oh $@%%%@! the food consumer changed and my company and i didn't

TRANSCRIPT

Is Your Distribution Operation prepared to succeed in 2015, 2016 …2025??orOh $*%#@@! The Food Consumer Changed and My Company and I didn’t!

Richard H. Kochersperger

June, 2015

Industry Gurus

04/15/23 2

Age Brings Wisdom

Tell Me and I Forget

Teach Me and I Remember

Involve me and I Learn

Ben Franklin

04/15/23 4

Previous Presentations

• 2015: Oh $*%#@@! The Food Consumer Changed and My Company and I didn’t!

• 2014: Disruptive Forces: Are U Prepared?

• 2013: Value Chain Strategy in a VUCA world

• 2012: Speed: The Consumer is Changing Faster than the Food Industry can change!

• 2011: Seek to stay out in front and don’t look back!

• 2010: The World is Changing Faster than you are!

04/15/23 5

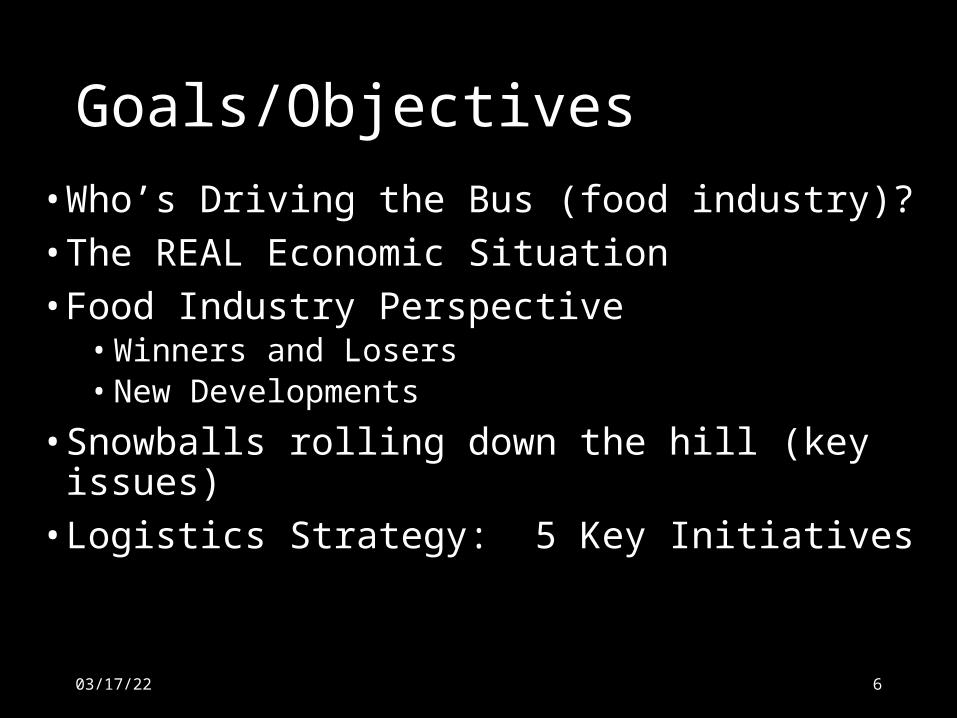

Goals/Objectives

• Who’s Driving the Bus (food industry)?

• The REAL Economic Situation

• Food Industry Perspective• Winners and Losers• New Developments

• Snowballs rolling down the hill (key issues)

• Logistics Strategy: 5 Key Initiatives

04/15/23 6

The Consumer Drives the Food Supply Chain

704/15/23

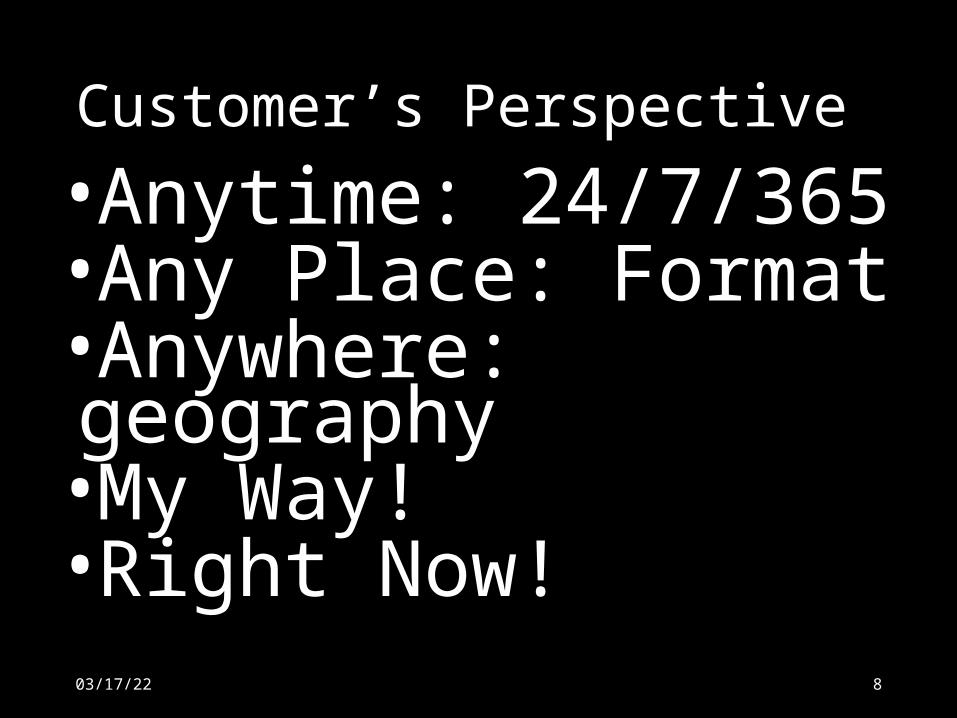

Customer’s Perspective

•Anytime: 24/7/365•Any Place: Format•Anywhere: geography•My Way!•Right Now!

