panel discussion tax considerations for the life … 06pd: tax considerations for the life insurance...

TRANSCRIPT

Session 06PD: Tax Considerations for the Life Insurance Actuary

Moderator:

Brian Prast FSA,MAAA

Presenters: Graham Green

Brian McBride FSA,MAAA Brian Prast FSA,MAAA

SOA Antitrust Disclaimer SOA Presentation Disclaimer

2017 Valuation ActuarySymposium

Moderator:Brian Prast, FSA, MAAA

Presenters:Graham R. Green, JD, LLMBrian McBride, FSA, MAAABrian Prast, FSA, MAAA

Tax Considerations for the Life ActuaryAugust 28, 2017

Disclaimer• This presentation is provided solely for the purpose of enhancing knowledge on

tax matters. It does not provide tax advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances.

• These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

• Presentations are intended for educational purposes only and do not replace independent professional judgment. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of the Society of Actuaries, its cosponsors, or its committees. The Society of Actuaries does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented. Attendees should note that sessions are audio-recorded and may be published in various media, including print, audio and video formats without further notice.

• The views expressed by the presenters are not necessarily those of KPMG, Kansas City Life Insurance Company, MassMutual Financial Group, or of Eversheds Sutherland (US) LLP.

2

Agenda• Tax policy and the regime for taxing life insurance companies• Basic Tax Reserve Topics• Additional Reserve Topics• Principle-Based Reserves and 2017 CSO:

Tax Reserve Issues• IRS Examination Process• Other Topics• Tax Authorities & Resources• Tax Reform• Summary

3

Tax policy and the regime for taxing life insurance companies

4

Principles of Tax Policy• Equity

• Horizontal Equity• Vertical Equity

• Efficiency• Administrability

5

Regime of Taxing Life Insurers• Life Insurance Company Taxable Income (LICTI) subject to

tax under § 801 at corporate rates• LICTI

• Life Insurance Gross Income minus• Life Insurance Deductions

• Life Insurance Gross Income • Premiums plus• Decreases in reserves (§ 803(a)(2))

• Life Insurance Deductions• Death benefits plus• Increases in reserves (§ 805(a)(2))

6

Regime for Taxing Life Insurers –Methods of Accounting• Taxpayers generally

• General Rule § 446(a): Start with book (e.g., GAAP)• Tax Override § 446(b): Clear reflection of income

• Insurers specifically § 811(a)• Start with book/statutory accounting consistent with NAIC

Annual Statement• Modify for tax purposes

7

Basic Tax Reserve Topics

8

Statutory vs. Tax Reserves

• Statutory Reserves• Solvency• Minimum Standards• Movement towards Principle-Based Reserves (PBR)

- AG43/VM-21 reserves for Variable Annuities - VM-20 for Life

• Tax Reserves• Start with statutory reserve assumptions• Adjust as required by Internal Revenue Code (IRC) • Final tax reserve is less than or equal to statutory reserve• This “inefficiency” results in higher taxable income

