overview of the tax structure - mid-state technical...

TRANSCRIPT

CCH Essentials of Federal

Income Taxation

1 of 35

Chapter 1

Overview of the Tax Structure

CCH Essentials of Federal Income Taxation

©2007, CCH INCORPORATED

4025 West Peterson Ave.

Chicago, IL 60646-6085

http://www.cch.com

CCH Essentials of Federal

Income Taxation

3 of 35

Responsibilities of Taxpayers

• Prepare appropriate tax forms and schedules

• Determine correct tax liability

• Pay tax due on time

• File return on time with proper IRS Regional

Service Center and keep evidence of on-time

mailing

• Maintain records and documents to support

tax return data

• Try to minimize tax return errors

CCH Essentials of Federal

Income Taxation

4 of 35Chapter 1

Taxable Income Formula

Income from all sources

– Exempt income

= Gross income

– Deductions

= Taxable income

CCH Essentials of Federal

Income Taxation

5 of 35Chapter 1

Which Form do I file?

• Individuals choose one of three tax forms:

– 1040EZ (no dependents)

– 1040A (limited sources of income)

– 1040 (all others)

• Wisconsin tax forms

CCH Essentials of Federal

Income Taxation

6 of 35

Tax Filing Groups

• Single

• Head of household

• Married filing a joint return

• Married filing a separate return

• Surviving spouse (a qualifying widow or

widower with a dependent child)

CCH Essentials of Federal

Income Taxation

7 of 35Chapter 1

Basic Tax Formula for IndividualsIncome from all sources

– Exempt income

= Gross income

– Deductions for AGI (adjusted gross income)

= AGI

– Deductions from AGI

Itemized or standard deduction

Exemptions (personal and dependency)

= Taxable income

Tax Rate

= Tax liability before:

+ Additions to tax

– Credits to tax

= Final tax due (refund)CCH Essentials of Federal

Income Taxation

8 of 35Chapter 1

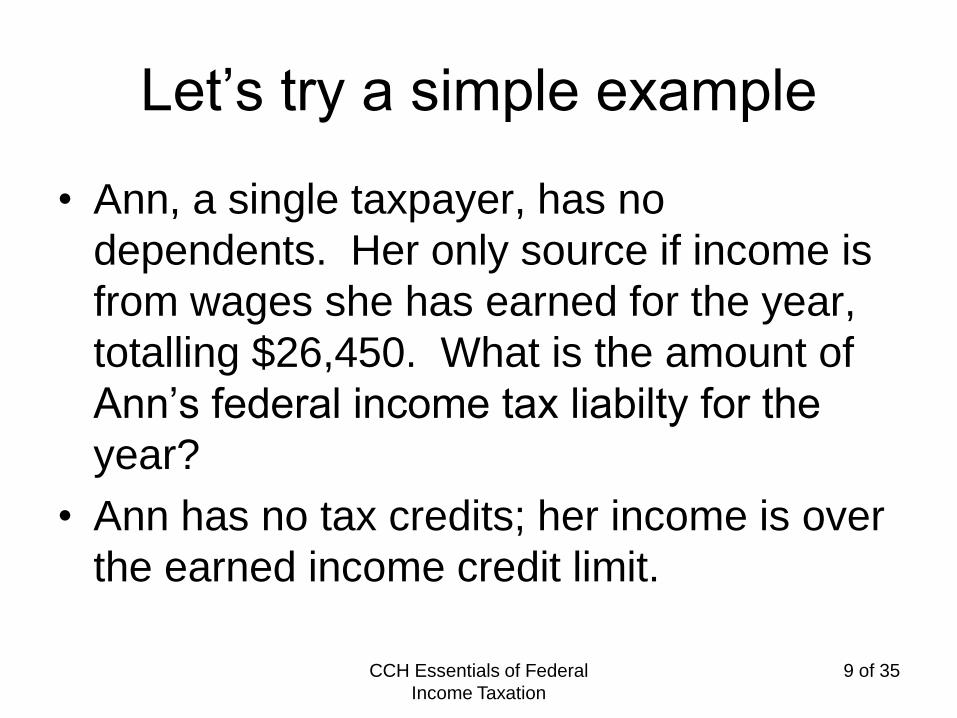

Let’s try a simple example

• Ann, a single taxpayer, has no

dependents. Her only source if income is

from wages she has earned for the year,

totalling $26,450. What is the amount of

Ann’s federal income tax liabilty for the

year?

• Ann has no tax credits; her income is over

the earned income credit limit.

