outline - afrinvest

TRANSCRIPT

Afrinvest West Africa Page 2

Outline

Section 1

Section 2

•

•

•

•

•

Section 4 Nigerian Oil Palm Sector •

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Section 6

• Contact

• Disclaimer

Section 7

Section 3

• Global Perspective on the Rubber Industry… Production of Natural Rubber Leads

• Market Share and Structure of the Rubber Industry… Thailand Leads in Global Production

• Growth Drivers of Rubber Production… Developments in the Asia Pacific Region a Key Influence

• The Nigerian Rubber Industry… A Brief Introduction.

Section 5

The Nigerian Insurance Sector Report

Page 4 The Nigerian Oil Palm Sector Report

Afrinvest West Africa Page 5

The Nigerian Insurance Sector Report

Section Two

Investment Thesis

Afrinvest West Africa Page 7

The Nigerian Insurance Sector Report

Afrinvest West Africa Page 9

Chart 1: Top Five (5) Oil Palm Producing Countries – Million MT

Source: United States Department of Agriculture (USDA), Afrinvest Research

Source: United States Department of Agriculture (USDA), Afrinvest Research

Chart 2: Global Production Vs Consumption Trends – (1964-2018) – Million MT

Chart 3: Global Consumption of the Edible Oils (2016- 2018) – Million MT

Source: United States Department of Agriculture (USDA), Afrinvest Research

Source: Palm Oil Analytics (POA), Afrinvest Research

Chart 4: : Top 10 Importers of Oil Palm (2016) – %

Page 10 The Nigerian Oil Palm Sector Report

Chart 5 Historical CPO Prices (2013-2019) – US$

Source: United States Department of Agriculture (USDA), Afrinvest Research

Chart 6: Global Drivers of Oil Palm Demand

Source: Afrinvest Research

The Nigerian Insurance Sector Report

Page 12 The Nigerian Oil Palm Sector Report

Chart 7: Palm Oil Production vs Consumption in Nigeria (1975-2017) – Million MT

Source: United States Department of Agriculture (USDA), Afrinvest Research

Chart 8: Oil Palm Yields Across Top 5 Producers (1983 - 2017)

Source: United States Department of Agriculture (USDA), Afrinvest Research

Afrinvest West Africa Page 13

Chart 9: Domestic Vs Industrial Consumption of Oil Palm (1981 - 2017) – Million MT.

Source: United States Department of Agriculture (USDA), Afrinvest Research

Chart 10: Total Oil Palm Supply, Oil Palm Importation and ratio of Import to Total

Supply in Nigeria (2008 – 2017)

