organizational performance by gregg schoppman, fmi … · length feature article. feature articles...

TRANSCRIPT

TH

E

THE OFFICIAL EDUCATIONAL JOURNAL OF THE AMERICAN SUBCONTRACTORS ASSOCIATION

ASA’s

WWW.ASAONLINE.COM JULY 2017

Cash Management

AMERICAN

ASSOCIATIONSUBCONTRACTORS

TM

Connecting the Dots: Utilizing Key Performance Indicators to Drive Organizational Performance by Gregg Schoppman, FMI

The Future of Payments in Construction: Pay Me on the Blockchain! by James L. Salmon, Esq., Benjamin, Yocum & Heather, LLC

Long Live the King! Why Your Company Needs Cash Flow Reporting by Steve Antill, Foundation Software

Improving Your Cash Flow: The Art of Billings & Collections by Stephane McShane, Maxim Consulting Group

Four Top Strategies to Retain and Motivate Key Employees by Mark Steranka, Moss-Adams, LLP

How Your Client’s Creditworthiness and Ability to Pay Can Impact Your Bottom Line by Scott Applegate, CapitalPlus Equity

Legally Speaking: Do We Have a Deal? Avoiding Handshakes (and Litigation) in Contracting by Lauren McLaughlin, Esq., Briglia McLaughlin, PLLC

SAVE THE DATE!February 28 – March 3, 2018

TEMPE MISSION PALMS HOTEL & CONFERENCE CENTER | TEMPE, AZ

TH

E

ASA’s July 2017

Quick Reference

ASA/FASA CALENDAR ............................................................................................25

COMING UP ................................................................................................................. 25

EDITORIAL PURPOSEThe Contractor’s Compass is the monthly educational journal of the Foundation of the American Subcontractors Association, Inc. (FASA) and part of FASA’s Contractors’ Knowledge Network. The journal is designed to equip construction subcontractors with the ideas, tools and tactics they need to thrive.

The views expressed by contributors to The Contractor’s Compass do not necessarily represent the opinions of FASA or the American Subcontractors Association, Inc. (ASA).

EDITORIAL STAFFEditor-in-Chief, Marc Ramsey

MISSIONFASA was established in 1987 as a 501(c)(3) tax-exempt entity to support research, education and public awareness. Through its Contractors’ Knowledge Network, FASA is committed to forging and exploring the critical issues shaping subcontractors and specialty trade contractors in the construction industry. FASA provides subcontractors and specialty trade contractors with the tools, techniques, practices, attitude and confidence they need to thrive and excel in the construction industry.

FASA BOARD OF DIRECTORSRichard Wanner, President Letitia Haley Barker, Secretary-Treasurer Brian Johnson Robert Abney Anne Bigane Wilson, PE, CPC

SUBSCRIPTIONSThe Contractor’s Compass is a free monthly publication for ASA members and nonmembers. Subscribe online at www.contractorsknowledgedepot.com.

ADVERTISINGInterested in advertising? Contact Richard Bright at (703) 684-3450 or [email protected] or [email protected].

EDITORIAL SUBMISSIONSContributing authors are encouraged to submit a brief abstract of their article idea before providing a full-length feature article. Feature articles should be no longer than 1,500 words and comply with The Associated Press style guidelines. Article submissions become the property of ASA and FASA. The editor reserves the right to edit all accepted editorial submissions for length, style, clarity, spelling and punctuation. Send abstracts and submissions for The Contractor’s Compass to [email protected].

ABOUT ASAASA is a nonprofit trade association of union and non-union subcontractors and suppliers. Through a nationwide network of local and state ASA associations, members receive information and education on relevant business issues and work together to protect their rights as an integral part of the construction team. For more information about becoming an ASA member, contact ASA at 1004 Duke St., Alexandria, VA 22314-3588, (703) 684-3450, [email protected], or visit the ASA Web site, www.asaonline.com.

LAYOUTAngela M Roe [email protected]

© 2017 Foundation of the American Subcontractors Association, Inc.

FeaturesTM

Departments

CONTRACTOR COMMUNITY .................................................................................. 4

LEGALLY SPEAKING ................................................................................................23Do We Have a Deal? Avoiding Handshakes (and Litigation) in Contractingby Lauren McLaughlin, Esq., Briglia McLaughlin, PLLC

Connecting the Dots: Utilizing Key Performance ................................. 8 Indicators to Drive Organizational Performance by Gregg Schoppman, FMI

The Future of Payments in ...................................................................10 Construction: Pay Me Pay Me on the Blockchain! by James L. Salmon, Esq., Benjamin, Yocum & Heather, LLC

Long Live the King! Why Your Company ..............................................14 Needs Cash Flow Reporting by Steve Antill, Foundation Software

Improving Your Cash Flow: The Art of Billings & Collections ..............16 by Stephane McShane, Maxim Consulting Group

Four Top Strategies to Retain and Motivate Key Employees ................19 by Mark Steranka, Moss-Adams, LLP

How Your Client’s Creditworthiness and Ability to ............................ 21 Pay Can Impact Your Bottom Line by Scott Applegate, CapitalPlus Equity

J U L Y 2 0 1 7 T H E C O N T R A C T O R ’ S C O M P A S S4

Civil Engineers Give Nation’s Infrastructure a D+

Although there has been some incremental progress toward restoring the nation’s infrastructure, it has not been enough, according to the American Society of Civil Engineers. As in 2013, the United States’ cumulative GPA for infrastructure is once again a D+. The 2017 grades range from a B for Rail to a D- for Transit, illustrating the clear impact of investment—or lack thereof—on the grades.

Three categories—Parks, Solid Waste, and Transit—received a decline in grade this year, while seven—Hazardous Waste, Inland Waterways, Levees, Ports, Rail, Schools, and Wastewater—saw slight improvements. Six categories’ grades remain unchanged from 2013—Aviation, Bridges, Dams, Drinking Water, Energy, and Roads.

ASCE has published its Infrastructure Report Card, which grades the current state of national infrastructure categories on a scale of A through F, since 1998. Since then, America’s infrastructure has earned persistent D averages, and the failure to close the investment gap with needed maintenance and improvements has continued. Even though the U.S. Congress and some states have recently made efforts to invest more in infrastructure, these efforts do not come close to what ASCE estimates is a $2 trillion need. ASCE estimates that to raise the overall infrastructure grade and maintain the country’s global competitiveness, Congress and the states must invest an additional $206 billion each year to prevent the economic consequences to families, business, and the economy.

Death by Contract: Design Disclaimers

A design disclaimer can come in many forms, but essentially, it is a statement in a contract that means “this part of the design might not be good enough.” When a contract or a subcontract contains a design disclaimer, it shifts the design risk to the contractor or subcontractor, whether or not a design-build warranty was supposed to be part of the deal.

From a financial standpoint, a design disclaimer amounts to the same thing as a design-build warranty, because both make the contractor or subcontractor responsible for increased costs should the design prove inadequate. For example, a Washington, D.C.-area contractor learned an expensive lesson about contractual design disclaimers when it spent twice its bid amount to complete a subway station. After an inconsistency between the final bid package and the resulting requirements, the winning contractor discovered that the design was inadequate and sued to recover for the resulting extra costs. The owner disclaimed its warranty of the design in the contract, effectively putting the contractor in the position of warranting the design. However, a court decision found that the contactor “had a duty to inquire about the true meaning of the contract.” The court also found that: “By failing to inquire, the contractor assumed the risk that the owner would offer reasonable but conflicting interpretation.” This is an example of a design-bid-build, lump-sum contractor, not involved with the design, assuming responsibility for cost overruns caused by design changes.

To make its case, the contractor might have pointed to industry best practices described in the Guidelines for a Successful Construction Project, developed and published by ASA, the Associated General Contractors of America and the Associated Specialty Contractors. The “Guideline on Design Responsibility” provides:

“Contractors and subcontractors must not be held responsible for the adequacy of the performance or design criteria indicated by the contract documents.”

Perhaps the best way to guard against design disclaimers is with a contract addendum that incorporates your bid proposal. For example, the ASA Subcontract Addendum provides:

2. Scope of Work. Subcontractor’s scope of work includes only the following:

[Insert your scope and pricing information below. Many subcontractors may wish to substitute a different format.]

