ofi july/august 2015

DESCRIPTION

ÂTRANSCRIPT

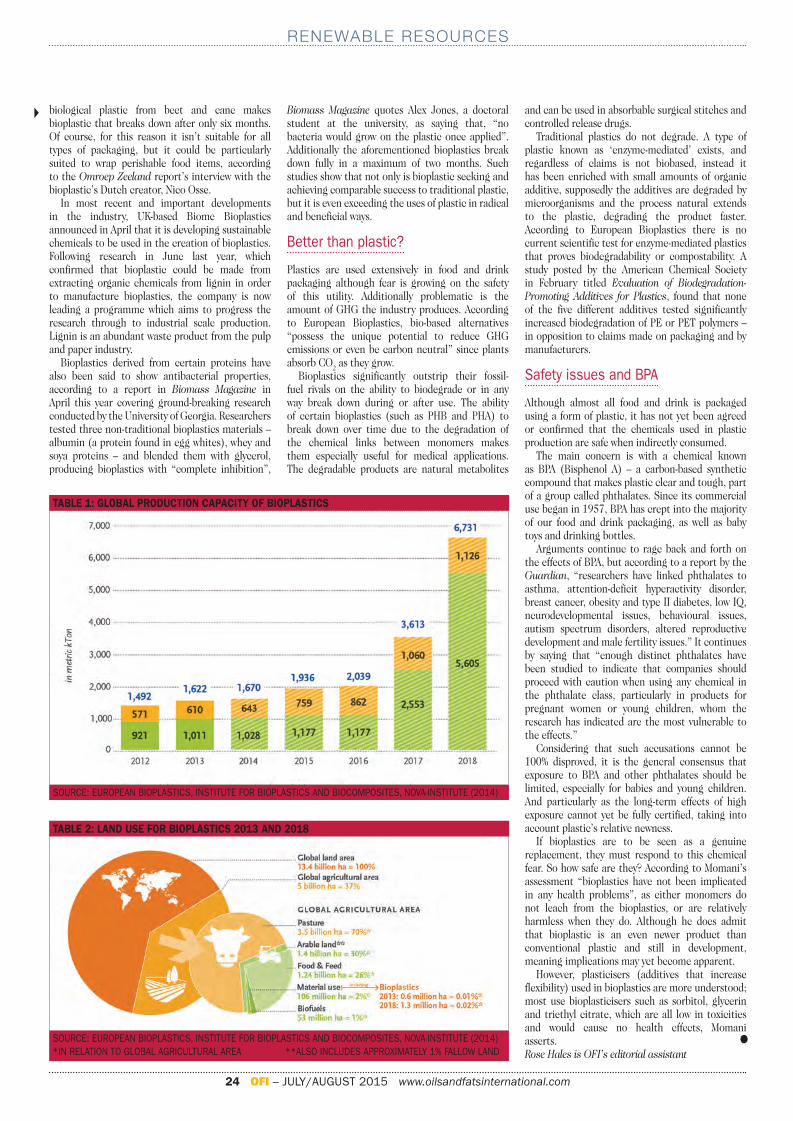

BIOPLASTICSNovel feedstocks

RUSSIA & UKRAINE

The impact of unrest

BIOTECHTerminator genes

July/Aug 2015 t Vol 31 No 6www.oilsandfatsinternational.com

Cover July/August.indd 1 16/07/2015 11:49

Leading edge technologies for refining plants

NeutralisingShort/long mix Neutralising

• Multimix Neutralising• Miscella Neutralising• Silica Purification

Bleaching

• Sparbleach Bleaching• Unibleach with prefiltration• Silica Purification

Winterising

•Wintrend Winterising•Combifrac Winterising

Deodorising

•Qualistock Deodorising•Multistock Deodorising• Sublimax Ice Condensing

Degumming

• Acid Degumming (wet/dry)• Ultra-shear acid Degumming•Bio Degumming•Membrane Degumming

Detoxification

• Combiclean Process• Active carbon Purification

FEATURESRENEWABLE RESOURCES

20 Pennycress:what’s the catch?

22 Seeking futuristic feedstocks

INSTRUMENTATION & ANALYSIS

25 The trans fatty acid conundrum

28 Setting a benchmark

BIOFUELS

30 If the cap fits

OILSEEDS

32 An inconvenient answer

RUSSIA & UKRAINE

34 The impact of unrest

BIOTECHNOLOGY

38 Hitting thegenetic switch

THE BUSINESS MAGAZINE FOR THE OILS AND FATS INDUSTRY

1 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

CONTENTS

LIKE BIOFUELS, BIOPLASTICS RAISE CONCERNS OVER THE USE OF FOOD CROPS AS FEEDSTOCKS, BUT ARE THESE CONCERNS VALID AND WHAT WILL REPLACE THEM? P22

VOL. 31 NO. 6 JULY/AUGUST 2015

EDITORIAL:

Editor: Serena LimTel: +44(0)1737 855066; Fax: +44 (0)1737 855034E-mail: [email protected]

Editorial Assistant: Rose HalesTel: +44(0)1737 855157; Fax: +44 (0)1737 855034E-mail: [email protected]

SALES:

Sales Manager: Mark Winthrop-WallaceTel: +44 (0)1737 855 114; Fax: +44 (0)1737 855034E-mail: [email protected]

Sales Consultant: Anita RevisTel: +44 (0)1737 855068; Fax: +44 (0)1737 855034E-mail: [email protected]

Chinese Sales Executive: Erik HeathTel: +44 (0)1737 855108; Fax: +44 (0)1737 855034E-mail: [email protected]

PRODUCTION:

Production Editor: Nikki WellerTel: +44 (0) 1737 855088; Fax: +44 (0)1737 855034E-mail: [email protected]

CORPORATE:

Vice President: Steve DiproseTel: +44 (0)1737 855164E-mail: [email protected]

SUBSCRIPTIONS:Tel: +44 (0)1737 855032; Fax: +44 (0)1737 855034E-mail: [email protected]: Subscriptions, Quartz House, 20 Clarendon Road, Redhill, Surrey, RH1 1QX, UK

Annual Subscription: UK £141, Overseas £163.Two years: UK £254, Overseas £293. Single copy £35

© 2015 Quartz Business Media ISSN 0267-8853

Website: www.oilsandfatsinternational.com

A member of FOSFA

Oils & Fats International (USPS No: 020-747) is published eight times/year by Quartz Business Media Ltd and distributed in the USA by DSW, 75 Aberdeen Road, Emigsville PA 17318-0437. Periodicals postage paid at Emigsville, PA. POSTMASTER: Send address changes to Oils & Fats c/o PO Box 437, Emigsville, PA 17318-0437

Published by Quartz Business Media Ltd Quartz House, 20 Clarendon RoadRedhill, Surrey RH1 1QX, UKTel: +44 (0)1737 855000Fax: +44 (0)1737 855034 E-mail: [email protected]

Printed by Pensord Press, Gwent, Wales

@oilsandfatsint Oils & Fats International

NEWS & EVENTS

2

Comment

Lawsuits may follow FDA move on trans fat

News

US removes GRAS status on trans fat

Biofuels News

Petrobras and Ceres moving away from biofuels in Brazil

Biotech News

US GMO framework to be modernised

Transport & Logistics News

Bunge expands in Australia

Renewable Materials News

Coca-Cola launches 100% sugarcane-based PET bottle

Diary of Events

International Market Review

Statistics

2

6

8

10

12

16

40

13

PHOT

O: C

HERN

ETSK

AYA/

DREA

MST

IME

PHOT

O: K

ARAP

IRU/

DOLL

ARPH

OTOC

LUB

Contents.indd 1 16/07/2015 12:23

Russia extends current food embargo

US removes GRAS status on trans fat Partially hydrogenated oils, the

primary source of artificial trans fats in processed foods, are no longer “generally recognised as safe” (GRAS) for human consumption, the US Food and Drug Administration (FDA) has said.

The FDA said it had conducted a thorough review of scientific evidence, resulting in its announcement on 16 June. US food manufacturers have three years to comply and remove all artificial trans fats from their products.

“The FDA’s action on this major source of artificial trans fat demonstrates the agency’s commitment to the heart health of all Americans,” said FDA’s acting commissioner Stephen Ostroff, M.D. “This action is expected toreduce coronary heart diseaseand prevent thousands of fatalheart attacks every year.”

Although the ban will cost the food industry US$6.2bn in the next 20 years as it reformulates products and substitutes ingredients, it is estimated US$140bn will be saved during the same period mainly due to lower spending on healthcare,

according to Bloomberg estimates.

In July 2003, a labelling rule was announced requiring producers to say if their products contained trans fats. The FDA estimated that there was a decrease of 78% of consumer consumption between 2003 and 2012, with the labelling rule and industry reformulation being credited for the change.

Just days after the GRAS status was removed, a false marketing class action lawsuit was filed against H.J.Heinz Co (Heinz) on 18 June, accusing Heinz of making false claims on the amount of trans fats contained in two of its products, Top Class Actions reported.

The lawsuit alleges that Heinz labelled both its brand name frozen French fires and tater tots as containing zero trans fats when they contained high levels of partially hydrogenated oils.

Heinz is not the first company to be accused of falsely advertising levels of trans fat. Similar allegations were made against ConAgra Foods earlier in June.

Russian embargoes on manyWestern products including

cooking oils, animal fats and dairy products are to be extended for a further six months, according to a Bloomberg report on 22 June.

