old dominion university director’s message hampton roads real … · 2020-03-13 · 1 old...

TRANSCRIPT

1

Old Dominion University Hampton Roads Real Estate

Market Review and Forecast2007

Presented by: E.V. Williams

Center for Real Estate and Economic Development

Director’s Message

John R. Lombard, PhDAssistant Professor, Department of

Urban Studies and Public Administration, College of Business and Public Administration

Director, E. V. Williams Center for Real Estate and Economic Development

A Message from the Dean

Nancy Bagranoff, DBADean, College of Business

& Public Administration, Old Dominion University

Executive CommitteeExecutive Committee

Chair: Joyce HartmanExecutive Director: John LombardVice Chair: Tom DillonPrograms Chair: Stephanie SankerPublications Chair: Brian DundonMembership Chair: Craig CopeCurriculum Co-Chairs: John Crunkleton, Brad SanfordSponsorship Chair: Cliff MooreBy-Laws Chair: Andrew KeeneyPast Chair: William E. KingAt Large: Jonathan Guion

Aubrey Layne

Sponsorship CommitteeSponsorship Committee

Cliff Moore, W.M. JordanBrad Sanford, Dominion Realty AdvisorsLarry Colorito, Axial Advisory Group

Program CommitteeProgram Committee

Stephanie Sanker, GVA AdvantisJoyce Hartman, Sperry Van Ness

Peggy Koch, GVA AdvantisDavid Chapman, Old Dominion University

2

Research Committee

Brian Dundon, Brian J. Dundon & Assoc. John Lombard, PhD, ODU

Beth Hancock, City of ChesapeakeJoy Learn, Resource Bank

Sandi Prestridge, City of NorfolkMaureen Rooks, Thalhimer

Bradley Sanford, Dominion Realty AdvisorsLane Shea, Harbor Group

Kristi Sutphin, City of Portsmouth

Our Proud SponsorsAtlantic Mortgage & Investment

Axial Advisory GroupBank of America

BB&TThe Breeden Company

Burgess & NippleCavalier Land, Inc.CB Richard Ellis

Chesapeake Economic DevelopmentCherry, Bekaert & Holland, LLP

Clancy & TheysClark Nexsen

CMSS ArchitectsCollins Enterprises

Continental Realty Services, Inc.CoStar Group

CREWCreative Office Environments

Davenport - Lefcoe DevelopmentDominion Realty Advisors

Drucker and Falk, LLCEmporia - Greensville Industrial Development Corp.

First American Title Insurance CompanyFirst Potomac Realty Trust

Great Atlantic Management CompanyGVA Advantis

Hampton Economic DevelopmentHarbor Group International

Our Proud SponsorsHayes, Seay, Mattern & Mattern, Inc.

Kaufman & CanolesLandMark Design Group

Laureate Capital Mortgage BankersLiberty Property Trust

McDonald Development CompanyMideastern Builders

The Morgan Real Estate GroupNAI Harvey Lindsay

Nancy Chandler & Associates, RealtorsNewport News Economic Development Authority

Norfolk Economic DevelopmentPortsmouth Economic Development

Resource BankRose and Womble Realty Co.

Runnymede CorporationS.L. Nusbaum Realty Company

Sam Segar & AssociatesSperry Van Ness Commercial Real Estate Advisors

Suffolk Economic DevelopmentSun Trust Real Estate Finance Group

Thalhimer Cushman WakefieldTowne Bank

Tri City Developers, LLCVirginia Beach Economic Development

Vanasse Hangen Brustlin, Inc.Williams Mullen

W.M. Jordan CompanyWall, Einhorn & Chernitzer, P.C.

Wexford Science & Technology, LLC

Special thank you to

Inside Businessfor their sponsorship

over the past five

years.

Residential Market Review

J. Van Rose, Jr. MIRMPresident

Rose & Womble Enterprises

Principal Owner of Rose & Womble Realty

Lifetime Teacher & Motivator

Travels the country sharing his knowledge and unique perspective.

15 Year New Construction and Resale History

0

50 0 0

10 0 0 0

150 0 0

2 0 0 0 0

2 50 0 0

19 9 2 19 9 3 19 9 4 19 9 5 19 9 6 19 9 7 19 9 8 19 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6

Resale NC

3

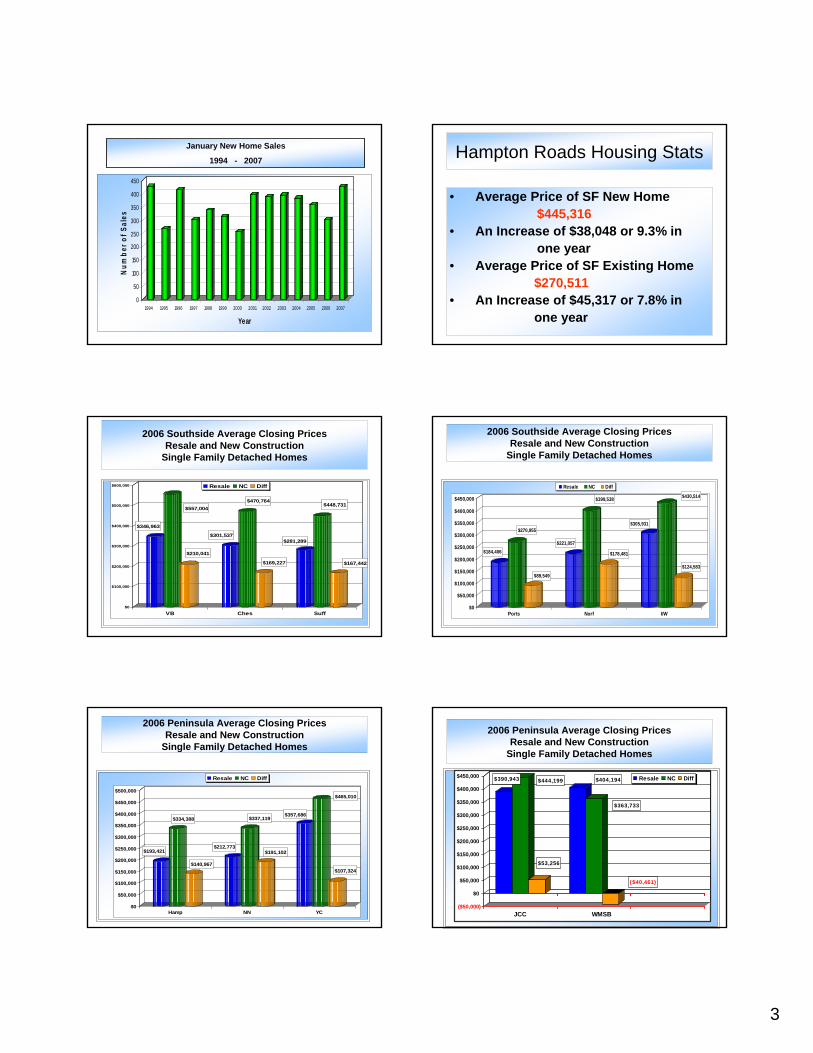

January New Home Sales

1994 - 2007

0

50

100

150

200

250

300

350

400

450

Num

ber o

f Sal

es

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Year

Hampton Roads Housing Stats

• Average Price of SF New Home$445,316

• An Increase of $38,048 or 9.3% in one year

• Average Price of SF Existing Home$270,511

• An Increase of $45,317 or 7.8% inone year

$346,963

$557,004

$210,041

$301,537

$470,764

$169,227

$281,289

$448,731

$167,442

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

VB Ches Suff

Resale NC Diff

2006 Southside Average Closing PricesResale and New Construction

Single Family Detached Homes

$184,406

$270,955

$89,549

$221,057

$399,538

$178,481

$305,931

$430,514

$124,583

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

Ports Norf I/W

Resale NC Diff

2006 Southside Average Closing PricesResale and New Construction

Single Family Detached Homes

2006 Peninsula Average Closing PricesResale and New Construction

Single Family Detached Homes

$193,421

$334,388

$140,967

$212,773

$337,119

$191,102

$357,686

$465,010

$107,324

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

Hamp NN YC

Resale NC Diff $390,943 $444,199

$53,256

$404,194

$363,733

($40,461)

($50,000)

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

JCC WMSB

Resale NC Diff

2006 Peninsula Average Closing PricesResale and New Construction

Single Family Detached Homes

4

A Market

In Transition

Sales By MonthJan 2005 through Nov 2006

0

500

1000

1500

2000

2500

3000

Uni

ts p

er M

onth

Jan

05

Feb

05

Mar

05

Apr

05

May

05

Jun

05

Jul 0

5

Aug

05

Sep

05

Oct

05

Nov

05

Dec

05

Jan

06

Feb

06

Mar

06

Apr

06

May

06

Jun

06

Jul 0

6

Aug

06

Sep

06

Oct

06

Nov

06

DateNew ConstructionResale

Growth of Home Sizes & Price Per S. F.

