or maintain social systems.” - maria ramos (ceo: … maintain social systems.” - maria ramos...

TRANSCRIPT

CORPORATE GOVERNANCE...

“Governance is the process whereby people in power make decisions that create, destroy or maintain social systems.” - Maria Ramos (CEO: Transnet)

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – The Hue & Cry!

“a system by which a corporation is directed and controlled ”

What is CG??

a system by which a corporation is directed and controlled.

(Cadbury Committee 1992)

“ h f k f l l i hi d i hi“the framework of rules, relationships, systems and processes within and by which authority is exercised and controlled in corporations”

(CG Principles & Recommendations, Australia)

“It involves a set of relationships between a company’s management, its board, its shareholders and other stakeholders. It also provides the structure through which the objectives of the company are set, and the means of attaining thosewhich the objectives of the company are set, and the means of attaining those

objectives and monitoring performance are determined.”

(OECD Principles of Corporate Governance )

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – The Hue & Cry!

Board Structure

Strategy

CEO Evaluation

KE

What is CG??

Board Structure

Role of the board

Role of individual directors

Role of the Chairman

Role of the CS

Monitoring

Risk Management

Compliance

Policy Framework

EY

BO

AR

DF

UN

C

RN

AN

CE

RO

LE

S

Role of the CEONetworking

Stakeholder Communication

Decision MakingCORPORATEGOVERNANCE

CT

ION

SE

GO

VE

R

Board meetings

Board meeting agenda

Board papers

Director protection

Board evaluation

EF

FE

CT

IVE

GO

VPR

OC

ED

UR

ES

Board papers

Board minutes

The board calendar

Committees

Director remuneration

Director development

Director selection & induction

VE

RN

AN

CE

BO

AR

DP

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – The Hue & Cry!

“It takes 20 years to build a reputation, and five minutes to ruin it”

Why is it important??

y p ,

(Warren Buffet)

“ boards generally met the characteristics of good governance but failed to perform effectively”

(Walker Review, U.K. 2010)

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

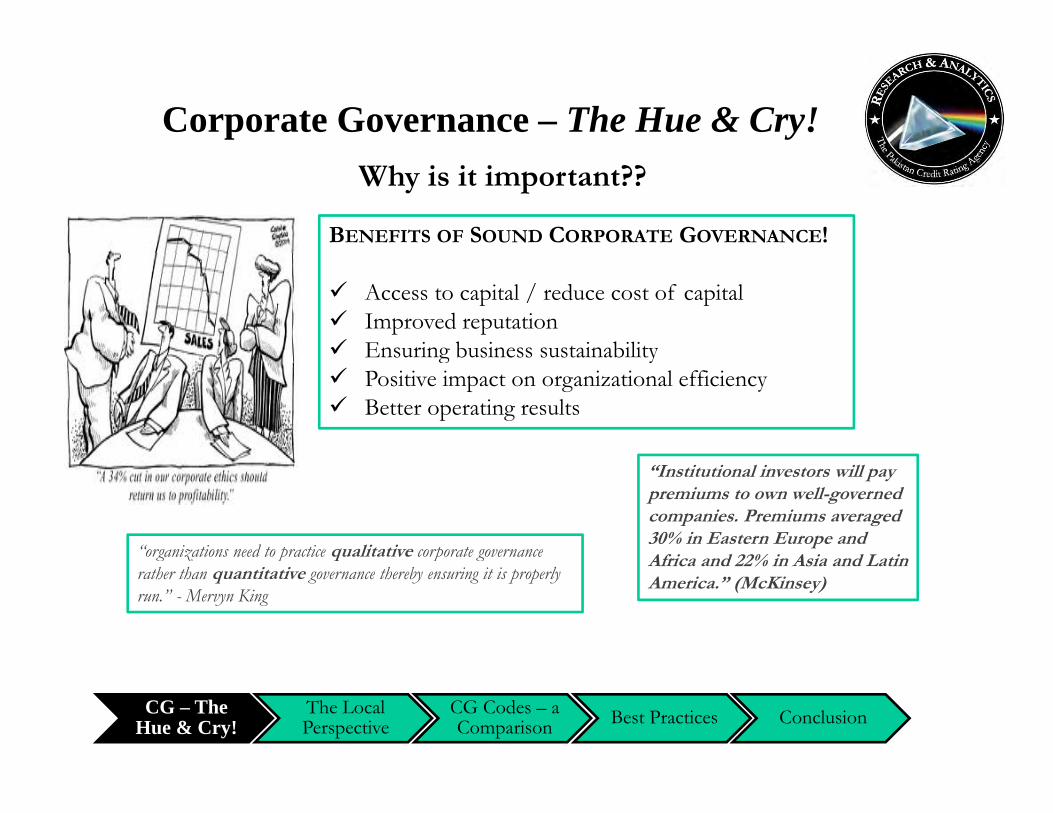

Corporate Governance – The Hue & Cry!