WORK CATEGORY(IES) AND SPECIFICATIONS TO WHICH THIS ADDENDUM APPLIES:

EXCLUDING, HOWEVER:

Subcontractor’s obligation to examine documents, the project site, and materials and work furnished by others is limited to notification of Customer of any defects or deficiencies that a person in the trade of Subcontractor would discover by reasonable visual inspection. No testing beyond reasonable visual inspection shall be required. Subcontractor is entitled to rely on the accuracy and completeness of plans, specifications and reports of site conditions provided to Subcontractor.

CONTRACTOR COMMUNITY

T H E C O N T R A C T O R ’ S C O M P A S S J U L Y 2 0 1 7 5

Any design services provided by Subcontractor will be reviewed by Designer to assure acceptability when integrated with the entire work. Customer is entitled to rely on the accuracy and completeness of design services or certifications provided by Subcontractor only to the extent that design responsibility is specifically delegated to Subcontractor by agreement in writing and all design and performance criteria are furnished to Subcontractor. A change in the price of an item of material of more than 5% between the date of subcontractor’s bid proposal and the date of installation shall warrant an equitable adjustment in the subcontract price.

Coupled with a bid proposal that specifically describes the work on which your bid is based, the ASA addendum shifts design risk back where it belongs, to the party who hired the design professionals. The ASA Subcontract Addendum is part of the ASA Subcontract Documents Suite, which is available at no cost to ASA members on the ASA Web site at www.asaonline.com.

Government List of Sureties Serves Many Purposes

The federal government “screens” the surety bond companies that are permitted to provide bonds, or to reinsure bonds, for federal construction projects. This may seem like a piece of trivia to contractors that do not perform much construction for the federal government. However, specialty contractors can be required in a variety of contexts, inside and outside of the sphere of federal construction, to qualify for bonding by one of these “approved” sureties, and so should be aware of this select group of sureties and some of the circumstances under which they might need to meet the sureties’ exacting requirements.

Specialty contractors that work as prime contractors on larger federal projects are already familiar with the U.S. Department of the Treasury’s list of approved sureties, since federal regulations require prime contractors on these projects to obtain a performance and payment bonds from a surety on the list. Federal law requires performance bonds on all prime contractors’ work on federal construction work valued at $150,000 or more.

Rather than judge the integrity of bonds on a case-by-case basis, the Bureau of the Fiscal Service of the Treasury Department compiles the Listing of Approved Sureties, a list of surety companies that it has examined and specifically judged to be financially sound for the purposes of insuring or re-insuring bonds. BFS continually monitors the financial status of companies approved for inclusion on the circular, and amends the circular as needed. BFS thus helps protect the federal government’s investment in construction by “screening” surety companies to ensure that they are capable of completing federal projects and/or paying subcontractors and suppliers should a bond be called.

Because only a surety on the list can bond federal construction, sureties seek to qualify for the list. After all, qualification means entry into a bond market covering billions of dollars’ worth of construction. A key point for contractors that do not perform much federal construction, or much public work at all, is that other entities use the list developed by BFS as a resource to protect their investments. Some state and local governments that desire the same level of security as the federal government, and even some private contractors, may ask for Treasury-approved bonding capacity in their bonding requirements.

Some subcontractors encounter the Treasury list of sureties for the first time when a private owner or prime contractor on a relatively small project requires them to qualify for bonding by one of the Treasury-approved sureties. Specialty contractors should be aware that this requirement serves a dual purpose. First, it ensures the financial integrity of the bond and, by extension, the financial ability to perform the bonded subcontract work and to pay suppliers and laborers. Second, owners or prime contractors may impose the requirement to pre-qualify subcontractors that can bid on the project. Because most subcontractors will undergo intense scrutiny of their finances and business operations in order to qualify for the bonds issued by this “select” group of surety companies, owners and prime contractors may impose the requirement to provide an extra layer of assurance that work will be performed according to contract requirements.

Could Arbitration Save You Time and Money?

Arbitration is a binding method to resolve claims among parties before a private arbitrator, rather than a judge or jury in the formal court process. Because mandatory arbitration provisions are common in many construction contracts, a prudent businessperson needs to evaluate whether such an arbitration provision is advisable or not in a certain circumstance.

Generally, arbitration proceedings are conducted under the arbitration rules of the American Arbitration Association or JAMS. A party seeking arbitration of a dispute initiates this procedure by filing a simple Demand for Arbitration with AAA in the regional

CONTRACTOR COMMUNITY

J U L Y 2 0 1 7 T H E C O N T R A C T O R ’ S C O M P A S S6

office and enclosing a filing fee. The fee charged by AAA is based, in part, upon the amount of each claim and the days of hearing. AAA then appoints an arbitrator or a panel of three arbitrators who are supposed to be knowledgeable in this type of dispute or industry to hear the dispute. Arbitrators may be lawyers, but need not be. Once the dispute is heard, the arbitrator(s) make an award within 30 days.

According to Don Gregory, partner with the Columbus, Ohio, law firm of Kegler, Brown, Hill and Ritter, general counsel of ASA, “There is no sure answer as to whether mandatory arbitration is advantageous as each situation depends on the particular facts of that case.”

According to Gregory, there are several practical advantages to arbitration instead of litigation in the courts. One is that arbitrators generally are more knowledgeable in the construction industry than a judge or jury with little or no experience in that area. Second, the arbitration hearing generally is less formal with a more relaxed and informal atmosphere, with more lenient rules of evidence than a court of law. This can be an advantage for individuals who feel uncomfortable in a formal court setting. Third is overall cost and speed. One authority reports that arbitration saves 80 percent of the time and money involved in traditional litigation in the courts.

Gregory advises subcontractors to seriously consider the disadvantages to arbitration. First, the filing fee costs generally are much higher than those to initiate a lawsuit. Second, the fact that there may be no appeal could be a serious detriment to a party who is

unsatisfied with the outcome of an arbitration proceeding, particularly in a sizable dispute. Also, there is the serious practical problem that an arbitration award must be reduced to judgment by filing a lawsuit with the courts before collection efforts can be made to satisfy the judgment. Therefore, the person or company that prevails in arbitration against an entity that refuses to voluntarily pay the arbitration award is faced with having to file a lawsuit anyway to collect the award, which is exactly what the arbitration procedure was supposed to avoid. There is a “privity of contract” problem that occurs with some regularity in complex disputes, in that one can usually only arbitrate with the party with which one contracted. There is no assurance that all parties arguably responsible for the problem are brought into the same forum to avoid inconsistent results. Once again, the intent behind arbitration—to provide a swift, certain and less expensive procedures for dispute resolution—is defeated.

Gregory says, “As a general rule, arbitration can be helpful when dealing with disputes over relatively small amounts in controversy between parties that agree to be bound by the results. Yet arbitration is often counterproductive when dealing with disputes concerning multiple parties and very large amounts in controversy, particularly where there is no assurance that the parties will voluntarily agree to be bound by the result.”

Construction Will Feel Impact of ‘Buy American, Hire American’ Order

On April 19, President Donald Trump signed an executive order initiating an aggressive policy “to buy American and hire American.” “Because the thrust of the E.O. is to direct federal departments and agencies to enforce existing laws and to study and report on the impact of those, it is difficult to predict its ultimate impact,” said ASA Chief Advocacy Officer E. Colette Nelson. The “buy American” policy is focused on federal contractors and subcontractors, including construction. Specifically, the E.O. directs federal agencies to:• “[S]crupulously monitor, enforce,

and comply with Buy American Laws, to the extent they apply, and minimize the use of waivers, consistent with applicable law.”

• Issue guidance to agencies about how to make the assessments and to develop the policies required by the E.O.

• Assess the monitoring, enforcement, implementation and compliance with existing Buy American Laws.

• Assess the use of waivers by type and impact on domestic jobs and manufacturing.

• Develop and propose policies “to ensure that, to the extent permitted by law, Federal financial assistance awards and Federal procurements maximize the use of materials produced in the United States, including manufactured products; components of manufactured products; and materials such as steel, iron, aluminum, and cement.”