2003 $260K $104 SF

2,570 SF

2004 $327K $123 SF

2,673 SF

2005 $416K $149 SF

2,781 SF

2006 $445 $161 SF

2,672 SF

2007 $394 $152 SF

2,589 SF 0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%>$1000K

$901K-$1000K

$801K-$900K

$701K-800K

$601K-$700K

$501K-$600K

$401K-$500K

<$401K

New Construction Price Points

61%

New Construction Product Mix

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1

Mixed Use

High Rise

Tow nhome

Att Condo

SFD Condo

SFD Custom

SFD Production46%

7%

4%

31%

8%

3%1%

Current Active Listings by Month

0

2,000

4,000

6,000

8,000

10,000

12,000

Uni

ts

Janu

ary

Februa

ry

March

April

MayJu

ne July

Augus

t

Septem

ber

Octobe

r

Novem

ber

Decem

ber

Month

2004 2005 2006

5

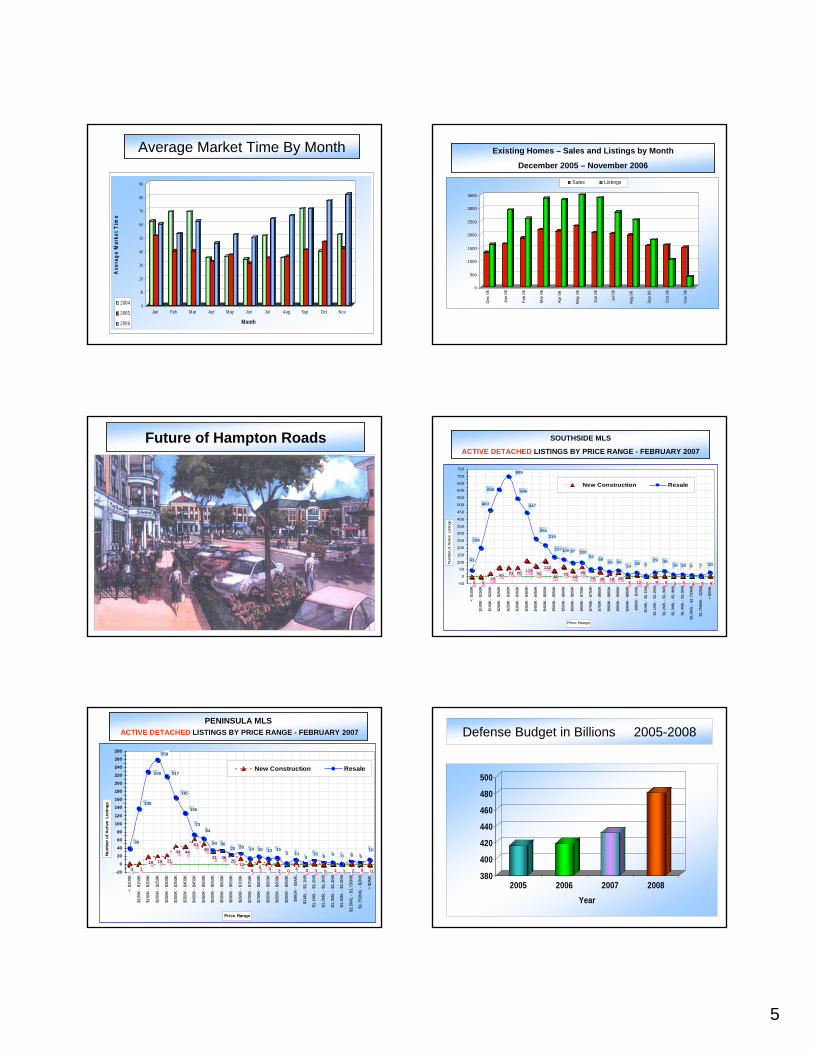

Average Market Time By Month

0

10

20

30

40

50

60

70

80

90

Ave

rage

Mar

ket T

ime

Jan Feb M ar Apr M ay Jun Jul Aug Sep Oct Nov

Month

2004

2005

2006

Existing Homes – Sales and Listings by Month

December 2005 – November 2006

0

500

1000

1500

2000

2500

3000

3500

Dec

05

Jan

06

Feb

06

Mar

06

Apr 0

6

May

06

Jun

06

Jul 0

6

Aug

06

Sep

06

Oct

06

Nov

06

Sales Listings

Future of Hampton Roads SOUTHSIDE MLS

ACTIVE DETACHED LISTINGS BY PRICE RANGE - FEBRUARY 2007

0 6644358512429183650

65447044

11276

11360616520

0

43

199

52

307915163929

52814

433359

10097120137

219264

699

608

463 447

545

-50

0

50

100

150

200

250

300

350

400

450

500

550

600

650

700

750<

$10

0K

$100

K - $

150K

$150

K - $

200K

$200

K - $

250K

$250

K - $

300K

$300

K - $

350K

$350

K - $

400K

$400

K - $

450K

$450

K - $

500K

$500

K - $

550K

$550

K - $

600K

$600

K - $

650K

$650

K - $

700K

$700

K - $

750K

$750

K - $

800K

$800

K - $

850K

$850

K - $

900K

$900

K - $

950K

$950

K - $

1MIL

$1M

IL -

$1.1

MIL

$1.1

MIL

- $1

.2M

IL

$1.2

MIL

- $1

.3M

IL

$1.3

MIL

- $1

.4M

IL

$1.4

MIL

- $1

.5M

IL

$1.5

MIL

- $1

.750

MIL

$1.7

50M

IL -

$2M

IL

> $2

MIL

Price Range

Num

ber o

f Act

ive

Lis

tings

New Construction Resale

PENINSULA MLSACTIVE DETACHED LISTINGS BY PRICE RANGE - FEBRUARY 2007

0 00211030202362

1325

3631

4961

4444

2119181

39

138

14 105804610

4112

15131928253634

6473

217

258

229

126

165

-20

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

< $

100K

$100

K - $

150K

$150

K - $

200K

$200

K - $

250K

$250

K - $

300K

$300

K - $

350K

$350

K - $

400K

$400

K - $

450K

$450

K - $

500K

$500

K - $

550K

$550

K - $

600K

$600

K - $

650K

$650

K - $

700K

$700

K - $

750K

$750

K - $

800K

$800

K - $

850K

$850

K - $

900K

$900

K - $

950K

$950

K - $

1MIL

$1M

IL -

$1.1

MIL

$1.1

MIL

- $1