9

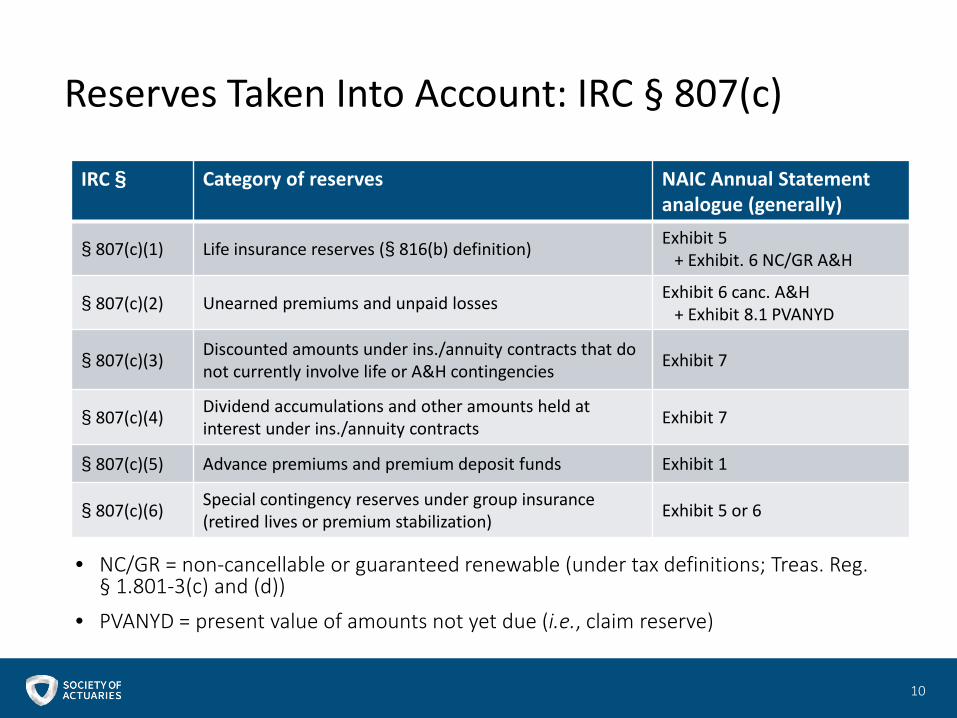

Reserves Taken Into Account: IRC § 807(c)

• NC/GR = non-cancellable or guaranteed renewable (under tax definitions; Treas. Reg. § 1.801-3(c) and (d))

• PVANYD = present value of amounts not yet due (i.e., claim reserve)

10

IRC § Category of reserves NAIC Annual Statement analogue (generally)

§ 807(c)(1) Life insurance reserves (§ 816(b) definition) Exhibit 5+ Exhibit. 6 NC/GR A&H

§ 807(c)(2) Unearned premiums and unpaid losses Exhibit 6 canc. A&H+ Exhibit 8.1 PVANYD

§ 807(c)(3) Discounted amounts under ins./annuity contracts that do not currently involve life or A&H contingencies Exhibit 7

§ 807(c)(4) Dividend accumulations and other amounts held at interest under ins./annuity contracts Exhibit 7

§ 807(c)(5) Advance premiums and premium deposit funds Exhibit 1

§ 807(c)(6) Special contingency reserves under group insurance (retired lives or premium stabilization) Exhibit 5 or 6

Definition of Life Insurance Reserves

• § 807(c)(1) refers to “life insurance reserves” as defined in § 816(b)

• § 816(b) defines “life insurance reserves” as amounts:

• Computed or estimated on the basis of recognized mortality or morbidity tables and assumed rates of interest

• Set aside to mature or liquidate, either by payment or reinsurance, future unaccrued claims arising from life insurance, annuity and noncancellable A&H insurance contracts

• Required by law

11

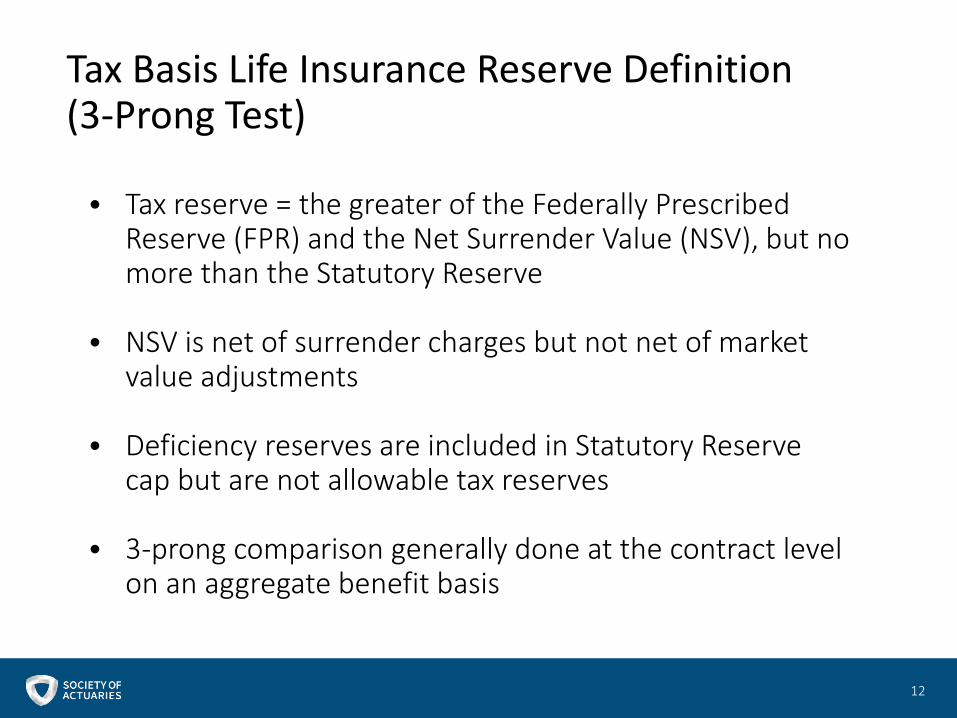

Tax Basis Life Insurance Reserve Definition (3-Prong Test)

