pakistan day conference_2011_strategy

TRANSCRIPT

Table of contents

Strategy| Pakistan

First Capital Equities Ltd

Economy

A glimpse into the past

Macro economic indicators

Concerns & Expectations

Key macro challenges in near term

Politics

Noisy but normal

Market

Dec-2011 index target of 13,500

Key drivers in 2011

Adopt a bottom-up approach

*All prices as of Feb 25, 2011

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES AT THE END OF THIS MATERIAL

A glimpse into past

Strategy| Pakistan

First Capital Equities Ltd

ECONOMY

2

· Pakistan underwent a series of economic shocks since 2008 that hurt the economic growth (GDP grew

by 1.2% in FY09); shocks that aroused from perpetual deterioration in external accounts, mounting internal

imbalances, sky-high inflation and portfolio de-leveraging by offshore investors primarily as a reciprocal

impact of the global meltdown.

· Meanwhile, the financial assistance from IMF has triggered much needed economic reforms starting

2009 while the ensuing dollar inflows have provided a cushion for the vulnerable foreign exchange reserves

in terms of currency.

· Country�s real output grew 4.1% in FY10 supported by industrial and service sectors.

· As required by IMF, major structural reforms have been initiated, like framework for introducing reformed

GST, improving tax administration, elimination of subsidies and allowing SBP to follow an independent

monetary policy.

· Headline inflation softened from the peak of 20.8% in FY09 to 11.7% in FY10.

· External side of the economy has shown pronounced signs of recovery. Current account deficit (CAD)

during FY10 has shrunk to US$3.9bn (2.3% of the GDP) from US$9.3bn (5.6% of the GDP) in FY09.

· Private sector credit demand also picked-up, which indicates the regaining economic confidence. That

said, the credit to the private sector during FY10 has increased by 3.9% after a muted growth of 0.7%

in the preceding year.

· Tough but crucial step to remove energy subsidies would augur well for the economy in the long term.

Nevertheless, it has a short term implication on the inflationary trend.

Macro Economic Indicators

Strategy| Pakistan

First Capital Equities Ltd

ECONOMY

3

Macro Snapshot 2007 2008 2009 2010 2011E

GDP Growth rates 6.8% 4.1% 1.2% 4.1% 2.2%

MacroAgriculture (%) 4.1% 1.1% 4.0% 2.0% -1.5%

Manufacturing (%) 8.8% 1.7% -2.0% 4.9% 2.5%

Services (%) 7.0% 6.6% 1.6% 4.6% 3.5%

Tax Collection (PRs bn) 890 1,051 1,205 1,473 1,630

FiscalTax revenue as % of GDP 10.3% 10.3% 9.5% 10.0% 9.5%

Fiscal deficit as % of GDP 4.4% 7.6% 5.3% 6.3% 5.9%

Trade balance (US$ bn) (13.6) (20.9) (17.1) (15.4) (15.3)

External

Export growth (%) 3.2% 12.2% -7.2% 9.1% 11.5%

Import growth (%) 6.9% 30.9% -12.9% -0.3% 6.0%

Remittances growth (%) 19.4% 17.4% 21.1% 14.0% 17.5%

Current account (US$ bn) (6.9) (14.0) (9.3) (3.9) (5.5)

Current account as % of GDP -4.8% -8.6% -5.6% -2.3% -2.8%

CPI (%) 7.8% 12.0% 20.8% 11.7% 14.5%

MonetaryM2 growth (%) 19.30% 15.30% 9.60% 12.50% 13.50%

10-Year PIB 10.2% 11.2% 14.1% 12.5% 14.0%

Pakistan External Debt (US$ mn) 40,322 46,161 52,331 55,626 58,412

Domestic Debt (PRs bn) 2,610 3,275 3,861 4,653 5,500

Pakistan External Debt as % of GDP 28% 28% 32% 32% 29%

Pakistan Domestic Debt as % of GDP 30% 32% 30% 32% 32%

Pakistan total Debt as % of GDP 58% 60% 62% 64% 62%

Source: SBP, Ec. Survey & FCEL Research

Debt

Concerns & Expectations

Strategy| Pakistan

First Capital Equities Ltd

ECONOMY

4

· Floods in Pakistan, affected more than 2.0mn of people and almost 20% of the Pakistan, have left a

desolate impact on the overall economy. Damage to infrastructures, crops and livestock is extensive. Full

impact of floods is yet to come.

· GDP growth projection is scaled down from 4.4% in pre-floods scenario to 2.0-2.5% in post-floods.

Agriculture sector (22% of GDP) is anticipated to decline 1.5% in FY11 due to damage to crops (cotton,

sugarcane & rice) and livestock.

· Importantly, despite the floods, the external position and the exchange rate have remained stable so

far. The envisaged loss of reserves due to flood-related imports has not materialized. Interestingly, in

1HFY11, the country recorded a current account surplus - albeit only 0.03% of GDP - and the FX reserves

increased by US$970 million to US$17.4bn.