.2M

IL

$1.2

MIL

- $1

.3M

IL

$1.3

MIL

- $1

.4M

IL

$1.4

MIL

- $1

.5M

IL

$1.5

MIL

- $1

.750

MIL

$1.7

50M

IL -

$2M

IL

> $2

MIL

Price Range

Num

ber o

f Act

ive

Lis

tings

New Construction Resale

380

400

420

440

460

480

500

2005 2006 2007 2008Year

Defense Budget in Billions 2005-2008

6

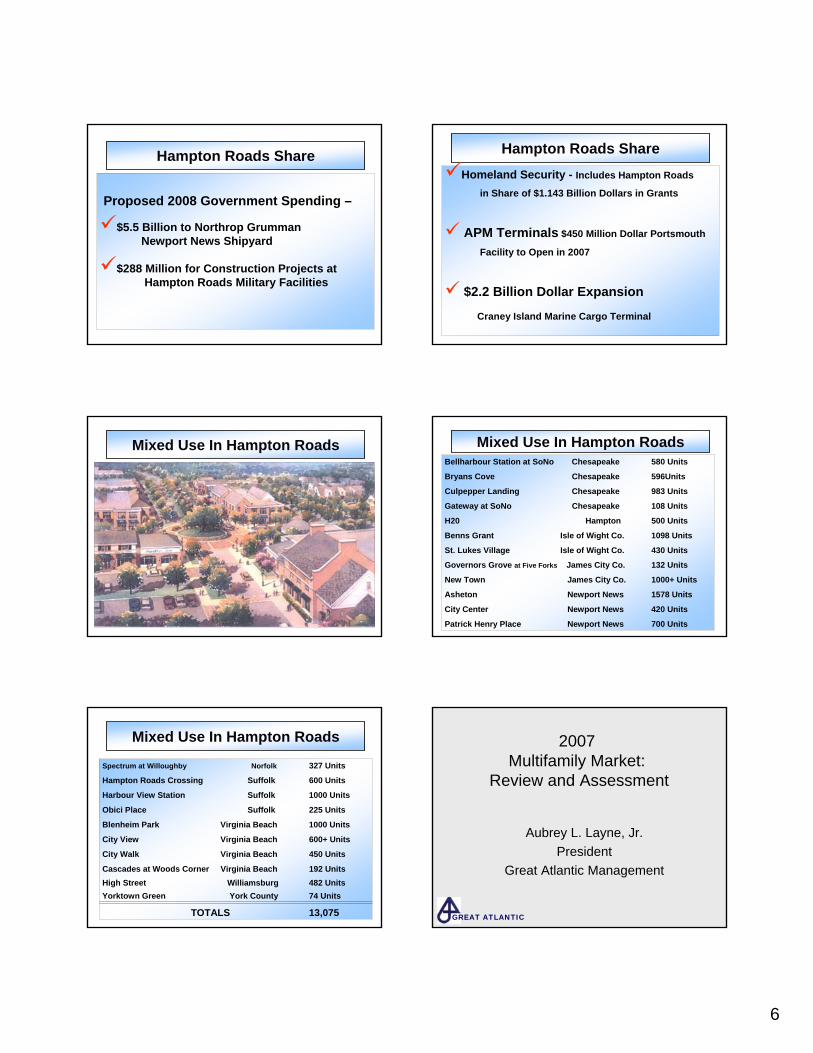

Hampton Roads Share

Proposed 2008 Government Spending –

$5.5 Billion to Northrop Grumman Newport News Shipyard

$288 Million for Construction Projects at Hampton Roads Military Facilities

Hampton Roads ShareHomeland Security - Includes Hampton Roads

in Share of $1.143 Billion Dollars in Grants

APM Terminals $450 Million Dollar Portsmouth

Facility to Open in 2007

$2.2 Billion Dollar Expansion

Craney Island Marine Cargo Terminal

Mixed Use In Hampton Roads Mixed Use In Hampton RoadsBellharbour Station at SoNo Chesapeake 580 Units

Bryans Cove Chesapeake 596Units

Culpepper Landing Chesapeake 983 Units

Gateway at SoNo Chesapeake 108 Units

H20 Hampton 500 Units

Benns Grant Isle of Wight Co. 1098 Units

St. Lukes Village Isle of Wight Co. 430 Units

Governors Grove at Five Forks James City Co. 132 Units

New Town James City Co. 1000+ Units

Asheton Newport News 1578 Units

City Center Newport News 420 Units

Patrick Henry Place Newport News 700 Units

Mixed Use In Hampton Roads

Spectrum at Willoughby Norfolk 327 Units

Hampton Roads Crossing Suffolk 600 Units

Harbour View Station Suffolk 1000 Units

Obici Place Suffolk 225 Units

Blenheim Park Virginia Beach 1000 Units

City View Virginia Beach 600+ Units

City Walk Virginia Beach 450 Units

Cascades at Woods Corner Virginia Beach 192 UnitsHigh Street Williamsburg 482 UnitsYorktown Green York County 74 Units

TOTALS 13,075

2007Multifamily Market:

Review and Assessment

Aubrey L. Layne, Jr.President

Great Atlantic Management

GREAT ATLANTIC

7

•Deal Activity and Headlines

•Economic and Operating Environment

•Outlook

Deal Activity Deal Activity -- 20062006

••Unit Volume DownUnit Volume Down

••Core Pricing FlatCore Pricing Flat

HR Apartment Deal Volume and Price

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1998 1999 2000 2001 2002 2003 2004 2005 2006

volu

me

in u

nits

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

pric

e in

$

volume priceSources: Great Atlantic, Real Data

8

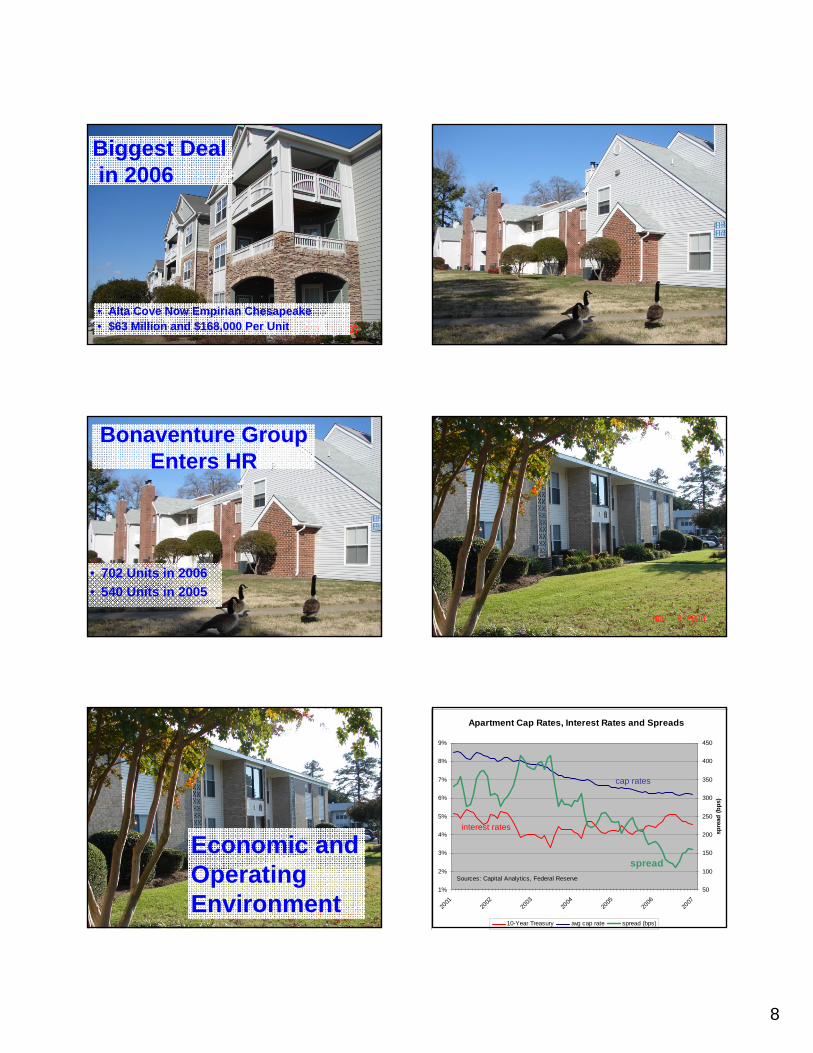

Biggest Dealin 2006

• Alta Cove Now Empirian Chesapeake• $63 Million and $168,000 Per Unit

Bonaventure Group Enters HR

• 702 Units in 2006• 540 Units in 2005

Economic and Operating Environment

Apartment Cap Rates, Interest Rates and Spreads

1%

2%

3%

4%

5%

6%

7%

8%

9%

2001

2002

2003

2004

2005

2006

2007

50

100

150

200

250

300

350

400

450

spre

ad (b

ps)