Source: United States Department of Agriculture (USDA), Afrinvest

Page 14 The Nigerian Oil Palm Sector Report

Chart 12: SWOT Analysis

Source: Afrinvest Research

•

•

•

•

•

•

•

•

•

•

•

•

Chart 11: Trend in Oil Palm Prices (2012 – 2018) – US$

Source: Bloomberg, OKOMUOIL, Afrinvest Research

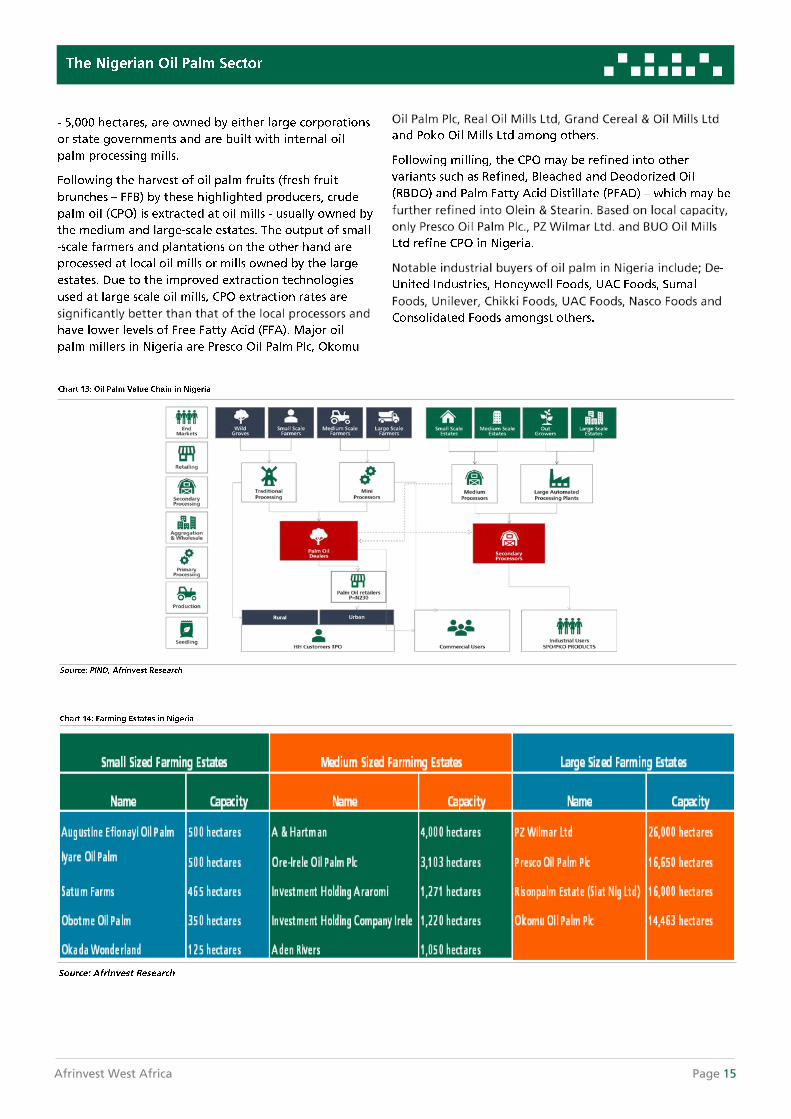

Afrinvest West Africa Page 15

Page 16 The Nigerian Oil Palm Sector Report

The Nigerian Insurance Sector Report

Page 18 The Nigerian Oil Palm Sector Report

Globally, there are two basic forms of Rubber; Natural

Rubber and Synthetic Rubbers. Whilst the natural rubber

is extracted in its natural origin - rubber trees -, synthetic

rubber is manmade and produced artificially under con-

trolled conditions. In terms of production areas, natural

rubber trees are usually grown and manufactured in

Southeast Asia (Indonesia, Thailand, Malaysia) while syn-

thetic rubbers are majorly manufactured in industrialized

countries such as United States and Japan and in devel-

oped countries in Western Europe and Eastern Europe.

Brazil is however the only developing country with a sig-

nificant synthetic rubber industry.

In 2017 the International Rubber Study Group (IRSG) esti-

mated global production of Rubber at 28.5m metric

tonnes which indicated a 2.7% CAGR from 23.3m metric

tonnes in 2011. In terms of rubber variants, natural rub-

ber accounted for 53.0% (15.0m metric tonnes) of global

production while the remainder was synthetic rubber at

47.0% (13.4 million metric tonnes). The trend so far in

2018 has seen a 3.3% increase Y-o-Y to 14.1m metric

tonnes in H1:2018 from 13.6m metric tonnes in H1:2018.

In terms of global rubber consumption, IRSG data show

that a 3.3% Y-o-Y increase from 27.5m metric tonnes in

2016 to 28.4 million metric tons in 2017 while its risen at

a CAGR of 1.9% between 2011 and 2017. Furthermore,

we saw an increase of 4.4% in total natural rubber con-

sumption to 13.2 million metric tonnes in 2017 while

there was a 2.4% Y-o-Y increase in total synthetic rubber

consumption to 15.2 million metric tonnes. The top 10

consumers of rubber in 2017 were China, USA, India, Ja-

pan, Thailand, Malaysia, Indonesia, Brazil, Germany and

Russia.

