oryx petroleum: building an upstream leader in africa … petroleum: an upstream leader in africa...

TRANSCRIPT

ORYX PETROLEUM: AN UPSTREAM LEADER IN AFRICA & THE MIDDLE EAST

Investor Presentation - July 2013

► Seven license areas focused on Africa and Middle East

► Significant recent discovery with further upside • 164 MMbbls proved plus probable reserves ($0.8 billion after-tax

NPV10)

• 200 MMbbls contingent resources ($1.5 billion after-tax NPV10)

► Large prospective oil resource base • 1,318 MMbbls unrisked ($9.0+ billion after-tax NPV10)

► Strong capitalisation • $700 million from The Addax & Oryx Group (AOG): a large private

diversified investment group

• $23 million from management and private investors

• $237 million net proceeds from IPO

► Cash on hand to fund active drilling and seismic program through mid-2014

► Listed on Toronto Stock Exchange (ticker: OXC)

Private and Confidential 2

BUILDING A FULL-CYCLE EXPLORATION, DEVELOPMENT AND

PRODUCTION COMPANY

A sizeable and diverse portfolio focused on highly prospective oil regions

Private and Confidential 3

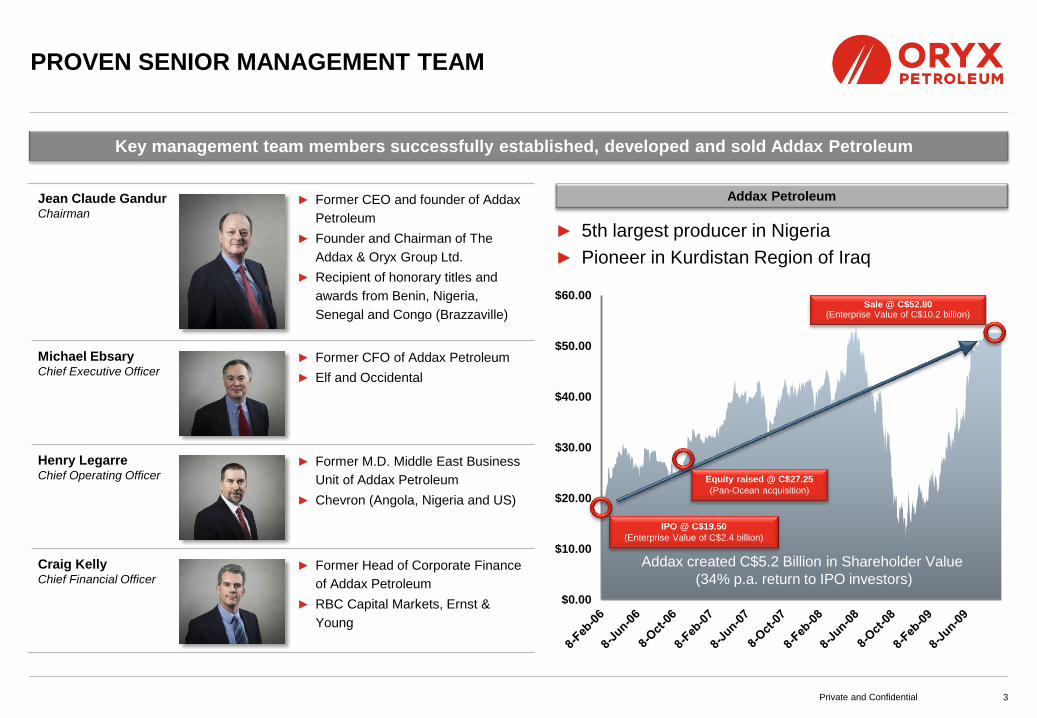

Jean Claude Gandur Chairman

► Former CEO and founder of Addax

Petroleum

► Founder and Chairman of The

Addax & Oryx Group Ltd.

► Recipient of honorary titles and

awards from Benin, Nigeria,

Senegal and Congo (Brazzaville)

Michael Ebsary Chief Executive Officer

► Former CFO of Addax Petroleum

► Elf and Occidental

Henry Legarre Chief Operating Officer

► Former M.D. Middle East Business

Unit of Addax Petroleum

► Chevron (Angola, Nigeria and US)

Craig Kelly Chief Financial Officer

► Former Head of Corporate Finance

of Addax Petroleum

► RBC Capital Markets, Ernst &

Young

PROVEN SENIOR MANAGEMENT TEAM

Key management team members successfully established, developed and sold Addax Petroleum

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

IPO @ C$19.50

(Enterprise Value of C$2.4 billion)

Sale @ C$52.80 (Enterprise Value of C$10.2 billion)

Addax created C$5.2 Billion in Shareholder Value

(34% p.a. return to IPO investors)

► 5th largest producer in Nigeria

► Pioneer in Kurdistan Region of Iraq

Equity raised @ C$27.25

(Pan-Ocean acquisition)

Addax Petroleum

Utilising its technical expertise to extract value and drive the pace of development

► Led by Henry Legarre (COO) • Formerly Managing Director of Addax Petroleum’s

Middle East operations

• Led the development of Taq Taq in Kurdistan

• 20 years with Chevron in Angola, Nigeria and U.S.