CCH Essentials of Federal

Income Taxation

9 of 35

Basic Tax Formula for AnnIncome from all sources

– Exempt income

= Gross income

– Deductions for AGI (adjusted gross income)

= AGI

– Deductions from AGI

Itemized or standard deduction

Exemptions (personal and dependency)

= Taxable income

Tax Rate

= Tax liability before:

+ Additions to tax (- Telephone tax refund)

– Credits to tax

= Final tax due (refund)CCH Essentials of Federal

Income Taxation

10 of 35Chapter 1

Gross Income

• Compensation for services, including fees, commissions, fringe benefits, and similar items

• Gross income from business

• Property transaction gains

• Interest

• Rents

• Royalties

• Dividends

• Alimony and separate maintenance payments

• Annuities

• Life insurance and endowment contract income

• Pensions

• Income from forgiven debt

• Share of distributive partnership income

• Income in respect of a decedent

• Income from an interest in an estate or trust

CCH Essentials of Federal

Income Taxation

11 of 35

The Code lists the following different gross income sources (and

implies that others exist):

Chapter 1

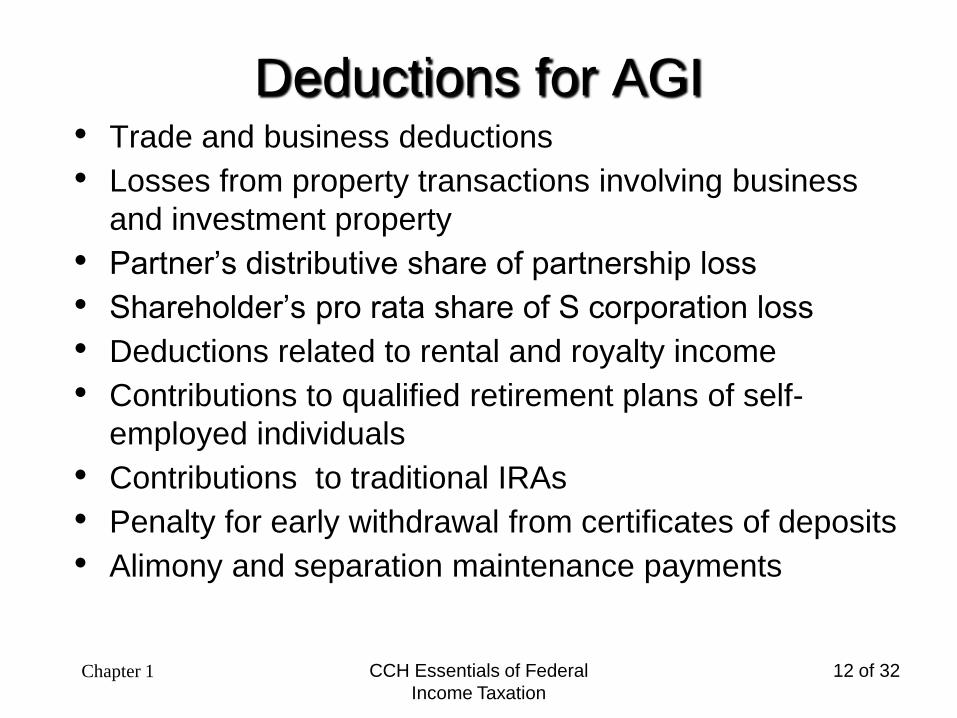

Deductions for AGI• Trade and business deductions

• Losses from property transactions involving business

and investment property

• Partner’s distributive share of partnership loss

• Shareholder’s pro rata share of S corporation loss

• Deductions related to rental and royalty income

• Contributions to qualified retirement plans of self-

employed individuals

• Contributions to traditional IRAs

• Penalty for early withdrawal from certificates of deposits

• Alimony and separation maintenance payments

CCH Essentials of Federal

Income Taxation

12 of 32Chapter 1

Deductions for AGI (continued)• Qualified moving expenses

• One-half self-employment tax

• 100% of health insurance premiums paid by a self-

employed person

• Contributions made to medical or health savings

accounts

• Interest paid on student loans

• Certain expenses of reservists, performing artists, and

fee-based government officials

• Deduction for domestic production activities

• Educator’s expenses

• Deduction for tuition and fees

CCH Essentials of Federal

Income Taxation

13 of 32Chapter 1

Deductions from AGI

(itemized deductions)• Medical

• Taxes

• Interest

• Contributions

• Casualty and theft losses

• Job expenses and some miscellaneous

deductions

• Other miscellaneous deductions

CCH Essentials of Federal

Income Taxation

14 of 35Chapter 1

Standard Deduction

The standard deduction consists of two

factors:

• Basic standard deduction (M, HOH, S)