In terms of prices, price determination are based on ex-

port prices in the Asian Rubber Industry. Benchmarking

international prices to the export prices in South East Asia

is only reasonable as total production in Thailand, Indo-

nesia and Malaysia account for about 70.0% of global

rubber production. We describe some of the different

grades and prices of rubber exported from Thailand and

Malaysia below:

• Thai RSS3 - US$1.34/kg

• Thai STR20 - US$1.23/kg

• Thai 60.0% Latex - US$920/tonne

• Malaysia SMR20 - US$1.23/kg

Our observation of rubber prices in 2018 has seen a fall in

rubber prices since April 2018 following the March 2018

expiration of a December 2017 agreement by Thailand,

Indonesia and Malaysia to reduce export by 350,000 met-

ric tonnes which has led to the current oversupply in the

rubber market. Moreover, rubber demand has been pres-

sured by trade tensions between China and United States

which are major importers of rubber, hence leaving prices

moderated.

In terms of industry structure, there are several compa-

nies within the value chain from owners and operators of

rubber plantations to manufacturers of synthetic rubber

as well as companies dependent on processed rubber as

complements for their production processes. Notable

players across the rubber value chain are Bridgestone,

ExxonMobil, Michelin, Sri Trang Agro-Industry and The

Dow Chemical Company amongst others. Other promi-

nent companies are the China National Petroleum Corpo-

ration, LANXESS, LG Chem, Thai Rubber Corporation

Afrinvest West Africa Page 19

(Thailand), Tianjin Lugang Petroleum Rubber, Trinseo, and

Versalis.

As at 2017, Thailand produces the largest quantity of rub-

ber and hence accounts for approximately 30.6% of total

production market worth US$26.6bn. The market share of

other rubber producing countries are Indonesia – 28.2%,

Malaysia – 9.1%, India – 8.2 and Vietnam – 7.2%.

In terms of usage, about 65.7% of total rubber supplied is

used as automotive components while usage for medical

equipment, industrial machines and equipment as well as

aiding the production in consumer goods companies ac-

count for the remainder. It is expected that growth in

medical equipment will expand in the following years as

the demand from both developed and developing regions

will increase.

prices is also a determinant of synthetic rubber demand.

Synthetic rubber which is produced as a bye-product dur-

ing the fractional distillation of crude oil and hence fluc-

tuations in crude oil prices affects the price of an im-

portant raw material for synthetic rubber. Therefore, the

more stable the prices of crude oil are, the higher the

production and sales of synthetic rubber.

Rising Income Levels: A study by the Freedonia Group

show that rising income across developing countries will

support growth in motor vehicle manufacturing and us-

age, thus, fuelling the demand for tryes and in turn, rub-

ber. This growth in manufacturing activity will also be

follow an expansion in demand for the use of rubber for

automotive components, industrial rubber products,

medical products, and footwears.

The Nigeria Rubber Industry has been hit with meagre

performances in recent times. The sector which used to

be the highest producer of Rubber in Africa has dwin-

dled from being a source of foreign exchange earnings

in the 90’s to falling behind Ivory Coast - which now

produces more than double of Nigeria’s yearly rubber

production. In Nigeria, Rubber is grown in about 18

states which include; Delta, Bayelsa, Rivers, Akwa Ibom,

Cross River, Abia, Imo, Edo, Ondo, Ogun, Oyo, Kaduna,

and Taraba

As at 2016, Nigeria had a total installed rubber produc-

tion capacity of 600,000 metric tonnes/annum with utili-

zation of only 16.7% of this production capacity. Inter-

estingly, total rubber production in 2016 was over

156,000 metric tonnes - the highest level since 1991. Pro-

duction levels are expected to remain tapered on the

back of lack of investment in rubber plantation and pro-

cessing while yields in older trees continue to decline. At

the peak of rubber processing in Nigeria, there were

approximately 54 processing firms in operation which

has declined to only about 20 firms, thus, a reason for a

40.0% fall in total export volumes.

It notable to state that the decline in the Nigerian rub-

ber industry can be attributed to the shift to the same

issues that have affected growth in the agricultural sec-

tor -for example government focus on crude oil produc-

tion and government policy support for production of

food crops such as rice, tomatoes, cassava and maize

over cash crops. We expect revitalizing production in the

rubber industry will require investment in research and

development especially for development of rubber

clones and buds suitable for the Nigerian climatic condi-

tions.