► Geologists

► Subsurface engineers

► Drilling / facilities engineers

► Regional operational managers

► New ventures specialists

► Health, safety and environment specialists

Private and Confidential 4

SUBSTANTIAL IN-HOUSE TECHNICAL EXPERTISE

Operational Team of 30+ Professionals Extensive Industry and Country Experience

Algeria Libya Egypt

UAE Qatar

Congo

Angola

Gabon

Saudi

Arabia

Senegal

Guinea

Bissau

Syria Lebanon

Cameroon Ivory

Coast

Tunisia

Ethiopia

Kenya

Tanzania

Iraq

Nigeria

Iraq

► 143 Bnbbls of proved oil reserves

► Kurdistan Region: Accessible emerging basin

► Wasit Province: Early stage opportunities

Nigeria

► 37 Bnbbls of proved oil reserves

► Largest production and resources in West Africa

AGC (Senegal / Guinea-Bissau)

► Working hydrocarbon system

► Overlooked shallow water play capitalizing on

proven seismic technology

Congo (Brazzaville)

► 1.9 Bnbbls of proved oil reserves

► Exploration around large producing fields

► Opportunities for Independents to build presence

Private and Confidential 5

OIL FOCUSED IN ESTABLISHED HYDROCARBON BASINS

Proven Plus Probable Reserves Best Estimate Contingent Resources Best Estimate Unrisked Prospective Resources

431

404

160

243

80

200

Kurdistan

Wasit

Congo

(Brazzaville)

Nigeria AGC

164

Exploring for oil in low geological risk regions

Oryx Petroleum Reserves and Resources (MMbbls)

Private and Confidential 6

DIVERSIFIED AND SIZEABLE ASSET BASE

Multiple play types, high average working interest and large scale opportunities

► Seven license areas covering 10,602 km2

► Multiple play types across different geographies • Onshore, shallow offshore, deepwater

► High equity interests and operatorship • >30% interest in 6 of 7 licenses

• Operator/technical partner in 4 of 7 licenses

► 1.7 billion barrels of reserves and unrisked resources (31/03/2013)

► 100% oil focused • ~80% of prospective resource base is light / medium oil

Hawler

OML141 HMA (MMbbls, WI) 1P/C 2P/C 3P/C

Reserves 59 164 624

CR 81 200 607

PR - Unrisked 530 1,318 3,023

PR - Risked 112 271 604

Private and Confidential 7

SIGNIFICANT NEAR-TERM DRILLING PROGRAM

Recent significant discovery with 14 additional wells planned prior to mid-2014

0

200

400

600

800

1000

Demir Dagh-2

Work

ing In

tere

st (M

Mbbls

)

Zey Gawra-1

Xiang

Ain Al Safra

Gara

Kaki

Dufriyah North

Demir Dagh-4

Nengia

Amedi

Dome Flore

OML-3

Banan

Ma

Demir Dagh-3

Q2 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2013 Q1 2013

Kurdistan, Iraq

Congo (Brazzaville)

AGC

Wasit, Iraq

Nigeria

2C Resources 2P Reserves Prospective Resources (unrisked)

Private and Confidential 8

HAWLER LICENSE (KURDISTAN REGION OF IRAQ)

► February 2013 discovery at Demir Dagh (100%)

• 252 MMbbls 2P reserves (3P: 960 MMbbls)

• 307 MMbbls 2C resources (3C: 933 MMbbls)

• 49 MMbbls unrisked prospective resources

► 3 additional identified prospects targeting light and heavy oil potential:

Work Program

► 2013: 3 more exploration wells (AAS-1, ZEG-1, BAN-1), 1 appraisal

well (DD-3)

► 1H 2014: 1 planned appraisal well (DD-4) with additional appraisal

wells likely

► Initial production facility and first oil expected in 2014

Wells

Planned

Discovery

Successful exploration result to be followed by drilling of three additional prospects in 2013

Working Interests

► 65% Oryx Petroleum (Operator)

► 20% KRG

► 15% KNOC

225

196

23

0

50

100

150

200

250

Ain Al Safra Banan Zey Gawra

Unrisked G

ross (

100

%)

Pro

spective R

esourc

es

Total Gross (100%) Prospective

Resources: 444 MMbbls

(WI: 289 MMbbls)

*

*does not reflect recent extension of license area

Spud: June 2013

Est TD: Oct/Nov 2013

Spud: July 2013

Est TD: Dec/Jan 2014

Spud: April 2013

Est TD: Aug/Sept 2013

Spud: July 2012

TD: Dec 2012

Pre Drill (MMbbls) WI

Post Drill (MMbbls) WI

Proved plus

Probable

Reserves

- 164

Contingent

Resources 79 200

Prospective

Resources 69 32

Private and Confidential 9

HAWLER LICENSE (KURDISTAN REGION OF IRAQ)