T H E C O N T R A C T O R ’ S C O M P A S S J U L Y 2 0 1 7 7

With respect to “public interest waivers from Buy American Laws,” the E.O. states they should be construed “to ensure the maximum utilization of goods, products, and materials produced in the United States, and before granting such a waiver, an agency “must take appropriate account of whether a significant portion of the cost advantage of a foreign-sourced product is the result of the use of dumped steel, iron, or manufactured goods or the use of injuriously subsidized steel, iron, or manufactured goods” and “integrate any findings into its waiver determination as appropriate.” Many federal construction contractors routinely request and obtain public-interest waivers from Buy American requirements.

The construction industry also will be impacted by the E.O.’s “hire American” provisions. The E.O. states that the government’s policy is “to rigorously enforce and administer the laws governing entry into the United States of workers from abroad …” It directs “the Secretary of State, the Attorney General, the Secretary of Labor, and the Secretary of Homeland Security, as soon as practicable, and consistent with applicable law, propose new rules and issue new guidance, to supersede or revise previous rules and guidance if appropriate, to protect the interests of United States workers in the administration of our immigration system, including through the prevention of fraud or abuse.” In addition, it directs these officials to “as soon as practicable, suggest reforms to help ensure that H-1B visas are awarded to the most-skilled or highest-paid petition beneficiaries.” H-1B visas allow U.S. employers to temporarily employ foreign workers in

“specialty occupations,” which includes engineering and architecture.

The new E.O. does not address H-2B visas, which allow U.S. employers to bring in foreign workers to fill temporary non-agriculture jobs, such as construction. ASA will monitor and provide input to federal departments and agencies about the impact of the new E.O. and the resulting regulatory actions on the construction industry.

OSHA Silica Rule Compliance Date Is Sept. 23

Construction contractors with more than 10 employees have until Sept. 23 to comply with OSHA’s rule regulating employee exposure to respirable crystalline silica. Under a rule issued by OSHA on March 25, 2016, construction employers must comply with all requirements of the standard by Sept. 23, except requirements for laboratory evaluation of exposure samples, which begin on June 23, 2018. Earlier, OSHA delayed enforcement of its rule, which requires construction employers to limit worker exposure to silica and to take other steps to protect workers, from June until September.

Crystalline silica is a common mineral found in many naturally occurring materials and used at construction sites. Inhaling very small crystalline silica particles can cause multiple diseases, including silicosis, lung cancer, chronic obstructive pulmonary disease and kidney disease. Respirable silica is generated by high-energy operations like cutting, sawing, grinding, drilling and crushing stone, rock, concrete, brick, block and mortar. Activities such as abrasive blasting with sand; sawing brick or concrete;

sanding or drilling into concrete walls; grinding mortar; and cutting or crushing stone generate respirable dust.

Under the OSHA standard, construction employers can either use a control method, as laid out in Table 1 of the standard, or they can measure workers’ exposure to silica and independently decide which dust controls work best to limit exposures to the permissible exposure limit in their workplaces.

To learn more about OSHA’s silica rule, see the webinar prepared for the Construction Industry Safety Coalition. Access the webinar using the password, CSC4. A hard copy of the webinar slides is available on the ASA Web site. For more information, see the ASA Fact Sheet on OSHA’s Rule on Respirable Crystalline Silica, the ASA Frequently Asked Questions on the OSHA Standard on Respirable Crystalline Silica, and the free ASA video-on-demand, “OSHA Silica Rule—Applications for Subcontractors” (Item #8101), presented by Gary Visscher, Esq., Law Office of Adele L. Abrams, P.C.

ASA, in collaboration with 22 other construction associations, has initiated a lawsuit to prevent OSHA from implementing its rule. In the meantime, ASA urges construction employers to take steps to be in compliance by the OSHA deadline.

CONTRACTOR COMMUNITY

J U N E 2 0 1 7 T H E C O N T R A C T O R ’ S C O M P A S S

Hearing the words “data driven” causes a certain cringe factor. Whether it is the way internet-based compa-nies always seem to know about that snazzy suit you had an eye on or even how they seem to know about the vaca-tion you were seemingly going to book before you booked it, there are count-less stories of firms capturing cus-tomer data, buying proclivities, likes, etc. From the transparent e-commerce site that matches your favorite authors with new authors you might like to the downright subversive businesses that capture your “clicks,” businesses are continuing to mine the treasure trove of data to help further their strategic aims. Now consider the mid-level con-struction organization—what are they measuring? Profitability, safety sta-tistics, collections. Is that enough in today’s world? Do organizations need to up their game and follow their peers across the myriad of industries?

Many firms lament about connect-ing their vision or desired state which is usually some abstract, yet forward reaching, picture with how they are cur-rently structured and operating. For instance, a firm might have a vision or mission such as: “We desire to be the leading specialty contractor in the New England marketplace.”

No one can argue that this hits all of the major bullets relating to text book visions/missions. However, visions/mis-sions often die on the vine when they lack the right objectives or KPIs to drive them further. “Leading,” “superior con-tractor” or “best contractor” are out-standing adjectives and superlatives to define performance, but they do lack a certain specificity. Does leading define market share, productivity, profitability, customer service, strongest team, etc.? All of them may be correct. In some cases, firms use their core values to supply stronger connective tissue to the

goals. However, without objectives or key performance indicators, firms will often languish like a team with a score-board. Ultimately, how does the team know if they are winning?

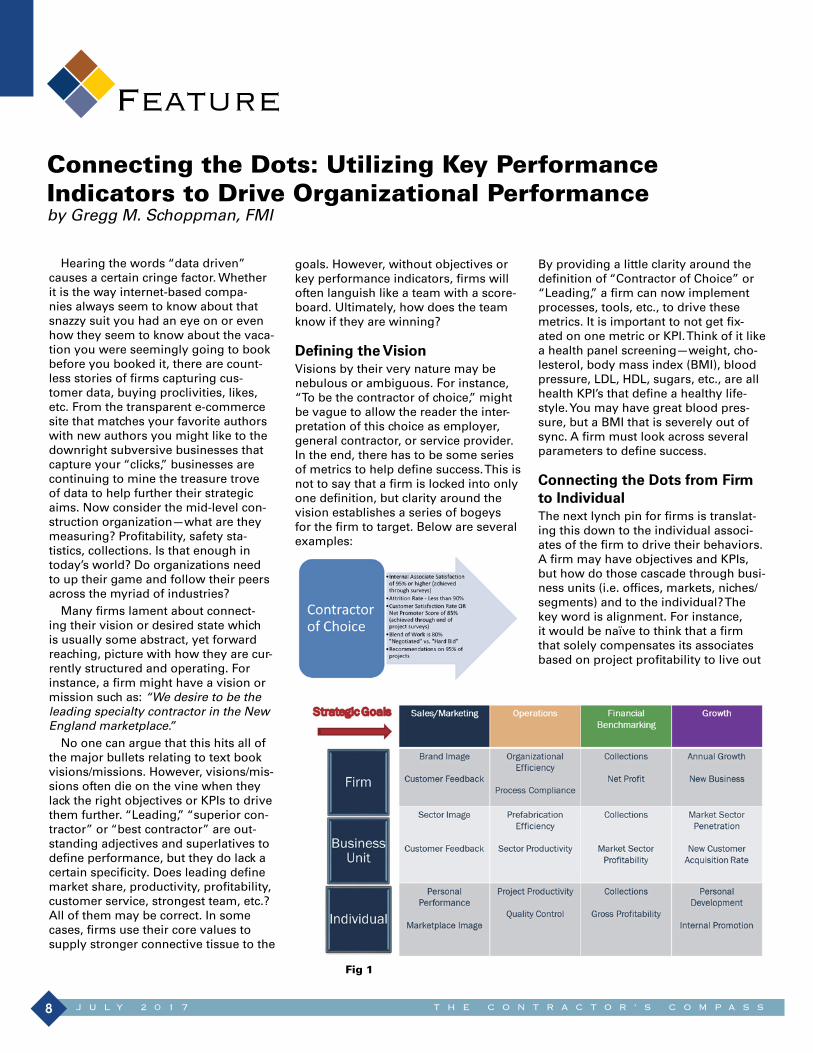

Defining the VisionVisions by their very nature may be nebulous or ambiguous. For instance, “To be the contractor of choice,” might be vague to allow the reader the inter-pretation of this choice as employer, general contractor, or service provider. In the end, there has to be some series of metrics to help define success. This is not to say that a firm is locked into only one definition, but clarity around the vision establishes a series of bogeys for the firm to target. Below are several examples:

By providing a little clarity around the definition of “Contractor of Choice” or “Leading,” a firm can now implement processes, tools, etc., to drive these metrics. It is important to not get fix-ated on one metric or KPI. Think of it like a health panel screening—weight, cho-lesterol, body mass index (BMI), blood pressure, LDL, HDL, sugars, etc., are all health KPI’s that define a healthy life-style. You may have great blood pres-sure, but a BMI that is severely out of sync. A firm must look across several parameters to define success.

