oil and gas infrastructure of georgia: ongoing and prospective projects

TRANSCRIPT

Dr. Sci, Prof. Teimuraz Gochitashvili,

Georgian Oil and Gas Corporation

DISCLAMER

2

Except for statements of historical fact, the forward looking statements and other

information presented herein involve known and unknown risks, uncertainties and

other factors which may cause the actual results, performance or achievements

expressed in presentation to be materially different from those presented herein.

Such factors include general economic and business conditions, the ability to

acquire and develop specific projects, the ability to fund operations and changes in

consumer and business consumption habits and other factors over which no

reasonable control can be done

Presentations/2014/BBSPA Presentation, 2, 10 03 14

3/27/2014

CONTENT

• Oil and Gas Transportation Infrastructure

• Rehabilitation/Development of Transportation Infrastructure

• Strategic Projects

• Southern Gas Corridor

• Conclusions

Presentations/2014/BBSPA Presentation, 2, 10 03 14

3 3/27/2014

Oil and Natural gas Transit Pipelines

4

The most significant projects of oil and gas sector in progress, are the transportation of oil and gas through Georgia by pipelines.

• Transit corridor passing Georgia represent one of the most attractive routes for supplying international markets with Caspian hydrocarbon resources. Georgia has been transporting Azeri oil for already a century by rail, sea ports or via pipelines. • Azerbaijan, as well as the entire Caspian region, owing abundant energy resources are isolated from world’s large consumer markets and motivated on selecting independent export routes bypassing other producing (and consequently competitive) countries. Under these conditions specific significance attained Georgia’s transit potential. • Strategic cooperation developed between Azerbaijan, Georgia and Turkay resulted in the effective implementation of Caspian energy resources transit projects through the Baku-Supsa (WREP), Baku-Tbilisi-Ceyhan (BTC) and Baku-Tbilisi-Erzurum (SCP) pipelines, as well as Georgian Black Sea terminals and Railways. • Georgia holds a significant transit potential in terms of further delivery of Azeri and entire Caspian region’s hydrocarbon resources to the international markets. Gas liquefaction (Pressurization) and its shipment to the European markets - attractive alternative to pipeline transport in certain conditions.

Presentations/2014/BBSPA Presentation, 2, 10 03 14

3/27/2014

Turkey

GEORGIA

Russia

AZERBAIJAN

BTC

SCP

Ceyhan

Erzurum

Tbilisi

NSCP

Supsa

Baku

Iran

Railway

WREP

GGMS

AzGGM

IrAzGM

IrArGM

Volume of Capacity,

Tanks, M3 Mta Oil

Batumi 570 000 ≈10 ≈12

Poti 118 000 1,5-2 ≈4

Supsa 195 000 ≈6 ≈10

320 000-600 000

Anaklia - -≈8-15

(dry cargo)

Prospects,

Mta Oil

Kulevi ≈6 ≈20

Rehabilitation/Development of transport Infrastructure to secure gas supply - one of the main strategic priorities of Georgia Presentations/2014/BBSPA Presentation, 2,