· Inflation is likely to shoot-up to 14.-14.5%, mainly fueled by agriflation. This is far high from pre-flood

target of 9.5%. Despite rising headline consumer inflation, core inflation (non food and non energy) has

been on declining trend and has reached to 9.4% in Jan-2011 from its peak level of 18.9% in February

2009.

· Cost of rehabilitation & construction (R&C) would be significant. External flows are not enough to cover

all cost related to R&C. As a result, fiscal side may come under stress. As per initial estimates, the budget

deficit for FY11 would touch ~6.0% of GDP, higher than 4.0% budget by the government.

· Though the balance of payments is expected to weaken in FY11 - mainly due to the floods� impact, we

expect that the higher trade deficit will be compensated partly by rising remittances from overseas

Pakistanis and other unilateral inflows like Coalition Support Fund and Kerry Lugar tranche.

· Structural reforms are in the pipeline targeting to improve the budgetary position. In this regard, the

reformed general sales tax (RGST), including an effective input-crediting mechanism, reduced exemptions,

and elimination of zero-rating and special rates is deemed to be a crucial measure.

Concerns & Expectations

Strategy| Pakistan

First Capital Equities Ltd

ECONOMY

5

· Meanwhile, power sector reform, with an objective to eliminate untargeted subsidies would be

helpful in the long run.

· Realization of donor financing would support the government�s efforts to finance flood relief and

reconstruction as well as raise development and social spending. Already, the country has received

US$450mn from IMF under emergency assistance.

· Monetary environment is anticipated to be tight. Interest rates are expected to trend upward in near

term. We have already witnessed a 150bps hike in the discount rate to 14% since the start of the ongoing

fiscal. Moreover, rising government recourse of SBP borrowing would induce continuation of tight stance

by SBP.

· Despite short-term economic woes caused by floods, both Moody�s and S&P�s kept Pakistan outlook

�Stable�.

· Pakistan�s 5years CDS currently stand at 1,126bps from peak level of 5,051bps observed in 2008.

· Yield on Pakistan�s Eurodollar bond (maturity in 2016) is hovering at 10.6%, 16pps lower than its record

level of 26% in Dec-2008.

Key Macro Challenges in near term

Strategy| Pakistan

First Capital Equities Ltd

ECONOMY

6

Below we provide key macro challenges faced by Pakistan.

Inflation

· Inflation in Pakistan has always remained a prime concern. Preceding FY08-09, country�s real output

grew at an average rate of 6.8% (5yrs average) while inflation remained comparatively benign at 6.5%.

· Global meltdown and escalating oil and commodity prices sparked high risk of inflation. Annual inflation

peaked in FY09 at 20.8%, in line with other regional economies and then receded to single digit.

· After a breath, inflation once again is on an uptrend and has reached to 14.2% in Jan 2011, mainly driven

by 20% YoY increase in food prices and 9% increase in fuel and lightening index.

Headline inflation rising but core inflation is stable

· Despite rising headline consumer inflation, core inflation (non food and non energy) has been on declining

trend and has reached to 9.4% in Jan-11 from its peak level of 18.9% in Feb-09.

· Major difference between two is the composition of CPI basket. In Pakistan, food and beverages comprise

more than 40% of the CPI basket, thereby, adding much volatility in the inflationary trend. Rising food

prices drive the inflation in the country.

· Food prices are surging due to damages caused by floods (as like in China), and it is more aggravated

by global bull-run in commodity prices. Moreover, the electricity reforms (which carries positive economic

implications in the long run) to eliminate untargeted subsidies has also caused a recent upsurge in headline

inflation.

Inflation to recede in 2HFY11

· Headline inflation to settle at 12.0% by the end of FY11 as compared to current level of ~15%. Average

inflation for 4QFY11 is estimated at 12.5% versus 15.5% expected in 2QFY11. Improvement in food supply

and administrator measures may bring down high food prices.

Key Macro Challenges in near term

Strategy| Pakistan

First Capital Equities Ltd

ECONOMY

7

External account showing recovery

· In 2008, Pakistan CAD surged to 8.6% of GDP. Sharp rise in CAD was due to oil and food import bill

(39% of total import) which grew 55% YoY in FY08. The country�s Fx reserves declined to US$7.0bn, an

import cover of 2.0 months only.

· Growing remittances and rising exports helped the country to reduce external imbalances in FY10 and

CAD shrank to 2.3% of the GDP in FY10. Recently, the country�s total Fx reserves hit the record level of

US$17.4bn.

· In first six months of current fiscal, CA balance of the country stood at positive US$26mn (0.03% of GDP)

versus a deficit of US$2.6bn (3% of GDP) in the same period of last year. However, due to bullish trend

in global commodity prices, we anticipate CAD to reach at US$5.5bn, 2.8% of the GDP in FY11. Though,

it represents YoY increase, CAD as % of GDP is competitive in the region.

Exchange rate - Stable outlook

· In the last three years Pakistan�s currency weakened sharply against the US$. PRs/US$ depreciated by

30% in 2008, after a stable trend in the preceding couple of years.