BENEFITS OF SOUND CORPORATE GOVERNANCE!

Why is it important??

Access to capital / reduce cost of capitalImproved reputationEnsuring business sustainabilityEnsuring business sustainabilityPositive impact on organizational efficiencyBetter operating results

“Institutional investors will pay premiums to own well-governed companies. Premiums averaged 30% in Eastern Europe and Africa and 22% in Asia and Latin“organizations need to practice qualitative corporate governance Africa and 22% in Asia and Latin America.” (McKinsey)

g z p q p grather than quantitative governance thereby ensuring it is properly run.” - Mervyn King

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – The Hue & Cry!

OECD Principles of Corporate Governance (2004)

A Global Phenomenon

The UK Code of Corporate Governance (2010)

Malaysia CG Code (2012)

NYSE Listing Rules (2003) + Review (2010)

y ( )

Code of CG Pakistan (2012)

Corporate Governance & Principles, Australia (2007)

IFC G id lin

India CG Guidelines (2009) + BSE Rules (2010)

IFC Guidelines

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – The Hue & Cry!Post-Crisis Lessons

“Good corporate governance is about ‘intellectual

Two principal conclusions were drawn by the Walker review in the UK:

Follow SPIRIT of the Code as well as its letter

honesty' and not just sticking to rules and regulations”

Mervyn King (Chairman: King Report)

Follow SPIRIT of the Code as well as its letter

Enhance interaction between the boards and S/H

There is so much smoke that we have lostThere is so much smoke, that we have lost sight of the fire

This fire is the real message and definition of corporate governance which is undoubtedlycorporate governance, which is undoubtedly beneficial to all, that we should be gooddirectors.

i e Encourage self-regulationi.e. Encourage self-regulation

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – The Local PerspectiveSurvey of Board Practices in Pakistan

Code of Corporate Governance

14

2

49

45

57

D h CG f k i bl f h h ld

Does the current CG framework ensure the rights of all stakeholders?

Does the current CG framework in Pakistan ensure timely and accurate disclosure of all material matters regarding the corporation?

8

5

10

51

54

49

Does current CG frame work in Pakistan promote transparent and efficient k ?

Does the current CG framework ensure Strategic Guidance and effective monitoring of risk and related matters impacting the corporation?

Does the current CG framework ensure equitable treatment of shareholders including minority and foreign shareholders?

0

8

59

0 10 20 30 40 50 60 70

Does CG Code 2002 provide intrinsic benefits beyond mere compliance?

markets?

Point to Ponder :Though almost all the companies have responded in affirmative but what is actually to be judged is whether the Boards have

come out of the tick box approach and have implemented the Code in spirit?

Yes No

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – The Local PerspectiveSurvey of Board Practices in Pakistan

Board Procedures & Practices

44

12

19

15

47

40

Does the Board have any retreat meetings?

Does the Board have a formal Corporate Social Responsibility (CSR) policy?

Is there a mechanism in place for whistle blowing?

15

5

31

44

54

28

Are non executive directors given opportunities to interact with employees?

Do you agree with the separation of Chairman and CEO's position?

Does the Board assess its own performance?

y g

25

22

27

15

34

37

32

D th B d i i l i ?

Does the Board formally assess the Human Resource?

Does the Board formally review appraisals of positions reporting to the CEO?

Are non executive directors given opportunities to interact with employees?

8

25

51

0 10 20 30 40 50 60

Are the internal Control Procedures reviewed annually by the Board?

Does the Board engage in succession planning?

Yes No

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – The Local PerspectiveSurvey of Board Practices in Pakistan

B d E l i

1

1

13

58

58

Are Board meetings of sufficient frequency/duration to complete the Company's Business?

Are Board committees playing a useful role?

Board Evaluation

3

10

46

53

56

49

13

A f d f b d

Are you satisfied with the mix of skills and competencies of Directors on your Board?

Has the presence of Independent Directors added value to the Board?

Has the presence of Women Directors added value to the Board?

5

5

6

58

54

54

53

Has the Board taken appropriate measures to implement governance

Are you satisfied with the level of involvement of Directors when formulating key business strategies?