Connecting the Dots from Firm to IndividualThe next lynch pin for firms is translat-ing this down to the individual associ-ates of the firm to drive their behaviors. A firm may have objectives and KPIs, but how do those cascade through busi-ness units (i.e. offices, markets, niches/segments) and to the individual? The key word is alignment. For instance, it would be naïve to think that a firm that solely compensates its associates based on project profitability to live out

Connecting the Dots: Utilizing Key Performance Indicators to Drive Organizational Performanceby Gregg M. Schoppman, FMI

J U L Y 2 0 1 7 T H E C O N T R A C T O R ’ S C O M P A S S8

Feature

Fig 1

T H E C O N T R A C T O R ’ S C O M P A S S J U N E 2 0 1 7 9

a vision that espouses customer service, integrity, and team orientation. While there are plenty of altruistic individuals that can do both, the vast majority will maximize personal gain at the expense of the organization leading to a mis-alignment. More importantly, the organ-ization will struggle with credibility and image. How often have we seen a firm talk about the right things in the board-room or only a fancy vision statement poster only to have individuals run amok like renegades on a pirate ship.There must be connective tissue to link each piece of an organization. In Fig. 1, a matrix illustrates potential KPIs that would run through the goals of a firm’s strategic plan:To illustrate the flow, consider the “Operations Goal.” The firm is focused on overall efficiency. As a self-perform-ing, labor-intensive contractor, this should be easy to measure. However, the firm is looking at the major head-ing of “Efficiency.” Within the business unit, they are focused on an element of efficiency, perhaps “Prefabrication for their Commercial HVAC Business Unit.” Lastly, the individual project man-ager or superintendent is tasked with measuring, tracking and adhering to the tenets of productivity through all direct labor on his/her project. All of this when rolled up would subscribe to this contractor achieving its moniker of “Leading contractor (for productivity in the commercial HVAC sector) in the Southern United States.”

Upstream/Downstream KPIs are also multi-dimensional. For instance, the main problem with meas-uring safety and profitability is that they

competition, this visualization was mag-nificent. It also worked well in light of the market (athletic shoes). Now con-sider your team—how do you moti-vate them to light up the scoreboard and achieve their individual and corpo-rate goals? How often do they see the scoreboard? How often are the data updated—put another way, is the team seeing a stale version of the score-card or live, up-to-the-minute results? Ultimately, there needs to be a mecha-nism that will guide the team’s behavior and also demonstrate success. Consider broadcasting the score at corporate meetings, via corporate bulletins, or even with live feeds on televisions throughout an office. There is no sin-gle recipe that works for every firm. The only inalienable truths are transparency of the data, the frequency of the data and the relevancy of the data.There has always been some mysti-cism about KPIs and what they mean to organizations. Some people worry that being a data-driven organization will require countless new overhead resources focused less on building and more on bytes. No one wants “Brand X Construction” to look like Skynet, but smart organizations, or “leading” organization, use the data afforded to them to provide context and more importantly provide direction.As a principal with FMI, Tampa, Fla., Gregg Schoppman specializes in the areas of productivity and project man-agement. He also leads FMI’s project management consulting practice. Prior to joining FMI, Schoppman served as a senior project manager for a general contracting firm in central Florida. He has completed complex and sophisti-cated construction projects in the med-ical, pharmaceutical, office, heavy civil, industrial, manufacturing, and multi-family markets. He has also worked as a construction manager and managed direct labor. Furthermore, Schoppman has expertise in numerous contract delivery methods as well as knowl-edge of many geographical markets. He can be reached at (813) 636-1259 or [email protected].

are often snap shots in time or more importantly a “history lesson.” Last month, there were two lost time inci-dents and the project spent $30,000. KPIs must measure the upstream and the downstream. The same principles apply in the previous health example. Examine the illustration in Fig. 2:

Stepping on the scale every week is the equivalent of looking at the financial statements at the end of the month. It is very important to study a firm’s finan-cials, but isn’t it more important to drive the behaviors that influence a project or firm’s performance? So rather than step-ping on the scale, it is equally as impor-tant to measure one’s diet or exercise/activities. The same could be said for the firm. Measure the processes that drive the vision. Fig. 3 illustrates sev-eral examples of upstream and down-stream KPIs.

Behavioral ModificationThere was a famous management guru that once said, “To manage some-thing, you must measure it.” Striving to become the “leading contractor” is an empty intangible target without some-thing to make it tangible. One of the great vision statements from the last 30 to 40 years was Nike—“Crush Adidas.” While there are not too many exam-ples of contractors publicly trolling their

T H E C O N T R A C T O R ’ S C O M P A S S J U L Y 2 0 1 7 9

Feature

The Future of Payments in Construction: Pay Me on the Blockchain! by James L. Salmon, Esq., Benjamin, Yocum & Heather, LLC

Would you rather get paid today or in six months?

Technology exists to enable payment of pay applications in construction within hours instead of months. If McDonald’s collects at the counter prior to delivery, why not allow trade contractors to collect upon delivery?

This article outlines a futuristic pay processes driven by blockchain technologies on the cloud. Just don’t be surprised if something very close to the process described herein emerges in the marketplace sooner rather than later. But first, a little background.

What Is the Blockchain?Everyone knows about the

internet and the cloud, but what is a blockchain?

A blockchain is an immutable database—usually distributed and networked around the world, via the internet—of secured tamper-resistant digital transactions. Blocks of data on the blockchain contain timestamps and links to previous blocks. Users around the globe connect to the network to send and verify transactions, creating new blocks in the chain.

Self-executing transactions on the blockchain, verified independently by random participants around the globe, reduce the need for trust between parties and enable swift, value-based exchanges on a global scale.

Blockchain 1.0, marked by the rise of Bitcoin and similar digital currencies, began in 2009 when Satoshi Nakamoto published the Bitcoin blockchain code described in his 2008 whitepaper that

introduced the concept1. Ethereum introduced the world to blockchain 2.0 powered by code with Turing capacity, that is the ability to insert logic forks and loops and, ultimately, write self-executing smart contracts on the blockchain2. Today, as blockchain 3.0 unfolds, startups offer Blockchain as a Service, (Baas) Data as a Service (DaaS) on blockchain platforms, Digital Asset Arrays (DAAs) and Distributed Autonomous Applications as a Service (DAAaaS). In short, blockchain offers an innovative new platform for services on the web3.

What Is a Smart Contract?Smart contracts reside on the

cloud as code and self-execute when a triggering event occurs. Online bill payment systems utilize smart contracts. The due date of a bill triggers automatic payment of the bill, electronically, by executing prior instructions. Smart contracts leverage software to increase efficiency and productivity by automating execution of the terms. The potential uses of smart contracts are legion, and limited only by the imagination of the drafters and, importantly, the appetite for risk of those entering into such agreements. Deploying smart contracts on a secure blockchain reduces those risks exponentially.

How Is the Blockchain Used Today?

Blockchains, resting on secure distributed ledgers, enable the intelligent secure use of smart contracts. Those transparent ledgers create immutable records of each transaction and as append-only databases they create the perfect audit trail, ensuring transparency and accountability and, over time, becoming more and more secure. Bitcoin and other crypto currencies reside on such ledgers.

Intrigued by the value of the blockchain, businesses and governments are exploring the use of blockchain-style ledgers as secure, distributed platforms. Multiple sectors of the economy, many ripe for digital disruption, appear vulnerable to the exponential increases in efficiency, productivity, security and transparency that blockchains enable. These include sectors as diverse as finance, government, real estate, medicine and, of course, construction and the built industry generally.

