o&g 2008 outlook

TRANSCRIPT

Oil & Gas 2008 Outlook

Alexander Burgansky +7 (495) 258 7904 [email protected] Adam Landes +44 (20) 7367 7777 [email protected] Elena Savchik +7 (495) 725 5265 [email protected] Roman Elagin +7 (495) 258 7763 [email protected] Irina Elinevskaya +7 (495) 783 5662 [email protected]

Sector update Equity Research

13 December 2007

Oil & Gas Russia, Central Asia and Ukraine

Report date: 13 December 2007 Total sector MktCap, $mn 645,507 Target MktCap, $mn 844,956 Weight In MSCI, % 61.4 RenCap Index High 3,532 RenCap Index Low 2,396 Average sector P/E 12.5 Average sector EV/EBITDA 8.0

Higher oil price forecasts. A tighter supply/demand outlook and rising production costs globally cause us to revise our long-term Brent price outlook to $60/bbl (from $50bbl). Our 2008 forecasts went up to $75/bbl (from $65/bbl). This resulted in an average 20% upgrade in our target prices.

Policy watch. Following crucial developments in the Russian gas sector in 2006-2007, we believe 2008 could see greater clarity in the long-term tax regulations of the oils sector in both Russia and Central Asia. Likely changes to gas taxation in Russia are also of great interest.

Corporate activity will be high, resulting in an even greater role played by state-controlled companies in Russia and Kazakhstan, in our view. Key stocks to watch are TNK-BP, Gazprom Neft, Surgutneftegas and KazMunaiGaz.

Gazprom remains our top pick with a 27% higher target price of $19/share, as a result of its dual exposure to strong gas price gains in Russia and Europe. A high oil price and strong refining margins make LUKOIL ever more attractive. KazMunaiGaz should strengthen its consolidator role in Kazakhstan, while CAToil is our preferred exposure to the oil field services sector.

Figure 1: Price performance – 52 weeks Figure 2: Sector stock performance – 3 months

0

500

1000

1500

2000

2500

3000

Dec

Jan

Feb

Mar

Apr

May

Jun Jul

Aug

Sep

Oct

Nov

Dec

0

20

40

60

80

100

120Sector Relative to MSREN M SREN

-60 -40 -20 0 20 40 60

Big Sky EnergyVictoria Oil & Gas

Max PetroleumCaspian Holdings

CAToilUrals Energy

Caspian EnergyCanargo Energy

West Siberian ResourcesIntegra

RosneftLUKOILTatneft

KazMunaiGazGazpromNovatek

Dragon OilBurren Energy

Imperial EnergyGazprom Neft

Source: MSCI, Bloomberg Source: MSCI, Bloomberg

Summary of key sector ratings

Ticker Company Current price, $

Target price, $ Rating Upside MktCap, $mn EV, $mn ADR since

GAZP Gazprom 13 19 Buy 41% 316,898 335,054 1996 SIBN Gazprom Neft 5.75 4.99 Hold -13% 27,262 23,119 1998 LKOH LUKOIL 88 112 Buy 27% 73,406 76,324 1995 NVTK Novatek 7.08 6.00 Hold -15% 21,482 21,395 2005 ROSN Rosneft 9.42 9.60 Hold 2% 92,352 111,294 2006 SNGS Surgutneftegas 1.23 2.11 Buy 72% 16,751 12,192 1996 TATN Tatneft 6.20 6.90 Hold 11% 12,742 10,811 1996 TNBP TNK-BP Holding 2.17 3.33 Buy 54% 35,184 42,372 TRNFP Transneft (pref) 1,945 3,300 Buy 70% 13,004 16,889 KMG Kazmunaigas 27.6 36.1 Buy 31% 12,744 12,100 2006 UNAF Ukrnafta 75 83 Hold 11% 4,070 4,044 2000 O2C CAToil 15.4 28.1 Buy 83% 1,042 759 INTE Integra 14.8 22.3 Buy 51% 2,164 2,426

Source: RTS, Bloomberg, Renaissance Capital estimates

Important disclosures begin on page 53. This research material is released by Renaissance Securities (Cyprus) Limited. Regulated by the Cyprus Securities & Exchange Commission (License No: KEPEY 053/04).