12

• Tax reserve = the greater of the Federally Prescribed Reserve (FPR) and the Net Surrender Value (NSV), but no more than the Statutory Reserve

• NSV is net of surrender charges but not net of market value adjustments

• Deficiency reserves are included in Statutory Reserve cap but are not allowable tax reserves

• 3-prong comparison generally done at the contract level on an aggregate benefit basis

Differences Between the Federally Prescribed Reserve (FPR) and Statutory Reserve

13

• Methodology• Valuation interest rate• Mortality/Morbidity tables• Deferred & uncollected premiums are generally

removed from FPR• Removal of excess interest reserves from FPR

Applies on contracts where an interest crediting rate above tax rate is guaranteed beyond the end of the tax year

FPR Computation – Methodology§ 807(d)

14

The tax reserve method applicable to that type of contract in effect on the date of the issuance of the contract as prescribed by the NAIC, which is:

• CRVM for a life insurance contract• CARVM for an annuity contract• 2-year full preliminary term method for noncancellable accident

and health insurance contracts• 1-year preliminary term for qualified long-term care, issued in 1998 or

later• Other prescribed method by the NAIC that covers such

contract as of the date of issuance• If such method does not exist, a method consistent with

other applicable prescribed methods

FPR Computation – Valuation Interest Rate§ 807(d)

15

The greater of the applicable federal interest rate (AFIR) or the prevailing state assumed interest rate (PSAR), determined for the calendar year in which the contract is issued

• AFIR = average of federal mid-term rates over the 60 months ending the December prior to the issue year of the contract (first applied on 1988 issues)

• PSAR = highest reserve valuation interest rate permitted in at least 26 states at the start of the issue year

Tax and Stat Interest Rates 1988 - 2017: Whole Life Insurance

• AFIR has had little impact in recent low interest rate environment

16

FPR Computation – Mortality/Morbidity Tables

17

• Prevailing Commissioners' Standard Table - Most recent NAIC approved table permitted in 26 or more states for the contract type

• Where no Commissioners’ Standard Table exists, table shall be determined by Treasury regulations.

• Can use the old table for 3 years after a prevailing table change

• Example: 2001 CSO became prevailing in 2004

• Optional for contracts issued in 2004, plus 2005-2007

• Required for contracts issued in 2008 (different from stat)

• IRC allows prevailing tables "adjusted as appropriate" to reflect the risks (such as substandard risks) incurred under the contractwhich are not otherwise taken into account

• If more than one table or option, must use the one which generally results in lowest reserves

FPR – § 807(d)(2)(C) Mortality Tables

18

Sources and abbreviations: Rev. Ruls. 92-19 and 2001-38, NAIC Model Reg. 821

Year become prevailing Life Individual annuity Group annuity1948 CSO 41 SA 37 SA 37

