overview of financial management_2

DESCRIPTION

An overviewof Financial Management for Built environmentTRANSCRIPT

Financial Management

Dr. Kinshuk Saurabh

CHAPTER 1

An Overview of Financial Management

• What is financial management?

– Managerial activity which concerned with the planning and controlling of the firm’s financial resources

• What is corporate finance?

– The activities involved in managing cash flows in a business environment

What are basic finance activities?

Financial Management

Capital Budgeting

Risk Management

Corporate Governance

Financing

(Raising Capital)

What are financial resources?

• Securities, are financial papers or instruments such as Equity or Debt which are claims to income generated by firm’s real assets

What are equity or debt?

• Equity represent ownership rights of theirholders. Shareholders are owners of thecompany. It can of two types:– Equity Shares

– Preference Shares

• Debts: represent liability of the firm towardsoutsiders. Lenders are not owners of thecompany. These provide interest tax shield.– Bonds or debentures

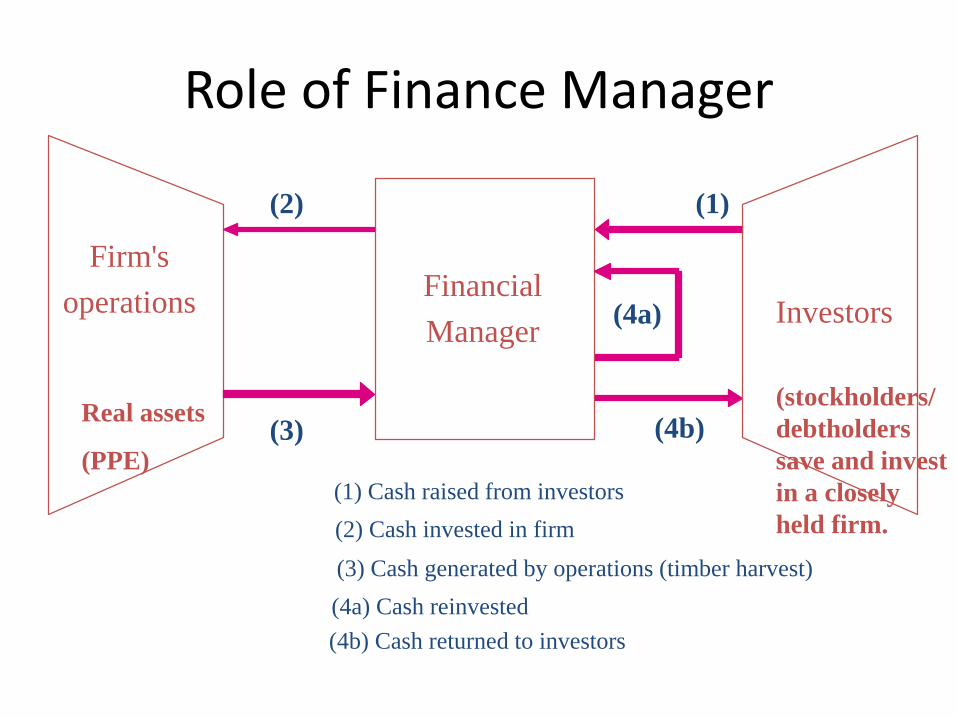

Role of Finance Manager

Financial

Manager

Firm's

operations Investors

(1) Cash raised from investors

(1)

(2) Cash invested in firm

(2)

(3) Cash generated by operations (timber harvest)

(3)

(4a) Cash reinvested

(4a)

(4b) Cash returned to investors

(4b)Real assets

(PPE)

(stockholders/

debtholders

save and invest

in a closely

held firm.

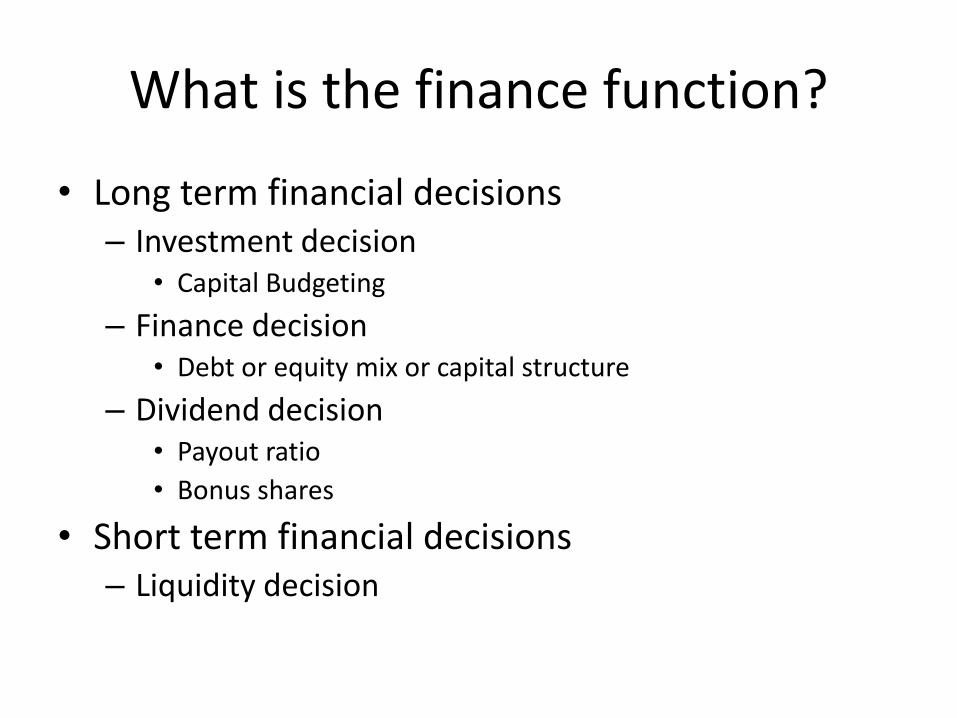

What is the finance function?

• Long term financial decisions– Investment decision

• Capital Budgeting

– Finance decision• Debt or equity mix or capital structure

– Dividend decision• Payout ratio

• Bonus shares

• Short term financial decisions– Liquidity decision

Goals: Profit vs. wealth maximization?

• When does profit maximization happen?

– Profit maximization causes efficient allocation of resources under the competitive market

• Would profit maximization or such a price system in a free market economy serve the interest of the society?

What are limitations of profit maximization?

• Definition of profit:

– Short term or long term profit? Profit before tax or profit after tax? Total profit or profit per share? Operating profit or profit accruing to shareholders

– Uncertainty effect

• Owners may prefer smaller but surer profits over larger but uncertain profits

– Ignores time value of money

What if Profit after Tax?

• Say a company has 10,000 shares outstanding, PAT of 50,000 and EPS of Rs 5. If the company sells 10,000 additional shares at Rs 50 per share and invests the proceeds at 5% after taxes then what is the new PAT and new EPS?

What if earning per share?

• Ignores timing and risks of expected benefits

• EPS is maximized when the firm makes no dividend payments

• Maximising PAT or EPS does not maximise the economic welfare of the owners. – Earnings per share are backward-looking, dependent

on accounting principles

– Does not fully consider cash flow timing

– Ignores risk

Shareholder wealth maximization

• Maximizes the net present value of a decision toshareholders. Positive NPV creates wealth forshareholders

• Accounts for the timing and risk of the expectedbenefits.

• Benefits are measured in terms of cash flows.

• Maximize stock price, not profits

• Fundamental objective—maximize the market value ofthe firm’s shares. Shareholders, as residual claimants,

have better incentives to maximize firm value.

Agency costs

• Maximize Profit?– Earnings per share are backward-looking,

dependent on accounting principles

– Does not fully consider cash flow timing

– Ignores risk

• Maximize Shareholder Wealth?– Maximize stock price, not profits

– Shareholders, as residual claimants, have better incentives to maximize firm value.

Ethics & Management Objectives

• Does value maximization justify unethical behavior?

• Enron example

• WorldCom example

• Putnam example

How agency costs can be controlled?

• Ways to limit agency problems:

– Activism by institutional investors

– Takeover threat

– Monitoring and bonding

– Compensation contracts

The financial sector of India

• Banks

• Non-banking finance companies

• Mutual Fund

• Private equity market

• Primary capital market

• Secondary capital market

Banking sector : History

• The state of banking sector in early 1990s– Cash reserve ratio as high as 15%

– Statutory liquidity ratio as high as 38.5%

– 40% of funds went to priority sector lending

– 25% of advances of public sector banks turned into non productive assets

– Very high operating costs because of improper manpower management

– Existence of uneconomic branches

– 50% of banks had negative net worth in 1993

Since then …what happened?

• CRR – 4%• SLR – 22%• Provisioning for NPAs• Tribunals set up to recover NPAs• Narsimhan committee recommended to cut down NPAs to 3% of

advances.• Securitization and reconstruction of financial assets and

enforcement of security interest (SARFAESI Act, 2002) to allows banks to recover their loans outside courts.

• Asset reconstruction company of India (ARCIL) was set up in 2003 to purchase NPAs of banks. PSB NPAs dropped to 1% in 2007-08.

• How much is the NPA now….say as of June 2014?

History of Interest rate administration

• Interest rate was GoI administered before October, 1994.

• In 2001-02 RBI permitted banks to lend at less than PLR prime lending rate. 2003-04 banks started announcing their own PLR by taking account of cost of funds and operating expenses.