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

2

Executive summary 3 Oil price: fundamentals stronger… 16

Technical snapshot 17 Supply/demand balance 18 OPEC watch 20 Inventories falling 21 Refining: The new scare 22 New paradigm 23

Fundamentals watch 28 Crude production 28 Investment-led growth 29 Crude netback parity 32

Policy watch 34 Oil taxation in Russia 34 Gas taxation in Russia 34 Amendments to Russia’s Subsoil Use law 34 Hydrocarbon taxation in Central Asia and Ukraine 35

Corporate actions 36 Performance and earnings 38

A special word on preferred shares 41 Company views 45

Russian vertically integrated oil companies 45 Russian gas 46 Oil & Gas infrastructure 48 Foreign-listed independents 48 Oil field services 49 Central Asia/Caspian 50 Ukraine 52

Important disclosures 53

Contents

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

3

Revised oil price forecasts

We still believe that we are in the midst of an extended oil cycle, although we accept that it will see considerably higher prices than previously anticipated and that the long-term oil price needed to deliver marginal supply has increased very significantly over recent years. Our 2008 Brent forecast rises to $75/bbl from $65/bbl. We then foresee price declines of $5/bbl in each of the next four years. Given the state of the futures market, this continues to look conservative. Our long-term Brent model input (meaning from 2011 onward) rises to $60/bbl from $50/bbl (both in nominal terms).

Policy watch: Oil taxes

Following crucial developments in the Russian gas sector in 2006-2007, we believe 2008 could see greater clarity in the Russian oils long-term tax regulations under the new government. Of equal importance are likely changes to the fiscal regime in Central Asian countries, a key source of crude production growth in the FSU. Likely changes to gas taxation in Russia are also of great interest.

Corporate activity to accelerate

We expect corporate activity will be at a high level, after an already eventful 2007. This should result in an even greater role played by state-controlled companies in Russia and Kazakhstan, in our view. Key stocks to watch are TNK-BP, Gazprom Neft, Surgutneftegas, Dragon Oil, Urals Energy and Bashkir oil assets on the sell-side, and Gazprom, Rosneft and KazMunaiGaz on the buy-side.

Our top picks

We believe the FSU oil and gas sector is attractively valued, and see plenty of potential upside throughout (our weighted-average estimated upside potential is 30%, following a 20% average increase in our target prices).

1. Russian gas through Gazprom (GAZP, BUY, target price $19.0 from $15.0). GAZP remains our top pick in the sector because of its higher, and more visible EPS growth, than for the oils stocks (we estimate Gazprom will deliver a three-year 2007-2010E EPS CAGR of 13% vs 2% for LUKOIL), amid broadly similar valuations. We see 41% potential upside for Gazprom over the next 12 months, through its unrivalled exposure to the liberalisation of the domestic gas market, strong gas prices in Europe and restructuring potential. We also believe that the recent changes to its regulatory framework have created new incentives for Gazprom to cut costs and increase gas production, which we expect will be followed by better operational performance, and improved management and organisational structures.

2. Russian oil through LUKOIL (LKOH, BUY, target price $112.0 from $92.0). Although the long-term visibility of the Russian oil sector is hindered by a lack of fiscal incentives, we believe this structural issue will have to be addressed by the new Russian government after its appointment in spring 2008. In the meantime, we see the short-term catalysts for the Russian vertically integrated oil companies (VIC) as positive, as a result of historically high refining margins (helped by the oil-price-linked subsidy on the export of oil products), flattening rouble and attractive relative

Executive summary

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

4

valuations. LKOH trades at a 19% discount to its international peers in terms of 2008E P/E multiples, based on consensus estimates, and we believe this gap should close by the end of next year, as regulation becomes clearer and LKOH’s production growth accelerates.

3. Central Asian oil through KazMunaiGas E&P (KMG, BUY, target price $36.12 from $29.62). We believe this state-controlled Kazakh company is likely to see its role as a state consolidator of all the best onshore assets grow in 2008 with likely acquisitions of its parent’s stakes in MangistauMunaiGas, Kazturkmunai and Kazakhoil-Actobe. At the same time we anticipate the effect of possible tax changes on Kazmunaigas E&P will be mitigated (given its links to the state) through off-setting benefits of asset contributions or tax privileges.

We also see considerable value in less liquid oil field services (OFS) and infrastructure companies. Our preferred exposure to the OFS segment is via CAToil (O2C, BUY, target price EUR28.1), where we see positive earnings momentum as a result of its recent acceleration in organic growth and diversification into new higher-end services. Although our pricing assumptions for its pressure pumping business recently became more conservative, we estimate it will still double its EPS next year.

Transneft’s (TRNFP, BUY, target price $3,300) share price performance has been less than impressive for the past two years, while the fundamental value of the company (and our target price) has been growing. We believe this could reverse under the new management team which, we believe, should bring the level of corporate governance and investor relations at least up to the level of other state-owned companies. We also see positive fundamental newsflow, including our expectations of strong financial results and greater regulatory visibility.

We expect 2008 will see consolidation of the gas distribution infrastructure (the so-called ‘oblgazes’) into Gazprom and believe that locally-listed Lipetskoblgaz (LPOG, BUY, target price $829) and Oreloblgaz (ORGZ, BUY, target price $973) offer the best exposure to this theme.

Finally, we see strong production growth and substantial valuation upside in junior E&P companies with our top three picks being West Siberian Resources (WSIB, BUY, target price SEK15.7 from SEK13.8) as a result of its balanced development portfolio and substantial undervaluation, Imperial Energy (IEC, BUY, target price GBP25.7 from GBP19.4) on low execution risk and significant resource potential, and Tethys Petroleum (TPL, BUY, target price CAD4.41 from CAD3.93) giving an exposure to an attractive gas sector in Central Asia.

