managers of

FBs consider this enlighted version of the structure regime less problematic then the ‘normal’ structure

regime entity. The size criteria that firms with a structure regime have to fulfill concern the equity of the

6

firm (more than €16 million), the number of employees (more than 100), and the presence of a

compulsory employees council. A recent descriptive study on governance in the Netherlands shows,

however, that many Dutch FBs are not familiar with the legal obligations concerning the structure regime

(Berent-Braun et al., 2013). Because of the fact that the members of the supervisory board are assigned

by the owners, supervisory boards in Dutch FBs have a remarkable position. When the owner-

manager(s) has/have the majority of the shares, supervisory boards monitor and control the

management board director(s) who in turn assign(s) the members of the supervisory board. Moreover,

the supervisory board often partly consists of family members. When these family members are owners

at the same time they more or less assign themselves. Companies that do not fulfill the size criteria are

free to choose whether they want a board and whether this should be a supervisory board, an advisory

board or possibly both. They have at least a management board existing of one or more executive

directors and a shareholders’ meeting, possibly complemented with a supervisory and/or an advisory

board. The firms in this group of companies free of obligations that do have a supervisory or an advisory

board deliberately choose to have a board. They either choose for a supervisory board, which involves

legal responsibility of the supervisors for the decisions made in the board. Or they choose to have an

advisory board which can have similar functions as the supervisory board but which is more accessible

because the members of the advisory board are not liable for the strategic decisions made and do not

have any real power (Berent-Braun et al., 2013).

Recent research shows that 7.9 per cent of all of the Dutch privately-held firms have either an advisory

or a supervisory board (see Table 1). Small firms appear to have more often an advisory board than a

supervisory board, whereas firms with more than 50 employees more often have a supervisory board.

Berent-Braun et al. (2013) argue that another reason for companies to choose for an advisory board

instead of a supervisory board, besides its legal status, is that individuals are limited by law to sit in a

maximum of five supervisory boards. Advisory boards are not included in this regulation. Having an

advisory board instead of a supervisory board provides possibilities to attract persons that would not

have been able to sit on the supervisory board. When we compare family firms with non-family firms, a

number of differences are visible. Non-family firms have a supervisory board almost twice as often as the

family firms. When considering the total group of firms having a board (so the advisory and the

supervisory boards taken together), the number of board members is significantly lower in the family

firms (2.7 members on average) as compared to the non-family firms (3.5 members on average).

Table 1: Firms with an advisory or supervisory board per number of employees

Advisory board Supervisory board

# employees % all firms % family firms % non-family firms % family firms % non-family firms

2-9 5.5 3.3 2.5 2.5 2.5

10-49 14.7 8.1 6.2 6.1 9.2

50-99 26.7 7.1 8.3 12.9 25.0

100-199 38.6 7.7 10.2 18.0 39.0

Min. 200 49.4 0.0 7.3 21,7 52.7

All firms 7.9 4.0 3.7 3.2 6.0

Source: Berent-Braun et al. (2013)

7

Berent-Braun et al. (2013) provide the following possible explanations for this: difference in firm size, the

willingness of firms to spend money on an advisory or supervisory board, the possibility to get qualified

persons for the position, the willingness to share inside information with outsiders and the need to keep

meetings as short and efficient as possible. In 46 per cent of the cases, one or more members of the

board is a family member and in 28 per cent of the cases a former director becomes a member of the

board in the Dutch privately-held family businesses. It rarely occurs that firms have both an advisory and

a supervisory board: only three family firms and 2 non-family firms out of 664 firms in total. The most

important reasons for both family firms and non-family firms to have a board is the need for an objective

sounding board and to help the directors to be on edge. Significant differences between family firms and

non-family firms were found with monitoring and control reasons for a board: governing the

shareholders’ interest and determining the salary of the directors. These reasons were found to be much

more important to non-family firm CEOs than the family firm CEOs. Also the main task of the board as

considered by the CEO is significantly different between family firms and non-family firms: family firm

CEOs consider the monitoring and control task to be less valuable than the advising task of the board

(6.7 per cent versus 60 per cent). Over thirty per cent of the family firms considers both tasks to be

equally important (Berent-Braun et al., 2013). Family firms also expect their board members to

understand the dynamics of family firms instead of focusing solely on the business side. Advisory and

supervisory boards in family businesses therefore need to focus on the entire business system, including

the parts that overlap with the family system and the ownership system (Tagiuri & Davis, 1982; Berent-

Braun et al., 2013). Privately-held Dutch family firms that do neither have a supervisory board nor an

advisory board indicate that the main reasons for this are the costs involved, no need for advice of

outsiders and insufficient familiarity with the advantages of a board (Berent-Braun et al., 2013).

3. THEORETICAL FOUNDATIONS TO FAMILY BUSINESS ADVISORY BOARD TASKS

Theoretical perspectives used to understand the contribution of boards are various. Zahra and Pearce

(1989) have reviewed empirical research on the contribution of boards on financial performance and

structured it around four research perspectives: the legalistic perspective, the resource dependence

perspective, class hegemony, and agency theory. This structure was adjusted by Stiles and Taylor (2002)

who suggested a classification of six perspectives: agency theory, transaction cost economics,

stewardship theory, resource dependence theory, class hegemony theory and managerial hegemony

theory. These authors already indicated that much of the empirical work supporting the theories provide

little information on the actual operations of the board and eschew detailed analysis of what directors

do. Huse (2007) added property rights theory, stakeholder theory, game theory, social capital and social

movement theory and resource and competence based theories to this list, structuring them around 6

different board tasks (output control task, networking task, internal control task, advisory task, decision

control task, collaboration and mentoring task). These scholars all agree on the fact that the theories

themselves may not be mutually exclusive and that there is strong potential for synthesis to better

understand board contribution. Bammens et al. (2011) reviewed the theoretical literature on boards of

directors within the organizational setting of the FB. Since this study focuses on advisory boards in

8

privately-held FBs, we use the review of Bammens et al. (2011) as a starting point for the theoretical

discussion. Their literature review was structured according to the board tasks: control and advice.

Whereas agency theory is the dominating perspective underlying the control task, Bammens et al. (2011)

found that the FB board’s advisory task can be said to have a multi-theoretic basis consisting of

stewardship theory, the resource based view(RBV)-theory and stakeholder theory.

