panera bread 2008 annual shareholders...

TRANSCRIPT

Panera Bread 2008 Annual Shareholders Meeting

2

Disclaimer

Matters discussed in this presentation, including any discussion or impact, express or implied, on the Company's anticipated

growth, and future earnings per share, contain forward–looking statements within the meaning of Section 27A of the Securities

Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All forward-looking statements made during this

presentation are made only as of this date, and we do not undertake any obligation to publicly update or correct any forward-

looking statements to reflect events or circumstances that occur or which we hereafter become aware after this date. The

statements identified by the words “believe”, “positioned”, “estimate”, “project”, “target”, “continue”, “will”, “intend”, “expect”,

“future”, “anticipates”, “preliminary” and similar expressions express management's present belief, expectations or intentions

regarding the Company’s future performance. The Company’s actual results could differ materially from those set forth in the

forward–looking statements due to known and unknown risks and uncertainties and could be negatively impacted by a number

of factors. These factors include but are not limited to the following: the availability of sufficient capital to the Company and the

developers party to franchise development agreements with the Company; variations in the number and timing of bakery–cafe

openings; public acceptance of new bakery–cafes; competition; national and regional weather conditions; changes in restaurant

operating costs, particularly food and labor; and other factors that may affect retailers in general. These and other risks are

discussed from time to time in the Company’s SEC reports, including its Form 10–K for the fiscal year ended December 25, 2008.

3

The Panera Bread Story

Strong and stable unit volumes driven by high consumer acceptance- $2.0 million AUV is highest of any public concept outside casual dining

- 87% of units have a greater than $1.5 million AUV

- 2008 YTD (as of April 22) company-owned comparable store sales growth of 4.38%

Unit level economics drive unit growth- 40% cash-on-cash, store level ROI

- 21% unit CAGR from 2002 to 2007

- 1,252 bakery-cafes open at end of Q1 2008 (543 company and 709 franchise)

Unit Growth and Operating leverage leads to strong corporate performance- From 2001 to 2006, 43% average annual EPS growth; 2007 EPS flat

- From January 2, 1998 to May 19, 2008 stock appreciation of nearly 1,300% or 29% annually

4

Unit Performance: Average Unit Volumes Are Better Than All But Casual Dining

T.G.I. Friday’s $3,444

Outback Steakhouse $3,355

Red Robin Gourmet Burgers & Spirits $3,172Chili’s Grill & Bar $3,063Applebee’s Neighborhood Grill & Bar $2,542Buffalo Wild Wings Grill & Bar $2,175Ruby Tuesday $2,141PANERA BREAD $2,007McDonald’s $1,974Chipotle Mexican Grill $1,555Wendy’s $1,304

Burger King $1,175

Boston Market $1,088KFC $978Arby’s $904Dunkin’ Donuts $844Starbucks $768Pizza Hut $689Quizno’s $406Subway $382

QUIC

K CA

SUAL

and

FAS

T FO

ODCA

SUAL

DIN

ING

Note: 2006 AUVs, in thousands of dollars. Source: Nation’s Restaurant News Top 100 Report; June 25, 2007

5

Average 2-Year Comp. Store Sales Growth of 7.4%

Com

para

ble

Stor

e Sa

les G

row

th %

5.5Yr. Avg. of 7.4%

QTD as of 4/22/08

6

Why? Consumers Rank Panera the Definitive Industry Leader

Ranked #1 or #2 in customer satisfaction on Sandelman survey five years in a row- Sandelman & Associates survey of 84,000 customers at 138 food service concepts over 70 markets

- 57% of customers ranked Panera as “excellent” on their last visit

Ranked “Most Popular” & “Top Food” among all fast food chains by Zagat for 2007

Ranked among the best in the industry in food quality five years in a row- Restaurants and Institutions “Choice in Chains” survey of 7,000 customers

Named “Chain of the Year” by Restaurant Hospitality and “Brand of the Year” by Fast Casual in 2006

7

High AUVs Drive Among the Most Attractive Store-Level ROIs in the Industry

Cash Flow $000, except % (a)

Average Net Sales/Unit $1,974

Unit EBITDA $332

Unit Margin % 17%

Invested Capital $000 (b)

Investment Before Overhead $831

Capitalized Overhead $82

Investment After Capitalized Overhead $913

Cash-On-Cash ROI

Before Capitalized Overhead 40%

After Capitalized Overhead 36%

(a) Trailing 52 weeks ending March 25, 2008 for 349 company-owned Panera bakery-cafes opened before March 25, 2008 (excluding acquisitions)(b) Average investment cost for 349 company-owned Panera bakery-cafes opened before March 25, 2008 (excluding acquisitions)

8

High ROIs Fuel Significant Unit Growth

81 90 110 132 173 226311

391532 572

102172

259346

429

515

566

636

698758

0

200

400

600

800

1000

1200

1400

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Proj.