• Average lending rate was 19% in 1991-92 fell to 10% in 2004-05. How much is the lending rate in 2014?

• RBI since April, 2010 introduced base rate system. Now banks set their lending rates in reference to the base rate. Base rate is the minimum rate and banks are now allowed to lend below base rate.

Non-banking finance companies

• Registered and regulated by RBI– Equipment leasing companies– Hire-purchase finance companies– Investment companies

• Not registered but regulated by RBI:– Nidhi companies– Chit funds

• Neither registered nor regulated by RBIs:– Insurance company– Merchant banks– Housing finance– Microfinance

Mutual Funds

• Till 1986 entire mutual fund activities were vested in UTI. In 1993 private sector was allowed to operate.

• The open ended schemes have perpetual existence and end only when the number of outstanding units fall below 50% of number of units. Sale and repurchase based on Net Asset Value are announced. The sale price is normally kept above NAV and repurchase price is below NPV.

• Close ended scheme exist only for an specified period after which the investment is liquidated and distributed among unit holders.

• Money market mutual funds the funds are invested in T-bills and certificate of deposits.

• Gilt funds invest in govt. securities.• Index funds try to replicate a stock market index• Funds of funds makes investments in units of other mutual funds.

Reforms in mutual funds

• SEBI (Mutual funds) regulations 1993– Mutual fund is constituted as a trust registered with SEBI.

It has a sponsor, trustees, an asset management company and a custodian. Trustees hold its assets for the benefit of unit holders. AMC manages the mutual fund. Custodian holds the securities in custody.

• SEBI (Mutual funds) regulations 1996– Trustee now has to monitor the AMC as well. The

minimum networth of AMC was raised to 100 million. Conversion of close ended scheme to open ended scheme was permitted. Weekly publication of NAV was now mandatory. Repurchase and resale price could not now move beyond +/- 7% of NAV.

Reforms in mutual funds

• Since then disclosure norms have been more tightened and a trustee can not be trustee of another mutual fund. Risk management system is must for fund management, operations, disaster recovery etc. investment policy has been liberalized. MFs can now invest abroad. MFs can now invest in listed/unlisted entities, and units of venture capital funds. In 2003-04 MFs were allowed to invest in derivative market equity oriented schemes for portfolio balancing. Each MF can now have a maximum of net derivative position of 50% of portfolio

Resource mobilization

Growth in Net Asset under Management

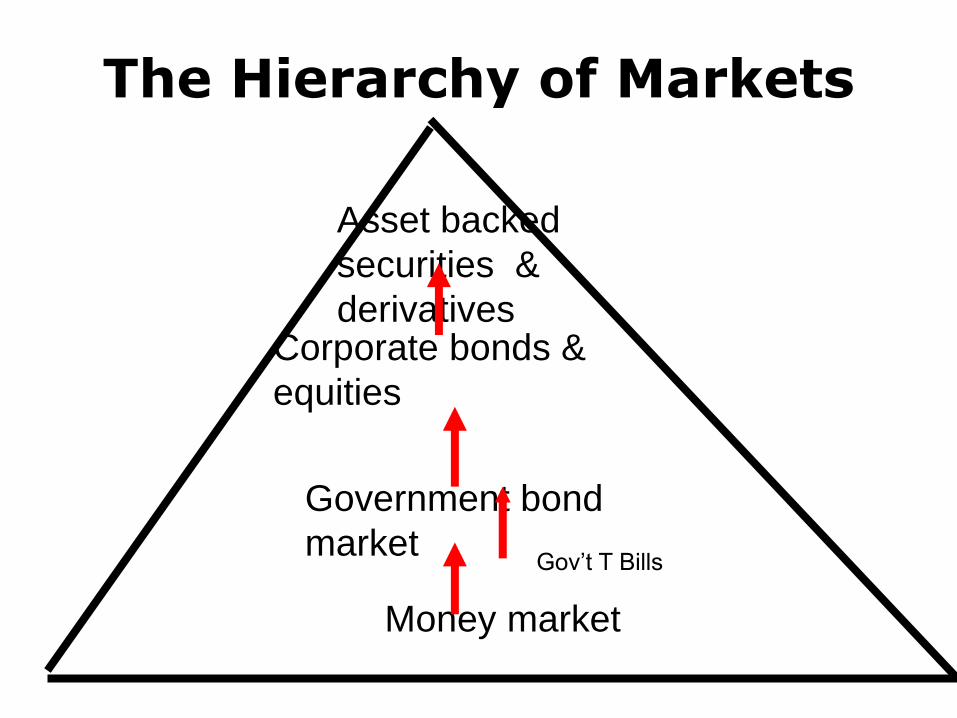

The Hierarchy of Markets

Money market

Government bond

market

Corporate bonds &

equities

Asset backed

securities &

derivatives

Gov’t T Bills

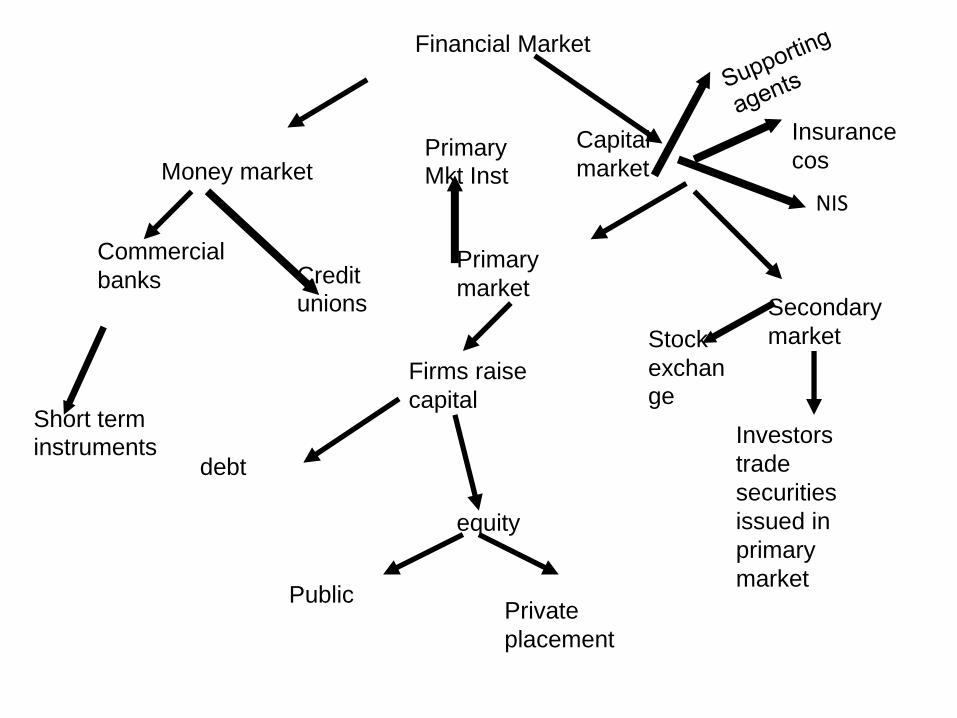

Financial Market

Money market

Capital

market

Primary

market Secondary

market

Commercial

banks

Firms raise

capital

Investors

trade

securities

issued in

primary

market

debt

equity

Public Private

placement

Short term

instruments

Primary

Mkt Inst

Stock

exchan

ge

Credit

unions

Insurance

cos

NIS

Regulation & SupervisionA few questions

• Ever wondered how the capital markets work

• Who sets the rules

• What does the stock exchange do

• What is the role of the stock broker

• How to become a registered broker

Capital Market

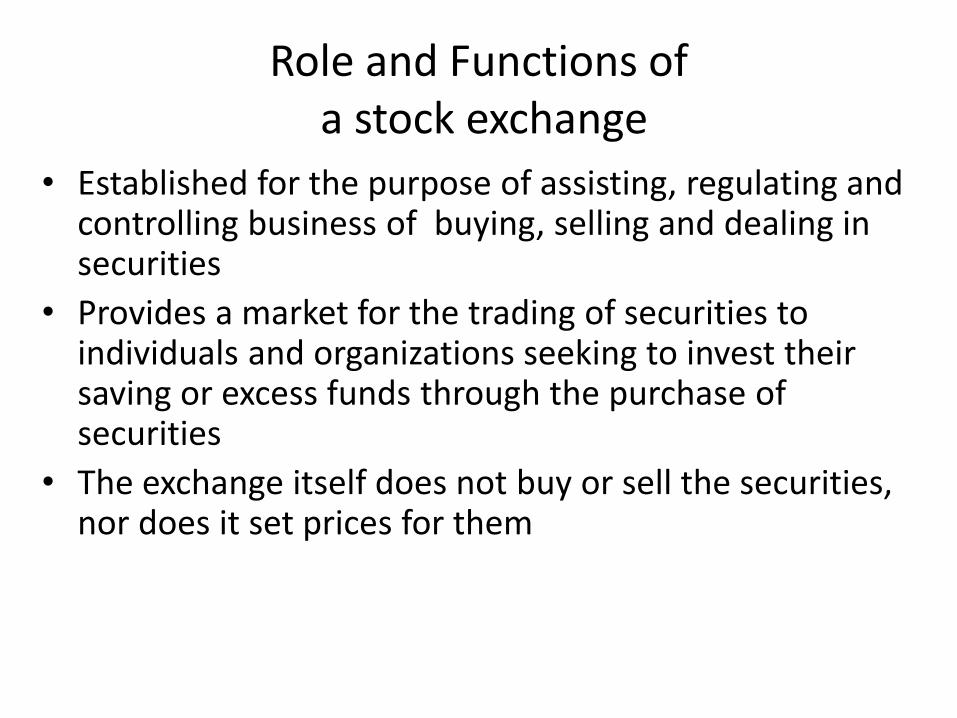

Role and Functions of a stock exchange

• Established for the purpose of assisting, regulating and controlling business of buying, selling and dealing in securities

• Provides a market for the trading of securities to individuals and organizations seeking to invest their saving or excess funds through the purchase of securities

• The exchange itself does not buy or sell the securities, nor does it set prices for them

Role and Functions of a stock exchange cont’d

• Fair– The exchange assures that no investor will have an undue

advantage over other market participants

• Efficient Market– This means that orders are executed and transactions are

settled in the fastest possible way

• Transparency– Investor make informed and intelligent decision about

the particular stock based on information– Listed companies must disclose information in timely,

complete and accurate manner to the Exchange and the public on a regular basis

Primary Equity Market

• When the firms go public for the first time, the primary market is known as the initial public offering(IPO) market.