Stewardship theory builds on a sociological and psychological perspective, arguing that managers in

general should be trusted as good stewards. Stewardship theory considers guiding management in

achieving the mission and objective of the firm as the main task of the board. Trust is expected to work

as an accelerator in creating cohesiveness, openness, generosity, creativity and involvement in the

board. Instead of a need for extrinsic incentives, stewardship theory suggests that managers are

motivated and intrinsically satisfied when they successfully perform, exercise responsibility and authority

and are recognized by their peers and bosses (Stiles & Taylor, 2002). In his review on board task

expectations and theories, Huse (2007) also includes the paternalistic logic which emphasizes that

interactions and structures are related to family values and norms. In the FB board context, stewardship

theory helps explaining the potential for pro-organizational attitudes among organizational decision-

makers and the strong focus on advice versus control (Bammens et al., 2011). The RBV of the firm theory

(Barney, 1991) considers the board and its board members as specific resources, including competence,

knowledge and skills, that create a competitive advantage to the firm by increasing strategic flexibility

and ensuring long term continuity (Huse, 2007). Key assumptions underlying this theory are that

resources are distributed heterogeneously across firms and that they cannot be transferred from one

organization to the next without incurring costs. So the most valuable resources are those that are rare

and difficult to imitate. A core concept used in the RBV of the firm theory is (dynamic) capability, which

represents the coordinated use of resources in order to respond and act competently when the

organization faces problems and challenges. In the FB board context, the resource based view supports

in the analysis of the potential contribution of board members through their professional competences,

skills and expertise (including both firm-specific knowledge and general business knowledge),

complementary to the management board’s knowledge base, to organizational value (Bammens et al.,

2011). From a stakeholder perspective, governance relates to the balance of power within an

organization, while taking the interests of different stakeholders into account. Different groups of

stakeholders include employees, customers, suppliers, owners, society in general, and in case of a family

firm the family members. These different stakeholder groups all have an interest in a well-managed firm

which increases the opportunities for value creation (Freeman & Reed, 1983). In the FB board context,

stakeholder theory can provide a theoretical basis to the role of the board in conflict resolution, by

helping to build consensus by keeping discussions focused on objective facts and promoting balanced

perspectives on firm goals and strategies (Bammens et al., 2011). A perspective which is not discussed by

Bammens et al. (2011), but which is also argued to have an important influence on the functioning of the

board is the insider/outsider perspective. The main idea underlying this perspective in relation to the

organizational setting of the FB is that people behave more rational when ‘strangers’ (outsiders) are

around. According to Huse (2007) the underlying concept of the outsider perspective is independence,

coming from managerial hegemony theory stating that board members in practice are dependent on

management and therefore unable to fulfil the task of managerial opportunism.

9

As Bammens et al. (2011) noticed, the number of studies focusing on the advisory role of the board is

very limited. The theoretical basis used in these studies do not provide insight in how this role is

performed in practice. To a certain extent, stewardship theory, the RBV and stakeholder theory help us

understand why FBs want their boards to have an advisory role. To understand how this role is

performed and which activities constitute the advisory role on the micro-level the multi-theoretic basis

fails. The practice perspective potentially offers an empirical, theoretical and philosophical approach to

study the organizational phenomenon of the Dutch FB advisory board (Feldman & Orlikowski, 2011).

Feldman & Orlikowski (2011) explain that the empirical approach of the practice perspective provides

insight on the ‘what’, the theoretical approach on the ‘how’ and the philosophical approach on the

‘why’. One domain in organization science that has adopted the practice perspective is the strategy

research field. Whereas traditional strategic management research has more or less neglected the role

of emotions, motivations, and interpersonal dynamics in search of explaining strategic change and firm

performance (Jarzabkowski & Spee, 2009), a new approach is developing to analyze the interplay of

practical activities in such varied subject areas as human beliefs, interpersonal relations, organizational

norms, organizational arenas, power relationships, and conflicts of interests in strategy-making. This

approach is the detailed strategy-as-practice (SAP) approach that addresses the micro level activities of

strategic management, studying what people do when they engage in strategy (Jarzabkowski, 2005;

Johnson, Langley, Melin, & Whittington, 2007; Whittington, 2003). It aims to offer a deeper level of

explanation and understanding regarding the nature of strategic activities (Rasche & Chia, 2009). For

example, it enables researchers to identify how strategic issues and actions are influenced by history and

tradition (Fletcher, 1997 in Nordqvist, 2012). The SAP perspective considers strategy as patterns of

activities and argues for a focus on strategy making as it occurs through the actions, interactions, and

negotiations of multiple actors (Floyd, Cornelissen, Wright, & Delios, 2011). Following the SAP

perspective, strategy is something that people do in interaction with others, as opposed to something

that organizations have (Johnson, Melin, & Whittington, 2003; Whittington, 2004). This implies that

strategic work is not the same for all organizations (Nordqvist & Melin, 2010). By focusing on the

behavior and interaction between individuals and balancing attention to these activities with strategic

outcomes, we can observe which strategy practices are effective, instead of making behavioral

assumptions in interpreting quantitative research output.

In this study we aim to combine the multi-theoretic basis as proposed by Bammens et al. (2011) with the

practice perspective to understand the FB advice board task. The practice perspective supports in

delivering insight into the value creating capacity of organizations (the utilization of the resources) and

their sources of sustainable competitive advantage (how the resources are built) by its focus on micro

level activities (Johnson et al., 2003) and by that has the potential to elaborate on the stewardship

theory, the RBV-theory and stakeholder theory. Whereas in the strategy literature the SAP perspective

has received increasing interest over the last decade, it has not looked at the role of the board as a

practice in strategy so far.