Franchise

Company

262 total

369 total

478 total

183 total

602 total

741 total

877 total

Tota

l Num

ber o

f Bak

ery-

Cafe

s

1,027 total

1,330 total1,230

total

9

Panera Has Become the Clear National LeaderWith Significant Development Potential Still Available

Note: 1,252 Bakery-cafes open as of 3/25/08

Maine

JacksonvilleOrlandoSoutheast FloridaTampa/Sarasota

Raleigh-DurhamCharlotteWinston-SalemTennessee. Western NC, Northern GASouth CarolinaAtlanta

Boston Metro

Connecticut &Rhode Island, So Mass

Upstate New YorkJersey/Long IslandPhiladelphia MetroBaltimoreNorthern Virginia/DCWest VirginiaWestern Virginia

Northern California

Houston

ToledoClevelandPittsburgh

Oklahoma

Denver

Las Vegas

Dallas

Alabama

St. LouisCentral MOSW MissouriNW Arkansas

KentuckyColumbusCincinnati

Central PA

Kansas City32

25

5

20

17

17

27

Milwaukee

20

Nebraska18

12

MinneapolisRochester

243

16

81

DetroitGrand Rapids

Indianapolis

1442

Chicago

29

Central IllinoisEastern & Central Iowa

13

33

13

25

30

523

7

3

4

34

41

4935

13

69

34

27

1313

11

12

3210

25

17

21

26

10

31

4Pensacola

239

SouthernCalifornia

48

21Pacific Northwest

1South Dakota

31 Arizona

4

Salt Lake City

Market Penetration LevelsBakery-Cafe to Population Ratio

1 : 100K or less (high penetration)1 : 150K1 : 200K1 : 250K (low penetration)

