office of debt management - u.s. department of the … of debt management ... d. treasury net...

TRANSCRIPT

Office of Debt ManagementOffice of Debt Management

Fiscal Year 2012 Q1 ReportFiscal Year 2012 Q1 Report

Table of ContentsTable of ContentsI. Fiscal

A. Quarterly Tax Receipts p. 4B. Receipt Base Levels p. 5C. Ten Largest Outlays p. 6D. Treasury Net Non-marketable Borrowing p. 8E. Cumulative Budget Deficits by Fiscal Year p. 9F. Deficit and Borrowing Estimates p. 10G. Budget Surplus/Deficit with OMB Forecast p. 11

II. Portfolio MetricsA. Historical and Projected Net Marketable Borrowing p. 13B. Weighted Average Maturity of Marketable Debt p. 15C. Recent and Future Portfolio Composition by Issuance Type p. 16D. Recent and Future Maturity Profile p. 18

III DemandIII. DemandA. Bid-to-Cover Ratios p. 23B. Investor Class Auction Awards p. 27C. Foreign Awards at Auction p. 34D. Primary Dealer Awards at Auction p. 38

2

Section I:Fiscal

3

Quarterly Tax Receipts

100%

150%

50%

100%

% C

hang

e

0%

Year

ove

r Yea

r %

-50%

-100%

Dec

-01

Mar

-02

Jun-

02Se

p-02

Dec

-02

Mar

-03

Jun-

03Se

p-03

Dec

-03

Mar

-04

Jun-

04Se

p-04

Dec

-04

Mar

-05

Jun-

05Se

p-05

Dec

-05

Mar

-06

Jun-

06Se

p-06

Dec

-06

Mar

-07

Jun-

07Se

p-07

Dec

-07

Mar

-08

Jun-

08Se

p-08

Dec

-08

Mar

-09

Jun-

09Se

p-09

Dec

-09

Mar

-10

Jun-

10Se

p-10

Dec

-10

Mar

-11

Jun-

11Se

p-11

Dec

-11

4

Corporate Taxes Non-Withheld Taxes (incl SECA) Withheld Taxes (incl FICA)

Receipt Base Levels(12-Month Moving Average)

100

120

80

40

60 $ bn

20

40

-

Dec

-01

Mar

-02

Jun-

02Se

p-02

Dec

-02

Mar

-03

Jun-

03Se

p-03

Dec

-03

Mar

-04

Jun-

04Se

p-04

Dec

-04

Mar

-05

Jun-

05Se

p-05

Dec

-05

Mar

-06

Jun-

06Se

p-06

Dec

-06

Mar

-07

Jun-

07Se

p-07

Dec

-07

Mar

-08

Jun-

08Se

p-08

Dec

-08

Mar

-09

Jun-

09Se

p-09

Dec

-09

Mar

-10

Jun-

10Se

p-10

Dec

-10

Mar

-11

Jun-

11Se

p-11

Dec

-11

5Individual Income Taxes include withheld and non-withheld. Social Insurance Taxes include FICA, SECA, RRTA, UTF Deposits, FUTA and RUIA. Other includes excise taxes, estate and gift taxes, customs duties and miscellaneous receipts.

Individual Income Taxes Corporation Income Taxes Social Insurance Taxes Other

Ten Largest Outlays for FY 2011

900

1000

600

700

800

300

400

500$ bn

0

100

200

0

Hea

lth a

ndH

uman

Ser

vice

s

Soci

al S

ecur

ityA

dmin

istr

atio

n

efen

se-M

ilita

ry

Trea

sury

Agr

icul

ture

Labo

r

eter

ans A

ffair

s

Tran

spor

tatio

n

ce o

f Per

sonn

elM

anag

emen

t

Educ

atio

n

6

H S A De V T

Offi

c M

Q1 Levels of Ten Largest Outlays

200

250

150

n

100

$ bn

0

50

0

Hea

lth a

ndum

an S

ervi

ces

Soci

al S

ecur

ityA

dmin

istr

atio

n

efen

se-M

ilita

ry

Trea

sury

Agr

icul

ture

Labo

r

eter

ans A

ffair

s

Tran

spor

tatio

n

ce o

f Per

sonn

elM

anag

emen

t

Educ

atio

n

7

Hu S A D

e Ve T

Offi

c M

Q1 FY 2011 Q1 FY 2012

Treasury Net Non-Marketable Borrowing

20

30

10

-10

0$ bn

-20

-30

Q2-

02Q

3-02

Q4-

02Q

1-03

Q2-

03Q

3-03

Q4-

03Q

1-04

Q2-

04Q

3-04

Q4-

04Q

1-05

Q2-

05Q

3-05

Q4-

05Q

1-06

Q2-

06Q

3-06

Q4-

06Q

1-07

Q2-

07Q

3-07

Q4-

07Q

1-08

Q2-

08Q

3-08

Q4-

08Q

1-09

Q2-

09Q

3-09

Q4-

09Q

1-10

Q2-

10Q

3-10

Q4-

10Q

1-11

Q2-

11Q

3-11

Q4-

11Q

1-12

8

Fiscal Quarter

Foreign Series State and Local Govt. Series (SLGS) Savings Bonds

1,400Cumulative Budget Deficits by Fiscal Year

1,200

800

1,000

600

$ bn

200

400

0

Oct

ober

ovem

ber

ecem

ber

Janu

ary

Febr

uary

Mar

ch

Apr

il

May

June

July

Aug

ust

ptem

ber

9

No De F

Sep

FY2010 FY2011 FY2012

FY 2012-2014 Deficit and Borrowing Estimates In $ Billion

Primary Dealers* CBO** OMB***

Estimates as of: Jan-12 Aug-11 Sep-11

FY 2012 Deficit Estimate 1,127 973 1,334

FY 2013 Deficit Estimate 899 623 883

FY 2014 Deficit Estimate 737 380 476

FY 2012 Deficit Range 1,000-1,275

FY 2013 Deficit Range 580-1,120

FY 2014 Deficit Range 85-1,037

FY 2012 Marketable Borrowing Range 1,025-1,275

FY 2013 Marketable Borrowing Range 635-1,120

10

*Based on primary dealer feedback on January 23, 2012. Deficit estimates are averages. **Current law, prior to any Joint Committee actions or sequester.***Deficit projections from September 2011 – “Living Within Our Means and Investing in the Future”.

Budget Surplus/Deficit with OMB Forecast from September 2011 – “Living Within Our Means and Investing in the Future”

2%

4%

0

500

g g

‐2%

0%

-500

0

‐6%

‐4%-1,000

‐10%

‐8%

-2,000

-1,500

‐12%-2,500

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Fiscal Year

11Projection

Fiscal Year

OMB Surplus/Deficit in $ bn-(L) OMB Surplus/Deficit as a % of GDP-(R)

Section II:Portfolio Metrics

12

Historical and Projected Net Marketable Borrowing Assuming All Issuance Remains Constant

1,7871,483

1,1041,500

2,000

787

1,064965 898

7481,000

684

466525

352251

169

500

$ bn

0

(500)

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

End of Fiscal Year

TIPS 7/10/30 2/3/5 Bill OMB D fi it P j ti

13

Portfolio & SOMA holdings as of 12/30/2011. Assumes current issuance sizes for Bills, Nominal Coupons and TIPS; along with SOMA reinvestment. The principal on the TIPS securities were accreted to each projection date based on market ZCIS levels. No attempt was made to match future financing needs. OMB deficit projections are from Table S-1 of September 2011, “Living Within Our Means and Investing in the Future”. Data labels represent net borrowing numbers in billions.

TIPS 7/10/30 2/3/5 Bills OMB Deficit Projections

Historical and Projected Net Marketable Borrowing Assuming All Issuance Remains Constant $ BillionIssuance Remains Constant, $ Billion

End of Fiscal Y Bills 2/3/5 7/10/30 TIPS Net Borrowing OMB Deficit

P j tiYear s /3/5 / 0/30 S Net o o g Projections

2008 532 106 109 40 787 -

2009 503 732 514 38 1,787 -

2010 (204) 869 783 35 1,483 -

2011 (311) 576 751 88 1,104 -

2012 65 131 790 77 1,064 1,334

2013 0 134 737 93 965 833

2014 0 85 744 70 898 476

2015 0 (28) 708 69 748 525

2016 0 94 534 56 684 589

2017 0 54 354 58 466 506

2018 0 69 393 63 525 482

2019 0 40 256 57 352 511

2020 0 (2) 227 26 251 549

2021 0 (30) 197 2 169 565

14

Portfolio & SOMA holdings as of 12/30/2011. Assumes current issuance sizes for Bills, Nominal Coupons and TIPS; along with SOMA reinvestment. The principal on the TIPS securities were accreted to each projection date based on market ZCIS levels. No attempt was made to match future financing needs. OMB deficit projections are from Table S-1 of September 2011, “Living Within Our Means and Investing in the Future”. Data labels represent net borrowing numbers in billions.