Russia initially imposed the bans in retaliation against EU sanctions following the crisis in Ukraine. EU foreign ministers extended the sanctions against Russia on 22 June and the

Russian prime minister Dmitry Medvedev immediately announced through a spokeswoman that a proposal for the continuation of the Russian bans, which were due to expire on 8 August, had been submitted to the president.

Australia, Canada, the EU, Norway and the USA are all affected by the bans. The current banned import list is expected to remain the same.

Acooking oil producer in southwest China, Wei Mingjin, received the death sentence in January having been found guilty of selling

more than 19,000 tonnes of tainted oil, refered to in China as ‘gutter oil’, according to a report in China Daily. The cooking oil was made from waste byproducts of slaughtered cattle that was unfit for human consumption.

The death sentence, which has been reprieved for two years, is the result of rigorous new sentencing guidelines for food safety crimes that were issued in 2013. Additionally, Wei was fined RMB340M (US$56M). Two accomplices were given prison terms.

2 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

NEWS

COMMENT

Lawsuits may follow FDA move on trans fat

The US Food and Drug Administration (FDA) has ended a two-year public comment period by confirming on 16 June that it is removing the

‘generally recognized as safe’ (GRAS) status from partially hydrogenated oils (PHOs) – the main source of artificial trans fatty acids in our diets.

Companies will have three years to remove PHOs from their food, although they will be able to file a petition seeking the specific use of PHOs in a product if they

have data proving the use isn’t harmful.However, some observers believe a wave of private lawsuits could

force firms to reformulate or remove PHO-containing products long before 18 June 2018.

Just two days after the FDA announcement, a California man has already filed a federal lawsuit against H J Heniz Co over the use of PHOs in its frozen potato products (see story, right).

In a commentary in Forbes.com, Glenn Lammi wrote that two key omissions from the FDA will support litigation over PHOs.

The FDA has not included a statement that PHO-containing products currently on the shelves up to June 2018 are marketed lawfully.

Under federal law, products containing unapproved additives are considered adulterated and subject to seizure.

This opens the door for people to sue food companies now over the presence of PHOs.

Secondly, the FDA says nothing about its GRAS-status decision only taking effect from now.

Without an explicit FDA statement, the door is open for retroactive lawsuits suing for reimbursement of public health care expenditure over the costs of treating cardiovascular disease, Type-II diabetes and other conditions.

Time will tell how many lawsuits are eventually filed.

A victory for public healthIn the meantime, the FDA has taken a positive step in tackling the trans fat problem.

Our feature on page ? traces the development of partial hydrogenation in the 1970s to tackle fears over saturated and animal fats, to the discovery of trans fat formation and growing concerns over their effect on our health.

Trans fats – used to improve the taste, texture and shelf life of foods – can be found in baked, fried and snack foods. They increase our risk of heart disease by increasing the ‘bad’ LDL cholesterol in our blood, while also lowering the ‘good’ HDL cholesterol.

When the FDA first determined in 2013 that PHOs were not generally thought to be safe, it said that eliminating trans fats from the food supply would prevent 20,000 heart attacks and 7,000 deaths every year in the USA.

The latest FDA move is therefore a “major victory for public health”, says Michael Jacobson, executive director of the Center for Science in the Public Interest.

“I don’t know how many lives will be saved, but probably in the thousands per year when all the companies are in compliance.” w

Chinese producer receives death sentence for selling tainted oil

Comment and News.indd 1 13/07/2015 11:30

Complaint over illegal land grabs in BorneoABorneo based human rights organisation,

Lingkaran Advokasidan Riset (LinkAR), filed a complaint on 11 May against PT Swadaya Mukti Prakarsa (PT SMP) – a key Wilmar Group supplier and subsidiary of First Resources Group – claiming the company had breached standards and made illegal land grabs, a press release publicised in June.

The complaint letter was delivered to the Roundtable on Sustainable Palm Oil (RSPO) and was presented on behalf of the indigenous communities living in West Kalimantan, Borneo, where PT SMP owns a permit covering

an area of around 3,700ha.Batu Daya Village in Simpang Dua Sub

District, Ketapang Regency is surrounded by plantation operations and has been the site of multiple clashes between PT SMP and the indigenous communities.

The press release said that on 5 May, five members of the village were forcibly arrested by the West Kalimantan Police Mobile Brigade and PT SMP security staff following demonstrations by community members, who accused PT SMP of conducting land-clearing operations in an area outside its

authorised permit zone. The complaint includes allegations that PT SMP cleared land using fire (which is illegal in Indonesia), not informing the community about the environmental impact analysis (EIA) of its proposed development. and intentions to withhold profits from the community for up to 18 years.

The district administration also asserted in a subsequent decree that even though the location permit had expired, PT SMP continued to clear and develop land.

PT SMP has not responded to the allegations.

3 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

NEWS

USA: The Agricultural Research Service of the US Department of Agriculture and Oklahoma State University have collaborated to grow foundation seed for a new type of Spanish peanut called OLé, they announced. It contains a greater proportion of oleic to linoleic acid than other high-oleic peanuts.

EGYPT: A new protocol on the recycling of used cooking oil was signed in Cairo in June, The Cairo Post reported. Under the new protocol, cooking oil would be collected by the Ministry of Supply in return for points to be exchanged for food, and then delivered to Alexandria Company for Petroleum Additives (ACPA) to be turned into biodiesel.

DENMARK: The European Commission has launched an investigation into the now-repealed Danish ‘fat tax’, according to a report in Tax-News. The tax was added to saturated fat in certain products in 2011 and was abolished in January 2013. The investigation will focus on whether some companies illegally benefitted by not being taxed correctly; all products containing more than 2.3% saturated fat should have been taxed. The Danish government said it planned to have a dialogue with the EC to find a sensible solution, Tax-News said.

DENMARK: Emulsifier producer Palsgaard has announced in its 2014 CRS report that sustainability and CO2 neutrality are its top concerns for the next five years, and that its sustainability efforts are in line with the principles of the UN Global Compact.

IN BRIEFInternational Olive Council agrees on new draft

Ruchi Soya Industries Limited,India’s number one edible

oil and soya foods company, has signed a €4.5M deal with NGO Solidaridad to expand sustainable production of palm oil in the country, a press release announced on 5 June.

Ruchi will share 55% of the investment, and Solidaridad – which works across supply chains to facilitate social and ecological responsibility – will take 45%.

Farmers will be trained to grow more palm oil with less land, water and energy, while also protecting the environment.

“The aim over the next five years is to make a significant volume of sustainable palm oil available for India, to save at least 1.5tr litres of water in palm production and generate major employment in the rural areas,” Solidaridad said.

Ruchi said the government had identified two million hectares of land for oil palm cultivation in India and it hoped to help India in saving valuable foreign exchange.

Sustainable palm oil deal in India

Members of the International Olive Council (IOC)met before the Council’s 24th session in Madrid

in June to discuss the new draft text that will replace the 2005 International Agreement on Olive Oil and Table Oils – as it is officially known. The Olive Oil Times reported the news, adding that the draft text will form a basis for negotiations taking place in October at the United Nations conference in Geneva.

Once agreed, the new document will enter into force on 1 January 2017 and will continue to be used until the end of 2026.

The 2005 agreement was also negotiated in Geneva, in April 2005. It is understood to have come a long way from previous agreements and new, innovative features would “help the IOC to adapt to the changing demands of the olive sector and society”, according to the IOC website.

According to Olive Oil Times, there are several important changes that the new draft text makes to the current agreement. These are:

More weight given to consumer countries. A formula has been proposed which will calculate each member’s participation shares in the budget by equally considering production, exports and imports.A new decision-making process for topics related to the IOC’s international trade standard. This includes new steps aimed at consensus-building, which will incorporate a new voting procedure.

After the discussions had come to an end, the Council of Members session was held from 16-19 June. The specialist committee discussed several measures for possible adoption.

Sungai Budi plans to expand plantsSungai Budi has set aside a

sum of Rp1.67tr (US$125M) for the construction of new sugar and palm oil plants, the Jakarta Globe reported in June.

The agriculture-based manufacturer, one of the largest in Indonesia, controls Tunas Baru Lampung and Budi Starch & Sweetener.

Tunas Baru’s vice president Sudarmo Tasmin told the Jakarta Globe that the company would

be investing Rp1.5tr (US$237bn) in a new sugar mill this year in Lampung. The mill will have a processing capacity of 8,000 tonnes/day of cane and should be operating by the end of 2016.

In addition Tunas Baru has plans to build a Rp200bn (US$3bn) biodiesel plant, Sudarmo said the plant was expected to contribute to 35% of the company’s revenue in 2017.

KTG looks to expand in ChinaGerman farm company KTG Agrar announced plans for a major

expansion into the Chinese food and grain sector – including GMO-free soyabeans, Reuters reported in June. The announcement follows the news that a unit of the Chinese group Fosun International bought a 9% stake in KTG.

KTG said it hoped to increase food sales to China to between €100-200M annually in the next three years. This year, the European- listed farm company expected to make sales of between €20-30M, KTG CEO Siegfried Hofreiter told Reuters. Around 80% of KTG’s sales are currently made in Germany, with the remaining 20% being exports. Hofreiter hoped that China could soon become the company’s largest market.

