osvaldo rosales - amcham chile · before the crisis (2003-2008)…. three simultaneous...

TRANSCRIPT

Osvaldo RosalesOsvaldo RosalesDirector, Trade and Integration Division

ECLAC

AMCHAM-Chile

July 14th, 2010

2

Before the crisis (2003-2008)….� Three simultaneous macroeconomic developments:

o Sound fiscal policies and a better public debt profile

o More flexible exchange rates and unprecedentedly high international reserves (+150% between 2003 and 2008)

o A regional current-account surplus with economic growth

� Ready access to external financing� Ready access to external financing� Increase in trade (M + X) (value: 138%/volume: 49%)� Terms of trade improved by 25% in the region� Per capita GDP grew by more than 3% per year for five

consecutive years� Unemployment diminished from 11% to 7.5% with job

quality� Poverty rates fell by 10 percentage points (from 44% to

34%)

Region’s real economy has been severely

affected: trade, remittances, tourism, FDI

1%

15% 14% 13%

0%0%

10%

20%

Latin America and the Caribbean: Year-on-year change in goods and services exports,

foreign direct investment and remittances, 2008 and 2009

-10%

-15% -15%

-37%

-13%

-40%

-30%

-20%

-10%

0%

Export volume Price of export goods

Services exports

Foreign Direct Investment

Remittances

2008 2009

4Source: ECLAC.

The region’s goods exports and imports fell 23% and 25%, respectively, in 2009, after an increase of 16% and 22% in 2008

LATIN AMERICA AND THE CARIBBEAN: MERCHANDISE EXPORT GROWTH 2008 AND 2009

(Growth rates relative to the same period in the previous year)

Exports Imports

9%

7%

17%

-9%

-21%

-30%

Central America

Mexico

Caribbean countries

14%

9%

21%-23%

-24%

-25%Central America

Mexico

Caribbean countries

Source: ECLAC, based on official sources.

16%

22%

25%

7%

9%

-23%

-24%

-22%

-20%

-20%

-9%

-2%

30%-28%

-40% -20% 0% 20% 40%

Latin America and the Caribbean

South America

MERCOSUR

Andean countries

Chile

Mexico and Central America

Central America

2008-2007 2009-2008

22%

34%

41%

23%

31%

10%

14%

-21%

-25%

-24%

-31%

-27%

-26%

-25%

-40% -20% 0% 20% 40% 60%

Latin America and the Caribbean

South America

MERCOSUR

Andean countries

Chile

Mexico and Central America

Central America

2008-2007 2009-2008

Among its major trade partners, exports to Asia fell the least

LATIN AMERICA AND THE CARIBBEAN: MERCHANDISE EXPORT GROWTH 2008 AND 2009,

BY DESTINATION AND ORIGIN

(Growth rates relative to the same period in the previous year)

Exports Imports

18%

24%

-14%

-28%

Other Asia countries

LAC

19%

21%

-26%

-25%

Other Asia countries

LAC

Source: ECLAC, based on official sources.

16%

9%

15%

21%

25%

-23%

-26%

-28%

-6%

6%

-40% -20% 0% 20% 40%

World

United States

European Union

Asia

China

2008 - 2007 2009 - 2008

22%

17%

24%

24%

32%

-25%

-25%

-23%

-21%

-16%

-40% -20% 0% 20% 40%

World

United States

European Union

Asia

China

2008 - 2007 2009 - 2008

Intra-regional trade remains below the peak levels reached prior to

the Asian Crisis… and in 2009 it fell even more than total trade

25%

30%

35%Andean Community MERCOSURCentr. American Common Mkt CARICOM

LATIN AMERICA AND THE CARIBBEAN: INTRAREGIONAL TRADE, 1986-2009(As a share of each group or subregion’s total exports)

0%

5%

10%

15%

20%

25%

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9p

7Source: ECLAC based on COMTRADE.

The drop in LAC exports has no recent precedent.

The nearest parallel happened 70 years ago

Latin America and the Caribbean: price and quantity of exports

1931-2009 (Annual growth rates)

40

60

80

Source: ECLAC, based on official sources. 2009 projections from ECLAC International Trade and Integration Division