Two big time players in this space are the R3 Consortium and the state of Delaware. Made up of 19 different members, all banks, the R3 Consortium controls a research lab that recently completed the origination, funding and payment of a Syndicated Loan on a private blockchain4. In 2016 Delaware launched the Delaware Blockchain Initiative, on Symbiont’s AssemblyTM platform. Delaware intends to record all government data on a state controlled blockchain, to issue, track and update UCC filings and, ultimately, issue, record and track stock ownership in Delaware Corporations5.

J U L Y 2 0 1 7 T H E C O N T R A C T O R ’ S C O M P A S S10

What Is ‘State of the Art’ in Construction?

More and more, sophisticated consumers of planning, design and construction services insist that integrated teams of designers, constructors and suppliers virtually plan, design and construct facilities, infrastructure and residential assets (FIR Assets). Those integrated teams, made up of the owner, designers, constructors and key trades, often execute new generation legal instruments patterned after the ConsensuDocs 300 Multi-Party Integrated Project Delivery (IPD) Agreement and related documents, or instruments contained in the AIA Integrated Project Delivery (IPD) Family of documents published by the American Institute of Architects. Virtually planning, designing and constructing FIR Assets together, as an integrated team, and signing an integrated agreement related to the delivery of such services, greatly increases efficiency and productivity and might be described as the “State of the Art” in construction. At a minimum these processes represent best practices in the industry.

Unfortunately, these best practices tend to replicate antiquated paper processes developed for use in “waste based” business models created to extract profits from the waste stream of a complex construction project. Historically, the built industry, operating under a design-bid-build procurement model, delivered planning, design and construction services out of a series of silos. Procurement via design-bid-build encourages waste and inefficiency, and the built industry delivers both in spades. From 1950 until 2013, a span of almost 65 years, labor productivity rates remained flat while labor productivity in all other non-farm sectors of the economy improved by over 250 percent!6

While flat to declining labor productivity is one measure of failure in construction, there are others. In 2004 the U.S. construction industry wasted $15.8 billion due to a lack of interoperability among digital platforms used in capital facilities . The value “added” by the construction

sector in 2007 was, purportedly, $1.2 trillion; however, at least 50 percent of that “value” was waste. In other words, the industry wasted $600 billion dollars in 2007! Nor have these numbers improved in the past 10 years.

Waste manifests as labor inefficiencies at a rate of 30 percent, as material waste at 30 percent, re-work at 10 percent, while 5 percent arises from poor planning and management. Together the foregoing account for $450 billion of the $600 billion wasted in 2007. Further, 72 percent of construction projects run over schedule, and 70 percent run over budget.

Not fully reflected above, additional failure manifests itself as injuries to workers, broken equipment, design defects, energy loss, inefficient operations and undue maintenance costs. These factors contribute billions more in red ink. Meanwhile, the industry embraces business models that extract profits from waste, while shunning those that earn profits by adding value.

How Can We Fix Our Broken Built Industry?

Forward-thinking firms in the built industry embraced building information modeling (BIM) in the late 1990s and early 2000s, and by 2005 the industry had begun to supplement those virtual planning and design tools with proven continuous improvement processes borrowed from manufacturing and agile project management concepts borrowed

from the IT industry. In 2010, the U.K. government mandated that all government projects in the U.K. worth more than £5.0 million be planned, designed and constructed virtually, and that the resulting digital asset be delivered to the U.K. government along with the completed physical asset.

Armed with the technologies described above, the built industry has the capacity to plan, design, construct, operate and maintain FIR Assets on a blockchain platform that combines virtual planning and design, lean construction processes and innovate financing options in a manner that enables automated payment of pay applications.

Leveraging Blockchain as a Service (BaaS) in Construction

Imagine a complex construction project financed by a member of the R3 Consortium on behalf of an owner that intends to manage the digital assets related to the FIR Assets it procures on Symbiont’s AssemblyTM blockchain platform. Further imagine that owner sought to procure planning, design and construction services from an integrated BIM enabled team capable of operating on a blockchain platform upon which all stakeholders recorded and tracked everything related to the project including, ultimately, pay applications.

In that environment, where proceeds from the construction loan reside in an escrow on the blockchain and the owner expects the physical FIR Assets as delivered to match the virtual, as designed version of those FIR Assets,

T H E C O N T R A C T O R ’ S C O M P A S S J U L Y 2 0 1 7 11

a trade contractor can complete a pay application on the blockchain and get paid immediately.

To process a pay application on a construction project three things must occur: The trade must properly complete a portion of its scope of work and request payment; the request for payment must be approved; and, a lien release related to that portion of the work must be executed. In a technologically empowered world, that entire process can be completed in a matter of seconds rather than months, resulting in a permanent, transparent record of the entire transaction being recorded on the blockchain. Under our current cumbersome system, processing pay applications easily takes 45 or even 90 days and consumes thousands of hours of administrative time, depending on the size and complexity of the project.

If the virtual design reflected in the BIM accurately depicts what the owner contracted to receive, and the photo/video from the trade contractor accurately depicts what the trade contracted to deliver, then proof of completion exists. Technology exists to compare such photos/videos to the BIM, thus automating two elements—proof of work and approval—of the smart contract referenced above. Of course, a human might “approve” the work and then click an online link

to satisfy the approval element of the smart contract as well.

Next, a lien release must be executed. Technology exists to create and execute lien releases digitally and to then store those releases on the blockchain. Or a PDF copy of a physically executed lien release could be stored on the blockchain. Either way, placing the release on the blockchain could be the last “if then” requirement prior to payment under the smart contract. Processing pay applications on the blockchain, rather than via the existing byzantine red-tape riddled process used now, will save the built industry billions.

All providers, including trades, designers, suppliers and general contractors will get paid more quickly. Owners will enjoy lower costs and access to a transparent and immutable record of all payments. That transparent and immutable record of payment will save lenders millions if not billions in administrative and regulatory compliance costs. Insurance companies and sureties will also benefit greatly from the increased precision and timeliness of information shared on projects. And as with all such technologies, numerous unknown benefits will likely accrue and trigger new opportunities to deploy new business models.

Trade contractors need to embrace the new knowledge economy and

think carefully about how emerging technologies, like the blockchain, will impact their businesses going forward. After all, wouldn’t you rather get paid today instead six months from now?

James L. Salmon joined Benjamin, Yocum & Heather as a BIM and IPD consultant in 2010. As president of Collaborative Construction, Salmon advocates the use of virtual planning, design and construction tools and integrated project delivery. Salmon also serves as an adjunct instructor of a master’s-level BIM strategy course offered by Middlesex University in London. Salmon is also a special advisor to the buildingSMARTalliance’s Thought Leadership Committee. Salmon advocates the use of integrated project delivery (IPD) and the use of virtual planning, design and construction software tools. He relishes the challenge of replacing the built industry’s broken culture with a smart procurement culture. Salmon works with clients to modify existing legal frameworks to ensure support for the vision, skills, incentives, resources and actions required to achieve the changes necessary to adopt, adapt to and deploy a smart procurement culture throughout the built industry. He can be reached at (513) 721-5672 or [email protected].

1 Bitcoin: A Peer-to-Peer Electronic Cash System, Satoshi Nakamoto, October 31, 2008, accessed June 2, 2017 http://nakamotoinstitute.org/bitcoin/2 History of Ethereum, Accessed June 2, 2017 http://ethdocs.org/en/latest/introduction/history-of-ethereum.html3 Blockchain explained in under a minute, accessed June 2, 2017 https://youtu.be/xrurxBEftMs4 Financial Institutions Move Closer to Realizing a Blockchain Solution for Syndicated Loans, Ipreo, March 30, 2017, accessed May 1, 2017 http://www.prnewswire.com/news-releases/finan-cial-institutions-move-closer-to-realizing-a-blockchain-solution-for-syndicated-loans-300431763.html5 Delaware Blockchain Initiative: Transforming the Foundational Infrastructure of Corporate Finance, Tinianow, Andrea and Long, Caitlin, March 16, 2017, accessed May 1, 2017 https://corpgov.law.harvard.edu/2017/03/16/delaware-blockchain-ini-tiative-transforming-the-foundational-infrastructure-of-corpo-rate-finance/6 AECbytes Viewpoint #67 (March 14, 2013) Labor-Productivity Declines in the Construction Industry: Causes and Remedies, Paul Teicholz, Professor Emeritus, Dept. of Civil and Env. Eng. Stanford University