804/15/23

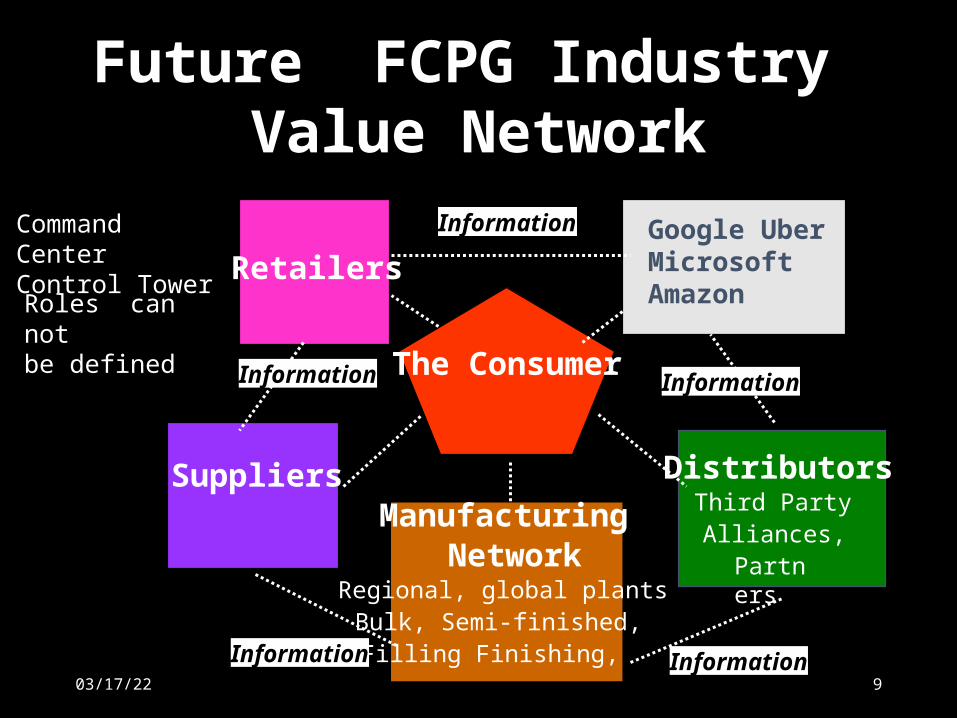

Future FCPG Industry Value Network

Command CenterControl Tower

Roles can not be defined

RetailersGoogle UberMicrosoftAmazon

The Consumer

DistributorsThird PartyAlliances,Partners

ManufacturingNetwork

Regional, global plantsBulk, Semi-finished,Filling Finishing,

Suppliers

Information Information

InformationInformation

Information

904/15/23

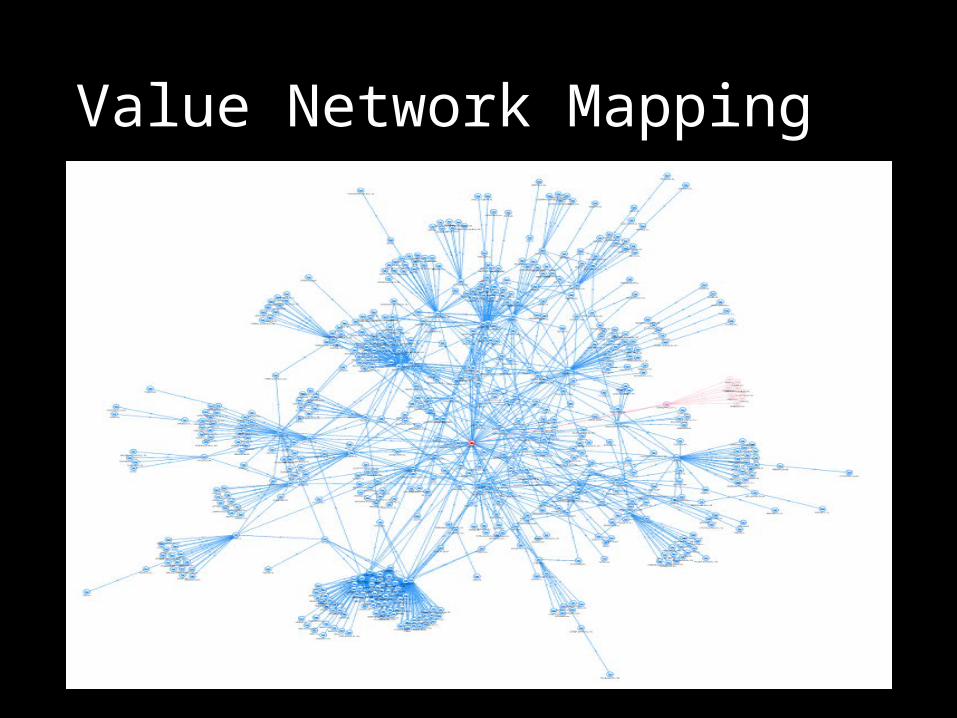

Value Network

Value Network Mapping

The “Have” and “Have Not’s”

1204/15/23

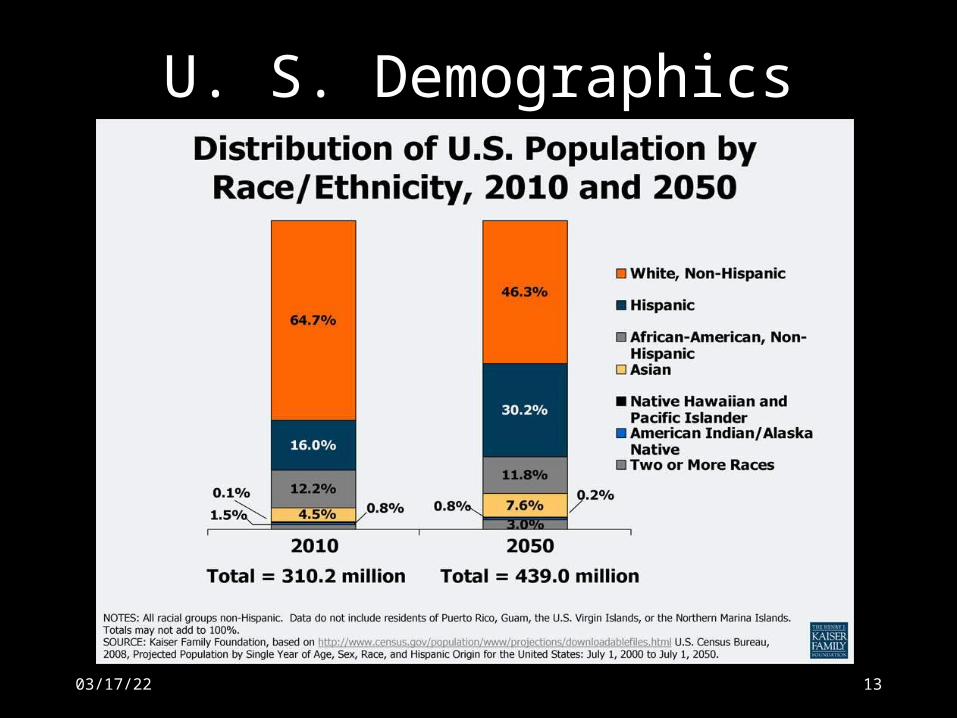

U. S. Demographics

1304/15/23

14

U. S. Demographics

04/15/23

Who Are My Consumers?Generation Age Millions of

People Generation Alpha 0 - 9 ??

Digital Natives (Generation Z) 10 - 17 25

Millennials (Generation Y) 18 - 24 91

Generation X (Busters) 25 - 35 41

Younger Boomers 35 - 50 48

Mature Boomers 50 - 65 40

Depression / WWII 67 - 80 35

G.I. - Pre 1928 Over 80 26

1504/15/23

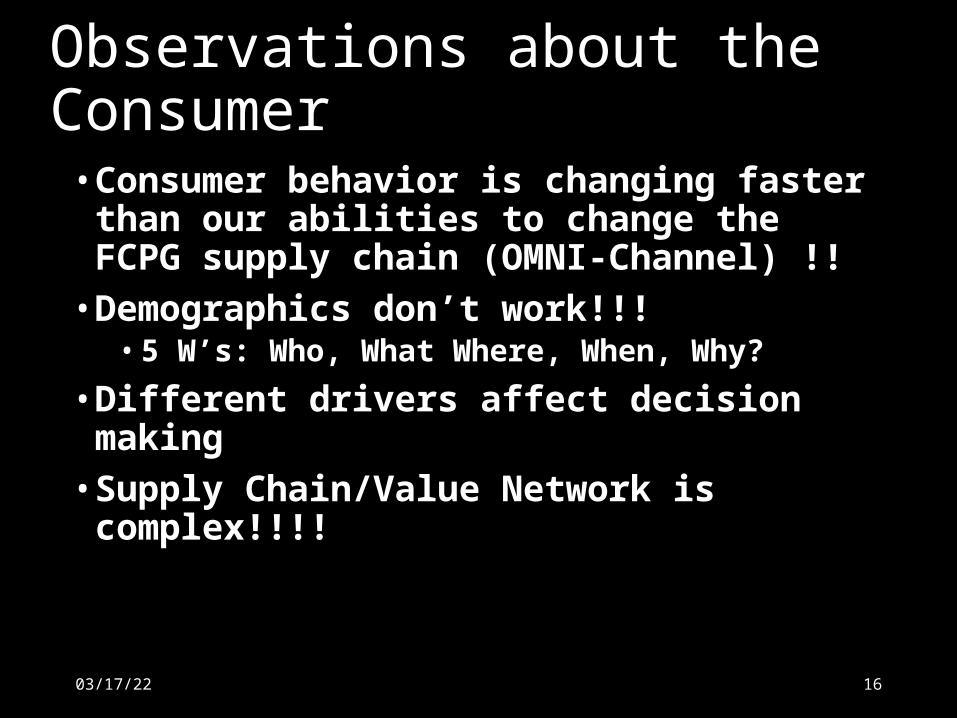

Observations about the Consumer

• Consumer behavior is changing faster than our abilities to change the FCPG supply chain (OMNI-Channel) !!