-40

-20

0

20

40

1931

1934

1937

1940

1943

1946

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

quantity price

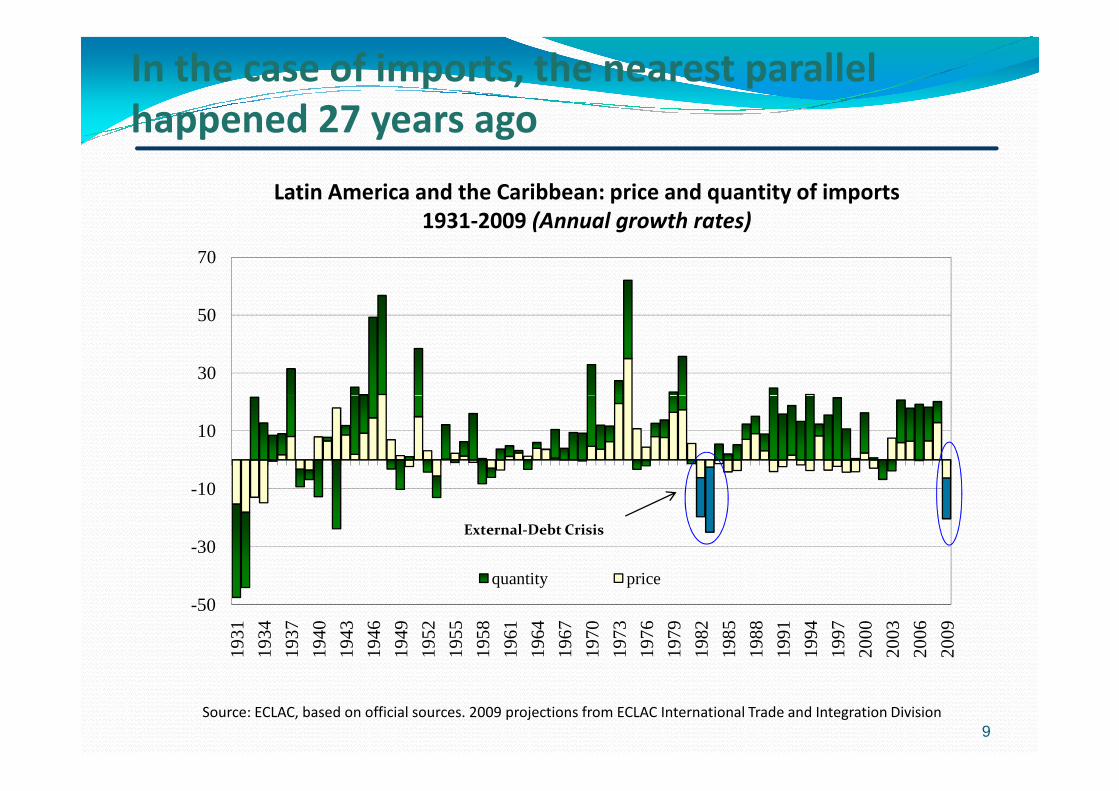

8

In the case of imports, the nearest parallel

happened 27 years ago

30

50

70

Latin America and the Caribbean: price and quantity of imports

1931-2009 (Annual growth rates)

-50

-30

-10

10

1931

1934

1937

1940

1943

1946

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

quantity price

External-Debt Crisis

Source: ECLAC, based on official sources. 2009 projections from ECLAC International Trade and Integration Division

9

But recovery has already started…� For 2010 ECLAC predicts an average GDP growth of 4.3%

� Regional exports for the second half of 2009 fell by 15% in value respect to the same period of 2008, but it grew 4.7% in December over November of 2009.

� For 2010 ECLAC predicts trade growth between 5 and 6% in terms of volumeterms of volume

� Terms of Trade for the region would improve 3,8% in 2010, stimulated principally by hydrocarbons and metals in South America and Mexico.

� Though current account balance might worsen in 2010 –thanks to faster increases in imports –, recovery in financial inflows, especially FDI, would compensate for the deficit.

10

60,000

70,000

80,000

90,000

Ba lance Exports Imports

LAC exports and imports, which fell drastically as a result of the

crisis, begin to recover to a pre-crisis level

LATIN AMERICA AND THE CARIBBEAN: EVOLUTION OF TRADE IN GOODS

(in million of dollars)January 2006-December 2009

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

Jan

/06

Fe

b/0

6M

ar/

06

Ap

r/0

6M

ay

/06

Jun

/06

Jul/

06

Au

g/0

6S

ep

/06

Oc

t/0

6N

ov

/06

De

c/0

6Ja

n/0

7F

eb

/07

Ma

r/0

7A

pr/

07

Ma

y/0

7Ju

n/0

7Ju

l/0

7A

ug

/07

Se

p/0

7O

ct/

07

No

v/0

7D

ec

/07

Jan

/08

Fe

b/0

8M

ar/

08

Ap

r/0

8M

ay

/08

Jun

/08

Jul/

08

Au

g/0

8S

ep

/08

Oc

t/0

8N

ov

/08

De

c/0

8Ja

n/0

9F

eb

/09

Ma

r/0

9A

pr/

09

Ma

y/0

9Ju

n/0

9Ju

l/0

9A

ug

/09

Se

p/0

9O

ct/

09

No

v/0

9D

ec

/09

Source: ECLAC, based on official sources.

20,000

30,000

40,000

50,000

60,000

Balance Exports Imports

Recovery has been quicker for South America, benefitting

from a strong demand of commodities by China

40,000

50,000

60,000

Balance Exports Imports

SOUTH AMERICA : EVOLUTION OF TRADE IN GOODS (in million of dollars)

January 2006-December 2009

MEXICO AND CENTRAL AMERICA: EVOLUTION OF TRADE IN GOODS

(in million of dollars)January 2006-December 2009

-10,000

0

10,000

Jan

/06

Fe

b/0

6M

ar/

06

Ap

r/0

6M

ay

/06

Jun

/06

Jul/

06

Au

g/0

6S

ep

/06

Oc

t/0

6N

ov

/06

De

c/0

6Ja

n/0

7F

eb

/07

Ma

r/0

7A

pr/

07

Ma

y/0

7Ju

n/0

7Ju

l/0

7A

ug

/07

Se

p/0

7O

ct/

07

No

v/0

7D

ec

/07

Jan

/08

Fe

b/0

8M

ar/

08

Ap

r/0

8M

ay

/08

Jun

/08

Jul/

08

Au

g/0

8S

ep

/08

Oc

t/0

8N

ov

/08

De

c/0

8Ja

n/0

9F

eb

/09

Ma

r/0

9A

pr/

09

Ma

y/0

9Ju

n/0

9Ju

l/0

9A

ug

/09

Se

p/0

9O

ct/

09

No

v/0

9D

ec

/09

-10,000

0

10,000

20,000

30,000

40,000

Jan

/06

Fe

b/0

6M

ar/

06

Ap

r/0

6M

ay

/06

Jun

/06

Jul/

06

Au

g/0

6S

ep

/06

Oc

t/0

6N

ov

/06

De

c/0

6Ja

n/0

7F

eb

/07

Ma

r/0

7A

pr/

07

Ma

y/0

7Ju

n/0

7Ju

l/0

7A

ug

/07

Se

p/0

7O

ct/

07

No

v/0

7D

ec

/07

Jan

/08

Fe

b/0

8M

ar/

08

Ap

r/0

8M

ay

/08

Jun

/08

Jul/

08

Au

g/0

8S

ep

/08

Oc

t/0

8N

ov

/08

De

c/0

8Ja

n/0

9F

eb

/09

Ma

r/0

9A

pr/

09

Ma

y/0

9Ju

n/0

9Ju

l/0

9A

ug

/09

Se

p/0

9O

ct/

09

No

v/0

9D

ec

/09

Source: ECLAC, based on official sources.

