oil & gas sector - inversionycomercio.org.ar · unconventional oil & gasand off-shore...

TRANSCRIPT

SEPT 13TH, 201614.30 -16.00

OIL & GAS SECTOR

AGENDA

Introduction: Global and Regional ContextPresented by Iván Martén, Senior Partner and Managing Director, The Boston Consulting Group

15 MIN.

25 MIN. The Government’s AgendaPresented by Juan José Aranguren, Minister of Energy & Mining

Investment OpportunitiesPresenters: José Luis Sureda – Secretary of Hydrocarbon Resources; Marcos Porteau – Undersecretary for Exploration and Production

15 MIN.

20 MIN.The Private Sector PerspectivePanelists: Miguel Gutiérrez, President -YPF; Marcos Bulgheroni, Board Member - PAE; Teófilo Lacroze, CEO - Shell Argentina; Gastón Remy, President - Dow Argentina and LATAM South Region

AGENDA

Q&A15 MIN.

Presented by Iván MarténSenior Partner and Managing Director

Global Leader Energy PracticeThe Boston Consulting Group

INTRODUCTION

GLOBAL DEMAND FOR OIL & GAS IS EXPECTED TO GROW MAINLY DRIVEN BY EMERGING MARKETS

0

50

100

150

1%

Mbpd1

20402030

115

2035

121109

2025

94100

2015

104

2020

OECDNon-OECD

1. GLOBAL DEMAND FOR OIL & GAS

2.1%

0%

2.7%

1.1%

1. Mbpd: million barrels per day 2. Tfc: Tera cubic feetSource: EIA IEO 2016 – Reference case scenario – BCG Analysis

Global oil demand Global natural gas demand

0

50

100

150

200

250

Tcf2

2020

149

124 133

2025 2030

167

2015

203185

2035

2%

2040

CAGRCAGR

Renewable energy sources Smart grids

Power Generation Transport Petrochemicals

Recycling and efficiency

~30% of global power

generation will come from

renewable sources by 2040

3% to 5% lower demand

from the power grid

Mature markets reaching saturation for plastics - growth

from 1.4 to 1 times

the rate of GDP

AICE1

Technology

AICEcould achieve 20% to 40% combustion efficiency

Electric Car

~35% of new cars

to be electric worldwide by 2030

1. AICE: Advanced Internal Combustion Engine

VTECHNOLOGICAL INNOVATIONS FOR CLEANER AND MORE EFFICIENT CONSUMPTION

WILL IMPACT FOSSIL FUELS DEMAND

1. GLOBAL DEMAND FOR OIL & GAS

Forecasted production (2016–2035)By play type—technical theme

Shale and tight oil & gas

Source: Rystad UCube (June 2016)Note – Production forecast includes potential new discoveries in the years ahead

Growth (Mboed)

Oil sands, Arctic & others

Off-shore

Onshore Russia

Onshore Middle East

Onshore RoW

4.70

19.60

11.86

-4.26

-0.49

-8.35

UNCONVENTIONAL OIL & GAS AND OFF-SHORE DEVELOPMENTS EXPECTED TO HAVE A LARGER ROLE IN SUPPLY

100

0

50

150

200

24%

2020

19%

2016

4%

10%

31%

22%

6%

17%

2025

+1%

12%

2030 2035

32%

16%17%

15%

Mboed

18%

28%

4%

14%

13%

CAGR

2. UNCONVENTIONAL & OFF-SHORE RELEVANCE

Note: Includes crude oil, condensate, NGLs and natural gas onlySource: Rystad energy UCube; BCG analysis

38%

FUTURE INCREASE IN PRODUCTION WILL BE DRIVEN BY OFF-SHORE

38% will come from off-shore fields not yet producing, many requiring new infrastructure