729m

80m

?m

Pila Spi

Gercus

Sinjar

Kolosh

Shiranish

Kometan

Qamchuqa & Sarmord

Garagu

Najmah

Naokelekan & Sargelu

Alan

Mus

Adaiyah

Butmah

Baluti

Kurra Chine

▲3711m ▼3768m

▲3488m

▼3711m

▲3322m

▲3302m

▲3026m

▲2953m

▲3768m

▲2223m

▲2107m

▲1766m

▲1757m

▲1638m

▲1305m

▲1190m

▲1137m

▲994m

▼3488m

▼3322m

▼3302m

▼3026m

▼2953m

▼2223m

▼2107m

▼1766m

▼1757m

▼1638m

▼1305m

▼1190m

▼1137m

▼4018m

74m

MD metres

Upper Cretaceous - Shiranish, Kometan, Upper Qamchuqa

• Tested 6,700 bbl/d good viscosity crude oil – classified as heavy (20 to 22°API)

• Sweet crude (Low GOR / H2S)

• Matrix porosity exceeded expectations

Upper Jurassic - Najmah

• Produced fluid at 4,000 bbl/d (10% heavy oil, 90% drilling fluid) (<10° API)

• Results inconclusive

Lower Jurassic / Upper Triassic

Butmah

• Technical issues during open hole testing; Results inconclusive

Kurra Chine

• Not tested

Prospective Resources

Demir Dagh: Significant oil discovery with further upside potential

Middle & Lower Jurassic

Naokelekan & Sargelu

• Produced light oil at surface (29° to 32° API)

• Testing stopped prematurely due to technical issues

Mus & Adaiyah

• Tested 2,210 bbl/d light oil (42° API), Tested 2,780 bbl/d light oil (37° API)

• Testing limited by surface facilities

Contingent Resources

No Reserves or Resources Booked

Reserves & Contingent Resources

263m

TE

RT

IAR

Y

CR

ET

AC

EO

US

JU

RA

SS

IC

TR

IAS

SIC

► NSAI Development assumptions for 2P+2C

(100%):

• $3.8 billion total capex including:

- 148 development wells ($1.8 bn)

- 30 injection wells ($550mm)

- 155 km pipeline to Faysh Khabur ($225 mm)

- Facilities ($1.0 bn)

- Abandonment ($325 mm)

• $10.19 bbl/d opex over life of field (includes $5-10/bbl/d

transportation)

• $10/bbl/d discount to Brent for 2P

• First oil in 2014 and peaking at 219,000 bbl/d

Private and Confidential 10

HAWLER LICENSE (KURDISTAN REGION OF IRAQ)

Demir Dagh Development Planning

Next Steps and Phase 1 Development

► Notification of Discovery delivered to KRG • Next step is Appraisal Plan followed by declaration of

Commercial Discovery and Field Development Plan

► Near-term drilling: • 2 planned appraisal wells (DD-3 & DD-4) in late 2013 / early

2014

• Banan exploration well late 2013

► Tendering for 25,000 bbl/d EPF underway • Expected to be in place by end of 2013

• Lease with total cost of ~$30 million(~$15 million set-up, ~$15 million lease/maintenance costs p.a)

► First Production from DD-2 and DD-3 in 2Q2014 • 7,000 - 9,000 bbl/d(Gross)

► Three rigs to drill throughout 2014 • 25,000 bbl/d by end 3Q 2014

NSAI Development Assumptions

Private and Confidential 11

HAWLER LICENSE (KURDISTAN REGION OF IRAQ)

ITP

40” & 46” pipelines

600 & 900 Mbbl/d capacity

Khurmala – Faysh Khabur

Planned 40” oil pipeline

1 MMbbl/d capacity

Khurmala – Erbil Refinery

20” oil pipeline

150 Mbbl/d capacity

Khurmala – Dohuk

24” gas pipeline

~600 MMcf/d(300Mbbl/d) ► Hawler license area well situated for both

domestic and export sales

► Domestic demand ~200,000 -250,000 bbl/d

• Production capacity estimated >400,000 bbl/d

by end of 2013

• Trucking unable to accommodate excess

capacity

► Two principal export pipeline options both

headed for Ceyhan port in Turkey

1) Via Federal Iraq – Khurmala Dome to ITP

2) Via Kurdistan – Khurmala – Dohuk – Faysh

Khabur

a) Converted gas pipeline (300,000 bbl/d)

b) Proposed 1 MMbbl/d mainline

► Ultimate export routes dependent on

regional politics and security

• Kurdistan, Federal Iraq, Turkey, US

Khurmala Dome > ITP 1

Converted gas pipeline

(300,000 bbl/d) 2a Proposed mainline

(1 MMbbl/d) 2b

Faysh Khabur

► Frontier license area with sizeable structures but high

geological risk

► Light oil prospectivity in multiple reservoirs

► On trend with Tawke field; nearby drilling at Gara-1

(Hillwood/Marathon)