• Demographics don’t work!!!• 5 W’s: Who, What Where, When, Why?

• Different drivers affect decision making

• Supply Chain/Value Network is complex!!!!

1604/15/23

Thought for the Moment

“Insanity is doing the same thing, over and over again, but expecting different results.” ― Albert Einstein

1704/15/23

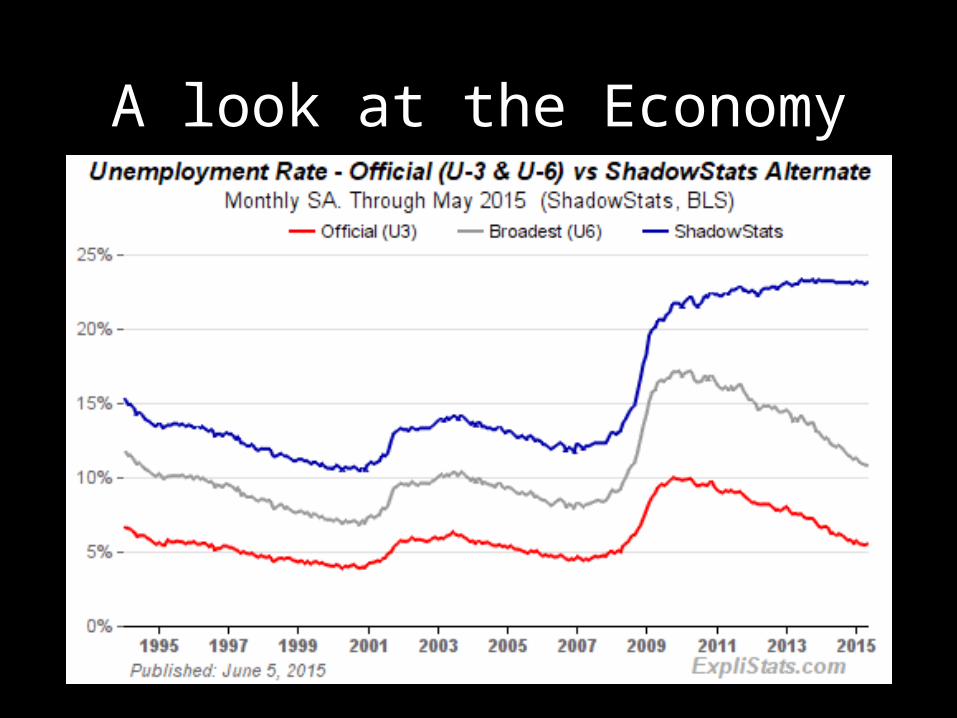

A look at the Economy

Food Economics

Food Prices• Bacon: 55% increase since 2010

• Ground beef: 45%

• Oranges: 35%

• Coffee: 31%

• Peanut Butter: 30%

• Margarine: 30%

• Wine: 25%

• Turkey: 24%

• Chicken: 22%

• Pork: 15% 2014

Thought for the Moment

Food Retail Industry Graveyard

04/15/23 22

Food Retail Industry Graveyard

04/15/23 23

Food Retail Industry Graveyard

04/15/23 24

Food Industry E R

04/15/23 25

Food Industry E R

04/15/23 26

Food Retail Winners

04/15/23 27

Food Retail Winners

04/15/23 28

Rise of the Ethnic Focused Retailer

04/15/23 29

Foodservice Losers

25% of new restaurants go out of business the first year

Foodservice Industry Winners

04/15/23 31

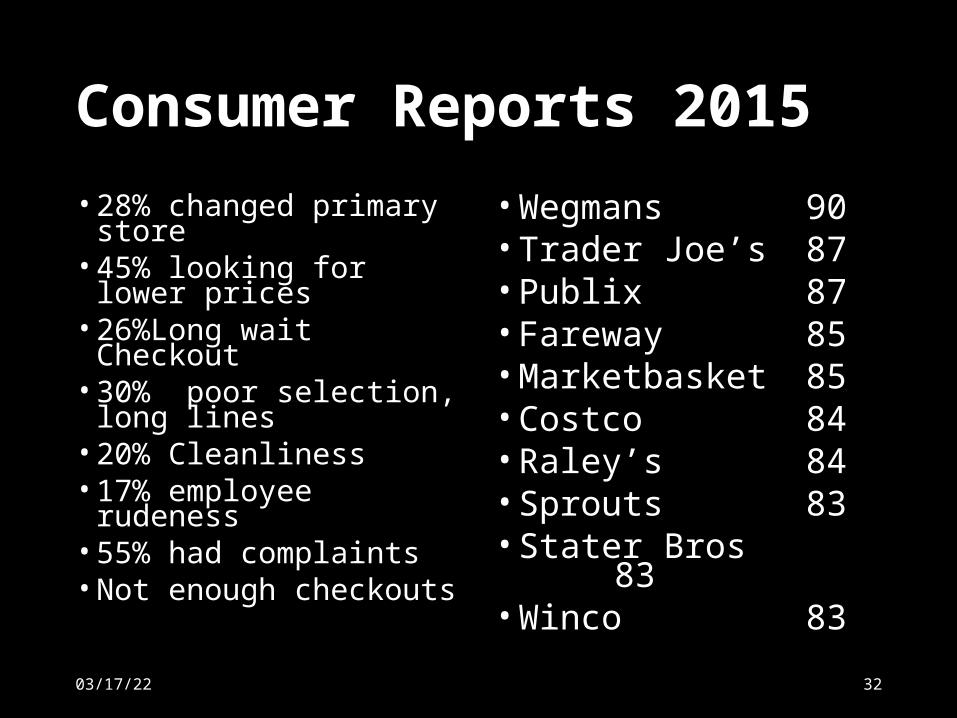

Consumer Reports 2015

• 28% changed primary store• 45% looking for lower

prices• 26%Long wait Checkout• 30% poor selection, long

lines• 20% Cleanliness• 17% employee rudeness• 55% had complaints• Not enough checkouts

• Wegmans 90• Trader Joe’s 87• Publix 87• Fareway 85• Marketbasket85• Costco 84• Raley’s 84• Sprouts 83• Stater Bros 83• Winco 83

04/15/23 32

Top US Food RetailersName Sales Stores Format

Wal-Mart Stores $288,049,000 4,024 Walmart Supercenter (3,407) Walmart Neighborhood Market (600) Walmart Express (15)

The Kroger Co $108,500,000 2,625 Multiple

AB Acquisition LLC $56,443,140 2,238 Safeway, Vons, Albertsons

Publix Super Markets $30,559,505 1,097 Publix (1,085) Sabor (9) GreenWise (3)

Ahold USA Inc $25,976,700 761 Stop & Shop (394) Giant-Landover (154) Giant-Carlisle (147)