LAC is lagging behind in international competitiveness…

8486

8892

98103104105

115118

120124

GuatemalaJamaica

ArgentinaTrinidad & Tobago

Dom. Rep.Suriname

EcuadorVenezuela, B.R.

GuyanaBolivia, P.S.

NicaraguaParaguay

Selected countries: Ranking in the WEF Global Competitiveness Index, 2008-09

46

1518

2224

2847

585960

647475

79828384

0 20 40 60 80 100 120 140

SwedenFinlandNorway

AustraliaIreland

N. ZealandChile

BarbadosPanama

Costa RicaMexico

BrazilColombiaUruguay

El SalvadorHonduras

PeruGuatemala

Better

13Source: WEF Global Competitiveness Report 2008-2009.

…and also in technological readiness

788182

8789

9596

100106

117122

125128

El SalvadorTrinidad y Tobago

GuatemalaArgentina

PerúHonduras

Venezuela, R.B.Guyana

EcuadorSurinamParaguay

NicaraguaBolivia, E.P.

Selected countries: Ranking in the WEF Network Readiness Index, 2008-09

26

814

2223

3639

5356

5964656667

7578

0 20 40 60 80 100 120 140

SwedenFinlandNorway

AustraliaN. Zealand

IrelandBarbados

ChileJamaicaC. Rica

BrazilColombiaUruguayPanamáMéxico

Rep. DominicanaEl Salvador

Better

14Source: WEF Global Competitiveness Report 2008-2009.

And there is a long way to go in trade facilitation

Chile &

Mexico

OECD

Korea

Singapore

Chile & Panama

Mexico

OECD

Korea

Singapore

Time to export and import

(days)

Cost to export and import

(US Dollars per container)

0 10 20 30 40

Andean countries

MERCOSUR

Central America

Caribbean

Chile & Panama

Time to import Time to export

0 500 1000 1500 2000 2500

Andean countries

MERCOSUR

Central America

Caribbean

Chile & Panama

Cost to import Cost to export

15

Source: ECLAC based on World Bank, Doing Business 2010.

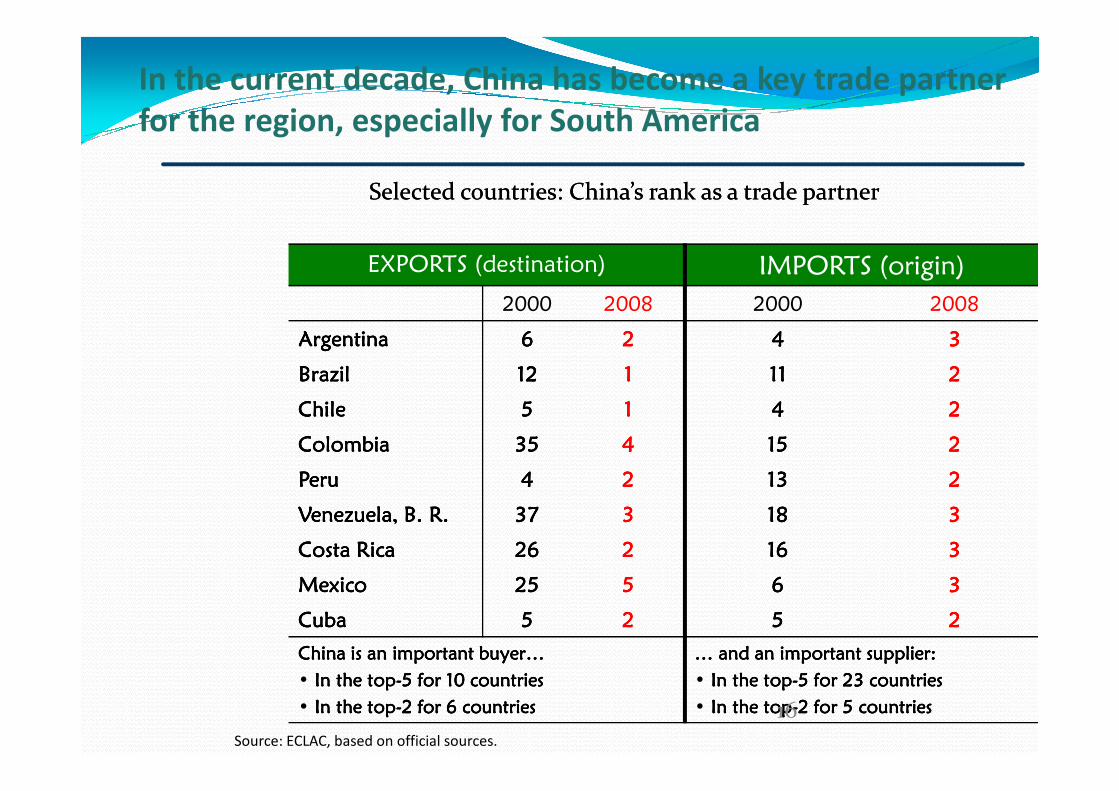

EXPORTS (destination) IMPORTS (origin)

2000 2008 2000 2008

ArgentinaArgentinaArgentinaArgentina 6666 2222 4444 3333

BrazilBrazilBrazilBrazil 12121212 1111 11111111 2222

In the current decade, China has become a key trade partner

for the region, especially for South America

Selected countries: China’s rank as a trade partnerSelected countries: China’s rank as a trade partner

ChileChileChileChile 5555 1111 4444 2222

ColombiaColombiaColombiaColombia 35353535 4444 15151515 2222

PeruPeruPeruPeru 4444 2222 13131313 2222

Venezuela, B. R.Venezuela, B. R.Venezuela, B. R.Venezuela, B. R. 37373737 3333 18181818 3333

Costa RicaCosta RicaCosta RicaCosta Rica 26262626 2222 16161616 3333

MexicoMexicoMexicoMexico 25252525 5555 6666 3333

CubaCubaCubaCuba 5555 2222 5555 2222

China is an important buyer… China is an important buyer… China is an important buyer… China is an important buyer…

• In the topIn the topIn the topIn the top----5 for 10 countries5 for 10 countries5 for 10 countries5 for 10 countries

• In the topIn the topIn the topIn the top----2 for 6 countries2 for 6 countries2 for 6 countries2 for 6 countries

… and an important supplier:… and an important supplier:… and an important supplier:… and an important supplier:

• In the topIn the topIn the topIn the top----5 for 23 countries5 for 23 countries5 for 23 countries5 for 23 countries

• In the topIn the topIn the topIn the top----2 for 5 countries2 for 5 countries2 for 5 countries2 for 5 countries

Source: ECLAC, based on official sources.