KTG cultivates organic grains, rapeseed, soyabeans, sugar beet and other crops and said it was seeing strong demand from 700M middle-class Chinese consumers for organic, GMO-free products.

t

t

Comment and News.indd 2 13/07/2015 11:30

NEWS

WORLD: The cheap price of petroleum has been recognised as causing the lowest global food prices for five years, according to the Food Price Watch’s latest edition in July. Less expensive fertiliser, fuel and transportation costs benefitted the agriculture and food sectors. Food prices continued to be steady despite a recent hike in petroleum prices recently, the report said. However, the arrival of El Niño could cause prices to increase again in the coming months.

PHILIPPINES: Small coconut farmers have reached a sustainability milestone by producing the world’s first Rainforest Alliance certified copra, thanks to the work of German international development company GIZ, BASF and Cargill, Cargill announced on 17 June. Agricultural training, sustainability training and access to new drying technology had resulted in 300 small farmers meeting the standards of the copra, the dried coconut flesh needed to process coconut oil, Cargill said.

MALAYSIA: Mr D Chandramohan, director of corporate affairs for Cargill Malaysia, has been appointed as chairman of the Palm Oil Refiners Association of Malaysia (PORAM) for 2015-2017. PORAM said Chandramohan’s expertise in government and industry relations, palm sustainability, communication and corporate responsibility activities for Cargill would serve the industry well. PORAM was formed in 1975 to present a representative voice to the government and trade in matters related to the palm oil industry. This year PORAM will celebrate its 40th anniversary.

MALAYSIA: The government’s Malaysian Sustainable Palm Oil (MSPO) certification standard has helped more than 400,000 smallholders become certificated as sustainable palm oil producers, the Jakarta Post reported in July. The report said the government’s standard made it easier for small producers to become certified, compared to the rules and costs of Roundtable on Sustainable Palm Oil (RSPO) certification.

IN BRIEF Fish oil market to grow by 6%

4 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

Wilmar and Volac in animal feed fat partnership

Wilmar International and Volac International announced the

creation of a global animal feed fat joint venture on 6 July.

The two companies said that the new partnership, Volac Wilmar Feed Ingredients (VWFI), would become a global leader in animal feed fats and support the dairy farming industry through a range of feed fat products, which were sourced responsibly and sustainably by “maximising operational efficiency”.

UK-based Volac brought its nutritional reputation, global brand and sales network to the partnership, with Singapore’s Wilmar providing operational raw material logistics.

According to David Neville, managing director of Volac Animal Nutrition, responsibly sourced feedstocks would play a vital role in sustainable livestock nutrition in the future. Therefore the company’s strategy was to expand the fat business.

Napoleon Pefianco, managing director of Wilmar Europe Holdings BV, said he hoped the joint venture would lead the way in the ethically sourced feed fat ingredients market, creating a global and sustainable solution.

The global fish oil market will grow to US$2.63bn by 2020, with supplements and functional

foods evolving as a promising application market, according to a report published in May by Allied Market Research. A compound annual growth rate of 6.1% between 2015 and 2020 is estimated for the market.

Aquaculture is currently the largest market for fish oil, although the study predicts that the supplement and functional food market will evolve to become a promising contender. The report said fish oil is a prime ingredient in aqua feed, which meant the market tended to grow in proportion with the aquaculture industry. It was also affected by the demand-supply gap, caused by strict fishing quotas and adverse climate conditions.

Fish oil had a high content of essential long chain omega 3 fatty acids, resulting in its wide use in many human and animal nutrition applications as a food and feed supplement. Omega 3 fish oil was becoming increasingly popular in nutraceutical and

pharmaceutical markets, which was providing a boost for the industry, the report said.

More than 50% of the world’s fish oil was produced in Latin America, chiefly Peru and Chile. The study found that China and Japan collectively accounted for about 39% of the market share, with Denmark and Norway both being major producers and consumers in the European market. Aquaculture production was rising in Asia in countries such as China, India, Vietnam and Indonesia, causing a rise in aquaculture grade fish oil requirements in the region. In North America and Europe the consumption for fish oil was for use in pharmaceuticals and the supplement and functional food industries – together these regions accounted for around two-thirds of global revenue for these applications. Furthermore, in Japan nutritional

fish oil consumption was high as the aging population took advantage of its

health benefits.

PHOTO: IVOLODINA/DOLLARPHOTOCLUB

Taiwan adds tracers to waste oilThe Environmental Protection Administration of Taiwan has revealed

10 tracers for waste cooking oil in an attempt to crackdown on substandard oil re-entering the food supply, the Taipei Times reported in February.

Under the new system, a tracer would be added at the food outlet, with an additional dose going in at the recycling facility before the oil is transported to soap and biodiesel manufacturers.

“The source of most problematic oil samples would be revealed following an analysis of the tracers, which would then lead us to the recycling or reuse facility the oil is originating from,” EPA Minister Wei Kuo-yen told the Taipei Times.

Out of the 10 tracers, six would be transparent. Wei said that these would be prioritised over the four additional opaque tracers.

The scheme is still being trialled and is voluntary at the moment. However, three local governments had already agreed to their use.

Hong Kong proposing new regulations for ‘gutter’ oilOn 7 July, the Hong Kong

government announced a three-month consultation on a new regulation to control the quality of edible oils and fats manufactured in the city, the South China Morning Post reported.

The proposals are in response to the Taiwanese gutter oil scandal last year (see News, OFI October/November 2014) and would amend the current Waste Disposal Ordinance, including a new licensing system. Individual licenses will be required for collectors, disposers, importers and exporters of waste oil.

Operating without a license could result in a fine or imprisonment. It will be mandatory for food manufacturers, canteens and restaurants to hand their used cooking oil to licensed collectors only, and records must be kept.

Furthermore, producers must provide official certificates, the South China Morning Post said, issued by a recognised independent testing institution.

The report said that vegetable oils, animal fats, and edible fats and oils used as ingredients would be covered. Fat emulsions (such as butter and cocoa butter) would be exempt.

Comment and News.indd 3 13/07/2015 11:30

PREP & DEHULLING | EXTRACTION | OIL PROCESSING | BIODIESEL | PILOT PLANT

CROWN IRON WORKS COMPANYCall us today 1-651-639-8900 or Visit us at www.crowniron.com

Additional offices in Argentina, Brazil, China, England, Honduras, India, Mexico, Russia and Ukraine

The Global Leader in Oil Seed Processing

Crown Raw Materials Ad-A4_MAR14_Layout 1 3/13/14 2:03 PM Page 1

BIOFUELS NEWS

FINLAND: The government has announced plans to increase the share of renewable fuel use to 40% by 2030, according to Biofuels Digest. Currently the country’s renewable fuel use is 8%.

MALAYSIA: Mercedes-Benz Malaysia has backtracked on its previous claim that its vehicles could not be run on B10 by saying that all Malaysian vehicles are fine to run on the blended biodiesel, according to Biofuels Digest. Mercedes-Benz Malaysia, UMW Toyota and Volkswagen Malaysia all followed in the footsteps of BMW Malaysia and in June issued warnings saying using B10 would cause adverse effects in their engines.

ARGENTINA: The biodiesel export tax for May has been cut to 9.8%, down from 13.2%, which was set for April, according to a report in Biofuels Digest on 22 June. Although it was a decrease of more than a quarter from April, the export tax was still nearly double any of the taxes set last year.

BRAZIL: Changes were made to the country’s tax policy on imported ethanol on 22 June, Ethanol Producer reported. President Dilma Rousseff signed a decree creating equal tax for domestic and imported products, including ethanol. This was a levelling of the playing field rather than an importation tariff, a statement from Brazil’s sugarcane association UNICA stressed.

EU: 2013-14 was a difficult year for the European ethanol industry due to a 30% decrease in domestic prices, the annual report from the European renewable ethanol association (ePURE) published 16 June revealed. Europe consumed 7.7bn litres of ethanol in the 2013-14 period, the main uses were fuel (86%), industrial (7%) and food and beverages (7%), according to the report. Additionally the main feedstocks used were corn (42%), wheat (33%), sugar beet (18%) and other cereals (7%). ePURE’s secretary general, Robert Wright, said the decrease was ultimately driven by “the uncertainty surrounding Europe’s biofuels policy.”

IN BRIEF Petrobras and Ceres moving away from biofuels in Brazil

The European Union (EU)’sgoal of sourcing 20% of its

energy from renewables by 2020 is on track, according to an announcement on 16 June from the European Commission (EC).

Although, as a whole, the EU is due to meet its target, the Netherlands, Luxemburg and the UK are falling behind. The report said that as targets would only get tougher in the next five years, those countries falling behind (and those at risk of falling behind – Belgium, France, Malta and Spain) would have to intensify their efforts and look to use cooperation mechanisms with other member states in order to meet their targets.Ensus ethanol plant remains closed

CropEnergies’ UK-based Ensus plant, which closed in

February, is unlikely to reopen unless there is prolonged improvement in the European ethanol market, Agrimoney reported in May. Low margins when producing ethanol from grain have meant that the plant cannot operate on a cost-covering basis, a letter from CropEnergies signed by Joachim Lutz, the group’s chief executive explained.

According to Agrimoney, CropEnergies said 2014-15 was the “most difficult financial year in the history” of the company and it unveiled a loss of €11M

for the period, which ended inFebruary, with further losses expected.

Agrimoney said that government support for increased blending of ethanol into gasoline was lacking, which was causing a constant decline in EU fuel ethanol consumption.

However, positive news came in June, when CropEnergies announced a minor profit for the first quarter, according to Platts. Lower operating costs from the closed Ensus plant played a part, as well as higher prices due to there being less ethanol on the market.