Tyre Production in Developed Areas: It is expected that

increases in demand from tyre industries will increases

especially in regions such as North America and Europe.

This surge is expected to be driven by an increase in the

use of renewable rubber raw materials for production of

tyres.

Growing Demand in APAC: Another major driver for

growth is continuous demand for rubber in the Asia-

Pacific region (APAC). As at 2017, rubber consumption

demand in APAC accounted for the largest demand for

rubber growth is expected to remain solid over the next

four years. It must be noted that China, which is the

highest consumer of rubber, is a member of the APAC

region and consumption of rubber in the country is ex-

pected to further increase following companies’ prefer-

ence for establishing tyre factories in the country. China

uses 80.0% of its natural rubber to manufacture tyres.

Fluctuations in Crude Oil Prices: Volatility in crude oil

The Nigerian Insurance Sector Report

Afrinvest West Africa Page 21

Source: Company Filings, Afrinvest Research

37.3%

62.7%

NIGERIANPUBLIC

SOCFINAF S.A

50.0

70.0

90.0

110.0

130.0

150.0

Dec-17 Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18

NSEASI OKOMUOIL

Page 22 The Nigerian Oil Palm Sector Report

Source: Company fillings, Afrinvest Research

Source: Company Fillings, Afrinvest Research

Afrinvest West Africa Page 23

Chart 25 & 26: Turnover – Historical and Forecast (2013 – 2022F) – N’bn

Source: Company Filings, Afrinvest Research

Page 24 The Nigerian Oil Palm Sector Report

Source: Company Filings, Afrinvest Research

Afrinvest West Africa Page 25

Year ROE Net Margin Asset Turnover

(x) Leverage (x)

2013 8.5% 23.6% 0.29 1.22

2014 13.8% 15.4% 0.48 1.86

2015 22.7% 28.0% 0.49 1.67

2016 28.7% 34.0% 0.59 1.44

2017 37.3% 45.1% 0.65 1.28

2018F 34.7% 45.3%

0.59 1.30

2019F 41.3% 52.7%

0.62 1.27

2020F 38.8% 48.0%

0.65 1.24

2021F 41.5% 49.7%

0.68 1.23

2022F 42.9% 49.8%

0.71 1.21

2023F 49.3% 53.4%

0.77 1.20

Page 26 The Nigerian Oil Palm Sector Report

Afrinvest West Africa Page 27

Page 28 The Nigerian Oil Palm Sector Report

Labour Shortages May Impact Production Capacity: Our

engagement with management revealed a key business

challenge in supply of labour for farming operations,

which run all through the year. Usually, labour is critical

for business activities such as, harvesting, weeding and

fire control. We however believe that the firms deliberate

strategy of building housing communities within the

plantation may support its current policy of sourcing

cheap labour from other states in Nigeria (Akwa Ibom

and Benue especially).

Persistent Volatility in Commodity Prices: The business

has no control over the prices of CPO and Rubber Cakes

that it produces, as they are both sold in the internation-

al market where prices are determined by a number of

factors which include dynamics in supply and demand,

climatic conditions as well as Indian consumption (the

largest importer of CPO).

Nigeria’s Signing of AfCTA Deal: We opine that the com-

pany has significant exposure risks if Nigeria appends its

signature to the African Continental Free Trade Agree-

ment (AfCTA). Nigeria’s participation may require the

removal of CPO from the CBN’s list as well as the influx of

cheap CPO from Malaysia and Indonesia to Nigeria. How-

ever, we believe the influx of cheap CPO into Nigeria may

not pose an immediate risk as neighbouring countries are

also in deficient supply of CPO.