Our changes to ratings and target prices

We have updated all our financial models for the sector, with new price targets and ratings shown in Figure 3. On average, we have increased our price targets for the FSU oil and gas companies by 20%, with the three changes in rating being Tatneft, which we have downgraded to HOLD (from Buy), Burren Energy (HOLD from Buy) and Canargo Energy (HOLD from Sell). Aside from the upgrade to our oil price forecasts, we have revised all of our financial models to take account of new macroeconomic forecasts, recent financial results and changes to the companies’ guidance.

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

5

Figure 3: Ratings and target price changes Old New TP/Rating Δ Upside

Ticker Stock TP Rating TP % Chg. Rating /(Downside) GAZP Gazprom 15.0 Buy 19.0 27% Buy +/= 41% NVTK Novatek 5.50 Hold 6.00 9% Hold +/= -15% SIBN Gazprom Neft 4.10 Hold 4.99 22% Hold +/= -13% LKOH LUKOIL 92.0 Buy 112.0 22% Buy +/= 27% ROSN Rosneft 8.75 Hold 9.60 10% Hold +/= 2% SNGS Surgutneftegas (common) 1.90 Buy 2.11 11% Buy +/= 72% SNGSP Surgutneftegas (preferred) 1.14 Buy 1.27 11% Buy +/= 90% TATN Tatneft (common) 5.80 Buy 6.90 19% Hold +/- 11% TATNP Tatneft (preferred) 3.11 Buy 3.59 15% Hold +/- 11% TNBP TNK-BP Holding (common) 2.88 Buy 3.33 16% Buy +/= 54% TNBPP TNK-BP Holding (preferred) 2.44 Buy 2.94 20% Buy +/= 54% TRNFP Transneft (preferred) 3,300 Buy 3,300 0% Buy =/= 70% IEC Imperial Energy £19.4 Buy £25.7 32% Buy +/= 91% SBE Sibr Energy £5.44 Hold £5.85 8% Hold +/= 13% UEN Urals Energy £6.37 Hold £4.71 -26% Hold -/= 124% VOG Victoria Oil & Gas £0.88 Hold £0.81 -8% Hold -/= 501% VGAS Volga Gas £3.75 Buy £4.17 11% Buy +/= 35% WSIB West Siberian Resources SEK 13.8 Buy SEK 15.7 14% Buy +/= 224% ABG Arawak Energy CAD 3.51 Buy CAD 3.63 3% Buy +/= 36% BSKO Big Sky Energy 0.22 Hold 0.13 -40% Hold -/= 51% KAZ BMB Munai 10.0 Buy 10.2 2% Buy +/= 79% BUR Burren Energy £12.65 Buy £12.76 1% Hold +/- 3% CNR Canargo Energy 0.49 Sell 0.50 1% Hold +/+ -26% CEK Caspian Energy CAD 0.77 Buy CAD 0.79 2% Buy +/= 102% CSH Caspian Holdings £0.06 Hold £0.06 0% Hold -/= 59% DGO Dragon Oil £3.69 Buy £4.36 18% Buy +/= 34% FRR Frontera Resources £1.41 Buy £1.37 -3% Buy -/= 142% KMG KazMunaiGas 29.62 Buy 36.12 22% Buy +/= 31% MXP Max Petroleum £1.22 Hold £1.07 -12% Hold -/= 44% RXP Roxy Petroleum £0.42 Hold £0.43 4% Hold +/= 13% TPL Tethys Petroleum CAD 3.93 Buy CAD 4.41 12% Buy +/= 52% TMY Transmeridian 1.57 Sell 1.71 9% Sell +/= -4% UNAF Ukrnafta 77 Hold 83 8% Hold +/= 11% O2C CAToil € 28.1 Buy € 28.1 0% Buy =/= 83% INTE Integra 22.3 Buy 22.3 0% Buy =/= 51%