Off-shore will account for 91% of absolute growth between 2016–2030

38% of off-shore oil&gas production will come from fields not yet producing

2. UNCONVENTIONAL & OFF-SHORE RELEVANCE

0

60

120

180

Mboed

2030f2020f20102000

On-shoreOff-shore

100

75

50

25

02010 2020f2000 2030f

Mboed

Off-shore / producingOff-shore / non-producing

1.6%

1.2%

CAGR2000–2016

0.1%

1.9%

38%

62%

CAGR2016–2030

Fields not yet producing as of today

Note: Shale/Tight Gas production includes non-associated, oil-associated tight gas production. Crude /Condensate production includes shale/tight oil and high API C5+ liquidsSource: EIA (historical information 1990-2015), EIA 2016 Annual Energy Outlook, Rystad Energy, BCG Analysis

CAGR05–15

UNCONVENTIONAL PRODUCTION RELEVANCE WILL FURTHER INCREASE

Shale gas & shale oil already account respectively for ~65% and ~30% of US production

US Gas production 1990–2020 US Oil production 1990–2020

+40%

-4%

-5%

2. UNCONVENTIONAL & OFF-SHORE RELEVANCE

0

25

50

75

100

Other production

2020e00

Imports

1005

Bcf/d

90

Shale/Tight Gas

95 150

15

20

10

5

90 95 00 05 10

Mbbl/d

15 2020e

Forecast

Shale oil

Imports

Forecast

Other production

CAGR05–15

+46%

-3%

-1%

ARGENTINE UNCONVENTIONAL OPPORTUNITY IS COMPARABLE TO U.S. DEVELOPMENT

Quality and size is massive; risks and barriers are manageable

IOC's already recognized the opportunity and are deploying

activities in Neuquén

Vaca Muerta key geological parameters in line with US plays:

• 6% organic content• 200 m thickness

Low environmental risks and great potential upside

2030 Unconventional production Forecast: 2.0 – 4.0 Mbpd

2030 Unconventional production Forecast: 6.9 – 7.7 Mbpd

Stacked pay volumes, mainly in the Permian Basin, are relevant for future

shale US production

Resource bookings willincrease as slow adopters

catch-up with first movers and pursue stacked pay volumes

2. UNCONVENTIONAL & OFF-SHORE RELEVANCE

Production to increase in US as stacked pay volumes are pursued

Argentine unconventional shows an outstanding opportunity

Source: BCG Analysis

OIL PRODUCTION WILL BE VIABLE AT PRICES BETWEEN ~55-70 USD/BBL WITH EXISTING TECHNOLOGIES AND RESOURCES

3. SUPPLY CURVE

1. Includes crude oil, condensates and NGLsNote: breakeven prices are calculated considering all cash flows since approval year with a 10% discount rate Source: Rystad Energy UCube (18 April 2016 release)

Brent real oil price,USD/bbl (2015$)

Break-even price range considering 1Q and 3Q prod. Break-even price range considering 10% and 90% prod.

Under development fields

Onshore Middle EastOnshore rest of worldOff-shore shelf

Tight liquidsDeep water, heavy oils, and others

2020 forecasted production1 from new fields in Mbbld

Development potential

15141312111098762 54310

150

50

125

100

75

25

01716

off-shore shale

Global production from new fields and break-even pricesby types of projects – 2020, in USD/bbl

deepwater

Preconditions for success On localagenda

Competitiveness

Fiscal terms

Regulatory risk

Access to acreage

Prospectivity

• Long-term predictability• Ease of doing business

•National government and provinces coordination

•Potential for technically recoverable resources1

2345

• Technical complexity• Labor productivity• Logistic costs

• Taxes, royalties and bonuses–Returns offered vs. risks taken–Stability of conditions

4. PRECONDITIONS FOR SUCCESS

ARGENTINA IS ADDRESSINGINVESTORS NEEDS

Global demand for oil & gas is expected to grow mainly driven by emerging markets

Cost competitiveness will be key for the development of the oil & gas sector

Argentina is addressing key investor needs: access to acreage, competitiveness, fiscal terms and political & regulatory risks

Unconventional oil & gas and off-shore developments will have a more important role in supply, with Argentina enjoying a privileged position