· Despite a relatively high domestic inflation and high interest rate, local currency remained stable due

to deliberate policy to support the exchange rate. Later on, hit by the global commodity crisis that

aggravates external balances, the country fully adopted a flexible exchange rate and allowed its currency

to depreciate.

· This resulted in a sharp decline in currency value, mainly as a correcting difference of past years.

· Fx reserves have increased from low of US$7.0bn in 2008 to ~US$17.4bn currently. In addition to this,

unilateral inflows and loans from donors and FI would boost the foreign exchange reserves of the country

going forward and will keep the domestic currency relatively stable.

Economy: Real sector

Strategy| Pakistan

First Capital Equities Ltd 8

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

2004

2005

2006

2007

2008

2009

2010

Domestic ExpenditureReal GDP

10

15

20

25

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

Investment % of GDP

National Savings % of GDP(%)

Private Consp. 73%

Invest. 15%

Govt Expd. 10%Others 3%

-3.0%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

2005

2006

2007

2008

2009

2010

2011E

GDP ManftgServices Agriculture

Source: SBP, FBS & FCEL Research

GDP Sub-Sec Performance

Source: SBP, FBS & FCEL Research

Saving & investment gap (% of GDP)

Agri: 22%

Services: 53%

Manftg: 25%

Source: SBP, FBS & FCEL Research

GDP Composition (FY10)

Source: SBP, FBS & FCEL Research

Growth Pattern

-10%10%

30%50%70%

90%110%

2005

2006

2007

2008

2009

2010

Pvt consumption Investments

Govt exp Net exports

Source: SBP, FBS & FCEL Research

Demand Side Nominal GDP

Source: SBP, FBS & FCEL Research

Demand Side GDP at FC (FY10)

-3.0%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

18.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011E

Manufacuring GDP

Social Serv.

Fin. & Ins.

Real Est.

Public Admn.

Transport & Com.

WS & Retail

-30%

-20%

-10%

0%

10%

20%

Jul-

08

Oct

-08

Jan-0

9

Apr-

09

Jul-

09

Oct

-09

Jan-1

0

Apr-

10

Jul-

10

Oct

-10

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011E

Agriculture GDP

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011E

Services GDP

50.0%

51.0%

52.0%

53.0%

54.0%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Source: SBP, FBS & FCEL Research

Services share in GDP

Source: SBP, FBS & FCEL Research

GDP vs IP (YoY) -Real

Source: SBP, FBS & FCEL Research

Service sector Composition (FY10)

Source: SBP, FBS & FCEL Research

Large Scale Manufacturing (YoY)

Source: SBP, FBS & FCEL Research

GDP vs Services (YoY) -Real

Source: SBP, FBS & FCEL Research

GDP vs Agri (Y0Y) -Real

Economy: Real sector (Contd�)

Strategy| Pakistan

First Capital Equities Ltd 9

HRI, 23%Fuel, 7%

Misc, 7%

Food, 40%

Transport, 7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2003

2004

2005

2006

2007

2008

2009

2010

2011E

2012

E

0%

5%

10%

15%

20%

25%

30%

Jan-0

8

May

-08

Sep-0

8

Jan-0

9

May

-09

Sep-0

9

Jan-1

0

May

-10

Sep-1

0

Jan-1

1

Core Headline

-2.0%

-1.0%

0.0%1.0%

2.0%

3.0%

4.0%

Jan-0

7

May

-07

Sep-0

7

Jan-0

8

May

-08

Sep-0

8

Jan-0

9

May

-09

Sep-0

9

Jan-1

0

May

-10

Sep-1

0

Jan-1

1

CPI (MoM change %)Average

0%

5%

10%

15%

20%

25%

Jan-0

7

May-

07

Sep-0

7

Jan-0

8

May-

08

Sep-0

8

Jan-0

9

May-

09

Sep-0

9

Jan-1

0

May-

10

Sep-1

0

Jan-1

1

CPI (YoY change %) Average

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

2004

2005

2006

2007

2008

2009

2010

2011E

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%IPGDPCPI (RHS)

Source: SBP, FBS & FCEL Research

Price vs Growth (YoY)

Source: SBP, FBS & FCEL Research

Annual Headline CPI (%)

Source: SBP, FBS & FCEL Research

CPI (YoY)

Source: SBP, FBS & FCEL Research

Break-up of CPI

Source: SBP, FBS & FCEL Research

CPI (MoM)

Source: SBP, FBS & FCEL Research

Headline vs Core CPI(YoY)

Economy: Prices

Strategy| Pakistan

First Capital Equities Ltd 10

0

200

400

600

800

1000

2005

2006

2007

2008

2009

2010

1Q2011

PrivatizationNon-BankBankExternal

-

500

1,000

1,500

2,000

2,500

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

Gross RevenueTaxNon-Tax

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1E

201

2E

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011E

0%

5%

10%

15%

20%

25%

30%

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1E

Nominal GDP

Gross Tax Collection

-

250

500

750

1,000

1,250

1,500

1,750

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011E

Direct Taxes Indirect taxes

Source: SBP, FBS & FCEL Research

FBR Tax Collection (PRs bn)