Source: Renaissance Capital estimates

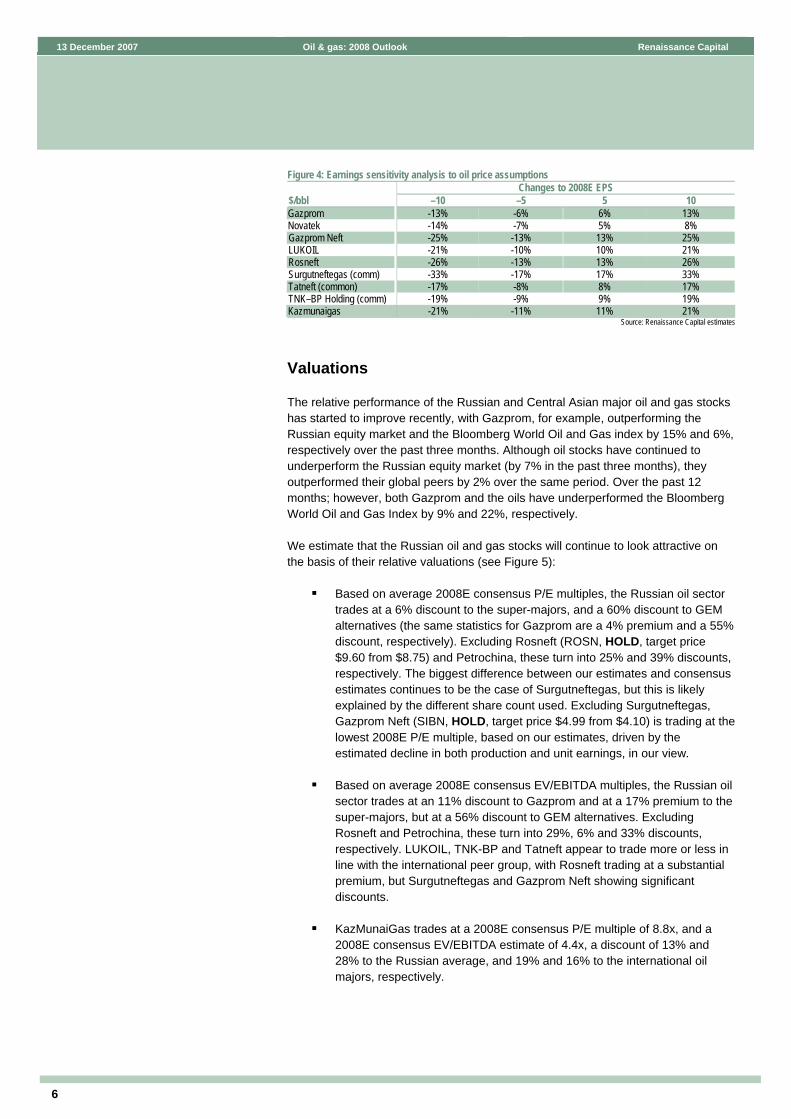

Sensitivity analysis of earnings to the oil price

The Russian oil industry’s punitive taxation makes pure upstream Russian oil producers (such as Tatneft) less sensitive to oil price assumptions than their international peers. However, vertically integrated companies benefit from higher oil prices disproportionately, as the Russian refining margin is directly linked to the oil price (via the tax subsidy on the export of oil products). Our analysis in Figure 4 suggests that Gazprom is the least sensitive to the oil price in terms of its 2008 EPS estimates (due to the lag effect on the gas price in Europe, and secular growth in domestic gas tariffs); while Surgutneftegas (SNGS, BUY, target price $2.11 from $1.90) is the most sensitive (because of its high operating leverage). We calculate that a $5/bbl drop in the oil price forecast reduces our 2008E EPS estimates for the Russian stocks 6% (for the gas producers), and 12% for the oil producers, on average. The same statistics for KazMunaiGaz E&P is 11%.

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

6

Figure 4: Earnings sensitivity analysis to oil price assumptions Changes to 2008E EPS

$/bbl –10 –5 5 10 Gazprom -13% -6% 6% 13% Novatek -14% -7% 5% 8% Gazprom Neft -25% -13% 13% 25% LUKOIL -21% -10% 10% 21% Rosneft -26% -13% 13% 26% Surgutneftegas (comm) -33% -17% 17% 33% Tatneft (common) -17% -8% 8% 17% TNK–BP Holding (comm)