1960 CSO 58 (3-year setback)

1962 A 49 GA 51

1974 IA 71 GA 71

1979 CSO 58 (6-year setback)

1982 CSO 80 (smoker-composite)1985 83 “a” 83 GAM

1986 CSO 80 (smoker-distinct;optional)1999 Annuity 2000 94 GAR

2004 2001 CSO

2015 2012 IAR

2017 2017 CSO

Additional Reserve Topics

19

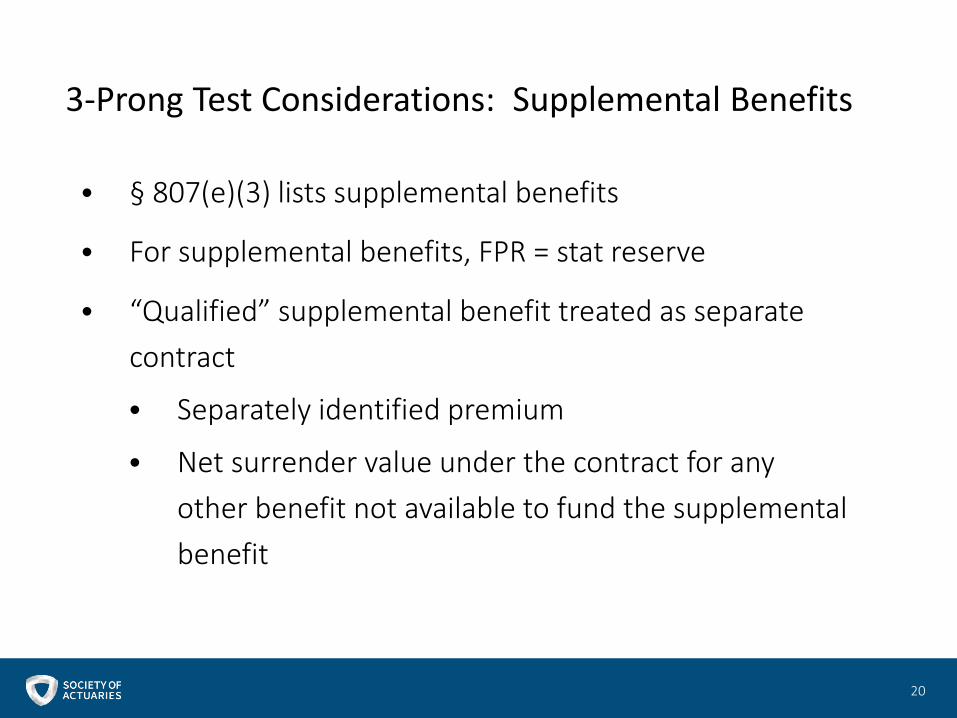

3-Prong Test Considerations: Supplemental Benefits

• § 807(e)(3) lists supplemental benefits

• For supplemental benefits, FPR = stat reserve

• “Qualified” supplemental benefit treated as separate contract

• Separately identified premium

• Net surrender value under the contract for any other benefit not available to fund the supplemental benefit

20

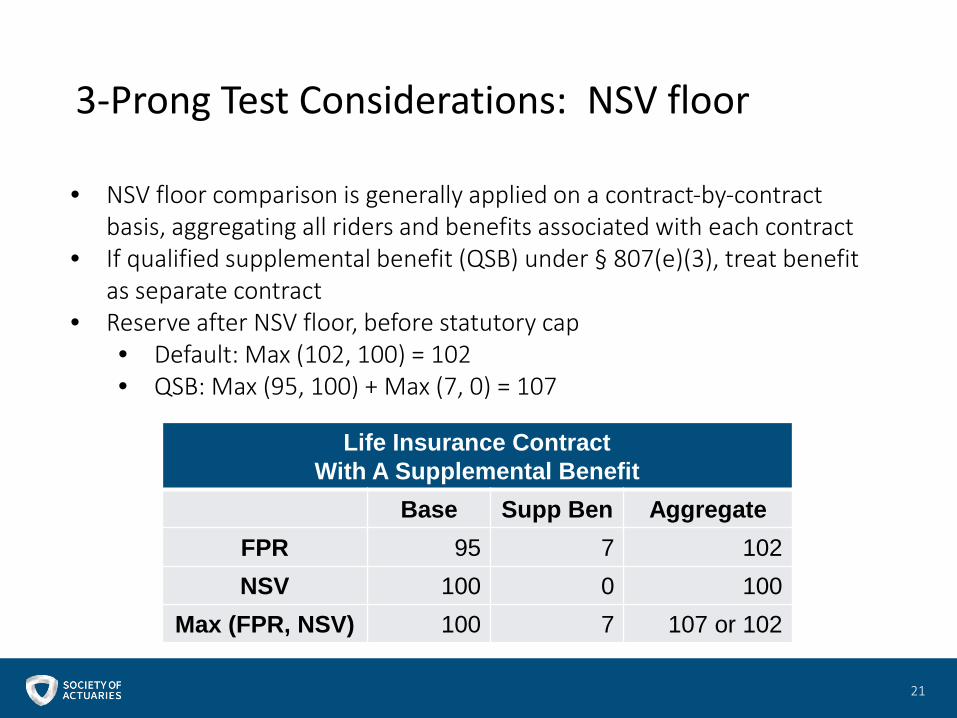

3-Prong Test Considerations: NSV floor

21

• NSV floor comparison is generally applied on a contract-by-contract basis, aggregating all riders and benefits associated with each contract