10-Year Treasury avg cap rate spread (bps)

cap rates

interest rates

spreadSources: Capital Analytics, Federal Reserve

9

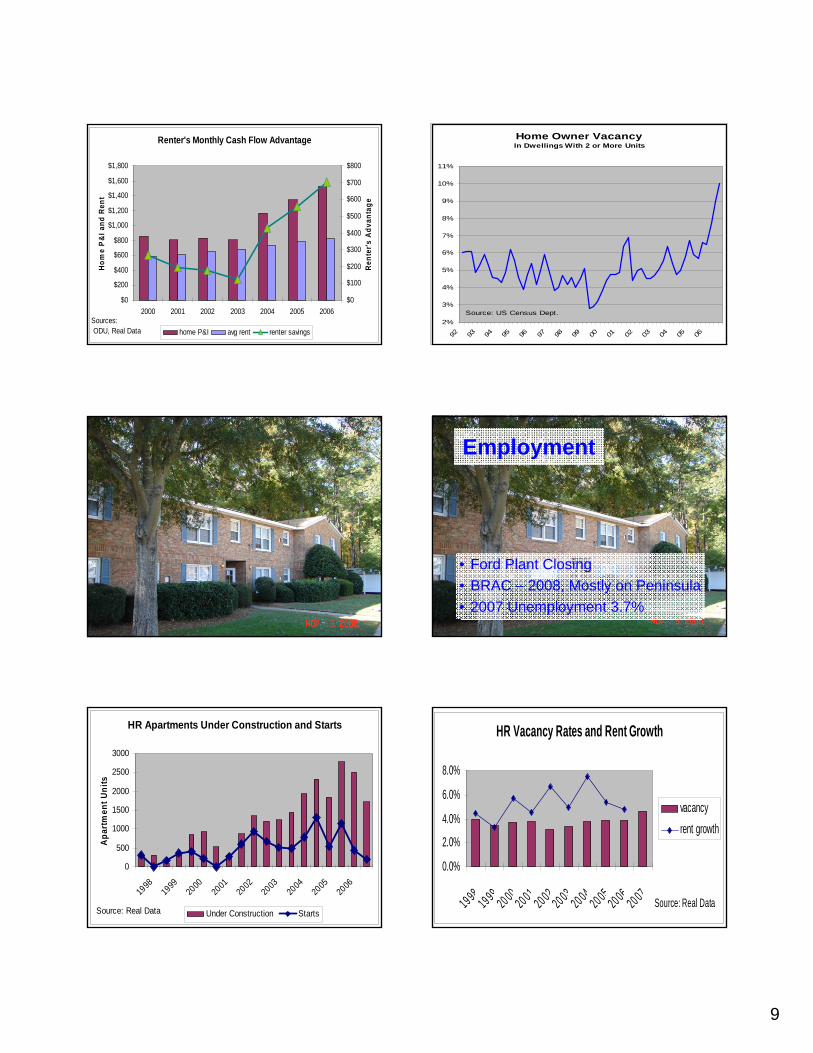

Renter's Monthly Cash Flow Advantage

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2000 2001 2002 2003 2004 2005 2006

Hom

e P

&I a

nd R

ent

$0

$100

$200

$300

$400

$500

$600

$700

$800

Rent

er's

Adv

anta

ge

home P&I avg rent renter savingsSources: ODU, Real Data

Home Owner VacancyIn Dwellings With 2 or More Units

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

Source: US Census Dept.

Employment

• Ford Plant Closing • BRAC – 2008, Mostly on Peninsula• 2007 Unemployment 3.7%

HR Apartments Under Construction and Starts

0

500

1000

1500

2000

2500

3000

1998

1999

2000

2001

2002

2003

2004

2005

2006

Apar

tmen

t Uni

ts

Under Construction StartsSource: Real Data

HR Vacancy Rates and Rent Growth

0.0%

2.0%

4.0%

6.0%

8.0%

19 9819 99

20 0020 01

20 0220 03

20 0420 05

20 0620 07

vacancyrent growth

Source: Real Data

10

HR Rent Growth and Core Inflation

0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006

HR Rent Growth Core Inflation

Sources: US Dept. of Labor, Real Data

• Buyers: Competitive Market• Sellers: Relatively High Prices• Owners: Positive Operating Environment• Renters: More Choice and Modestly