7 Cost Analysis of Inadequate Interoperability in the U.S. Capital Facilities Industry, Gallaher, M. P.; O'Connor, A. C.; Dettbarn, J. L., Jr.; Gilday, L. T. NIST GCR 04-867; 194 p. August 2004.8 Rex Miller, Dean Strombom, Mark Iammarino, and Bill Black, “The Commercial Real Estate Revolutions,” John Wiley & Sons, Inc. 2009 at pg. 3.9 Martin Fischer, Howard Ashcraft, Dean Reed and Atul Khanzode, “Transitioning to Integrated Project Delivery: The Owner's Experience” Wiley & Sons, Inc. 201710 Rex Miller, Dean Strombom, Mark Iammarino, and Bill Black, “The Commercial Real Estate Revolutions,” John Wiley & Sons, Inc. 2009 at pg. 3.11 Id. 12 The Built Industry’s Backwards Bicycle, Blog Post on the Collaborative Construction Blog, accessed 4-4-2017, http://collaborativeconstruction.blogs-pot.com/2015/08/the-built-industrys-backwards-bicycle.html13 The UK government set up a BIM Task Force to ensure compliance with the BIM mandate. Accessed June 2, 2017 http://www.bimtaskgroup.org/

T H E C O N T R A C T O R ’ S C O M P A S S J U L Y 2 0 1 7 13

Feature

J U L Y 2 0 1 7 T H E C O N T R A C T O R ’ S C O M P A S S14

Long Live the King! Why Your Company Needs Cash-Flow Reportingby Steve Antill, Foundation Software

Why do we say cash is king? It’s one of the most powerful assets in your company, because it sets the reality for your business every day of your project cycle—not just at year-end when your financials tie out. That’s why it’s always critical for subcontrac-tors to go beyond high-level financial statements and look at the different angles offered by company-wide and job-level cash-flow reporting.

The Heart of a King: Why Cash Is Different From Assets or Income

Let’s look at a different metaphor—one with a little more body. Cash is the lifeblood of construction projects. In a medical exam, there are numer-ous tests your doctor will want to run. Some are routine; some are based on specific risk factors. All of them can be important. But none of them count for much if the heart isn’t working properly and carrying life throughout the body.

The Balance Sheet. One of those basic, essential health checks for any business is the balance sheet. The balance sheet looks at a spec-ified moment in your fiscal year. It represents the balance of your resources that have value (assets) and your resources owed (liabilities) plus owner or shareholder resources (equity). In other words, it’s a state-ment of the things a company has (assets) and how it pays for them—either money owed (liabilities) or invested in the business (equity).

The simple logic of a balance sheet looks like this:

Assets = Liabilities + Equity

What does a balance sheet look at with regard to cash? Basically, it just takes it into account. In the bal-ance sheet, your cash accounts are numbered among several other asset accounts that show your company’s big-picture worth in a moment-in-time snapshot. So, you can see how

much is in your cash accounts and how much of your current value that accounts for, but that’s about it.

The Income Statement. Another key health check is the income state-ment, or P&L statement, which reports your profitability over a period of time. It does this with a very simple formula, which can have addi-tional layers to it:

Income – Expenses = Net Profit (Loss)

A P&L can also be divided out, for example, to show separate income sources, as well as expenses incurred directly versus indirectly from jobs. Obviously, if revenues exceed expenses, it shows a profit, and if expenses exceed income it reports a loss. What’s not obvious is what this tells you about your cash. Hint: not as much as you might think.

The main reason is that P&Ls rec-ognize revenue when it’s billed by accounts receivable—not when it’s collected. If you’ve invoiced your

T H E C O N T R A C T O R ’ S C O M P A S S J U L Y 2 0 1 7 15

client $150,000 and they’ve haven’t made a payment, your P&L still counts that as income. That can make you look more profitable than your checking account would indicate. Just as important, your accounts paya-ble are reported as expenses even before you’ve paid them from cash. As a result, if you’re looking just at your income statement, a run of A/R invoices can lead you to think your cash flows are healthy, even though you won’t see that money for another 30 days. Thus, a P&L will suggest whether you’re profitable overall, but if you ask, “Will we have enough cash for payroll in September?” it’s pretty silent.

Cash Flows. While the balance sheet and income statement can tell you a lot about your company’s health, construction projects don’t run on “assets” or “income”—they operate on cash. No amount of X-rays or lab work will tell you how well your heart is pumping and whether the blood is getting where it needs to be. That’s where two vital types of reports come in: statement of cash flows and cash flow by job.

The Heart of the Matter: How to Track Cash

To see how readily cash is being made available to the projects that need it, contractors should view and understand cash flow from two per-spectives: across the entire compa-ny’s financial picture and at the level of each job.

Statement of Cash Flows. Like the balance sheet and P&L, the state-ment of cash flows is a general ledger financial statement; however, it’s structured specifically to separate out the non-cash assets (like receivables and inventory) and non-cash liabili-ties (like accruals) the balance sheet reports.

So why not just look at your G/L cash account balances? There are two reasons: First, your statement of cash flows provides an additional check of your books; your net change in cash should always tie out to the changes in your balance sheet accounts. Second, it shows you where cash is being made available and where it’s going—whether that’s from operat-ing activities, investing activities or financing activities.

With assistance from a financial professional like a construction CPA, you can use this in projecting future cash flows, as well as gauging some of your overall business health. In general, consistent, strong cash flow suggests the ability to reduce debt and invest in growth. But is all well just because your cash from oper-ating activities is pumping away strong?

Cash flow by job. If you have integrated job costing through your accounting software, you can and should also look at your cash flows on a contract level. Every project of course needs a healthy movement of billings and purchasing—but more importantly, they need cash receipts; otherwise, your projects are drawing on your cash accounts. If too many of your jobs are borrowing on company cash, you can easily find yourself needing to take on additional debt or grinding to a halt in the field.

The benefit of contract cash-flow reporting is that it shows you where each project stands in its cash cycle and how each project is affecting cash activity for the company. Struggling projects can hide on a cash flows statement—but not here. At its most basic, these reports lay out your esti-mated gross profit (contract amount – estimated costs), cash received to date (billings – open A/R invoices) and cash paid to date (costs + labor – open A/P invoices). This enables you to see your net cash flow at a glance

and even project future cash flow as your projects move forward.

Received job dollars to date – Cash paid to date = Net cash flow

A job-level cash flow report can also offer an additional perspective on your job progress by calculating the proportion of your net cash flow to (a) your contract amount and (b) your gross profit estimate, each as a percentage. To get even more from it, you can also look at the “cash flow to gross profit” figure alongside the percent contract billed, the job pro-gress by cost, etc., to get comparison job progress metrics. Cash flow by job reporting opens up a whole new world for your project financial data.

When it comes to important finan-cial reporting, your income state-ment and balance sheet will never be dethroned—but cash is king, and the reason is that it carries life to the pro-jects that keep you profitable. A cash flows statement tells you how well the heart of your business is pump-ing. Job-level cash reports then show you how well that flow is working in your active jobs. Together, they help complete the picture of your business health so you can keep conquering the industry.

Steve Antill is the director of sales for Foundation Software, where he builds partnerships and relationships across the construction industry with contractors, CPA firms, associations and technology vendors. Over 18-plus years, he’s led more than 1,000 soft-ware selections and implementations. Foundation Software delivers job cost accounting, project management and mobile applications, along with edu-cation and bookkeeping services, to help contractors run the business side of construction. Antill can be reached at (800) 246-0800 or [email protected].

J U N E 2 0 1 7 T H E C O N T R A C T O R ’ S C O M P A S S16

Feature

Contractors take on tremendous risk when they perform work. However, more contractors go out of business due to poor cash flow than for lack of profitability. Why? Is there as much emphasis on billing and collections as there is on daily construction opera-tions? While management executives typically have a firm grasp on the cycle of cash through their organizations, what does the financial acumen of your remaining staff look like? More impor-tantly, how educated are your PMs, pro-ject administrators, and A/R clerks in the art of billing and collections? Are your company’s systems and processes standardized in these critical areas? A contractor’s cash flow is driven by one thing: the cash flow of its individual projects.

This article will discuss the key indi-cators that are necessary to give early warning to cash flow issues, the impor-tance of a properly crafted schedule of values, how to implement a struc-tured billing process, and how to define the internal escalation process for collections.