► 1 prospect and 2 leads

Private and Confidential 12

SINDI AMEDI (KURDISTAN REGION OF IRAQ)

Work Program

► 2013: 2D seismic (180km)

► 1H 2014: 2 exploration wells

Wells

Planned

Large exploration area with high potential yet to be fully established

174

99

51

0

40

80

120

160

200

Gara Amedi Yakmalah

Unrisked

Gro

ss (

100%

) P

rospective R

esourc

es

Prospects Leads

Total Gross (100%) Prospective

Resources: 325 MMbbls

(WI: 82 MMbbls)

Working Interests

► 30.94% Perenco (Operator)

► 25.31% Oryx Petroleum

► 25.00% KRG (back in right)

► 18.75% Third Party (back in right)

► Proven active petroleum system: 3 fields under

development with 1.3 Bnbbls of estimated reserves

► Provincial government awarded contracts: right to

nominate up to 3,500 km2 in one or more license areas

► Fiscal terms similar to 2007 vintage KRG PSCs

Private and Confidential 13

WASIT (IRAQ)

► 2013: 2D seismic (540 km)

► 1H 2014: 1 exploration well

Wells

Planned

CNPC

Gazprom

Work Program

Unique early stage oil opportunity in large underexplored and underdeveloped Shia province

344

285

213

100 68

0

80

160

240

320

400

Wasit West Wasit Central Dhufriya North Sa'd Wasit East

Unrisked

Gro

ss (

100%

) P

rospective R

esourc

es

Working Interests

► 40% Oryx Petroleum (Operator)

► 40% Other shareholders of KPA / Amira Hydrocarbons

► 20% WPG

Total Gross (100%) Prospective

Resources: 1,010 MMbbls

(WI: 404 MMbbls)

Leads

► 2013: 3D seismic acquired, 3 exploration wells (XIA-1, MA-1, Kaki Main)

• XIA-1 spudded in May 2013

Work Program

► 890 km2 in 200 – 1,200m water depth

► 5 prospects and 11 leads identified targeting 625 MMbbls best

estimate unrisked gross (100%) prospective resources (WI:

160 MMbbls)

► Heavy (Tertiary) and light (Cretaceous) oil potential

► 3 prospects to be drilled in 2013

• Xiang Prospect: Excellent reservoir quality and with heavy oil

encountered in prior shallow drilling – 86 MMbbls (risked: 39 MMbbls)

• Ma Prospect: Good reservoir quality and biodegraded oil encountered in

prior shallow drilling – 70 MMbbls (risked: 7 MMbbls)

• Kaki Main Prospect: Cretaceous carbonate play – 121 MMbbls (risked:

39 MMbbls)

► On trend with neighbouring large discoveries

• Moho Bilondo & N’kossa - >100,000 bbl/d

• Chevron: Block 14 (Angola) - 200,000 bbl/d

Private and Confidential 14

HAUTE MER A & HAUTE MER B (CONGO (BRAZZAVILLE))

Haute Mer A (WI) Haute Mer B (WI)*

* Pending Final Government Approval.

Wells

Planned

Exploration for oil adjacent to large producing fields

► 20% Oryx Petroleum

► 45% CNOOC (Operator)

► 20% CPC

► 15% SNPC

► 30.00% Oryx Petroleum

► 34.62% Total (Operator)

► 20.38% Chevron

► 15.00% SNPC

Spud: Nov/Dec 2013

Est TD: Jan/Feb 2014

Spud: July/Aug 2013

Est TD: Sept/Oct 2013

Spud: May 2013

Est TD: June/July 2013

Private and Confidential 15

AGC SHALLOW (SENEGAL / GUINEA BISSAU)

► Working petroleum system with two shallow heavy oil

discoveries in the 1960s (500 - 1000 MMbbls in place)

► Deeper targets prospective for lighter oil facilitated by

proven seismic technology

► Sub-salt related structural traps in ≤ 100m water depth

• Analogous to a play on Gulf of Mexico shelf

► 3 prospects and 2 leads identified to date

► 2013: Interpreting 800 km2 3D seismic acquired in Q4 2012 and well

location selection

► 1H 2014: 1 exploration well

Wells

Planned

Significant light oil potential with hydrocarbon system established by discovered heavy oil

Work Program Working Interests

► 80% Oryx Petroleum (Operator)

► 20% AGC

151

45 35 39 35

0

32

64

96

128

160

Dome Flore Dome Gea Dome Iris Dome B Dome A

Prospects Leads

Unri

ske

d G

ross (

10

0%

)

Pro

sp

ective

Reso

urc

es

Total Gross (100%) Prospective

Resources: 304 MMbbls

(WI: 243 MMbbls)