H-E-B Grocery Co. $22,590,000 363 H-E-B (258) H-E-B Plus (36) H-E-B Central Market (9)

Delhaize America Inc. $16,900,000 1,296 Food Lion (1,108) Hannaford (188)

Meijer Inc $15,400,000 213

Wakefern Food Corp. $14,700,000 141 ShopRite (77) Price Rite (58) The Fresh Grocer (6)

Whole Foods Market $14.194,005 414

Global Food Industry

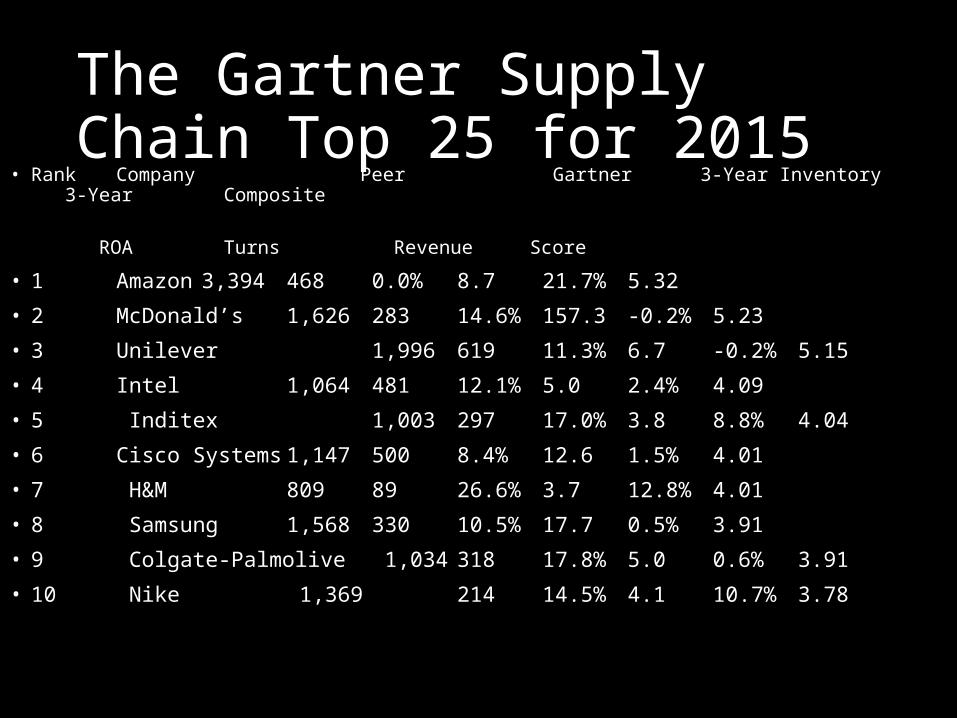

The Gartner Supply Chain Top 25 for 2015

• Rank Company Peer Gartner 3-Year Inventory 3-Year Composite

ROA Turns Revenue Score

• 1 Amazon 3,394 468 0.0% 8.7 21.7% 5.32

• 2 McDonald’s 1,626 283 14.6% 157.3 -0.2% 5.23

• 3 Unilever 1,996 619 11.3% 6.7 -0.2% 5.15

• 4 Intel 1,064 481 12.1% 5.0 2.4% 4.09

• 5 Inditex 1,003 297 17.0% 3.8 8.8% 4.04

• 6 Cisco Systems 1,147 500 8.4% 12.6 1.5% 4.01

• 7 H&M 809 89 26.6% 3.7 12.8% 4.01

• 8 Samsung 1,568 330 10.5% 17.7 0.5% 3.91

• 9 Colgate-Palmolive 1,034 318 17.8% 5.0 0.6% 3.91

• 10 Nike 1,369 214 14.5% 4.1 10.7% 3.78

Lidl

• 850,000 sq ft DC in Almance, NC

• Lexington, Winston-Salem, NC

Thought for the Moment

Issues Impacting your Business!!

Foodies: Green, Natural, Organic

04/15/23 72

Clean Food

04/15/23 73

Real FoodReal Food is food which truly nourishes producers, consumers, communities and the earth. It is a food system--from seed to plate--that fundamentally respects human dignity and health, animal welfare, social justice and environmental sustainability.Some people call it "local," "green," "slow," or "fair." We use "Real Food" as a holistic term to bring together many of these diverse ideas people have about a values-based food economy

04/15/23 74

Pure Food

eating food that mother nature grew and offered for us.

No Man Made products

FRESH

77

Farmers Markets

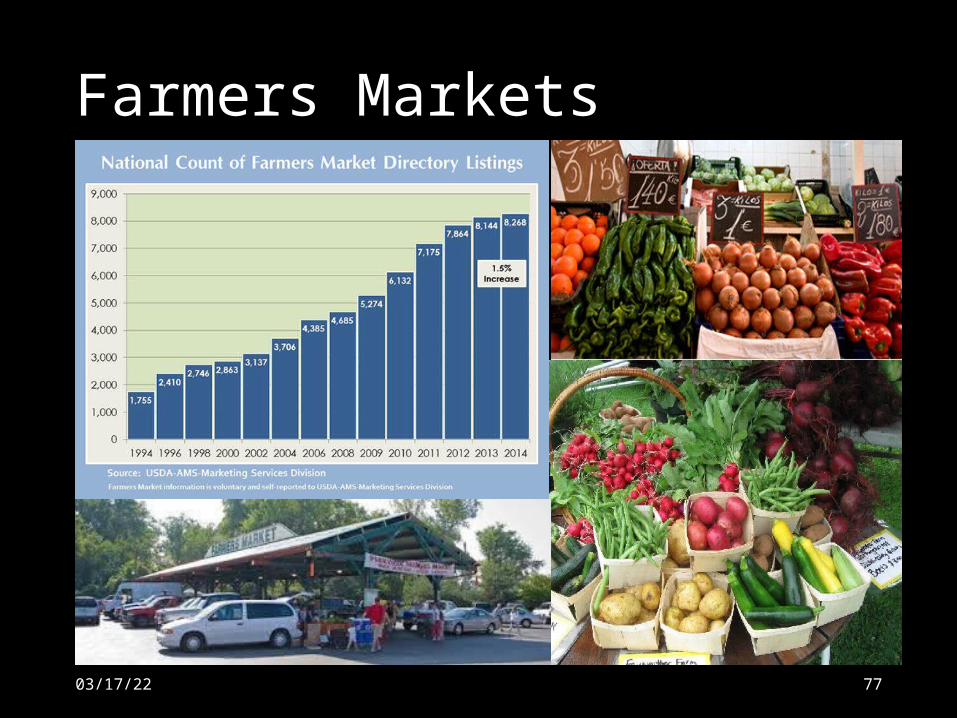

2013: 8,000+

04/15/23

Rise of the Grocerant• "Grocerant means any retail food item that is ready-2-eator ready to heat. Traditionally

these items can be found in grocery stores in the deli / lifestyle section, C-stores in the prepared food area and prepackaged, ready to eat items and in restaurants under the To-go, takeout or take away or delivery section of the menu or on the website."

Rise of the Grocerant

Eataly

Subscription Meals

Click and Collect

Arkansas, Arizona, Canada, Great Britain

Walmart Click/Collect/Flex siteThis is a typical welcome site that is displayed when Wal-Mart delivery trucks park offsite in Phoenix and act as a collection point for online grocery orders. Customers are treated to gifts, with first timers receiving a welcome box and loyal customers a rewards box. All users are treated to bottled water and a snack while they wait for their order to be loaded in their vehicle.

Delivery to the Consumer!