Source: SBP, FBS & FCEL Research

Fiscal deficit as % of GDP

Source: SBP, FBS & FCEL Research

Growth pattern (YoY)

Source: SBP, FBS & FCEL Research

Deficit Financing (PRs bn)

Source: SBP, FBS & FCEL Research

Gross Tax to GDP (FBR)

Source: SBP, FBS & FCEL Research

Fiscal Consolidation (PRs bn)

Economy: Fiscal Position

Strategy| Pakistan

First Capital Equities Ltd 11

Economy: External Sector

Strategy| Pakistan

First Capital Equities Ltd 12

-

4

8

12

16

20

24

Jan-0

7

May-

07

Sep-0

7

Jan-0

8

May-

08

Sep-0

8

Jan-0

9

May-

09

Sep-0

9

Jan-1

0

May-

10

Sep-1

0

Jan-1

1

40

50

60

70

80

90Reserves (US$ bn)

PRs/US$ (RHS)

-

200

400

600

800

1,000

Jul-

07O

ct-0

7Ja

n-0

8Apr-

08Ju

l-08

Oct

-08

Jan-0

9Apr-

09Ju

l-09

Oct

-09

Jan-1

0Apr-

10Ju

l-10

Oct

-10

Jan-1

1

US$ mnAvg-FY09Avg-FY11

-25.0

-15.0

-5.0

5.0

15.0

25.0

35.0Inc. (net)Services (net)Cur. Trans. (net)Trade Bal.CA. bl.

5.0

10.0

15.0

20.0

25.0

2005

2006

2007

2008

2009

2010

2011E

-20%

-10%

0%

10%

20%

30%

40%

50%Trade deficitExport Growth (RHS)Import Growth (RHS)

-

5

10

15

20

25

200

1

200

3

200

5

200

7

200

9

201

1E

-10%

-5%

0%

5%

10%

15%

20%

25%

30%Export (US$ bn)

Export growth

Source: SBP, FBS & FCEL Research

Export Performance (US$ bn)

Source: SBP, FBS & FCEL Research

Monthly Remittances (US$ mn)

Source: SBP, FBS & FCEL Research

Export Growth Pattern (YoY)

Source: SBP, FBS & FCEL Research

Reserves Vs Currency

Source: SBP, FBS & FCEL Research

Trade Gap (US$ bn)

Source: SBP, FBS & FCEL Research

Current Ac. Bal (US$ bn)

-40%

-20%

0%

20%

40%

60%

Jul-

06

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

GrowthFY06-10 Avg.FY11 Avg.

Rise in Avg. YoY

export growth

Avg-FY08Avg-FY10

2007

2008

2009

2010

2011E

Noisy but normal

Strategy| Pakistan

First Capital Equities Ltd

POLITICS

13

· During 2010, the political scenario of the country remained comparatively calm as against an almost

chaos like situation during 2007-09.

· The end of the year also marked the completion of almost 3-years in power for the prevailing ruling

setup. In Pakistan, historically, a period of 3-year is more than the average period for any democratic

setup.

· Though the political noise level increased quite a few times during the year on many critical issues,

the ruling setup remained relatively more efficient in taking the corrective measures and to keep the

situation under-control.

· For 2011, the most immediate problem for the ruling setup would be to tackle the situation developed

after PML-N�s decision to dissociate PPP from the Punjab cabinet amid dissatisfaction over the implementation

of its 10-point agenda. However, we do not foresee any serious threat to the government benches in the

federal assembly due to this move as the number game for PPP has become more positive in the National

Assembly.

· We also do not foresee any significant negative dent on PAK-USA relationships due to �Raymend Davis

Case� after discounting the American realization of ground-realities over the general public sentiments

and the USA-backed government�s position in any extra beneficial move for it.

· Furthermore, for the time being, the government is not likely to gather the required support for the

implementation of RGST, however, keeping in view the nature of domestic politics, we cannot rule out

such a possibility by the mid-2011. As a positive surprise, a road-map to implement it could also be

announced after the upcoming All party round-table conference.

· Otherwise, in a worse-case scenario, the government still has some constitutional power to implement

RGST (though for a specified period) without the parliament�s approval.

Noisy but normal

Strategy| Pakistan

First Capital Equities Ltd

POLITICS

14

· During the last three years, the sensible and rational approach by top opposition leader Nawaz Sharif

towards the continuation of democracy as well as the parliament�s setup provide us a strong argument

to assume that there will be very limited chances of any government-derailing efforts at least by PML-

N.

· While, the judiciary is still expected to pursue its so-called uncompromised approach, the ruling setup�s

�no-collision with institutions� strategy is providing enough grounds to assume a low-probability of any

major legal/constitutional break-down in the near-future.

· On the law and order front, the provincial government - with the help of Pakistan Army has successfully

established its writ in the Swat and South Waziristan regions.

· Going forward, Pak Army is likely to start a full scale military operation in North-Waziristan as there is

an immense pressure from US and the international community to pursue a military operation in the

region in order to eliminate the remaining terrorist hide-outs and their cross-border movement in

Afghanistan.