10

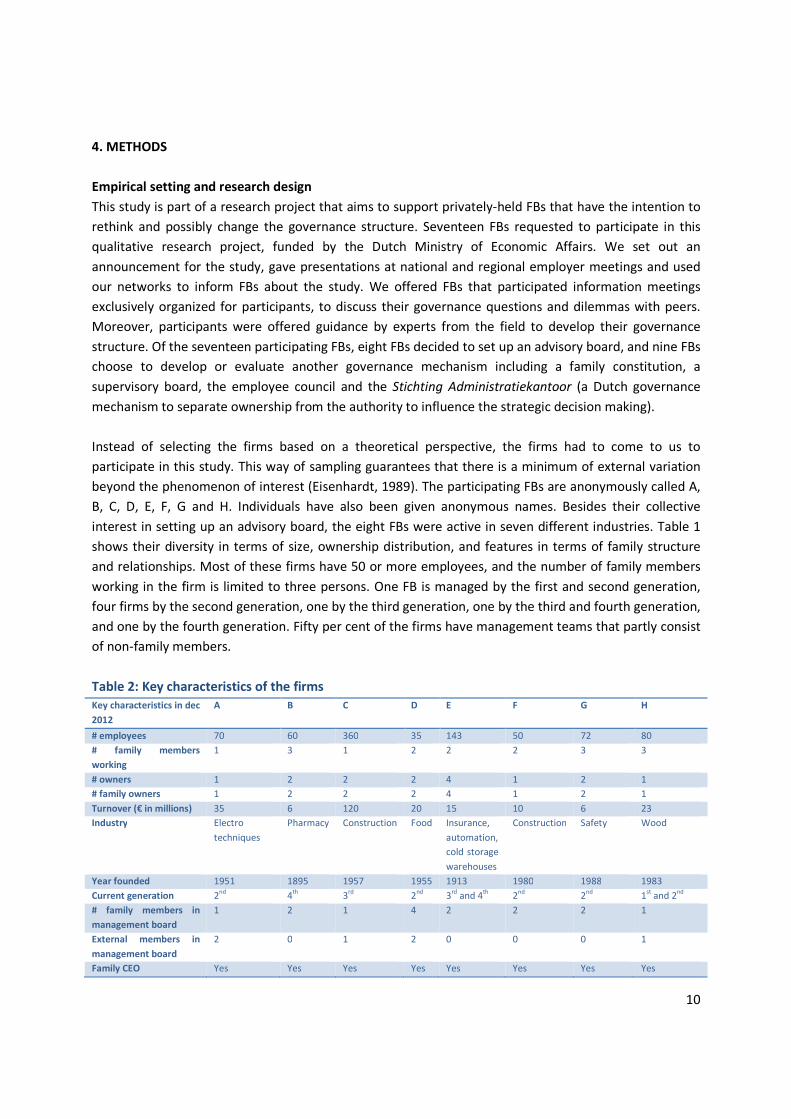

4. METHODS

Empirical setting and research design

This study is part of a research project that aims to support privately-held FBs that have the intention to

rethink and possibly change the governance structure. Seventeen FBs requested to participate in this

qualitative research project, funded by the Dutch Ministry of Economic Affairs. We set out an

announcement for the study, gave presentations at national and regional employer meetings and used

our networks to inform FBs about the study. We offered FBs that participated information meetings

exclusively organized for participants, to discuss their governance questions and dilemmas with peers.

Moreover, participants were offered guidance by experts from the field to develop their governance

structure. Of the seventeen participating FBs, eight FBs decided to set up an advisory board, and nine FBs

choose to develop or evaluate another governance mechanism including a family constitution, a

supervisory board, the employee council and the Stichting Administratiekantoor (a Dutch governance

mechanism to separate ownership from the authority to influence the strategic decision making).

Instead of selecting the firms based on a theoretical perspective, the firms had to come to us to

participate in this study. This way of sampling guarantees that there is a minimum of external variation

beyond the phenomenon of interest (Eisenhardt, 1989). The participating FBs are anonymously called A,

B, C, D, E, F, G and H. Individuals have also been given anonymous names. Besides their collective

interest in setting up an advisory board, the eight FBs were active in seven different industries. Table 1

shows their diversity in terms of size, ownership distribution, and features in terms of family structure

and relationships. Most of these firms have 50 or more employees, and the number of family members

working in the firm is limited to three persons. One FB is managed by the first and second generation,

four firms by the second generation, one by the third generation, one by the third and fourth generation,

and one by the fourth generation. Fifty per cent of the firms have management teams that partly consist

of non-family members.

Table 2: Key characteristics of the firms

Key characteristics in dec

2012

A

B

C

D

E

F

G

H

# employees 70 60 360 35 143 50 72 80

# family members

working

1 3 1 2 2 2 3 3

# owners 1 2 2 2 4 1 2 1

# family owners 1 2 2 2 4 1 2 1

Turnover (€ in millions) 35 6 120 20 15 10 6 23

Industry Electro

techniques

Pharmacy Construction Food Insurance,

automation,

cold storage

warehouses

Construction Safety Wood

Year founded 1951 1895 1957 1955 1913 1980 1988 1983

Current generation 2nd

4th

3rd

2nd

3rd

and 4th

2nd

2nd

1st and 2

nd

# family members in

management board

1 2 1 4 2 2 2 1

External members in

management board

2 0 1 2 0 0 0 1

Family CEO Yes Yes Yes Yes Yes Yes Yes Yes

11

Data collection

Data were collected during the research project, lasting from May 2011 and October 2013. This period

was generally characterized by contracting market conditions and hence presented a period of

heightened environmental uncertainty. The aim was to follow FBs over a longer period of time to

identify the main steps in the process of setting up an AB, but also to facilitate that participants became

familiar with the involvement of the researcher. For this study, we chose to include both primary and

secondary data. The two key primary data sources were in-depth interviews with the main actors (24

interviews in total), and observations during the information meetings held with the participants (8

meetings). We held introductory interviews with the firms to identify the starting point of the process.

Questions were asked regarding the reasons to set up an AB, the expectations of the AB, goals of the

firm, the strategic decision making process and the expected influence of the AB on strategy, and on the

characteristics of the FB. These interviews ranged between 1.5 and 2 hours and were recorded and

transcribed verbatim. After a year, meetings were planned with a FB governance expert with the aim to

provide input for the profiles with which to recruit AB members. Again, these meetings lasted on average

1.5 hours and all were recorded and transcribed verbatim. At the end of the two-year period, interviews

have been held during which questions were asked regarding developments in the governance structure

over the past two years, perceived pitfalls in the process, and again questions regarding the expectations

of the AB, goals of the firm, the strategic decision making process and the expected influence of the AB

on strategy. These interviews lasted a bit shorter, around one hour, and were also recorded and

transcribed verbatim. The interviews were semi-structured which means that the topics discussed were

determined beforehand, but that the questions were asked in an open manner. Secondary sources

included the profiles developed to recruit AB members, strategic plans (if available), organization

structure outlines, marketing documentation, newsletters and the websites. The secondary data sources

provided mainly contextual information about the FBs and their main decision makers.