10 03 14 6 3/27/2014

Infrastructure Rehabilitation/Development Projects

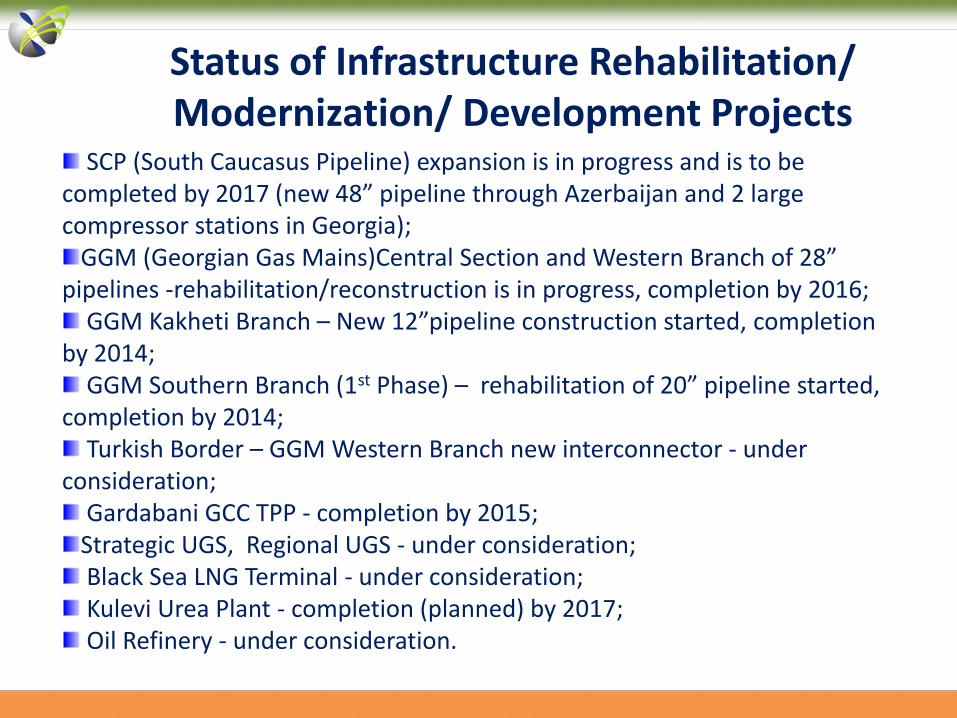

Status of Infrastructure Rehabilitation/ Modernization/ Development Projects

SCP (South Caucasus Pipeline) expansion is in progress and is to be completed by 2017 (new 48” pipeline through Azerbaijan and 2 large compressor stations in Georgia);

GGM (Georgian Gas Mains)Central Section and Western Branch of 28” pipelines -rehabilitation/reconstruction is in progress, completion by 2016;

GGM Kakheti Branch – New 12”pipeline construction started, completion by 2014;

GGM Southern Branch (1st Phase) – rehabilitation of 20” pipeline started, completion by 2014;

Turkish Border – GGM Western Branch new interconnector - under consideration;

Gardabani GCC TPP - completion by 2015; Strategic UGS, Regional UGS - under consideration; Black Sea LNG Terminal - under consideration; Kulevi Urea Plant - completion (planned) by 2017; Oil Refinery - under consideration.

Potential for Development

• Potential for development of high pressure reverse pipelines and swaps with every neighbor;

• Connection to more than 500000 householders and all industrial consumers & TPP’s;

• Sovereign ownership of all infrastructure by Georgian Government (ultimately);

• Freedom of TPA;

• Potential for additional flows;

• Moderate and transparent regulatory framework;

• Harmonized procedures with partners (long term contracts)

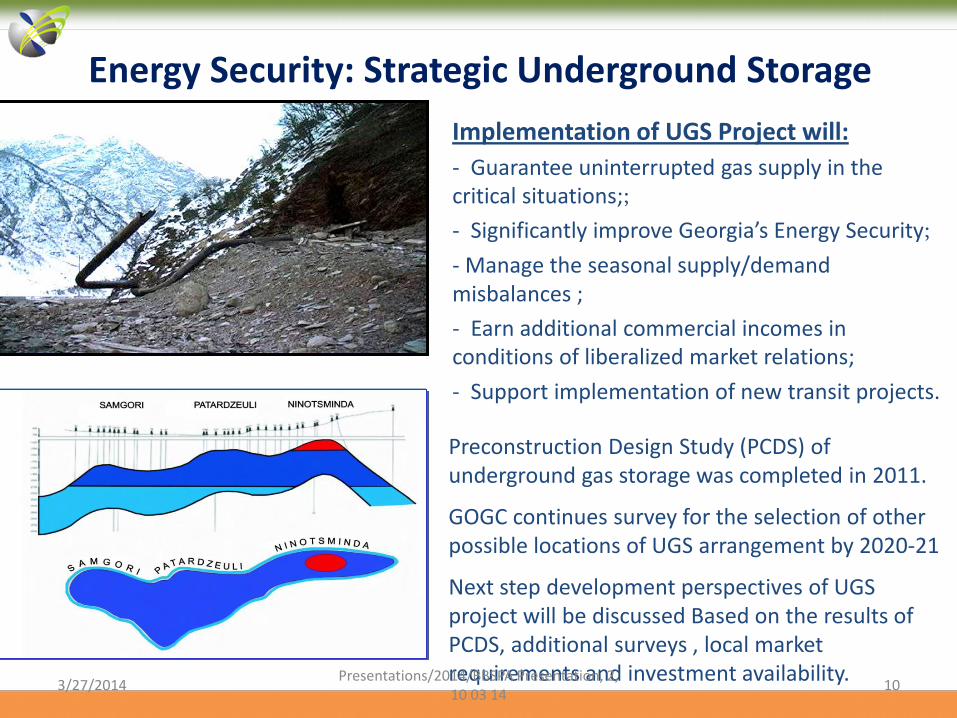

Energy Security: Strategic Underground Storage

Implementation of UGS Project will:

- Guarantee uninterrupted gas supply in the critical situations;;

- Significantly improve Georgia’s Energy Security;

- Manage the seasonal supply/demand misbalances ;

- Earn additional commercial incomes in conditions of liberalized market relations;

- Support implementation of new transit projects.

Preconstruction Design Study (PCDS) of underground gas storage was completed in 2011.

GOGC continues survey for the selection of other possible locations of UGS arrangement by 2020-21

Next step development perspectives of UGS project will be discussed Based on the results of PCDS, additional surveys , local market requirements and investment availability. Presentations/2014/BBSPA Presentation, 2, 10 03 14

10 3/27/2014

New Combined Cycle Power Plant

Project duration – 3 years Project commencement - 2012 Project cost – USD 205 million Output capacity – 230 MW

Annual generation – 1 337 million KWh

Gas consumption – 221 Mm3/y

Natural Gas the most advantageous backup fuel for renewables

Gas fired Combined Cycle TPP is

flexible, cost-effective,

ecologically attractive and easy

to use tool for balancing of

Renewables in Power Generation Presentations/2014/BBSPA Presentation, 2,

10 03 14 11 3/27/2014

• Small scale refinery for localy produced oil

• Annual capacity up to 100 th. tons;

• Gasoline and Diesel oil of Euro standard 4-5;

• Roughly10% of local consumption of petroleum

products (demand of strategic consumers: military

sources, police…)

• Sub products for local industry and road construction

Utilization of Local Recourses

Presentations/2013/Policy Presentations Tbilisi/Oil and Gas Sector, November 2013 ,

Final

Urea Plant at Kulevi

• Capacity 1200 t/day ammonia or 2000 t of

carbamide for export;

• Annual consumption of gas 365/500 Mcm

• Status: Preliminary feasibility study by

Samsung Eng., Planned completion of

construction by 2017; • Social-Economic advantages for Georgia

(taxes, employment, load of local infrastructure and guaranteed incomes, …)