FMI: Store of the Future• Nearly half of shoppers want store associates to provide in-depth

product information.

• 52 percent continue to be annoyed by long lines.

• More than 50 percent will want to integrate their mobile devices into their shopping.

• 5 percent include online grocery shopping as a primary future channel.

• 28 percent say competitive pricing will be the main reason for choosing their grocer.

• 39 percent want retailers to reward them for making healthy purchases and trying new foods.

• 30 percent ranked virtual grocery stores as a top-three "want" for the future.

Amazon Dash

Amazon Income Promotions

Walmart

New Developments• Tesco to sell off Korea

• XOXO: 900 stores in Texas

• Target to invest $50 million in Va DC

• Sysco acquires Tannis Trading

• Amazon to build new DC in Shakopee, MN

• Wegmans to open in Brooklyn/Richmond/Tysons Corner

• Sycamore Partners buys 330 Family Dollar Stores

• Blue Bell Creamery shuts down due to listeria

• C&S closes White Rose operations

New Developments• Schnucks to build new DC in Missouri

• ACON buys Fiesta

• Ahold Fresh opens in Phila/Boston

• Meijer curbside/Wisconsin

• Publix continues invasion of Carolinas

• Giant Eagle closes Good Cents

• I supply to Michigan

• Reinhart Foodservice to Washington DC

New Developments

• Amazon Now Offers Free Same-Day Delivery in 14 Metro Areas

• Walmart Turns Weekly Circular into Online Catalog, Focus on 'Live Better'

• Amazon Working on Pinterest-Like Browsing Called 'Amazon Stream'

• Walmart Launches App-Based Virtual Store in China

• Apple Partners With Postmates for Same-Day Delivery Trial

New Developments

• Taco Bell Pledges to Remove Artificial Ingredients as Consumers Demand More Information

• Walmart Announces Changes for Food Suppliers Around Animal Treatment

• Ebay To Extend Click and Collect in Europe Following Successful UK Pilot

• Ecommerce business models are disrupting the historical value chain

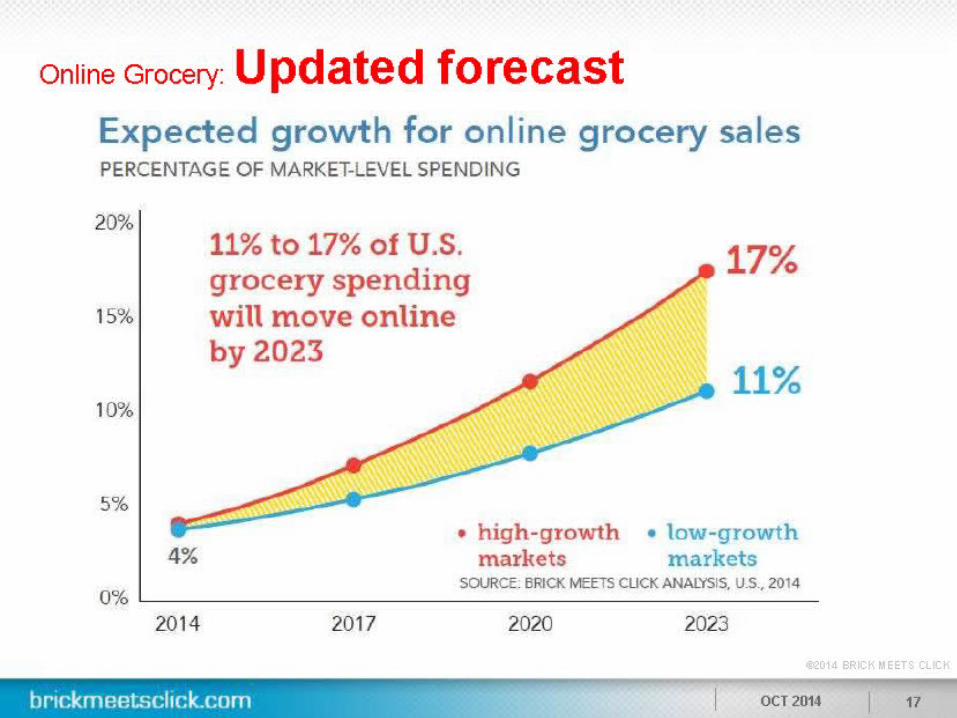

• Ecommerce to account for 22% of global chain retail by 2020

Thought for the Moment

7 most expensive words in businessWe have always done it that way!!!

5 Strategic Initiatives

•Manage the Network• Inventory Management Plan• Step up to the Omnichannel Opportunity• Embrace Technology• Invest in Education/Mentors

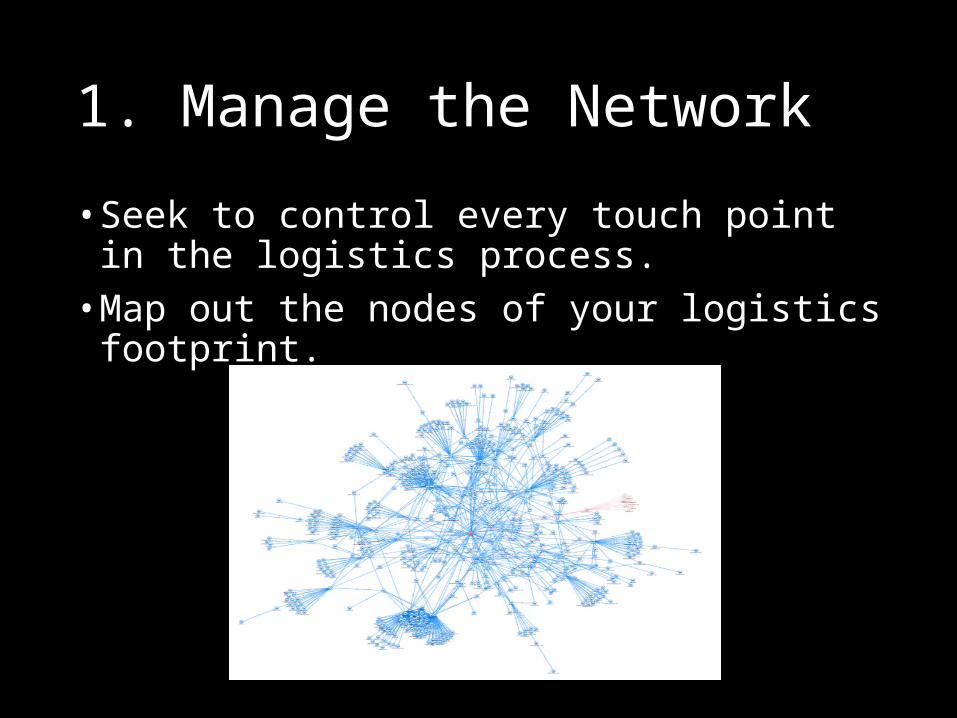

1. Manage the Network

• Seek to control every touch point in the logistics process.

• Map out the nodes of your logistics footprint.