16

LAC, as an increasing trade partnership of China

Trade growth rates, key regional partners, 1995-2009 (Average

annual rates) Trade Partners

Regions 1990-1995 1995-2000 2000-2005 2005-2009 (1)

Latin America and the Caribbean 32.2 17.8 26.8 26.1

Asia Pacific (2) 26.5 9.3 20.3 11.6

United States 36.7 16.1 25.6 10.2

European Union 26.3 15.0 28.8 14.9

Rest of the World 8.6 7.1 26.6 14.3

World 19.1 10.9 25.0 13.4

Exports

17

Source: Economic Commission for Latin America and the Caribbean (ECLAC), on the basis of the United Nations

statistical database on merchandise trade (COMTRADE) and DOTs (IMF)

Notes: (1) corresponds to DOTs data for January to November and moving average estimates for December. (2)

Includes ASEAN, Australia, Republic of Korea, Japan and New Zealand.

World 19.1 10.9 25.0 13.4

Latin America and the Caribbean 14.5 12.7 37.6 22.8

Asia Pacific (2) 32.4 12.2 23.9 7.1

United States 19.7 6.8 16.8 10.2

European Union 18.2 7.6 18.8 14.4

Rest of the World 11.2 13.4 26.8 14.5

World 19.9 11.3 24.0 11.7

Imports

17

Share of Asia-Pacific (17)a and China in the total exports of Latin American countries,

2001-2006 (% of the total exports of each country)

2000 2009

18

Source: Economic Commission for Latin America and the Caribbean (ECLAC), on the basis of information from the

United Nations Commodity Trade Database (COMTRADE).a Asia Pacific (17) includes Australia, Brunei Darussalam, Cambodia, Hong Kong (Special Administrative Region of

China), India, Indonesia, Japan, Lao PDR, Malaysia, Myanmar, New Zealand, Philippines, Republic of Korea,

Singapore, Taiwan Province of China, Thailand, and Viet Nam.

18

Latin America and the Caribbean (16 countries):

share of the main destinations in total exports,

2000-2020(In percentages)

19

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on data from the

COMTRADE database and national sources.

Notes: the 16 countries are: Argentina, Bolivia (Plurinational State), Brazil, Chile, Colombia, Costa Rica,

Ecuador, El Salvador, Guatemala, Honduras, Mexico, Panama, Paraguay, Peru, Uruguay, Venezuela

(Bolivarian Republic of). Estimates and projections based on GDP growth rates for the years 2000-2009

in the United States, European Union, China, Latin America and the Caribbean, Asia Pacific, and Rest of

World. It is expected a growth rate of trade which converges to the economies' long-term growth rate.

19

Latin America and the Caribbean (16 countries):

share of the main sources of total imports,

2000-2020(In percentages)

20

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on data from the

COMTRADE database and national sources.

Notes: the 16 countries are: Argentina, Bolivia (Plurinational State), Brazil, Chile, Colombia, Costa Rica,

Ecuador, El Salvador, Guatemala, Honduras, Mexico, Panama, Paraguay, Peru, Uruguay, Venezuela

(Bolivarian Republic of). Estimates and projections based on GDP growth rates for the years 2000-2009

in the United States, European Union, China, Latin America and the Caribbean, Asia Pacific, and Rest of

World. It is expected a growth rate of trade which converges to the economies' long-term growth rate.

20

Latin America and the Caribbean: Three leading Latin America and the Caribbean: Three leading export products for Selected Countries, by Country export products for Selected Countries, by Country

or Region of Destination, 2004or Region of Destination, 2004--20062006(Percentages)

Asia-Pacific European Union China United States World

Argentina 57.8% 44.9% 83.4% 24.6% 21.9%

Brazil 34.4% 22.1% 55.7% 13.9% 12.2%

Chile 71.7% 65.4% 85.8% 47.5% 55.3%

Costa Rica 89.8% 56.8% 94.2% 36.2% 30.0%Costa Rica 89.8% 56.8% 94.2% 36.2% 30.0%

Guatemala 86.7% 74.7% 97.5% 45.2% 23.8%

Mexico 20.3% 46.3% 47.6% 23.8% 24.8%

Peru 61.9% 41.5% 70.6% 51.3% 40.0%

Source: ECLAC, on the basis of information from the United Nations Commodity Trade Database (COMTRADE).