► 1,295 km2 in 0 - 30m water depth

► Numerous prospects identified

► 6 light oil prospects included in NSAI Report representing

Gross (100%) Prospective Resources: 397 MMbbls (WI

153 MMbbls)

► Recently completed drilling of Dila prospect (DIL-1)

• Gross (100%) unrisked Prospective Resources: 189 MMbbls (WI

73 MMbbls)

• Oil discovered but not in commercial quantities

► Significant opportunities remain

• Sizeable prospect inventory

• Large area with no prior drilling or 3D seismic coverage

Private and Confidential 16

OML141 (NIGERIA)

► 2013: 3D seismic acquisition

► 1H 2014: 1 exploration well, 1 appraisal well

Large underexplored license area within the prolific Niger Delta

Work Program Working Interests

► 38.67% Oryx Petroleum (Technical Partner)

► 33.00% Emerald Energy Resources Limited (Operator)

► 27.00% AMNI Oil & Gas

► 01.33% Bluewater Oil & Gas Investment

3D Seismic

Private and Confidential 17

PORTFOLIO WITH SIGNIFICANT VALUE POTENTIAL

High value portfolio anchored by Demir Dagh discovery

Risked Net Present Values (NSAI)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2P 2C PR 2P 2C PR 2P 2C PR

HMA/HMB

AGC

OML141

Wasit

Sindi Amedi

Hawler PR

Hawler 2C

Hawler 2P

► Assumes share price of C$14.25 per share,

1.05USD/CAD and net cash of $483 mm

► 2P+ 2C: ~15% avg. recovery rate

► Prospective Resources: ~20% avg. recovery rate and

19% geologic risking

► Oil Price Assumption (Brent)

• $100 bbl/d Brent in 2015 escalating to $109 in 2021; 2%

production escalation after 2021

• $10 differential for 2P

► Key factors not reflected in NPVs

• Banan extension

• Potential connection between Demir Dagh and Banan

• No low API(<15°) heavy oil in Demir Dagh (Hawler) and

AGC or any natural gas

► Current market value implies large discount to NSAI

NPV 2P+2C at 15-20% discount rates

10% Discount Rate 15% Discount Rate 20% Discount Rate

Ent Value $875mm

Private and Confidential 18

WELL FUNDED TO MEET NEAR TERM REQUIREMENTS

* Pending Final Government Approval.

2013 Capital Budget ($ mm)

Location License Drilling

Seismic

&

Studies Other Total

Iraq

Kurdistan

Region

Wasit Province

Hawler 120 4 6 130

Sindi Amedi 16 5 4 25

Wasit 1 22 9 32

Nigeria OML141 30 12 20 62

Senegal AGC Shallow 3 2 1 6

Congo (Brazzaville) Haute Mer A 46 1 2 49

Haute Mer B* 7 4 9 20

Corporate — — 1 1

Total 224 49 52 325

Exploration and appraisal program fully funded through mid-2014

69%

16%

15%

Drilling

Other

Seismic

& studies

Planned Use of 2013 $325 Million

Capital Budget

$mm

Mar 31/13 cash 246

IPO net proceeds 237

483

Balance of 2013 & 1H 2014:

Capital expenditures 408

G&A/business development 28

Balance 47

1. Focused on oil in established hydrocarbon

basins

• Large license areas

• Large scale resources

2. Sizeable and diversified portfolio with significant

near-term drilling program

• Recent significant discovery

• Variety of plays

• Significant working interests / Operator

• Well funded

3. Experienced management team with strong

relationships and successful track record

• Established through Addax Petroleum

4. Substantial in-house technical expertise

Private and Confidential 19

A COMPELLING INVESTMENT OPPORTUNITY

Demir Dagh

APPENDIX

Private and Confidential 20

Private and Confidential 21

COMMITMENT TO STRONG CORPORATE GOVERNANCE,

CORPORATE INTEGRITY AND SOCIAL RESPONSIBILITY

Experienced and professional board with six independent directors

Board of Directors Our Commitments

Member Experience Independent Good Governance a Corporate Priority

Jean Claude Gandur

Chairman

Founder and Chairman of AOG

Former CEO of Addax Petrolelum –

► Fully independent Corporate Governance and

Audit Committees

► Anti-Corruption policy and supporting processes

Active CSR Program

► Disaster relief in Senegal and Congo (Brazzaville)

► Community outreach in Kurdistan (education,

schools, health services)

► $40m funding and organisational support for

regional flagship Children’s Hospital in Erbil

Michael Ebsary

Chief Executive Officer

Former CFO of Addax Petroleum

Elf and Occidental –

Rick Alexander

Lead Independent Director

Parallel Energy, Alta Gas, Niko Resources,

Husky Oil, Gulf Canada

David Codd Addax Petroleum, Texaco, ConocoPhillips

Michel Contie Total, John Wood Group

Evan Hazell HSBC, Citi, Harrison Lovegrove, RBC,

Canadian Occidental

Gerry Macey Encana, PanCanadian, Addax Petroleum,

PanOrient, Gran Tierra Energy

Peter Newman Deloitte, Arthur Andersen, Mobil Corporation

Field / Prospect

(Region) Activity Well

2013 2014

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Hawler (Kurdistan, Iraq)