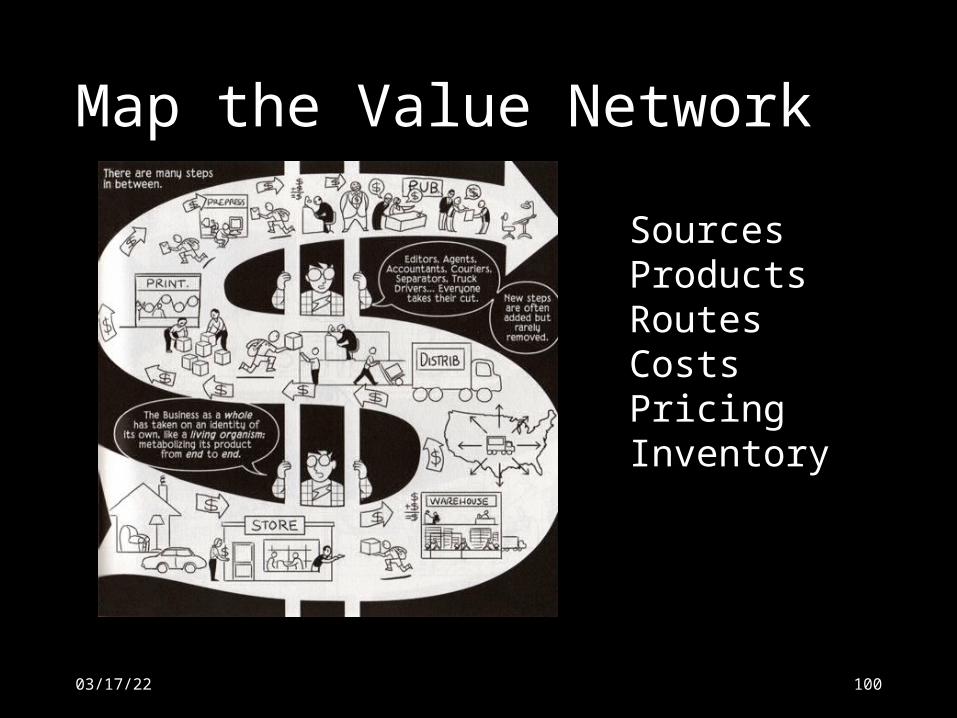

Map the Value Network

04/15/23 100

SourcesProductsRoutesCostsPricingInventory

Product Visibility

• Track and trace from source to your operation

• Procurement is a supply chain function

• Ensure integrity of the product

• Identify opportunities to improve in-stock performance throughout the supply chain• Temperature• Quality• On-time• Lowest Cost

04/15/23 101

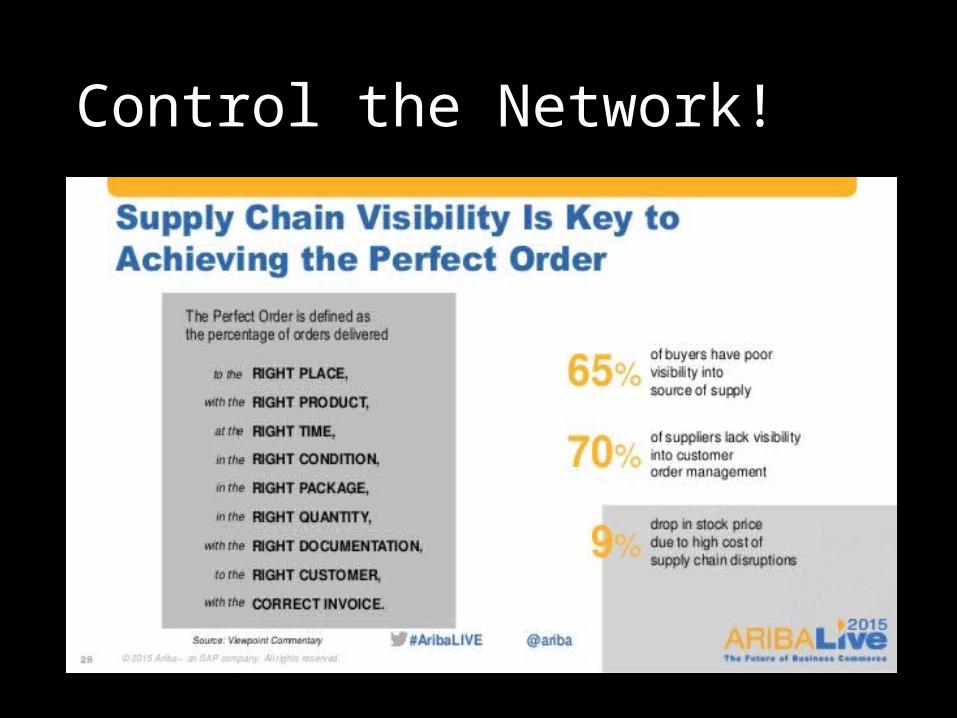

Control the Network!

2. Inventory Management Plan

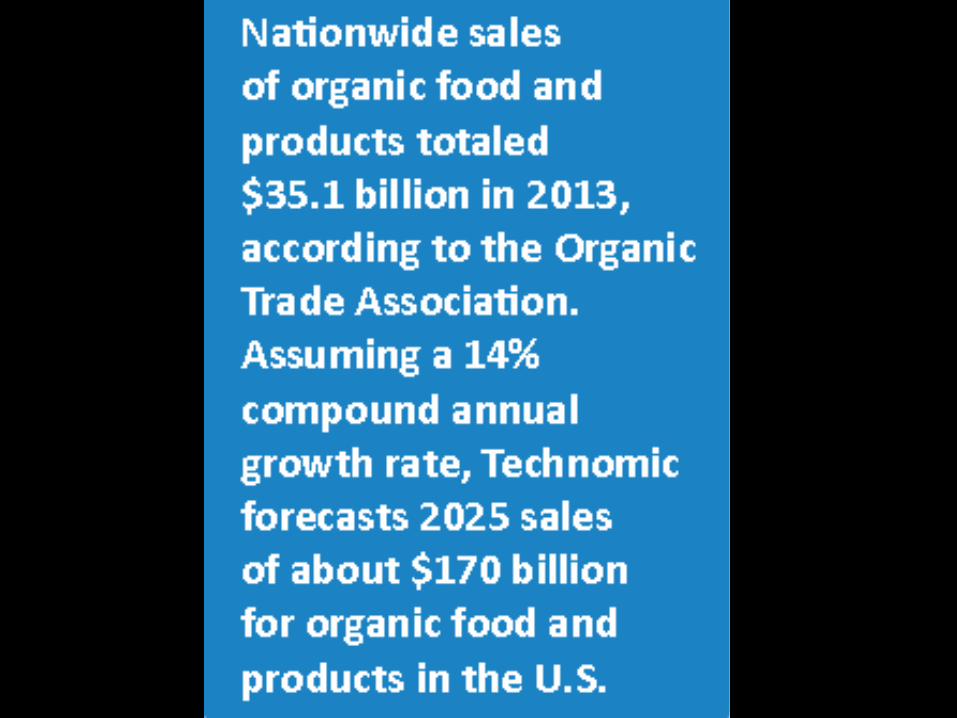

• New Items:• Current strategy of 1 for 1 doesn’t work!• Organics growing at 14% rate annually• Fresh, Natural, Healthy 10-15% annually• If you say no! You make UNFI the hero.