B15 mandate will lead to54% consumption increase

Waste to ethanol plant completed

When Indonesia moves from its current B10 mandate to B15, consumption of biodiesel is expected to increase by 54%, according

to a Platts report in June. Typically the country consumes 1.3M tonnes/year, which would increase to 2M tonnes/year with the increased blending percentage.

It still remains unclear whether the mandate would be introduced as planned, an official from Pertamina, the country’s state-owned oil corporation, said. Platts said Pertamina had not bought any biodiesel since February, instead relying on inventories. A total of 767M litres of biodiesel had been contracted to Pertamina this year from producers Pelita Agung Agrindustri, Wilmar International and Darmex Agro, none of which had yet been delivered. This was largely due to biodiesel not being economically viable, the report said.

An export tax of US$50/tonne on crude palm oil and US$30/tonne for processed palm oil product shipments was finally introduced on 16 July after weeks of delays, Reuters reported. Proceeds from the tax, first announced in March, would be partly used to fund biodiesel subsidies.

6 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

EU on target to hit energy goal

Confidence in the Brazilianbiofuels sector appears to

be falling following reports that Petrobras and Ceres are planning to move away from investments in the market.

Petrobras, Brazil’s state-run oil company, is planning to sell its stake in ethanol producer Guarani SA to raise money for investment elsewhere and to pay off debts, according to a Reuters report on 17 June. The company’s ethanol plants would be the first to go as they were less profitable than other assets although it was reported that Petrobras does not plan to leave the biofuels sector completely.

However, on 23 June, Reuters reported that Petrobras’ plans had hit a hurdle, and the US$200M that its partner in Guarani, Tereos was willing to pay was not enough. In its latest financial reports, Petrobras valued its investment in Guarani as being worth US$407M. In an interview with Reuters, Tereos Brazil head Jacyr Costa said “we are not in the market to buy or to sell mills at the moment.”

Following a corruption scandal and stagnant output, Petrobras wanted to sell around US$3bn in assets this year and US$13.7bn by the end of 2016, Reuters said.

US-based biotech group Ceres

also announced a shift away from research into advanced biofuel crops in Brazil in June due to Brazil’s struggling economy and low oil prices causing “serious challenges”, according to an Agrimoney report (see story p8).

Ceres has been working alongside Brazil’s energy giant Raízen to develop sweet sorghum as a biofuel feedstock. However Agrimoney quoted the company as saying it considered sugarcane “a more attractive use of capital”.

Ceres chief executive Richard Hilton said Ceres wanted to direct its attention to “markets being fuelled by global prosperity growth”.

St1 Biofuels Oy completed thebuilding of an Etonolix plant in

Gothenburg, Sweden in June, the first outside Finland.

The plant would utilise feedstocks such as biowaste and process residues from local bakeries and bread past its sell-by date into ethanol for transport fuel, a press release from the company said.

The plant has an annual production capacity of 5M litres.

Biofuel News July.indd 1 20/07/2015 13:55

BIOFUELS NEWS

United Airlines invests US$30M in advanced biofuels

Malaysia plans to implement B10 mandate by October

The USA’s United Airlines has announced a large biofuel agreement with advanced

biofuels developer Fulcrum BioEnergy, Biofuels Digest reported on 30 June.

The agreement includes a US$30M direct investment in Fulcrum, the option to invest in five future commercial-scale aviation biofuel plants, and signed offtake agreements for up to 90M gallons/year of biofuel for 10 years.

According to AP Airlines, United chose to invest in the renewable energy company to reduce its vulnerability to oil price shocks and limit its carbon emissions.

Biofuels Digest said the offtake agreement was worth around US$1.58bn over the 10

years that it spans. This represented 3% of United’s annual fuel consumption.

United hoped to be receiving fuel by 2018 and could be taking 90M gallons/year by 2021, AP Airlines reported.

Fulcrum BioEnergy produces aviation biofuels from municipal solid waste. Its first commercial facility is currently under development near Reno, Nevada and is expected to open before the end of 2017.

Cathay Pacific also invested in Fulcrum BioEnergy in 2014 and signed offtake agreements from the first facility.

Fulcrum CEO Jim Macias said in an interview with Biofuels Digest: “This is a big event for us.

We are seeing more and more that United is going to be a prime mover. Having companies come in with a very significant commitment to participate is good news all around. For us, it tightens up our schedule and gives us greater certainty that these plants will be built on schedule and on time.”

The five new plants would range in size from 30M gallons to 60M gallons/year, according to Biofuels Digest.

United Airlines made its first test flight using biofuels in 2009 and, in 2011, powered its first passenger flight with algae-based fuel. It expects to begin flights from Los Angeles using AltAir Fuels’ biofuel this summer.

7 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

Targets for renewable energy have increased globally since 2005, and

164 countries have adopted at least one type of renewable energy target, according to an International Renewable Energy Agency report published in June.

“Governments are increasingly adopting renewable energy targets to meet multiple objectives including energy security, environmental sustainability and socio-economic benefits,” Adnan Amin, director-general of IRENA told Biodiesel Magazine. “The rapid growth of targets is just one more signal of the world’s ongoing shift towards renewable energy and away from fossil fuels.”

Out of the 164 countries, 131 are developing and emerging economies, and 150 of the countries have adopted renewable electricity targets. Additionally, targets for renewable fuel use in transport have increased from 27 in 2005 to 59 countries now.

The Malaysian government has announced plans to implement the

B10 biodiesel programme in October, The Rakyat Post reported in June. The programme will raise the country’s biodiesel mandate to 10%; the current mandate of 7% was implemented in November 2014.

The Star Online quoted Douglas Uggah Embas, the Minister of Plantation Industries and Commodities, who said: “We are looking at about 1M tonnes of crude palm oil (CPO) usage/year from the B10 biodiesel programme.”

It is hoped that the B10 mandate would support palm oil prices which are currently at RM2,344 (US$631)/tonne.

Renewable energy targets on the up

Naturally bleached vegetable oil, shaped by ONE ALL-ROUND SOLUTION: TONSIL®.FOR EFFICIENT AND SUSTAINABLE OIL, FAT AND BIOFUEL PURIFICATION: TONSIL® BY CLARIANT FUNCTIONAL MINERALS.Clariant’s TONSIL® bleaching earths have now been in use for more than 100 years. To meet today’s growing global demand and ensure certified solutions for your scope of applications, we constantly research into new products and into the optimization of TONSIL® qualities in Europe, America and Asia. TONSIL® has become synonymous with activated bleaching earths, which we view as both a challenge and an obligation for the future.

WWW.FUNCTIONALMINERALS.CLARIANT.COM

TONSIL® bleaching earths: the standard for efficient and sustainable purification and refinement.

49

20

14

VISIT US AT OILS + FATS 2015, MÜNCHEN 15 – 17 SEPTEMBER, HALL 3, BOOTH 3.208

3279_FM_Tonsil_128x185_en.indd 1 03.06.15 11:56

Biofuel News July.indd 2 20/07/2015 13:55

China’ changes GM approval regulations

$2.5M investment for field pennycressArvegenix, a mid-western US company developing

field pennycress for use asan advanced biofuel feedstock has successfully raised US$2.5M from investors including Monsanto and Cultivation Capital, according to the St. Louis Business Journal in a report published on 8 May.

The company would use the money to expand its research and development programme, fund regulatory studies and grow operations, the

report said. In addition, a general partner of Cultivation Capital, Rick Holton, would join the board at Arvegenix.

According to the report, another investor – the St Louis Arch Angels – invested US$500,000. The company invests in early-stage companies that it considers to have high growth potential. The Yield Lab, an agtech start-up developer led by Thad Simons, committed US$100,000.

US GMO framework to be modernised

US GMO framework must be updated

8 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

BIOTECH NEWS

Brazilian agriculturalbiotechnology company Ceres

announced on 19 June that it plans to realign its activities.

The restructure will move the company away from biofuel research, which was already announced earlier in the year and shift focus towards biotechnology traits for sugarcane and other crops, as well as food and forage opportunities.

Ceres wants to expand the number of market opportunities

available for its technology and products and said it would begin “prioritising its working capital in additional areas beyond Brazil.” It is expected that most of the realignment will be completed by the end of October this year.

Once the restructure has taken place, Ceres’ Brazilian operations will focus primarily on sorghum breeding and sugarcane. This will predominantly mean an expansion of the company’s sugarcane trait development activities for the

Brazilian sugarcane market. Ceres will fund these activities in part through a grant from the Brazilian government.

As Ceres implements its realignment plan, there will be a workforce reduction mainly in Brazil but also in the USA, and over US$1M of charges will be incurred through this process.

However, Ceres said the plan was expected to deliver cash savings of US$6-8M in fiscal year 2016.

The White House issued a memo on 2 Julydirecting three US agencies overseeing

biotechnology products to modernise and improve their regulatory framework, accordiing to reports from Reuters and Ethanol Producer magazine.

The memo was directed to the heads of the US Department of Agriculture (USDA), the US Food and Drug Administration (FDA) and the US Environmental Protection Agency (EPA).

The move was designed to boost public confidence in a regulatory framework which some critics had called a failure, Reuters said.

The memo defines biotechnology products as those developed through engineering of the targeted or in vitro manipulation of genetic information of organisms including plants, animals and microbes.

It said each agency had developed its own regulations, resulting in a complex system which protected health and the environment but sometimes left uncertainty over agency jurisdiction, processes and timeframes for review.