Higher Rents

Outlook - 2007 Office Market Review

Vivian Turok

Senior Vice President Office Leasing Division

Divaris Real Estate

30 years experience in office sales, leasing, tenant and landlord representation

Bachelor of Social ScienceUniversity of Cape Town

South Africa

Hampton Roads Historical Vacancy Rate Trends

7.8%

9.7%

11.8%

14.3% 13.1%

10.1%

8%6.9%

0

2

4

6

8

10

12

14

16

1999 2000 2001 2002 2003 2004 2005 2006

Office Market Rental Rates

•Class A = $20.00 per square foot

•Class B = $15.42 per square foot

•Class C = $12.39 per square foot

11

Pembroke Six, Virginia Beach

Interstate Corporate Center, Norfolk

Southern Boulevard, Virginia Beach

Social Security Building, Norfolk

Commonwealth of VirginiaLeases Signed in 2006

Convergence III, Virginia Beach

Rosemont Interstate Center, Virginia BeachWorld Trade Center, Norfolk

Amerigroup, Virginia Beach

Chesapeake Leases

12

Innovation Research Park

Lockheed Martin Modeling Center

2006 Developments

Gallery I and II, Virginia Beach Liberty III, Chesapeake

Central Center Office Building, Norfolk Amerigroup II, Virginia Beach

2006 Developments

BECO Building, ChesapeakeHRRA Building, Chesapeake

Bridgeway Technology Center, Suffolk

2006 Developments

Merchants Walk South, Newport News

One City Center,

Newport News

2007 Developments

Two Columbus Center, Virginia Beach

2007 Developments

Dominion Enterprises, Norfolk

Oakbrooke Professional Center, Chesapeake

Convergence III, Virginia Beach

Harbourview Medical Building, Suffolk

13

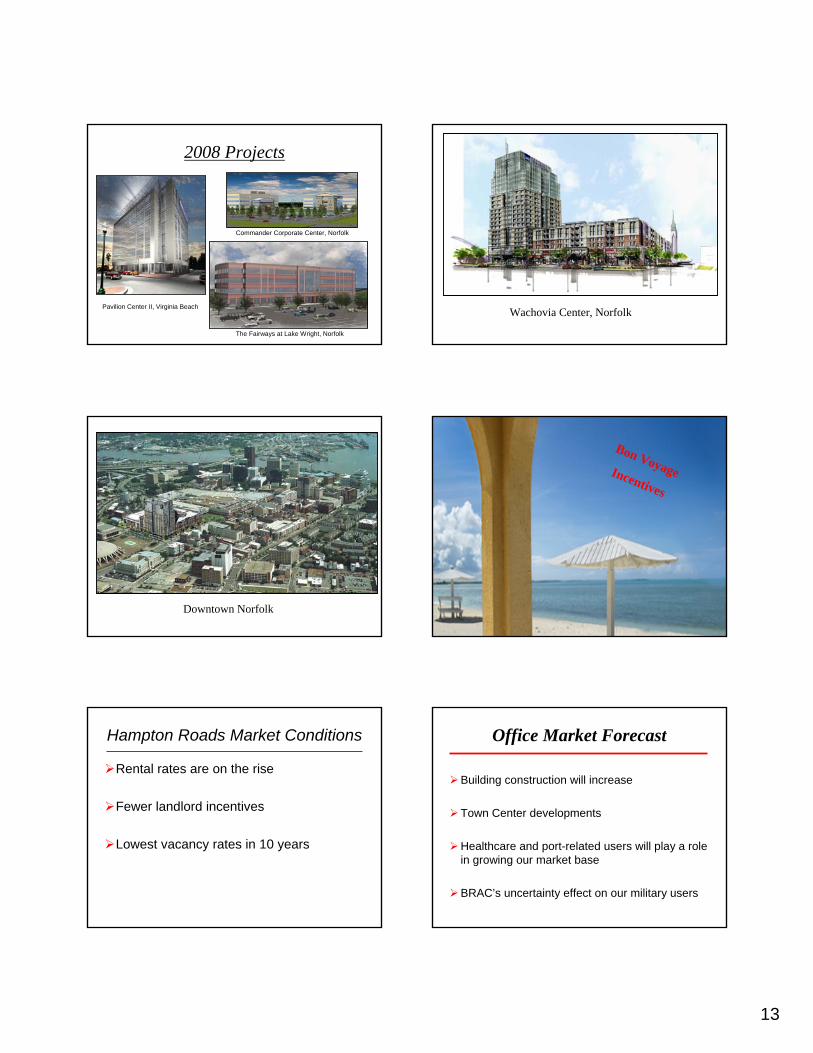

2008 Projects

Commander Corporate Center, Norfolk

Pavilion Center II, Virginia Beach

The Fairways at Lake Wright, Norfolk

Wachovia Center, Norfolk

Downtown Norfolk

Bon Voyage Incentives

Hampton Roads Market Conditions

Rental rates are on the rise

Fewer landlord incentives

Lowest vacancy rates in 10 years

Office Market Forecast

Building construction will increase

Town Center developments

Healthcare and port-related users will play a role in growing our market base

BRAC’s uncertainty effect on our military users

14

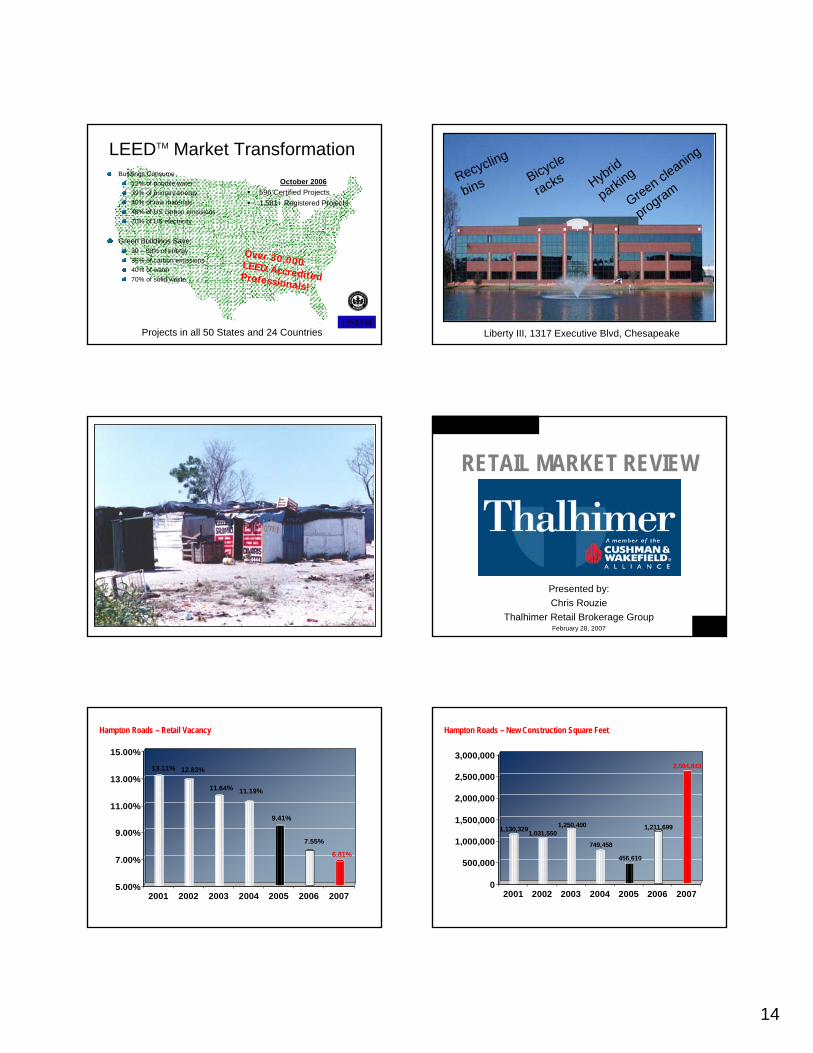

LEEDTM Market TransformationOctober 2006

596 Certified Projects1,581+ Registered Projects

Over 30,000 LEED Accredited Professionals!

Projects in all 50 States and 24 CountriesHSMM

Buildings Consume12% of potable water39% of primary energy40% of raw materials48% of US carbon emissions70% of US electricity

Green Buildings Save:30 – 50% of energy35% of carbon emissions40% of water70% of solid waste