21

Higher quality in the exports oriented to US markets

…more tech intensity in LAC EXPORTS

US EU AP

Primary products

26% 46% 59%

NRBM 12% 29% 24%

LTM 11% 5% 3%LTM 11% 5% 3%

MTM 30% 15% 9%

HTM 19% 4% 5%

22

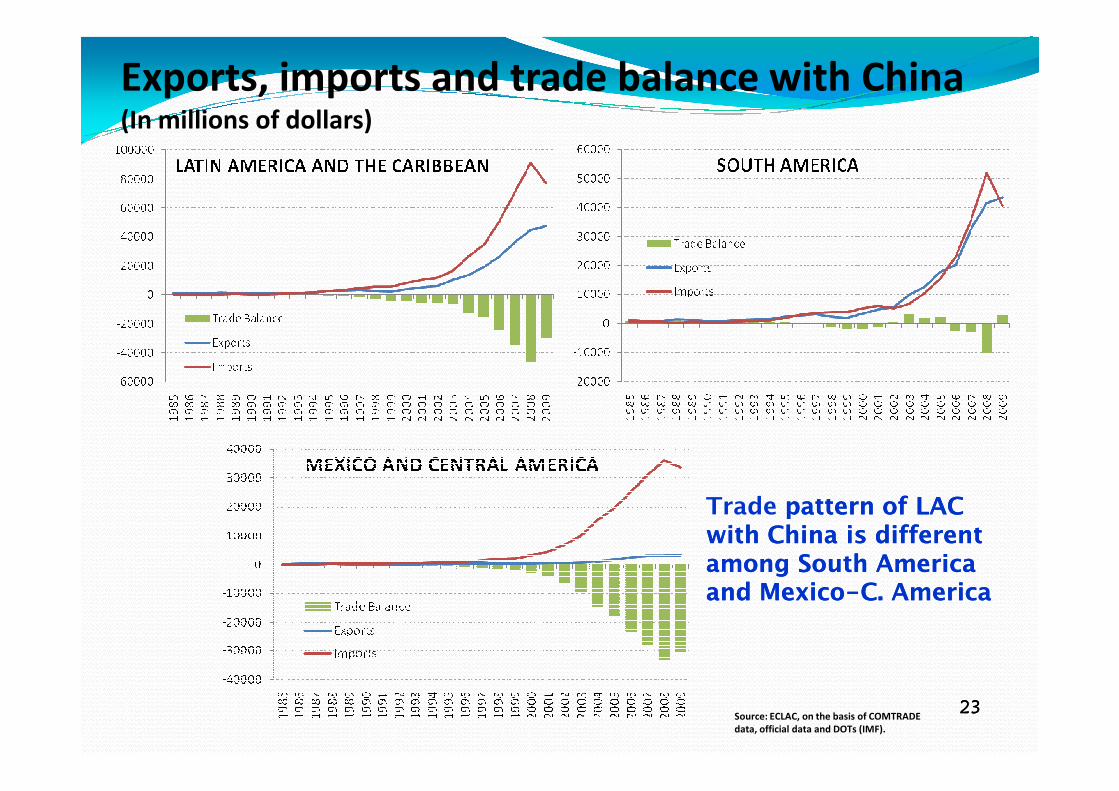

Exports, imports and trade balance with China(In millions of dollars)

23Source: ECLAC, on the basis of COMTRADE

data, official data and DOTs (IMF).

Trade patternpattern of LAC of LAC withwith China China isis differentdifferentamongamong South South AmericaAmericaand and MexicoMexico--C. C. AmericaAmerica

23

Official visits of Head of States are growingOfficial visits of Head of States are growingOfficial visits of Head of States are growingOfficial visits of Head of States are growing

24

Summary of the trade relationship with China

� Asymetry between levels of trade and investment

� Asymetry between South America and Mexico-C America

� Few products explain the majority of exports

� Mainly natural resources¨; low technology content

� Trade flows almost exclusively inter-industry

� Asymetry between the organized Chinese agenda for LAC and the LAC reaction, without regional coordination

� China displacing EU as second trade partner of LAC by 2015.� China displacing EU as second trade partner of LAC by 2015.

� Backward trend in export diversification

� Risks of “Dutch disease”

� Risk to reinforce the inter-industry specialization with China

� Complacency with the cycle of commodities, delaying choices of industrial and innovation policies

� Loosing opportunities to advance on internationalization of enterprises, fostering linkages between services, manufactures and natural resources

25

Regional scenarios on trade

� In 2012, 9 LA countries will have FTA with US� Colombia &Panama pending

� 11 or 16 with EU (depending on Mercosur)

� 15 trade agreements will link 5 LA countries with 11 � 15 trade agreements will link 5 LA countries with 11 Asian economies

� Plus a lot of regional agreements within LAC � Demand of convergence

26

FTAs with US in the AmericasFTAs with US in the AmericasFTAs with US in the AmericasFTAs with US in the Americas

CanadáCanadáCanadáCanadá

27

ChileChileChileChile

PerúPerúPerúPerú

ColombiaColombiaColombiaColombiaCostaCostaCostaCosta RicaRicaRicaRica

NicaraguaNicaraguaNicaraguaNicaraguaEl SalvadorEl SalvadorEl SalvadorEl Salvador

HondurasHondurasHondurasHonduras República República República República DominicanaDominicanaDominicanaDominicanaGuatemalaGuatemalaGuatemalaGuatemala

MéxicoMéxicoMéxicoMéxico

EcuadorEcuadorEcuadorEcuador

PanamáPanamáPanamáPanamá

OSVALDO ROSALES27

Some salient trends � CAFTA-NAFTA convergence: a huge potential to exploit

� Amplified markets with similar rules and disciplines on goods, Services and Investment

� Tech and business alliances to deal with Asian challenges

� Mexico-C. America

� US-Mexico-C America

� Accumulation origin

� Within all FTAs in LA with US

� CAFTA-NAFTA will over Panama-Colombia� Real state boom in Panama and other CA countries