Backward Integration by Off-Takers: Several off-takers

(mostly Food Manufacturers and Consumer Goods –

FMCGs) in Nigeria are increasingly investing in oil palm

plantation development, oil palm milling and refining of

CPO. Of interest is the backward integration investments

by PZ Wilmar Limited, (a subsidiary of PZ Cussons Limited

created in partnership with Wilmar Foods in Indonesia). It

was reported in 2013 that the company acquired approxi-

mately 26,000 hectares of land in Cross River State to es-

tablish an oil palm plantation while also investing an ad-

ditional US$75.0m in 2015 for acquisition of equipment

for building an oil palm mill. In our opinion, we believe

these programmes should bridge the deficit in the indus-

try although it portends a normalisation in industry prices

and hence OKOMU’s revenues.

The Nigerian Insurance Sector Report

Page 30 The Nigerian Oil Palm Sector Report

Presco Plc is a fully-integrated agro-industrial company

and the market leader in supply and production of speci-

ality fats and oil in Nigeria and was incorporated on the

24th of September 24, 1991. The company owns several

oil palm plantations, a palm oil mill (90.0 FFB MT/hour),

palm kernel crushing plant (60.0M MT/day) and vegetable

oil refining and fractionation plant (100.0 MT/day). It also

has an olein and stearin packaging plant and a biogas

plant to treat its palm oil mill effluent.

Presco plantations which are in Edo and Delta States in

Nigeria, include the Obaretin (a concession of 6,462 hec-

tares) the Ologbo (a concession of 12,560 hectares) Es-

tates – both located in Edo State, and the Cowan Estate,

a concession of 2,800 hectares in Delta State. The compa-

ny also recently acquired an additional concession called

Sakponba Estate (17,000 hectares) also in Edo State. Also,

Presco has a 3,600 hectares rubber plantation planted in

2016 at the Orhionmwon Local Government Area of Edo

State, Nigeria. This plantation is yet to mature.

The company is a subsidiary of SIAT. S.A. (which owns

60.0% shareholding in Presco). SIAT is a Belgian agro-

industrial company specialized in industrial and small-

holder plantations of tree crops, mainly oil palm and rub-

ber. The company also engages in allied processing indus-

tries such as palm oil milling and refining/fractionation,

soap making and crumb rubber production.

Business Operational Model and Products

Presco’s business operations are primarily centred on pro-

duction of specialty fats and oil (especially RBD Oil - Re-

fined, Bleached and Deodorized and PFAD - Palm Fatty

Acid Distillate) from crude palm oil (CPO). The company

mills harvested fresh fruit brunches at its 90.0 FFB MT/

hour (upgraded from 60.0 FFB MT/hour in 2018) located

within the plantation. Presco had an average CPO extrac-

tion rate of 22.0% between FY:2015 and FY:2017 against

an average FFB output of 170,114 MT within the same

period.

In addition, Presco’s production of RBD and PFAD which

averaged at 26,568 MT and 9,620 MT between FY:2014

and FY:2017, is limited by the capacity of its 100.0 CPO

MT/day refinery. Hence, the company sells unprocessed

CPO to industrial off-takers in Nigeria at prices similar to

local CPO producer - OKOMUOIL. However, management

has guided that upgrades on this refinery to a 500.0 CPO

Chart 34: Shareholding Structure (PRESCO)

40.0%

60.0%

NIGERIANPUBLIC

SIAT.S.A

Chart 35: One Year Price Trajectory of NSEASI & PRESCO

Source: NSE

50

100

150

200

250

Dec-17 Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18

NSEASI PRESCO

Afrinvest West Africa Page 31

MT/hour would be completed in Q4:2019, which would

lead to an higher RBD and PFAD output going forward.

As at FY:2017, Presco’s total are under oil palm cultiva-

tion was 19,913 hectares with 11,587 hectares matured.

Also, the company produced a total of 169,352 MT of

FFBs (14.6 FFB MT/hectare) which translated to 37,637 MT

of CPO at an extraction yield of 22.2%. Based on our en-

gagement with management, we expect FFB tonnage to

reach 183,000in 2018, which would represent a 8.1% Y-o-

Y increase from 169,352 MT in FY:2017 while we also ex-

pect matured oil palm plantation area to have increased

to 13,659 hectares in FY:2018.