SIGNIFICANT POTENTIAL OPPORTUNITIES FOR INVESTING IN ARGENTINA

Presented by Juan José Aranguren

Minister of Energy & Mining

THE GOVERNMENT´SAGENDA

+50 years of world class operations with major companies & skilled human capital

Top natural gas and oil producer in the region

50+ Operations and service providers – including top international players

100k +Qualified jobs and highly trained management

8+Universities & institutions specialized in oil & gas

50+ Years of developed world class operations

ARGENTINA IS A KEY OIL & GAS PLAYER IN SOUTH AMERICA

1. INTRODUCTION

101

3500

500

0518567

Oil production/ K barrels per day

90

30742065

982

646

367 337 327224 185

607

800

0

400

Gas production / K boe per day

2nd

4th

Source: IEA Statistics 2015

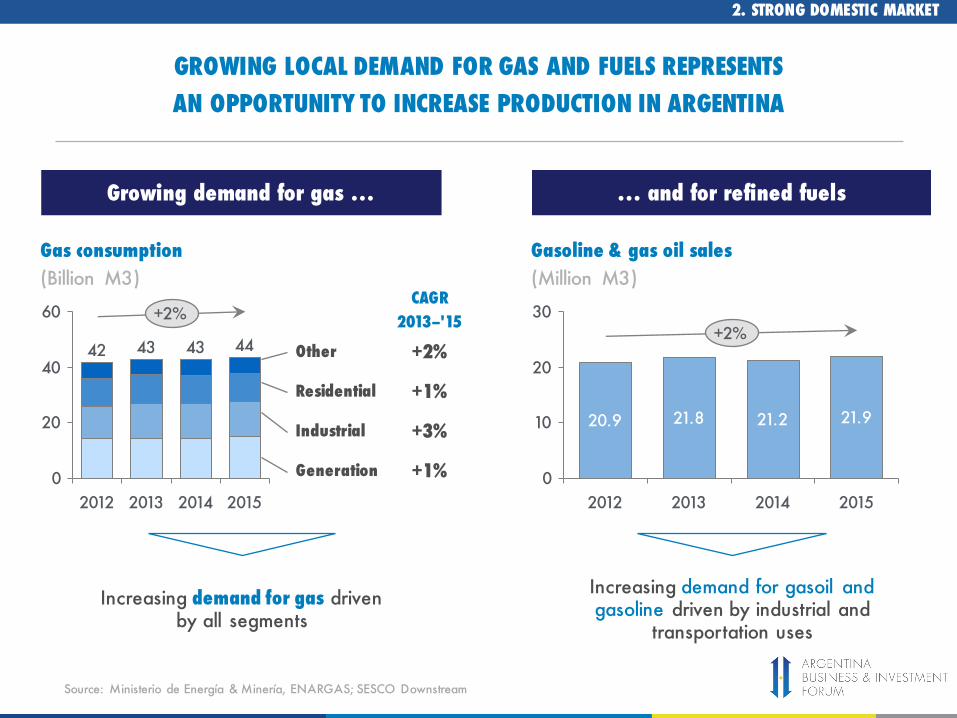

Increasing demand for gas driven by all segments

Increasing demand for gasoil and gasoline driven by industrial and

transportation uses

Growing demand for gas … … and for refined fuels

GROWING LOCAL DEMAND FOR GAS AND FUELS REPRESENTS AN OPPORTUNITY TO INCREASE PRODUCTION IN ARGENTINA

2. STRONG DOMESTIC MARKET

10

20

0

30

2013

+2%

2012

21.220.9 21.8

20152014

21.9

Gasoline & gas oil sales(Million M3)

40

20

0

60

20132012

Gas consumption (Billion M3)

2014

+2%

43

2015

42 43 44 +2%

+1%

+3%

+1%Generation

Industrial

Residential

Other

CAGR 2013–'15

Source: Ministerio de Energía & Minería, ENARGAS; SESCO Downstream

Discoveredresources for

approximately 50 billion barrels,

mainly in Santos basins

3. KEY COMPETITIVE ADVANTAGES OF THE SECTOR

Extensive areas in Argentina with exploration potential

Similar basins have shown significant untapped potential

BasinsProductiveExploration potential

HIGH POTENTIAL FOR EXPLORATION & PRODUCTION

Large unexplored potential, particularly for off-shore and deepwater exploration

Source: Brazil’s National Petroleum Agency - Bloomberg

2nd country in the world:recoverable resources of shale gas

4th country in the world:recoverable resources of shale oil

Shale gas TRR

HIGH QUALITY SHALE RESOURCES IN EARLY STAGE OF DEVELOPMENT: VACA MUERTA, LAS LAJAS, AGUADA BANDERA AND LOS MOLLES

Sources: EIA/ARI World shale gas and shale oil Resource Assessment 2013; BP Statistical Review 2015 – Oil & gas proved reserves include conventional and unconventional resourcesTRR: Technically Recoverable Resources