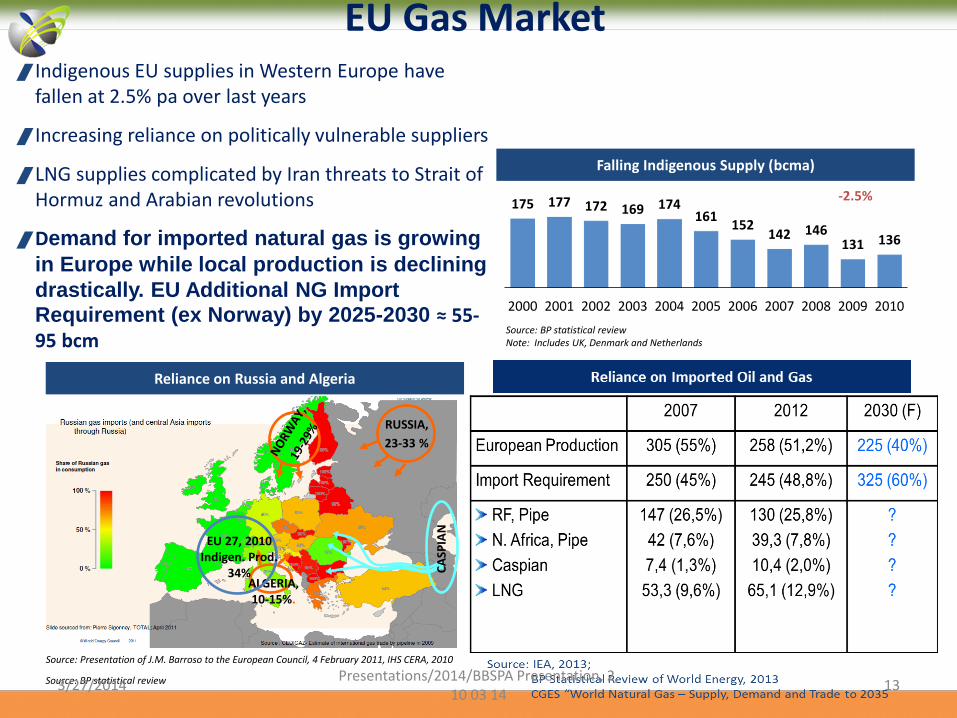

EU Gas Market

Indigenous EU supplies in Western Europe have fallen at 2.5% pa over last years

Increasing reliance on politically vulnerable suppliers

LNG supplies complicated by Iran threats to Strait of Hormuz and Arabian revolutions

Demand for imported natural gas is growing

in Europe while local production is declining

drastically. EU Additional NG Import Requirement (ex Norway) by 2025-2030 ≈ 55-95 bcm

175 177 172 169 174 161

152 142 146

131 136

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

-2.5%

Falling Indigenous Supply (bcma)

Reliance on Russia and Algeria

Source: BP statistical review Note: Includes UK, Denmark and Netherlands

RUSSIA,

23-33 %

ALGERIA, 10-15%.

CA

SPIA

N

EU 27, 2010 Indigen. Prod.

34%

Source: Presentation of J.M. Barroso to the European Council, 4 February 2011, IHS CERA, 2010

Source: BP statistical review Presentations/2014/BBSPA Presentation, 2, 10 03 14

13 3/27/2014

Azerbaijan Gas Prospects

Source: Wood Mackenzie, 2013 Presentations/2014/BBSPA Presentation, 2,

10 03 14 14 3/27/2014

SCP Planned Expansion

Transportation of Caspian oil & gas through Georgian Pipelines instead of territories of

competitor producer countries (Russia, Iran) - an extra economic attractiveness

Presentations/2014/BBSPA Presentation, 2, 10 03 14

Economics of South Stream pipeline determines that it’s development might be mainly of Russia’s political interest and of Gazprom’s attitude to control CA energy resources delivery to Europe

Southern Gas Corridor Projects support to ensure not only diversification of supply routes, but also diversification of supply sources, decreasing dependence on gas import from politically sensitive regions.

15 3/27/2014

AGRI LNG Project

16

ტრანსპორტი რუმ-უნგრ

ტრანსპორტი აზერბ-საქართვ.

LNG ტერმინალი

ReGas. ტერმინალი

Presentations/2014/BBSPA Presentation, 2, 10 03 14

16 3/27/2014

Gas liquefaction and its shipment to European markets is an attractive alternative to pipeline transport in certain conditions.

Trends of LNG and Core Industrial Markets support project realization

In case of low to moderate throughput, the existing infrastructure and possible low cost technological solutions (Minimal Capex and Opex: existing infrastructure, sea water for conditioning, small sized storage/tankers/FLNG, stable production etc.), are available, that significantly improves cost effectiveness and the flexibility of project in terms of timing and market requirements satisfaction

AGRI LNG (or CNG) Project Prospects for Caspian Gas Transportation

Small Medium to Large

1 mtpa 2 mtpa 3 mtpa 4+ mtpa

Movable Modular Liquefaction System (MMLS)

Medium LNG Facility

Floating LNG (FLNG)

Large LNG Facility

AGRI

Presentations/2014/BBSPA Presentation, 2, 10 03 14

17 3/27/2014

ITALY

GREECE

ALBANIA

RUSSIA

KAZAKHSTAN UKRAINE

POLAND

TURKEY

MOLDOVA

ROMANIA

BULGARIA GEORGIA

AZERBAIJAN

To R

ussia

Caspian Oil Transportation Routes (existing and proposed)

0

Odessa-Brody-Gdansk

Caspian Pipeline Consortium

Baku-Tbilisi-Ceyhan

Baku - Supsa

Baku - Novorossiysk

Burgas-Vlore

Constanta-Trieste

Tanker shipments

Presentations/2014/BBSPA Presentation, 2, 10 03 14

Caspian production can grow significantly, with

prospects of additional export, potentially

reaching 3,7 Mb/d by 2020-25, including exports

to Europe. New Infrastructure will be required 18 3/27/2014

Brody Kralupy

Bratislava

Odessa

Baku Batumi, Kulevi, Supsa

Plock Adamowo

Leuna

Schwedt

Gdansk

Mazeikiai

EAOTC creates an alternative, independent and reliable transportation route for the crude oil from the Caspian Region to Europe;