• The subsequent offerings known as the subsequent equity offering (SEO) market.

• The offerings are made either through prospectus or through private placement. In case of the issue of securities through prospectus, the general public, at least 50 in number, subscribe to them directly.

Reform in primary market

• Capital Issues (Control) Act was abolished in 1992 to avoid rigidity in the system. SEBI was set up in 1992 to regulate the primary market.

• Since then what improvement has happened? – Disclosure norms have improved, transactions cost

has reduced and procedures have been simplified.– companies were allowed to raise funds in the inter-

national financial market under the global depository receipt (GDR)/American depository receipt (ADR) mechanism.

– Allowed all categories of companies to apply for an IPO of Indian depository receipts

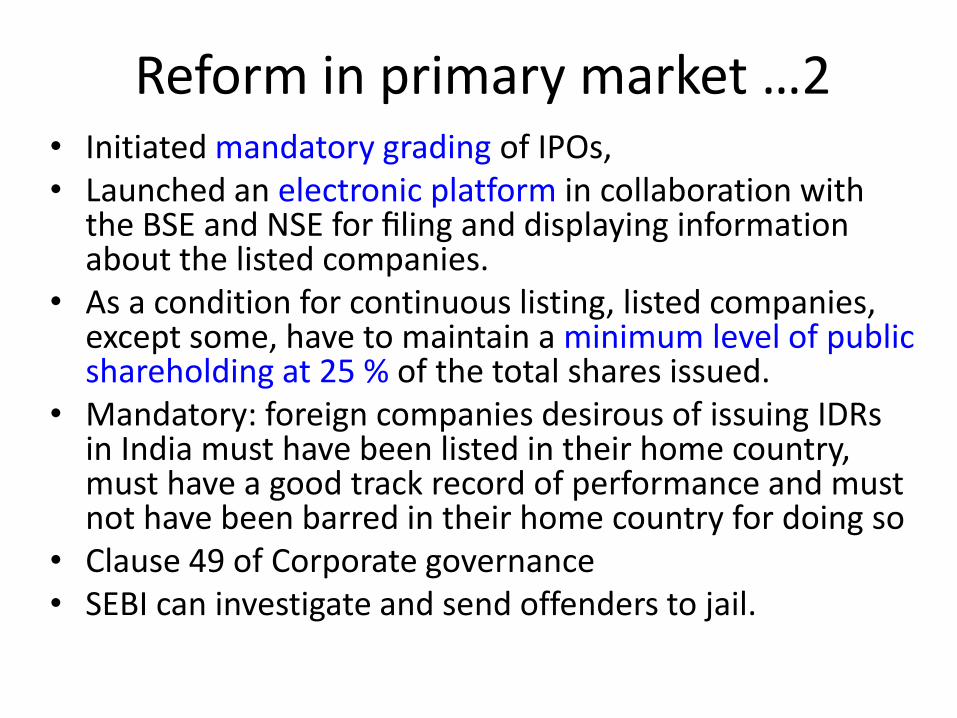

Reform in primary market …2• Initiated mandatory grading of IPOs, • Launched an electronic platform in collaboration with

the BSE and NSE for filing and displaying information about the listed companies.

• As a condition for continuous listing, listed companies, except some, have to maintain a minimum level of public shareholding at 25 % of the total shares issued.

• Mandatory: foreign companies desirous of issuing IDRs in India must have been listed in their home country, must have a good track record of performance and must not have been barred in their home country for doing so

• Clause 49 of Corporate governance• SEBI can investigate and send offenders to jail.

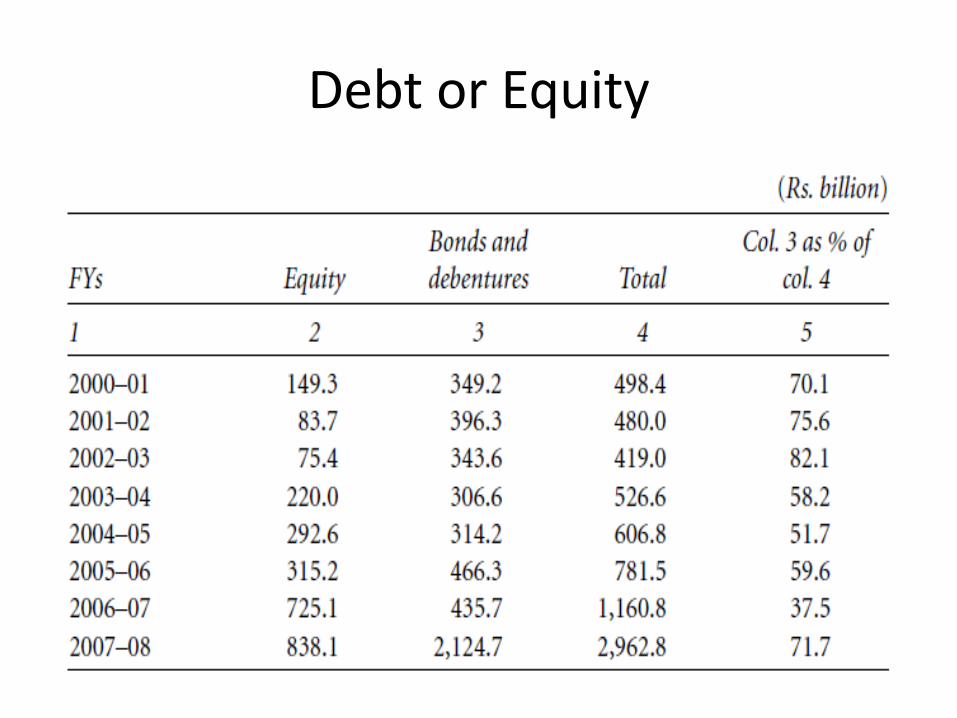

Debt or Equity

Secondary Capital Market

• 1875, the Bombay Stock Exchange (BSE) was set up, followed by some other stock exchanges in major cities.

• By the end of 1990, there were 19 stock exchanges in the country with a market capitalization of over Rs. 70.5 billion.

• But the Indian stock market remained underdeveloped till the early 1990s with the result that the pricing, delivery and settlement systems were much behind the mark.

What were problems in secondary capital market?

• The cost of transactions was high

• Stock exchanges were broker owned and managed with the result that many of the deals lacked transparency.

• The interests of general investors were hardly protected.

• Risk management mechanism was utterly lacking.

• Market closures were a recurring phenomenon.

• The size of turnover was only limited – Mutual funds were limited to the UTI and a few banks

– Foreign participants were not permitted to trade at the Indian stock exchanges.

• Debt securities never received the desired focus– Equity shares dominated the stock exchange transactions.

Reforms in Secondary Market• SEBI was set up as statutory body in 1992.

• NSE was set up as a demutualised exchange– divorce between ownership and management on the

one hand and the stock trading rights on the other.

– Hinders insiders’ trading or any broker-sponsored scam and sets a healthy secondary market. It was this reason that the government made demutualisation mandatory for all the stock exchanges after the 2001 crisis. In 2005, demutualisation of all the stock exchanges was approved and notified. Under this process, the BSE turned into a company in August 2005.

• Feb, 2000, the SEBI allowed stock exchanges to set up trading terminal in foreign countries so as to attract the nonresident Indians to the secondary market trading.

Reform in Secondary Market..2

• OCTEI and NSE introduced screen-based trading – enhances the efficiency of the market where larger

number of persons can participate, – helps participants to have a full view of the entire

market and ensures transparency. – generates trust among the participants which is vital

for the secondary market operations.

• NSE helped set up the National Securities Depository Limited (NSDL) in 1996 for keeping ownership records in a dematerialised form– transfer of ownership through electronic book entries – No more problems related with the physical delivery of

securities after trading.

• computer-based clearing and settlement system – Buyer and the seller settle the deal without delay; settlement period was reduced from a

fortnight to a week from August 1996. Now settled within 2 working days after trading day

– Trade is recorded automatically showing the quantity, price and the settlement date to participants being in different locations

– complete transparency

– Information efficiency of the market is now much improved

• Clearing Corporation receives the online information from the stock exchange about the details of the trade and ensures that trading members meet their settlement obligations.

