overview of yavapai college comprehensive annual financial

TRANSCRIPT

YC Yavapai CollegeFebruary 2019

Overview of Yavapai CollegeComprehensive Annual Financial

Report & Audit Results

FY 2017-18

Financial Audit & Internal Controls Report over Financial Reportingo No audit findings

Unmodified Audit Opinion

The Certificate of Achievement for Excellence in Financial Reporting award from GFOA

Federal Single Audito No audit findings

YC

Positive Financial Results

Statement of Net Position (Balance Sheet)

Statement of Revenues, Expenses, and Changes in Net Position (Income Statement)

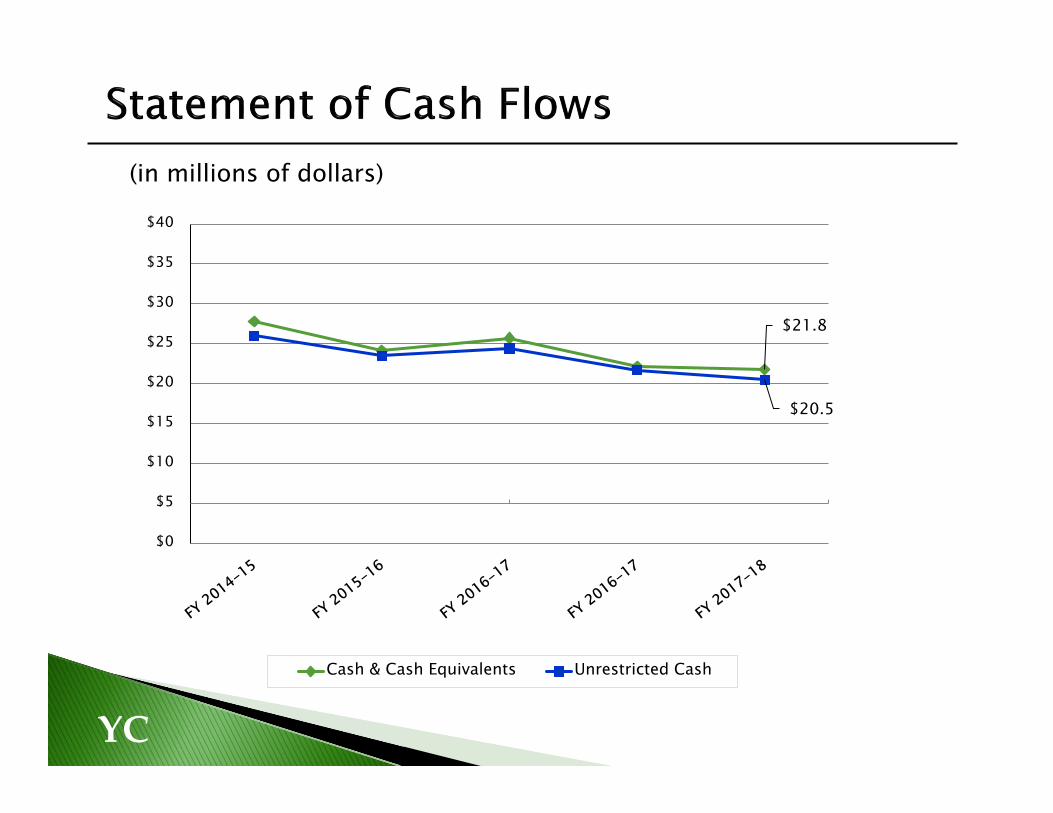

Statement of Cash flows

YC

YC

$86.5 $97.8

$107.9 $121.9

$133.8 $1.8

$1.9 $1.4

$1.3 $1.3

$(11.2) $(10.7) $(8.9) $(10.7) $(11.2)

$77.1

$89.0

$100.4 $112.5

$123.9

($20)

$0

$20

$40

$60

$80

$100

$120

$140

2013-14 2014-15 2015-16 2016-17 2017-18

Net Investment in Capital Assets Restricted Net Assets Unrestricted Net Assets

(in millions of dollars)

YC

$74.5

$62.7

$11.9

$-

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

Total Revenues

Total Expenses

Increase in Net Position

(in millions of dollars)

YC

(in millions of dollars)

$21.8

$20.5

$0

$5

$10

$15

$20

$25

$30

$35

$40

Cash & Cash Equivalents Unrestricted Cash

YC

$49.5M

$16.1M

$235

$71

$-

$50

$100

$150

$200

$250

$-

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

GO Bond Debt Debt per Capita

YC

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

$‐

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

Other

Tuition & Fees

Property Taxes

State Aid

State Aid %

Tuition & Fees %

(in millions of dollars)

Report to HLC annually• Both with and without the impact of GASB 68

pension liabilities. • NACUBO benchmarks have not been updated

to reflect the impact of GASB 68.• YC’s CFI score meets the HLC’s acceptable

range.

Provides insight on the financial health of the District

YC

Composite Financial Index

YC

Primary Reserve Ratio Viability Reserve Ratio

Return on Net Assets Ratio Net Operating Revenue Ratio

YC

The CFI is a combination of the four core ratios using a prescribed weighting thatis an indicator of the overall financial health of an institution. It’s important to note that the benchmarks used for the CFI have not been updated to reflect pension liabilities, and consequently, the benchmarks do not necessarily provide the financial guidance intended when developed. The HLC requires the CFI be reported with and without the pension liabilities.

(NACUBO)

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Composite Score

Composite Score (w/Pension Liability)

Benchmark

YC