Key IndicatorsWhen a project’s cash flow goes

south, it is not usually a surprise. Your team can spot the early warning signs if it has the right tools and knows how to use them. There should be standard reports both at the corporate and pro-ject levels that allow for cash flow visi-bility. While monitoring cash flow at the corporate level is important, the solu-tions to cash flow are derived at the project level.

Corporate LevelIt is critical to monitor key financial

indicators at the corporate level so that upper-level managers can detect a cash-flow issue early. There are many items to review regularly that can serve as early warning signals. At the enterprise

level, monitoring current ratio and quick ratio give a snapshot in time of the asset to liabilities calculation as a roll-up. Establishing minimums for these ratios and building red flags into your reporting structure is key to identifying issues quickly. Analysis of working cap-ital by dollars, percentage, and yearly turnover are also important indicators of the company’s financial health. From the corporate perspective, a roll-up of project overbillings and the cash posi-tion are also essential to review. Lastly, looking at debt-to-equity ratios and establishing a maximum threshold for this is also an important data point to monitor. All of these are key indicators that would compel you to dig deeper once a problem was identified. (You can also use such tools as CFMA’s Financial Benchmarker to compare this data. Visit www.financialbenchmarker.com.)

Many companies create a balance sheet and income statement either monthly or quarterly. Interestingly, fewer publish a statement of cash flows. Best-in-Class companies also pub-lish a forward-looking cash projection, which could be crafted as a 12-week look-ahead based upon the projects on the WIP and the PMs’ understand-ing of their project schedules and work planned. This cash projection gives the company time to react to an oncoming shortfall more effectively.

Project LevelThere are relevant indicators that can

be created at the project management level. Within your company’s job status report, there should be two very clear indicators of cash position of the pro-ject: overbillings/underbillings and net cash position. During the monthly pro-ject review, these two key data points should be reviewed and expectations for the PMs to uphold should be set; the PM is the singular point of responsibility over a project.

There is a distinct difference between a “project witness” and a “project man-ager.” If expectations are clearly set around overbillings, such as a net over-billed position of 20 percent or greater, this can be measured and the PM can be held accountable. There is a quanti-fiable data point to measure the PMs’ effectiveness in this area. This meas-urable can be incentivized, drive the desired positive behavior, and turn those who might be simply witness-ing a job’s cash position into those who want to drive it and ensure that they hit their targets.

The very same can be said for the net cash position. Cash position simply states how much has been paid out vs. what has been collected. While this may seem remedial to some, driving this level of knowledge to the project level is key. A true PM wants to manage all of the direct job costs, the billing, and the collections process. (Billing and collec-tions strategies will be discussed later on in this article.)

Schedule of ValuesCreating a schedule of values

includes the mechanics of how the budget cost data is procured and organ-ized, what format to use to ensure that the correct costs fall into the correct cat-egories, a review of the schedule of the project to clarify which activities will occur early in the project, and correct assignment of the general conditions and start-up costs (e.g., mobilization, design, detailing, submittals, material procurement, and prefabrication). If a schedule of values is done poorly, then maintaining a positive cash position is virtually impossible.

A controversial piece to define is whether or not to front-end load the schedule of values and, if so, by how much. This is an enterprise-level deci-sion that should be driven by the type of vertical markets your company

Improving Your Cash Flow: The Art of Billings & Collectionsby Stephane McShane, Maxim Consulting Group

J U L Y 2 0 1 7 T H E C O N T R A C T O R ’ S C O M P A S S16

T H E C O N T R A C T O R ’ S C O M P A S S J U L Y 2 0 1 7 17T H E C O N T R A C T O R ’ S C O M P A S S J U L Y 2 0 1 7 17

serves, the normal payment terms of your client base, and your compa-ny’s position on the topic. (Refer to the Construction Financial Management Association article, “Taking Risks with Numbers: How Far Can You Go?” by Susan L. McGreevy & Kathryn I. Landrum, in the September/October 2014 issue of Building Profits for more on this topic.)

Should front-end loading become a company standard, the minimum per-cent frontload should be a calculation on the schedule of values tool, to be reviewed for compliance and used as a metric for a PM’s performance. The goal of an effective schedule of values is to get paid for overhead and profit as quickly as possible, and is the single greatest impact a PM can have on his/her project cash flow.

Billing StrategiesYour company’s internal billing pro-

cess should be well defined, commu-nicated, reviewed, and measured. Let’s take a look at a sample billing process:Repeat steps 1-4 for each line item on the billing:1. Review the existing cost to date for

labor, material, and other direct job costs

2. Identify additional costs of each direct job cost projected through the end of the month

3. Evaluate the percent complete4. Mark up the billing item with the

percent completeQuality check:

1. Verify the total billing amount for all line items

2. Verify this total billing amount meets or exceeds the minimum established billing amount

3. Call or visit the client, review the bill, and get “pencil approval” prior to submission

To clarify this example, let’s dis-cuss the minimum established billing amount. While some contractors take a “bill as much as you can” approach, this is not a measurable target. When discussing a minimum billing amount, targets should drive the positive reve-nue recognition that is the goal of a bill-ing process.

For example, the minimum billing amount could be set at percent com-plete of the project plus 20 percent of cost. This approach verifies how effec-tive the schedule of values is at driving

positive cash flow. The reason that 20 percent of project cost to date is added is due to the cost of capital we encoun-ter by having retainage withheld, and payment cycles that typically hover between 45 and 60 days. Establishing the minimum billing amount and method should be standardized, and billing amount approval should occur before sending to the client.

Too often, we see billings that are submitted and then kicked back for revision. Sometimes the owner or GC does not agree with the billing amount, causing tremendous rework inside of the accounting group to revise the amounts. We have also seen billings that were submitted 60 or 90 days prior get kicked back, causing all of the sub-sequent billings to be recalculated and reissued. Depending on your com-pany’s accounting software, this can cause both a time delay to process and tremendous labor expenditure to accomplish.

This also has a devastating effect on cash flow since it is much later in the payment cycle to even be approved, much less the waiting time to receive a check. One solution is to get billings “preapproved” prior to submission: Walk the owner or GC through the bill-ing, and have him or her sign off on your preliminary copy. This is critical in helping to avoid the billing adjust-ment scenario, thus keeping you in the correct payment cycle and driv-ing a shorter wait to actually receive payment.

When a billing is withheld, the cause is often something that the PM forgot to do (e.g., waivers not submitted, certi-fied payrolls not included, etc.). To pre-vent these types of delays, the billing process should include a job-specific checklist so that all required documen-tation is included each time a billing is submitted. We cannot always control what the other party does with our bill-ing, but we can control our ability to meet the contractual requirements in a timely manner.

There also seems to be a tremendous challenge at the end of projects to get final billings approved. So, the amount placed on final billings should be held to a minimum. Here are some strategies to consider:• Ensure that the last regular progress

billing is as large as possible, keeping the final billing amount small. Progress bills are much easier to get approved than a final billing.

• Delay submitting a final billing if substantial progress is made and collection has been difficult. Instead, submit an additional progress billing.

• Set up a separate contract or purchase order for small, last minute change orders. Don’t hold up a $200,000 retainage for an additional month or two for a $1,200 change order that contains $400 in margin.

• Ask for preliminary approval of the final billing in advance, similar to the preapproval of the progress billings previously discussed.

• Use the waiver of your lien rights as leverage to get final billings approved.

CollectionsWhile the PM may not be the person

performing each of these tasks, he or she must ensure that items are accom-plished in a timely manner in order to release payments quickly. The PM has the relationship with the client, and must be on the collections team.

Defining levels of ownership of the collections process is a method by which a person is assigned responsi-bility over a project’s receivables for a specific period during the aging. As the receivable gets older, it becomes the responsibility of a higher classifica-tion of employee, thus escalating the level of personnel handling it until the collection has occurred. Most compa-nies are great at publishing an aging report. Assign a job title to each aging period to establish who owns the account at that moment. Fig. 1 illus-trates an example:

The collections process should doc-ument the actions taken at each level of aging and explain how documenta-tion is to occur. The project coordina-tor should pursue the contact weekly, recording each step of the way. Once the aging has reached 31 days, it becomes the PM’s responsibility to contact the recipient and document

Aging in Calendar Days

Responsible Party

0–30 Project Coordinator or Billing Clerk

31–40 PM

41–55 A/R Representative

56+ Division Manager or Vice President

New On-demand Video from FASAWhen it comes to managing your business, the Foundation of ASA is your partner in education. View and listen to FASA’s on-demand videos at an individual workstation or in a conference room for group training. Your order includes access to the on-demand video any time, and as many times as you’d like! This is just one of the on-demand videos available through the FASA Contractors’ Knowledge Depot to meet your business management training needs.