� Business linked to the expansion of Panama Canal

� Plan Puebla-Panama-Colombia

� Investment on infrastructure, logistics, ICT’s

28

JapónJapónJapónJapón

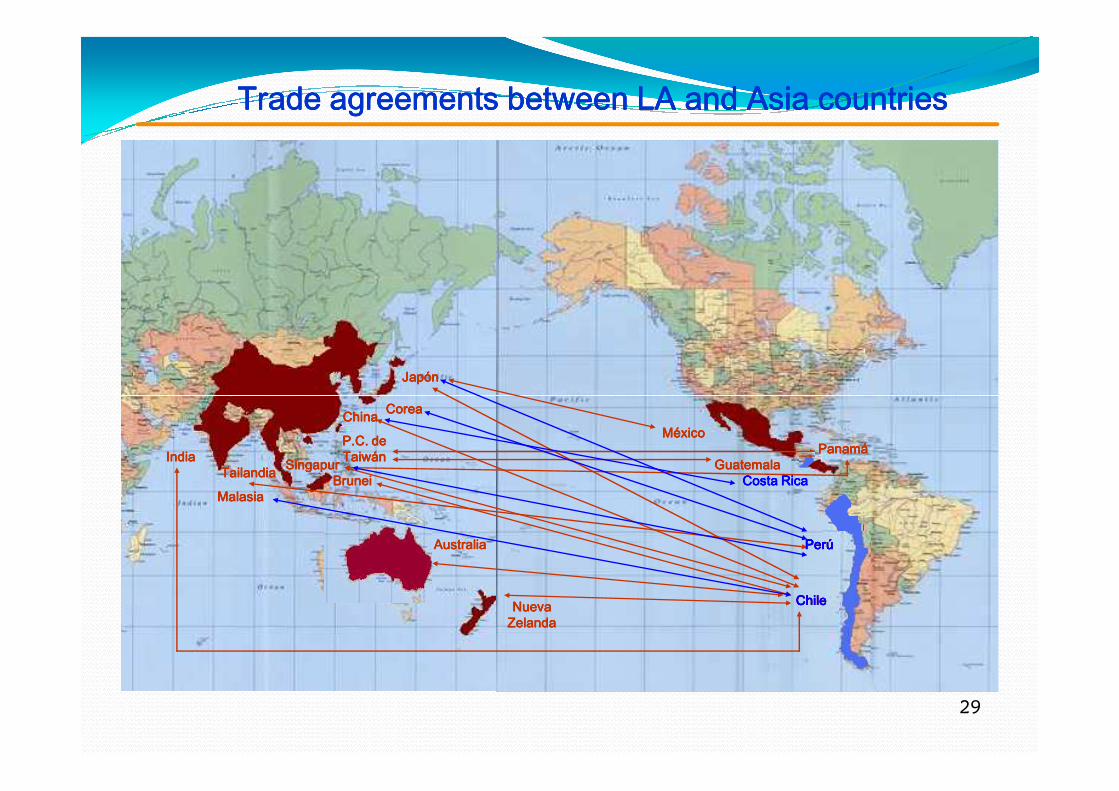

Trade agreements between LA and Asia countriesTrade agreements between LA and Asia countriesTrade agreements between LA and Asia countriesTrade agreements between LA and Asia countries

TailandiaTailandiaTailandiaTailandia

P.C. de P.C. de P.C. de P.C. de TaiwánTaiwánTaiwánTaiwán

CoreaCoreaCoreaCoreaChinaChinaChinaChina

BruneiBruneiBruneiBruneiSingapurSingapurSingapurSingapur

Nueva Nueva Nueva Nueva ZelandaZelandaZelandaZelanda

IndiaIndiaIndiaIndia

MalasiaMalasiaMalasiaMalasia

ChileChileChileChile

PerúPerúPerúPerú

PanamáPanamáPanamáPanamáMéxicoMéxicoMéxicoMéxico

GuatemalaGuatemalaGuatemalaGuatemala

AustraliaAustraliaAustraliaAustralia

Costa RicaCosta RicaCosta RicaCosta Rica

PerúPerúPerúPerú

ChileChileChileChile

29

Other Initiatives on Asia Pacific

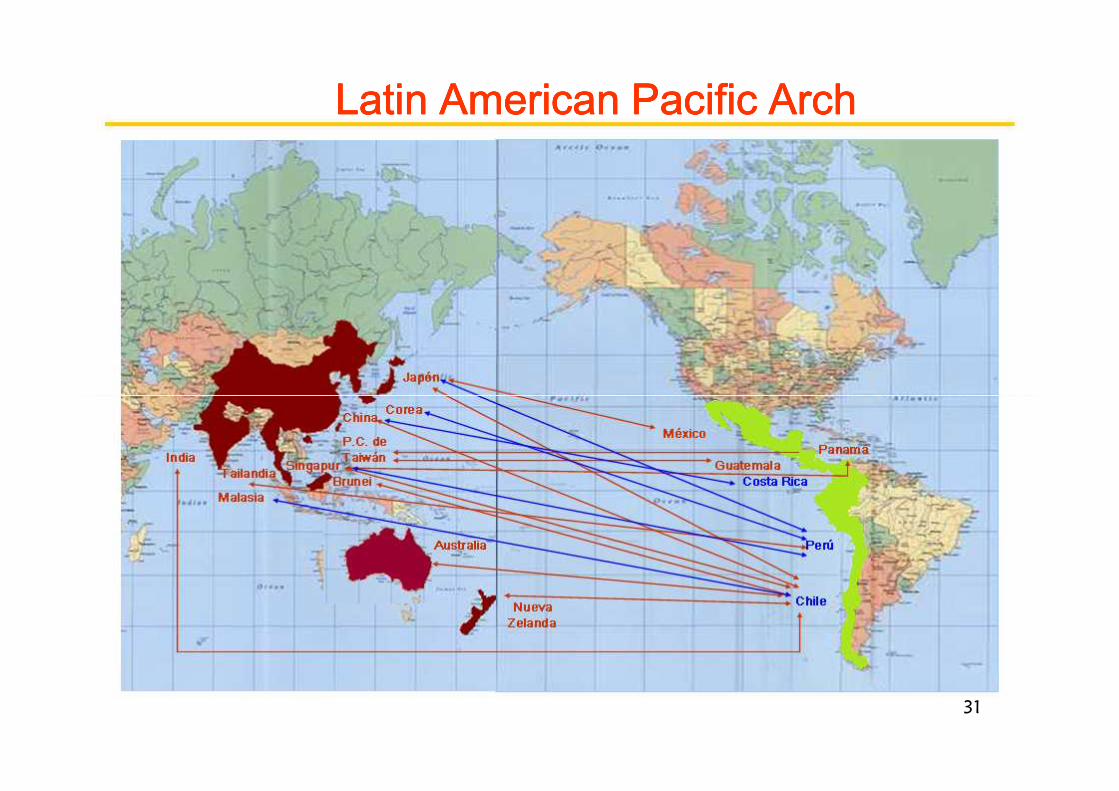

� Latin-American Pacific Arch is a good initiative

� 11 countries: Colombia, C. Rica, Chile, Ecuador, El Salvador, Guatemala, Honduras, Mexico, Nicaragua, Panama and Peru