3- KEY COMPETITIVE ADVANTAGES OF THE SECTOR3. KEY COMPETITIVE ADVANTAGES OF THE SECTOR

ARGENTINA IS AMONG THE TOP COUNTRIES IN THE WORLD IN TECHNICALLY RECOVERABLE SHALE OIL & GAS RESOURCES

429

545

573

623

707

802

1115

0 500 1000 1500

Natural gas - TCF

13

16

26

27

32

58

75

0 20 40 60 80

Oil – Billion barrels

Shale oil TRR

4- VACA MUERTA SHALE RESOURCE

1. Average TOC per play 2. Data from three main basins: Marcellus, Haynesville and BarnettSource: SPE, Halliburton; EIA/ARI World Shale Gas and Shale Oil Resource Assessment 2013

Vaca MuertaParameters of attractive plays Ideal Range

1,200m–3,000m

0.6% < Ro < 2%

> 0.4 psi/ft

3,000m

0.65–1.00 psi/ft

0.85–1.5%

> 3% 6% 4–12%

> 20 mts ~200m 60–90m

2,500–4,000m

0.43–0.90 psi/ft

0.5–2.6%

US Basins2

Depth(Meters)

Pressure –gradient (psi/ft)

Thermalmaturity (Ro)

Total organiccontent 1 (TOC%)

Net thickness(Meters)