• $10,700; 7,850; 5,350

• Additional standard deduction

• $1,050 or 1,350 for HOH & S

CCH Essentials of Federal

Income Taxation

15 of 35Chapter 1

Standard Deduction--

Dependents• Greater of:

o $850 or

o Earned Income plus $300

o But cannot > $5,350

See text figure 1-1

CCH Essentials of Federal

Income Taxation

16 of 35

Exemptions

• $3,400

• Exemption for self

• Exemption for spouse

• Exemptions for dependents

– Qualifying relatives

– Qualifying nonrelatives

– Qualifying children

CCH Essentials of Federal

Income Taxation

17 of 35Chapter 1

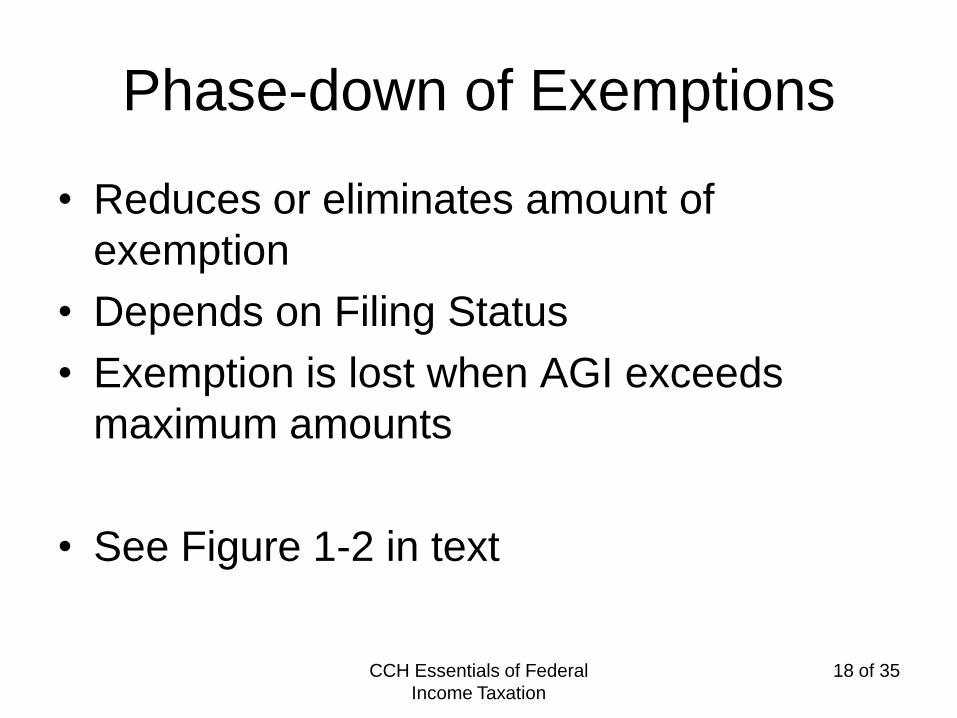

Phase-down of Exemptions

• Reduces or eliminates amount of

exemption

• Depends on Filing Status

• Exemption is lost when AGI exceeds

maximum amounts

• See Figure 1-2 in text

CCH Essentials of Federal

Income Taxation

18 of 35

Who is a dependent?

• Let’s brainstorm.

• In a small group, make a list of any

person who you know who is financially

dependent on another person. We don’t

want names, but rather how these persons

are connected. Think of situations you

know of personally, as well as situations

which may occur in various aspects of life.