Recycling

bins Bicycle

racks

Liberty III, 1317 Executive Blvd, Chesapeake

Hybrid

parking

Green cleaning

program

RETAIL MARKET REVIEW

Presented by:Chris Rouzie

Thalhimer Retail Brokerage GroupFebruary 28, 2007

13.11% 12.83%

11.64% 11.19%

9.41%

7.55%

6.81%

5.00%

7.00%

9.00%

11.00%

13.00%

15.00%

2001 2002 2003 2004 2005 2006 2007

Hampton Roads – Retail Vacancy

1,130,3291,031,5501,250,400

749,458

456,610

1,211,699

2,594,843

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

2001 2002 2003 2004 2005 2006 2007

Hampton Roads – New Construction Square Feet

15

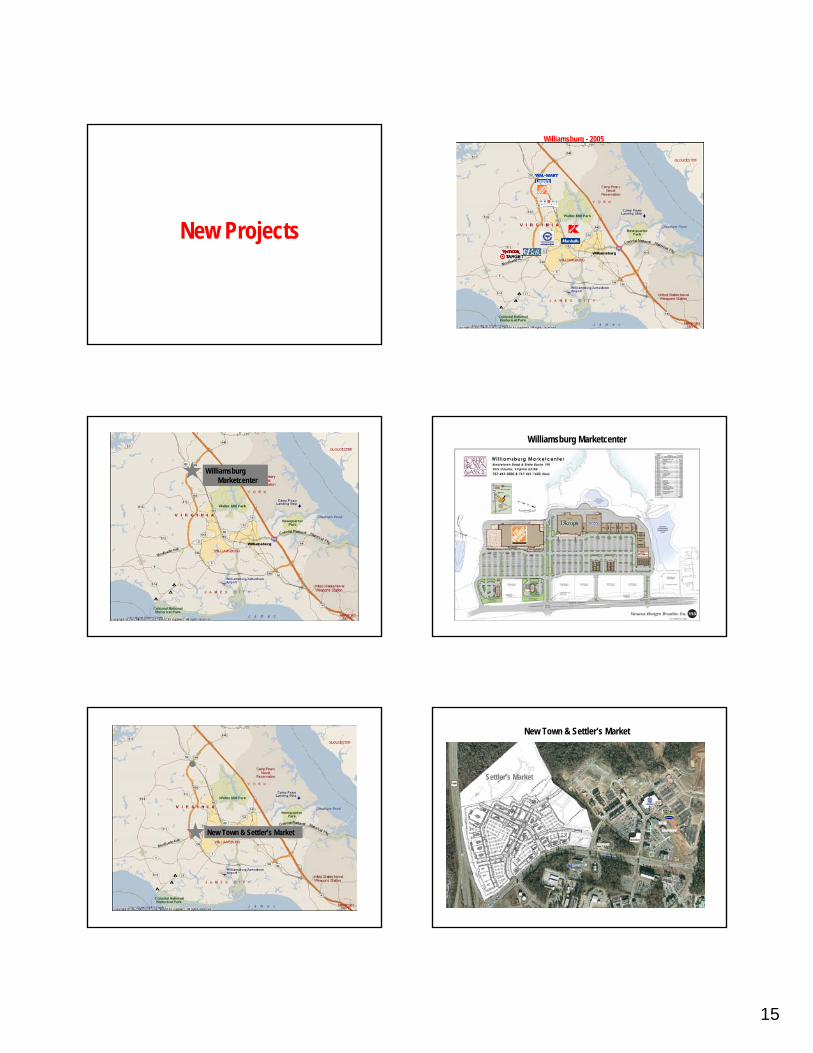

New Projects

Williamsburg - 2005

Williamsburg Marketcenter

Williamsburg Marketcenter

New Town

New Town & Settler’s Market

New Town & Settler’s Market

Settler’s Market New Town

16

Marquis Development

Marquis

City Center

City Center

Mercury Plaza

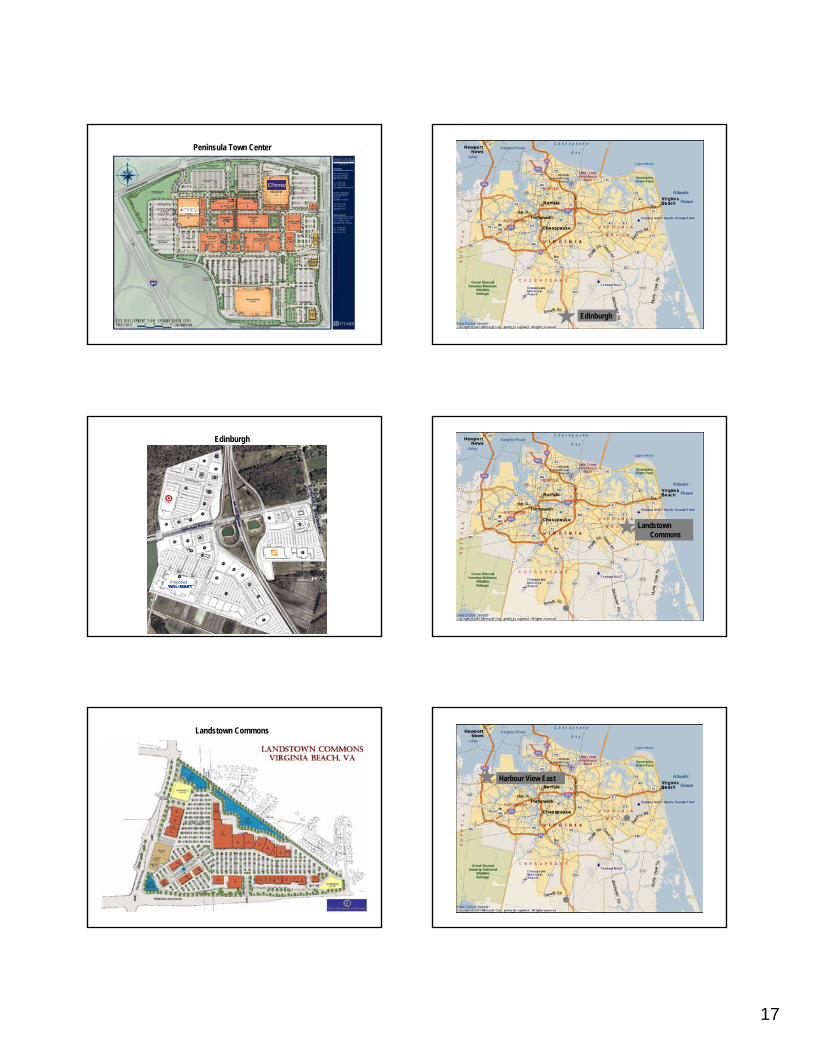

Peninsula Town Center

NetCenter

Mercury Plaza

17

Peninsula Town Center

Edinburgh

Edinburgh

Proposed

Landstown Commons

Landstown Commons

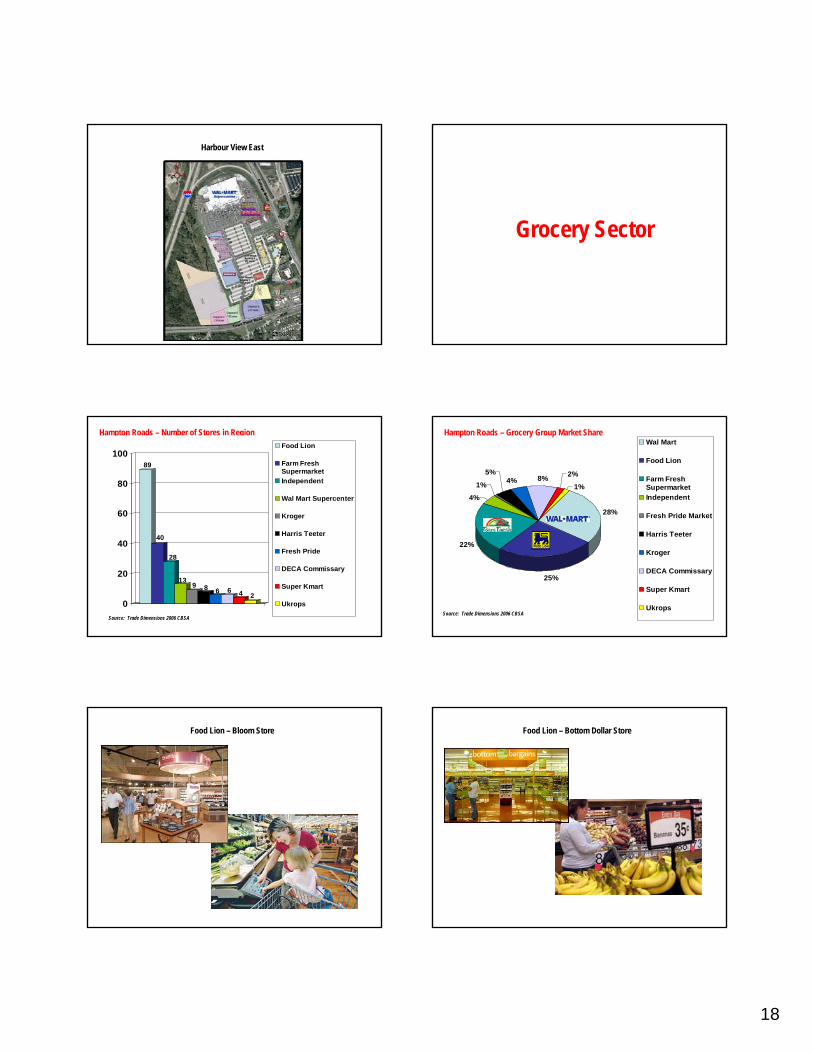

Harbour View East

18

Harbour View East

Grocery Sector

Hampton Roads – Number of Stores in Region

89

40

28

139 8 6 6 4 2

0

20

40

60

80

100Food Lion

Farm FreshSupermarketIndependent

Wal Mart Supercenter

Kroger

Harris Teeter

Fresh Pride

DECA Commissary

Super Kmart

Ukrops

Source: Trade Dimensions 2006 CBSA

28%

25%

22%

4%

1%

5%4% 8% 2%

1%

Wal Mart

Food Lion

Farm FreshSupermarketIndependent

Fresh Pride Market

Harris Teeter

Kroger

DECA Commissary

Super Kmart

Ukrops