� Except Ecuador, 10 countries with FTA with US

� The idea: to strengthen the linkage with Asia Pacific, reinforcing the owns linkages within the region

� 4 working groups� 4 working groups

� Convergence on trade agreements

� Trade Facilitation, Infrastructure and Logistics

� Promotion and Protection of Investments

� Cooperation on Competitiveness

30

Latin American Pacific ArchLatin American Pacific ArchLatin American Pacific ArchLatin American Pacific Arch

31

The US Dilemma: How to deal with

the Chinese connection?

� Moving forward on Doha Round

� Moving pending FTAs in the Congress

� Deepening its economic and trade commitment to Deepening its economic and trade commitment to Latin America

� Put in practice the cooperative relationship with LAC “seeking an equal partnership”

� Advancing on the TPP

32

The TPP: an opportunity to reassert

the leadership of US on world

trading system� US requires flexibility and political will to move Doha

agenda

� World trading system needs leadership to deal with the new issues: trade & climate change; labor, the new issues: trade & climate change; labor, environment; security; private rules and standards

� APEC 2011 (Hawai) and the TPP are excellent opportunities to take up again the initiative

33

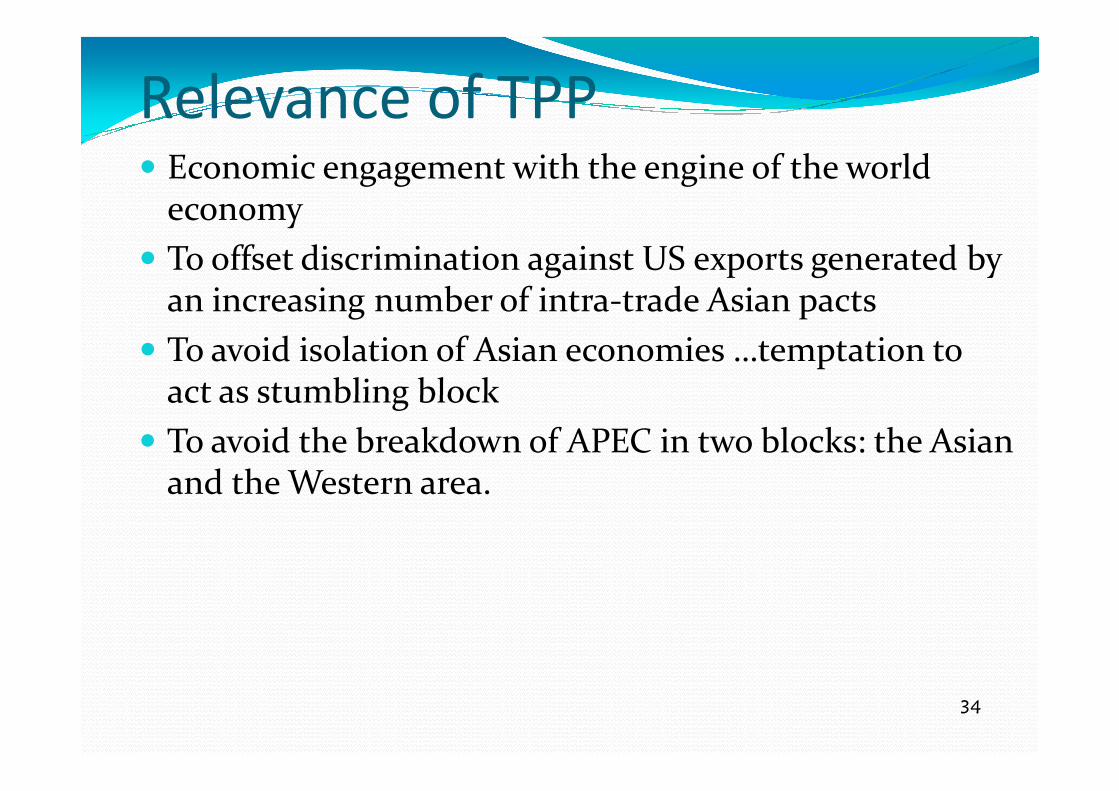

Relevance of TPP� Economic engagement with the engine of the world

economy

� To offset discrimination against US exports generated by an increasing number of intra-trade Asian pacts

� To avoid isolation of Asian economies …temptation to act as stumbling blockact as stumbling block

� To avoid the breakdown of APEC in two blocks: the Asian and the Western area.