• Inventory performance controls your productivity (layout, shorts, mistakes)

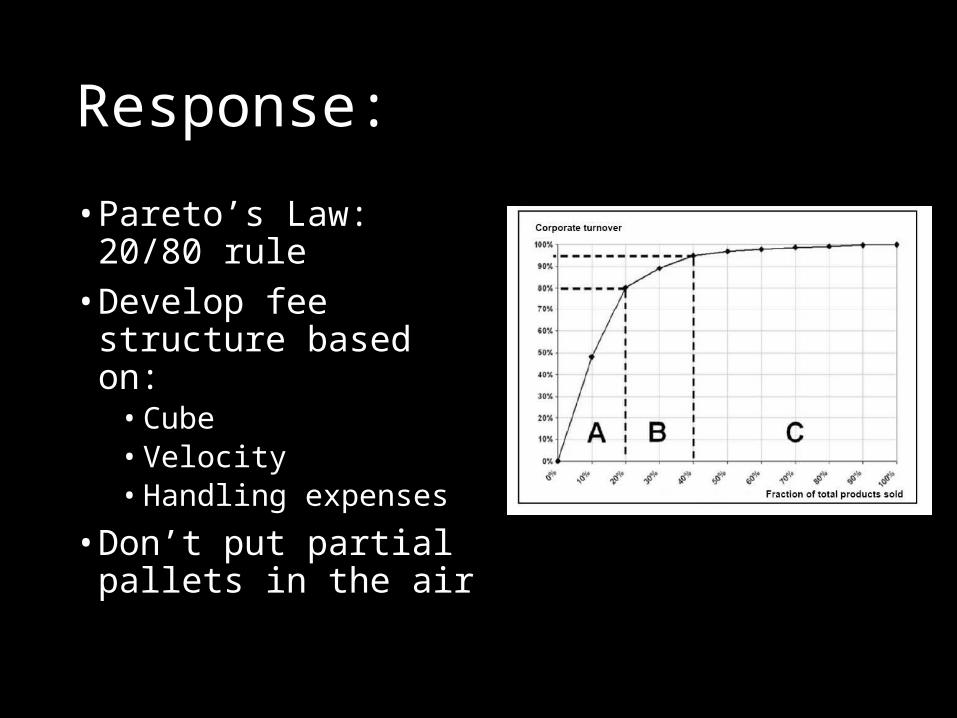

Response:

• Pareto’s Law: 20/80 rule

• Develop fee structure based on:• Cube• Velocity• Handling expenses

• Don’t put partial pallets in the air

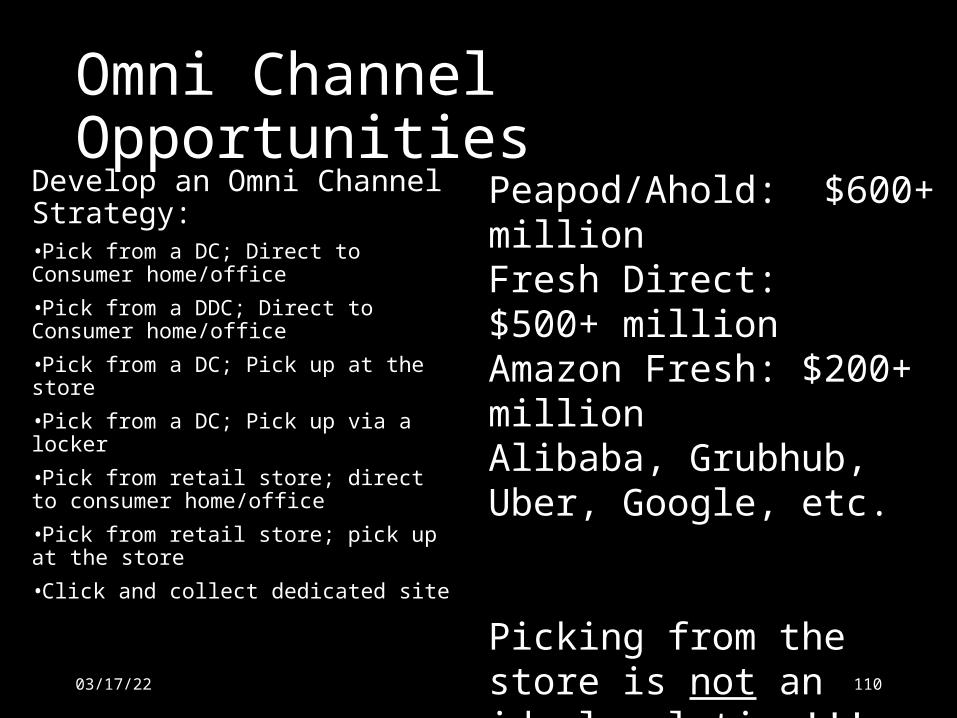

3. Step UP to the Omnichannel Opportunity

Omni Channel OpportunitiesDevelop an Omni Channel Strategy:•Pick from a DC; Direct to Consumer home/office

•Pick from a DDC; Direct to Consumer home/office

•Pick from a DC; Pick up at the store

•Pick from a DC; Pick up via a locker

•Pick from retail store; direct to consumer home/office

•Pick from retail store; pick up at the store

•Click and collect dedicated site

04/15/23 110

Peapod/Ahold: $600+ million Fresh Direct: $500+ millionAmazon Fresh: $200+ millionAlibaba, Grubhub, Uber, Google, etc.

Picking from the store is not an ideal solution!!!