• The clearing bank opens an account with the Clearing Corporation on behalf of the trading members and receives funds for the pay-in obligation from the trading member before the dead line. The Clearing Corporation sweeps the funds from the account and credits the designated account of the seller with the swept funds.

• Again, depository transfers the securities in electronic form from the account of the custodian as per the schedule set by the Clearing Corporation.

• What is settlement?

• Who ensures the settlement?

• What is a settlement cycle?

• How many times can one buy and sell within a settlement cycle?

• What are rolling settlements?

• How is the schedule followed?

Types of orders

• Limit order

• Market order

• Day order

• Open

• All or none

• Any part

• Good through

Limit order

• A limit order is an order to buy or sell a stock at a specific price or better. A buy limit order can only be executed at the limit price or lower, and a sell limit order can only be executed at the limit price or higher.

• A limit order is not guaranteed to execute. A limit order can only be filled if the stock’s market price reaches the limit price.

• Limit orders help ensure that investors do not pay more than a pre-determined price for a stock.

• Note that if the price of the stock never reaches your limit price, your trade won't be executed.

Limit order

• For example, you want to buy ABC Inc. at $50. The stock is currently trading at $51, so you set a limit order to buy at $50. The price may go up or it may go down, but you know that as soon the stock trades at $50, your order will be triggered and you'll buy at your predetermined price.

• Once you buy ABC at $50, let's say you decide you want to sell at $53. Again, you place your limit order and wait. Once ABC trades at $53, your order becomes active and will sell at your target price of $53.

• Limit orders are especially useful in volatile environments.

Market order

• A market order is an order to buy or sell a stock at the best available price. Generally, this type of order will be executed immediately. However, the price at which a market order will be executed is not guaranteed.

– buy/sell order to be executed at best price

-- get lowest price for buy order

-- get highest price for sell order

– market orders given priority in trading

– no guarantee of execution price

-- price could rise/fall from time order is placed to time it is executed

Day order

• A day order is an order that is good for that day only. If it is not filled it will be canceled, and it will not be filled if the limit or stop order price was not met during the trading session

Short selling

• Sale of borrowed stock

• Short sellers profit from belief that stock price is too high will fall soon. If prices rise and then face unlimited losses.

• how?• borrow stock through broker

• sell stock

• buy and return later

Short selling could further destabilize falling prices

Circuit breakers

• An index based market-wide circuit breaker system applies at three stages of the index movement either way at 10%, 15% and 20%.

• The breakers are triggered by movement of either S&P CNX Nifty or Sensex, whichever is breached earlier

Clearing and Settlement

• Stock Markets follow a system of settling trades on T+2 basis, which means transactions done on Monday, are to be settled by Wednesday by way of giving securities or funds.

• Providing of securities or funds to Exchange / Clearing Corporation is called ‘Pay-In’.

• Receiving securities or funds from Exchange / Clearing corporation is called ‘Pay-Out’.

Desirable Characteristics

of a stock market

• Liquidity– Ability to sell an asset quickly at a fairly known price Low

transactions costs

• Market efficiency• Availability of information

• Prices react quickly to new information

• Small Volatility• Price fluctuations

• Narrow price spread

• Disclosure

• Protection to minority Shareholder

• Corporate Governance

• The BSE sensitive Index(Sensex) is a value weighted

index. Composed of 30stocks with the base April

1979=100.

• These companies account for around one-fifth of the market capitalization of the BSE

• The index has increased by over13 times from June 1990

to today. Using information from April 1979 onwards the

long run rate of return on the BSE Sensex can be

estimated to be 0.52%per week (continuously

compounded) with a standard deviation of 3.67%.this

translates to 27%per annum, which translate to roughly

18% pa after compensating for inflation.16 February 2016 IIPM

BOMBAY STOCK EXCHANGE

Turnover and Market Cap at BSE and NSE (Cash Segment)

Stock Market Indices and the Price/Earning Ratio

What is the Debt Market?

• The Debt Market is the market where fixed income securities of various types and features are issued and traded.

• Fixed income securities issued by Central and State Governments, Municipal Corporations, Govt. bodies and commercial entities like Financial Institutions, Banks, Public Sector Units, Public Ltd. companies and also structured finance instruments.

Main features of G-Secs?

• All G-Secs in India currently have a face value of Rs.100/- and are issued by the RBI on behalf of the GoI. All G-Secs are normally coupon (Interest rate) bearing and have semi-annual coupon or interest payments with a tenor of between 5 to 30 years.

• Issued by the Government for raising a public loan or as notified in the official Gazette.

• No default risk as the securities carry sovereign guarantee.

• Ample liquidity as the investor can sell the security in the secondary market

• e.g: a 11.50% GOI 2005 security will carry a coupon rate(Interest Rate) of 11.50% p.a. on a face value per unit of Rs.100/- payable semi-annually and maturing in the year 2005

Main features of Treasury Bills• Treasury Bills are for short-term instruments

issued by the RBI for the Govt. for financing the temporary funding requirements and are issued for maturities of 91 Days and 364 Days. T-Bills have a face value of Rs.100 but have no coupon (no interest payment). T-Bills are instead issued at a discount to the face value (say @ Rs.95) and redeemed at par (Rs.100). The difference of Rs. 5 (100 - 95) represents the return to the investor obtained at the end of the maturity period.

Important qualities of treasury bills • The high liquidity

• Absence of risk of default

• Ready availability

• Assured yield

• Low transaction cost

• Eligibility for inclusion in statutory liquidityratio (SLR)

• Negligible capital depreciation

TREASURY BILLS MARKET• Treasury bills are available for a minimum

amount of Rs.25K and in multiples of Rs. 25K. • T-bills auctions are held on the Negotiated

Dealing System (NDS) and the members electronically submit their bids on the system

• 91- Day, 182- day, 364- day, and 14- day TBs• 91 day T-bills, auctioned every week on

Wednesdays, are not self-liquidating in the way genuine trade bills are, although the degree of their liquidity is greater than that of trade bills.

• According to their liquidity, the descending order would be cash, call loans, treasury bills and commercial bills.

• 182 day T-bills sold in the market fortnightly by the RBI. It is quite liquid because of the availability of refinance facility against it and the existence of the secondary market in it.

• 364 day T-bills sold in the market fortnightly by the RBI. The RBI dose not purchase and rediscount this bill

• Two types of 14-day TBs: known as intermediate treasury bill (ITB)

• It can be repaid/renewed at par on the expiration of 14days from the date of issue.

• The disadvantage of 14-day ITB is that it is not tradableor transferable.

Type of T-bills Day of Auction Day of Payment

91-day Wednesday Following Friday

182-day Wednesday of non-

reporting week

Following Friday

364-day Wednesday of

reporting week

Following Friday

COMMERCIAL BILLS MARKET• Funds for working capital required by industry

are mainly provided by banks through cash credits, overdrafts, and purchase/ discontinuing of commercial bills

BILL OF EXCHANGE

• The financial instrument which is traded in the bill market of exchange. It is used for financing a transaction in goods that takes some time to complete.

• It shows the liquidity to make the payment on afixed date when goods are bought on credit.

• Accordingly to the Indian Negotiable InstrumentsAct, 1881, it is a written instrument containing asunconditional order, signed by the maker,directing a certain person to pay a certain sum ofmoney only to, or to the order of, a certainperson, or to the bearer of the instrument.

• INLAND BILLS– Be drawn or made in India, and must be payable in

India– Be drawn upon any person resident in India

• FOREIGN BILLS– Drawn outside India and may be payable in and by a

party outside India, or may be payable in India ordrawn on a party resident in India

– Drawn in India and made payable outside India.– A related classification of bills is export bills and

import bills

What purpose bill of exchange used?

• Commercial bills may be used for financingthe movement and storage of goods betweencountries, before export (pre-export credit),and also within the country.

• In India the use of bill of exchange appears tobe in vogue for financing agriculturaloperations, cottage and small scale industries,and other commercial and trade transactions.

ACCOMMODATION AND SUPPLY BILLS• Apart from the genuine bill of exchange, i.e. bills

which evidence sale and /or dispatch of goods,there are other bills which are known to themoney market. They are accommodation billsand supply bills.

• As “accommodation bill” is defined as one inwhich a person, called as accommodation party,puts his name (accept it) to accommodateanother person without receiving andconsideration. Such bill is sometimes called, a kiteor wind bill.

BANKERS ACCEPTANCE

• A banker's acceptance is a short-term investmentplan created by a company or firm with aguarantee from a bank.

• It is a guarantee from the bank that a buyerwill pay the seller at a future date. A goodcredit rating is required by the company orfirm drawing the bill.

• This is especially useful when the creditworthiness of a foreign trade partner isunknown.

BANKERS ACCEPTANCE..2

• The terms for these instruments are usually 90 days,but this period can vary between 30 and 180 days.Companies use the acceptance as a time draft forfinancing imports, exports and trade.

• In India, there are neither specialised acceptanceagencies for providing this service on a commissionbasis nor is it provided to any significant extent bycommercial banks.

• Under the bill market schemes introduced by RBI in1952, banks are required to select the borrowers aftercareful examination of their means, respectability, anddealings for conversion of their advances in to bills.

• Banks maintain opinion registers on differentdrawers of bills and they get reports from time totime on these drawers of bills.