10

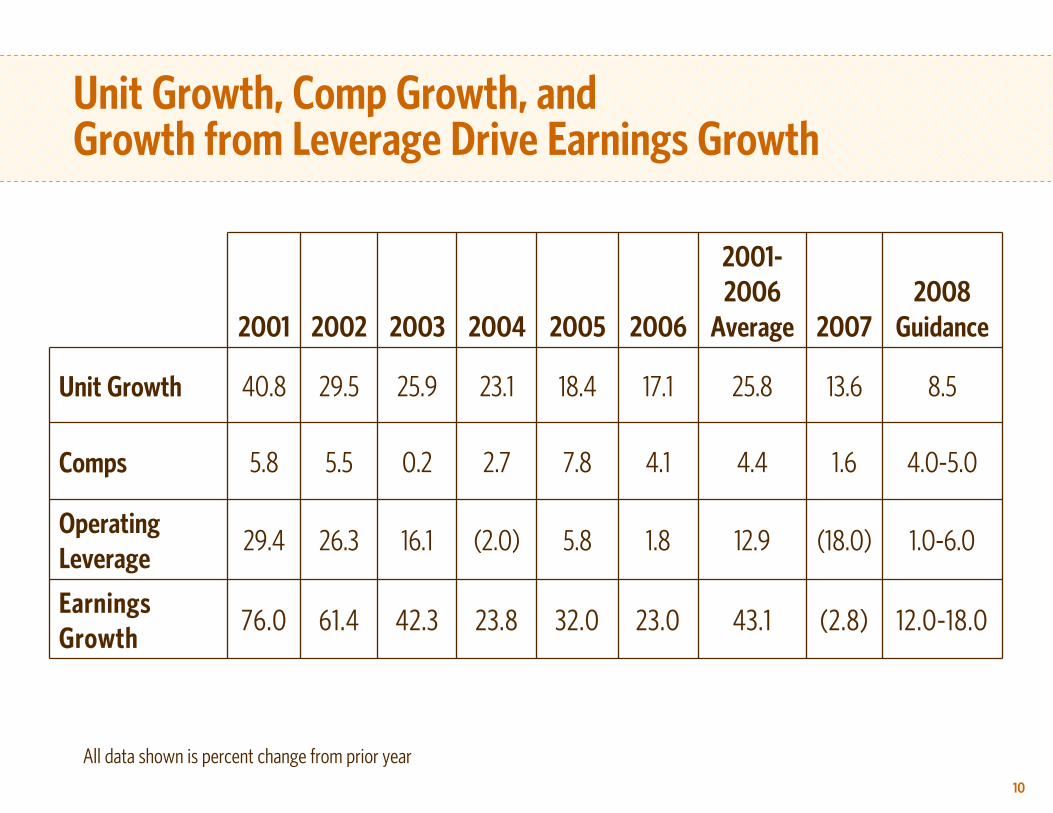

Unit Growth, Comp Growth, andGrowth from Leverage Drive Earnings Growth

All data shown is percent change from prior year

2001 2002 2003 2004 2005 2006

2001-2006

Average 20072008

Guidance

Unit Growth 40.8 29.5 25.9 23.1 18.4 17.1 25.8 13.6 8.5

Comps 5.8 5.5 0.2 2.7 7.8 4.1 4.4 1.6 4.0-5.0

Operating Leverage

29.4 26.3 16.1 (2.0) 5.8 1.8 12.9 (18.0) 1.0-6.0

Earnings Growth

76.0 61.4 42.3 23.8 32.0 23.0 43.1 (2.8) 12.0-18.0

11

What happened over the last 2 years?

Stable transaction growth- Positive growth 11 of the last 13 quarters in company-owned bakery-cafes

Margin compression- Focus on transaction growth at the expense of margin

- Wheat and oil prices reached historically high levels

- Crispani showed limited growth

Negative trajectory on ROIC- Margin compression affects all bakery-cafes

- 40% of system are immature bakery-cafes

12

A 2 Year View of Panera

6.8%

8.4%

7.2% 7.2%

8.9%

3.7%

2.5%

1.6%

-0.6%

1.7%

3.4%

2.6%

3.3%

Company-owned Comps

7.3%

QTD as of 4/22/08

13

Focus in 2008

Improve margin: grow gross profit per transaction year over year(despite hyper-inflation in wheat)

Maintain or grow transactions (despite consumer headwinds)

Drive increased ROIC

14

Improve Margin:Grow Gross Profit per Transaction Year over Year

Paradigm evolution- Rather than focus on comps, focus is on driving transactions and gross profit per transaction

Category management team added- Philosophy: Actions to impact customer behavior- Process: Data collection and rigorous testing- Utilize menu placement to focus on high penny profit items

- Celebrations focused on high penny profit items like You Pick Two- New product introduction process: breakfast sandwich

Pricing initiatives- Pricing philosophy: hi/low (differentiated)- Take price to cover hyper-inflation in wheat consistent with contractual ability- 2.5% increase taken in November 2007 and 2.7% late March 2008 with no transaction loss- In mid-June revised bagel pricing to roll out

Crispani removed- Effectively out mid-first quarter- 100 bps run-rate labor margin improvement

Increase fresh dough sales through bakery initiatives- “Be a Hero” in the office or home: bulk bagel sales- Bread merchandising: seasonal products

15

Improve Margin: Category Management (Old Menu Board)

16

Improve Margin: Category Management (New Menu Board)

17

Improve Margin:Category Management

You Pick TwoYou Pick TwoCinnamon Crunch Cinnamon Crunch

Bagel & Cafe MochaBagel & Cafe Mocha Breakfast SandwichBreakfast Sandwich

18

Improve Margin:Increase Fresh Dough Sales

Bulk BagelsBulk BagelsIrish Soda Bread / Irish Soda Bread /

Hot Cross BunsHot Cross Buns TakeTake--home Breadhome Bread

Hyperinflation: 2008 Locked Costs vs. 2007 Actual Cost

19

*Estimated average for Q3 & Q4 2008

20

Maintain or Grow Transactions

Breakfast- Breakfast sandwiches

Lunch- New soups, salads, sandwiches

- Service system: to go and ease of use

- Via Panera

Platform- Ops excellence: speed / accuracy / customer satisfaction

- Media Trials III

Maintain or Grow Transactions

21

22

Drive Increased ROIC

Invest incremental capital at minimum 15% + long-term free cash flow return- 85% of capital at a 15%+ return, and maximum of 15% of capital non-ROI