Also, we forecast Presco’s CPO production to reach

40,334.1MT and 41,946.6MT in FY:2018 and FY:2019, up

4.0%% and 11.3% Y-o-Y respectively. Our forecasts are

based on the company recent upgrade to the company’s

oil mill to 90.0 FFB MT/hour from 60.0 FFB MT/hour as

well as expanded output from maturing hectares in 2018.

We expect 7,100 hectares to mature in 2020 (3,600 hec-

tares) and 2021 (3,500 hectares) respectively.

Consequently, we expect CPO production and therefore

RBD and PFAD output to be buoyed by this additional

FFB output as well as completion of upgrades on the

company’s 100.0 CPO MT/day refinery. Based on this, we

expect the company’s RBD and PFAD output to more

than double by 2020 with a corresponding reduction in

CPO sales.

Presco has recorded strong growth in its revenue rising

from N8.5bn in FY:2013 to N22.4bn in FY:2017, growing

at a CAGR of 27.4% and buoyed especially by attractive

local prices of CPO and RBD in FY:2016 and FY:2017. In

FY:2018 and FY:2019, we project an improvement in turn-

Costs Significant Constituents

In terms of cost, our analysis showed a 17.3% decline in

cost of sales from N3.9bn in FY:2013 to N3.2bn in

FY:2014, although it has been on the uptrend since then,

rising by 19.2%, 15.5% and 34.9% to N3.8bn, N4.4bn and

N5.9bn in FY:2015, FY:2016 and FY:2017 respectively. We

attribute these increases to high pace of upticks in mill-

ing, refining and packaging costs.

Also, cost of sales expressed as a percentage of total turn-

over settled at an average of 34.3% between 2013 and

2017, with the lowest percentage recorded in 2017 at

26.6% impacted by the fast pace of revenue growth in

over to N22.8bn and N26.8bn respectively while we antic-

ipate revenues to settle at N63.8bn in FY:2023 represent-

ing a CAGR of 19.1% between 2017 and 2023.

As at 9M:2018, the company recorded a total turnover of

N16.2bn, down 4.1% Y-o-Y while a 20.4% decline in cost

of sales buoyed gross profit margins to N12.3bn within

the same period. However, a 38.7% expansion in selling,

general and administrative expenses moderated overall

profitability.

Cost of Sales… Mill Processing, Refinery and Packaging

9.1 10.4

15.7

22.4 22.8

26.829.5

37.6

48.6

63.8

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2014 2015 2016 2017 2018E 2019F 2020F 2021F 2022F 2023F

162.1176.5

164.5 169.4183.0 190.3

211.9

259.9

329.4

425.4

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

2014 2015 2016 2017 2018E 2019F 2020F 2021F 2022F 2023F

27.6

39.335.6 37.6

40.3 41.946.6

57.4

72.6

93.7

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

2014 2015 2016 2017 2018E 2019F 2020F 2021F 2022F 2023F

Page 32 The Nigerian Oil Palm Sector Report

2016 and 2017.

Impressive Operating Income Growth… Performance

weighed on by Expenses

Presco’s operating income has consistently grown since

2014, following a decline of N20.5% from N3.0bn to

N2.4bn in FY:2014. Thereafter, operating income has

grown consistently at annual rates; +58.5% (FY:2015),

+82.2% (FY:2016) and +29.9% (FY:2017). Furthermore,

operating margin averaged at 37.1% over this period,

peaking at 44.7% in FY:2016 due to favourable local pric-

es and lowest at 26.7% in FY:2014.

Also, operating expenses expanded 125.9% Y-o-Y from

N1.6bn in FY:2013 to N3.4bn in FY:2014, declined by

20.8% in FY:2015 to N2.5bn while in FY:2016 and FY:2017

expanded 54.2% and 70.3% Y-o-Y respectively. We note

that Presco’s operating expenses is significantly driven by

selling, general and administrative expenses (S, G & A)

which constitute an average of 91.8% of operating ex-

penses.