Data analysis

Data analysis proceeded in two stages. We first developed the individual case summaries by combining,

synthesizing and comparing the transcripts, reflection reports and field notes of the interviews, and

observations during the information meetings. By using specialized software (QDA Dataminer) the

transcripts were coded and analyzed. The transcripts but also the recordings were read and listened to

several times to develop the coding structure. During the data analysis process, through all the steps

(individual case summaries, coding, analyzing) the second author acted as a critical reviewer and

interrogator of the first author. Since the second author was not involved in the data collection and

could therefore only draw upon the tapes and verbatim transcripts, this interrogation was important to

provide results that are as valid as possible (both internally and externally). Where there was

disagreement between the coders, the items were compared and discussed to arrive at a common view

on their categorization. The cases were compared in different ways: we compared the developments of

the individual cases over time and we compared the different cases mutually and looked for differences

and similarities in terms of choices made and the considerations underlying the choices. Tables 3 and 4

provide insight into the structure and ordering of the data. The examples represent researcher-induced

generalizations from the first-order data, to different categories of the reasons why FBs want to have an

12

AB and categories of the process steps of setting up an AB (the how question). The categories derived in

the answers on why and how FBs set up an AB serve as the basis for the subsequent comparison to the

theoretical framework.

5. FINDINGS

By the end of October 2013, of the eight firms that decided to set up an advisory board three FBs had an

operating AB, and five FBs had developed a profile to recruit AB members. In three of the eight FBs, in

which both the current and the new generation are active, the new generation takes the initiative to set

up the AB. These persons view the AB as a resource for the FB and to support their new role as owner-

manager. We start the findings section with offering two concise case descriptions that present

illustrative examples of situations in which FBs choose to have an AB.

Description of FB E

FB E is a fourth generation firm that specializes in three different sectors: insurance services (parent

company, 15 employees), automation (18 employees), and cold storage warehouses (about 100

employees). The financial activities have been organized in the family office (10 employees). The FB is run

by John and his daughter Anna. Anna has two sisters and the three of them own the company together

with equal ownership positions. Formally, on paper, John is the CEO of the FB. However, in practice Anna

is in charge and her father takes a step back in the daily operations. Anna (38 years old) entered the FB in

2006 after having worked for a large attorney office. Anna’s youngest sister has worked in the FB for a

very short period of time.

The family thinks in generations. This implies that continuity is the main goal of the FB. However, because

of the diverse business activities it is possible that one of the divisions will be sold in the future. Anna

wants to create more time for strategy formulation. Strategic issues that the FB currently deals with

include the professionalization of the HRM-structure and component in the business, structuring

communication between departments and managers, developing a strategic plan. The family members

have not made any explicit agreements concerning their roles in the FB. Anna wants to prevent that the

sisters have different ideas concerning the family involvement in the business in the event that her father

would suddenly pass away. She wants to safeguard the continuity of the firm by a family constitution that

sets regulations for the involvement of the family members. Moreover, she wants her sisters to be well

informed about the developments of the firm. This matter has become urgent after the involvement of

her youngest sister in the business. This did not work out well because she was not qualified for the job.

Anna wants to professionalize the FB and prepare for the future by setting up new governance

instruments: a family constitution and an AB. The family constitution should lay down the norms and

values of the family, also to guide the future generations. The AB should provide support Anna in dealing

with the strategic issues and in further growth of the FB.

Anna decided to start with developing a family constitution first. Together with an FB expert and her

father she developed a family constitution that discusses a number of different topics. She then discussed

13

the concept version of the family constitution with her sisters and made some minor adjustments

afterwards. Topics discussed in the family constitution include:

• the frequency, contents and content of family meetings (involving at least the three sisters);

• The way in which the AB and the STAK are to be composed and their role in strategic decision

making in the FB;

• Dividend policy (continuity of the FB always comes first);

• Employment policy for family members (management quality should be guaranteed);

• Non-family members should not be able to form a majority position in strategic decision making;

• Norms and values of the FB;

• External communication about the FB;

• Guidelines for the succession process;

• Ownership position;

• Principles relating to autonomous growth;

• Possibilities for adjusting the family constitution in the future.

The family constitution should function as the family regulations in the FB. Some of the agreements laid

down in the family constitution are also included in the formal regulations.

John would have liked to take the role of chair in the AB. However, Anna feels that this would possibly

hinder her in setting out her own plans. She would prefer two outsiders, of whom one would take the role

of chair. Her father could be the third person in the AB. Both John and Anna want to have committed AB

members and are willing to invest time and money to start up the new governance mechanism. They

both feel that they do not need persons with expertise on the specific business activities. Instead, they

want AB members with experience and knowledge of general business management, affinity with the FB

culture, diplomacy and an objective view on strategic issues. They hope to get access to a new network

via the AB members. John and Anna are now recruiting members for the AB. The period of two years has

been necessary to get a clear view on the new governance structure of the FB.

Description of FB G

FB G has been founded in 1988 and has grown into a medium-sized firm (currently about 100 employees)

that offers safety solutions to organizations: e-learning tools, training, and consultancy. The FB has been

founded by the father of the current owner-managers. Sam and Max run and own the FB together since

2007 when they succeeded their father. Besides Sam and Max only one other family member is involved

in the business. Sam and Max do not consider the firm to be a real FB, continuity is however the main

goal of the FB. They specifically indicate that they do not want their family to be dependent on the

business which implies that it is not obvious for them that other family members would possibly enter the

business. The firm operates in an industry that is considered to be a growth market, and Max and Sam

see a lot of opportunities to act proactive in this dynamic environment.