Exploration Hawler – DD-2

Exploration Hawler – ZEG-1

Exploration Hawler – AAS-1

Appraisal Hawler – DD-3

Exploration Hawler – BAN-1

Appraisal Hawler DD-4

Seismic Acquisition

Sindi Amedi (Kurdistan, Iraq)

Exploration Sindi Amedi – 2

Exploration Sindi Amedi – 3

Seismic Acquisition

Wasit (Wasit, Iraq)

Exploration Wasit – 1

Seismic Acquisition

OML 141 (Nigeria)

Exploration OML 141 – DIL-1

Appraisal* OML 141 – OML-3

Exploration OML 141 – OML-2

Seismic Acquisition

AGC (AGC Shallow)

Exploration AGC – 1

Haute Mer A (Congo Brazzaville)

Exploration HMA – XIA-1

Exploration HMA – MA-1

Haute Mer B** (Congo Brazzaville)

Exploration HMB – 1

Seismic Acquisition

Private and Confidential 22

DEFINED ACTIVE NEAR-TERM DRILLING PROGRAM

* Appraisal well is based upon successful exploration drilling.

WELL SPUD EXPECTED COMPLETION SEISMIC ACQUISITION

** Pending Final Government Approval.

16 well exploration and appraisal program fully funded provides near-term catalysts

Private and Confidential 23

PROPERTY SUMMARY

Location License Area (km2) Water Depth

(metres) W.I. (%)

Operator/

Technical

Partner

Iraq

Kurdistan

Region

Wasit

Province

Hawler 1,643 Onshore 65.00

Sindi Amedi 1,574 Onshore 33.75

Wasit 3,500 Onshore 40.00

Nigeria OML141 1,295 0-30 38.67

AGC (Senegal /

Guinea Bissau) AGC Shallow 1,700 0-100 80.00

Congo

(Brazzaville)

Haute Mer A 488 350-1,200 20.00

Haute Mer B 402 150-1,075 30.00

Total 10,602

Private and Confidential 24

RESERVES & CONTINGENT RESOURCES (31/03/2013)

Heavy Oil Reserves (Mbbl) Future Net Revenue After Taxes (MM$)

Gross(2)

(100%)

Company Interest Discounted

at 0%

Discounted

at 5%

Discounted

at 10%

Discounted

at 15%

Discounted

at 20% Category Gross Net(1)

Proved (1P) 91,329 59,364 23,395 589 419 296 205 136

Proved + Probable (2P) 252,165 163,907 50,766 1,570 1,122 815 598 439

Proved + Probable + Possible (3P) 960,338 624,219 160,336 5,912 3,306 1,996 1,263 817

(1) Net reserves are Oryx Petroleum’s share of oil production after PSC deductions.

(2) Gross oil reserves are based on commercially recoverable volumes within the life of the PSC.

Unrisked(1) Contingent Oil Resources Unrisked Net Contingent Cash Flow(2) (MM$)

Light / Medium Oil (Mbbl) Heavy Oil (Mbbl) After Taxes

Category Gross(2) Company

Gross Net(3) Gross(2) Company

Gross Net(3) Discounted

at 0%

Discounted

at 5%

Discounted

at 10%

Discounted

at 15%

Discounted

at 20%

Low Estimate (1C) 12,943 8,412 2,999 111,112 72,223 25,744 988 795 642 519 418

Best Estimate (2C) 65,284 42,437 13,471 241,901 157,236 49,912 2,338 1,827 1,451 1,166 947

High Estimate (3C) 335,372 217,992 66,150 598,122 388,779 117,976 7,441 5,050 3,576 2,612 1,952

(1) Contingent resources have not been adjusted for risk based on the chance of commercial development.

(2) Does not include net contingent cash flow for gas because there is no existing gas market for these properties.

(3) Net contingent resources are Oryx Petroleum’s share of oil production after PSC deductions.