Are Directors on your Board sufficiently oriented to perform effectively?

Are you satisfied with the size of the board?

1

0 10 20 30 40 50 60 70

improvement planning?

Yes No

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – The Local Perspective

Shareholders' Rights

Survey of Board Practices in Pakistan

39

20Is there a written Dividend policy in

place?

Shareholders Rights

List your top three suggestions in descending order to make your Board more effective

1 I iti ti B rd E l ti pr r m

35

24Is there a mechanism in place to resolve conflicts of interest between

a major shareholder and the company?

1. Initiating a Board Evaluation program2. More focus on strategy setting by the Boards3. More effective use of Board committees4. Reduced interference from the Government5 Red ced n mber of Directorships

52

7

0 10 20 30 40 50 60

Is there a written policy relating to minority shareholder rights?

5. Reduced number of Directorships6. Need for more independent directors

0 10 20 30 40 50 60

Yes No

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance Codes – A Comparison

CG Code 2012 CG Code 2002 India USA U.K.

Chairman of the Board Mandatory:

Board Composition

Mandatory:ONE

Preference:

Chairman of the Board is a non-executive director: At least 1/3rd

But is a promoter of the

Mandatory:Majority

GE : Minimum of 10At least 2/3rd

Larger Companies: At least 50%

S ll C p iIndependent Directors

(Next election)

f1/3rd

Professional indemnity insurance cover in

f

Encouraged a minimum of one independent director

p fcompany or is related to any promoter or personoccupying managementpositions at the board level or at one level below h b d

Citigroup:At least 2/3rd

P&G:Ch i i

Small Companies: At least 2

Should arrange appropriate insurance cover inrespect of

independent directors shall be encouraged

the board:At least 50%

Chairman is an executive director:At least 50%

Chairman is independent, at least a majorityChairman is not independent, at least 2/3rd

insurance cover in respect oflegal action against its directors

At least 50% 2/3

ExecutiveDirectors

(Next election)

Not more than 1/3rd of elected directors including CEO

Not more than 3/4th of elected directors including CEO

Not more than 50%

Silent

GE: No executive directors

An appropriate combination of executive andnon-executive directors

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

directors directors

Corporate Governance Codes – A ComparisonIndependent Director(s)

CG Code 2012 (Following cannot be independent) CG Code 2002

Has been an employee of the company, any of its subsidiaries or holding company within the last 3 years;

Is or has been the CEO of subsidiaries, associated company, associated undertakingor holding company in the last 3 years;

A director who is not connected with the company or its promoters or directors on the basis of family relationship and who does not have any other relationship, whether pecuniary or otherwise, with the or holding company in the last 3 years;

Has, or has had within the last 3 years, a material business relationship with the company either directly, or indirectly

H i d i i h 3 di i di

whether pecuniary or otherwise, with thelisted company, its associated companies, directors, executives or related parties.

The test of independence principally f h f h h hHas received remuneration in the 3 years preceding appointment as a director

or receives additional remuneration, or has participated in the company’s share option or a performance-related pay scheme;

Is a close relative of the company’s promoters, directors or major S/H (>10%)

emanates from the fact whether such person can be reasonably perceived as being able to exercise independent business judgment without being subservient to any apparent form of interference.p y p j ( )

Holds cross-directorships or has significant links with other directors through involvement in other companies or bodies;

Served on board for > than 3 consecutive terms

Has not been nominated under sections 182 and 183 of the Companies Ordinance, 1984

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Served on board for > than 3 consecutive terms

Corporate Governance Codes – A ComparisonOther Codes – some differences

India – a non-executive director of the company who:

USA (Following cannot be independent)

Is or was not not a partner or an executive during the preceding 3 years, of the statutory audit or the internal audit firm of the company, and the legal firm(s) and

An employee, or whose immediate family member is/has been an executive officer, of the company in the last 3 years

A director, or whose immediate family member received, > $100,000 per year in direct compensation from the company, in the last 3 years the company, and the legal firm(s) and

consulting firm(s) that have a material association with the company

is not a substantial S/H of the company i.e. i >2% f i h

year in direct compensation from the company, in the last 3 years

A director, or whose immediate family member is affiliated with or employed in a professional capacity by, a present or former internal or external auditor of the company in the last 3 years

owning >2% of voting shares.

is not less than 21 years of age.