CCH Essentials of Federal

Income Taxation

19 of 35

Dependency groups

• 1. A relative dependent

• 2. A non-relative dependent

• 3. A child

CCH Essentials of Federal

Income Taxation

20 of 35

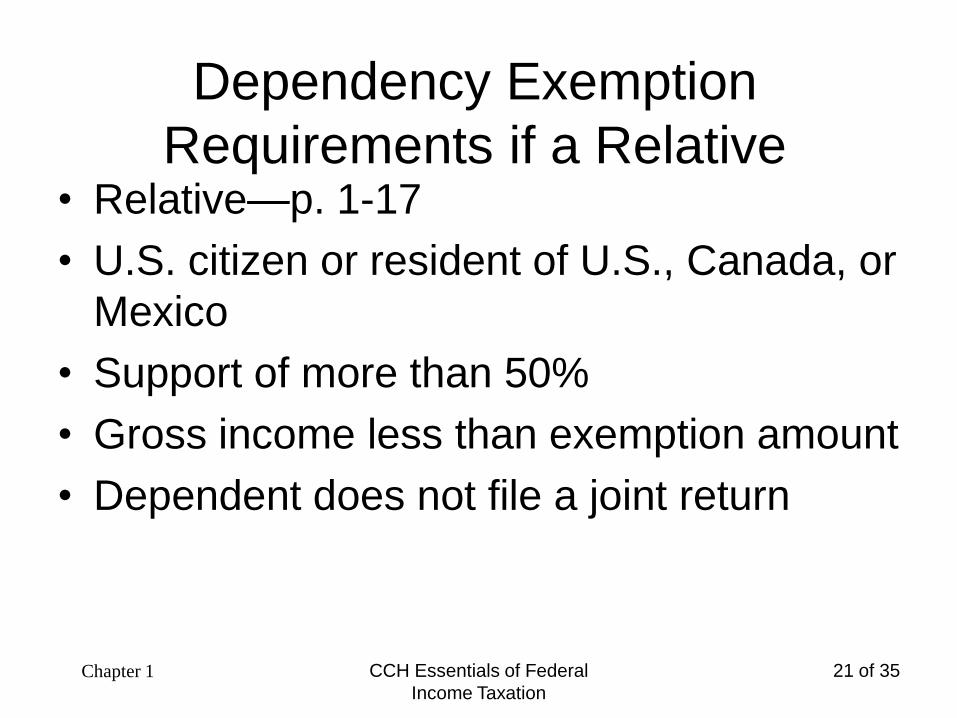

Dependency Exemption

Requirements if a Relative• Relative—p. 1-17

• U.S. citizen or resident of U.S., Canada, or

Mexico

• Support of more than 50%

• Gross income less than exemption amount

• Dependent does not file a joint return

CCH Essentials of Federal

Income Taxation

21 of 35Chapter 1

Gross Income Test

see page 1-16

• Dependent’s gross income must be

<$3400

EXCEPTIONS:

if child and under age 19

if child is full-time student under age 24

do not count Soc. Sec., Medicare, or

exempt interest the dependent may

receive

CCH Essentials of Federal

Income Taxation

22 of 35

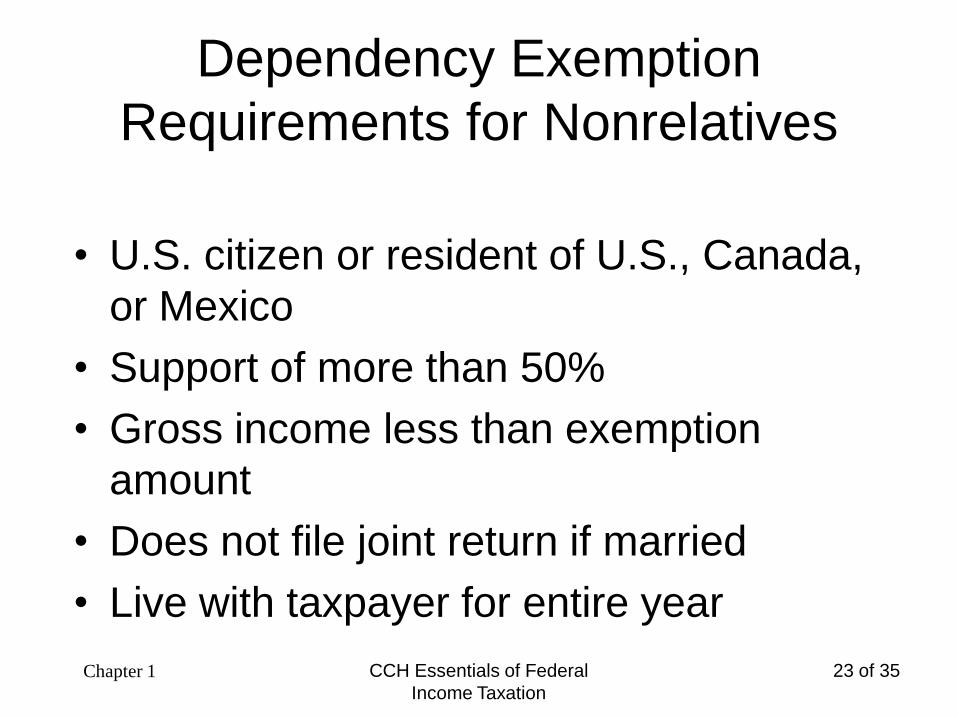

Dependency Exemption

Requirements for Nonrelatives

• U.S. citizen or resident of U.S., Canada,

or Mexico

• Support of more than 50%

• Gross income less than exemption

amount

• Does not file joint return if married

• Live with taxpayer for entire year

CCH Essentials of Federal

Income Taxation

23 of 35Chapter 1

Criteria for Qualifying Children

• Does not provide over half of own support

• Does not file a joint return (if married)

• Is a U.S. citizen or resident of the U.S., Canada or Mexico

• Passes the relationship test by being the taxpayer’s descendent (child, grandchild, etc.), sibling (sister or brother) or descendent of the taxpayer’s sibling (niece or nephew)

• Passes the age test by being under age under 19 or a full-time student under age 24

• Passes the residency test by having as a principal residence the taxpayer’s home

CCH Essentials of Federal

Income Taxation

24 of 35Chapter 1

Calculation of Dependent’s Support

A dependent’s support consists of these three

amounts:

• Fair rental value of lodging

• Proper share of expenses incurred or paid

directly to or for the dependent

• Share of household expenses (such as food but

not lodging) unrelated to specific household

members

CCH Essentials of Federal

Income Taxation

25 of 35Chapter 1

Multiple Support Agreement

• Provide more than 10% of the dependent’s support

• Provide, with the other group members, more than 50% of the dependent’s support

• Meet the other dependency tests

• Group members who do not claim the exemption need to complete and deliver a Form 2120 to the claiming member. By signing the form, they agree not to claim the exemption for that year. See p. 1-20.