Several one-year objectives have been outlined including updating the 1986 Coordinated Framework for the Regulation

of Biotechnology (CF) to clarify the roles and responsibilities of the three agencies; formulating a long-term strategy to ensure the risks of any future products are efficiently assessed; supporting innovation, health and environmental protection; promoting public confidence; and increasing transparency and predictability while reducing unnecessary costs and burdens. The memo also called for the commissioning of an independent analysis of the future landscape of biotech products.

The White House has established a new Biotechnology Working Group to support these objectives.

Ceres realigns away from biofuels research

USA: SunOpta Inc, which processes non-GMO, organic soyabeans and corn, has become the first company in the USA to receive official verification that its manufacturing facility uses no genetically modified organisms or genetically engineered products, it announced in May.The facility in Hope, Minnesota gained an initial six-month period of certification from the US Department of Agriculture Process Verified Program. At the end of the period, SunOpta plans to apply for an extension. SunOpta will be the first US company to be able to label its products as non-GMO/GE.

WORLD: Monsanto’s talks with Syngenta shareholders were “very constructive”, Swiss newspaper Le Temps reported in an interview with Monsanto’s chief executive Hugh Grant on 7 July. Syngenta rebuffed Monsanto’s last offer of US$45bn plus an additional US$2bn reverse breakup fee on 8 June due to it ‘undervaluing’ the company. Grant told Le Temps that if Syngenta could detail why it believed it was worth more, then Monsanto may reconsider its offer.

USA: On 24 June, Monsanto reported net sales for its fiscal year 2015 third quarter rising to US$4.6bn, with gross profit increasing to US$2.7bn. It also reiterated its strategic rationale for buying Syngenta to create a new company providing a comprehensive portfolio to help farmers address current and future agricultural, environmental and sustainability challenges.

IN BRIEF

China is reported to have made an about-turnon its policies regarding genetically modified

organisms (GMO) through changes to its current GMO approval laws and its own research into the controversial science, according to reports from Reuters and Bloomberg in May.

China’s current regulations include three fixed deadlines each year for submitting new GMO crops for approval – 1 March, 1 July and 1 November. A biosafety committee meets at each deadline to review pending applications. Reuters Africa said China revealed plans to remove these deadlines in April. This would result in further delays to an already lengthy approval process for importing new GMO crops, according to CropLife Asia, a plant science industry association whose members include Monsanto, Bayer CropScience and DuPont.

In addition, the new version of the law stipulated

that “scientific, economic and social factors” would affect the ministry’s decision-making. This meant that consideration for approval would be broader, allowing scientific considerations to be taken into account, Reuters Africa said.

As well as law changes for importing GMOs, Bloomberg reported that China’s officials were preparing to turn the country into a GMO superpower. China’s leaders saw self-sufficiency in grain as a strategic imperative Bloomberg said. It quoted Origin chairman Han Gengchen who said, “Biotechnology is our investment for the future”.

Papers in China have called for more GMO research, a pro-GMO ad campaign was issued and companies were working on new rice varieties. Bloomberg said that at least US$3bn had been distributed by the government to institutes and companies to develop GMOs.

Biotech News July.indd 1 13/07/2015 11:05

Untitled-3 1 23/03/2015 11:52

BRAZIL: Archer Daniels Midland Company and Norton Lilly International announced on 15 June that their joint venture Agri Port Services LLC had acquired Brazilian port and shipping agency Blue Ocean Agencia Maritima (BOAM). BOAM serves as a shipping company at ports throughout the country and will expand Agri Port Services’ logistics offerings in Brazil.

WORLD: Inspection, testing and certification company SGS and BeFlexi, a leading flexitank provider, announced a new partnership on 7 July to provide a global flexitank logistics service to industries involved in break bulk cargo transportation.

BRAZIL: Raízen transported its first shipment of biodiesel by rail in June, according to Biofuels Digest. The Brazilian biofuel giant’s shipment travelled from Rondonópolis to Paulina. By taking advantage of reverse logistics, Raízen would be able to transport its biodiesel for much cheaper rates on railcars that would otherwise be empty, returning from delivering fossil fuels. According to the Biofuels Digest report, 50M litres of the fuel could be transported in this way annually.

IN BRIEF Bunge expands in Australia

India planning to use B20 at 12 major portsIndia’s Union Shipping Ministry

has announced that it will be using 20% blended biodiesel (B20) at 12 major ports, according to a report in The Hindu on 24 June. The Bureau of Indian Standards had been asked by the government to set higher biofuel standards for cars, trains, heavy engineering machines and generators, the report said.

The country’s first biodiesel dispensing pump was opened

in June at Haldia Port and will be supplied by Emami Agrotech, the edible and biodiesel arm of India’s Emami Group. Emami’s 300 tonnes/day Haldia, West Bengal biodiesel plant, which makes use of palm oil residues among other things, was eastern India’s first and largest biofuel facility set up in technical collaboration with Desmet Ballestra in 2006.

According to the union minister

for road transport, highways and shipping, Emami’s biodiesel is cost effective. “We are looking at the possibility of buying biodiesel for all major ports at a price much lower than the petroleum diesel price”, he told The Hindu.

In January, the government made a decision to allow biodiesel to be sold directly to consumers for transport use, which will expand India’s clean energy market.

Push for Sea-Tac airport to offer biofuels to all airlines

EU duties affected imports

The Seattle Port Commission wants the Seattle-Tacoma (Sea-Tac) International Airport to be

the first in North America to offer biofuels to all airlines, the Puget Sound Business Journal reported in June.

The commission wants financial incentives, such as those in Oslo and Amsterdam, to make biofuels more affordable for aviation. Currently biofuels cost significantly more than traditional petroleum-based

fuels. Several airlines including Alaska Airlines and Boeing had demonstrated the safe use of blended aviation biofuel, the commission said.

Sea-Tac is trying to minimise its greenhouse gas emissions and the port has already converted all its ground vehicles to electric. However, a representative for the Seattle Port Commission told the Puget Sound Business Journal that a study showed 89% of emissions from the airport came from jet engines.

Anti-dumping taxes andduties imposed by the EU on

Argentina and Indonesia are said to have contributed to a drop of 36% in biodiesel imports into Europe in 2014, according to a report from the Port of Rotterdam.

The duties were introduced in 2013 for five years as a measure to curb dumping (selling the

fuel for below cost) which was severely affecting EU producers. As a consequence of the taxes, domestic production has increased and Europe is becoming more of an internal market for biofuel.

The most important suppliers were Spain (contributing 60%) and Malaysia, with the largest amount being imported into the UK (42%) followed by France (17%).

10 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

TRANSPORT & LOGISTICS NEWS

Global processor and trader Bunge Ltd has begunconstruction of an inland grain storage site near

Kukerin, Western Australia, it announced in June. It hopes that the site will be fully operational by the harvest time later this year.

The first stage will create capacity for 120,000 tonnes, which will increase to 200,000 tonnes in time. Bunge is also planning the construction of a second site in Arthur River, Tasmania with an initial 160,000 tonne capacity, growing to 250,000 tonnes.

General manager of Bunge Australia, Chris Aucote, reiterated the importance of storage in the supply chain to assist with a smooth grain flow to port. He also said Bunge would like to provide solutions for

each grower to more efficiently manage harvests.In April, Bloomberg reported that Bunge was

contemplating opening an additional third port in either eastern or southern Australia. Currently Bunge has a port in Bunbury, Western Australia with another under construction in Geelong, in the southeast of the country. Schroder told Bloomberg that Bunge prefered to convert or build new facilities in Australia rather than making acquisitions.

Chief executive officer Soren Schroder also told Bloomberg that Bunge was looking at ways to access crop exports from the west coast of Canada.

Australia and Canada would complete the company’s “global footprint”, he said.

More ethanol moved by railThe US ethanol industry is

experiencing a rail-induced revival, according to Reuters, which reported that plummeting lease rates on cars, weak crude oil prices and new safety measures for transporting oil by rail may be responsible.

Rail car owners are apparently cleaning their tank cars so that they can carry corn-based ethanol instead. Reuters’ report was not clear on how widespread or long-term the trend is.

New tank safety standards were announced in May following a growing number of derailings and research which said the disasters would continue unless something was done. Although the standard applies to ethanol and petroleum, it is more lenient for the less volatile corn-based fuel.

It has also become more economical to transport crude oil by sea, which has caused a surplus of car capacity. It is though that the ethanol industry is taking advantage of the overcapacity and much lower tank car lease rates that it has resulted in. The Reuters report said the cost of taking a car off the rails was as much as US$100, so it was more cost effective to clean out the cars and make them suitable for ethanol transportation.

EARTHMOVERS IN ACTION AT KUKERIN, AUSTRALIA WHERE BUNGE IS BUILDING A GRAIN STORAGE SITE

PHOTO: WW

W.BUNGE.COM

.AU

Transport News.indd 1 13/07/2015 11:06

11 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

p11_Schutter_Blackmer_Ads_feature.qxp 22/07/2015 14:22 Page 20

WORLD: The natural fatty acids market sourced from vegetable oils, animal fats and crude tall oil was worth US$17.1bn in 2013, and is expected to climb to US$25.7bn by 2019, according to a new report from BCC Research. This will be equal to a compound annual growth rate of 7.1% over the five-year period.

ITALY: Bio-on S.p.A. has made an advancement in the technology able to produce bioplastics from glycerine, Biodiesel Magazine reported in June. The high-performing PHA plastics are made from a combination of crude glycerine, sugar beets, sugarcane and potatoes and have been certified by Vincotte in Europe and the USDA in the USA.