Weighted Average Maturity of Marketable Debt

75

80

85hs

)

65

70

e M

atur

ity (M

onth

50

55

60

Wei

ghte

d A

vera

ge

40

45

50W

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

Calendar Year

Historical Adjust Nominal Coupons to Match Financing Needs

15

Portfolio & SOMA holdings as of 12/30/2011. To match OMB’s projected financing needs for the next 10 years, nominal coupon securities (2-, 3-, 5-, 7-, 10-, and 30-year) were adjusted by the same percentage. OMB deficit projections are from Table S-1 of September 2011, “Living Within Our Means and Investing in the Future”. The principal on the TIPS securities were accreted to each projection date based on market ZCIS levels. This scenario does NOT represent any particular course of action that Treasury is expected to follow. Instead, it is intended to demonstrate the basic trajectory of average maturity absent changes to the mix of securities issued by Treasury.

j p g

Recent and Future Portfolio Composition by Issuance Type, Percent

80%

90%

100%

y

60%

70%

80%

folio

30%

40%

50%

% o

f Por

tf

10%

20%

0%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

End of Fiscal Year

Bills Nominal Coupons TIPS (principal accreted to projection date)

16

p (p p p j )

Portfolio & SOMA holdings as of 12/30/2011. To match OMB’s projected financing needs for the next 10 years, nominal coupon securities (2-, 3-, 5-, 7-, 10-, and 30-year) were adjusted by the same percentage. OMB deficit projections are from Table S-1 of September 2011, “Living Within Our Means and Investing in the Future”. The principal on the TIPS securities were accreted to each projection date based on market ZCIS levels. This scenario does NOT represent any particular course of action that Treasury is expected to follow. Instead, it is intended to demonstrate the basic trajectory of average maturity absent changes to the mix of securities issued by Treasury.

Recent and Future Portfolio Composition by Issuance Type, Percent

End of Fiscal Year Bills Nominal Coupons

TIPS (principal accreted to

projection date)2006 21 3% 69 5% 9 2%2006 21.3% 69.5% 9.2%2007 21.6% 68.1% 10.3%2008 28.5% 61.4% 10.0%2009 28.5% 63.6% 7.9%2010 21 1% 71 9% 7 0%2010 21.1% 71.9% 7.0%2011 15.4% 77.3% 7.3%2012 14.1% 78.7% 7.3%2013 13.1% 79.3% 7.7%2014 12 5% 79 4% 8 1%2014 12.5% 79.4% 8.1%2015 12.0% 79.5% 8.5%2016 11.4% 79.8% 8.8%2017 11.0% 79.9% 9.1%2018 10 6% 80 0% 9 4%2018 10.6% 80.0% 9.4%2019 10.2% 80.1% 9.7%2020 9.8% 80.4% 9.8%

2021 9.5% 80.9% 9.7%

17

Portfolio & SOMA holdings as of 12/30/2011. To match OMB’s projected financing needs for the next 10 years, nominal coupon securities (2-, 3-, 5-, 7-, 10-, and 30-year) were adjusted by the same percentage. OMB deficit projections are from Table S-1 of September 2011, “Living Within Our Means and Investing in the Future”. The principal on the TIPS securities were accreted to each projection date based on market ZCIS levels. This scenario does NOT represent any particular course of action that Treasury is expected to follow. Instead, it is intended to demonstrate the basic trajectory of average maturity absent changes to the mix of securities issued by Treasury.

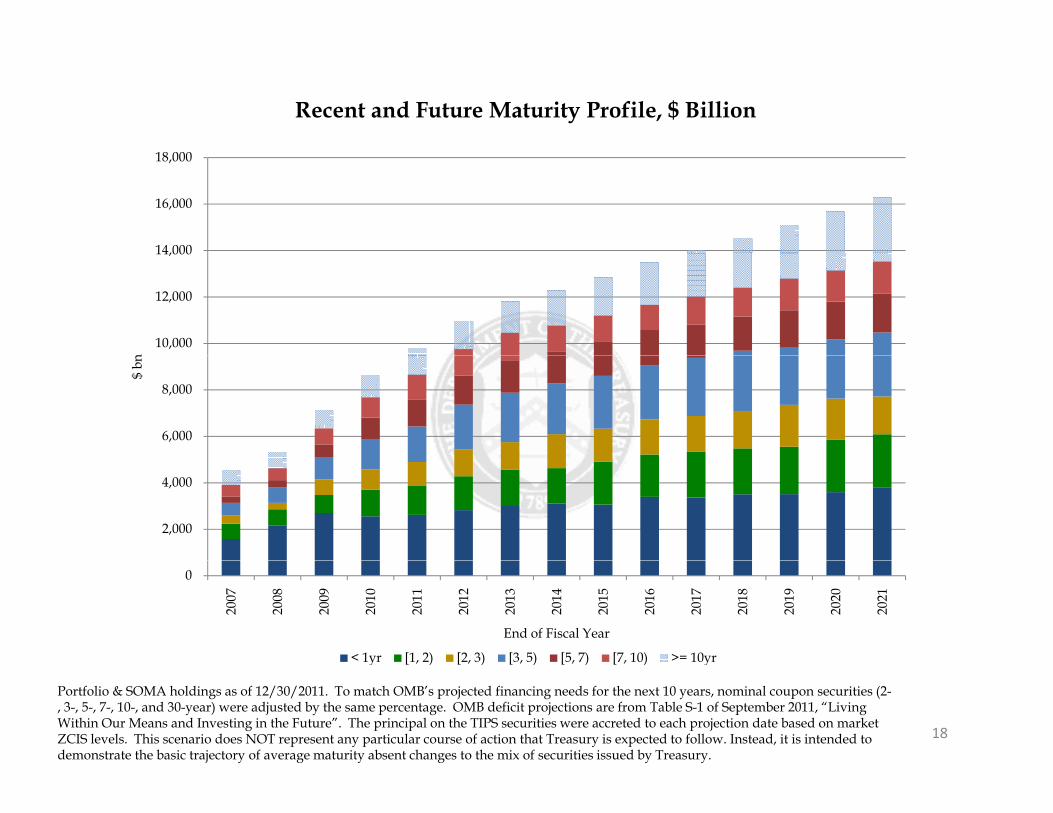

Recent and Future Maturity Profile, $ Billion

14,000

16,000

18,000

10,000

12,000

14,000

n

6,000

8,000

$ bn

2,000

4,000

0

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

End of Fiscal Year

< 1yr [1, 2) [2, 3) [3, 5) [5, 7) [7, 10) >= 10yr

18

y [ , ) [ , ) [ , ) [ , ) [ , ) y

Portfolio & SOMA holdings as of 12/30/2011. To match OMB’s projected financing needs for the next 10 years, nominal coupon securities (2-, 3-, 5-, 7-, 10-, and 30-year) were adjusted by the same percentage. OMB deficit projections are from Table S-1 of September 2011, “Living Within Our Means and Investing in the Future”. The principal on the TIPS securities were accreted to each projection date based on market ZCIS levels. This scenario does NOT represent any particular course of action that Treasury is expected to follow. Instead, it is intended to demonstrate the basic trajectory of average maturity absent changes to the mix of securities issued by Treasury.

Recent and Future Maturity Profile, $ Billion

End of Fiscal Year < 1yr [1, 2) [2, 3) [3, 5) [5, 7) [7, 10) >= 10yr

2007 1,582 664 342 551 276 499 627 2008 2,151 710 280 657 318 515 690 2009 2,702 775 666 970 540 691 779 2010 2,563 1,143 872 1,310 918 881 952 2011 2,621 1,273 1,004 1,527 1,146 1,086 1,129 0 , , , , , , ,2012 2,824 1,458 1,160 1,923 1,255 1,139 1,208 2013 3,002 1,570 1,182 2,123 1,400 1,181 1,359 2014 3,114 1,518 1,467 2,177 1,361 1,133 1,543 2015 3,063 1,843 1,426 2,273 1,489 1,098 1,674 2016 3 395 1 825 1 505 2 322 1 532 1 081 1 826 2016 3,395 1,825 1,505 2,322 1,532 1,081 1,826 2017 3,370 1,967 1,541 2,500 1,427 1,221 1,999 2018 3,512 1,971 1,609 2,594 1,474 1,252 2,131 2019 3,516 2,036 1,803 2,458 1,615 1,368 2,293 2020 3,602 2,265 1,760 2,546 1,631 1,344 2,530 2021 3,811 2,281 1,627 2,751 1,686 1,370 2,760

19

Portfolio & SOMA holdings as of 12/30/2011. To match OMB’s projected financing needs for the next 10 years, nominal coupon securities (2-, 3-, 5-, 7-, 10-, and 30-year) were adjusted by the same percentage. OMB deficit projections are from Table S-1 of September 2011, “Living Within Our Means and Investing in the Future”. The principal on the TIPS securities were accreted to each projection date based on market ZCIS levels. This scenario does NOT represent any particular course of action that Treasury is expected to follow. Instead, it is intended to demonstrate the basic trajectory of average maturity absent changes to the mix of securities issued by Treasury.

Recent and Future Maturity Profile, Percent

80%

90%

100%

60%

70%

30%

40%

50%

10%

20%

0%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

End of Fiscal Year

< 1yr [1, 2) [2, 3) [3, 5) [5, 7) [7, 10) >= 10yr

20

y [ , ) [ , ) [ , ) [ , ) [ , ) y

Portfolio & SOMA holdings as of 12/30/2011. To match OMB’s projected financing needs for the next 10 years, nominal coupon securities (2-, 3-, 5-, 7-, 10-, and 30-year) were adjusted by the same percentage. OMB deficit projections are from Table S-1 of September 2011, “Living Within Our Means and Investing in the Future”. The principal on the TIPS securities were accreted to each projection date based on market ZCIS levels. This scenario does NOT represent any particular course of action that Treasury is expected to follow. Instead, it is intended to demonstrate the basic trajectory of average maturity absent changes to the mix of securities issued by Treasury.