• If qualified supplemental benefit (QSB) under § 807(e)(3), treat benefit as separate contract

• Reserve after NSV floor, before statutory cap• Default: Max (102, 100) = 102• QSB: Max (95, 100) + Max (7, 0) = 107

Life Insurance Contract With A Supplemental Benefit

Base Supp Ben AggregateFPR 95 7 102NSV 100 0 100

Max (FPR, NSV) 100 7 107 or 102

3-Prong Test Considerations: Statutory Cap

• Tax life insurance reserves capped by statutory reserves for the contract

• Statutory reserves defined as aggregate amount set forth in the Annual Statement “with respect to” tax reserves

• Amounts included in statutory cap• Deficiency reserves – confirmed by Notice 2013-19• CTE excess under AG43?• Additional actuarial reserves/cash flow testing reserves?

• Life PBR deterministic and stochastic excesses?

,

22

“Change in Basis” vs. “Correction of Error”

• § 807(f) – Adjustments for Changes in Reserve Basis• “Changes in basis” require a 10-year spread of the change • “Corrections of errors” are reflected currently

• Rev. Rul. 94-74 guidance• Example 1: use of wrong mortality table in prior years• Example 2: use of wrong interest rates• Example 3: change from curtate to continuous reserves• Example 4: missed range of contract cells in in-force file

• FFA 20165101F (Dec. 16, 2016)• Taxpayer incorrectly applied AG 33, understating reserves• IRS determined that a change in basis occurred requiring 10-year pro

rata spreading of reserve increase

23

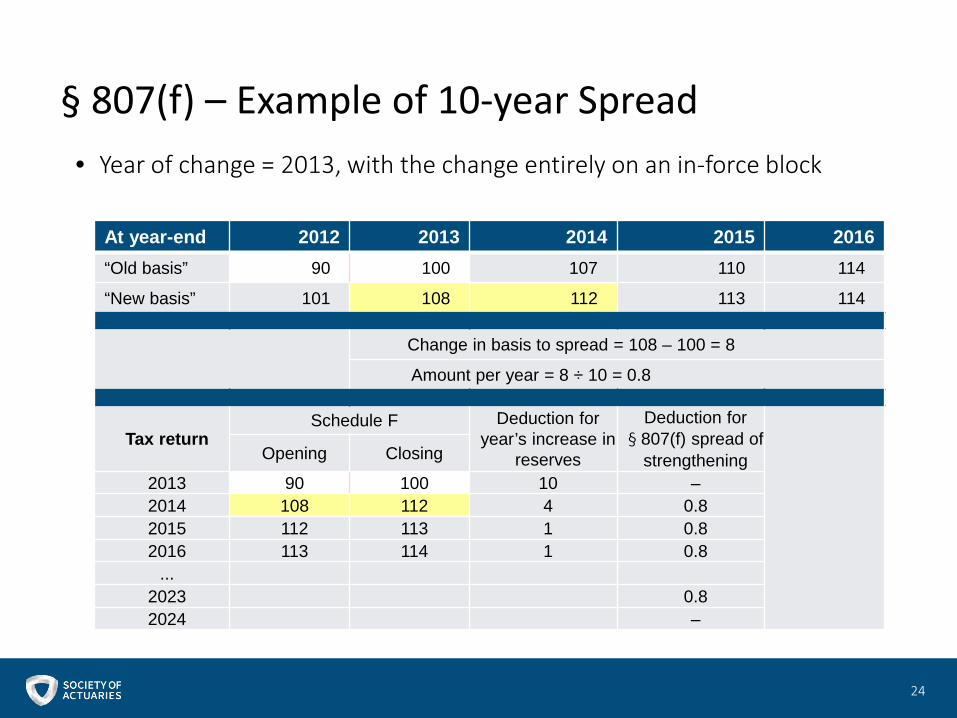

§ 807(f) – Example of 10-year Spread• Year of change = 2013, with the change entirely on an in-force block

24

At year-end 2012 2013 2014 2015 2016“Old basis” 90 100 107 110 114

“New basis” 101 108 112 113 114

Change in basis to spread = 108 – 100 = 8

Amount per year = 8 ÷ 10 = 0.8

Tax returnSchedule F Deduction for

year’s increase in reserves

Deduction for § 807(f) spread of

strengtheningOpening Closing

2013 90 100 10 –2014 108 112 4 0.82015 112 113 1 0.82016 113 114 1 0.8

...2023 0.82024 –

Principle-Based Reserves and 2017 CSO: Tax Reserve Issues

25

Tax Reserves – AG43 (IRS Notice 2010-29)