UK (Following cannot be independent)

A director, or whose immediate family member is employed, as an executive of another company where any of this company’s present executives have served on that company’s compensation committee in the last 3 years

U ( g d p d )

has been an employee of the company or group within the last 5 years;

A director, or whose immediate family member is an executive officer, of a company that makes payments to, or receives payments from, the company for property or services in an amount which, in any single fiscal year, exceeds the greater of $1 million, or 2% of such other company’s consolidated gross revenues in the last 3 years

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

consolidated gross revenues, in the last 3 years

Corporate Governance Codes – A Comparison

CG Code 2012CG Code

2002India USA U.K.

Not be a member in For a full-time ED: Max ONE non-

Number of Directorships

(Next election)

Max.:7 listed companies at one time

does not include directorship in listed subsidiaries of a listed holding company

Max.:10 listed companies at one time

more than 10committees

or act as Chairman of more than 5committees across all

Silent

Max. ONE non-executive directorship or chairmanship in a FTSE 100 company

NED should election) subsidiaries of a listed holding company committees across all

public limited companies

undertake that they will have sufficient time

Board E l i

In 2 years of implementation of NED could be l d b At least an annual self

Formal and rigorous annual self-

Evaluation

(April 2014)

y pCode, board has to put in place mechanism

- evaluated by a peer group comprising the entire board

evaluation of board and its committees

evaluation of board and its committees and individual directors

Office ofThe Chairman and CEO shall not be the same person Can be held by the The Chairman and

Office ofChairman & the CEO

(Next election)

be the same person

The Chairman shall be a NED

Chairman shall preside over AGM (Companies Ordinance 1984, Clause

The Chairman shall preferably be a NED

Silent

Reliance Industries:Mukesh Ambani is Chairman and MD

same person

P&G:If Chairman is CEO, one ID will be chosen as presiding director

CEO shall not be the same person

The Chairman shall be an ID on appointment

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

160 (3)) presiding director appointment

Corporate Governance Codes – A ComparisonCG Code 2012 CG Code 2002 India USA U.K.

A company may train itsDirector orientation and

The Chairman should ensure that new

Training of Board ofDirectors

(June 2016)

Will be mandatory to attain certification under any director training program (DTP)

It is mandatory for directors of listed companies to attain certification

A company may train its board members regarding, business model, risk profile of the business parameters, their responsibilities as

orientation and continuing education must be addressed in the CG Guidelines

ensure that new directors receive a full, formal and tailored induction and should regularly review and agree with each

(June, 2016) certification directors, and the best ways to discharge them

presented on the company website

director their training and development needs

Appoint, remun and terms and Approval of appoint f CFO b A di

Appointment, and removalandqualification

pp ,conditions of employment of the CFO, CS and the Head of IA shall be determined by the board

Appoint, remun and terms and conditions of employment and removal of CFO

of CFO by Audit Committee

The information on recruit, remun, appoint or removal of CFO/CS Silent

Both the appoint and removal of the company secretaryqualification

criteria forCFO and CS

(Immediate)

The removal will also be by the board for CS and CFO, while removal of Head of IA is with the approval of the board only upon recommendation of Chairman of the BAC

and CS determined by CEO and approved by board

or removal of CFO/CS to be presented to board

Appoint, removal and remun of Chief IA shall be subject to review by

Silent company secretary should be a matter for the board

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Chairman of the BAC BAC

Corporate Governance Codes – A Comparison

CG Code 2012CG Code

2002India USA U.K.

All pecuniaryrelationship ortransactions of the Director

Sufficient to attract, retain and motivate

Remuneration

(Imm di t )

A formal and transparent procedure to be followed and disclosure of -

NED vis-à-vis thecompany along with criteria of making payments to NEDs shall be disclosed in th l p t

compensation guidelines should include general principles for d t i i th

directors of the quality required to run the company successfully

(Immediate) aggregate remuneration in the annual report

the annual report

Reliance Industries (for NEDs):Per meeting: INR 20KCommission: INR

determining the form and amount of director compensation

HSBC:Annual Board Fee: GBP 95KCommittee Fee:Member: 30KCommission: INR

2.1mln Member: 30KChairman: 50K

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance Codes – A Comparison

CG Code 2012 CG Code 2002 India USA U.K.