Robust Profitability Growth… Revaluation Gain and Tax

Credits Support Strong Performance

Presco has posted positive profit before tax (PBT) since

2013, rising from N2.3bn in 2013 to N10.95bn in 2017 at

a CAGR of 47.2%. In line with sector dynamics, the com-

pany benefited from higher local prices of CPO, RBD and

PFAD which buoyed earnings especially in FY:2016 and

FY:2017 based on previously highlighted reason (CBN’s

list of 42 excluded items). However, we note a stronger

growth in profit after tax (PAT) from N2.5bn in FY:2015

to N21.7bn (PBT – N31.2bn) in FY:2016 driven by a reval-

uation gain (N24.9bn) on biological assets while the

business tax credit claim (N14.5bn) aided a further rise in

PAT to N25.4bn in FY:2017 (up 16.9%).

3.2

3.8

4.4

5.95.6

6.3 6.5

7.1

7.7

8.2

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2014 2015 2016 2017 2018E 2019F 2020F 2021F 2022F 2023F

Afrinvest West Africa Page 33

The company had an average ROE of 21.2% between 2013

and 2017 buoyed by the jump in ROE in FY:2016 and

FY:2017. We however forecast ROE in FY:2018 and

FY:2019 to normalise to 7.5% apiece as we view the reval-

uation gain and tax credit recorded in FY:2016 and

FY:2017 as being unsustainable. Also, average net margin

between FY:2013 and FY:2017 pegged at 64.8% also lifted

by stellar performance in FY:2016 and FY:2017 (ex-FY:2016

and FY:2017, net margin averaged 24.1% between 2013

and 2015). We forecast net margin to decline to 30.2% in

FY:2018 but improve to 30.4% in FY:2019 while we project

an average net margin of 33.2% between 2018 and 2023.

Presco’s asset turnover averaged at 0.23x between 2013

and 2017 reflecting the general weak asset turnover in the

industry attributed to a significant contribution of bearer

assets (accounting for 63.2% between 2013 and 2017) to

non-current assets. Bearer assets (the oil palm and rubber

trees) are expected to generate output over their econom-

ic life. We forecast an improvement in asset turnover to an

average of 0.24x between 2018 and 2023 based on im-

proved revenues in the forecast period.

Furthermore, the company’s leverage ratio (or equity mul-

tiplier), computed as total assets divided by net assets,

show a decline from 1.88x in FY:2013 to 1.75x in FY:2014.

However, it improved marginally to 1.77x in FY:2015 but

has since maintained a downturn to 1.60x and 1.29x in

FY:2016 and FY:2017 respectively. We forecast an average

leverage of 1.30 between 2018 and 2023.

Price Target and Recommendation… Our Valuation Sug-

gests ACCUMULATE

Over our forecast period, that is between 2018 and 2023,

we expect Presco’s revenues and overall profitability to

be essentially buoyed by improvements in RBD output

based on improved operational capacity of its refinery –

500 CPO MT/day capacity. Also, we expect that addition-

al FFB output from maturing plantations in 2020 (3,600

hectares) and 2021 (3,500 hectares) to increase the com-

pany’s CPO and RBD output levels.

In valuing PRESCO, we utilized a blended valuation of

the Dividend Discount, Free Cash Flow to Equity (FCFE),

Residual Income, EV/EBITDA, Justified P/E & P/B valuation

models. Input assumptions were raw beta of 0.61, cost of

equity of 24.8% (risk free rate of 14.17% & risk premium

of 11.42%) and sustainable growth rate of 2.0% to real-

ise a blended 12-month target price (TP) of N77.29. This

represents an upside of 24.65% from current price of

N62.00 (24/01/2019). Hence, we recommend a

‘ACCUMULATE’ rating on PRESCO.