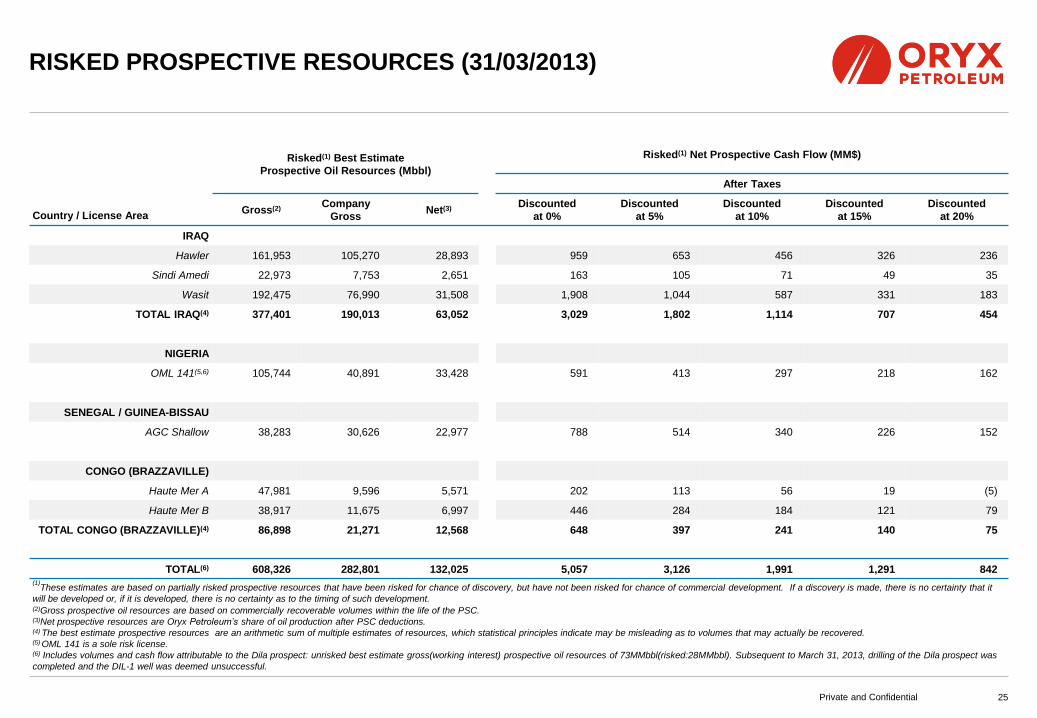

Risked(1) Best Estimate

Prospective Oil Resources (Mbbl)

Risked(1) Net Prospective Cash Flow (MM$)

After Taxes

(1)Gross(2) Company

Gross (2)Net(3)

Discounted

at 0%

Discounted

at 5%

Discounted

at 10%

Discounted

at 15%

Discounted

at 20% Country / License Area

IRAQ

Hawler 161,953 105,270 28,893 959 653 456 326 236

Sindi Amedi 22,973 7,753 2,651 163 105 71 49 35

Wasit 192,475 76,990 31,508 1,908 1,044 587 331 183

TOTAL IRAQ(4) 377,401 190,013 63,052 3,029 1,802 1,114 707 454

NIGERIA

OML 141(5,6) 105,744 40,891 33,428 591 413 297 218 162

SENEGAL / GUINEA-BISSAU

AGC Shallow 38,283 30,626 22,977 788 514 340 226 152

CONGO (BRAZZAVILLE)

Haute Mer A 47,981 9,596 5,571 202 113 56 19 (5)

Haute Mer B 38,917 11,675 6,997 446 284 184 121 79

TOTAL CONGO (BRAZZAVILLE)(4) 86,898 21,271 12,568 648 397 241 140 75

TOTAL(6) 608,326 282,801 132,025 5,057 3,126 1,991 1,291 842 (1)

These estimates are based on partially risked prospective resources that have been risked for chance of discovery, but have not been risked for chance of commercial development. If a discovery is made, there is no certainty that it

will be developed or, if it is developed, there is no certainty as to the timing of such development. (2)Gross prospective oil resources are based on commercially recoverable volumes within the life of the PSC. (3)Net prospective resources are Oryx Petroleum’s share of oil production after PSC deductions. (4) The best estimate prospective resources are an arithmetic sum of multiple estimates of resources, which statistical principles indicate may be misleading as to volumes that may actually be recovered. (5) OML 141 is a sole risk license. (6) Includes volumes and cash flow attributable to the Dila prospect: unrisked best estimate gross(working interest) prospective oil resources of 73MMbbl(risked:28MMbbl). Subsequent to March 31, 2013, drilling of the Dila prospect was

completed and the DIL-1 well was deemed unsuccessful.

Private and Confidential 25

RISKED PROSPECTIVE RESOURCES (31/03/2013)