26

• Notice 2010-29 provides interim tax guidance on AG43• For statutory purposes, AG43 effective at YE 2009 for 1/1/1981 and later

issues• For tax purposes, AG43 applies to contracts issued on or after December 31,

2009• Life insurance reserves under § 816(b) for determining whether an insurance

company is a life insurance company• Standard scenario is included• Silent on CTE amount

• Federally prescribed reserve under § 807(d)(2)• Standard scenario is included• CTE amount is specifically excluded

• Statutory cap under § 807(d)(1) and § 807(d)(6)• Standard scenario is included• Silent on CTE amount

Life PBR/VM-20: Background

• NAIC Valuation Manual (VM-20) prescribes minimum reserve valuation standards for individual life insurance policies

• What are some of the features of VM-20?• Net premium reserve (NPR) – serves as a floor• Deterministic Reserve

• Formulaic• Relies on company-specific information

• Stochastic Reserve• Similar to CTE amount of AG43• Computed for a group of contracts based on many

scenarios• PBR made effective by the NAIC for 2017, with a 3-year transition

period

27

Tax Reserve Issues Under VM-20

• What pieces of the reserve (NPR, Deterministic, Stochastic) can be included in:

• Life insurance reserves under § 816(b) for determining life insurance company status

• Federally Prescribed Reserves under § 807(d)(2)• Statutory cap under § 807(d)(1) and § 807(d)(6)

• What are the tax reserve implications of the statutory 3-year transition period?

28

How Will These Issues be Resolved?

What guidance is available?• Notice 2008-18 identifies key issues that could arise out of PBR

• Continued taxation of life insurers under Part 1 of Subchapter L• Qualification of contracts as life insurance contracts• Contract-by-contract v. aggregate reserving• Prevailing assumed interest rate and prevailing mortality tables

• Notice 2010-29 on AG43• Industry has received guidance on product qualification (Notice 2016-

63) and has requested guidance on reserve transition and substantive reserve issues

• VM-20 and AG43/VM-21 included on Priority Guidance Plan and added as an IRS Campaign

• Industry Issue Resolution (IIR)Program – Collaborative effort between industry and IRS/Treasury to develop guidance on VM-20 and AG43/VM-21

29

2017 CSO: Tax Reserve Implications• VM-20 effective 1/1/2017

• VM-20 states 2017 CSO tables may be used on or after January 1, 2017, and shall be used for all policies on or after January 1, 2020

• 2017 CSO is a series of tables

• Federally prescribed reserve (per § 807(d)(2)) must be determined using the prevailing mortality table as of the date of issue of the contract

• Per IRS Notice 2016-63, 2017 CSO tables became prevailing on January 1, 2017.• 2017 CSO may be used for contracts issued on or after January 1, 2017• For contracts issued on or after January 1, 2020, use of the 2017 CSO tables will be

mandatory

30

2017 CSO: Tax Reserve Implications• § 807(d)(5)(E) – If more than one table, use the one which generally results in

lowest reserves

• Has historically been interpreted by the life insurance industry as meaning a general application at the industry-wide level

• For the 2001 CSO, this interpretation has resulted in three sets of prevailing tables - the ultimate versions of:

• Unismoke - Composite – 1 class • Smoker distinct - Smoker/Nonsmoker – 2 class • Preferred structure – 5 class

• Society of Actuaries – Report on 2014 VBT/2017 CSO Impact Study looked at three plans – whole life, 20 year level term and ULSG.

• Results showed: Reserves using the ultimate valuation tables were lower at most durations than reserves using the select & ultimate valuation tables.

• Overall level of reserves approximately the same on all three structures –unismoke, smoker-distinct and preferred.