-19% -9% 9% 19% Kazmunaigas -21% -11% 11% 21%

Source: Renaissance Capital estimates

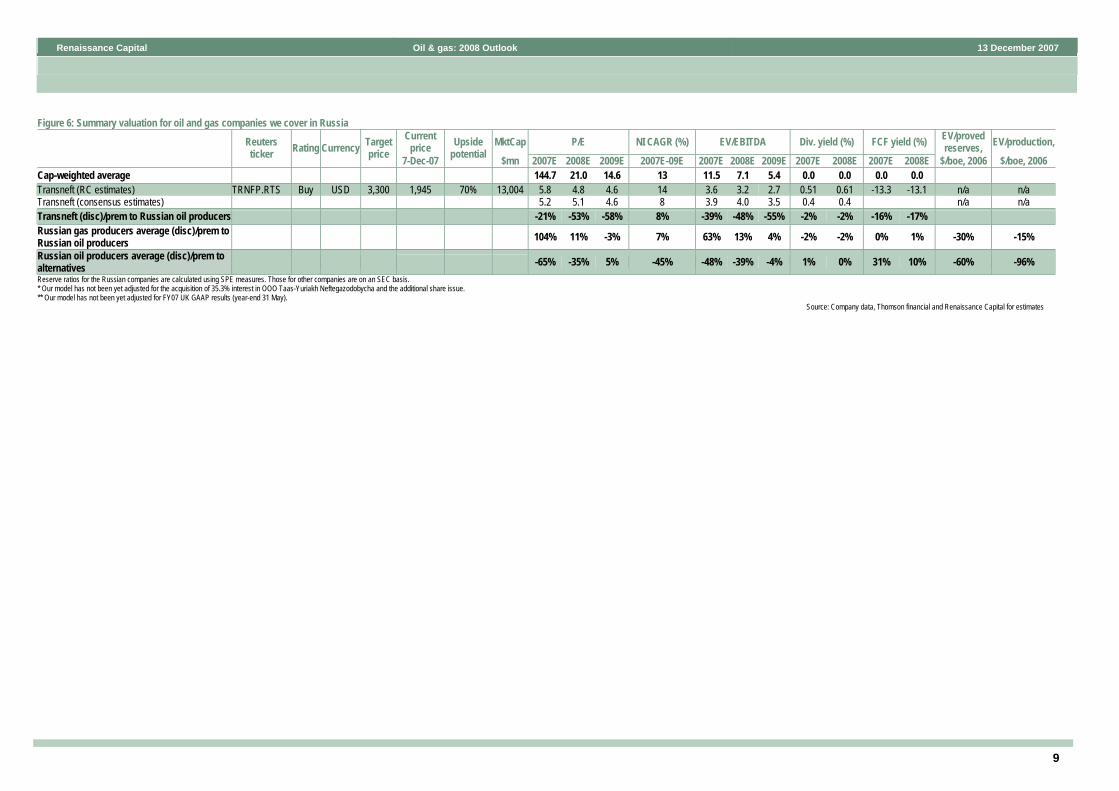

Valuations

The relative performance of the Russian and Central Asian major oil and gas stocks has started to improve recently, with Gazprom, for example, outperforming the Russian equity market and the Bloomberg World Oil and Gas index by 15% and 6%, respectively over the past three months. Although oil stocks have continued to underperform the Russian equity market (by 7% in the past three months), they outperformed their global peers by 2% over the same period. Over the past 12 months; however, both Gazprom and the oils have underperformed the Bloomberg World Oil and Gas Index by 9% and 22%, respectively.

We estimate that the Russian oil and gas stocks will continue to look attractive on the basis of their relative valuations (see Figure 5):

Based on average 2008E consensus P/E multiples, the Russian oil sector trades at a 6% discount to the super-majors, and a 60% discount to GEM alternatives (the same statistics for Gazprom are a 4% premium and a 55% discount, respectively). Excluding Rosneft (ROSN, HOLD, target price $9.60 from $8.75) and Petrochina, these turn into 25% and 39% discounts, respectively. The biggest difference between our estimates and consensus estimates continues to be the case of Surgutneftegas, but this is likely explained by the different share count used. Excluding Surgutneftegas, Gazprom Neft (SIBN, HOLD, target price $4.99 from $4.10) is trading at the lowest 2008E P/E multiple, based on our estimates, driven by the estimated decline in both production and unit earnings, in our view.

Based on average 2008E consensus EV/EBITDA multiples, the Russian oil sector trades at an 11% discount to Gazprom and at a 17% premium to the super-majors, but at a 56% discount to GEM alternatives. Excluding Rosneft and Petrochina, these turn into 29%, 6% and 33% discounts, respectively. LUKOIL, TNK-BP and Tatneft appear to trade more or less in line with the international peer group, with Rosneft trading at a substantial premium, but Surgutneftegas and Gazprom Neft showing significant discounts.

KazMunaiGas trades at a 2008E consensus P/E multiple of 8.8x, and a 2008E consensus EV/EBITDA estimate of 4.4x, a discount of 13% and 28% to the Russian average, and 19% and 16% to the international oil majors, respectively.

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

7

Another way of showing the relative valuations of the FSU oil and gas companies vs international benchmarks is by comparing their unit valuations (market capitalisation per unit of output) with unit profitability (net income per unit of output), as shown in Figure 5. As is evident from this analysis, Russian oil companies have much lower unit valuations as a result of much lower unit net income. Most of the Russian companies seem to be positioned on, or below, the trend line, with the notable exception of Rosneft. KazMunaiGas enjoys a higher unit net income, and a higher unit valuation.