The strategy of the FB is determined by Max and Sam in close consultation with the management team. It

has been five years since the brothers succeeded their father and they actively search for further

development of the FB. Market demand is changing quickly which requires adjustments in personnel

14

policies. Moreover, with the fast E-learning market developments, the FB wants to embed this service

more strongly in its organization. The transition from offline to online (and blended) learning has started,

but has major consequences for the FB activities, personnel management and organizational structure.

This transition has not been finalized yet. Sam and Max indicate that they lack the specific knowledge and

expertise to fully utilize the current market potential. They surround themselves with people who they can

ask for advice in an informal way, but they are interested in the possibility to set up an AB. They do not

see any advantages of a formal supervisory board over the advisory board. They have the following

expectations of the AB:

• a sounding board with persons who bring in expertise, inspiration and critically reflect on

strategic issues;

• strategy discussed on a regular basis. The AB should support in determining the long term

strategy and keep a close watch on its suitability;

• less dependence on commercial services of ad hoc consultants and advisors;

• flexible to adjust to the developments of the firm, for example by working with maximum ‘job’

periods of three years;

• a controlling mechanism in the sense that it should check to what extent strategic decisions align

with the goals of the FB.

The persons sitting in the AB should be outsiders, but they should be well informed about the major

developments of the FB. They should be easily accessible and available in between meetings as well.

It has taken the firm two years to set up a profile for the ideal AB members. This is due to the fact that

the organizational developments in response to the fast changes in the market have been time

consuming. Moreover, Max and Sam feel that setting up the AB is not very urgent.

Reasons to set up an AB – the ‘why’ question

The analysis shows that FBs can have various reasons to set up an AB. Table 3 provides an overview of

the different reasons with illustrative examples. For the FBs that participated in this study, the reasons

most often given include the wish of the owner-manager to have a sounding board, professionalization,

succession, and the need for a controlling mechanism. Moreover, the FBs expect the AB to add value by

bringing in expertise, knowledge and skills and a network which they can use as acquisition mechanism

to gain new information.

Generally, the participants consider the AB to be an attractive alternative to the formal supervisory

board. Participants indicate that they expect the AB to offer similar advantages without providing formal

decision making authority to board members, and they consider the supervisory board to be too formal,

too serious. Another issue is the ownership paradox (p.7: when the owner-manager(s) has/have the

majority of the shares, supervisory boards monitor and control the management board director(s) who

in turn assign(s) the members of the supervisory board).

15

Table 3: coding of reasons to set up an AB and examples

Examples of 1st

order data 2nd

order themes Aggregate 2nd Order

Dimensions:

Reason for AB

B: “I expect them not to communicate on one specific theme, but to

support in strategy in general. They should be critical in strategic

issues, but also on financial issues. I hope that by providing support

we can increase the speed of evaluating strategic alternatives.”

Better informed decision

making / critical reflection / it

is lonely at the top

Need for a sounding

board (5 cases)

A: “The AB members should not be selected from the foundation

'friends of [name company]. It should be strangers’ eyes.”

D: “I feel comfortable in discussing some issues with persons that are

not part of the management team, because communication on these

[family] issues may be harmful to the firm”.

E: “we see an important role for our accountant. He knows the

company very well. Together with my father and an outsider he could

sit in the AB”.

G: “a sounding board, sparring partner or the like with outsiders that

would be good in my view. The accountant has an important role as

sparring partner, but is not completely independent”.

Insider versus outsider

A: “the tendency is to develop a blind spot. Tunnel vision. How to

create an open view? I struggle with these issues”.

Fear for tunnel vision

D: “We want to professionalize and report agreements on strategic

decision making”.

F: “we want to professionalize the business, also the information

flows, lay down some agreements… in the family business we often

communicate casually and formal meetings that are well reported are

lacking”

Reporting agreements (need

for clarification)

Professionalization of

governance structure

in general (7 cases)

E: “I see the advisory board as a continuation of the family

constitution. It provides security and clarity”.

H: “The AB should be a mirror to the owner-manager. It should keep

the owner-manager from mistakes and be some kind of security

actor”.

Security

C: “the AB should have added value for the company. However, it is

assigned by the owner. In consultation with the AB these roles and

interests should be dealt with”.

Role clarification (family

versus owner vs manager)

A: “Strategy realisation remains a challenge in these hectic times. To

keep focusing on goals that matter for [name company]”.

G: “You realize that you tend to spend all your time on daily

operations”.

Making time for strategy

E: “If my father would pass away, I only have the accountant as a

sparring partner. That makes it very vulnerable”.

Making arrangements for

possibility that something

happens to owner-manager

B: “The AB is something that I have come up with”

E: “because I represent the new generation in the business and run

into practical issues that I’d like to discuss with others. I don’t look for

solutions, but I would like to have some advice”

Need of incumbent to have a

sounding board

Succession (5 cases) H: “It is important to determine the course of the company now

succession is coming up in a few years time. Employees feel that

things are going to change, so it is important to be transparent and

clear. An AB could guide this process”.

Need of successor to arrange

and plan succession well

B: “I expect the AB to guide my father by asking questions such as:

‘how are you planning to take distance of the company? What are

you going to do after retirement? What is your planning regarding

retirement?’”

C: “My father needs to step down from operations. He should be

relieved from the daily issues, but we need to use his knowledge,

Role transition from owner-

manager to AB member

16

experience and network”.

F: “We want to channel the advice of my father and we think that

being one of the AB members would be a good solution for him and

for us”.

G: “the AB could act as a controlling mechanism”.

Being accountable for major

decisions

Need for control (2

cases) A: “The AB members can check whether we act in line with our

goals”.

How do strategic decisions

and activities align with

mission, vision and goals

A: “when we have questions on specific themes, we can ask for

advice”.

G: “the AB could provide support on things that we know little about

ourselves. We don’t think that we can know it all. By the AB we get

less dependent on commercial parties”.

Market knowledge in terms

of innovation and

development

Resources (3 cases)

A: “I look for inspiration; a sounding board, strategy, guidance”.

H: “The AB looks at things from a different angle. We need people

how support in creating dynamics and inspiration”.

Inspiration on strategy

The process of setting up an advisory board – the ‘how’ question

The process that the FBs go through in setting up an AB has shown to be rather similar across the cases.