• The claiming member needs to file the Forms 2120 with the year’s tax return.

CCH Essentials of Federal

Income Taxation

26 of 35

The group member claiming the exemption must pass the

following tests:

Chapter 1

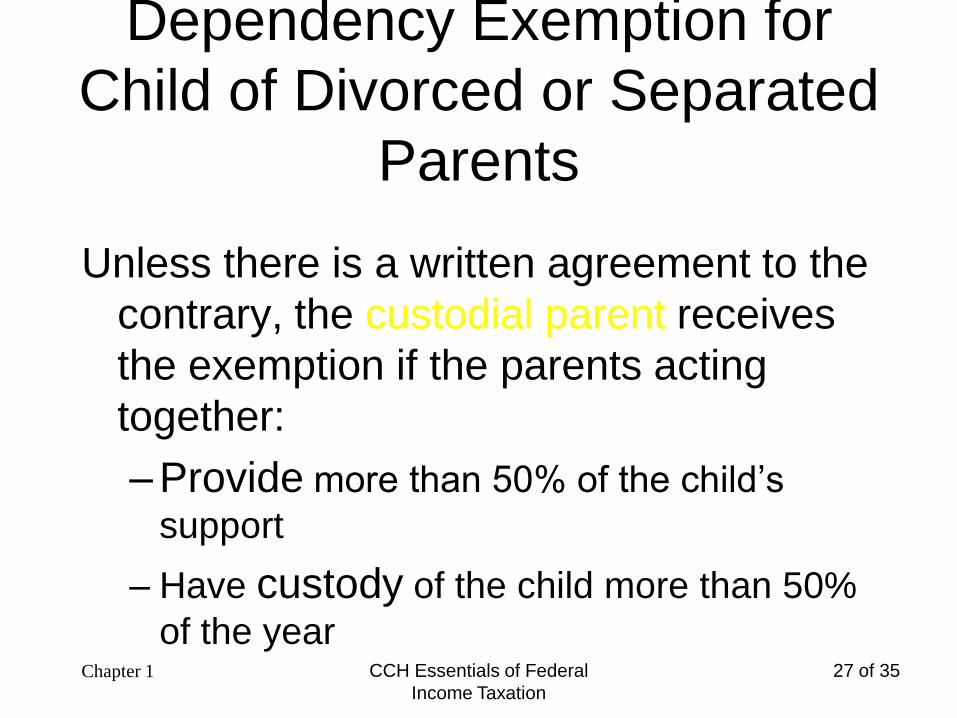

Dependency Exemption for

Child of Divorced or Separated

Parents

Unless there is a written agreement to the

contrary, the custodial parent receives

the exemption if the parents acting

together:

– Provide more than 50% of the child’s

support

– Have custody of the child more than 50%

of the yearCCH Essentials of Federal

Income Taxation

27 of 35Chapter 1

Tie Break Rules for the

Dependency Exemption

• When only one of the child’s parents is among the group of persons who qualifies to claim the child as a dependent, the dependency exemption goes to the parent.

• When both parents qualify to claim the child as a dependent, the exemption goes to the custodial parent.

• When both parents qualify to claim the child as a dependent and there is no custodial parent, the exemption goes to the parent with the highest AGI.

• When neither parent qualifies to claim the child as a dependent, the dependency exemption goes to the (non-parent) taxpayer with the highest AGI who can claim the child as a dependent.