Figure 5: Price/Earnings ratio: relative valuation of Russian oil companies

Kazmunaigas

Gazprom

ConocoPhillips

Chevron

Petrobras

ONGCBP

Gazprom NeftLukoil

TNK-BP Holding

Tatneft

Surgutneftegas

Rosneft

RoyalDutchShell

Petrochina

CNOOC

Total

Sinopec ExxonM obil

Novatek

-

100

200

300

400

500

600

700

800

- 5 10 15 20 25 30 35NI/bbl, $/boe

MC

ap/b

bl,

$/bo

e

Source: Thomson Datastream, Renaissance Capital estimates

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

8

Figure 6: Summary valuation for oil and gas companies we cover in Russia Current

price MktCap P/E NI CAGR (%) EV/EBITDA Div. yield (%) FCF yield (%) EV/proved reserves, EV/production,

Reuters ticker Rating Currency Target

price 7-Dec-07

Upside potential $mn 2007E 2008E 2009E 2007E-09E 2007E 2008E 2009E 2007E 2008E 2007E 2008E $/boe, 2006 $/boe, 2006

Russian gas producers Gazprom (RC estimates) GAZP.RTS Buy USD 19 13.5 41% 316,898 14.0 10.5 9.8 13 9.1 6.4 5.9 0.9 1.1 2.7 5.4 2.8 91.1 Gazprom (consensus estimates) 13.3 11.3 9.9 17 8.7 7.1 6.0 0.8 1.0 2.8 89.9 Novatek (RC estimates) NVTK.RTS Hold USD 6.0 7.08 -15% 21,482 27.4 22.5 20.4 27 17.3 14.3 13.0 1.4 1.7 0.7 1.9 4.6 115.5 Novatek (consensus estimates) 28.0 21.4 18.5 27 17.8 13.7 12.5 1.1 1.3 4.6 115.5 Cap-weighted average 14.9 11.2 10.5 14 9.6 6.9 6.4 0.9 1.2 2.6 5.2 3.0 92.7 Russian oil producers Rosneft (RC estimates) ROSN.RTS Hold USD 9.6 9.42 2% 92,352 6.9 13.8 14.4 22 7.9 8.3 8.1 0.6 0.7 -6.3 -0.7 5.5 168.0 Rosneft (consensus estimates) 18.9 15.1 15.9 10 10.8 9.1 8.5 0.6 0.8 5.7 173.2 LUKOIL (RC estimates) LKOH.RTS Buy USD 112 88 27% 73,406 7.6 8.2 9.1 2 5.1 5.3 5.6 1.8 2.0 5.1 3.8 3.9 97.7 LUKOIL (consensus estimates) 8.9 8.8 10.2 -2 5.7 5.6 6.0 2.0 2.1 3.9 98.7 TNK-BP Holding (RC estimates) TNBP.RTS Buy USD 3.33 2.17 54% 35,184 8.3 9.0 10.5 -17 5.6 5.8 6.2 9.3 9.1 7.3 8.2 4.3 69.0 TNK-BP Holding(RC estimates) TNBPP.RTS Buy USD 2.94 1.91 54% TNK-BP Holding (consensus estimates) 7.0 7.7 8.5 -11 4.8 5.3 5.3 7.0 6.2 3.9 62.1 Surgutneftegas (RC estimates) SNGS.RTS Buy USD 2.11 1.23 72% 16,751 4.8 7.5 7.5 -8 1.5 2.3 2.1 2.8 1.8 20.1 6.7 0.9 21.6 Surgutneftegas (RC estimates) SNGSP.RTS Buy USD 1.27 0.67 90% Surgutneftegas (consensus estimates) 4.0 4.5 4.9 -6 0.9 0.9 0.7 2.0 1.7 0.6 13.2 Gazprom Neft (RC estimates) SIBN.RTS Hold USD 4.99 5.75 -13% 27,262 7.2 6.7 6.7 3 5.2 4.4 4.0 4.7 5.1 11.1 13.1 3.7 67.7 Gazprom Neft (consensus estimates) 7.3 7.8 8.3 0 4.4 4.3 4.2 4.9 4.4 3.8 68.9 Tatneft (RC estimates) TATN.RTS Hold USD 6.90 6.20 11% 12,742 8.8 9.3 9.3 8 4.4 4.6 4.3 1.2 1.5 5.1 11.8 1.8 56.3 Tatneft (RC estimates) TATNP.RTS Hold USD 3.59 3.23 11% Tatneft (consensus estimates) 9.6 10.7 9.6 6 5.4 6.3 5.5 3.1 2.8 2.0 60.8 Cap-weighted average 7.3 10.2 10.9 6 5.9 6.1 6.1 2.8 2.8 2.9 4.3 4.2 108.8 Alternatives -11% Imperial Energy (RC estimates) IEC.L Buy GBP 25.65 13.44 91% 1,394 n/a 37.0 18.4 n/a n/a 21.3 11.8 0.0 0.0 -19.1 -16.5 9.8 12,321.6 Imperial Energy (consensus estimates) n/a 27.5 16.0 n/a n/a 19.7 10.5 0.0 0.0 9.7 12,148.7 Sibir Energy (RC estimates) SBE.L Hold GBP 5.85 5.17 13% 4,052 23.4 10.3 8.8 75 9.5 6.0 5.6 2.7 4.6 -21.3 3.7 11.4 410.0 Sibir Energy (consensus estimates) 18.0 11.0 10.1 59 12.0 7.9 6.3 1.4 5.9 11.0 397.6 Urals Energy (RC estimates)* UEN.L Hold GBP 4.71 2.10 124% 509 n/a n/a 3.9 56 68.9 17.7 4.2 0.0 0.0 -141.8 -47.9 4.2 284.0 Urals Energy (consensus estimates) 58.3 17.1 4.3 102 13.5 6.9 3.0 0.1 0.5 2.5 165.8 West Siberian Resources (RC estimates) WSIB.SG Buy SEK 15.70 4.84 224% 898 19.5 14.4 10.5 41 9.7 5.2 4.1 0.0 0.0 -9.6 1.5 10.3 142.4 West Siberian Resources (consensus estimates) 20.3 9.5 7.3 50 9.1 5.8 4.1 0.0 0.0 10.8 148.4 Victoria Oil & Gas (RC estimates)** VOG.L Hold GBP 0.81 0.14 501% 32 n/a 5.5 2.3 n/a n/a 4.6 2.3 0.0 0.0 -44.5 -46.7 2.9 1,367.3 Victoria Oil & Gas (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Volga Gas (RC estimates) VGAS.L Buy GBP 4.17 3.09 35% 335 116.8 17.3 5.3 n/a n/a 12.8 2.9 0.0 0.0 -12.3 -15.9 15.6 n/a Volga Gas (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Cap-weighted average 21.0 15.5 10.3 51 11.4 10.0 6.3 1.5 2.6 -27.6 -5.3 10.6 2,653.5 Oil field services CAToil (RC estimates) O2C.DE Buy EUR 28.1 15.39 83% 1,042 26.1 12.1 10.5 40 13.5 7.1 5.8 0.0 0.0 0.0 0.0 n/a n/a CAToil (consensus estimates) 24.3 13.7 9.1 43 12.9 7.8 5.3 0.4 0.7 n/a n/a Integra (RC estimates) INTEq.L Buy USD 22.3 14.81 51% 2,164 201.9 25.3 16.6 n/a 10.6 7.1 5.2 0.0 0.0 0.0 0.0 n/a n/a Integra (consensus estimates) 30.7 17.7 15.4 n/a 11.8 8.2 6.1 0.0 0.0 n/a n/a