Recent and Future Maturity Profile, Percent

End of Fiscal Year < 1yr [1, 2) [2, 3) [3, 5) [5, 7) [7, 10) >= 10yr

2007 34.8% 14.6% 7.5% 12.1% 6.1% 11.0% 13.8%2008 40.4% 13.3% 5.3% 12.3% 6.0% 9.7% 13.0%2009 37.9% 10.9% 9.3% 13.6% 7.6% 9.7% 10.9%2010 29.7% 13.2% 10.1% 15.2% 10.6% 10.2% 11.0%2011 26 8% 13 0% 10 3% 15 6% 11 7% 11 1% 11 5%2011 26.8% 13.0% 10.3% 15.6% 11.7% 11.1% 11.5%2012 25.8% 13.3% 10.6% 17.5% 11.4% 10.4% 11.0%2013 25.4% 13.3% 10.0% 18.0% 11.8% 10.0% 11.5%2014 25.3% 12.3% 11.9% 17.7% 11.1% 9.2% 12.5%2015 23.8% 14.3% 11.1% 17.7% 11.6% 8.5% 13.0%2016 25.2% 13.5% 11.2% 17.2% 11.4% 8.0% 13.5%2017 24.0% 14.0% 11.0% 17.8% 10.2% 8.7% 14.3%2018 24.1% 13.6% 11.1% 17.8% 10.1% 8.6% 14.7%2019 23.3% 13.5% 12.0% 16.3% 10.7% 9.1% 15.2%2020 23 0% 14 4% 11 2% 16 2% 10 4% 8 6% 16 1%2020 23.0% 14.4% 11.2% 16.2% 10.4% 8.6% 16.1%2021 23.4% 14.0% 10.0% 16.9% 10.4% 8.4% 16.9%

21

Portfolio & SOMA holdings as of 12/30/2011. To match OMB’s projected financing needs for the next 10 years, nominal coupon securities (2-, 3-, 5-, 7-, 10-, and 30-year) were adjusted by the same percentage. OMB deficit projections are from Table S-1 of September 2011, “Living Within Our Means and Investing in the Future”. The principal on the TIPS securities were accreted to each projection date based on market ZCIS levels. This scenario does NOT represent any particular course of action that Treasury is expected to follow. Instead, it is intended to demonstrate the basic trajectory of average maturity absent changes to the mix of securities issued by Treasury.

Section III:Demand

22

Bid-to-Cover Ratios for Treasury Bills

5

5.5

6

4

4.5

5

Rat

io

3

3.5

4

Bid-

to-C

over

2

2.5

1.5

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

23

4-Week (13-week moving average) 13-Week (13-week moving average)

26-Week (13-week moving average) 52-Week (6-month moving average)

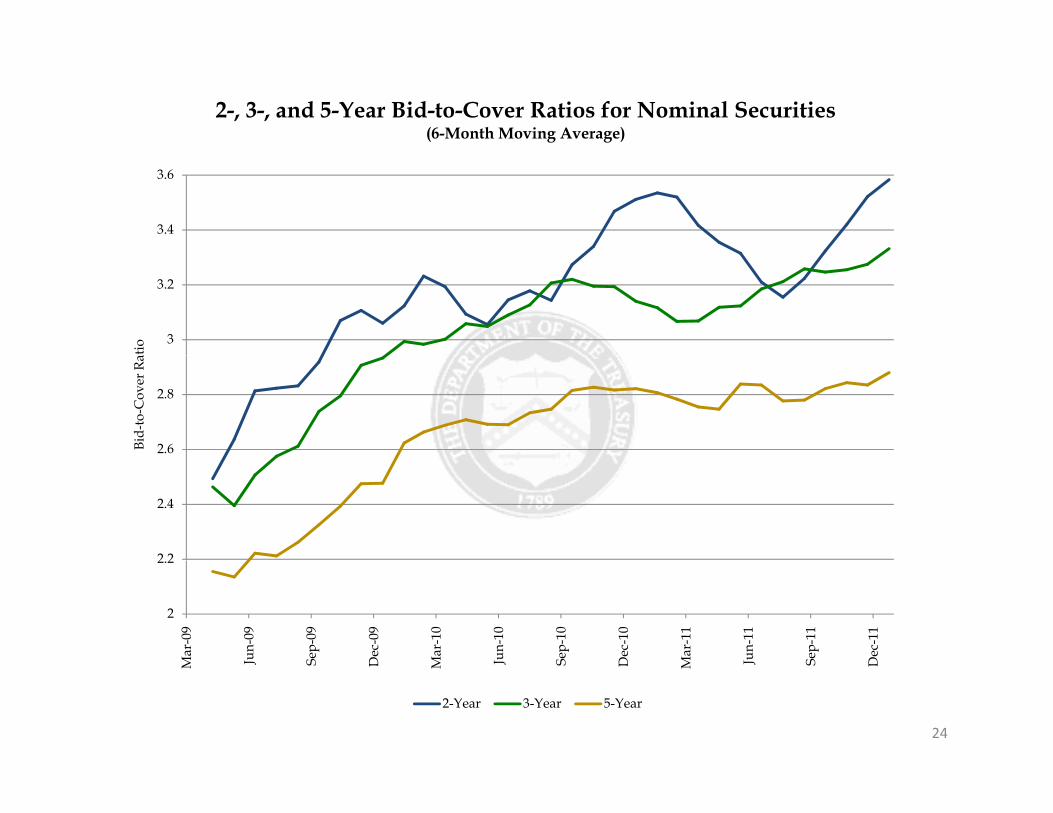

2-, 3-, and 5-Year Bid-to-Cover Ratios for Nominal Securities(6-Month Moving Average)

3.4

3.6

3

3.2

atio

2.6

2.8

Bid-

to-C

over

Ra

2 2

2.4

2

2.2

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

24

M J S D M J S D M J S D

2-Year 3-Year 5-Year

Bid-to-Cover Ratios for 7-, 10-, and 30-Year Nominal Securities(6-Month Moving Average)

3.2

3.4

3

atio

2.8

Bid-

to-C

over

R

2.4

2.6

2.2

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

25

J S D M J S D M J S D

7-Year 10-Year 30-Year

Bid-to-Cover Ratios for TIPS

3

3.5

2.5

3

Ratio

2Bid-

to-C

over

R

1.5

1

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

26

5-Year 10-Year (6-month moving average) 20-Year 30-Year

Investor Class Auction Awards: BillsCalendar Year 2011

Other4.1%

Foreign & International

11.0%

Investment Funds 15.8%

Primary Dealers59.1%

Other Dealers & Brokers Brokers

9.9%

27Excludes SOMA add-ons. “Other” includes categories that are each less than 2%, which include Depository Institutions, Individuals, Pension and Insurance.

Calendar Year Change in Bill Auction Awards by Investor Class

5%

10%

0%

Cha

nge

-10%

-5%

Cal

enda

r Yea

r

-15%

-20%

Prim

ary

Dea

lers

Oth

er D

eale

rs&

Bro

kers

Inve

stm

ent

Fund

s

Fore

ign

&

Inte

rnat

iona

l

28Excludes SOMA add-ons.

O I

2011 less 2010 2011 less 2009 2011 less 2008 2011 less 2007 2011 less 2006

Investor Class Auction Awards: Investor Class Auction Awards:

Other1.0%

Investor Class Auction Awards:2-, 3-, and 5-Year Nominal Securities

Calendar Year 2011Other0.7%

Investor Class Auction Awards:7-, 10-, and 30-Year Nominal Securities

Calendar Year 2011

Foreign & International

1.0%

Foreign & I t ti l International

22.6%

Primary Dealers45.5%

International 24.4%

Primary Dealers50.6%Investment

Funds 15.0%

Investment Funds

Other Dealers & Brokers

10.8%

Other Dealers &

Brokers 7.0%

Funds 22.3%

29Excludes SOMA add-ons. “Other” includes categories that are each less than 2%, which include Depository Institutions, Individuals, Pension and Insurance.

Calendar Year Change in 2-, 3-, 5-Year Nominal Securities Auction Awards by Investor Class

10%

15%

y

0%

5%

Cha

nge

-10%

-5%

Cal

enda

r Yea

r

-20%

-15%

20%

Prim

ary

Dea

lers

Oth

er D

eale

rs&

Bro

kers

Inve

stm

ent

Fund

s

Fore

ign

&

Inte

rnat

iona

l

30

2011 less 2010 2011 less 2009 2011 less 2008 2011 less 2007 2011 less 2006

Excludes SOMA add-ons.