Audit CommitteeAudit Committee

Committees

Composition of HR:

Audit Committee

Human Resources and Remuneration Audit Committee

Audit Committee

Shareholders/Investors Grievance Committee

Nominating/CG committee with all independent directors

Audit Committee

Nomination Committee with majority NEDs

(Immediate) Committee introduced May set up a remuneration committee

Compensation committee with all independent directors

The IA may be

Internal Audit

The IA may be outsourced or be performed by the IA staff of the holding company

There shall be an IA function

Th h d f IA

No specific provisions although referred to

Mandatory to have an internal audit function

Not mandatory

Reasons for not

(Immediate)When outsourced, the company shall appoint or designate a fulltime employee other than the CFO, as Head of IA

The head of IA shall have access to the chair of the Audit Committee

gwithin the code on several occasions

A company may choose to outsource this function

having one must be disclosed in annual report

IA

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance Codes – A ComparisonCG Code 2012 CG Code 2002 India USA U.K.

The Chairman shall be an independent

Minimum 3 members and 2/3rd should be independent

AuditCommittee

Composition:(Next

be an independent director, who shall not be the chairman of the board

At least 3 NEDs

independent

All members of audit committee shall be financially literate and at least 1 member shall

Minimum 3 members

At least 3, or in the (Next election)

Frequency of meetings,

At least 1 member should have recent and relevant financial experience

The Chairman of shall preferably be NED

have accounting or related financial management expertise

Chairman shall be an i d d di

All members of audit committee shall be financially literate and at least one member shall h i

case of smaller companies 2, independent non executive directors

A l 1 bg ,attendance, terms of reference and reporting procedures:(Immediate)

At least quarterly meetings

The secretary of BAC shall either be the CS

Appoint a secretary of the Committee

independent director

Chairman BAC to be present at AGMs

CS as secretary

have accounting or related financial management expertise

All members must

At least 1 member should have recent and relevant financial experience

shall either be the CS or Head of IA

CFO shall not be appointed as the secretary to the BAC

CS as secretary

Meetings: at least 4times a year and not more than four months shall elapse between

All members must be independent

two meetings

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance Codes – Best Practices

India (Holding Company’s role w.r.t to Subsidiaries)

At least one independent director of the holding company shall be a director of a material non-listed Indian subsidiary company (exceeds 20% of the consolidated turnover or net worth of group)

The BAC shall review the financial statements, in particular, the The B C shall review the financial statements, in particular, theinvestments made by the unlisted subsidiary

The board meetings minutes of the unlisted subsidiary shall be placed at the meeting of the listed holding company

USA

Companies must schedule regular executive sessions in which those directors meet without

All significant transactions and arrangements entered into by the unlisted subsidiary company should be periodically reported to the Board of Directors of the listed holding company

executive participation

Johnson & Johnson: The independent directors will meet in regular executive sessions without any non independent directors or memberswithout any non-independent directors or members of management present at least four times each year. In addition, the independent directors will hold private meetings with the Chairman and the CEO on a regular basis

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance Codes – Best Practices

Chairman’s Role

Set board’s agenda and ensure that adequate time is available for discussion of all agenda items, in particular strategic issues

Promote a culture of openness and debate by facilitating the effective contribution of NEDs in particularof NEDs in particular

Ensure constructive relations between executive and NEDs

Ensure that the directors receive accurate, timely and clear information.

Ensure effective communication with shareholders Chairman of Committees

Chairman of the board should not be Chairman of U.K.

any committee

Chairman of Committees should ideally be independent di t

The board should appoint one of the independent NEDs to be the senior independent director

Reliance Industries: Has appointed a Lead Independent Director

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

directorsReliance Industries: Has appointed a Lead Independent Director

Corporate Governance Codes – Best Practices

IFC

Annual off-site sessions dedicated for strategy-related discussionAnnual off site sessions dedicated for strategy related discussion

Engro Corp: Not off-site but every year Engro’s board dedicates a complete working week for such deliberations

A l b d l d h ld b i i dAnnual board calendar should be maintained

Gender diversity is encouraged on boards

Pakistan: 13% of 303 publically listed companies surveyed in 2010 had more than 1 woman directorf p y p y

Board Size: Too few may result in inadequate oversight, or lack of understanding of certain key issues, and too many may make execution and decision making problematic

AustraliaAustralia

Companies should disclose the process for evaluating the performance of senior executives

Companies should disclose the process for evaluating the performance of the board, its committees and

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

individual directors

Corporate Governance AssessmentsCommon Observations/Key Learning

Vision/mission of the entities is unclear. Disconnect amongst directors with regards to company’s strategy

Focus on Risk Management is low in the corporate sector

Although the board has a requisite skill mix, directors are not vocal/participative enoughg

A strong commitment towards enhancing CG practices is key to improving governance