· In our opinion, a notable surge in the terrorist attacks in retaliation of this possible full scale military

operation cannot be ruled out. However, as their infrastructure has been considerably damaged due to

the army�s targeted strikes in the region along with weak country network strength, the fall-out is not

likely to be notable as was in 2008 Swat Operation.

Dec-2011 Index target of 13,500

Strategy| PakistanMarch 07, 2011

First Capital Equities Ltd

MARKET

15

KSE yielded 28% gain in 2010

· Despite macro concerns, imposition of a capital gains tax, devastating floods, monetary tightening and

political hiccups, Pakistan equities provided a lucrative gain of 28% in 2010.

· Upturn in the earnings cycle, increased foreign participation, status quo on sovereign ratings and positive

expectations over the reintroduction of leverage product caused equity values to continue their upward

trajectory.

· It may not be wrong to argue that the index remained single-stock driven. That said, the heavyweight

OGDC (current index weightage of 24%) rallied 54% in 2010. Thus, OGDC alone contributed nearly 40%

of the 2010 index gain.

Bull run expected to continue in 2011

· In our opinion, the bull run at Pakistan market will be carried forward in 2011 too with scope for yet

another double-digit gain.

· Despite 28% price gains in 2010, Pakistan�s equity valuations remain attractive as companies� earnings

are likely to see a rebound in 2011.

· The Pakistani market is currently trading at an FY11E PE of ~7.2x � a discount of 24% from its average

of 9.5x over the last 15 years.

· Interestingly, excluding OGDC, which is trading at a higher PE multiple, the market multiples look more

attractive at 6.3x on 2011E estimates.

· At a target of PE 8.0x, we have calculated the end-December 2011 KSE-Index at ~13,500. This also

incorporates the FY11E dividend yield of 7.5% because the KSE-100 is a total return index.

Key drivers in 2011

Strategy| PakistanMarch 07, 2011

First Capital Equities Ltd

MARKET

16

Pakistan�s equity market is likely to be influenced by the following catalysts in upcoming trading sessions:

· Corporate earnings are likely to depict double digit growth in 2011. In 2010, the overall corporate profits

were up by 18%. The earnings trend is likely to show further improvement in 2011 due to better expectations

from the core growth of E&P, banking, fertilizer and power sector companies. All in all, we expect

corporate earnings in Pakistan to depict an average growth of ~22% in 2011. High earnings growth on the

corporate side will ensure valuations to remain at attractive levels even after 28% increase in equity

prices during 2010.

· We expect share prices to react positively on the introduction of the much needed leverage product.

In this regard, the Margin Trading System (MTS) is likely to be launched by mid March 2011.

· Developments on structural reforms, like elimination of nonproductive subsidies, RGST implementation

and settlement of circular debt would be positive for the overall economic situation.

· With investment opportunities in emerging giants like China & India and frontier markets continuing

to lessen, Pakistan�s untapped and under-capitalized equity market would continue to attract the foreign

interest. Despite the challenging macro and political situation, we have not witnessed panic selling by

the foreign investors. In fact, offshore funds have remained net buyers and injected ~US$526mn in 2010

(2011 YTD US$66mn). We expect foreign inflows to continue in 2011 given the steep valuation gap of

Pakistan vis-à-vis regional peers and strong global liquidity.

· With strong valuations pegged with Pakistani equities, the PE discount to regional peers could see a

further re-rating depending on progress on structural reforms (RGST, circular debt), macro recovery/stability,

IMF assistance, inflows from US & FODP and security situation.

· Monetary tightening is likely to continue till mid-2011 with the expectation of further 50-100bps hikes

in policy rate. Thus, interest rate would peak out in mid-2011. Thereafter, we expect stable (if not

relaxing) monetary environment.

2011E 2012E 2011E 2012E 2011E 2012E

Key drivers in 2011

Strategy| Pakistan

First Capital Equities Ltd

MARKET

17

· Positive developments on privatization front and M&As would also help in retaining investors� confidence.

· On the political front, we think the government will keep facing problems and we might see political

hiccups to continue. However, this is inherited in the domestic political system of the country. We do

not anticipate any serious threat for the prevailing democratic setup. Meanwhile, the successful 18th

and 19th constitutional amendments have highlighted the growing political maturity.

· In the absence of other viable investment options, the market will keep attracting the domestic liquidity,

we believe. Meanwhile, the fundamental recovery would also attract the foreign investment flows.