31

IRS Examination Process

32

IRS Audit Process

• Federal Tax Dispute Stages:

Tax Return IRS Audit IRS Appellate Division Litigation

• The entire process starts with the tax return; every position, every tax planning idea, will ultimately be judged by its ability to hold up under audit

• The IRS Audit / Appeals / Litigation continuum for each year can be a long and expensive process

• Accurate documentation is a necessity; record retention of supporting materials is vital

33

34

• IRS groups taxpayers based on asset size

• Large companies fall under the jurisdiction of the IRS Large Business and International Division (LB&I)

• Each years’ tax returns for companies that are subject to LB&I jurisdiction generally are subject to audit

• An on-site IRS examination team is assigned

Overview of a Typical IRS Audit - Exam

35

• Exam• Kickoff meeting: Scope, agreed plan, timeline• § 6662 Disclosures • Information Document Requests (IDRs)

• Timelines• Enforcement• Standard IDR - Reserve Questionnaire

• Numerical analysis and presentation – by coverage type, issue year, interest rates, mortality and reserve method

• Application of statutory cap and net surrender value floor • Calculation of federally prescribed reserves

• Notices of Proposed Adjustments - Forms 5701

Overview of a Typical IRS Audit - Exam

36

• Revenue Agent’s Report (RAR) – compilation of 5701s• Taxpayer analysis of RAR and determination of issues to protest, if any• Protest – file written protest with Appeals Office • IRS Rebuttal• Appeals - All protested issues are discussed with an IRS Appeals

Officer in an effort for each issue to be settled on the basis of the strength of the party’s position (i.e. based on hazards of litigation). Upon completion of this phase, a Form 870-AD is issued.

• Litigation - For those protested issues not resolved with the IRS Appellate Division, and reserved on the Form 870-AD, a taxpayer may still pursue them further via Litigation in one of three forums (U.S. Tax court, U.S. Court of Federal Claims or Federal District Court)

Overview of a Typical IRS Audit – after IRS Exam

Eversheds Sutherland

Changes in IRS Audit Process• Address compliance and resource challenges • Set clearer expectations for examiners and taxpayers• Encourage collaboration and transparency• Move toward issue based examinations• Introduction of Campaigns

• First 13 Campaigns announced January 31, 2017• Two insurance-specific campaigns:

• Section 831(b) micro-captives• Principle Based Reserves – AG43/VM-21 and VM-20

37

Other Topics

38

Capitalized Policy Acquisition Costs (“Tax DAC”)• § 848 enacted in Revenue Reconciliation Act of 1990• Policy acquisition costs are deemed to be a specified

percentage of net premiums in each category• Annuity contracts - 1.75%• Group life insurance contracts - 2.05%• Other contracts - 7.70%

• Individual life• Individual/Group NC/GR A&H

• Tax DAC is amortized on a straight-line basis, generally over 120 months starting in second half of tax year

39

Tax DAC Example• In 2013, Company receives premiums as shown below• Premiums and capitalization:

• Amortization:

40

Contract Premiums Capitalization % Tax DACAnnuity 400,000,000 1.75% 7,000,000

Group life 38,000,000 2.05% 779,000

Individual life 133,000,000 7.70% 10,241,000

Total 571,000,000 18,020,000

Tax year Amortization Expense2013 5% 901,0002014-2022 10% per year 1,802,000 per year2023 5% 901,000

Total 100% 18,020,000

Proration and the “Company’s Share”

• Most corporations are entitled to a deduction (DRD), which is usually equal to 70% of dividends received from domestic corporations

• Proration concept: because part of every dollar of life insurer’s investment income is credited to policyholder reserves, which in turn are deductible, insurer should be required to reduce deductions to prevent a double benefit (compare § 265)

• Applies separately to general account and separate accounts

41

Proration and the “Company’s Share”

• Only life insurance company’s share of DRD and tax-exempt interest is taken into account in determining taxable income

• Example: if policyholders’ share is 75%, company’s share is 25%, so only 25% of tax-exempt income would effectively be tax-free

• Effectuated through deduction disallowance• DRD allowed only for company’s share of dividends• Reserves reduced by policyholder’s share of tax-exempt

income

42

Proration and the “Company’s Share”

• Company’s share = company’s share of net investment income divided by net investment income

• Company’s share of net investment income = net investment income less policy interest

• Net investment income = 90% of gross investment income; 95% for separate accounts

• Policy interest = required interest at greater of PSAIR or AFIR

• Although the formula is complex, the concept is simple: How much of the company’s net investment income is required to satisfy obligations to policyholders?