EAOTC allows to increase the level of energy security in the participating countries and EU;

EAOTC increases opportunity for Energy Solidarity and partnership between the EU and countries participating in the Project;

EAOTC is included among the EU Energy Infrastructure priorities for 2020 and beyond;

Brody-Adamovo section of EAOTC is icluded in the list of Projects of Common Interest of EU (PCI) and of the Energy Community (PECI);

Demand will come from Central and Eastern Europe refineries, also probably from Mazeikai and Rotterdam via Gdansk

EAOTC PROJECT OVERVIEW

Presentations/2014/BBSPA Presentation, 2, 10 03 14

19 3/27/2014

“Sarmatia” projected tariff to Klarupy to be $1/bbl less than via BTC-TAL-IKL Pipelines (Consultants estimation, 2010)

EU Projects of Common Interests (PCI) List of Infrastructure which is planned and implemented for the period up to 2020 and

beyond.

EU PCI’s involving Infrastructure projects on GEORGIAN Territory: 6. Priority corridor North-South gas interconnections in CE and SE Europe 6.22. Cluster AGRI Project (European Sections of Infrastructure); 7. Priority Corridor Southern Gas Corridor (‘SGC”) 7.1. Cluster of transport infrastructure and associated equipment from the Caspian Region, crossing GEORGIA and Turkey and Ultimately Reaching Final EU Markets 7.1.1. Gas Pipeline from the EU to Turkmenistan via Turkey, Georgia, Azerbaijan and Caspian (combination of TANAP, SCP-(F)X, and TCP); 7.2. PCI consisting of integrated, dedicated and scalable transport infrastructure for new sources of gas from Caspian Region to Romania including: 7.2.2. Upgrade of the pipeline between Azerbaijan and Turkey via Georgia (SCP-(F)X); 7.2.3. Submarine pipeline linking Georgia with Romania (White Stream); 9. Priority corridor oil Supply Connections in Central Eastern Europe 9.1. PCI Adamowo-Brody Pipeline (EAOTC, Ukraine-Poland section)

Presentations/2014/BBSPA Presentation, 2, 10 03 14

20 3/27/2014

Conclusions Being the shortest route for the Caspian oil and gas to Turkish and European markets, and having an transport infrastructure with significant reserves and successful operational experience Georgia offers an opportunity to reduce further capital investments for the new transit projects.

Experience acquired during the number of pipeline rehabilitation/construction projects completed during the last years, better positions of Georgia to successfully continue implementation of new, large scale regional infrastructure projects.

Focus on integration in the regional and EU energy structures is Georgia’s next phase development strategy, that will result the further development of the gas market and closest approach to the modern international practices.

Some problems related to the Georgia’s integration in the regional and EU energy structures require particular approach, taking into consideration local specifics, including challenging geopolitical surroundings, established after 2008 Russian-Georgian and recent Russian-Ukrainian Conflicts.

Presentations/2014/BBSPA Presentation, 2, 10 03 14

21 3/27/2014

Georgian Oil and Gas Corporation www.gogc.ge

22

Georgian Oil and Gas Corporation (GOGC) is a joint stock company with 100% of its shares fully owned by the state (through Partnership Fund).

GOGC holds a National Oil Company status and as a NOC manages state interests in Production Sharing Agreements with investors.

GOGC is the owner of the Western Route Export Pipeline (WREP) and Georgian Main Gas Pipeline System (MGPS), works on Design and Construction/Expansion of pipeline systems.

GOGC is involved in import, transit and transport activities of natural gas and plays a leading role in ensuring the country’s energy security.

GOGC monitors the operations of existing transportation infrastructure on the territory of Georgia and works on development of new transit projects, supporting diversification of supply and energy security of the EU and International Markets.

GOGC Major Partners: BP, SOCAR, Statoil, Total, Botas, Romgaz, MVM, PERN, UkrTransnafta, Gazprom Export, KazTransGas

GOGC bonds are traded on London Stock Exchange

Thank You for Your Attention