Documentation of policies & processes is not given due consideration. This is essential for sustainability of good practices

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

Corporate Governance – Quotable Quotes

“Curiosity, courage, and persistence are th ti l q liti f b d

“What matters most is not the techniques used in risk measurement. it’s culture.”

among the essential qualities of a board member.”

a former executive and director of a European bank

a Chief Risk Officer of a bank in Central Asia

“Bankers sometimes think that risk management is about not taking risks. How wrong. if bankers didn’t take risks, then what would i have to manage?”g

a Chief Risk Officer of a bank in Central Asia

“one Wall street executive admits that it would not be too difficult for him to presentone Wall street executive admits that it would not be too difficult for him to present financial information to this board ‘in such a complex way, that people would be prevented from asking whether the emperor is naked, for fear of looking stupid.’”

CG – The Hue & Cry!

The Local Perspective

CG Codes – a Comparison Best Practices Conclusion

BIBLIOGRAPHY

The Cadbury Report, The Financial Aspects of Corporate Governance (1992)http://www.ecgi.org/codes/documents/cadbury.pdf

Code of CG Pakistan (2012) http://www.secp.gov.pk/corporatelaws/pdf/Code-CorporateGovernance-2012.pdf

Code of Corporate Governance (2002)CG Principles & Recommendations, Australia (2007)http://www.ecgi.org/codes/documents/corp_governance_principles_asx_2007.pdf

OECD Principles of Corporate Governance (2004)http://www.oecd.org/corporate/corporateaffairs/corporategovernanceprincipl

Code of Corporate Governance (2002)http://www.secp.gov.pk/corporatelaws/pdf/CodeofCorporateGovernance.pdf

Corporate Governance Development Framework (2011)http://www1.ifc.org/wps/wcm/connect/52e2e6804a7184689953dbe6e3180238/Corporate%2BGovernance%2BDevelopment%2BFramework.pdf?MOD=AJPEREShttp://www.cgdevelopmentframework.com/p g p p p g p p

es/31557724.pdf

A Review of Corporate Governance in UK Banks and Other Financial Industry Entities, Final Recommendations (26 November 2009)http://webarchive.nationalarchives.gov.uk/+/http:/www.hm-treasury.gov.uk/d/walker_review_261109.pdf

p g p

Governing Banks (2010)http://www1.ifc.org/wps/wcm/connect/5be7ea004c34430d98fedaf12db12449/Governing+Banks+Supplement_Final+Publication.pdf?MOD=AJPERES

Clause 49: Quarterly Corporate Governance Report

The UK Code of Corporate Governance (2010) http://www.frc.org.uk/getattachment/a7f0aa3a-57dd-4341-b3e8-ffa99899e154/UK-Corporate-Governance-Code-September-2012.aspx

Malaysia Code on Corporate Governance (2012)http://www.sc.com.my/eng/html/cg/cg2012.pdf

Bombay Stock Exchangehttp://www.bseindia.com/Static/about/downloads.aspx?expandable=2

Corporate Governance Voluntary Guidelines (2009)http://www.mca.gov.in/Ministry/latestnews/CG_Voluntary_Guidelines_2009_24dec2009.pdfhttp://www.sc.com.my/eng/html/cg/cg2012.pdf

NYSE Listing Rules (2003) http://www.nyse.com/pdfs/finalcorpgovrules.pdf

Report of the New York Stock Exchange Commission on Corporate Governance (September 23, 2010)

// / /

09.pdf

Survey of Board Practices in Pakistan (2011)http://www.icap.org.pk/mies/MIES_28.pdf

The Irresistible Case for Corporate Governance, IFC (2006)http://www1.ifc.org/wps/wcm/connect/966ad18048a7e6e3a8d7ef6060ad5911/Irresisti

http://www.nyse.com/pdfs/CCGReport.pdf bleCase4CG.pdf?MOD=AJPERES

DISCLAIMER

PACRA h d d i i f hi d O i f iPACRA has used due care in preparation of this document. Our informationhas been obtained from sources we consider to be reliable but its accuracy orcompleteness is not guaranteed. The information in this document may becopied or otherwise reproduced, stored or disseminated in whole or in part inp p , pany form or by any means whatsoever by any person, provided the source isduly acknowledged.

Th t ti h ld t b li d f i l d i IThe presentation should not be relied upon as professional advice. Inaddition, the presentation is not meant to be an endorsement by PACRA ofgovernance framework of any country.

Th k !!Thank you!!