This document has been prepared by Oryx Petroleum Corporation Limited (“Oryx Petroleum” or “the Company”) for information purposes only, solely for the use at this presentation and must be treated confidentially by attendees at such presentation and must not be distributed, passed on or otherwise disclosed. This document should be read in conjunction with the supplemented prep prospectus of Oryx Petroleum dated May 8 2013. This presentation contains forward-looking statements which reflect management’s current views with respect to certain future events and financial performance. Examples of such forward-looking statements include, but are not limited to, statements regarding plans, objectives and expectations with respect to existing and future operations; statements regarding the business and financial prospects of the Company; statements regarding the performance characteristics of the Company’s properties, the Company’s potential production levels, exploration work and development plans and the reserve and resource potential of the Company’s license areas; statements regarding anticipated financial or operating performance and cash flows; and statements regarding strategies, objectives, goals and targets. No person should rely on these forward-looking statements because they involve known and unknown risks, uncertainties and other factors which are, in many cases, beyond the control of management and may cause the Company’s actual results, performance or achievements to differ materially from anticipated future results, performance or achievements expressed or implied by such forward-looking statements. Prospective investors should carefully consider, among other things, the cautionary note regarding forward looking statements, the Reserves and Resources advisory, the risk factors and notice to investors set out in the supplemented prep prospectus of Oryx Petroleum dated May 8, 2013. In making the forward-looking statements in this presentation, the Company has also made assumptions regarding the timing and results of exploration activities; the enforceability of the Company’s production sharing contracts and risk exploration contracts; the costs of expenditures to be made by the Company; future crude oil prices; access to local and international markets for future crude oil production, if any; the Company’s ability to obtain and retain qualified staff and equipment in a timely and cost-efficient manner; the political situation and stability in the jurisdictions in which the Company has licenses; the regulatory, legal and political framework governing the production sharing contracts, the risk exploration contracts, royalties, taxes and environmental matters in the jurisdiction in which the Company conducts and will conduct its business and the interpretation of applicable laws; the ability to renew its licenses on attractive terms; the Company’s future production levels; the applicability of technologies for the recovery and production of the Company’s oil resources; operating costs; availability of equipment and qualified contractors and personnel; the Company’s future capital expenditures; future sources of funding for the Company’s capital program; the Company’s future debt levels; geological and engineering estimates in respect of the Company’s resources; the geography of the area in which the Company is conducting exploration and development activities; the impact of increasing competition on the Company; and the ability of the Company to obtain financing, and if obtained, to obtain acceptable terms. Although the Company considers the assumptions that it has utilized to be based on available information, such forward-looking statements are based on a number of assumptions which may prove to be incorrect. The Company or its advisers or representatives accept no obligation to update any forward-looking statements set forth herein or to adjust them to future events or developments. Further, this presentation contains market, price and performance data which have been obtained from Company and public sources. The Company believes that such information is accurate as of the date of this presentation. The information contained in this document has not been independently verified and no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein. None of the Company or any of its affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss whatsoever arising from any use of this document, or its contents, or otherwise arising in connection with this document. The Company has exercised reasonable care in preparing this document (and in confirming that where any information or opinion in this document is from or based on a third party source, that the source is accurate and reliable). However, to the fullest extent permitted by law, the Company, its affiliates, advisors and representatives make no representation or warranty, express or implied, nor will they bear responsibility or liability as to the fairness, accuracy, adequacy, completeness or correctness of this document (including information provided by third parties), nor as to the reasonableness of projections, targets, estimates or forecasts nor as to whether any such projections, targets, estimates or forecasts are achievable. Nothing in this document constitutes or should be relied upon by a recipient or its advisors as a promise or representation as to the future or as to past or future performance. The Company reserves the right to terminate discussions with any recipient in its sole and absolute discretion at any time and without notice. No person is authorised to give any information or to make any representation not contained in and not consistent with this document and any such information or representation must not be relied upon and has not been authorised by or on behalf of the Company. Past performance is not necessarily indicative of future results. This presentation is for information only and nothing in this presentation is intended as, or constitutes an advertisement, offer, invitation or solicitation to purchase or sell any Oryx Petroleum securities and neither it nor part of it shall form the basis of, or be relied upon in connection with, any contract or commitment whatsoever. No investment decision should be made on the basis of the information contained in this document. This presentation is not an offer of securities for sale or any solicitation to buy or sell Oryx Petroleum securities in the United States of America. Securities may not be offered or sold in the United States of America absent registration or an exemption from registration under the US Securities Act of 1933, as amended. This presentation and its contents are confidential and may not be reproduced, redistributed or passed on directly or indirectly to any other person or published, in whole or part, for any purpose and it is intended for distribution in the United Kingdom only to: (i) persons who have professional experience in matters relating to investments falling within Article 19(5) of The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, “the Order”; or (ii) persons falling within Article 49(2)(a) to (d) of the Order; or (iii) to those persons to whom it can otherwise be lawfully distributed (all such persons together being referred to as “relevant persons”). This presentation is directed only at relevant persons and must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this communication relates is available only to relevant persons and will be engaged in only with relevant persons. The information in this presentation is given in confidence and the recipients of this presentation should not base any behaviours in relation to qualifying investments or relevant products, as defined in the Financial Services Markets Act 2000, or FSMA, and the Code of Market Conduct, made pursuant to the FSMA, which would amount to market abuse for the purposes of the FSMA on the information in this presentation until after the information has been made generally available. Nor should the recipient use the information in this presentation in any way that would constitute “market abuse”. This document is given in conjunction with an oral presentation and should not be taken out of context. Additional information about Oryx Petroleum is available on Oryx Petroleum`s profile at www.sedar.com

Private and Confidential 26

DISCLAIMER