“Prompt Payment and How/When to Suspend Work” (Item # 8103)

In this on-demand video, presenter Jason Ebe, Esq., Snell & Wilmer, LLP, Phoenix, Ariz., discusses best practices for ensuring prompt payment of invoices and shares tips for how subcontractors can mitigate their own damages by suspending work without breaching their subcontract and getting fired, replaced and sued.

$65 for ASA members $95 for nonmembers.

TM

ORDER ONLINE AT www.contractorsknowledgedepot.com

this information on the same project collection log. This continues until the bill reaches the 41st and 56th day, each time transferring ownership up the company chain so that they may reach out to their peers at the client office in order to resolve the issue. This affords the opportunity to consistently com-municate non-payment and secure a customer’s commitment to pay. As with any process, the days sales out-standing (DSO) of a project is meas-ured and rolled up by the PM, A/R representative, and division manager as another very effective performance metric

Monitoring key indicators can ena-ble early warnings of a cash flow issue. The development, implemen-tation, and monitoring of effective schedule of value practices, billing strategies, and collections processes increase the chances of collecting the full revenue due, help drive down the timeline between submission of billing and receipt of payment, and place your company in a positive cash position earlier, thus reducing the cost of capi-tal to perform work. In addition, these processes establish levels of owner-ship and the ability to both measure

and incentivize the right behaviors to keep cash flow positive for each pro-ject and the company as a whole.

Stephane McShane is a direc-tor at Maxim Consulting Group and is responsible for the evalua-tion and implementation processes with Maxim clients. McShane works with construction-related firms of all sizes to evaluate business practices and assist with management chal-lenges. With a large depth of expe-rience working in the construction industry, McShane is keenly aware of the business and, most specifically, operational challenges firms’ face. Her areas of expertise include lead-ership development, organizational assessments, strategic planning, pro-ject execution, business develop-ment, productivity improvement, and training programs. McShane is an internationally recognized speaker, mentor, author, and teacher. Her abil-ity to motivate, inspire, and create confidence among your work groups is extremely rare and very effec-tive. McShane can be reached at [email protected].

What Happens If You Don’t Get Paid?

So, what happens when you don’t get paid? You have a number of options, including leveraging your lien rights or filing on the payment bond. Be sure, however, that you thoroughly understand the notifications requirements for either of these options to be effective. Bring in your bonding agent and have an educational session with your project staff on the essentials of filing a bond claim. This could prevent the all-too-common late filing and loss of rights. If you have disputed work, claims, or outstanding change orders, then negotiate a settlement if at all possible. If you are forced to go into arbitration or litigation, the chances of collecting the full amount of what you are owed diminishes greatly, and the amount of time your project staff will spend preparing documentation for the case may diminish their capacity to manage profitable work.

T H E C O N T R A C T O R ’ S C O M P A S S J U N E 2 0 1 7T H E C O N T R A C T O R ’ S C O M P A S S J U L Y 2 0 1 7 19

Feature

In today’s robust construction mar-ketplace, subcontractors and con-struction firms face a significant challenge to their business: retaining an effective employee base. In addi-tion, employee engagement in the United States has hovered around 33 percent since 2000, according to annual surveys conducted by the Gallup organization. This dismal level of employee engagement is compli-cated by the fact that as baby boom-ers retire, there simply aren’t enough Generation Xers to replace them. This alarming trifecta of a strong construc-tion market, low employee engage-ment, and a shortage of human capital threatens the ability for con-struction firms to retain and motivate their most valued employees.

These challenges can impact per-formance and affect your compa-ny’s bottom line. As reported in the 2017 Gallup State of the American Workplace survey, behaviors of highly motivated employees resulted in 21 percent greater profitability, and busi-ness units with highly motivated workers experienced a 20 percent increase in sales. So how can you engage your employees in ways that encourage them to stay and thrive, while also enabling your company to reach its full potential?

Here are four top strategies to retain key employees, foster engagement, and ultimately enhance performance:• Create a clear strategic plan.• Define and monitor performance.• Cultivate and compensate employ-

ees based on performance.• Commit to clear communication.

Create a Clear PlanThe first strategy is to create a stra-

tegic plan that defines a roadmap for reaching its goals. All subcontrac-tors should have a long-term vision that guides your strategic decisions, reflects a thorough understanding of how your organization reached its current state, and defines a clear path of practical actions to achieve your desired future state. Core elements of a comprehensive strategic plan include:• Mission, vision, and core values to

guide decisions.• Goals and objectives to quantify

your expected outcomes.• Strategies and tactics to achieve

your goals and objectives.• Action plan to identify responsibili-

ties, costs, and timelines for strate-gies and tactics.It’s important to understand that

the planning process is just as impor-tant as the plan itself. Involving your management and staff throughout the process is critical to success. By ask-ing for input from your employees, you will develop a more informed plan, strengthen buy-in, increase the likelihood of implementation success, and ultimately increase employee engagement.

Define and Monitor Performance

Key performance indicators play an integral role in monitoring per-formance. The second strategy is to develop KPIs for each facet of your business, and to tie them back to your strategic goals and objectives. Think of performance at three different lev-els: company, business unit or depart-ment (team), and individual. Focusing

on performance at each of these lev-els is important to your organization’s success. For instance, subcontractors need all employees to perform in a manner that is in the best interest of the organization in order to achieve company goals; work together as teams to achieve departmental/team objectives; and conduct themselves in accordance with core values to achieve individual expectations.

Cultivate and Compensate Employees Based on Performance

The third strategy is to determine how your organization will attract, retain, develop, and motivate your key employees to meet your goals at every level—and in every facet—of the company. For instance, sub-contractors need to clearly define and articulate what core competen-cies their employees are expected to possess to successfully perform each role at each level of the organization, and how the company will support development of those competencies. Similarly, organizations need to craft performance-based compensation programs that are aligned with the demonstration of core competencies and achievement of multi-level per-formance expectations. Annual per-formance reviews should reinforce this alignment.

Employee cultivation and compen-sation programs should include the following key components in order to be as effective as possible:• Well-defined recruiting needs

for entry-level and experienced personnel.

• Career paths that enable mana-gerial and technical personnel to progress.

Four Top Strategies to Retain and Motivate Key Employeesby Mark Steranka, Moss Adams, LLP

• Compensation programs that incentivize employees to accom-plish goals.

• Training programs designed to help employees reach their potential.Ultimately, the goal should be to

motivate employees to strive for strong company, team, and individ-ual performance. The most effec-tive employees are those with a clear understanding of how their perfor-mance contributes to company suc-cess, how to navigate their career, and how they benefit from perfor-mance-based compensation.

Commit to Clear Communication

Although the first three strate-gies form the cornerstones of perfor-mance, engagement, and retention, they can’t be fully effective without clear and consistent employee com-munication. Communication is the

glue that aligns and binds these strat-egies together, helping employees understand how they individually and collectively contribute to your com-pany’s success. As a result, subcon-tractors need to focus on making communication crisp, clear, struc-tured, and regular. For example, sub-contractors can engage employees through quarterly communications on their company’s progress toward implementing the strategic plan, and explaining how that progress impacts performance and, in turn, perfor-mance-based compensation payouts.

When Employees Thrive, Companies Succeed

These four strategies lay the groundwork to develop key manage-ment staff into future leaders, help reach your company’s full potential, and sustain your business over the long term. The key is to take an hon-est and transparent approach with

your key employees by treating them like essential members of the team, and making it clear that each person plays a valuable role in achieving the company’s mission. Employees need to understand your strategic goals, the expectations for achieving those goals, the competencies required to meet those performance expecta-tions, and how compensation is tied to performance in order to perform at their best. When they do, your organ-ization will have incentivized key employees, strong retention, and high employee engagement.