Regional Valuations

Pakistan

Korea

Thailand

Philippine

Hong Kong

Taiwan

China

Indonesia

Malaysia

India

Median

Pakistan Discount to Region

Source: Bloomberg, FCEL Research

7.2

10.0

11.7

12.1

12.4

12.6

13.4

13.7

14.5

16.6

12.64

-43%

1.5

1.3

1.8

1.9

1.7

1.8

2.1

2.8

2.2

2.8

1.9

-20%

7.4

1.5

3.8

3.7

3.4

3.9

2.2

2.4

3.6

1.4

3.4

0.5

0.9

0.8

1.0

0.8

1.1

0.7

0.7

1.3

0.9

0.9

PE(x)

6.3

9.0

10.2

10.8

10.8

11.3

11.3

11.4

13.1

13.9

11.3

-44%

8.6

1.6

4.3

3.8

3.9

4.2

2.5

2.9

3.9

1.6

3.8

1.4

1.2

1.6

1.7

1.5

1.6

1.8

2.5

2.0

2.4

1.7

-19%

PBv(x) Div Yield (%) PEG Ratio

2011ECountries

Adopt a bottom-up approach

Strategy| Pakistan

First Capital Equities Ltd

MARKET

18

· A bottom-up approach seems more effective than a top-down investment strategy for Pakistani market

where selective stock pickings could help the investors to outperform the broader market.

· We say this by considering the fact that despite a modest GDP growth of 5% on average in last 10 years

(FY01-10), Pakistan�s equity market has yielded an impressive return of 26% annually.

· GDP growth does not necessarily transform into a proportionate growth in corporate earnings, EPS,

dividends and ultimately returns to investors. While short-term changes in GDP growth can have an impact

on equity values, there may not necessarily a long-term connection.

· In Pakistan, stock market represents smaller part of the overall domestic GDP. Market Cap as % of GDP

is only ~18-20%. Total sales of listed companies represent only 22% of the total GDP. That means performance

of non listed companies, which occupy major chunk of economy is not reflected in the stock market

return.

· Another argument is that GDP represents a total value of goods and services produced in the country

for a given year. It does not indicate the profitability of the companies. If sales are growing but profitability

is declining, stocks are not likely to rally.

· This does not mean that GDP is a totally useless indictor to look for before making investment.

Pakistan equities: Cheapest in the region

Strategy| Pakistan

First Capital Equities Ltd 19

Source: Bloomberg, FCEL Research

PE2011E

Source: Bloomberg, FCEL Research

PE 2011E vs EPS growth 2012E

3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Pakistan

Korea

Thailand

Philippine

Hong Kong

Taiwan

China

Indonesia

Malaysia

India

MARKET

Source: Bloomberg, FCEL Research

Dividend Yield 2011E

0

1

2

3

4

5

6

7

8

9

India

Kore

a

Chin

a

Indonesi

a

Hong

Kong

Mala

ysia

Philip

pin

e

Thailand

Taiw

an

Paki

stan

Source: Bloomberg, FCEL Research

PBv 2011E

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Kore

a

Paki

stan

Hong

Kong

Thailand

Taiw

an

Philip

pin

e

Chin

a

Mala

ysia

India

Indonesi

a

0%

5%

10%

15%

20%

25%

Pakistan

Korea

Thailand

Philippine

Hong Kong

Taiwan

China

Indonesia

Malaysia

India

5 7 9 11 13 15 17 19

Market PE & Index target

Strategy| Pakistan

First Capital Equities Ltd 20

MARKETSource: Bloomberg

Market PE (12-months trailing EPS)

0

5

10

15

20

25

Feb-0

6

Jun-0

6

Oct

-06

Feb-0

7

Jun-0

7

Oct

-07

Feb-0

8

Jun-0

8

Oct

-08

Feb-0

9

Jun-0

9

Oct

-09

Feb-1

0

Jun-1

0

Oct

-10

Feb-1

1

Source: KSE & FCEL Research

Dec-2011 Index Target

KSE-100: Still more upside

5,000

7,000

9,000

11,000

13,000

15,000

17,000

11,223.5

13,500

(+ 20%)

Aug-

08

Nov-

08

Mar-

09

Jun-0

9

Oct

-09

Jan-1

0

May-

10

Aug-

10

Dec-

10

Mar-

11

May-

11

Aug-

11

Oct

-11

Dec-

11

Foreign participation

Strategy| Pakistan

First Capital Equities Ltd 21

MARKET

Source: NCCPL, KSE & FCEL Research

FPI vs KSE

Source: SBP, KSE & FCEL Research

Foreign Ownership

0

50

100

150

200

250

300

350

Jan-0

7

Apr-

07

Aug-0

7

Dec-

07

Mar-

08

Jul-

08

Nov-

08

Mar-

09

Jul-

09

Oct

-09

Feb-1

0

Jun-1

0

Sep-1

0

Jan-1

1

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%Foreign Inv (PRs bn) % of M.Cap

(200)

(150)

(100)

(50)