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

9

Figure 6: Summary valuation for oil and gas companies we cover in Russia Current

price MktCap P/E NI CAGR (%) EV/EBITDA Div. yield (%) FCF yield (%) EV/proved reserves, EV/production,

Reuters ticker Rating Currency Target

price 7-Dec-07

Upside potential $mn 2007E 2008E 2009E 2007E-09E 2007E 2008E 2009E 2007E 2008E 2007E 2008E $/boe, 2006 $/boe, 2006

Cap-weighted average 144.7 21.0 14.6 13 11.5 7.1 5.4 0.0 0.0 0.0 0.0 Transneft (RC estimates) TRNFP.RTS Buy USD 3,300 1,945 70% 13,004 5.8 4.8 4.6 14 3.6 3.2 2.7 0.51 0.61 -13.3 -13.1 n/a n/a Transneft (consensus estimates) 5.2 5.1 4.6 8 3.9 4.0 3.5 0.4 0.4 n/a n/a Transneft (disc)/prem to Russian oil producers -21% -53% -58% 8% -39% -48% -55% -2% -2% -16% -17% Russian gas producers average (disc)/prem to Russian oil producers 104% 11% -3% 7% 63% 13% 4% -2% -2% 0% 1% -30% -15%

Russian oil producers average (disc)/prem to alternatives -65% -35% 5% -45% -48% -39% -4% 1% 0% 31% 10% -60% -96% Reserve ratios for the Russian companies are calculated using SPE measures. Those for other companies are on an SEC basis. * Our model has not been yet adjusted for the acquisition of 35.3% interest in OOO Taas-Yuriakh Neftegazodobycha and the additional share issue. ** Our model has not been yet adjusted for FY07 UK GAAP results (year-end 31 May).

Source: Company data, Thomson financial and Renaissance Capital for estimates

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

10

Figure 7: Summary valuation for oil and gas companies we cover in other FSU countries Reuters Rating Currency Target Current