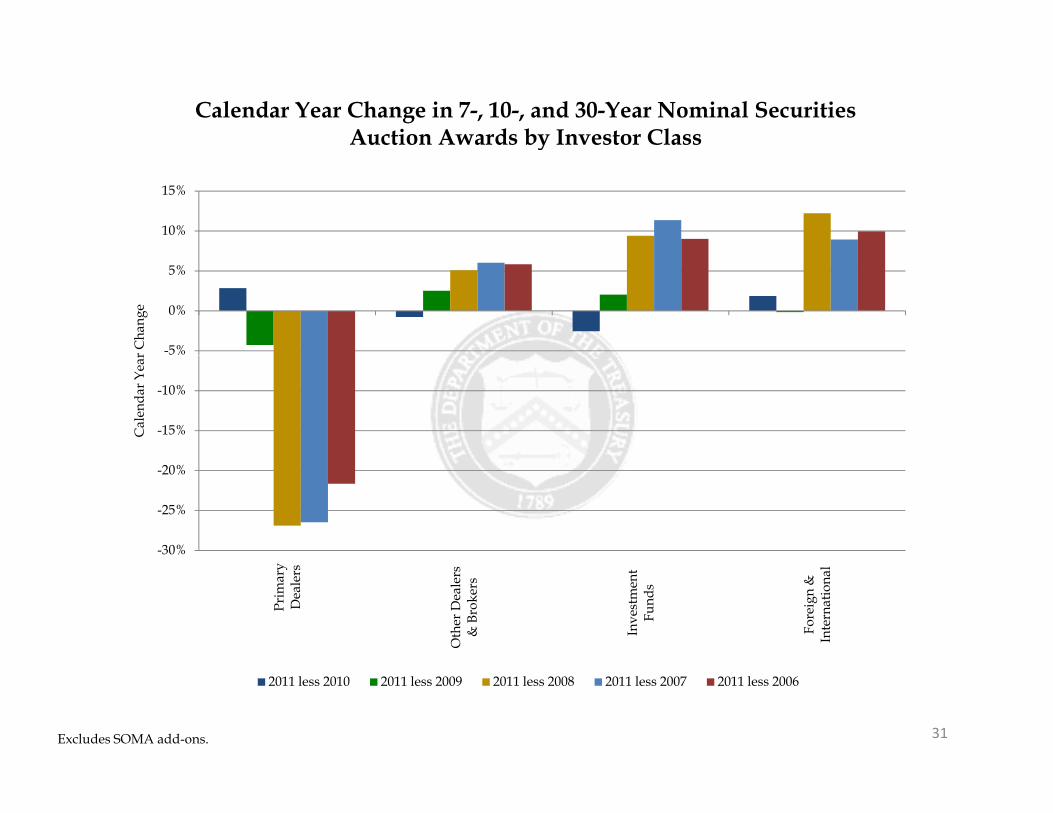

Calendar Year Change in 7-, 10-, and 30-Year Nominal Securities Auction Awards by Investor Class

10%

15%

y

-5%

0%

5%

r Cha

nge

-15%

-10%

Cal

enda

r Yea

r

-30%

-25%

-20%

Pr

imar

y D

eale

rs

Oth

er D

eale

rs&

Bro

kers

Inve

stm

ent

Fund

s

Fore

ign

&

Inte

rnat

iona

l

31

2011 less 2010 2011 less 2009 2011 less 2008 2011 less 2007 2011 less 2006

Excludes SOMA add-ons.

Investor Class Auction Awards: TIPSCalendar Year 2011

Foreign &

Other1.4%

Foreign & International

13.0%

Primary Dealers47.1%

Investment Funds 35.8%

32

Other Dealers & Brokers

2.7%

Excludes SOMA add-ons. “Other” includes categories that are each less than 2%, which include Depository Institutions, Individuals, Pension and Insurance.

Calendar Year Change in TIPS Auction Awards by Investor Class

10%

15%

5%

ar C

hang

e

-5%

0%

Cal

enda

r Yea

-10%

-15%

Prim

ary

Dea

lers

Oth

er D

eale

rs&

Bro

kers

Inve

stm

ent

Fund

s

Fore

ign

&

Inte

rnat

iona

l

33

O I

2011 less 2010 2011 less 2009 2011 less 2008 2011 less 2007 2011 less 2006

Excludes SOMA add-ons.

Foreign Awards of Treasuries at Auction, $ Billion

160

180

200

120

140

160

war

d ($

bn)

80

100

onth

ly P

riva

te A

w

40

60Mo

0

20

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

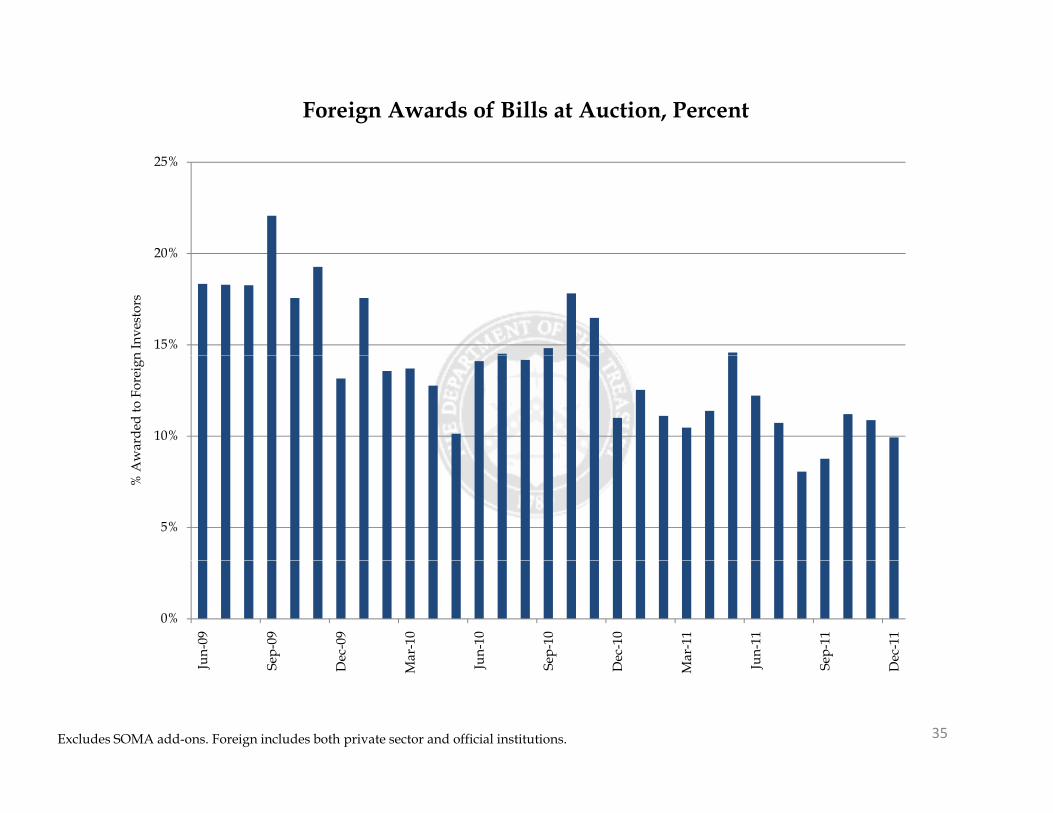

34Foreign includes both private sector and official institutions.

J S D M J S D M J S D

Bills 2/3/5 7/10/30 TIPS

Foreign Awards of Bills at Auction, Percent

20%

25%

15%

20%

n In

vest

ors

10%

war

ded

to F

orei

gn

5%

% A

w

0%

un-0

9

ep-0

9

Dec

-09

Mar

-10

un-1

0

ep-1

0

Dec

-10

Mar

-11

un-1

1

ep-1

1

Dec

-11

35Excludes SOMA add-ons. Foreign includes both private sector and official institutions.

Ju S D M Ju S D M Ju S D

Foreign Awards of Nominal Coupons at Auction, Percent

40%

45%

50%

30%

35%

40%

n In

vest

ors

20%

25%

war

ded

to F

orei

gn

10%

15%% A

w

0%

5%

un-0

9

ep-0

9

ec-0

9

ar-1

0

un-1

0

ep-1

0

ec-1

0

ar-1

1

un-1

1

ep-1

1

ec-1

1

36Excludes SOMA add-ons. Foreign includes both private sector and official institutions.

Ju Se De

Ma Ju Se De

Ma Ju Se De

2/3/5 7/10/30

Foreign Awards of TIPS at Auction, Percent

20%

25%

15%

20%

n In

vest

ors

10%

war

ded

to F

orei

gn

5%

% A

0%

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

37Excludes SOMA add-ons. Foreign includes both private sector and official institutions.

J S D M J S D M J S D

5-Year 10-Year 20-Year 30-Year

Primary Dealer Awards at Auction, Percent

65%

70%d

55%

60%

Am

ount

Aw

arde

45%

50%

Tota

l Com

petit

ive

35%

40%

% o

f T

30%

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

4/13/26-Week (13-week moving average) 52-Week (6-month moving average)

38

/ / ( g g ) ( g g )

2/3/5 (6-month moving average) 7/10/30 (6-month moving average)

TIPS (6-month moving average)

U S T R E A S U R Y F L O A T I N G R A T E N O T E S

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

February 2012

The demand backdrop 1

FRN issuance – motivation and estimated benefits 8

Choice of reference indices and sample structures 19

ES

1US

TR

EA

SU

RY

FL

OA

TI

NG

RA

TE

NO

T

The demand backdrop for US Treasuries – whether FRNs or fixed rate debt –

should benefit from a structural decline in the stock of high quality assets

Using market-based risk assessment provides

a useful view of the altered investment

environment

The stock of bonds issued by sovereigns

with 5Y CDS spreads below 100bp has

fallen sharply since 2007, excluding the

US (whose CDS spread is below 50bp)

In other words, US sovereign debt is now

Total debt outstanding for G-10 countries with 5Y CDSspreads less than 100bp, as of end-2007 and end-2011; USDbn

Total debt outstanding for G-10 countries with 5Y CDSspreads less than 100bp, as of end-2007 and end-2011; USDbn

8,000

10,000

12,000

14,000

16,000

18,000

20,000

United States

United Kingdom

Netherlands

Japan

Italy

Germanya higher fraction of the “higher quality”

sovereign debt universe, likely resulting

in a supportive demand backdrop for US

Treasuries

Note: Sweden and Switzerland were excluded due to lack of data. For end-2011, Canadadata is as of March 2011, and Japan data is as of September 2011. For Europeansovereigns, we assume that the amount of bills and non-domestic bonds outstanding isunchanged between 2007 and 2011.