However, the pace by which FBs go through this process differs substantively. It is a process that can last

a few months to a few years. The pace is slowed down by urgent organizational matters and

transformations that absorb the time of the CEO (FB F, FB G), by differences in attitudes towards and

expectations from the AB of the different actors involved (FB E, FB F, FB H), by an awareness of the need

for the AB that grows really slow (FB H), or by private issues (FB G).

FB D: “I have shared my ideas on setting up an AB with the other members of the management board.

Some members wondered whether it would be a good idea to have an AB in such a relatively small

business. They had some objections and were quite critical. I have motivated my idea and explained my

arguments to have it and eventually we have decided unanimously to get started”.

It is questionable whether FB C will ever set up a real AB because in the recruitment process the CEO is

hesitant towards hiring real independent AB members. The CEO claims to have hired an outsider,

however this person comes from his own network. It is questionable how independent this outsider

really is. This is illustrated by the following quote:

FB C: “Eventually we want an AB with 4 members, consisting of two former managers and two outsiders.

One of the former managers is my father, he will also be the chair of the AB. We have decided to use our

own network to look for the first outsider. The second outsider will only be recruited after the second

insider has started. This gives us the possibility to get used to the mechanism”.

Table 4 provides an overview of the subsequent steps taken during the process of setting up the AB.

17

Table 4: coding of process of setting up an AB and examples

Step in process Examples

1. Develop awareness

on the reason why FBs

feels it needs an AB

• Better informed decision making

• Ownership structure versus decision-making capacity

• …see Table 3

2. Task identification • Guarantee knowledge development

• Access to new network

• Sounding board function

• Inspiration

• Control

3. Determine size and

composition

• Outsider/insider

• Who will ‘sit in’ (the CEO or also other persons, possibly the successor)

4. Develop AB member

profile, composing of:

• FB description

• AB composition

• Tasks of AB

• General qualifications such as broad experience in business and affinity

with the FB and its norms and values

• Specific qualifications such as technical knowledge, or marketing expertise,

etc.

• Personal characteristics such as analytical skills, strong independent

mindset etc.

• Specific tasks of the chair

5. Recruitment • Network mobilization (via colleague entrepreneurs, sector associations

etc.)

• Approach employers’ organizations

• Use professional services (e.g. via INSEAD)

6. Start off • Information sharing with AB members

• Structuring the meeting

• Frequency of meetings

First, the CEO and possibly other actors involved develop an awareness on the reason why they feel they

need an AB. The first step of the process therefore relates to the ´why´ question (Table 3). Then, the CEO

and his/her companions identify the most important task(s) to be assigned to the AB and how these

relate to the other governance mechanisms of the firm. The FBs involved in the study expect the

members to be independent and provide a new perspective on the business.

FB A: “If you recruit AB members from your own network, you run the risk to, I would not dear to say

less business, but get more friendly support.”

For most of the respondents, it is not clear for whom or for what the AB should be active: for the owner-

manager, for the business, or for the owners. Generally however, the comparison of the cases shows

that for most firms the advisory role involves having a sounding board, gaining access to a new network,

18

expertise and skills, get inspiration for strategic issues and being controlled in the sense that activities

performed should be compared to the strategic direction set in the strategic plan, as explained by the

following respondents:

“FB G: “what is the market? Is it safety? Or is it selling training? Physically or via e-learning?”

FB H: “you need people in the AB who inspire, who provide input that we have not thought about

before”.

After the main task had been identified, the actors involved would continue with determining the AB size

and its composition (insiders versus outsiders). Moreover, they developed thoughts about who would

possibly attend the meetings. In general, this was supposed to be the CEO, possibly augmented with

other members of the management board or other family members.

FB F: “We see a role for our accountant in the AB, because he is so familiar to the FB. Together with my

father and one outsider he could form the AB”.

They continued with setting up a profile of the ideal AB members, which could later on be used for

recruitment purposes. This last step (recruitment) was a difficult step for the FBs involved in the study,

because they had no idea who to turn to or how to get into contact with potential AB members.

FB B: “Finding AB members, well I do not have an appropriate network to recruit these people.

Preferably, to keep things as objective as possible, I look for someone I do not know already”.

To develop the AB member profile one needed to think about the requested knowledge, qualities,

experience and skills. These qualifications were then written down and transformed to a job offer which

supported the quest for members. All eight FBs involved made such a profile. Even though the

participating firms are very different, operate in different industries and engage in various activities, the

profile of the advisory members were very similar. The analysis shows that AB members should primarily

be able to give advice in the field of strategy and organizational development. Also advanced knowledge

of the field in which the FBs are active and experience as manager or entrepreneur is considered to be of

crucial importance. Only three of the eight FBs started working with the AB during the research period.

Interesting to note is that these three firms struggle with the power balance between the management

board and the AB members. In principle, the management board can choose to ignore the advice given

by the AB. Whereas the actors involved understand that the AB members will leave when time after time

advice is ignored, they also want to retain enough freedom to take strategic decisions that they think is

best:

FB C: “When the AB indicates that it would be best to go right, but the CEO feels that he should go left,

then he should be able to act as he thinks it is best”.

During the information meetings AB members indicate that it happens every now and then that the CEO

acts against the advice of the AB, but that in a normal situation the CEO should have to back up his

19

actions with sufficient arguments. This is possibly an issue that plays a role at the start of working with

the AB and becomes more natural once the AB has been ‘in function’ for quite some time.