Hampton Roads – Grocery Group Market Share

Source: Trade Dimensions 2006 CBSA

Food Lion – Bloom Store Food Lion – Bottom Dollar Store

19

Farm Fresh

Haygood Shopping Center

Mt. Pleasant Marketplace

Bennett’s CreekThe Market @ Harbor Heights

Orchard Square

Harris Teeter

Ferrell Parkway

Hanbury Village

Expanding Footprint

RETAIL MARKET REVIEW

Presented by:Chris Rouzie

Thalhimer Retail Brokerage GroupFebruary 28, 2007

Industrial Market Review

Clay Culbreth, SIOR, CCIM

GVA Advantis,Senior Director, Industrial Brokerage

20

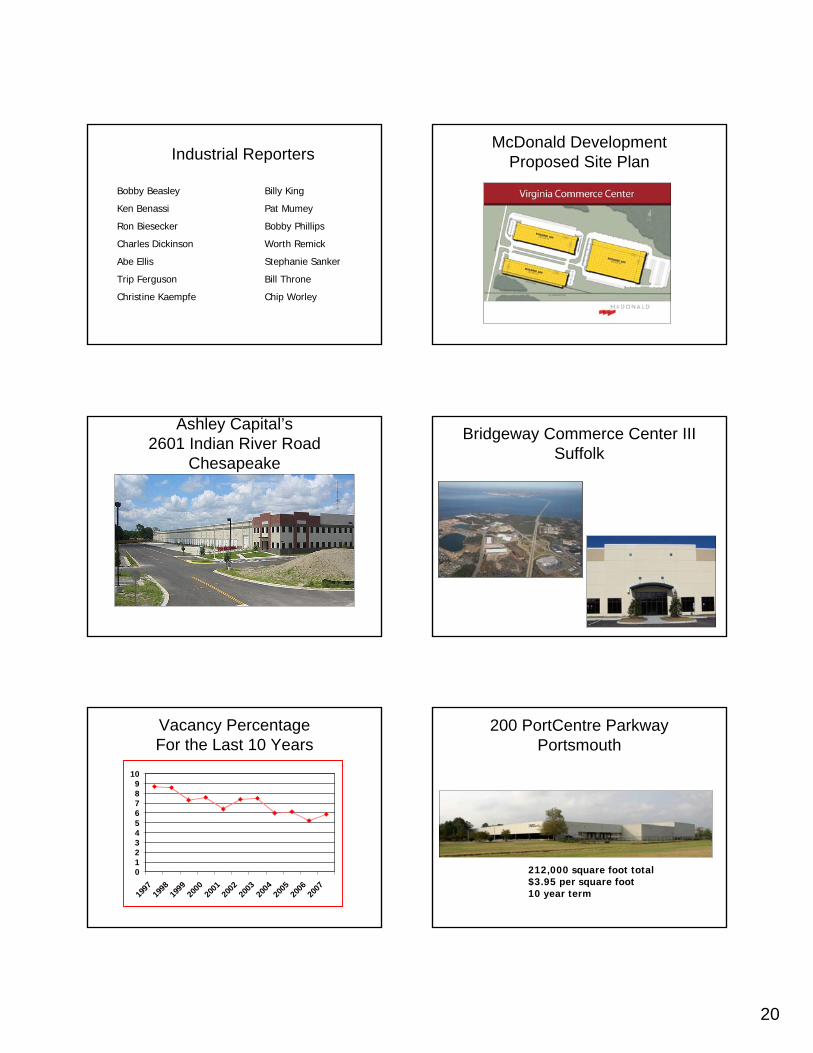

Industrial Reporters

Bobby Beasley Billy King

Ken Benassi Pat Mumey

Ron Biesecker Bobby Phillips

Charles Dickinson Worth Remick

Abe Ellis Stephanie Sanker

Trip Ferguson Bill Throne

Christine Kaempfe Chip Worley

McDonald Development Proposed Site Plan

Ashley Capital’s2601 Indian River Road

Chesapeake

Bridgeway Commerce Center IIISuffolk

Vacancy Percentage For the Last 10 Years

0123456789

10

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

200 PortCentre ParkwayPortsmouth

212,000 square foot total$3.95 per square foot10 year term

21

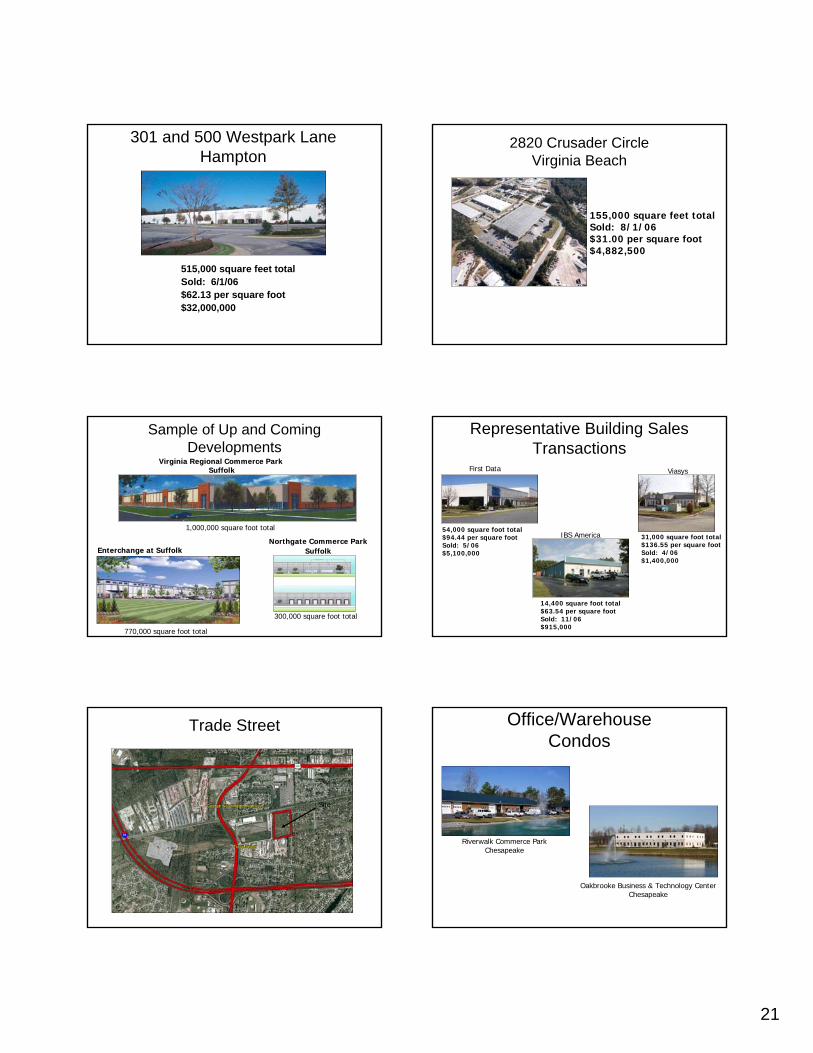

301 and 500 Westpark LaneHampton

515,000 square feet totalSold: 6/1/06$62.13 per square foot$32,000,000

2820 Crusader Circle Virginia Beach

155,000 square feet totalSold: 8/1/06$31.00 per square foot$4,882,500

Sample of Up and Coming Developments

Virginia Regional Commerce ParkVirginia Regional Commerce ParkSuffolkSuffolk

Northgate Commerce ParkNorthgate Commerce ParkSuffolkSuffolkEnterchange at SuffolkEnterchange at Suffolk