-

2,000

4,000

6,000

8,000

End-2007 End-2011

Germany

France

Canada

Belgium

2TH

ED

EM

AN

DB

AC

KD

RO

P

Within the US fixed income markets, the share of Treasuries is growing while the

share of other high-quality assets is falling

Net issuance for various fixed income products by year ; $bnNet issuance for various fixed income products by year ; $bn

300

800

1300

1800

2300ABS Net of Fed Purchases

BABS

Agency MBS Net of Fed & TSYPurchases

AGY Net of Fed Purchases

Financial Corps (ex ABS)

3TH

ED

EM

AN

DB

AC

KD

RO

P

-1200

-700

-200

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

E

20

12

F

Financial Corps (ex ABS)

Non-Financial Corps

TSY Net of Fed Purchases/Sales

Net Fixed Income Supply ex Fed & TSYpurchases/sales

Will the Basel III LCR requirements trigger increased demand for US Treasuries

in general and FRNs in particular?

Market analysts estimated a Liquidity Coverage Ratio of 57% for 30 large bank holding

companies, resulting in a gross shortfall of about $500bn - $1Tn depending on mitigation

actions undertaken

While Treasury floaters would be attractive for LCR purposes, the net demand for FRNs

due to LCR provisions is likely to be modest

Treasury floaters are likely to yield less than liquid assets currently held by banks

(fixed rate Treasuries/Agencies/Agency MBS).

While Treasury floaters would be lower duration than current alternatives, many

banks are efficient duration hedgers and may be able to achieve higher returns net

of hedging cost using the current mix of assets

With the Fed currently paying banks 25bp on excess reserves, banks are likely

ignore Treasury floaters unless the yield at least matches IOER.

Also, certain regulatory capital implications of Basel III provisions related to AOCI could,

on the margin, incentivize banks to buy FRNs over fixed rate debt

However, this is one factor among several driving asset selection, and we expect the

net preference for FRNs over fixed rate debt to be rather modest

4TH

ED

EM

AN

DB

AC

KD

RO

P

Implementation of Dodd Frank’s central clearing provisions will also create some

modest net new demand for high quality collateral such as US Treasuries

Growth of value of total reported and estimated collateral,2000-2010; $bnGrowth of value of total reported and estimated collateral,2000-2010; $bn

About 82% of gross credit exposure appears

collateralized already—full implementation of Dodd-

Frank could cause demand for collateral to rise by

about $650bn

However, this does not directly translate into increased

demand for Treasuries—the ISDA margin survey also

indicates that Treasuries and Agencies make up only

about 6% of collateral, which is predominantly

composed of cash

Thus, the incremental demand for USTs due to

increased collateral requirements stemming from the

implementation of Dodd-Frank’s central clearing491707

854 922 924

1470

2649

21501984

437

719

10171209

1329 1335

2126

3957

31512934

1000

2000

3000

4000

Reported Estimated

implementation of Dodd-Frank’s central clearing

provisions could turn out to be modest.

Caveat – it is possible that the move to hold

collateral in custodial accounts rather than on a

bilateral basis could lower returns on cash and

alter the fraction of USTs in the mix. An increase

in this fraction could result in considerable

demand for USTs

In addition, the fraction of cash relative to overall

collateral could decline as short-term rates rise,

leading to higher fractions of other assets such

as USTs

Here again, any such incremental demand will

not discriminate between FRNs and fixed-rate

securities

Source: ISDA Margin Survey 2011

Value of collateral received and delivered by respondents,$mnValue of collateral received and delivered by respondents,$mn

Collateral

received Percent

Collateral

delivered Percent

Cash 877,552 81% 715,444 80%

Government securities 106,697 10% 154,821 17%

US 38,606 4% 48,409 5%

EU 22,943 2% 66,705 7%

UK 10,948 1% 13,414 1%

Japan 21,005 2% 17,438 2%

Other 13,196 1% 8,854 1%

Others 100,699 9% 29,143 3%

Total collateral 1,084,949 899,408

138 145289

491200 250

437

01999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

5TH

ED

EM

AN

DB

AC

KD

RO

P

Money market investors have been increasing Treasury holdings recently thanks

to a plunge in supply ex-Treasuries …

Money fund AUM is modestly lower over the past four years, but money

market supply has shrunk by 18%

MMMF’s are significant holders of Treasury and Agency securities

MMMF’s hold about $400bn in Treasury and Agency securities each

for combined $800bn, representing about 1/3 of AUM

In addition, repo holdings backed by Treasury securities and Agency

securities (including Agency MBS) are approximately $150bn and

$250bn, respectively

Preference for T-bills and Agency discount notes, but funds do own

coupon securities including about $125bn in Agency FRNs with

maturities 2 years or less

There could be demand for Treasury floaters yielding more than T-

bills, but MMMF preference is likely under 2 year final maturity

Other significant money market investors not bound by rule 2a-7 may have

Estimate of MMMF Treasury and agency securitiesholdings, $bnEstimate of MMMF Treasury and agency securitiesholdings, $bn

Other significant money market investors not bound by rule 2a-7 may have

interest in Treasury floaters as a substitute for lower yielding bank deposits,

money market fund shares, fixed-rate Treasuries and agencies, or other

money market instruments.

Securities Lending operations of custodial banks. Historically

buyers of floating rate ABS, corporates and agencies with maturities

out to 3 years. Market analysts have estimated total investments by

these securities lenders exceed $1tn, of which floaters currently

account for about $200bn

State and local governments. Commonly invest operating and other

funds in Treasuries, Agencies and MMMF shares.

The mortgage GSEs. Actively invest excess cash by selling Fed

funds, investing in Treasuries and repo and time deposits with a

limited number of financial institutions. Treasury floaters with yields in

excess of the Fed funds rate could be attractive.

Corporate cash. The recent growth of US corporate cash balances

has led to growth in bank deposits, MMMF and other liquid investment

strategies. For many firms, Treasury floaters could be an easy to use

alternative to these investments.

2a-7 Taxable MMF AUM vs. Money Market Supply,$bn, cumulative since 2007 year-end2a-7 Taxable MMF AUM vs. Money Market Supply,$bn, cumulative since 2007 year-end

Source: iMoneyNet, Crane Data, J.P. MorganNote: Agency securities holdings includes discount notes and floating rate notes.

Source: iMoneyNet, J.P. Morgan, Bloomberg6T

HE

DE

MA

ND

BA

CK

DR

OP

Over the past 2 years, declining supply of T-Bills and Agency obligations have forced

short-term liquidity investors into credit products such as CP/CDs, and any new supply

would likely be well received

However, in the longer term, regulation of money-market funds could alter their appeal to

investors, subsequently altering their demand profile for any floating rate note issuance.

One offset – to the extent that money market regulation could cause assets to flow

into short-term bond funds, those funds could in turn emerge as a demand source for

FRNs

... but while this could be an initial tailwind, it is unlikely to be a long-term positive

for demand

FRNs

7TH

ED

EM

AN

DB

AC

KD

RO

P

FRN issuance – motivation and estimated benefits 8

The demand backdrop 1

Choice of reference indices and sample structures 19

ES

8US

TR

EA

SU

RY

FL

OA

TI

NG

RA

TE

NO

T

Treasury terms out debt in order to reduce debt rollovers as well as the uncertainty regarding future debt

service costs. Thus, extending the average maturity of outstanding Treasury debt is most beneficial when

current term rates are low and/or the risk of large future changes in Treasury rates are at risk to the upside.

Term Treasury yields are a composite of three things

Expectations of the future path of the Fed Funds rate

Sovereign credit spreads, and

Term premium

By replacing T-Bill issuance with nominal fixed rate Treasury issuance, the Treasury locks in:

Revisiting the case to term out debt maturities

IT

S

By replacing T-Bill issuance with nominal fixed rate Treasury issuance, the Treasury locks in:

The current path of the expected increase in Fed Funds (currently benign)

Current credit costs as reflected in the current sovereign CDS credit spread (currently low)

The current yield curve term premium (currently low)

9FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

FRNs can help reduce the debt roll-over burden, without paying the yield curveterm premium, but at the expense of retaining exposure to rising interest ratesand credit costs

By issuing FRNs with a term of (say) 2 years, Treasury can capture the low funding costs of T-bills,

while effectively terming out issuance and reducing roll-over requirements

As an example, monthly issuance of (say) $10bn of 2-year FRNs raises $240bn over two years,

and increases the rollover burden by $10bn/month once the auction cycle is fully phased in (i.e.,

after two years)

Issuing an equivalent $240bn of securities by increasing 3 and 6 month bill offerings could boost

the monthly roll-over requirement by $40-80bn.