4. VACA MUERTA SHALE RESOURCE

VACA MUERTA IS A HIGHQUALITY SHALE RESOURCE

Key parameters are in line with US basins

Increasing number of oil & gas wells

Faster horizontal well drilling & completion

Decreasing costsof horizontal wells

EXPERIENCE EFFECTS REDUCED AVERAGE WELLS COSTS AND FURTHER REDUCTIONS ARE EXPECTED AS NUMBER OF WELLS INCREASES

Sources: Expert interviews; BCG Upstream Performance Database, BCG Analysis

New PAD for well alignment increases productivity

4- VACA MUERTA SHALE RESOURCE4. VACA MUERTA SHALE RESOURCE

AS ACTIVITY INCREASES, VACA MUERTA'SFUTURE IS BECOMING EVEN MORE ATTRACTIVE

0

200

400

600

800

Number of producing wells

+69%

2015

562

388

2013

234

116

2011

69

Oil wellsGas wells

11

14

17

0

5

10

15

20

Well costs (MM US$) -35%

201620152014

25

6584

120

181

0

50

100

150

200

2011 2013

Time in days

2015

-86%

Declining trend in oil production

Header

International context increasing pressure on unconventional profitability

Legal and institutional disorder

ARGENTINA'S OIL & GAS SECTOR FACES THREE MAIN CHALLENGES

5. CHALLENGES

1

2

3

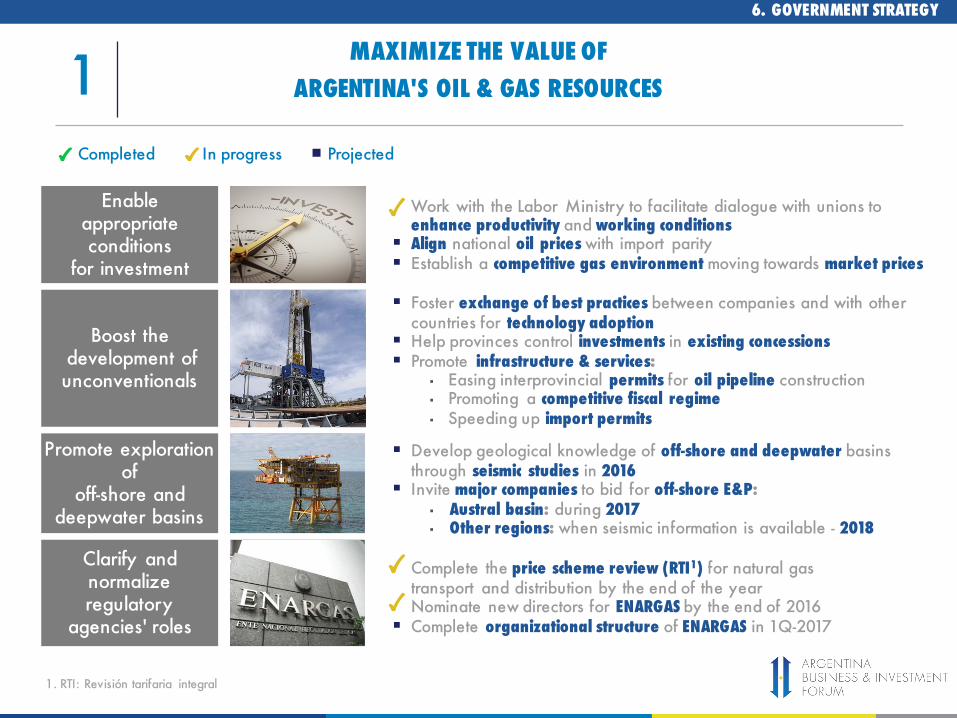

6- GOVERNMENT STRATEGY

Maximize the value of Argentina's oil & gas resources

Promote value addedproduction in the downstream sector

Argentina is moving forward on the oil & gas agenda

1 2

6. GOVERNMENT STRATEGY

THE MINISTRY OF ENERGY & MININGHAS DEFINED TWO KEY GOALS

Completed In progress Projected

Complete the price scheme review (RTI1) for natural gas transport and distribution by the end of the yearNominate new directors for ENARGAS by the end of 2016

§ Complete organizational structure of ENARGAS in 1Q-2017

Clarify and normalizeregulatory

agencies' roles

§ Develop geological knowledge of off-shore and deepwater basins through seismic studies in 2016

§ Invite major companies to bid for off-shore E&P:▪ Austral basin: during 2017▪ Other regions: when seismic information is available - 2018

Promote exploration of

off-shore and deepwater basins

§ Foster exchange of best practices between companies and with other countries for technology adoption

§ Help provinces control investments in existing concessions§ Promote infrastructure & services:

▪ Easing interprovincial permits for oil pipeline construction▪ Promoting a competitive fiscal regime▪ Speeding up import permits

Boost thedevelopment ofunconventionals

Enable appropriate conditions

for investment

■ Work with the Labor Ministry to facilitate dialogue with unions to ■ enhance productivity and working conditions§ Align national oil prices with import parity§ Establish a competitive gas environment moving towards market prices

6. GOVERNMENT STRATEGY

MAXIMIZE THE VALUE OF ARGENTINA'S OIL & GAS RESOURCES1

1. RTI: Revisión tarifaria integral

NormalizeLPG market

Support investments in petrochemicals

Reach global standardsfor cleaner

refined fuels

■ Evaluate which sectors need demand-side subsidies§ Allow LPG prices to converge with international prices§ Promote a more efficient and competitive market

Establish clear path through res. 5/2016, towards clean fuel standards(starting 2016)Aim at lowering sulfur content on gas oil and gasolineReview investment plans of existing refineries

§ Increase ethanol usage for industry

Set the conditions to optimize fuel production from

existing refineries

Promote enhancement of conversion and processing capacities of existing refineries

▪ Enhance conversion reducing heavy products▪ Minimize gas oil imports▪ Increase use of biofuels

§ Encourage potential investment in ethane and propaneprocessing plants

▪ Support the industry to set up of a world class steam crackerand a PDH plant to supply growing regional demands for chemicals

6. GOVERNMENT STRATEGY

Completed In progress Projected

PROMOTE VALUE ADDED PRODUCTION IN THE DOWNSTREAM SECTOR2

Argentina is a key oil & gas player in South America

The Argentine oil & gas sector has strong development potential

In particular, Vaca Muerta is a high quality shale resource with a promising future