• BA acts as a negotiable time draft for financingimports, exports or other transactions in goods.

• Acceptances are traded at discounts from facevalue in the secondary market.

• BA’s are guaranteed by a bank to make payment.

DISCOUNT MARKET• DISCOUNTING SERVICE

• The central banks help banks in their liquiditymanagement by providing them discountingand refinancing facilities.

• The RBI are in abundance liquidity (funds) tobanks on occasions when liquidity shortagesthreaten economic stability.

• The central bank performs his functionthrough its discount window or discountingmechanism.

• Bank borrow funds temporarily at thediscount window of the central bank.

• They are permitted to borrow or are given theprivilege of doing so from the central bankagainst certain types of eligible paper, such asthe commercial bill or treasury bill, which thecentral bank stands ready to discount for thepurpose of financial accommodation to banks.

DISCOUNT AND FINANCE HOUSE OF INDIA

• It should be the sole depository of the surplus liquid funds of the banking system as well as the non-banking financial institutions.

• It should use surplus funds to even out theimbalance in liquidity in the banking systemsubject to the RBI guidelines.

• It should create ready market for commercialbills, treasury bills, and government guaranteedsecurities by being ready to purchase from andsell to the banking system such securities.

COMMERCIAL PAPER

• Commercial Paper (CP) is an unsecuredmoney market instrument issued in the formof a promissory note.

• It was introduced in India in 1990 with a viewto enabling highly rated corporate borrowers/to diversify their sources of short-termborrowings and to provide an additionalinstrument to investors.

• Only company with high credit rating issues CP’s

• Subsequently, primary dealers and satellitedealers were also permitted to issue CP to enablethem to meet their short-term fundingrequirements for their operations.

• Primary dealers (PDs) and the All-India FinancialInstitutions (FIs) are eligible to issue CP.

• CP is very safe investment because the financialsituation of a company can easily be predictedover a few months.

• CP can be issued for maturities between a minimum of 15days and a maximum up to one year from the date of issue.

• The aggregate amount of CP from an issuer shall be withinthe limit as approved by its Board of Directors or thequantum indicated by the Credit Rating Agency for thespecified rating, whichever is lower.

• As regards FIs, they can issue CP within the overall umbrellalimit fixed by the RBI i.e., issue of CP together with otherinstruments viz., term money borrowings, term deposits,certificates of deposit and inter-corporate deposits shouldnot exceed 100 per cent of its net owned funds, as per thelatest audited balance sheet.

• Only a scheduled bank can act as an IPA for issuance of CP.• Individuals, banking companies, other corporate bodies registered

or incorporated in India and unincorporated bodies, Non-ResidentIndians (NRIs) and Foreign Institutional Investors (FIIs) etc. caninvest in CPs.

• Amount invested by single investor should not be less than Rs.5lakh (face value).

• However, investment by FIIs would be within the limits set for theirinvestments by Securities and Exchange Board of India

• CP will be issued at a discount to face value as may be determinedby the issuer.

• The investor in CP is required to pay only the discounted value ofthe CP by means of a crossed account payee cheque to the accountof the issuer through IPA.

CERTIFICATES OF DEPOSIT

• With a view to further widening the range ofmoney market instruments and give investorsgreater flexibility in deployment of their short-term surplus funds, Certificates of Deposit (CDs)were introduced in India in 1989.

• Certificate of Deposit (CD) is a negotiable moneymarket instrument and issued in dematerialisedform or as a Usance Promissory Note againstfunds deposited at a bank or other eligiblefinancial institution for a specified time period

CDs can be issued by

• Scheduled commercial banks excludingRegional Rural Banks (RRBs) and Local AreaBanks (LABs)

• Select all-India Financial Institutions that havebeen permitted by RBI to raise short-termresources within the umbrella limit fixed byRBI.

• Banks have the freedom to issue CDs depending ontheir requirements.

• An FI may issue CDs within the overall umbrella limitfixed by RBI, i.e., issue of CD together with otherinstruments, viz., term money, term deposits,commercial papers and inter-corporate deposits shouldnot exceed 100 per cent of its net owned funds, as perthe latest audited balance sheet.

• Minimum amount of a CD should be Rs.1 lakh, i.e., the minimum deposit that could be accepted from a single subscriber should not be less than Rs.1 lakh and in the multiples of Rs. 1 lakh thereafter.

INVESTORS

CDs can be issued to individuals, corporations,companies, trusts, funds, associations, etc.Non- Resident Indians (NRIs) may alsosubscribe to CDs, but only on non-repatriablebasis, which should be clearly stated on theCertificate. Such CDs cannot be endorsed toanother NRI in the secondary market.

MATURITY

• The maturity period of CDs issued by banksshould be not less than 7 days and not morethan one year.

• The FIs can issue CDs for a period not less than1 year and not exceeding 3 years from thedate of issue.

Other aspect of CD

• CDs may be issued at a discount on face value.• Banks / FIs are also allowed to issue CDs on

floating rate basis provided the methodology ofcompiling the floating rate is objective,transparent and market-based.

• Banks have to maintain appropriate reserverequirements, i.e., cash reserve ratio (CRR) andstatutory liquidity ratio (SLR), on the issue priceof the CDs.

• CDs in physical form are freely transferable byendorsement and delivery.

Structure of Indian Money Market?

ORGANISED STRUCTURE1. Reserve bank of India.2. DFHI (Discount And Finance House of India).3. Commercial banks

i. Public sector banksSBI with 7 subsidiariesCooperative banks20 nationalised banks

ii. Private banksIndian BanksForeign banks

4. Development bankIDBI, IFCI, ICICI, NABARD, LIC, GIC, UTI etc.

II. UNORGANISED SECTOR1. Indigenous banks2 Money lenders3. Chits4. Nidhis

III. CO-OPERATIVE SECTOR1. State cooperative

i. central cooperative banksPrimary Agri credit societiesPrimary urban banks

2. State Land development bankscentral land development banksPrimary land development banks

What are the segments in the secondary debt market?

• Wholesale Debt Market - where the investors are mostly Banks, Financial Institutions, the RBI, Primary Dealers, Insurance companies, MFs, Cash rich corporates and FIIs, Co-operative Banks, Investment Institutions

• Retail Debt Market involving participation by individual investors, provident funds, pension funds, private trusts, NBFCs and other legal entities in addition to the wholesale investor classes.

What is the structure of the Wholesale Debt Market?

• A negotiated deal market where most of the deals take place through telephones and are reported to the Exchange for confirmation.

• FIIs can now invest 100% of their funds (earlier the limit was 30%). Since 98-99, FIIs can invest in T-bills.

What is the issuance process of G-secs?

• Issued by RBI in either a yield-based (participants bidfor the coupon payable) or price based (participantsbid a price for a bond with a fixed coupon) auctionbasis.

• The Auction can be either a Multiple price (participantsget allotments at their quoted prices/yields) Auction ora Uniform price (all participants get allotments at thesame price).

• RBI has recently announced a non-competitive biddingfacility for retail investors in G-Secs through which non-competitive bids will be allowed up to 5 percent of thenotified amount in the specified auctions of datedsecurities.

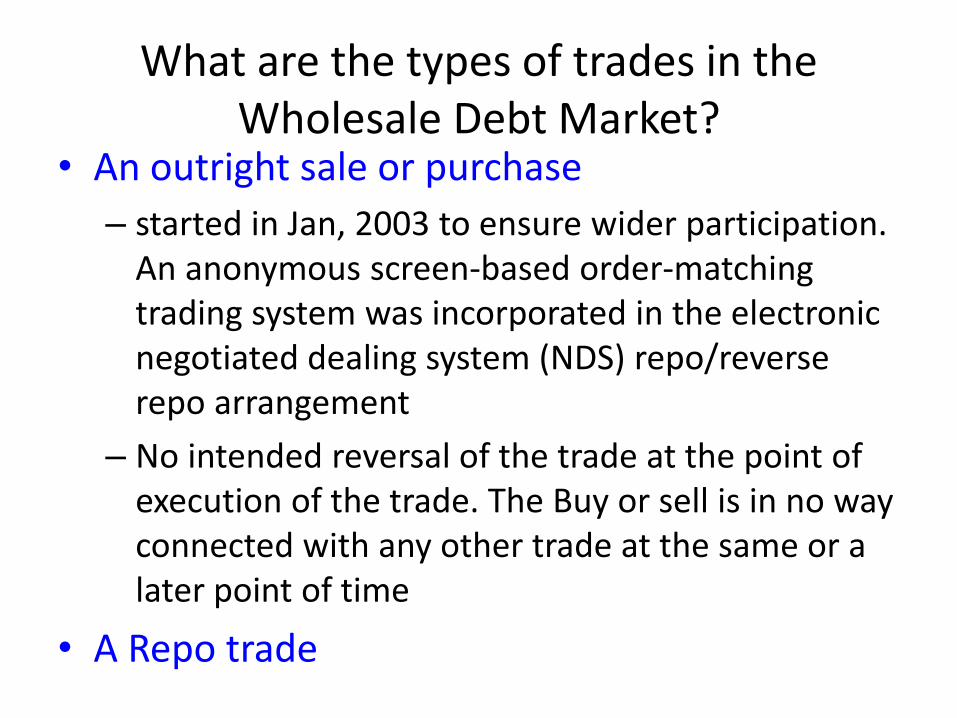

What are the types of trades in the Wholesale Debt Market?