However, by choosing to substitute T-Bill issuance with FRNs rather than with fixed rate debt of

similar maturity, the Treasury:IT

S

similar maturity, the Treasury:

Does not lock in a future path of short rates, and instead takes on that risk in exchange for

not paying the (usually positive) interest rate risk premium priced into the curve

It does lock in term funding, and thus takes advantage of its currently low sovereign CDS

spread.

However, it may retain exposure to a widening in its sovereign CDS spread if its floating debt

costs are indexed to some benchmark that is affected by it (e.g., T-bill yields)

10FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

The benefits of issuing Floating Rate Notes versus fixed-rate debt

Trailing hypothetical savings (relative to a 2Y fixed rate note)from issuing a 2Y FRN indexed to 6-month T-bill yields at a zerospread, versus the trailing change in the fed funds rate over the2-year period

Trailing hypothetical savings (relative to a 2Y fixed rate note)from issuing a 2Y FRN indexed to 6-month T-bill yields at a zerospread, versus the trailing change in the fed funds rate over the2-year period

Trailing hypothetical savings (relative to a 5Y fixed rate note)from issuing a 5Y FRN indexed to 6-month T-bill yields at a zerospread, versus the trailing change in the fed funds rate over the5-year period

Trailing hypothetical savings (relative to a 5Y fixed rate note)from issuing a 5Y FRN indexed to 6-month T-bill yields at a zerospread, versus the trailing change in the fed funds rate over the5-year period

-6

-4

-2

0

2

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Cha

nge

inF

edFu

nds

Rat

e(2

yr)

%S

avin

gsof

Issu

ing

FRN

2yr - 6mo 2yr Change in Fed Funds-6

-5

-4

-3

-2

-1

0

10.0

1.0

2.0

3.0

4.0

5.0

Cha

nge

inFe

dF

unds

Rat

e(5

yr)

%S

avin

gsof

Issu

ing

FR

N

5yr - 6mo

5yr Change in Fed Funds

IT

S

FRNs allow Treasury to term out its funding while lessening average funding costs in the long run

Given typically positive term premium in the yield curve, the realization of short rates over a fixed term

(say, 2- or 5-years) will on average be lower than the ex-ante term rate

Thus, issuing FRNs—assuming the issuance spread is not too high, and assuming that FRNs substitute

for fixed rate notes—can produce cost savings on average. This has historically been the case, as shown

in the charts above

Last, to the extent that UST FRNs draw in new incremental demand from investors who cannot hedge the

interest rate risk in fixed rate Treasuries, this should result in an aggregate benefit to Treasury

4

6-1.5

-1.0

-0.5

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Cha

nge

inF

edFu

nds

Rat

e(2

yr)

%S

avin

gsof

Issu

ing

FRN

2

3

4-2.0

-1.0

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

Cha

nge

inFe

dF

unds

Rat

e(5

yr)

%S

avin

gsof

Issu

ing

FR

N

11FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

Savings depend less on the choice of the reference rate index, and more on the tenorof issuance that FRNs will replace - issuing FRNs instead of Bills will yield maturityextension benefits but not cost reduction

FRNs – whether indexed to bill yields or an overnight

index such as fed funds or GCF – would have

historically produced largely similar cost savings

Charts alongside show that the rolling differential

between GC/fed funds with respect to bills is stable

and relatively small. Thus, savings from issuing

FRNs might be expected to be less dependent on the

choice of index

Savings with respect to rolling bill issuance would

be expected to be negative; the price of terming out

3-month T-bill yield and ex-post 3-month average of GC index(GCFRTSY Index) versus cost/savings of floater3-month T-bill yield and ex-post 3-month average of GC index(GCFRTSY Index) versus cost/savings of floater

0

5

10

15

20

0.05

0.10

0.15

0.20

0.25 3M T-bill yield (%; left axis)

3M avg GC (%; left axis)

Differential (bp, right axis)

IT

S

be expected to be negative; the price of terming out

debt while still paying short term rates will be

reflected in the spread over bill yields that Treasury

will need to pay on an FRN, which is discussed later.3-month T-bill yield and ex-post 3-month average of effectiveFed funds (FEDL01 Index) versus cost/savings of floater3-month T-bill yield and ex-post 3-month average of effectiveFed funds (FEDL01 Index) versus cost/savings of floater

-50.00Oct 09 Feb 10 May 10 Aug 10 Dec 10 Mar 11 Jun 11 Sep 11

-5

0

5

10

15

0.00

0.05

0.10

0.15

0.20

Oct 09 Feb 10 May 10 Aug 10 Dec 10 Mar 11 Jun 11 Sep 11

3M T-bill yield (%; left axis)

3M avg FF (%; left axis)

Differential (bp, right axis)

12FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

Estimating the forward-looking benefits to Treasury from FRN issuance

Three factors determine the costs/savings of FRNs versus fixed-rate debt

The pricing spread – e.g., what fixed spread over (say) floating 3-month bill yields Treasury

pays to issue a par priced FRN

The level of interest rate risk premium at time of issuance

The Fed’s monetary policy stance—savings are likely to be greater when the change in the

funds rate is negative, and especially when such change is more negative than the

expectations priced into forwards

The first of these – pricing spreads – will likely not be onerous enough to materially reduce theIT

S

The first of these – pricing spreads – will likely not be onerous enough to materially reduce the

savings from issuing FRNs

Even if FRNS are initially less liquid, market participants will likely arbitrage away any

significant differences from the spread implied by fixed rate note asset swap levels, thanks

to a highly developed interest rate derivatives market

Experience in other fixed income product sectors that have fixed rate notes as well as

FRNs suggests that this is historically true

13FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

A closer look at yield curve term premium

Term premium itself may be thought of as being composed of two parts

the cost of maturity extension, as well as

the premium for the privilege of fixing funding costs, which we may think of as just the

interest rate risk premium

We may estimate the former by looking at the asset swap spread of term Treasury debt over

Bills – e.g., if 2Y notes swap to 3M bill yields + 8bp to term, then 8bp represents the cost of

maturity extension

In near-zero rate regimes, we may estimate the interest rate risk premium via cap costsIT

S

In near-zero rate regimes, we may estimate the interest rate risk premium via cap costs

It is reasonable to assume that the risk to short-rates is one-sided, there is similarity

between the cost of an at-the-money cap on short rates (expressed in yield terms) and the

portion of term premium attributable to the uncertainty in short rates

Estimation is subject to basis risks, since the cap market is based on Libor and not OIS

forwards; Libor cap costs likely overestimate interest rate risk premium currently, because

of higher Libor rate volatility

FRNs will incur the costs associated with maturity extension, while saving on interest rate risk

premium (relative to issuing term debt)

14FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

Is this the best time in the cycle for FRN issuance from Treasury’s perspective?

Estimated interest rate risk premium* by maturity; bp of yieldEstimated interest rate risk premium* by maturity; bp of yieldRolling 2-year savings from issuing a 2-year FRN linked to6-month T-bills relative to issuing fixed-rate notes versus 2Yinterest rate risk premium; bp of yield

Rolling 2-year savings from issuing a 2-year FRN linked to6-month T-bills relative to issuing fixed-rate notes versus 2Yinterest rate risk premium; bp of yield

20

30

40

50

60

70

80

90

100

1102Y3Y5Y

60

80

100

120

140

160

180

200

220

240Trailing cost savingsSavings attributable to term premium

IT

S

Current levels of interest rate risk premium are low, and the risk to the expected path of policy rates is likely asymmetrically

biased higher

The Fed’s commitment to low rates until late-2014, as well as its new communications policy of projecting a path for

the funds rate, have already lowered interest rate risk premium, and this is unlikely to rise for several years.

Given de minimis monetary policy rates currently, the next move by the Fed is only likely to take the funds rate higher

With interest rate risk premium currently near all time lows, savings are likely to be marginal

10

Jan 10 Jul 10 Jan 11 Jul 11 Jan 1220

40

Jul 10 Jan 11 Jul 11 Jan 12* Estimated as the cost of an at-the-money cap on short rates, in yield terms. This is premised on the notion that in near-zero policy rate regimes, the one-sided nature of policy raterisk makes interest rate risk premium comparable to cap costs.

15FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

What about the cost – where might Treasury FRNs price?

Estimated pricing spread on a hypothetical 2Y FRN linked to3M Treasury bills*; bpEstimated pricing spread on a hypothetical 2Y FRN linked to3M Treasury bills*; bp

Regardless of the choice of floating rate index used to

specify the coupons in any potential FRN issued by

Treasury, it is useful to consider the par priced FRN

spread-over-bills for purposes of analysis

I.e., if the basis swap market is used to transform

the FRN into a floater linked to bill yields, what

would the pricing spread be for a par priced FRN

at time of issuance

This represents the direct “cost” incurred by

Treasury, for the sole purpose of terming out its

debt0

5

10

15

20

25

Estimated pricing spread; bpAverage = 11.7

IT

S

It is reasonable to assume that this will not fall

below zero; should it do so, Treasury has a strong

incentive to issue FRNs in place of T-bills

The chart alongside shows the hypothetical pricing

spread, if FRNs were to price at the same asset swap

spread as a maturity matched fixed rate Treasury note.