34

Challenges for US policy (on TPP

initiative)� To approve the TPA

� To approve pending FTAs (mainly Korea,)

� Significant concessions on agriculture and textile and clothing

� Flexibility on AD

� Less pressure on the new “platinum standard”

� To avoid the bad combination: platinum standard in the new � To avoid the bad combination: platinum standard in the new issues and the tin standard in the traditional issues (agriculture, AD, public procurements, services Mode 4)

35

The challenges for the partners� If US does its homework, then the partners may be available to engage

on the initiative

� The issues

� To start new negotiations on politically sensitive issues, already settled with the US after difficult negotiations (including several non-voluntary changes after the negotiations were formally closed)

� To combine trade arrangements of different scope and depth

� To articulate the TPP with an immense web of preference � To articulate the TPP with an immense web of preference agreements

� If US does not its homework, it will be very difficult to advance in the TPP

36

The Pending Trade Agenda

with LAC� To approve pending FTAs (Colombia, Panama)

� Lower the trade barriers it still maintains to key LAC exports: agriculture, textiles and clothing, ethanol

� Be more forthcoming on the reduction of its agricultural subsidies on Doha RoundDoha Round

� Become more involved in Trade Facilitation and Aid for Trade projects, committing resources, collaborating with its FTA partners: a new way of understanding the administration of the FTAS

� Setting up trade finance squemes to support exporting SME from its FTA partners in the region

� Promoting cumulation of origin across all its FTAs in the region

37

US choices: a) indifference

� Lost opportunities

� Reduced share on LAC and Asian trade

� Loosing leadership

Protectionism against China� Protectionism against China

� No hemispheric initiatives on trade

� China gaining presence on trade and investment

� New international alliances on trade and investment

38

US choices: b) active engagement

� Pushing free trade initiatives on Doha and APEC

� Leading the TPP initiative with pragmatism, flexibility and platinum standard for all the issues

� Promoting origin accumulation among the FTA’s with Canada and LA countries

� Promoting value chains of these countries on business oriented to Asia PacificPacific

� Business and tech alliances with LA partners

� Aid for strategic trade� Administration of FTA’s

� SME’s exports

� Quality certification

� Trazability

� Training work force……� Trade Facilitation

39

Cooperation and integration are necessary to better

address the post-crisis structural problems

� Moving toward an integrated regional market would:o foster productive integration and economies of scaleo enhance the region’s attractiveness internationally

� However, the current political environment in the region does not favor large trade liberalization region does not favor large trade liberalization initiativeso Due to large differences in orientation towards “free trade”o South American FTA project has been put in the backburner

� But differences over trade issues should not impede cooperation in a series of more urgent areas:o Need to look beyond trade

40

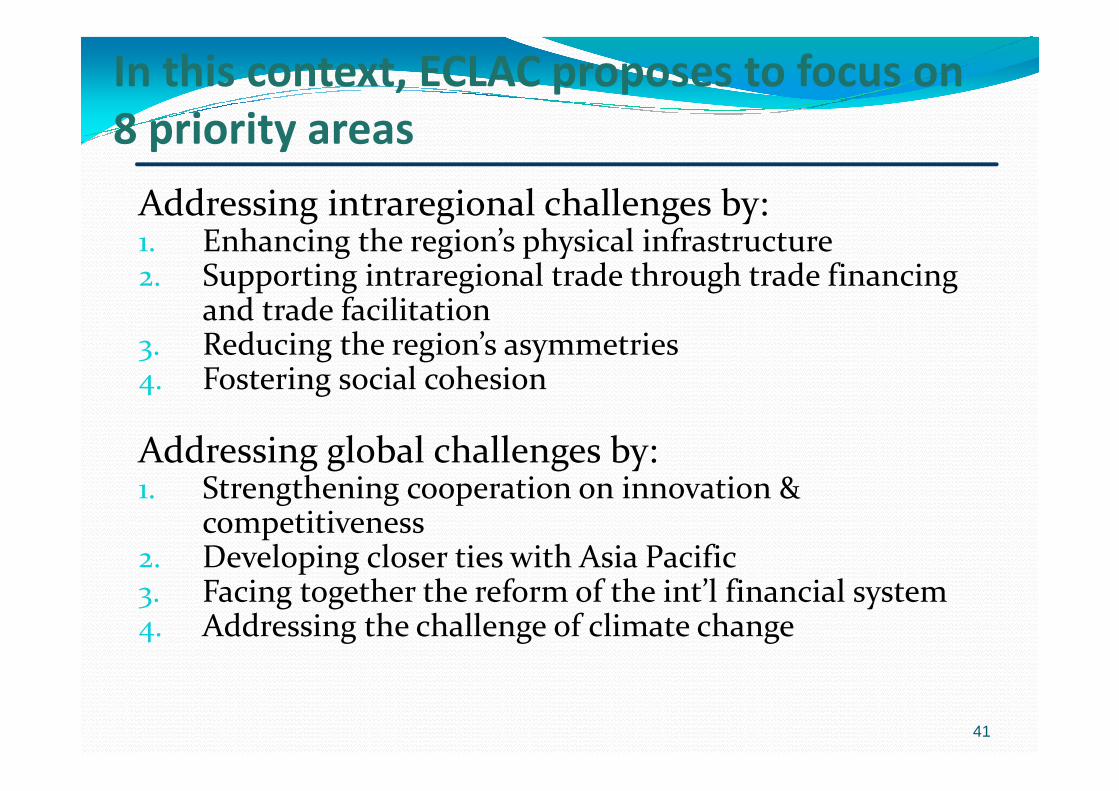

In this context, ECLAC proposes to focus on

8 priority areas

Addressing intraregional challenges by:1. Enhancing the region’s physical infrastructure2. Supporting intraregional trade through trade financing

and trade facilitation3. Reducing the region’s asymmetries4. Fostering social cohesion4. Fostering social cohesion

Addressing global challenges by:1. Strengthening cooperation on innovation &

competitiveness2. Developing closer ties with Asia Pacific3. Facing together the reform of the int’l financial system 4. Addressing the challenge of climate change

41

The new trade policy should address….

� New issueso Labor; environment; security; sanitary and phytosanitary traceability; food

safety; carbon traceability; climate change; certifications; best practices; corporate social responsibility

� Multiple objectiveso Competitiveness-innovation-sustainabilityo Internationalization of firmso Global value chainso Climate change

� Key institutional challenge is to achieve an integrated approach � Key institutional challenge is to achieve an integrated approach comprising the following policy areas:

o Trade o Productive development; Innovation and technological diffusiono FDI o Human resources (education and capacity building)o Environment

� Strengthen the role of the State in two main areas:o Address institutional coordination failureso Foster public-private partnerships for a leap in innovation and

competitiveness

42