6. DISCUSSION

In this study we addressed the question of why and how privately-held FBs in the Netherlands set up an

AB. A growing stream of literature on board contribution has investigated the antecedents (such as

composition) and consequences (financial performance of the firm) of board tasks. Most of these studies

conceptualize the tasks as discrete categories, do not explain the board context and use quantitative

methods. In line with the study of Machold and Farquhar (2013), this study aims to address unanswered

questions relating to the micro level activities of advisory boards. Our focus was on the organizational

setting of the family business. It has addressed the main reasons why FBs choose to have an AB and on

the process that the go through when setting up the AB. Our results provide a number of fresh insights

into the motivation of Dutch FBs to have an AB, in the tasks assigned to the advisory board, its relevance

in relation to formal supervisory boards in the Netherlands, the steps that the FBs go through when

setting up the AB and the influences on the pace with which this happens. The analysis shows that the

why question can be linked to the resource based view. Table 3 shows 5 reasons why FBs choose to have

an AB: the AB is seen as a resource that makes strategy formulation and implementation a less lonely

activity (need for sounding board), that provides clarity on agreements and roles of actors

(professionalization of governance structure in general), that supports in the succession process

(succession), reviews activities against strategic goals (need for control) and inspires, reflects and brings

in knowledge and expertise in the elaboration of strategic issues (resources). The process that the FBs go

through consists of 6 steps. The answer to the why and how question can both be interpreted by the

multi-theoretic-basis as suggested by Bammens et al. (2011). Stewardship theory helps us to understand

the money and time invested to pay attention to the strategy of the firm. The findings have shown that

most businesses do not have a strategic plan on paper. It is in their heads, most respondents say.

Moreover, stewardship theory provides insight in the reason why the CEO and the management board is

willing to involve independent outsiders. The CEO is willing to step out of his/her comfort zone with the

expectation to create value for the business. The stakeholder view provides support for the finding that a

number of FBs want to set up an AB to support the succession process, in which many different

stakeholders are involved. However, also the finding that FBs aim to provide clarity how the AB relates to

the shareholders’ meeting or the family council (professionalization) indicates that the interests of the

different stakeholders are taken into account in the governance of the firm. We propose that relating the

multi-theoretic basis to practice theory helps to understand how the setting up process of the AB and in

a later phase the functioning of the AB itself are resourced at the micro-level. With resourcing we imply

to derive value from the process by practicing specific activities (Feldman & Orlikowski, 2011). The

findings have been presented in the Figure 1.

Scholars have argued that we need to get closer to the topic of interest if we want to understand better

whether and how boards add value to the firm and how board processes and dynamics impact on

strategy (Pugliese et al., 2009; Zattoni et al., 2013). The comparative character of the multiple case study

20

design, combined with longitudinal data from different sources, enabled us to address questions relating

to the implementation process and contextual influences.

Figure 1: Emergent model of resourcing the AB

Next to formal boards, advisory boards seem to be a promising and accessible governance mechanism,

for FBs with a specific focus on the advice task. The advisory board is acknowledged and recognized by

businesses and practitioners, but it has not been a research topic so far. Research on advisory boards in

firms is almost non-existent. Existing studies on advisory boards almost exclusively focus on public

organizations such as schools, hospitals, local authorities, instead of businesses. There are a few

exceptions. Morkel and Posner (2002) have studied how advisory boards operate in the context of new

ventures, where advisory boards are rather commonplace. They note that advisory boards can provide

the director(s) the benefits of experience, expert knowledge, contacts and credibility without taking on

the legal and administrative responsibilities associated with joining a board of directors or a supervisory

board. Moreover, since there are no legal requirements involved, firms can decide themselves on the

size of the advisory board, the frequency of the meetings, the terms and responsibilities of service. So

whereas an advisory board can provide similar resources as a board of directors or a supervisory board,

it is less official and therefore potentially more accessible to firms. Akers and Giacomino (2004) have

looked at the use of advisory boards in the context of small firms. They found that only a few number of

small firms had an advisory board, but those that did were very satisfied with it. Whereas the popularity

of advisory boards might have increased over the years, practice shows that also nowadays the use of

advisory boards is still limited (Berent-Braun et al., 2013). A possible explanation for this is that many

small business owners are not aware of the phenomenon of the advisory board.

This study has shown that FBs expect to benefit from the resources provided by the advisory board

without fearing to lose control because the power remains in the hands of the owners (Gersick & Feliu,

Family business context

- Characteristics

- Governance situation

AB

Composition

Identified need for

AB (why):

- sounding board

- professionalization

- succession

- need for control

- resources

Setting up

the AB

(Table 4)

Resourcing

the AB

Value

creation:

Performance

evaluation in

relation to

tasks ascribed

21

2013). Blumentritt (2006) found that there exists a strong correlation between various forms of planning

(succession planning and strategic planning) and the presence of an advisory board in FBs. Lambrecht

and Lievens (2008) argue that advisory boards can be used in family firms as a transitional stage towards

a formal board. Whereas this suggestion makes sense and can be a promising governance route for

family firms to take when they grow or professionalize, it is not backed up by any empirical assessments.

We acknowledge that this study does not inform us on the activities and practices performed in the

advisory board. However, research has shown that board activities depend on contextual issues such as

board composition. With this study we have aimed to identify the objectives that FBs have with the AB

that can eventually be linked to actual practices and activities performed.

REFERENCES

Bammens, Y., Voordeckers, W., & Gils, A. (2008). Boards of directors in family firms: a generational

perspective. Small Business Economics, 31(2), 163-180.

Bammens, Y., Voordeckers, W., & Van Gils, A. (2011). Boards of Directors in Family Businesses: A

Literature Review and Research Agenda. International Journal of Management Reviews, 13(2),

134-152.

Barney, J. (1991). Firm Resources and Sustained Competitive Advantage. Journal of Management, 17(1),

99.

Berent-Braun, M.M., Bus, C.A.C.J., Van Dijk, C.C., Van Druten, E.W.J.A., Flören, R.H., Van den Hurk, Y., . . .

Webbink, R. (2013). Goed ondernemingsbestuur bij familiebedrijven: Baker Tilly Berk

NV/Nyenrode Business Universiteit.

Bezemer, P.-J., Peij, S., de Kruijs, L., & Maassen, G. (2014). How two-tier boards can be more effective.

Corporate Governance, 14(1), 15-31.

Blumentritt, T. (2006). The Relationship Between Boards and Planning in Family Businesses. Family

Business Review, 19(1), 65-72.

Calkoen, W.J.L. (2012). The one-tier board in the changing and converting world of corporate governance.

A comparative study of boards in the UK, the US and the Netherlands. Deventer: Kluwer.

Daily, C.M., Dalton, D.R., & Cannella Jr, A.A. (2003). Corporate governance: decades of dialogue and data

Academy of Management Review, 28(3), 371-382.

Eisenhardt, K.M. (1989). Building Theories From Case Study Research. Academy of Management. The

Academy of Management Review, 14(4), 532.