43

Proration and the “Company’s Share”

• Industry understanding of current law has been consistent, and a one-time IRS controversy was resolved in 2014

• Camp Discussion Draft proposes replacing existing regime with an approach based on the ratio of surplus to total assets

• Obama Administration FY 2016 Revenue Proposal is similar

44

Tax Authorities &Resources

45

Tax Authorities• Internal Revenue Code

• §§ 72, 101, 7702, 7702A, and Subchapter L (§§ 801-848)• Legislative History (Committee and Conference Reports)• JCT Bluebook – But beware of United States v. Woods (2013)

• Treasury Regulations• Revenue Rulings• Revenue Procedures• Notices• Private Letter Rulings• Chief Counsel Advice (CCA), Field Service Advice (FSA),

Technical Assistance Memo (TAM)• Internal Revenue Manual (IRM)

46

2016-2017 IRS Priority Guidance Plan (PGP) Insurance Companies and Products• Final regulations under § 72 on the exchange of property for an

annuity contract. Proposed regulations were published on October 18, 2006.

• Regulation under §§ 72 and 7702 defining cash surrender value.• Guidance on annuity contracts with a long-term care insurance

rider under §§ 72 and 7702B.• Guidance under §§ 807 and 816 regarding the determination of

life insurance reserve for life insurance and annuity contracts using principles-based methodologies, including stochastic reserves based on conditional tail expectation.

• Guidance on exchanges under § 1035 of annuities for long-term care insurance contracts.

• Guidance relating to captive insurance companies.

47

Tax Resources• DesRochers et. al., Life Insurance & Modified

Endowments Under Internal Revenue Code Sections 7702 and 7702A

• Robbins & Bush, U.S. Tax Reserves for Life Insurers• Burstein, Federal Income Taxation of Insurance

Companies• Black & Skipper, Life Insurance• Tax Notes Today, Insurance Tax Review

48

Tax Reform

49

Tax Reform• Background

• The Camp Draft (February 28, 2014)

• Summary of Key Insurance Provisions

• Ways & Means Blueprint (June 24, 2016)

• President Trump’s Tax Outline (April 26, 2017)

• Joint Statement by “Big Six” (July 27, 2017)

50

Background• With a Republican-controlled government, comprehensive tax reform is a realistic

possibility.

• Prior to the release of President Trump’s outline in April 2017, the Blueprint released in June 2016 by Speaker Ryan and House Ways and Means Chairman Brady was the focus of most of the discussions around tax reform.

• On April 26, 2017, President Trump released a high-level outline for his tax plan.

• The President’s tax outline does not contain many specifics, but does reflect some important differences in the President’s approach compared to the Blueprint.

• Meanwhile, Senate Republicans are reportedly focusing on the provisions of the 2014 Camp Draft as the starting point for tax reform.

• On July 27, 2017, the “Big Six” released a joint statement of goals for tax reform and reconciling House and Trump plans.

51

52

Camp Draft – Insurance Proposals

Ways & Means Blueprint• Published June 24, 2016• “Simpler, flatter, and fairer”

• Simplify the IRC – Eliminate corporate AMT• Flatten rates• Lower rates – Lower corporate tax rate to 20%

• Destination-based cash-flow tax• Deemed repatriation tax• Limit interest deduction to net interest expense• Full expensing of business assets

53

President Trump’s Tax Outline• 15% corporate rate• Territorial tax system• One-time Repatriation Tax• Elimination of tax breaks for special interests• Campaign Plan

• 10% rate for one-time repatriation tax• Election between full interest deduction or full expensing

for business assets• Phase out exemption for inside build-up for high-income

earners

54

Joint Statement by “Big Six”• Big Six:

• Paul Ryan, House Speaker• Mitch McConnell, Senate Majority Leader• Steven Mnuchin, Treasury Secretary• Gary Cohn, National Economic Counsel Director• Orrin Hatch, Senate Finance Committee Chairman• Kevin Brady, House Ways and Means Committee Chairman

• What’s In:• “Simpler, fairer, and lower [rates]” • “Unprecedented capital expensing”• Repatriation

• What’s Out – Destination-based cash-flow tax• House and Senate tax writing committees to take lead• Timing – Goal to move through committees this Fall

55

Summary

56

In Summary

• The Internal Revenue Code has very specific rules for taxing life insurance companies.

• Those rules, although straightforward in concept, are sometimes complex in practice and require the application of actuarial rules that sometimes differ from the statutory accounting rules that apply to the same block of business.

• The goals are equity (horizontal and vertical), efficiency, and administrability.

57

Questions & Answers

58