WORLD: New research from MarketsandMarkets has projected that the oleochemicals market will reach US$25.91bn by 2019, equaling a compound annual growth rate (CAGR) of 4.2% from 2014 to 2019. Asia-Pacific dominated the oleochemicals market in 2013 and is projected to remain the major market, growing at a CAGR of 5.1% between 2014 and 2019.

USA: Renewable energy company Methes Energies announced in May that it will begin offering epoxidised soyabean oil (ESO) and natural polyol from its Sombra, Ontaria facility, with an expectation that production and sales will begin by the third quarter of this year.

IN BRIEF Coca-Cola launches 100% sugarcane-based PE T bottle

The Coca-Cola Company unveiledthe world’s first PET plastic

bottle made entirely from plant materials at the World Expo in Milan on 3 June.

Coca-Cola said its PlantBottle packaging built on its vision to develop a more responsible plant-based alternative to packaging traditionally made from fossil fuels and other non-renewable materials.

PlantBottle packaging used patented technology that converted natural sugars found in plants into the ingredients for making PET plastic bottles. “The packaging looks, functions and recycles like traditional PET but has a lighter footprint on the planet and its

scarce resources.”Coca-Cola said its 100% plant-

based packaging was made from sugarcane and the waste from the sugarcane manufacturing process – materials which met the company’s sustainability criteria.

“Since its 2009 launch, Coca-Cola has distributed more than 35bn bottles in nearly 40 countries using its current version of PlantBottle packaging which is made from up to 30% plant-based materials,” the company said. “It is estimated the use of PlantBottle packaging since the launch has helped save equivalent annual emissions of more than 315,000 tonnes of carbon dioxide.”

Avantium and Tereos announce bioplastic partnership

Bio-based leather breakthrough

Glycerine use forecast to fallThere will be a slowdown in glycerine use in China this year but

an increase in 2016 to over 1M tonnes, according to HBI’s FredWang at the third Global Glycerine Conference on 26-27 May 2015 in France.

The conference concluded that there is unlikely to be much discretionary blending of biodiesel in 2015 and 2016 and this, together with increased production globally of hydro-treated vegetable oil (HVO) biodiesel and the use of more double-counted raw materials in Europe, will see glycerine generation decline to below 18M tonnes by the end of 2016.

Increased demand and declining production is likely to result in a tighter glycerine market by the end of next year.

Investing in sustainable LEGO

TerraVerdae’sbiodegradable microspheres

12 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

RENEWABLE MATERIALS NEWS

An innovative artificial leatherfabric using bio-based

materials supplied by BioAmber and DuPont Tate & Lyle has been developed by the Flokser Group, according to a press release in June. The fabric makes use of a polyester polyol made from BioAmber’s Bio-SA bio-based succinic acid and DuPont Tate & Lyle Bio Products’ Susterrea bio-based 1,3-propanediol.

The artificial leather had 70% renewable content and was softer and more durable than petroleum-based leather alternatives, Flokser said.

Sugar producer Tereos is to partner with catalyticresearch company Avantium to produce

bioplastics made from 2,5 furandicarboxylic acid (FDCA), Bioplastics News reported on 16 June. A formal announcement has not yet been made but is expected to be released soon.

According to Bioplastics News, Avantium has

developed a proprietary two-step chemical, catalytic process to produce FDCA from sugars called the ‘YXY’ process. The FDCA will be combined with bio-based MEG to produce PEF, an alternative to PET with enhanced oxygen barrier properties.

The PEF will be produced at Tereos’ site in Lillebonne, France.

Sustainable materials biotechnology company

TerraVerdae BioWorks announced in June that it has released a line of biodegradable, natural microspheres to directly replace non-degradable plastic microbeads.

The traditional plastics used in abrasive cosmetic products are currently the subject of restrictive legislation worldwide due to their ability to pass through water filtration systems and build up in lakes and reservoirs, harming wildlife.

Companies such as Johnson & Johnson, Proctor & Gamble, Unilever, L’Oreal and Colgate-Palmolive have already pledged to end the use of polyethylene microbeads in their products.

The TerraVerdae microspheres were biodegradable, non-toxic and environmentally safe, the company said.

The LEGO group announced inJune that it plans to invest

DKK1bn (US$150M) to research and implement new sustainable materials to manufacture LEGO toys as well as packaging.

The group will establish a Sustainable Materials Centre at its current headquarters in Billund, Denmark during 2015 and 2016, and said it

would employ an additional 100 specialists during the coming years.

In 2012, LEGO announced it would implement sustainable alternatives to its current raw materials by 2030 and, at

the company’s general assembly in May this

year, the decision was made to significantly boost the search.

Renewable News July.indd 1 13/07/2015 11:06

DIARY OF EVENTS

13 OFI – JULY/AUGUST 2015

OFI events13-14 April 2016OFI India 2016VENUE: Hyderabad International Convention Centre,India

www.ofievents.com/india

For sales and sponsorship, contact:

Mark Winthrop-Wallace, Sales ManagerTel: +44 1737 855114; E-mail: [email protected]

Anita Revis, Sales ConsultantTel: +44 1737 855068; E-mail: [email protected]

Erik Heath, Chinese Sales ExecutiveTel: +44 1737 855108; E-mail: [email protected]

oils+fats 2015 acts as bridge between research and industryBuilding bridges between R&D and industrial applications is a central

aim of oils+fats 2015, the International Trade Fair for Business, Technology and Innovations being held on 15-17 September at the MOC Veranstaltungscenter in Munich.

A key component in this initiative is the innovations platform in the exhibition hall where experts will discuss the markets and technologies of the future.

In the opening lecture at the innovations platform, Thomas Mielke, ISTA Mielke GmbH, Oil World, Hamburg, will be casting a glance at the factors at play in oil processing worldwide.

“Falling growth rates in worldwide palm oil production have led to an increased demand for soya oil, rapeseed oil and sunflower oil and therefore to a rise in the quantity of oilseeds processed,” explains the expert. In his lecture, Mielke will also set out how global demand for vegetable oil in the food and biodiesel industries will be trending in future and what can be expected in the protein market.

Around 50 exhibitors and approximately 1,000 participants from around the world are expected to attend oils+fats 2015.

Among the trade visitors are producers of crude and refined oils and fats, fatty acids, margarine, nutraceuticals, edible oils and fats, as well as producers of feedstuffs, biofuels, detergents, glycerine, lanolin, lubricants and waxes.

Exhibitors will be presenting the latest solutions in the production and processing of oils and fats including process and quality control, raw and auxiliary materials, logistics, filling and packaging technology, and – for the first time – deep frying.

In addition, the 8th International Symposium on Deep Frying will be held, for the first time, as part of oils+fats 2015. The symposium is organised by Euro Fed Lipid. It will look at aspects of deep frying, with the aim of optimising and enhancing understanding of the deep frying process, and thereby strengthening the market for deep-fried products in future.

Also running in parallel with oils+fats 2015 is the 15th Practical Short Course on Advanced Oilseed and Oil Processing and Food Applications aimed at young professionals and newcomers.

For further information on oils+fats 2015, contact: Messe München GmbH, oils+fats Press Office, Johannes Manger and Isabella Lauf Tel: +49 89 94921482/94921487E-mail: [email protected] [email protected]

Come and visit the OFI stand at oils+fats 2015

Clean and efficient vacuum systems

ICE Ice condensation

ACL Alkaline Closed Loop

Körting Hannover AG30453 Hannover/Germany Tel.: +49 511 2129-253 [email protected]

www.koerting.de

Ice condensationIce condensationIce condensation

Hall 3 Stand 305

Clean and Efficient-102x297(105x303 bleed size)-oils and fats-150714.indd 1 14.07.2015 14:05:36

July/Aug diary.indd 1 20/07/2015 13:52

DIARY OF EVENTS

14 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

For a full listing of oils and fats industry events, go to: www.ofimagazine.com

20-21 AUGUST 2015Palmex Thailand 2015 ExhibitionVENUE: Surat Thani, ThailandCONTACT: Fireworks Media (Thailand) Co LtdTel: +66 2513 1418E-mail: [email protected]: www.thaipalmoil.com

14-15 OCTOBER 20159th Global Oils and Fats Forum 2015VENUE: Los Angeles, USACONTACT: Mohd Izham Hassan, Haznita Husin, Malaysian Palm Oil CouncilTel: +603 7806 4097; E-mail: [email protected] or [email protected]: www.mpoc.org.my

6-11 SEPTEMBER 2015FOSFA - Basic Introductory CourseVENUE: Royal Holloway, Egham, Surrey, UKCONTACT: Anna Baran, FOFSA, UKTel: +44 20 7283 5511E-mail: [email protected] Website: www.fosfa.org

2-4 SEPTEMBER 20152nd High Oleic Oils CongressVENUE: Paris, FranceCONTACT: FAT & Associés, FranceTel: +33 567 339 206; Fax: +33 567 339 203Website: www.higholeicmarket.com/hoc-2015

31 OCT – 4 NOVEMBER 2015World Congress on Oils + Fats and 31st ISF Lectureship Series VENUE: Rosario, ArgentinaCONTACT: Jeffry Newman, International Society for Fat Research SecretariatTel: +1 217 359 2344; Fax: +1 217 351 8091E-mail: [email protected]: www.isfnet.org