4. Embrace Technology• Invest in the technical opportunities

Goal is to go paperless with immediate response time

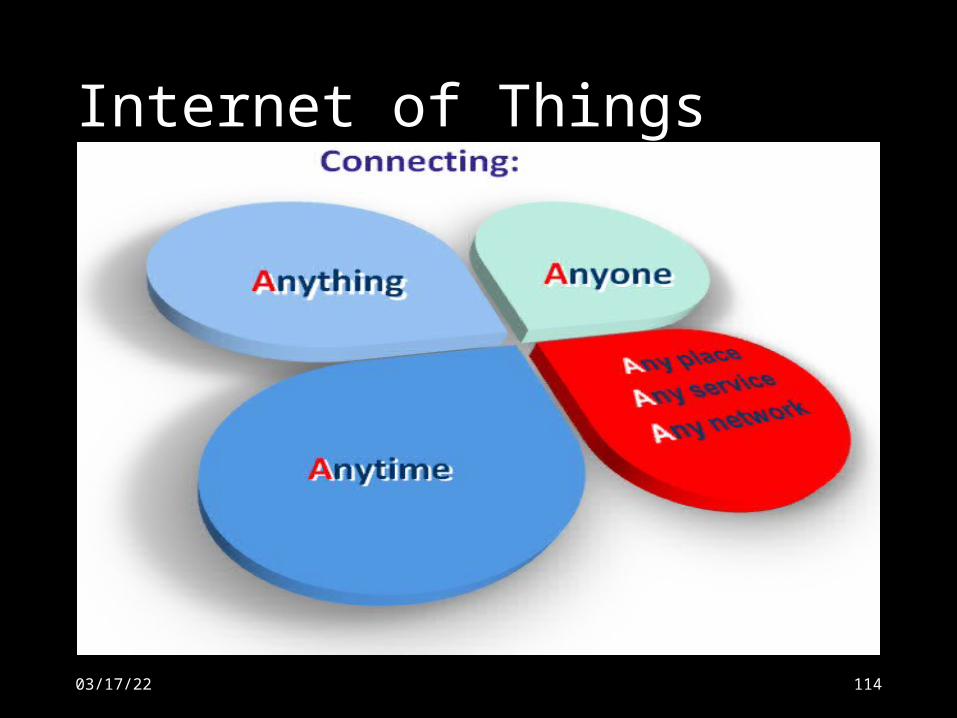

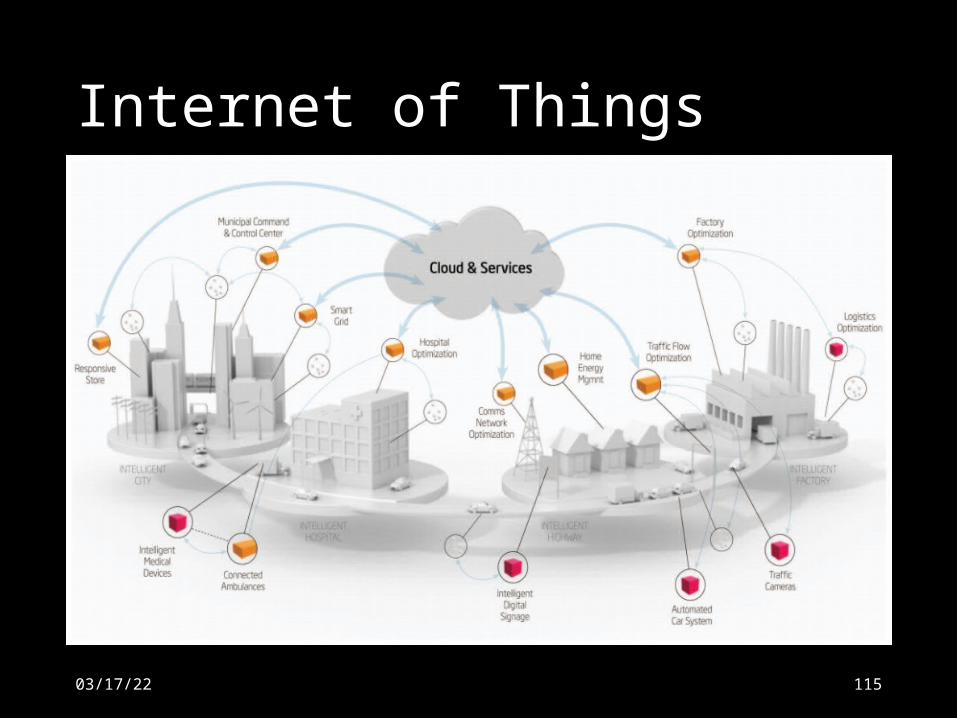

• Internet of things

Wearables

Scannables

Flyables

• Big Data: the ability to analyze and identify developments as they happen

• Cloud: Opportunity to connect/collaborate/share

Target: 2016

Amazon: Partners with Auburn University RFID lab

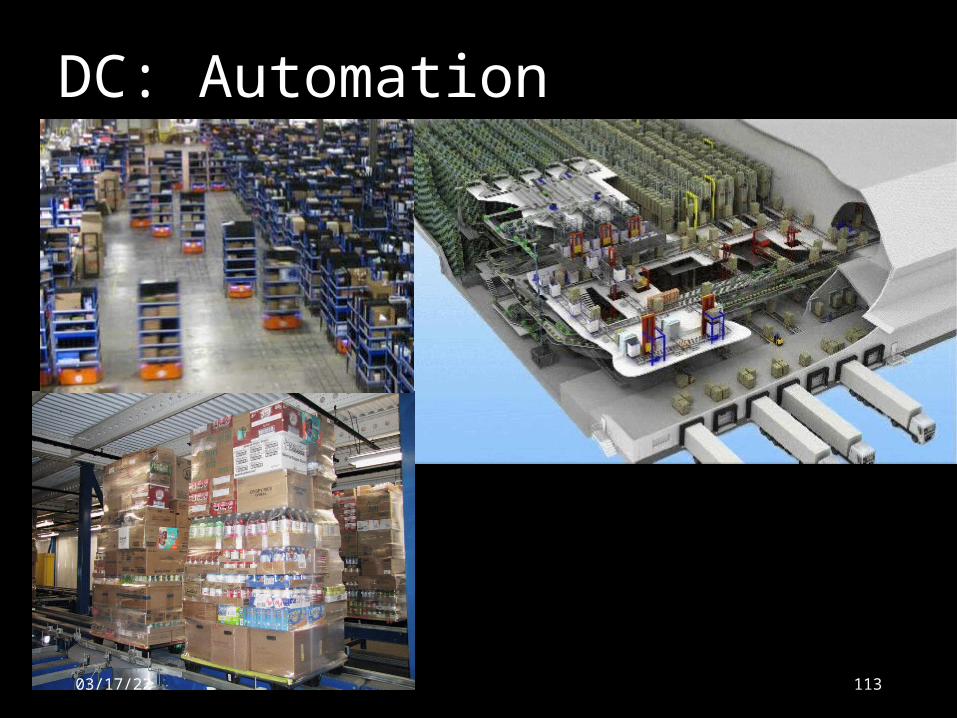

DC: Automation

113

Take Fingerprints off the Box!

04/15/23

Internet of Things

04/15/23 114

Internet of Things

04/15/23 115

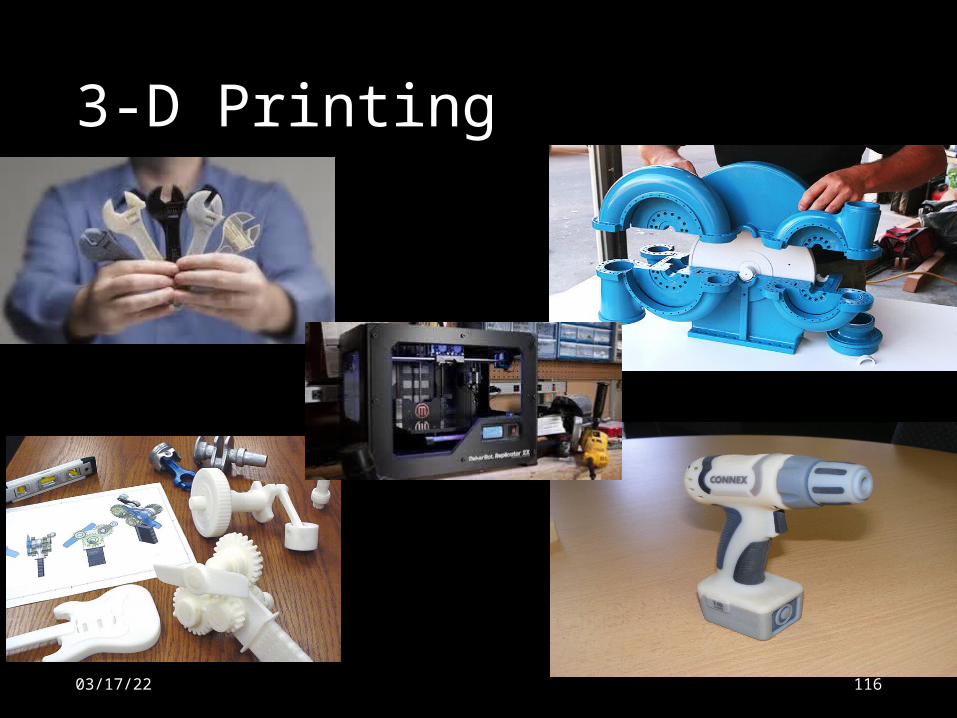

3-D Printing

04/15/23 116

Video: SAP GlassGoing Paperless in the supply chain• https://www.youtube.com/watch?v=9Wv9k_ssLcI

04/15/23 117

Video: Amazon Drones

• https://www.youtube.com/watch?v=Le46ERPMlWU

• https://www.youtube.com/watch?v=qmHwXf8JUOw

Video: Kiva

• https://www.youtube.com/watch?v=6KRjuuEVEZs

5. Invest in Education/Mentors

5. Invest in Education/Mentors• Share Groups

• Association local meetings• CSCMP, APICS, WERC, ASM

• Road Trips

• Educational Programs: 600 colleges/universities now offer degrees in Supply Chain Management• Logistics Institute (Canada)• Consultants

• Blogs

04/15/23 121

Blogs:

• Food: valuenetworkissues.blogspot.com•Marketing: haccmarketing.blogspot.com• Logistics: logisticsvaluenetworks.blogspot.com • http://www.scoop.it/t/food-value-networks• [email protected]• 610-256-6636

• Post on www.slideshare.com04/15/23 122

Closing Thought

123