• An outright sale or purchase

– started in Jan, 2003 to ensure wider participation. An anonymous screen-based order-matching trading system was incorporated in the electronic negotiated dealing system (NDS) repo/reverse repo arrangement

– No intended reversal of the trade at the point of execution of the trade. The Buy or sell is in no way connected with any other trade at the same or a later point of time

• A Repo trade

What is a Repo trade and how is it different from a normal buy or sell transaction?

• where the trade is intended to be reversed at a later point of time at a rate which will include the interest component for the period between the two opposite legs of the transactions.

• one party sells securities to other with an agreement to purchase them back at a later date. The trade is called a Repo transaction from the point of view of the seller and it is called a Reverse Repo transaction from point of view of the buyer.

• Reverse repo meant injection of liquidity in the system. Repo is undertaken by RBI, although inter-bank repo is found in a highly regulated way.

What is the Money Market?

• The Money Market is basically concerned with the issue and trading of securities with short term maturities or quasi-money instruments.

• The Instruments traded in the money-market are Treasury Bills, Certificates of Deposits (CDs), Commercial Paper (CPs), Bills of exchange and other such instruments of short-term maturities (i.e. not exceeding 1 year with regard to the original maturity)

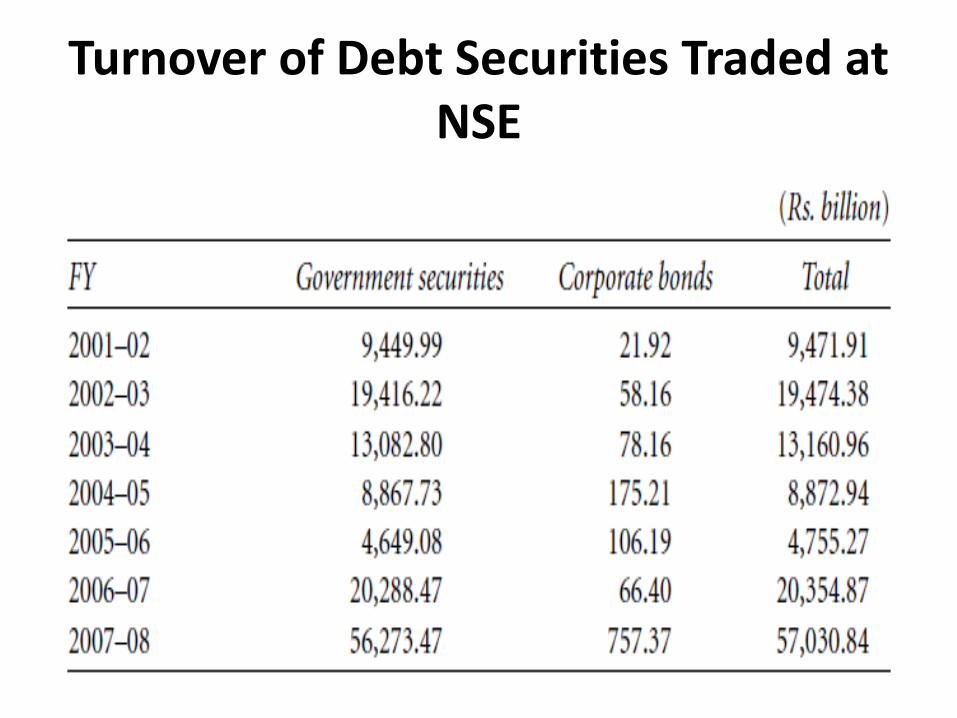

Turnover of Debt Securities Traded at NSE

• Secondary market for the corporate bonds was shrinking in terms of depth and width. Moreover, the trade in highly rated bonds dwindled in favour of greater liquidity oriented bonds.

What are the various kinds of debt instruments available in the Corporate Debt Market?

• Non-Convertible Debentures

• Partly-Convertible Debentures/Fully-Convertible Debentures (convertible in to Equity Shares)

• Secured Premium Notes

• Debentures with Warrants

• Deep Discount Bond

• PSU Bonds/Tax-Free Bonds

How is the trading, clearing and settlement in Corporate Debt carried out at BSE?

• BOLT order-matching system based on price-time priority. The trades in the 'F Group' at BSE are to be settled on a rolling settlement basis with a T+2 Cycle with effect from 1st April 2003. Trading continues from Monday to Friday during the week.

What are the securities/instruments traded in the Retail Debt Segment

• Central Government Securities commenced on January 16, 2003 through the BOLT System of the Exchange

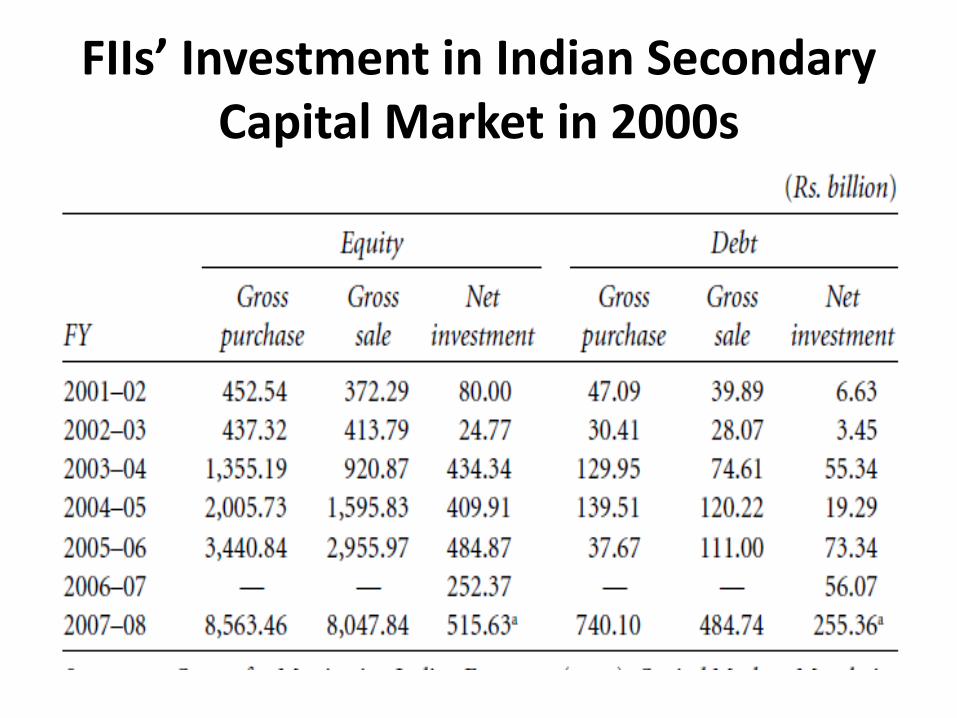

FIIs’ Investment in Indian Secondary Capital Market in 2000s

Return and Risk in BSE Sensex and NSE Nifty

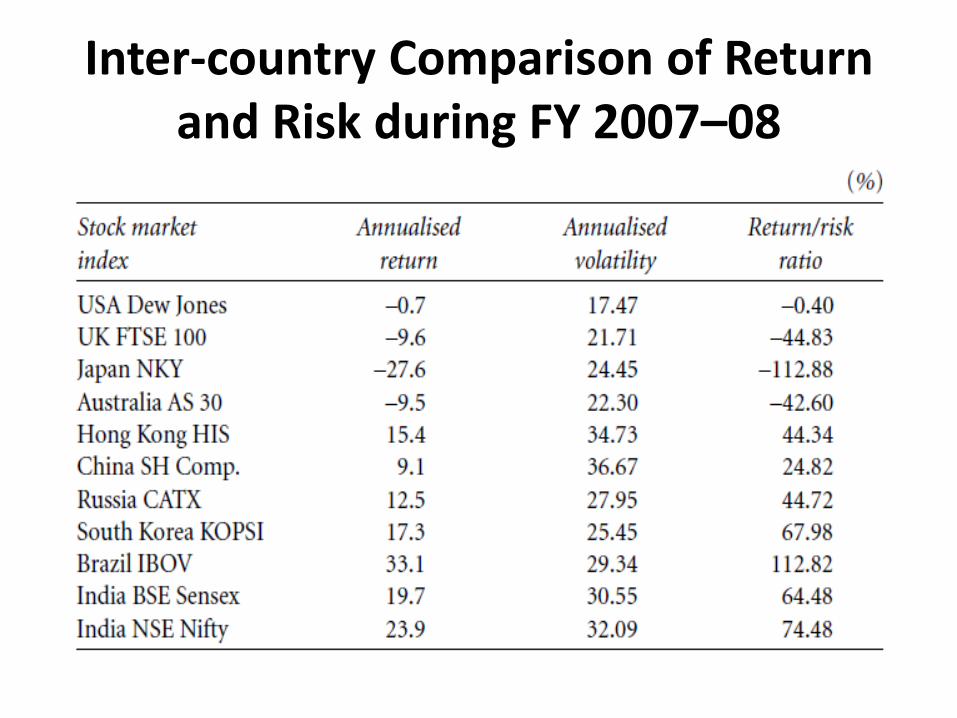

Inter-country Comparison of Return and Risk during FY 2007–08

Corporate Debt Market

• No transparency• Little information• Lack of legal enforcement mechanism• Lack of market making to provide liquidity• An active secondary market is needed for reaching a wider

investor base, reducing borrowing cost, and lengthening maturity

• Lack of uniform stamp duty structure– Stamp duty on debenture is 0.375%– Promissory notes 0.05%

• Why do banks prefer to lend to firms but do not subscribe to their debt issuances?