3-5 NOVEMBER 20157th Palmex Indonesia 2015VENUE: Santika Premiere Dyandra Hotel & Convention, Medan, IndonesiaCONTACT: PT Fireworks IndonesiaTel: +62 21 4290-0030E-mail: [email protected]: www.palmoilexpo.com

27-30 OCTOBER 2015SODEOPEC2015 – Soaps, Detergents, Oleochemicals and Personal CareVENUE: Miami, Florida, USACONTACT: Doreen Berning, AOCS, USATel: +1 217 693 4813E-mail: [email protected]: http://sodeopec.aocs.org/index.cfm

9 SEPTEMBER 20153rd International Conference – Black Sea Veg Oil Trade 2015VENUE: Hilton Hotel, Kiev, UkraineCONTACT: Julia Feofilova, UkrAgroConsult, Ukraine. Tel: +38 044 451 46 34E-mail: [email protected]: http://bso.blackseagrainconference.com/en

18-19 SEPTEMBER 2015Malaysia-Poland Palm Oil Trade Fair & Seminar (POTS) 2015VENUE: Warsaw, PolandCONTACT: Malaysian Palm Oil CouncilTel: +603 78064097; E-mail: [email protected] or [email protected]: www.mpoc.org.my

6-8 OCTOBER 2015PIPOC 2015VENUE: Kuala Lumpur, MalaysiaCONTACT: Malaysian Palm Oil BoardE-mail: [email protected] Website: www.mpob.gov.my

15-17 SEPTEMBER 2015oils+fats International Trade Fair for the Technology and Trade of Oils and FatsVENUE: Messe München, MOC Veranstaltungscenter München, GermanyCONTACT: Messe München GmbH, GermanyTel: +49 89 949 11 328E-mail: [email protected]: www.oils-and-fats.com/en

15-17 SEPTEMBER 2015Deep Fat Frying SymposiumVENUE: MOC, Munich, GermanyCONTACT: Euro Fed Lipid, GermanyTel: +49 69 7917 533; Fax: +49 69 79 17565E-mail: [email protected]: www.eurofedlipid.org/meetings/munich2015/index.php

15-16 DECEMBER 2015Malaysia-Egypt Palm Oil Trade Fair & Seminar (POTS) 2015VENUE: Cairo, EgyptCONTACT: Zainuddin Hassan, Nur Adibah, Malaysian Palm Oil CouncilTel: +603 7806 4097; Fax: +603 7806 2272E-mail: [email protected] or [email protected]: www.mpoc.org.my

3-5 DECEMBER 20157th biennial Journées Internationales d’Etude sur les Lipides (JIEL) conference VENUE: Marrakech, MoroccoCONTACT: Société Marocaine pour l’Etude des Lipides (SMEL). Tel: +212 0522 704 672Fax: +212 0522 704 675E-mail: [email protected]: (French): Société Francaise pour l’Etude des Lipides (SFEL). Tel: + 33 567 339206; E-mail: [email protected]

14-15 OCTOBER 2015International Sunflower Oil SymposiumVENUE: Shanghai, ChinaCONTACT: APK-Inform, UkraineTel: +380 562 320795E-mail: [email protected]: http://www.apk-inform.com/en/conferences/china/program

5 NOVEMBER 2015FOSFA Annual DinnerVENUE: Divani Apollon Palace and Thalasso, Athens, GreeceCONTACT: Gemma Hale, FOSFA, UK. Tel: +44 20 72835511; E-mail: [email protected] Website: www.fosfa.org

20-21 NOVEMBER 2015PORAM Annual Forum and DinnerVENUE: One World Hotel, Selangor, MalaysiaCONTACT: PORAM Secretariat, MalaysiaTel: +603 7492 0006E-mail: [email protected]: www.poram.org.my

19-23 OCTOBER 201582nd National Renderers Association (NRA) Annual ConventionVENUE: Ritz Carlton, Laguna Niguel, California, USACONTACT: Marty Covert, NRA Convention Coordinator, USA. Tel: +1 703.754.8740 E-mail: [email protected]: www.nationalrenderers.org/events/convention

30 SEPT – 2 OCTOBER 201510th Oilseed & Grain Trade SummitVENUE: Hyatt Regency, Minneapolis, USACONTACT: HighQuest Group, USATel: +1 810 6608683E-mail: [email protected]: www.oilseedandgrain.com

27-30 SEPTEMBER 201513th Euro Fed Lipid CongressVENUE: Florence, ItalyCONTACT: Euro Fed Lipid, GermanyTel: +49 69 79 17533E-mail: [email protected] Website: www.eurofedlipid.org/meetings/florence2015/index.php

22-24 SEPTEMBER 20158th Biofuels International ConferenceVENUE: Porto, PortugalCONTACT: Ishemin Juma, Biofuels International, UK. Tel: +44 20 3551 5751E-mail: [email protected]: www.biofuels-news.com/conference

July/Aug diary.indd 2 20/07/2015 13:52

‘Weather market’ stalls price dropDespite smaller rapeseed and flattening sunflowerseed production, oilseed raw material supply should remain adequate thanks to the highest ever global soyabean stock, and provided palm oil output doesn’t falter with El Niño. However, things could change quickly if rapeseed seriously underperforms crop forecasts. John Buckley writes

INTERNATIONAL MARKET REVIEW

16 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

Oilseed raw material markets have been stronger than expected in the second quarter of 2015, as soya futures responded to rain-delayed sowings in the US and traders began

to take more notice of declining prospects for global rapeseed and sunflower crops. El Niño might also be raising medium/longer-term dry weather risk for Asian palm oil output – usually the largest contributor to growth of global oil supply and subject to new demand pressures from origin countries’ biodiesel expansion plans. Analysts also continued to debate the impact of financial squeezes on the coming autumn’s Latin American soyabean plantings.

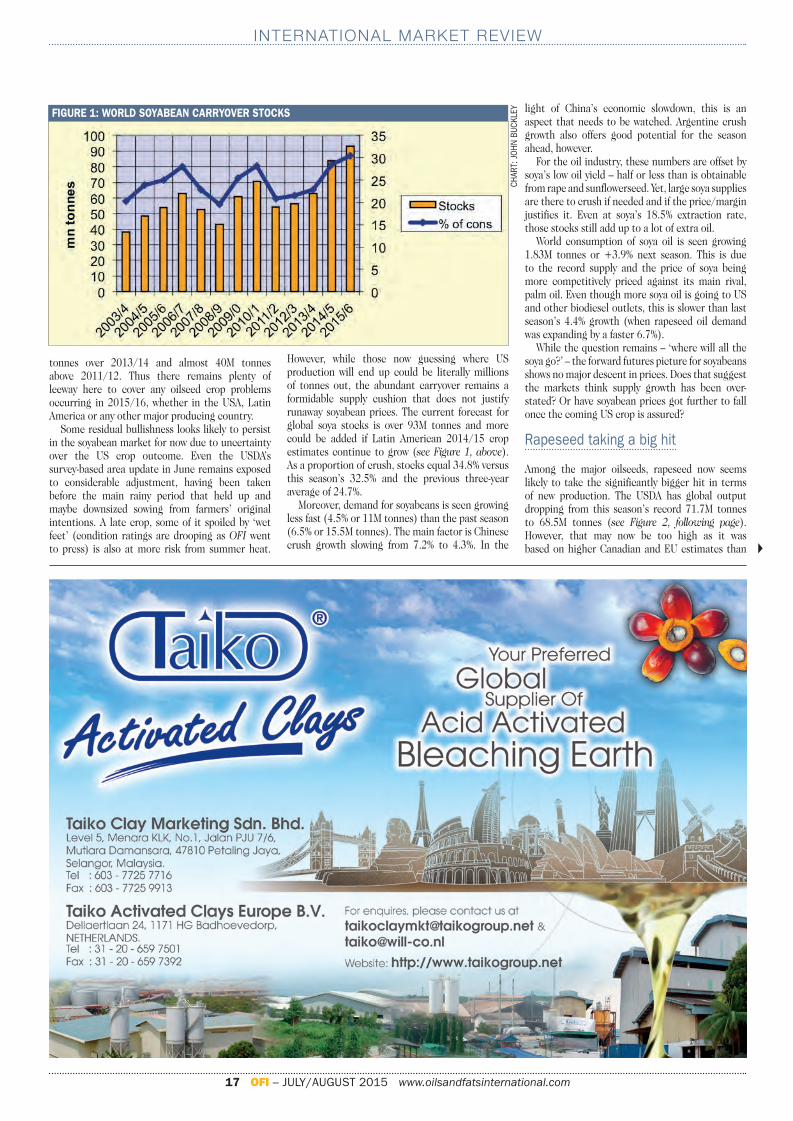

All that said, the global oilseed complex has done well to rally as far as it has (CBOT soyabean futures recently by as much as 12% off their May lows). For what still can’t be ignored is the backdrop of the largest-ever global soyabean stock – both in absolute terms and in relation to consumption needs.

Yet, due to soya’s relatively low extraction rate, the direction in which stocks of vegetable oils seem to be travelling looks far less bearish. The USDA, for example, recently forecast global stocks of the nine main oils declining in the coming season (starting in October) to a five-year low of 15.77M tonnes. That also assumes consumption will be rising by a below trend 3.5% (versus last season’s 4.3% and the previous year’s 5.7%).