(infrastructure/test)

Tighter development with focus on raised AWS hurdles

23

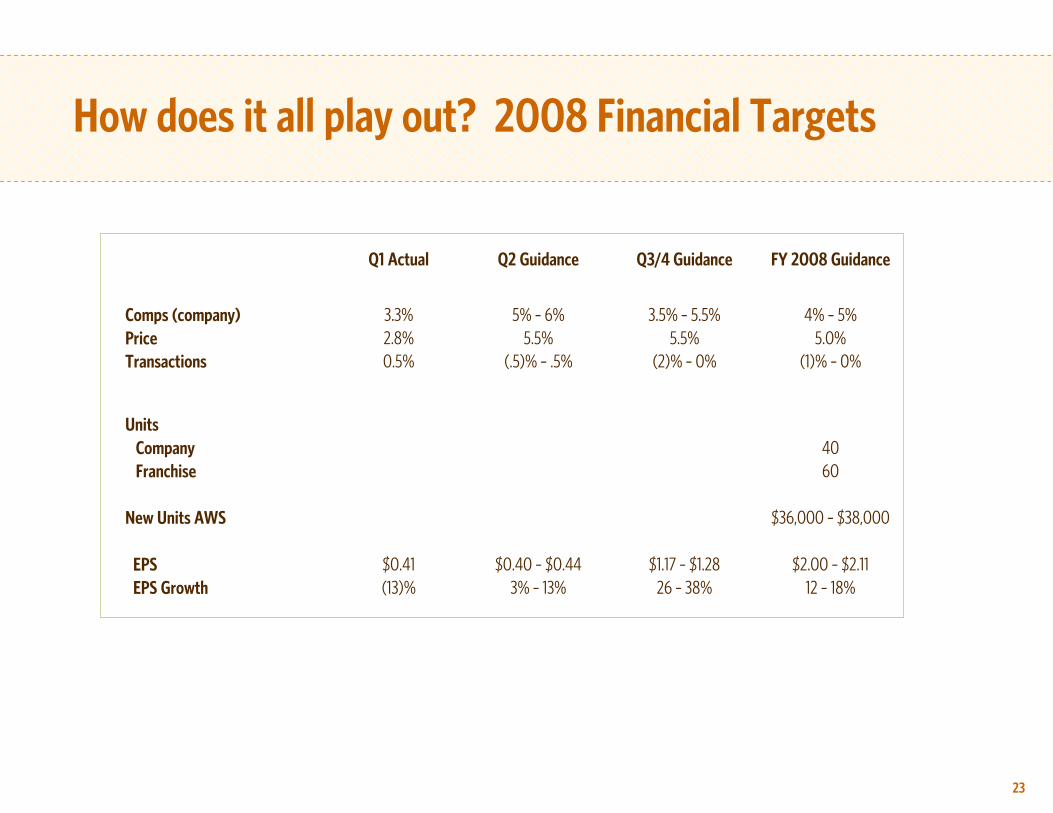

How does it all play out? 2008 Financial Targets

Q1 Actual Q2 Guidance Q3/4 Guidance FY 2008 Guidance

Comps (company) 3.3% 5% – 6% 3.5% – 5.5% 4% – 5%Price 2.8% 5.5% 5.5% 5.0%Transactions 0.5% (.5)% – .5% (2)% – 0% (1)% – 0%

UnitsCompany 40Franchise 60

New Units AWS $36,000 – $38,000

EPS $0.41 $0.40 – $0.44 $1.17 – $1.28 $2.00 – $2.11 EPS Growth (13)% 3% – 13% 26 – 38% 12 – 18%

24

Investment Considerations

Exceptional consumer acceptance drives superior store volumes, which in turn drives 40% cash-on-cash returns

Significant potential for future development

Short term: positioned to drive improved performance through focus on improved margin, transaction growth and increased ROIC improvement

Medium term: positioned to drive expanded earnings growth through concept differentiation + development + leverage

Panera Bread Companywww.panerabread.com