Growing local demand for fuels represents an opportunity to increase production

1-

2-

3-

4-

ARGENTINA IS AN ATTRACTIVE MARKET FOR OIL & GAS PRODUCTION

ARGENTINA IS AN ATTRACTIVE MARKET FOR OIL & GAS PRODUCTION

Argentina's oil & gas sector faces three main challenges:

• Declining trend in oil production

• International context increasing pressure on profitability

• Legal and institutional disorder

5-

The Ministry of Energy & Mining has defined two key goals:

• Maximize the value of Argentina's oil & gas resources

• Promote value added production in the downstream sector

6-

Argentina is moving forward on the oil & gas agenda

Presented by Juan José Aranguren

Minister of Energy & Mining

THE GOVERNMENT´SAGENDA

Panelists:

Ø Miguel Gutiérrez, President – YPFØ Marcos Bulgheroni, Board Member – PAEØ Teófilo Lacroze, CEO – Shell ArgentinaØ Gastón Remy, President – Dow Argentina and LATAM South Region

THE PRIVATE SECTOR PERSPECTIVE

Presenters:

Ø José Luis Sureda – Secretary of Hydrocarbon ResourcesØ Marcos Porteau – Undersecretary of Exploration and Production

INVESTMENT OPPORTUNITIES

INVESTMENT OPPORTUNITIES

Opportunity Context

THERE IS A USD 20 BN+ ANNUAL INVESTMENT OPPORTUNITY TO PARTICIPATE IN ARGENTINA’S ENERGY REVOLUTION

Opportunity Detail (USD Bn)

Argentina’s oil & gas sector has very strong development potential• Conventional resources across the country with a history of strong production• Vast and high quality known shale oil & gas resources in the early stages of development (including

Vaca Muerta, the 2nd largest shale gas and 4th largest shale oil reserves -TRR- in the world)• Large unexplored potential in offshore and deepwater

The country’s long history in O&G has already attracted many companies (50+ operations and service providers) to the country and led to the development of skilled human capital in the sector (100K+ qualified personnel)

O&G relatedinfrastructure 3.3**

Off-Shore O&G

Vaca Muerta (per year) 20.01

2

Opportunities to partner with operators and participate in the world’s 2nd largest shale gas and 4th largest shale oil TRR

Opportunities to secure concessions for proven offshore O&G reserves

Projects to expand and increase the capacity of Argentina’s gas pipelines and freight rail to keep pace with the increased production out of Vaca Muerta

TBC (7 basins totaling 500 thousand km2)

**USD 1 Bn of the 3.3 Bn (railway project) also included in the transportation section, but included here for context, given it’s importance for O&G