This is a reasonable estimate of where FRNs might price

-5

0

Jul 10 Jan 11 Jul 11 Jan 12

* Assumes that FRNs will price at the same asset swap level as a maturitymatched bullet Treasury.

16FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

A stylized illustration of the relationship between pricing spreads and the

attractiveness to Treasury

A schematic illustration of the attractiveness of issuing FRNs from Treasury’s perspective, for various pricing spreads(versus a T-bill floating index)A schematic illustration of the attractiveness of issuing FRNs from Treasury’s perspective, for various pricing spreads(versus a T-bill floating index)

Not attractive

Attractive

FRNs deliver maturity extension at a higher

cost than term fixed-rate debt

FRNs still deliver savings from term premium

but give some of it back for the privilege of

Likely pricing

spread = bills +

maturity extension

premium

Bills + maturity

extension premium

+ interest rate risk

premium

IT

S

Very attractive

FRNs deliver maturity extension as well as

cost savings relative to term debt or rolling

bills

Bills + 0

but give some of it back for the privilege of

extension

premium

17FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

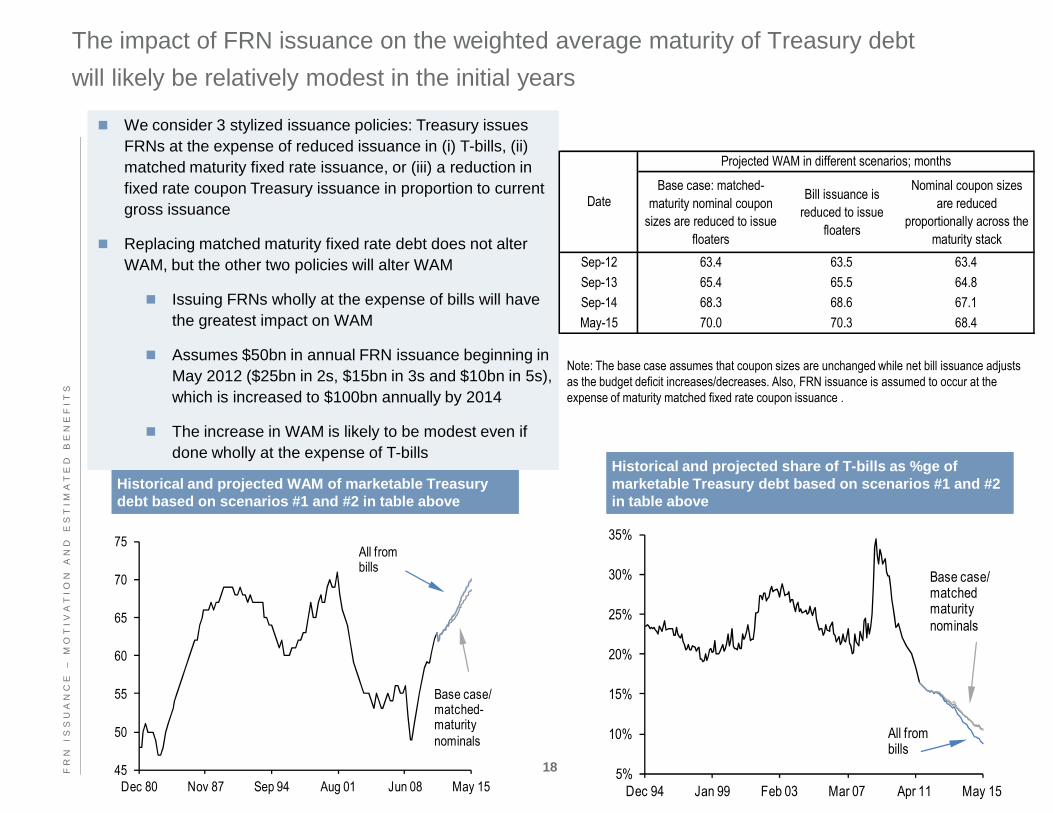

The impact of FRN issuance on the weighted average maturity of Treasury debt

will likely be relatively modest in the initial years

We consider 3 stylized issuance policies: Treasury issues

FRNs at the expense of reduced issuance in (i) T-bills, (ii)

matched maturity fixed rate issuance, or (iii) a reduction in

fixed rate coupon Treasury issuance in proportion to current

gross issuance

Replacing matched maturity fixed rate debt does not alter

WAM, but the other two policies will alter WAM

Issuing FRNs wholly at the expense of bills will have

the greatest impact on WAM

Assumes $50bn in annual FRN issuance beginning in

May 2012 ($25bn in 2s, $15bn in 3s and $10bn in 5s),

which is increased to $100bn annually by 2014

Base case: matched-

maturity nominal coupon

sizes are reduced to issue

floaters

Bill issuance is

reduced to issue

floaters

Nominal coupon sizes

are reduced

proportionally across the

maturity stack

Sep-12 63.4 63.5 63.4

Sep-13 65.4 65.5 64.8

Sep-14 68.3 68.6 67.1

May-15 70.0 70.3 68.4

Projected WAM in different scenarios; months

Date

Note: The base case assumes that coupon sizes are unchanged while net bill issuance adjustsas the budget deficit increases/decreases. Also, FRN issuance is assumed to occur at theexpense of maturity matched fixed rate coupon issuance .I

TS

Historical and projected WAM of marketable Treasurydebt based on scenarios #1 and #2 in table aboveHistorical and projected WAM of marketable Treasurydebt based on scenarios #1 and #2 in table above

45

50

55

60

65

70

75

Dec 80 Nov 87 Sep 94 Aug 01 Jun 08 May 15

Base case/matched-maturitynominals

All frombills

The increase in WAM is likely to be modest even if

done wholly at the expense of T-bills

5%

10%

15%

20%

25%

30%

35%

Dec 94 Jan 99 Feb 03 Mar 07 Apr 11 May 15

Base case/matchedmaturitynominals

All frombills

Historical and projected share of T-bills as %ge ofmarketable Treasury debt based on scenarios #1 and #2in table above

Historical and projected share of T-bills as %ge ofmarketable Treasury debt based on scenarios #1 and #2in table above

18FR

NI

SS

UA

NC

E–

MO

TI

VA

TI

ON

AN

DE

ST

IM

AT

ED

BE

NE

F

Choice of reference indices and sample structures 19

The demand backdrop 1

FRN issuance – motivation and estimated benefits 8

ES

19US

TR

EA

SU

RY

FL

OA

TI

NG

RA

TE

NO

T

The majority of the Agency floater market is linked to Libor or Fed funds

Distribution by originalmaturity (years)Distribution by originalmaturity (years)

About $153bn of Agency floaters are outstanding

currently, which is about 7.2% of the total Agency

debt market

Most of these structures reference Libor or Fed

funds as an index

Demand for floaters linked to Libor and FF

may be due in part to the deep and liquid

derivatives markets based on these

indices, allowing for efficient hedging of

risks

Distribution by underlyingbenchmark typeDistribution by underlyingbenchmark type

1M Libor 64.8%

FF Effective 25.9%

3M Libor 5.4%

Prime rate 2.8%

3M T-bill 0.7%

CPI 0.1%

Distribution by resetfrequencyDistribution by resetfrequency

Monthly 64.9%

Daily 28.6%

0-1 0.2%

1-2 16.7%

2-3 75.5%

3-4 4.9%

4-5 0.3%

5-6 1.5%

6-7 0.1%

7-8 0.0%

8-9 0.0%

10-11 0.1%

12-13 0.1%

15-16 0.4%TU

RE

S

risks

These indices have disadvantages too –

exposure to banking system credit risk (in

the case of Libor), and the Fed funds

effective rate is distorted by IOER and

related inefficiencies

Daily 28.6%

Quaterly 5.6%

Weekly 0.7%

Semi-annually 0.2%

15-16 0.4%

20-21 0.1%

>30 0.2%

FNMA, FHLMC and FHLB floaters outstanding; $bnFNMA, FHLMC and FHLB floaters outstanding; $bn

12598

123152

7045

137

318

267250

214

0

50

100

150

200

250

300

350

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 20CH

OI

CE

OF

RE

FE

RE

NC

EI

ND

IC

ES

AN

DS

AM

PL

ES

TR

UC

T

The corporate floater market is also predominantly linked to Libor as an index rate

Distribution by originalmaturity (years)Distribution by originalmaturity (years)

Distribution by underlyingbenchmark typeDistribution by underlyingbenchmark type

Distribution by resetfrequencyDistribution by resetfrequency

0-1 3.42%

1-2 23.46%

2-3 34.89%

3-4 1.86%

4-5 13.76%

5-6 2.03%

6-7 5.24%

7-8 1.50%

8-9 0.28%

3M Libor 96.10%

1M Libor 3.38%

FF Effective 0.38%

6M Libor 0.09%

Prime Rate 0.04%

3M T-bill 0.01%

High grade corporate floaters outstanding*; $bnHigh grade corporate floaters outstanding*; $bn

256

444

509

392

267300

350

400

450

500

550

TU

RE

S

frequencyfrequency8-9 0.28%

9-10 12.02%

10-11 0.22%

11-12 0.24%

19-20 0.63%

12-13 0.03%

28-29 0.00%

29-30 0.32%

30-31 0.09%

Quarterly 96.13%

Monthly 3.39%

Daily 0.42%

Semi-annually 0.05%

Weekly 0.01%

* Includes only index-eligible floaters. (Floaters with <$300mn outstanding and less thanone year to maturity are excluded.)