What is money market?

• A segment of the financial market in which financial instruments with high liquidity and very short maturities (less than one year) are traded.

• It doesn’t actually deal in cash or money but deals with substitute of cash like trade bills, promissory notes & govt papers which can converted into cash without any loss at low transaction cost

• Money market transaction do not happen on stock exchanges but take place through informal mechanisms like over telephone without the help of brokers

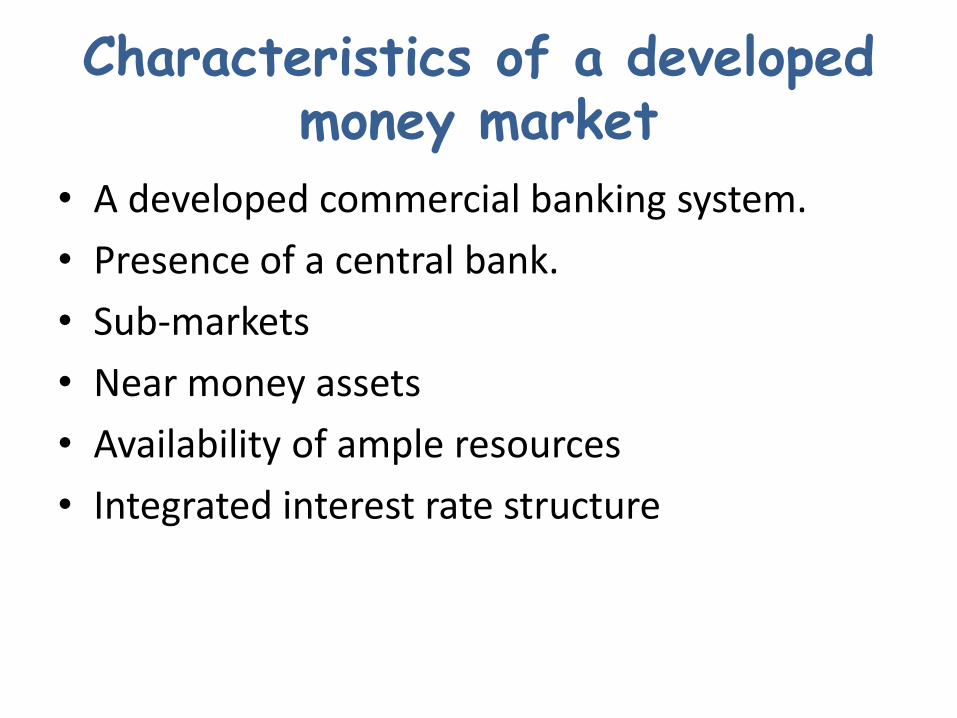

Characteristics of a developed money market

• A developed commercial banking system.

• Presence of a central bank.

• Sub-markets

• Near money assets

• Availability of ample resources

• Integrated interest rate structure

Functions of money market• Economic development – Money market assures supply of funds;

financing is done through discounting of the trade bills, commercial banks, acceptance houses and brokers.

• Profitable Investment – the excess reserves of commercial banks invested in near money assets.

• Borrowings by the Government – short term funds at very low interest. It is non-inflationary source of finance to government.

• Importance For Central Bank – the central bank implements the monetary policy successfully by influencing and regulating liquidity in the economy through its interventions.

• Mobilization of Funds – helps in transferring funds from one sector to another.

• Savings And Investment – encouraging savings and investment by promoting liquidity and safety of financial assets.

• Self-sufficiency Of Commercial Banks – commercial banks can meet their financial requirements by recalling some of their loans.

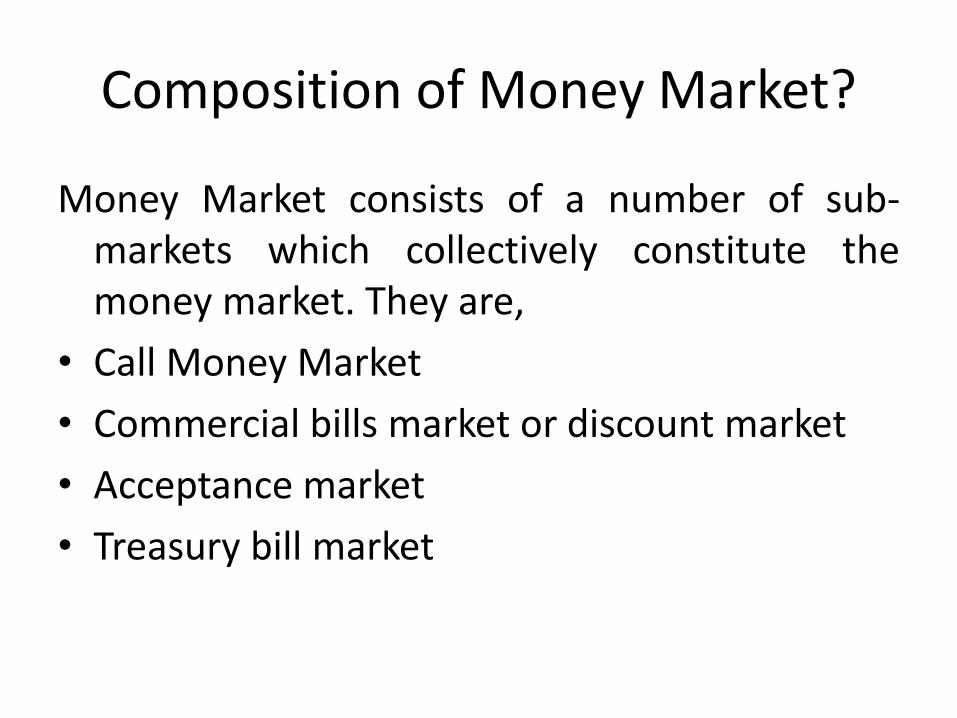

Composition of Money Market?

Money Market consists of a number of sub-markets which collectively constitute themoney market. They are,

• Call Money Market

• Commercial bills market or discount market

• Acceptance market

• Treasury bill market

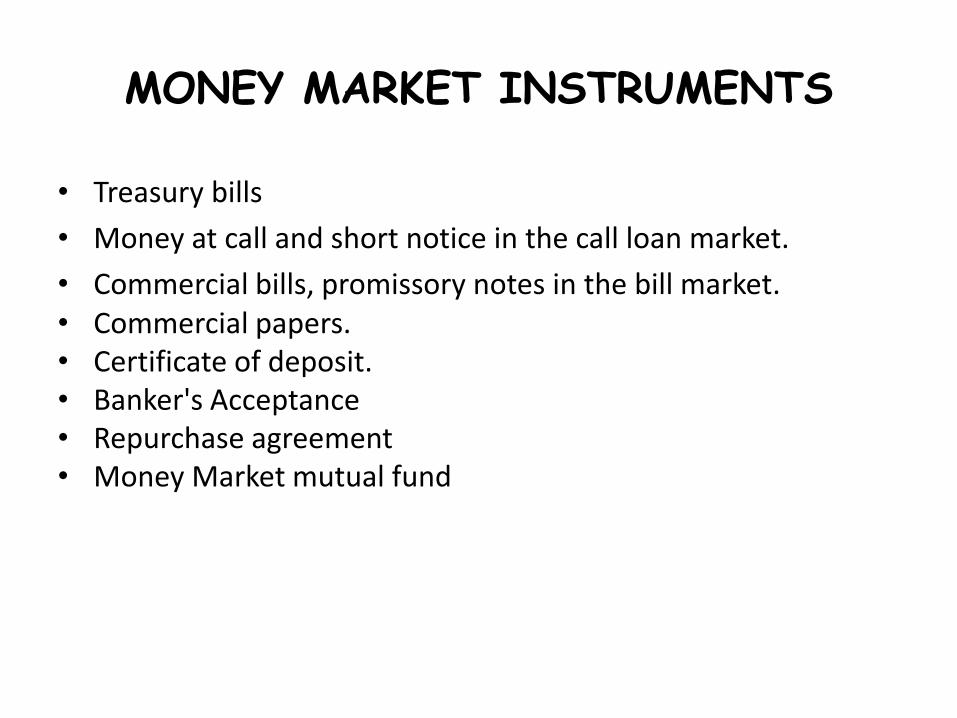

MONEY MARKET INSTRUMENTS

• Treasury bills

• Money at call and short notice in the call loan market.

• Commercial bills, promissory notes in the bill market.• Commercial papers.• Certificate of deposit.• Banker's Acceptance• Repurchase agreement• Money Market mutual fund

MONEY MARKET AT CALL AND SHORT NOTICE

• Money at call is a loan that is repayable on demand, and money at short notice is repayable within 14 days of serving a notice.

• Participants are banks & all other Indian Financial Institutions as permitted by RBI.

• Banks borrow call funds for a variety of reasons to maintain their CRR, to meet their heavy payments, to adjust their maturity mismatch etc.

CALL MONEY MARKET• Call money market is that part of the national money

market where the day to day surplus funds, mostly ofbanks are traded in.

• They are highly liquid, their liquidity being exceedonly by cash.