Assumptions and weights assigned for the valuation

models are described below;

2.7 3.44.2

31.2

11.09.8

11.513.0

18.1

24.7

34.5

-9.5% 27.9% 23.2%

640.9%

-64.9%-2.7% 1.7% 11.9%

26.5% 27.1% 32.7%

-200.0%

-100.0%

0.0%

100.0%

200.0%

300.0%

400.0%

500.0%

600.0%

700.0%

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F 2022F 2023F

PBT PBT Growth Rate

Year ROE Net Margin Asset Turnover (x) Leverage (x)

2013 7.7% 15.8% 0.26 1.88

2014 13.1% 28.5% 0.26 1.75

2015 8.0% 23.9% 0.19 1.77

2016 41.7% 138.3% 0.19 1.60

2017 33.4% 113.6% 0.23 1.29

2018F 7.5% 30.2% 0.19 1.31

2019F 7.5% 30.4% 0.19 1.29

2020F 8.4% 31.0% 0.21 1.29

2021F 10.1% 33.9% 0.23 1.30

2022F 12.5% 35.8% 0.27 1.30

2023F 16.8% 38.1% 0.34 1.30

Page 34 The Nigerian Oil Palm Sector Report

Afrinvest West Africa Page 35

Page 36 The Nigerian Oil Palm Sector Report

The Nigerian Insurance Sector Report

Section Seven

Afrinvest (West Africa) Limited

Page 38 The Nigerian Oil Palm Sector Report

About US

Afrinvest (West Africa) Limited (“Afrinvest” or the “Company”) is a leading independent investment banking firm with a

focus on West Africa and active in four principal areas: investment banking, securities trading, asset management, and

investment research. The Company was originally founded in 1995 as Securities Transaction and Trust Company Limited

(“SecTrust”) which grew to become a respected research, brokerage and asset management firm. Afrinvest (West Africa)

Limited is licensed by the Nigerian Securities and Exchange Commission (“SEC”) as an issuing house and underwriter. We

provide financial advisory services as well as innovative capital raising solutions to High Net-worth Individuals (“HNIs”),

corporations, and governments. Afrinvest is a leading provider of research content on the Nigerian market as well as a

leading adviser to blue chip companies across West Africa on M&A and international capital market transactions. The

company maintains three offices in Lagos, Abuja and Port-Harcourt.

Afrinvest Securities Limited (“ASL”) is licensed by the Nigerian SEC as a broker dealer and is authorized by the Nigerian

Stock Exchange (“NSE”) as a dealing member. ASL acts as a distribution channel for often exclusive investment products

originated by Afrinvest and AAML as well as unique value secondary market trading opportunities in equity, debt,

money market and currency instruments.

Afrinvest Asset Management Limited (“AAML”) is licensed by the Nigerian SEC as a portfolio manager. AAML delivers

world class asset management services to a range of mass affluent and high net worth individual clients. AAML offers

investors direct professionally managed access to the Nigerian capital markets through equity focused, debt focused and

hybrid unit trust investment schemes amongst which are the Nigeria International Debt Fund (NIDF), Afrinvest Equity

Fund (AEF), Balance Growth Portfolio (BGP), Ethical Investment Portfolio (EIP) and Guaranteed Income Portfolio (GIP).

Contacts

For further information, please contact:

Afrinvest West Africa Limited (AWA)

27,Gerrard Road

Ikoyi, Lagos

Nigeria

Tel: +234 1270 1680 | +234 1 270 1689

www.afrinvest.com

Investment Research

Robert Omotunde [email protected] +234 1 270 1680 ext. 314

Jolomi Odonghanro [email protected] +234 1 270 1680 ext. 319

Adedayo Bakare [email protected] +234 1 270 1680 ext. 317

Omoefe Eromosele [email protected] +234 1 270 1680 ext. 321

Abiola Gbemisola [email protected] +234 1 270 1680 ext. 312

Adeoluwa Eweje [email protected] +234 1 270 1680 ext. 318

Institutional Sale and Marketing

Ayodeji Ebo [email protected] +234 1 270 1680 ext. 315

Bolaji Fajenyo [email protected] +234 1 270 1680 ext. 261

Investment Banking

Oladipo Ajike [email protected] +234 1 270 1680 ext. 180

Jessica Essien [email protected] +234 1 270 1680 ext. 171

Asset Management

Ola Belgore [email protected] +234 1 270 1680 ext. 281

Rotimi Ashimi [email protected] +234 1 270 1680 ext. 282

Afrinvest West Africa Page 39

Page 40 The Nigerian Oil Palm Sector Report

Afrinvest West Africa Page 41