INVESTMENT OPPORTUNITIES

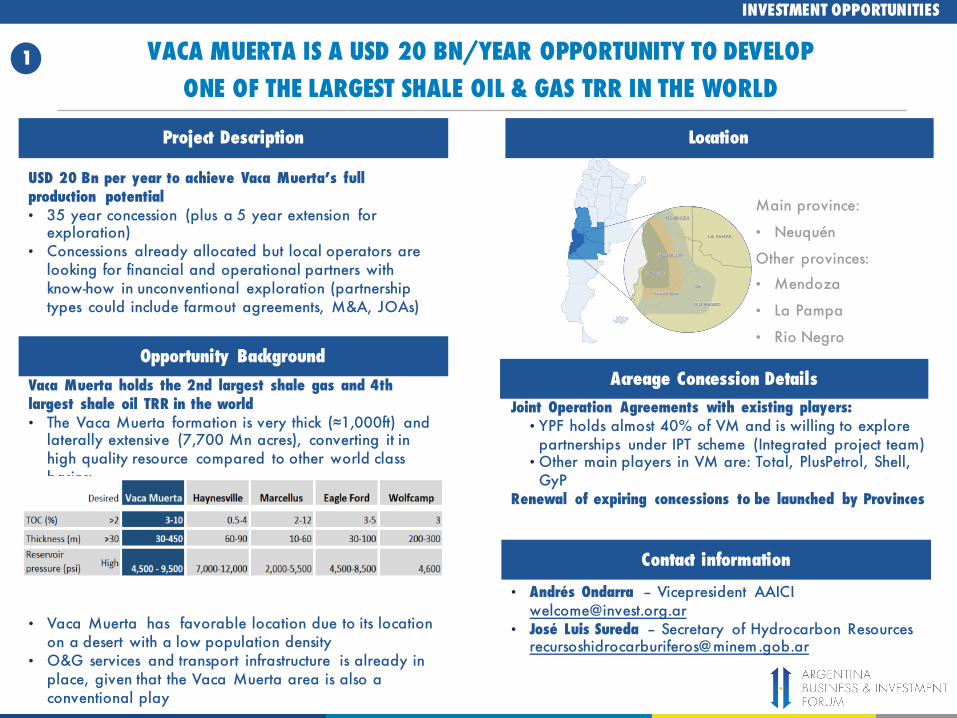

VACA MUERTA IS A USD 20 BN/YEAR OPPORTUNITY TO DEVELOP ONE OF THE LARGEST SHALE OIL & GAS TRR IN THE WORLD

Opportunity Background

USD 20 Bn per year to achieve Vaca Muerta’s full production potential• 35 year concession (plus a 5 year extension for

exploration)• Concessions already allocated but local operators are

looking for financial and operational partners with know-how in unconventional exploration (partnership types could include farmout agreements, M&A, JOAs)

Vaca Muerta holds the 2nd largest shale gas and 4th largest shale oil TRR in the world• The Vaca Muerta formation is very thick (≈1,000ft) and

laterally extensive (7,700 Mn acres), converting it in high quality resource compared to other world class basins:

• Vaca Muerta has favorable location due to its location on a desert with a low population density

• O&G services and transport infrastructure is already in place, given that the Vaca Muerta area is also a conventional play

Project Description Location

Acreage Concession Details

Contact information

Joint Operation Agreements with existing players:• YPF holds almost 40% of VM and is willing to explore

partnerships under IPT scheme (Integrated project team)• Other main players in VM are: Total, PlusPetrol, Shell,

GyPRenewal of expiring concessions to be launched by Provinces

• Andrés Ondarra – Vicepresident [email protected]

• José Luis Sureda – Secretary of Hydrocarbon Resources [email protected]

Main province:

• Neuquén

Other provinces:

• Mendoza

• La Pampa

• Rio Negro

1

INVESTMENT OPPORTUNITIES

THE GAS PIPELINE INFRASTRUCTURE WILL REQUIRE USD 2.25 BN IN INVESTMENTS TO KEEP PACE WITH INCREASED PRODUCTION ACTIVITY

Opportunity Background

• USD 1.5 Bn work for construction of GNEA´s 4th tranche

• GNEA to connect to Juana Azurduypipeline (coming from Bolivia) and provide natural gas to 3.4 million inhabitants

• Work to be tendered by Enarsa• USD 750 Mn to increase and broad the

gas transport capacity of TGS and TGN• Work to be tendered by Enarsa• USD 1 Bn for the development and

improvement of freight railway to connect Vaca Muerta with the port of Bahia Blanca (Atlantic Ocean). Will significantly decrease the cost of transporting equipment, sand and other supplies to develop Vaca Muerta

• Part of Argentina’s transportation plan to improve freight railway utilization at national level

Argentina will require significant investments to expand its infrastructure, following the expected expansion of its oil & gas exploration and production capacity• The additional infrastructure needed includes the

expansion of Argentina´s gas pipeline network, treatment facilities and the improvement of freight rail to provide Vaca Muerta with sand and other supplies

Project Description Location

Contact information

• Andrés Ondarra – Vicepresident [email protected]

• José Luis Sureda – Secretary of Hydrocarbon Resources [email protected]

GNEA Gas Pipeline

Extension

Añelo-Bahia Blanca

Railway*

TGS/TGN

*Project accounted for in the Transportation section, but also included here for context

AÑELO – BAHIA BLANCA RAILWAY

GNEA

2

QUESTIONS & ANSWERS