• The loans made in this market are of the short termnature.

• Banks borrow from other banks in order to meet a sudden demand for funds, large payments, large remittances, and to maintain cash or liquidity with the RBI. Thus, to the extent that call money is used in India for the purpose of adjustment of reserves.

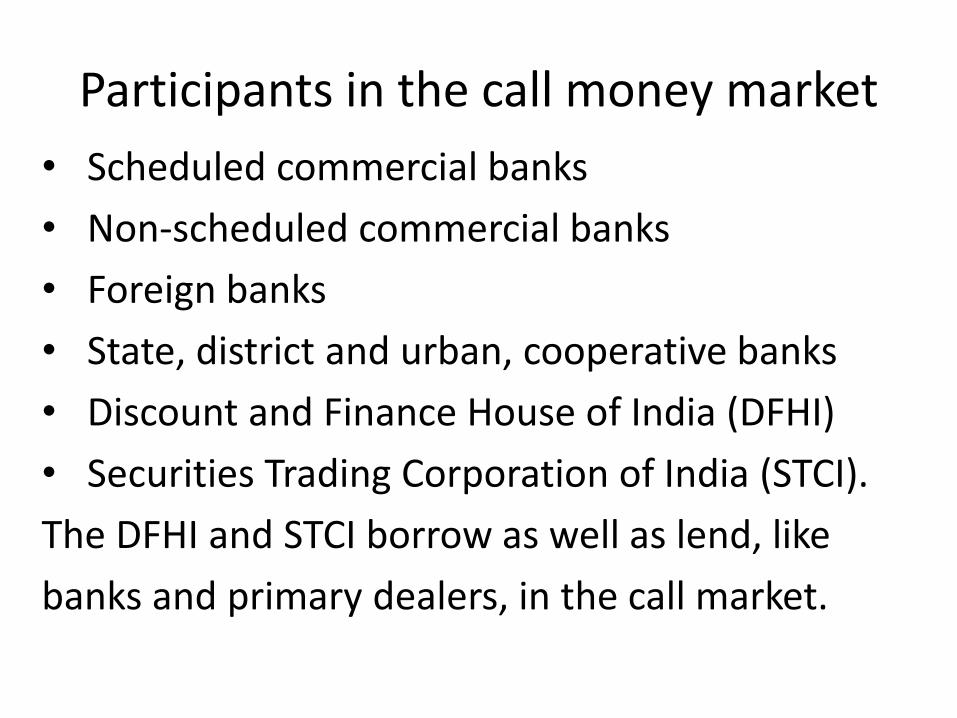

Participants in the call money market

• Scheduled commercial banks

• Non-scheduled commercial banks

• Foreign banks

• State, district and urban, cooperative banks

• Discount and Finance House of India (DFHI)

• Securities Trading Corporation of India (STCI).

The DFHI and STCI borrow as well as lend, like

banks and primary dealers, in the call market.

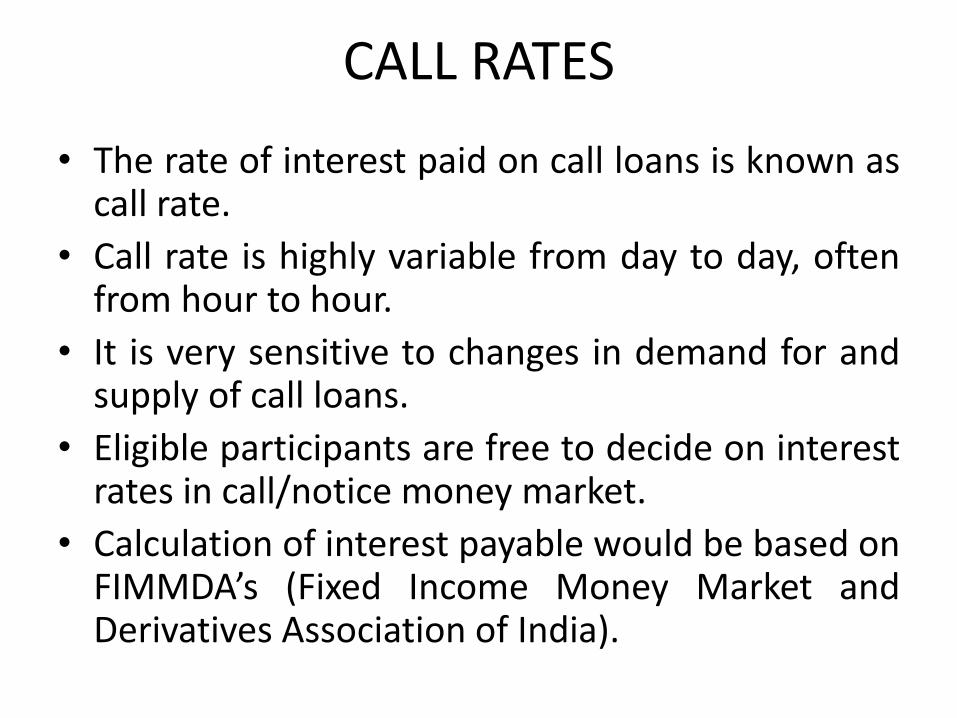

CALL RATES

• The rate of interest paid on call loans is known ascall rate.

• Call rate is highly variable from day to day, oftenfrom hour to hour.

• It is very sensitive to changes in demand for andsupply of call loans.

• Eligible participants are free to decide on interestrates in call/notice money market.

• Calculation of interest payable would be based onFIMMDA’s (Fixed Income Money Market andDerivatives Association of India).

CALL RATE IN INDIA• CALL RATE IN INDIA had reached as high a level as 30% in

December 1973.• It is an alarming level for any short-term rate of interest to

reach, and as bank defaulted in a major way in respect ofcash and liquidity requirements at that time due to theprohibitively high cost of call money, it became necessary toregulate call rates within reasonable limits.

• Indian Banks’ Association (IBA) in 1973 fixed a ceiling of 15%on the level of call rate.

• The IBA lowered this ceiling of 15% to 12.5% in March 1976,10 % in June 1977, and 8.6% in March 1978, and 10.0% inApril 1980.

• And current call rate in India is 8%.• There are now two call rates in India: one, the interbank call

rate, and the other, the lending rate of DFHI.

CERTIFICATES OF DEPOSITS

• A CD is a time deposit, financial product commonly offered to consumers by banks.

• CDs are negotiable instrument.

• Financial Institutions are allowed to issue CDs for a period between 1 year and up to 3 years.

• normally give a higher return than Bank term deposit, and are rated by approved rating agencies.

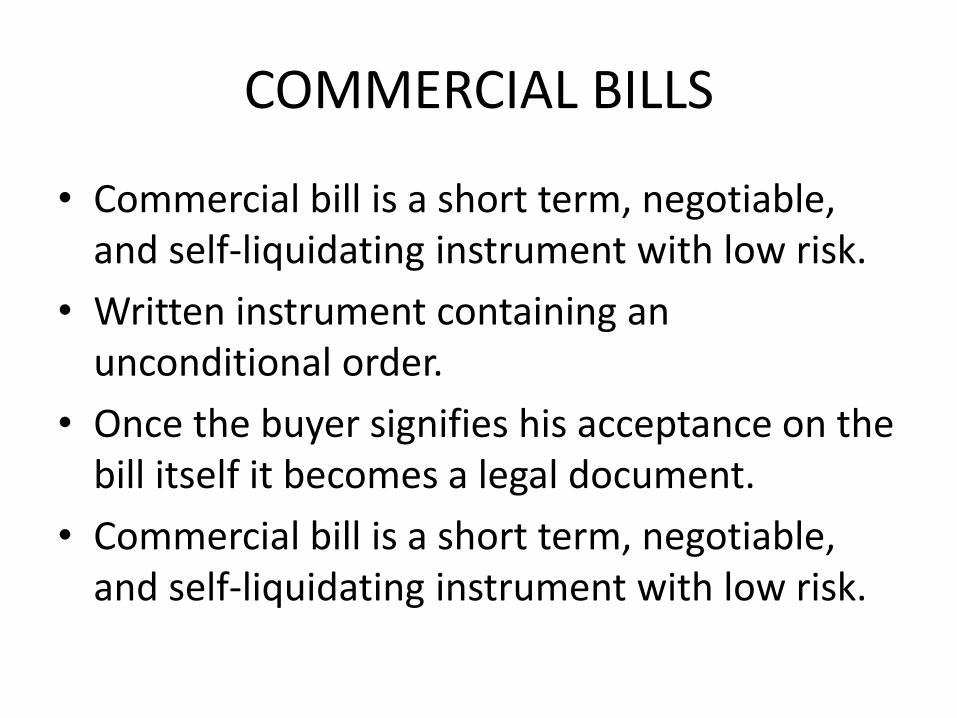

COMMERCIAL BILLS

• Commercial bill is a short term, negotiable, and self-liquidating instrument with low risk.

• Written instrument containing an unconditional order.

• Once the buyer signifies his acceptance on the bill itself it becomes a legal document.

• Commercial bill is a short term, negotiable, and self-liquidating instrument with low risk.

COMMERCIAL PAPER

• Commercial Paper is a money-market security issued (sold) by large banks and corporations to get money to meet short term debt obligations .

• Commercial paper is usually sold at a discount from face value.

• Interest rates fluctuate with market conditions, but are typically lower than banks‘ rates.