0

50

100

150

200

Apr-

08

Jun-0

8

Aug-

08

Oct

-08

Dec-

08

Feb-0

9

Apr-

09

Jun-0

9

Aug-

09

Oct

-09

Dec-

09

Feb-1

0

Apr-

10

Jun-1

0

Aug-

10

Oct

-10

Dec-

10

FPI (US$ mn) KSE-100 (RHS)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

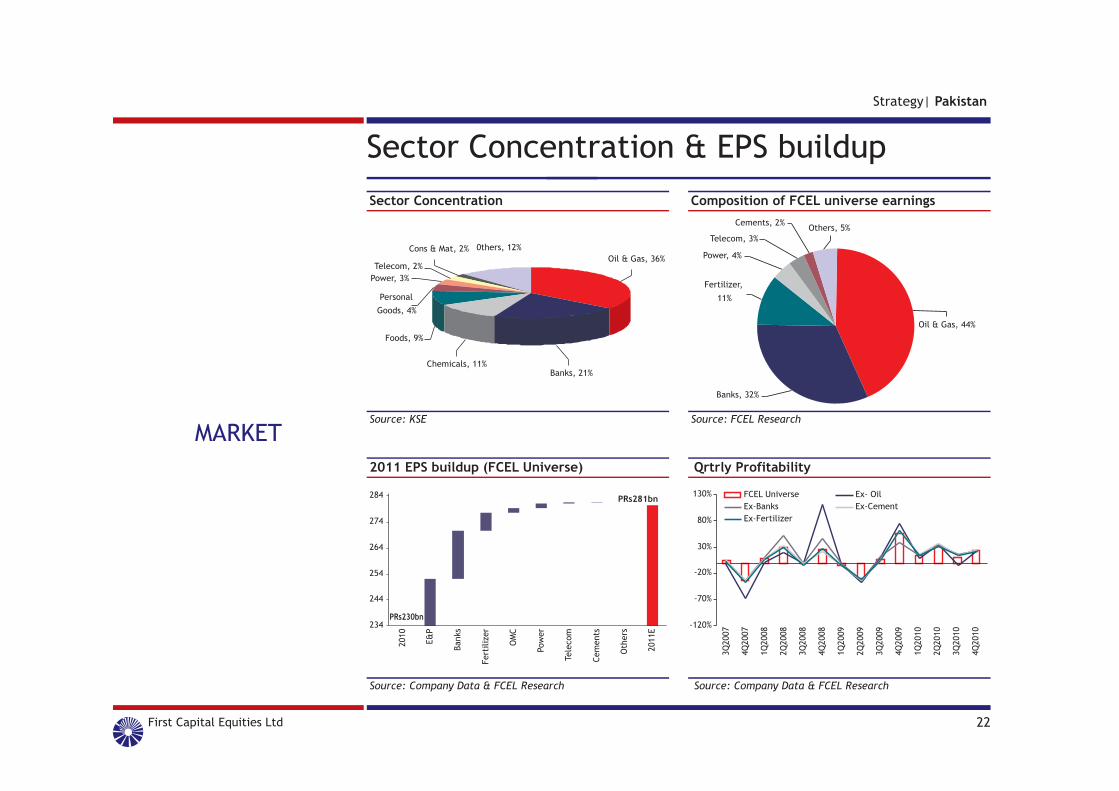

Sector Concentration & EPS buildup

Strategy| Pakistan

First Capital Equities Ltd 22

Source: KSE

Sector Concentration

Source: FCEL Research

Composition of FCEL universe earnings

MARKET

Fertilizer,

11%

Banks, 32%

Oil & Gas, 44%

Others, 5%

Power, 4%

Telecom, 3%

Cements, 2%

Oil & Gas, 36%

Banks, 21%Chemicals, 11%

Foods, 9%

Personal

Goods, 4%

0thers, 12%

Power, 3%

Telecom, 2%

Cons & Mat, 2%

234

244

254

264

274

284

2010

E&

P

Banks

Fert

iliz

er

OM

C

Pow

er

Tele

com

Cem

ents

Oth

ers

2011E

PRs281bn

PRs230bn

Source: Company Data & FCEL Research

2011 EPS buildup (FCEL Universe)

Source: Company Data & FCEL Research

Qrtrly Profitability

-120%

-70%

-20%

30%

80%

130%

3Q

2007

4Q

2007

1Q

2008

2Q

2008

3Q

2008

4Q

2008

1Q

2009

2Q

2009

3Q

2009

4Q

2009

1Q

2010

2Q

2010

3Q

2010

4Q

2010

FCEL Universe Ex- Oil

Ex-Banks Ex-Cement

Ex-Fertilizer

Earnings uptrend to continue in 2011

Strategy| Pakistan

First Capital Equities Ltd 23

Source: Company Data & FCEL Research

FCEL Universe Earnings growth

Source: Company Data & FCEL Research

Yearly profitability trend

MARKET

-5%

0%

5%

10%

15%

20%

25%

2007

2008

2009

2010

2011E

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2006

2007

2008

2009

2010

2011E

0%

5%

10%

15%

20%

25%

30%Revenues EBITDAEBIT PATEBITDA margins (RHS) Net margins (RHS)

Source: Company Data & FCEL Research

Earnings uptrend to continue

Earnings (PRs mn)Earnings growth (%)ROAE (%)ROAA (%)ROCE (%)PE (x)PBv (x)PS (x)EV/EBITDA (x)Dividend Yield(%)PEG Ratio

2010

230,32417.620.94.0

26.68.11.61.05.46.40.4

2011E

280,61021.822.54.4

30.67.21.50.94.37.40.5

2009

195,8409.1

20.13.9

25.16.81.30.86.58.70.4

2008

179,531(5.0)20.34.0

28.311.22.21.56.45.21.2

FCEL Universe

Decline in the country�s risk perception

Strategy| Pakistan

First Capital Equities Ltd 24

MARKET

Source: Bloomberg

Pakistan Euro Bond Yield (%)