CCH Essentials of Federal

Income Taxation

28 of 32Chapter 1

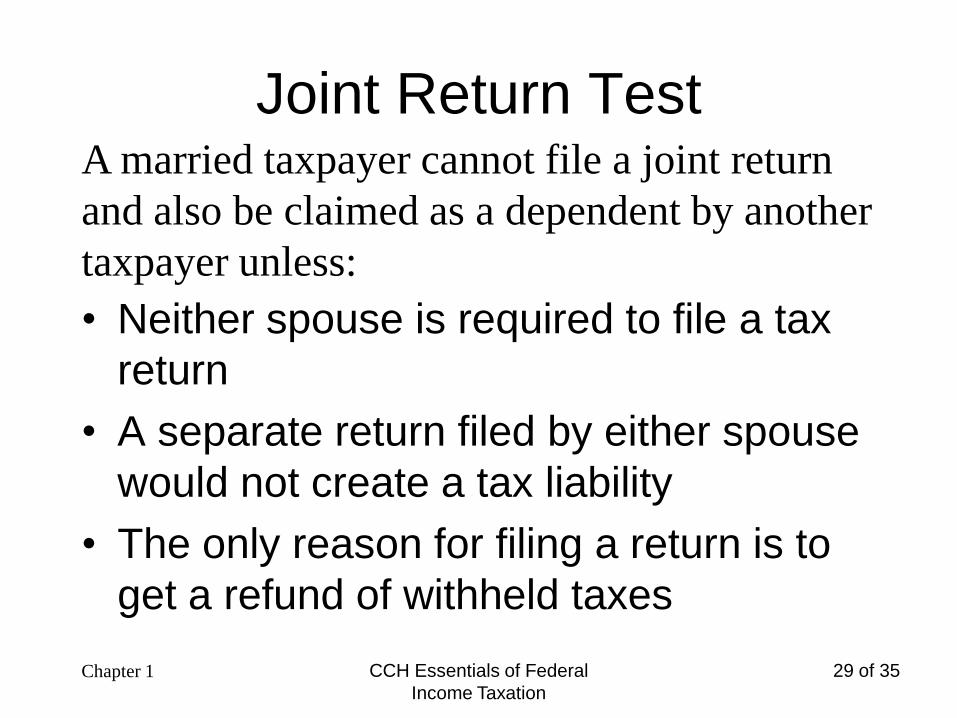

Joint Return Test

• Neither spouse is required to file a tax

return

• A separate return filed by either spouse

would not create a tax liability

• The only reason for filing a return is to

get a refund of withheld taxes

CCH Essentials of Federal

Income Taxation

29 of 35

A married taxpayer cannot file a joint return

and also be claimed as a dependent by another

taxpayer unless:

Chapter 1

CCH Essentials of Federal

Income Taxation

30 of 35

FILING STATUS

Single TaxpayerPersons who fall into this group include:

• Unmarried persons

• Persons separated by a final divorce

decree or separate maintenance

agreement

• Certain widow(er)s and abandoned

spouses

CCH Essentials of Federal

Income Taxation

31 of 35Chapter 1

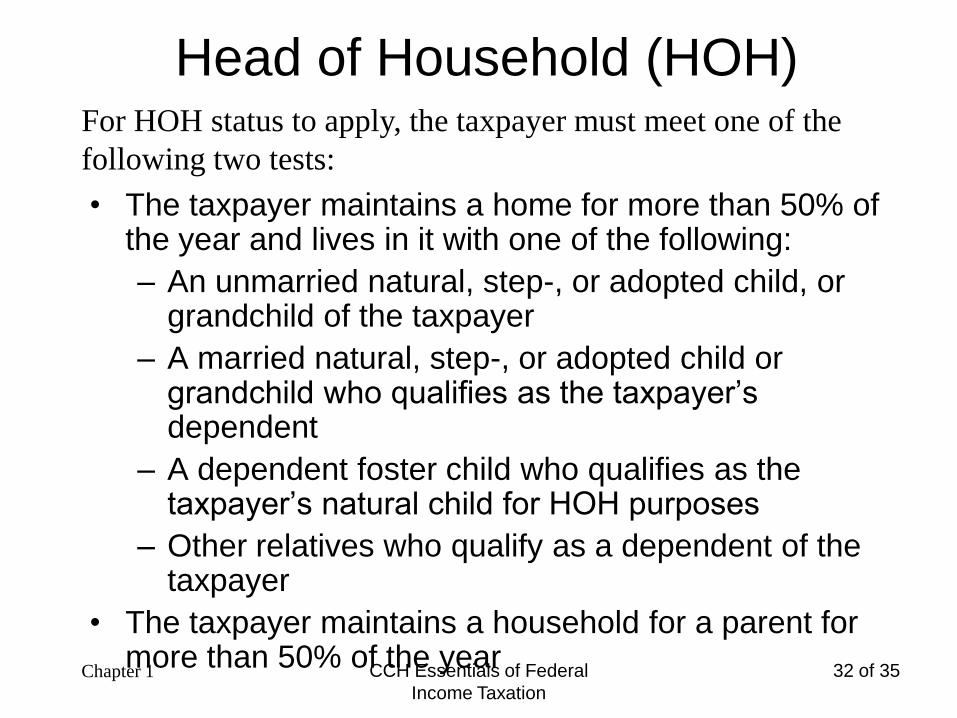

Head of Household (HOH)

• The taxpayer maintains a home for more than 50% of the year and lives in it with one of the following:

– An unmarried natural, step-, or adopted child, or grandchild of the taxpayer

– A married natural, step-, or adopted child or grandchild who qualifies as the taxpayer’s dependent

– A dependent foster child who qualifies as the taxpayer’s natural child for HOH purposes

– Other relatives who qualify as a dependent of the taxpayer

• The taxpayer maintains a household for a parent for more than 50% of the year

CCH Essentials of Federal

Income Taxation

32 of 35

For HOH status to apply, the taxpayer must meet one of the

following two tests:

Chapter 1

Joint Return Test

• Neither spouse is required to file a tax

return,

• A separate return filed by either spouse

would not create a tax liability, and

• The only reason for filing a return is to get

a refund of all federal income taxes

withheld CCH Essentials of Federal

Income Taxation

33 of 32

A married taxpayer cannot file a joint return

and also be claimed as a dependent by another

taxpayer unless:

Chapter 1

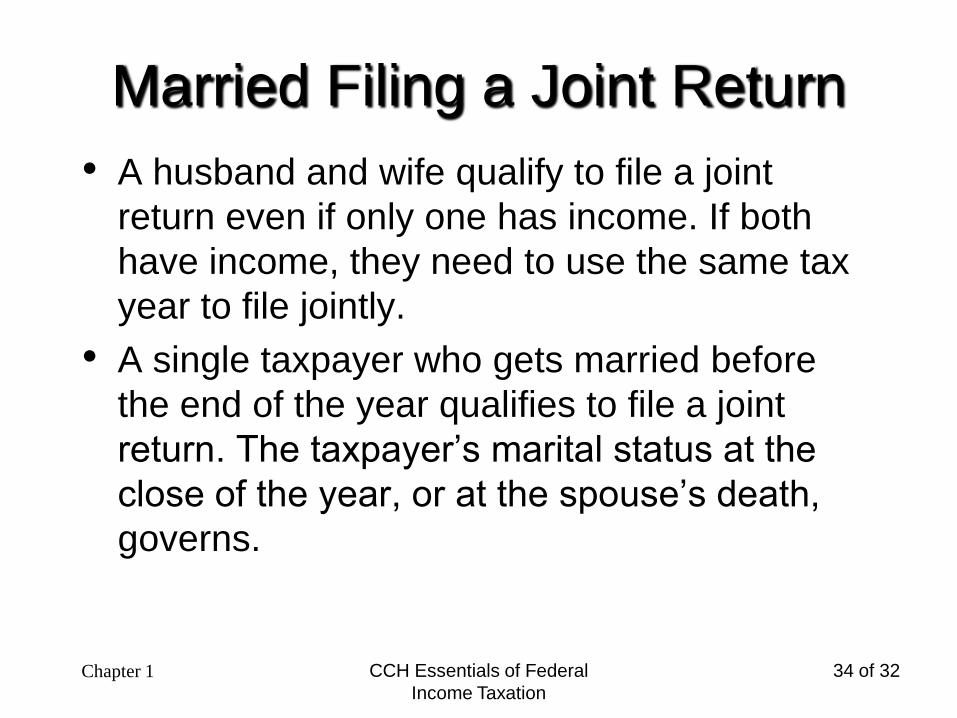

Married Filing a Joint Return

• A husband and wife qualify to file a joint

return even if only one has income. If both

have income, they need to use the same tax

year to file jointly.

• A single taxpayer who gets married before

the end of the year qualifies to file a joint

return. The taxpayer’s marital status at the

close of the year, or at the spouse’s death,

governs.

CCH Essentials of Federal

Income Taxation

34 of 32Chapter 1

Married Filing a Separate

ReturnWhen a husband and a wife have

separate incomes, they may realize savings

by filing separate returns. Taxpayers should

test joint and separate return status to see

which one yields the least tax liability.