1,000,000 square foot total

300,000 square foot total

770,000 square foot total

Representative Building Sales Transactions

First Data

54,000 square foot total$94.44 per square footSold: 5/06$5,100,000

IBS America

14,400 square foot total$63.54 per square footSold: 11/06$915,000

Viasys

31,000 square foot total$136.55 per square footSold: 4/06$1,400,000

Trade Street

Site

Office/WarehouseCondos

Oakbrooke Business & Technology CenterChesapeake

Riverwalk Commerce ParkChesapeake

22

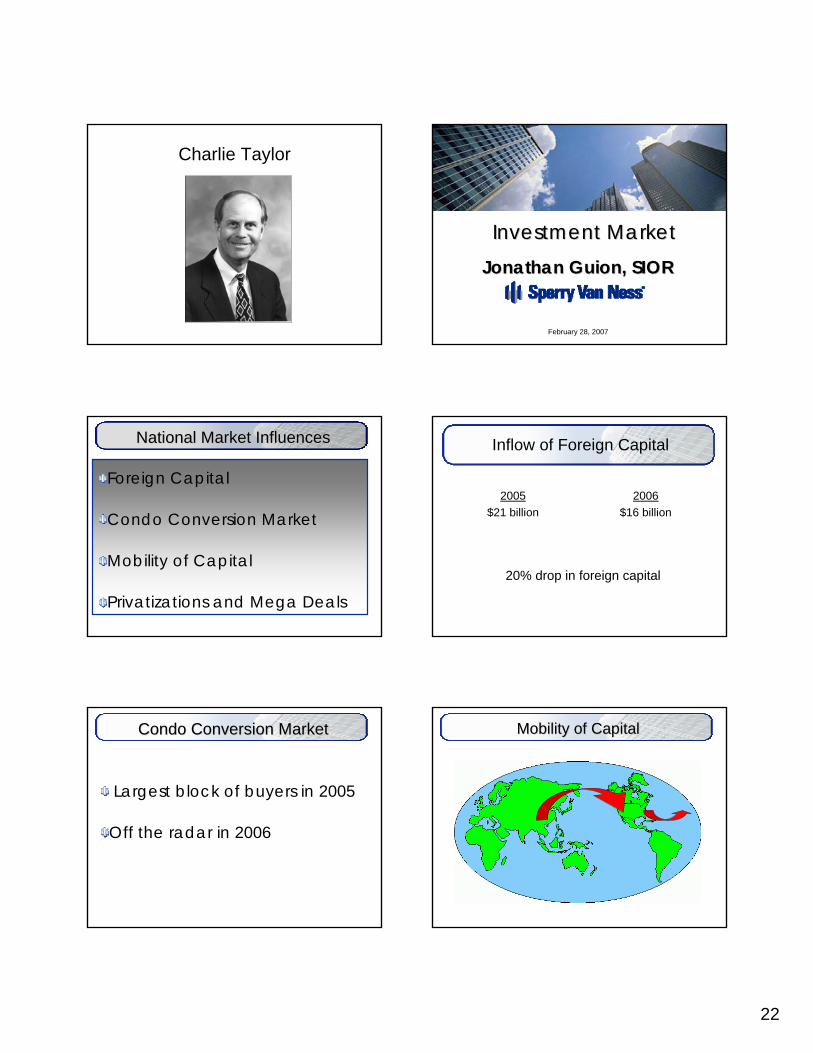

Charlie Taylor

Investment MarketInvestment Market

Jonathan Guion, SIORJonathan Guion, SIOR

February 28, 2007

National Market InfluencesNational Market Influences

Foreign Capital

Condo Conversion Market

Mobility of Capital

Privatizations and Mega Deals

Inflow of Foreign Capital

$16 billion$21 billion20062005

20% drop in foreign capital

Condo Conversion MarketCondo Conversion Market

Largest block of buyers in 2005

Off the radar in 2006

Mobility of CapitalMobility of Capital

23

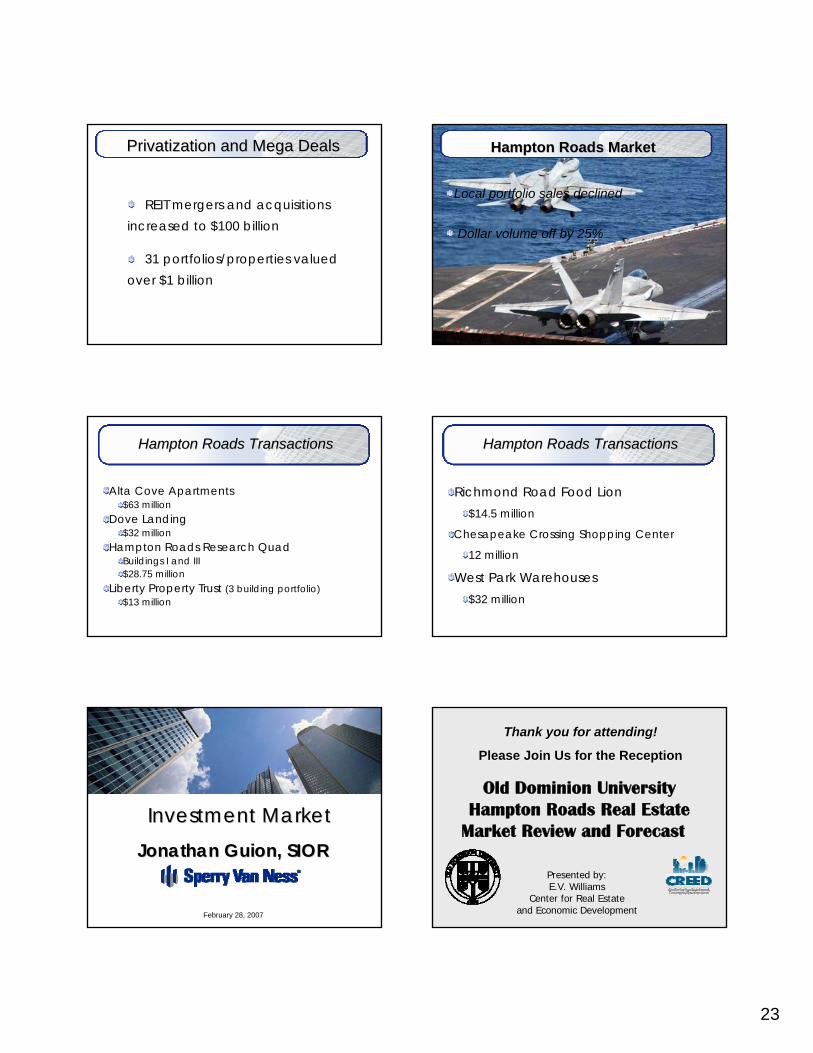

Privatization and Mega DealsPrivatization and Mega Deals

REIT mergers and acquisitions increased to $100 billion

31 portfolios/properties valued over $1 billion

Hampton Roads MarketHampton Roads Market

Local portfolio sales declined

Dollar volume off by 25%

Hampton Roads TransactionsHampton Roads Transactions

Alta Cove Apartments$63 million

Dove Landing$32 million

Hampton Roads Research QuadBuildings I and III$28.75 million

Liberty Property Trust (3 building portfolio)$13 million

Hampton Roads TransactionsHampton Roads Transactions

Richmond Road Food Lion$14.5 million

Chesapeake Crossing Shopping Center

12 million

West Park Warehouses$32 million

Investment MarketInvestment Market

Jonathan Guion, SIORJonathan Guion, SIOR

February 28, 2007

Old Dominion University Hampton Roads Real Estate

Market Review and Forecast

Thank you for attending!Thank you for attending!

Please Join Us for the ReceptionPlease Join Us for the Reception

Presented by: E.V. Williams

Center for Real Estate and Economic Development