Feldman, M.S., & Orlikowski, W.J. (2011). Theorizing Practice and Practicing Theory. Organization

Science, 22(5), 1240-1253.

Floyd, S.W., Cornelissen, J.P., Wright, M., & Delios, A. (2011). Processes and Practices of Strategizing and

Organizing: Review, Development, and the Role of Bridging and Umbrella Constructs. Journal of

Management Studies, 48(5), 933-952.

Forbes, D.P., & Milliken, F.J. (1999). Cognition and Corporate Governance: Understanding Boards of

Directors as Strategic Decision-Making Groups. Academy of Management Review, 24(3), 489-

505.

Freeman, R.E., & Reed, D.L. (1983). Stockholders and Stakeholders: A New Perspective on Corporate

Governance. California Management Review, 25(3), 88-106.

Gersick, K.E., & Feliu, N. (2013). Governing the family enterprise: practices, performance and research. In

L. Melin, M. Nordqvist & P. Sharma (Eds.), The Sage Handbook of Family Business: Sage

Publications Ltd.

22

Hambrick, D.C., Werder, A.v., & Zajac, E.J. (2008). New Directions in Corporate Governance Research.

Organization Science, 19(3), 381-385.

Hendry, K., & Kiel, G.C. (2004). The Role of the Board in Firm Strategy: integrating agency and

organisational control perspectives. Corporate Governance: An International Review, 12(4), 500-

520.

Hendry, K., Kiel, G.C., & Nicholson, G. (2010). How Boards Strategise: A Strategy as Practice View. Long

Range Planning, 43(1), 33-56.

Huse, M. (2007). Boards, governance and value creation. The human side of corporate governance.

Cambridge: Cambridge University press.

Huse, M., Hoskisson, R., Zattoni, A., & Viganò, R. (2011). New perspectives on board research: changing

the research agenda. Journal of Management & Governance, 15(1 ), 5-28.

Jarzabkowski, P. (2005). Strategy as Practice: an Activity-Based View. London: Sage.

Jarzabkowski, P., & Spee, A.P. (2009). Strategy-as-practice: A review and future directions for the field.

International Journal of Management Reviews, 11(1), 69-95.

Jaskiewicz, P., & Klein, S. (2007). The impact of goal alignment on board composition and board size in

family businesses. Journal of Business Research, 60(10), 1080-1089.

Johnson, G., Langley, A., Melin, L., & Whittington, R. (2007). Strategy as Practice, Research Directions and

Resources. Cambridge: Cambridge University Press.

Johnson, G., Melin, L., & Whittington, R. (2003). Guest Editors’ Introduction. Journal of Management

Studies, 40(1), 3-22.

Lambrecht, J., & Lievens, J. (2008). Pruning the Family Tree: An Unexplored Path to Family Business

Continuity and Family Harmony. Family Business Review, 21(4), 295-313.

Levrau, A. (2007). Corporate governance and the board of directors: a qualitative-oriented inquiry into

the determinants of board effectiveness. (doctorate), Ghent University.

Machold, S., & Farquhar, S. (2013). Board Task Evolution: A Longitudinal Field Study in the UK. Corporate

Governance: An International Review, 21(2), 147-164.

McNulty, T., Zattoni, A., & Douglas, T. (2013). Developing Corporate Governance Research through

Qualitative Methods: A Review of Previous Studies. Corporate Governance: An International

Review, 21(2), 183-198.

Morkel, A., & Posner, B. (2002). Investigating the effectiveness of corporate advisory boards. Corporate

Governance, 2(3), 4 - 12.

Mustakallio, M., Autio, E., & Zahra, S.A. (2002). Relational and Contractual Governance in Family Firms:

Effects on Strategic Decision Making. Family Business Review, 15(3), 205-222.

Nordqvist, M. (2012). Understanding strategy processes in family firms: Exploring the roles of actors and

arenas. International Small Business Journal, 30(1), 24-40.

Nordqvist, M., & Melin, L. (2010). The promise of the strategy as practice perspective for family business

strategy research. Journal of Family Business Strategy, 1(1), 15-25.

Pearce II, J.A., & Zahra, S.A. (1991). The Relative Power of CEOs and Boards of Directors: Associations

with Corporate Performance. Strategic Management Journal, 12(2), 135-153.

Pugliese, A., Bezemer, P.-J., Zattoni, A., Huse, M., Van den Bosch, F.A.J., & Volberda, H.W. (2009). Boards

of Directors' Contribution to Strategy: A Literature Review and Research Agenda. Corporate

Governance: An International Review, 17(3), 292-306.

Rasche, A., & Chia, R. (2009). Researching Strategy Practices: A Genealogical Social Theory Perspective.

Organization Studies, 30(7), 713-734.

Stiles, P., & Taylor, B. (2002). Boards at work: how directors view their roles and responsibilities. New

York Oxford University Press.

Tagiuri, R., & Davis, J.A. (1982). The advantages and disadvantages of the family business.

23

Uhlaner, L., Wright, M., & Huse, M. (2007). Private Firms and Corporate Governance: An Integrated

Economic and Management Perspective. Small Business Economics, 29(3), 225-241.

Van Den Heuvel, J., Van Gils, A., & Voordeckers, W. (2006). Board Roles in Small and Medium-Sized

Family Businesses: performance and importance. Corporate Governance: An International

Review, 14(5), 467-485.

Whittington, R. (2003). The Work of Strategizing and Organizing: For a Practice Perspective. Strategic

Organization, 1(1), 117-125.

Whittington, R. (2004). Strategy after modernism: recovering practice. European Management Review,

1(1), 62-68.

Zahra, S.A., & Pearce, J.A. (1989). Boards of Directors and Corporate Financial Performance: A Review

and Integrative Model. Journal of Management, 15(2), 291-334.

Zattoni, A., Douglas, T., & Judge, W. (2013). Developing Corporate Governance Theory through

Qualitative Research. Corporate Governance: An International Review, 21(2), 119-122.

Zattoni, A., & Van Ees, H. (2012). How to Contribute to the Development of a Global Understanding of

Corporate Governance? Reflections from Submitted and Published Articles in CGIR. Corporate

Governance: An International Review, 20(1), 106-118.