CCH Essentials of Federal

Income Taxation

35 of 35Chapter 1

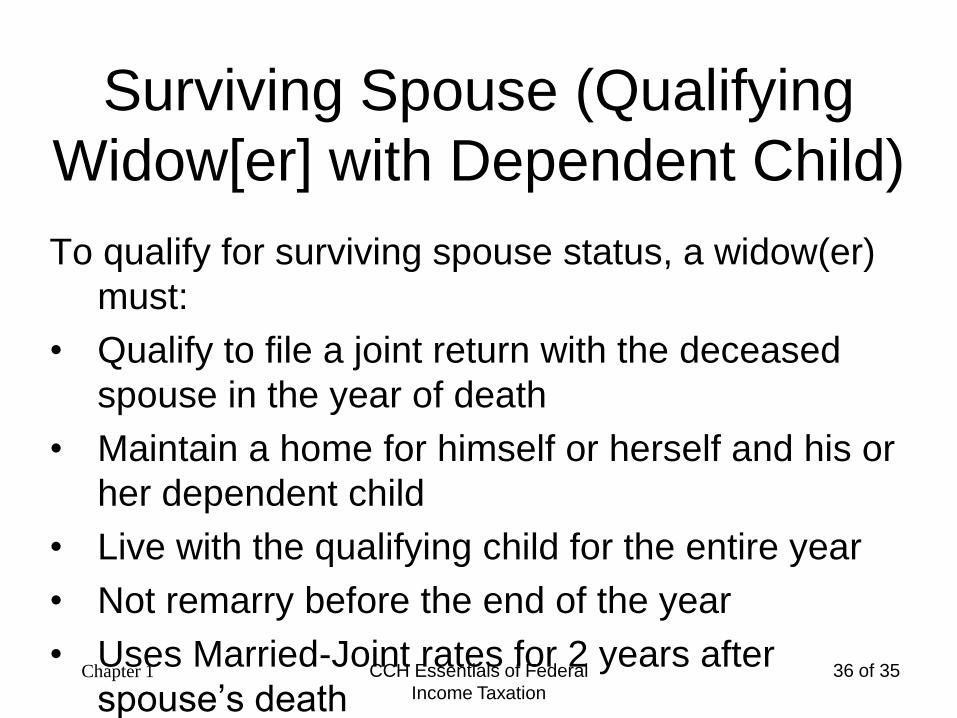

Surviving Spouse (Qualifying

Widow[er] with Dependent Child)

To qualify for surviving spouse status, a widow(er)

must:

• Qualify to file a joint return with the deceased

spouse in the year of death

• Maintain a home for himself or herself and his or

her dependent child

• Live with the qualifying child for the entire year

• Not remarry before the end of the year

• Uses Married-Joint rates for 2 years after

spouse’s deathCCH Essentials of Federal

Income Taxation

36 of 35Chapter 1

Married Filing a Joint Return

• A husband and wife qualify to file a joint

return even if only one has income. If both

have income, they need to use the same tax

year to file jointly.

• A single taxpayer who gets married before

the end of the year qualifies to file a joint

return. The taxpayer’s marital status at the

close of the year, or at the spouse’s death,

governs.

CCH Essentials of Federal

Income Taxation

37 of 32Chapter 1

Married Filing a Separate

Return• When a husband and a wife have

separate incomes, they may realize

savings by filing separate returns.

Taxpayers should test joint and

separate return status to see which one

yields the least tax liability.

CCH Essentials of Federal

Income Taxation

38 of 32Chapter 1

Filing Requirements for Persons

Not Claimed as a Dependent

A tax return must be filed when:

• Net earnings from self-employment >

$400, or

• Gross income > personal exemption

amount + basic standard deduction +

additional standard deduction for age (if

applicable)

– If MFS, a return must be filed if gross income

exceeds the personal exemption amount

– If MFJ, use both spouse’s exemption

CCH Essentials of Federal

Income Taxation

39 of 32Chapter 1

Filing Requirements for Persons

Claimed as a Dependent

A tax return must be filed when:

• Gross income > the sum of additional

standard deductions for age and blindness

(if applicable) plus the greater of (i) $850 or

(ii) earned income (up to $5,050) +$300, or

• Unearned income > $850 + additional

standard deductions for age and blindness

(if applicable)CCH Essentials of Federal

Income Taxation

40 of 32Chapter 1

Minimize Errors

• Get appropriate forms, schedules, and

instructions

• Study the instructions and assemble data

before preparing the return

• Enter data on a tax organizer (if available)

• Review IRS identification label for correct

facts

• Supply all data

• Check all calculations

• Look for minor omissions due to carelessnessCCH Essentials of Federal

Income Taxation

41 of 35Chapter 1

Statutory Limit for Assessing

Additional Taxes

Normal Limit

Three years after the later of the return’s due

date or the filing date

Income Omissions

Six years after the later of the return’s due date

or the filing date for taxpayer’s inadvertent

omission of more than 25% of gross income

reported on return

Fraudulent Return

Tax year never closesCCH Essentials of Federal

Income Taxation

42 of 35Chapter 1

Capital Assets

Capital assets are defined as all property

except:

• Property held for resale (inventory)

• Real and depreciable property used in a

trade or business

• Accounts receivable acquired in normal

business operations

• Artistic works created by the taxpayerCCH Essentials of Federal

Income Taxation

43 of 35Chapter 1

Capital Assets

Capital assets are associated with

investments such as stocks, bonds,

mutual funds, or other investments.

Capital assets may be any other asset the

taxpayer owns not on the preceding list

Capital assets are taxed differently from

ordinary or ―earned‖ income

CCH Essentials of Federal

Income Taxation

44 of 46Chapter 1

Capital Assets

Capital assets are classified as either :

Short term if owned for 12 months or less

Gains are taxed at the taxpayers marginal tax

rate

Long term if owned for more than 12 months

Gains are taxed at

5% if taxpayer is in 10—15% bracket

15% if taxpayer is in 25% or above

Losses up to $3,000 are deductible against other

income CCH Essentials of Federal

Income Taxation

45 of 35Chapter 1

Tax Planning Principles

• Acquire working knowledge of tax laws

• Plan transactions in advance to reduce

taxes

• Maximize unrealized income

• Keep good records

CCH Essentials of Federal

Income Taxation

46 of 35Chapter 1