256

212 216

200

250

2005 2006 2007 2008 2009 2010 2011

21CH

OI

CE

OF

RE

FE

RE

NC

EI

ND

IC

ES

AN

DS

AM

PL

ES

TR

UC

T

Possible Options for a Reference rate indexT

UR

ES

Index

Decrease

Treasury's

rollover risk

Diversify

Treasury's

funding

costs

Reduce

basis risk

in the

system

Already

used in

existing

markets

Will likely

appeal to retail

investors

Will likely

appeal to

money market

investors

Additional Notes

LIBOR yes partially yes yes yes yes

Provides for a variety of reset frequencies from overnight to 12-month.

More attractive to some investors as more closely linked to their

liabilities. Subject to banking system funding pressures. Diversification

benefits will be somewhat limited, since issues around sovereign credit

concerns would likely also result in higher LIBOR. Nonetheless, with

only 3 US banks in the USD Libor panel, some degree of

diversification is likely.

Typically indexed to weekly auction clearing rates. Treasury could

also explore daily resetting to secondary/ constant maturity T-bills data

released by the Fed, but this could reduce transparency. Would

enable frequent resets keeping price of floater close to par and thus

making it more attractive to investor types that value price stability such

22CH

OI

CE

OF

RE

FE

RE

NC

EI

ND

IC

ES

AN

DS

AM

PL

ES

TR

UC

T

T-bills yes no yes yes yes yes

making it more attractive to investor types that value price stability such

as money market funds. Will be of interest to investors who typically roll

T-bills. While this market exists, very small percentage of Agency and

Corporate FRNs are linked to T-bills (0.7% and 0.1% , respectively).

Changes in Bill auction schedule would result in changes in floaters in

which resets are linked to bill auctions. Not significantly different than T-

Bills, risking cannibalization of T-Bill demand.

Fed

funds eff.

rate

yes yes yes yes partially yes

Daily resets. Would enable daily resets keeping price of floater close to

par and thus making it more attractive to investor types that value price

stability such as money market funds. Predictably low in current rate

environment. Subject to changes in the Fed's monetary policy. Future

of Fed Funds market is uncertain, as future of GSEs and Fed chosen

policy tool is uncertain.

Fed

funds

target

yes yes no no yes yesA highly visible rate, but would will be hard to hedge given basis risk

with tradable markets.

GCF

repo rateyes no yes no partially yes

Could enhance Repo market itself. Could decrease demand for repo

product and indirectly for nominal Treasuries.

Comments on structural characteristics of FRNs

Issuance in the existing floater market has been concentrated in maturities 5-years and in. More than 92%

of the Agency market and 61% of the corporate floater market were issued with an original maturity of less

than 3-years.

Having a more frequent reset frequency will result in lower interest rate duration and thus lower price vol,

and could be more desirable to investors seeking stable value assets. Daily and Monthly resets are more

typical in Agency FRNs, while quarterly resets are more typical in Corporate FRNs

Treasury should floor coupons payments at zero

This does note necessarily mean a zero floor on observations of the floating index rate. For instance,

a note paying semiannual coupons, with daily accruals could result in negative observations on one or

more days between coupon payment dates. Only the ultimate coupon payment needs to be floored atTU

RE

S

more days between coupon payment dates. Only the ultimate coupon payment needs to be floored at

zero

23CH

OI

CE

OF

RE

FE

RE

NC

EI

ND

IC

ES

AN

DS

AM

PL

ES

TR

UC

T

Choice of index rate and final maturity could also be a determinant of incrementaldemand for the product

Depending on final maturity there could be significant demand

for a Treasury Floater Indexed to either overnight fed funds or

GC Repo, primarily from Money-market funds and liquidity

portfolios.

Demand for an FRN linked to either of these indices would

likely be driven by:

2a-7 Money Market Funds (if the contingent final

maturity is less than 397 days)

Corporate Treasury accounts not set-up to trade repo

Investment funds / Foreign accounts looking for a high

quality floating rate asset

1-week average of GCF Treasury index versus 1-weekaverage of par amount traded;

% $bn

1-week average of GCF Treasury index versus 1-weekaverage of par amount traded;

% $bn

50

100

150

200

250

0.00

0.05

0.10

0.15

0.20

0.25

0.30 Index level Par amount traded

TU

RE

S

quality floating rate asset

The basis between GCF and fed funds is small on a smoothed

basis, so returns on an FRN linked to either would likely be

similar

Both indices are amenable to daily resets, which would produce

very low interest rate duration risk (but not spread duration),

and thus lower price volatility. However, ratings agency

guidelines favor indices that are more than 95% correlated to

either fed funds or Libor, possibly making fed funds a better

choice

500.00

Nov

09

Feb

10

May

10

Aug

10

Nov

10

Feb

11

May

11

Aug

11

Nov

11

GC Index (GCFRTSY Index) versus effective Fed funds(FEDL01 Index); 1-week moving average; %GC Index (GCFRTSY Index) versus effective Fed funds(FEDL01 Index); 1-week moving average; %

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Jul 10 Jan 11 Jul 11 Jan 12

GC indexFed funds

24CH

OI

CE

OF

RE

FE

RE

NC

EI

ND

IC

ES

AN

DS

AM

PL

ES

TR

UC

T

Description of a sample 2Y FRN linked to 6M T-bill yields

Characteristics

Maturity: 2-years

Coupon: Floating

Payment Frequency: Semi-

Annual

Reference Index: The average

auction yield of 6-mo T-bill

Auctions during reference period

Hypothetical annualized funding cost for a 2-year Treasury FRN linkedto 6-month T-bill yields versus actual 2-year Treasury yield; %Hypothetical annualized funding cost for a 2-year Treasury FRN linkedto 6-month T-bill yields versus actual 2-year Treasury yield; %

2

3

4

5

6Hypothetical annualized funding cost for 2Y FRN linked to 6M T-bills

2YTreasury yield

TU

RE

S

Day Count: Act / Act

0

1

Aug

01

Dec

01

Apr

02

Aug

02

Dec

02

Apr

03

Aug

03

Dec

03

Apr

04

Aug

04

Dec

04

Apr

05

Aug

05

Dec

05

Apr

06

Aug

06

Dec

06

Apr

07

Aug

07

Dec

07

Apr

08

Aug

08

Dec

08

Apr

09

Aug

09

Dec

09

25CH

OI

CE

OF

RE

FE

RE

NC

EI

ND

IC

ES

AN

DS

AM

PL

ES

TR

UC

T

Description of a sample 2Y FRN linked to the overnight fed funds and GCFrate indices

GC Index Floater Characteristics

Maturity: 2-years

Coupon: Floating

Payment Frequency: Semi-Annual

Reference Index: GCFRTSY <Index>

The Index is the weighted average interest paideach day on General US Treasury Collateral in thedealer to dealer repo market.

Average current daily volume is approximately$150bn.

Average Fed funds Floater Characteristics

Maturity: 2-years

Coupon: Floating

Payment Frequency: Semi-Annual

Reference Index: FEDL01 <Index>

The index represents the volume-weightedaverage of interest rates at which depositoryinstitutions lend balances at the Federal Reserve toother depository institutions overnight.

Day Count: Act / Act

TU

RE

S

$150bn.

Day Count: Act / Act

Day Count: Act / Act

26CH

OI

CE

OF

RE

FE

RE

NC

EI

ND

IC

ES

AN

DS

AM

PL

ES

TR

UC

T

Conclusions

The demand backdrop is currently favorable for US Treasuries, but it is prudent for Treasury to consider broadening its

issuance strategy to draw in more incremental demand

Floating Rate Notes issued by Treasury are one such avenue, and could be attractive to money funds, investors seeking bonds

with low duration risk, and possibly banks seeking to mitigate the accounting effects of some of the Basel III provisions

That said, any such incremental demand is likely to be modest in the near term

The current timing does not appear ideal, although initiating an issuance program now could allow Treasury to position itself to

capitalize on a more favorable market environment

Term premium in the yield curve is currently at all time lows, and the risk to the path of the funds rate is biased

asymmetrically towards higher rates since further Fed easing is not possible

However, initiating a program now could help position Treasury for a future environment marked by higher term premia

TU

RE

S

The choice of a floating rate index must balance the need for simplicity and transparency with the need to diversify Treasury’s

funding risk

Indexing to T-bills offers simplicity and transparency, but does not fully diversify funding cost risk

GCF offers the prospect of daily resets and very low duration risk, but is a more complex choice that is mostly unknown

to retail investors

Libor offers simplicity & transparency, but this index creates exposure to banking sector credit for Treasury

Indexing to average Fed funds rate offers simplicity and transparency, overnight reset frequency, and a viable

derivatives market for risk management. In addition, a reasonably well developed FRN market exists in other sectors. Its

appeal to retail investors needs to be further studied

27CH

OI

CE

OF

RE

FE

RE

NC

EI

ND

IC

ES

AN

DS

AM

PL

ES

TR

UC

T