Source: Bloomberg

Pakistan CDS

0

5

10

15

20

25

30

Feb-1

1

Oct

-10

Jun-1

0

Feb-1

0

Oct

-09

May-

09

Jan-0

9

Aug-

08

Apr-

08

Dec-

07

Aug-

07

Apr-

07

Dec-

06

Aug-

06

KSE versus monetary indicators

Strategy| Pakistan

First Capital Equities Ltd 25

Source: SBP, KSE & FCEL Research

DR vs KSE

Source: SBP, KSE & FCEL Research

T-Bill vs KSE

MARKET

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

Jan-9

9

Dec-

99

Oct

-00

Oct

-01

Sep-0

2

Jul-

03

Jun-0

4

May-

05

Apr-

06

Mar-

07

Feb-0

8

Jan-0

9

Dec-

09

Oct

-10

KSE100

DR

-

3

5

8

10

13

15

18

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Jul-

01

Jan-0

2

Aug-

02

Mar-

03

Sep-0

3

Mar-

04

Sep-0

4

Apr-

05

Oct

-05

May-

06

Nov-

06

May-

07

Dec-

07

Jun-0

8

Jan-0

9

Jul-

09

Jan-1

0

Aug-

10

Feb-1

1

KSE-100

T-Bill

0%

2%

4%

6%

8%

10%

12%

14%

16%

Source: SBP, KSE & FCEL Research

Price to Money ratio

0%

20%

40%

60%

80%

100%

120%

140%

Jan-0

2

Jun-0

2

Nov-

02

Apr-

03

Sep-0

3

Feb-0

4

Jul-

04

Dec-

04

May-

05

Oct

-05

Mar-

06

Aug-0

6

Jan-0

7

Jun-0

7

Nov-

07

Apr-

08

Sep-0

8

Feb-0

9

Jul-

09

Dec-

09

May-

10

Oct

-10

Source: SBP, KSE & FCEL Research

M2 growth vs KSE

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Sep-0

4

Feb-0

5

Jul-

05

Dec-

05

May-

06

Oct

-06

Mar-

07

Aug-

07

Jan-0

8

Jun-0

8

Nov-

08

Apr-

09

Sep-0

9

Feb-1

0

Jul-

10

Dec-

10

-5%

0%

5%

10%

15%

20%

25%

30%

35%KSE 100

M2

Strategy| Pakistan

First Capital Equities Ltd

Analyst Certification

All of the views expressed in this document accurately reflect the personal views of the responsible analyst(s) about any and all of the subject securitiesor issuers. No part of the compensation of the responsible analyst(s) named herein is, or will be, directly or indirectly, related to the specificrecommendations or views expressed by the responsible analyst(s) in this report.

Disclaimer

This information and opinion contained in this report have been complied by our research department from sources believed by it to be reliable and ingood faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. All opinions and estimatescontained in the document constitute the department�s judgment as of the date of this document and are subject to change without notice and areprovided in good faith but without legal responsibility.

This report is not, and should not be construed as, an offer to sell or a solicitation of an offer to buy any securities. First Capital Equities Limited (thecompany) or persons connected with it may from time to time have an investment banking or other relationship, including but not limited to, theparticipation or investment in commercial banking transactions (including loans) with some or all of the issuers mentioned therein, either for their ownaccount or the account of their customers. Persons connected with the company may provide or have provided corporate finance and other services tothe issuer of the securities mentioned herein, including the issuance of options on securities mentioned herein or any related investment and may makea purchase and/or sale, or offer to make a purchase and/or sale of the securities or any related investment from time to time in the open market orotherwise, in each case either as principal or agent.

This report may contain forward looking statements which are often but not always identified by the use of words such as �anticipate�, �believe�,�estimate�, �intend�, �plan�, �expect�, �forecast�, �predict� and �project� and statements that an event or result �may�, �will�, �can�, �should�,�could� or �might� occur or be achieved and other similar expressions. Such forward looking statements are based on assumptions made and informationcurrently available to us and are subject to certain risks and uncertainties that could cause the actual results to differ materially from those expressedin any forward looking statements. Readers are cautioned not to place undue relevance on these forwardlooking statements. FCEL expressly disclaimsany obligation to update or revise any such forward looking statements to reflect new information, events or circumstances after the date of thispublication or to reflect the occurrence of unanticipated events.

Exchange rate fluctuations may affect the return to investors. Neither the company or any of its affiliates, nor any other person, accepts any liabilitywhatsoever for any direct or consequential loss arising from any use of this report or the information contained therein.

First Capital Equities, their respective affiliate companies, associates, directors and/or employees may have investments in securities or derivatives ofsecurities of companies mentioned in this report, and may make investment decisions that are inconsistent with the views expressed in this report.Neither the company or any of its affiliates, nor any other person, accepts any liability whatsoever for any direct or consequential loss arising from anyuse of this report or the information contained therein.