Raw material supplies

Some important changes have been seen over the past two months in estimates of raw material supplies. For soyabeans, Latin American output estimates have continued to increase, as was expected. Combined Argentine, Brazilian and Paraguayan output is now up to at least 162.5M tonnes. Possibly as much as 3M more will be added if the highest local estimates prove correct.

The two leading Latin American producers also started the new season with record carryover stocks, expected to increase yet again in 2015/16 based on current new crop estimates. The USDA has Brazil’s next crop at 97M tonnes versus this season’s (already a record) 94.5M tonnes. Some local sources are either side of the new crop figure, due to uncertainty over how farmers will respond to farm credit and other economic squeezes. If Brazil does finish with the 28M tonnes or so of surplus soyabean stocks that the USDA forecasts, then that would be double the amount taken forward just four years earlier. Similarly, Argentina is seen starting next season with 33M tonnes and expanding that to around 34M tonnes in 2015/16 (versus a mere 16M tonnes in 2011/12).

The USA, meanwhile, expects to start the new season with about 9M tonnes of soyabean carryover against an unusually low 2.5M tonnes for 2015/16. The USDA has global soyabean ending stocks for 2015/16 about 3M tonnes lower than in May (largely due to historical upward revisions to Brazil’s crush). However, this total would still be 10M tonnes higher than in 2014/15, 30M

John Buckley July.indd 1 23/07/2015 11:15

CHAR

T: J

OHN

BUCK

LEY

INTERNATIONAL MARKET REVIEW

17 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

tonnes over 2013/14 and almost 40M tonnes above 2011/12. Thus there remains plenty of leeway here to cover any oilseed crop problems occurring in 2015/16, whether in the USA, Latin America or any other major producing country.

Some residual bullishness looks likely to persist in the soyabean market for now due to uncertainty over the US crop outcome. Even the USDA’s survey-based area update in June remains exposed to considerable adjustment, having been taken before the main rainy period that held up and maybe downsized sowing from farmers’ original intentions. A late crop, some of it spoiled by ‘wet feet’ (condition ratings are drooping as OFI went to press) is also at more risk from summer heat.

However, while those now guessing where US production will end up could be literally millions of tonnes out, the abundant carryover remains a formidable supply cushion that does not justify runaway soyabean prices. The current forecast for global soya stocks is over 93M tonnes and more could be added if Latin American 2014/15 crop estimates continue to grow (see Figure 1, above). As a proportion of crush, stocks equal 34.8% versus this season’s 32.5% and the previous three-year average of 24.7%.

Moreover, demand for soyabeans is seen growing less fast (4.5% or 11M tonnes) than the past season (6.5% or 15.5M tonnes). The main factor is Chinese crush growth slowing from 7.2% to 4.3%. In the

light of China’s economic slowdown, this is an aspect that needs to be watched. Argentine crush growth also offers good potential for the season ahead, however.

For the oil industry, these numbers are offset by soya’s low oil yield – half or less than is obtainable from rape and sunflowerseed. Yet, large soya supplies are there to crush if needed and if the price/margin justifies it. Even at soya’s 18.5% extraction rate, those stocks still add up to a lot of extra oil.

World consumption of soya oil is seen growing 1.83M tonnes or +3.9% next season. This is due to the record supply and the price of soya being more competitively priced against its main rival, palm oil. Even though more soya oil is going to US and other biodiesel outlets, this is slower than last season’s 4.4% growth (when rapeseed oil demand was expanding by a faster 6.7%).

While the question remains – ‘where will all the soya go?’ – the forward futures picture for soyabeans shows no major descent in prices. Does that suggest the markets think supply growth has been over-stated? Or have soyabean prices got further to fall once the coming US crop is assured?

Rapeseed taking a big hit

Among the major oilseeds, rapeseed now seems likely to take the significantly bigger hit in terms of new production. The USDA has global output dropping from this season’s record 71.7M tonnes to 68.5M tonnes (see Figure 2, following page). However, that may now be too high as it was based on higher Canadian and EU estimates than v

FIGURE 1: WORLD SOYABEAN CARRYOVER STOCKS

John Buckley July.indd 2 23/07/2015 11:15

INTERNATIONAL MARKET REVIEW

18 OFI – JULY/AUGUST 2015 www.oilsandfatsinternational.com

those that are now circulating. Over the past two months, unusually dry weather held up and reduced Canadian sown area. This was followed by a cold spell delaying development. The warmth that was needed to speed things up might now veer towards becoming excessive, further damaging late crops’ yield potential.

The Canadian Wheat Board recognised the deterioration at the end of June when it issued a crop range of 12.6M to 13M tonnes, versus the USDA’s 14.8M tonnes and last year’s 15.56M tonnes. As drought drags on in some major areas, some private analysts have been suggesting the crop will be lucky to make 10M tonnes – but that seems a bit too pessimistic at this stage.

To keep crush stable around 7.2M tonnes and assuming exports are within 500,000 tonnes of the past season’s 8.8M tonnes, Canada will have to cut carryover stocks to the bone. The USDA says stock will need to be cut from 2.1M to 1.6M tonnes but, on their demand assumptions, the lower crop estimates above would actually imply a considerable negative carryout.

Within the EU, all the talk has been about lower yields after dry weather accompanied by heatwaves in some regions. This has especially affected leading producers France and Germany. The total crop is probably at least 500,000 tonnes under the USDA estimate of 22.1M tonnes. Europe is also expected to draw stocks down by at least 800,000 tonnes to maintain crush anywhere near a 25M tonne level but, at this stage, projections for carryout at 1.6M tonnes look optimistic. This also assumes that the EU can find imports close to last year’s 2.5M tonnes in a year of tighter global supplies.

In the CIS region, as expected, the tighter fiscal climate seems to be taking a toll on planted area (Ukraine) and yields (Russia and Ukraine), implying a drop of 10-15% in output and a corresponding fall in exports from these major suppliers to the EU.

Local estimates have also marked down output in another key supplier, Australia, possibly as low as 3M tonnes (3.4M tonnes last year).

Globally, rapeseed stocks will hit their lowest level for some years. Prices have already responded by racing to 14-month highs on the Paris and 21-month highs on the Winnipeg futures markets. The rise may not quite be mirrored on the Canadian physical markets. However, amid a slower advance in product value, it has been enough to collapse margins and take crush down to unusually low levels recently. Although this is currently well under-utilising Canada’s crush capacity, it is unlikely to make a huge difference to the country’s tight carryover stocks if product value eventually rises accordingly.

The tighter European supply is already reflected in advancing prices for rapeseed oil, which is also being boosted by the chronically weak Euro. Since the last review, the cost of bulk crude rapeseed oil has moved from a modest 4% discount to a near 9% premium over soya oil. It will be interesting to see to what extent this move – which is surely not over yet – tests consumer loyalty to an oil that has enjoyed a value boost in recent years from successful ‘healthy eating’ promotions. EU food consumption of rapeseed oil is, in fact, still forecast by the USDA to grow 4.6% in 2015/16 after an 11% jump in 2014/15, whereas industrial use is seen flattening out (down about 3%) with pausing expansion in the biodiesel sector.

Extension of sunflower oil premium

Sunflower oil’s premium over the other soft oils and palm has also been extended lately on what appears to be a deteriorating supply outlook. On the European market, RBD sunflower has recently been quoted almost 22% over soya and 17.5% over rapeseed oil. World production of sunflowerseed is

currently expected to be not far off last year’s 40M tonnes but still about 3M tonnes under the 2013/14 record. High production in 2013/14 left larger stocks that helped supplement the next season’s smaller crop. Main supply elements for 2015/16 include the EU’s crop, seen down from about 9M tonnes to 8.5/8.2M tonnes on slightly smaller area and lower yields than last year.

Ukraine’s crop is forecast slightly below last year’s 10.2M tonnes (versus 2013’s 11.6M tonnes). This is due mainly to falling yield, which some analysts say may take it lower still. Russia’s crop, on the other hand could improve from last year’s 8.9M tonnes to 9.4M tonnes on bigger area and yield. Overall, Russia and Ukraine could export almost as much as 2014/15 but price premiums over soya and palm may have to increase further to ration supplies among customers who consumed more sunflower oil last season (some Asian countries as well as Europe and the CIS countries themselves) Overall, world sunflower oil use is seen by the USDA as rising from 14.8M tonnes to 15M tonnes, a narrow new record (see Figure 3, left). However, crushing that much seed would, on present crop pointers, mean cutting sunflower stocks by 27% to a very low 1.9M tonnes.

Taxes cause problems for palm oil

Palm oil markets have been erratic over the past couple of months. Traders have tried to divine the impact of origin biodiesel expansion programmes, Indonesia’s new export taxes, the extent of the seasonal uptrend in Asian production and still rising competition from unusually cheap soya oil.

Malaysian May exports showed an impressive 37% jump when China, Europe and India came back to buy in a big way as prices fell to new lows. However, preliminary June export figures suggested a drop to between 2% and 9% growth and the early July estimates little or no gain. Importers turned to Indonesia to beat the latter’s punitive new export taxes (US$50/tonne on crude, US$30/tonne on processed palm oil).

Markets also wondered if Indonesia was getting cold feet as it twice postponed the levies’ introduction into mid-July. Traders also questioned again whether the new Indonesian biofuel programme really could consume 4M tonnes of palm oil as some reports suggested. Of the current year’s output of 32.5M tonnes, about 10M tonnes is used domestically and about half of that in biofuel. Some leading auto-industry firms have also criticised plans to raise blending to as much as 15%, claiming many vehicles’ engines cannot cope with that.