price Upside MktCap, P/E NI CAGR (%) EV/EBITDA Div. yield

(%) FCF yield

(%) EV/proved reserves, EV/production,

ticker price 7-Dec-07 potential $mn 2007E 2008E 2009E 2007E-09E 2007E 2008E 2009E 2007E 2008E 2007E 2008E $/boe, 2006 $/boe, 2006 Kazakhstan Arawak Energy (RC estimates) ABG.C Buy CAD 3.63 2.67 36% 479 24.3 9.3 10.2 56 5.0 2.8 2.4 n/a n/a 0.4 5.1 15.3 160 Arawak Energy (consensus estimates) 21.7 9.1 11.4 26 6.4 3.3 2.6 n/a n/a 17.3 181 Big Sky Energy (RC estimates) BSKO.US Hold USD 0.13 0.085 51% 14 3.6 0.8 0.8 n/a 5.3 0.9 0.3 n/a n/a -7 56 4.3 115.3 Big Sky Energy (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a BMB Munai (RC estimates) KAZ.US Buy USD 10.2 5.70 79% 256 7.9 5.1 4.4 283 5.3 3.7 3.1 n/a n/a -17 -9 19.1 892 BMB Munai (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Caspian Energy (RC estimates) CEK.C Buy CAD 0.79 0.39 102% 40 n/a 3.1 3.2 n/a 417 3.1 1.5 n/a n/a -59 -9 33.6 416 Caspian Energy (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Caspian Holdings (RC estimates) CSH.L Hold BPN 5.98 3.75 59% 7 n/a 10.9 2.7 n/a n/a 3.5 2.3 n/a n/a -64 -86 1.0 222 Caspian Holdings (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a KazMunaiGas (RC estimates) KMG.L Buy USD 36.1 27.6 31% 12,744 8.9 8.3 9.9 10 4.7 4.5 5.3 1.5 1.4 6 4 17.7 176 KazMunaiGas (consensus estimates) 12.2 8.8 8.2 31 5.8 4.4 4.4 0.6 0.6 18.3 182 Max Petroleum (RC estimates) MXP.L Hold BPN 107 74 44% 513 48.7 14.4 11.2 n/a 30.1 11.3 9.0 n/a n/a -1 5 198 17,110 Max Petroleum (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Roxy Petroleum (RC estimates) RXP.L Hold BPN 43 38.5 13% 132 493.4 18.7 8.8 n/a 345.4 7.3 4.2 n/a n/a -24 0 n/a n/a Roxy Petroleum (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Tethys Petroleum (RC estimates) TPL.C Buy CAD 4.41 2.90 52% 135 n/a 18.2 17.4 n/a n/a 15.0 14.3 n/a n/a -2 0 n/a n/a Tethys Petroleum (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Transmeridian (RC estimates) TMY.US Sell USD 1.71 1.78 -4% 181 n/a n/a n/a n/a 19.8 6.3 4.8 n/a n/a -36 -15 6.3 559 Transmeridian (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Cap-weighted average 15.0 8.5 9.8 15 10.0 4.8 5.4 1.3 1.2 3.9 3.5 24.0 803.5 Georgia Canargo Energy (RC estimates) CNR.US Hold USD 0.50 0.67 -26% 344 266.6 25.3 50.1 n/a 65.4 11.5 12.7 n/a n/a 5.0 4.9 97.9 2,085 Canargo Energy (consensus estimates) n/a 28.6 20.2 78 n/a 9.3 7.3 n/a n/a 92.5 1,969 Frontera Resources (RC estimates) FRR.L Buy BPN 137 57 142% 72 n/a n/a n/a n/a n/a 6.5 8.3 n/a n/a -20.8 -2.6 n/a 2,263.4 Frontera Resources (consensus estimates) n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Cap-weighted average 220.3 20.9 41.4 - 54.0 10.6 14.4 0.0 0.0 0.5 3.6 97.9 2,116.4 Turkmenistan Burren Energy (RC estimates) BUR.L Hold BPN 1,276 1,245 3% 3,601 10.5 11.0 11.1 9 6.5 6.8 6.4 1.1 0.9 5.6 5.9 36.3 213 Burren Energy (consensus estimates) 12.1 11.4 11.4 6 8.4 7.9 7.6 n/a n/a 40.9 240 Dragon Oil (RC estimates) DGO.L Buy BPN 436 326 34% 3,414 12.8 8.2 7.5 36 7.7 4.9 3.9 0.0 0.0 -3.4 4.6 21.5 421.3 Dragon Oil (consensus estimates) 10.2 6.4 6.9 41 7.3 4.8 3.5 n/a n/a 21.5 421 Cap-weighted average 11.6 9.7 9.4 22 7.1 5.9 5.2 0.6 0.5 1.2 5.3 29.1 314.5 Ukraine Ukrnafta (RC estimates) UNAF.PFT Hold USD 83 75 11% 4,070 18.8 20.7 22.8 -25 7.8 8.7 9.5 2.1 1.9 4.5 3.4 7.6 94 Ukrnafta (consensus estimates) 10.2 9.2 12.4 -10 n/a n/a n/a 4.7 4.8 8.1 100 Central Asia cap-weighted average 17.9 9.1 10.2 17.3 9.9 5.3 5.5 1.1 1.0 3.0 4.1 27.1 669.1 FSU cap-weighted average 18.0 11.0 12.3 10.6 9.6 5.8 6.1 1.2 1.1 3.2 4.0 24.0 577.4

Source: Company data, Thomson financial and Renaissance Capital for estimates

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

11

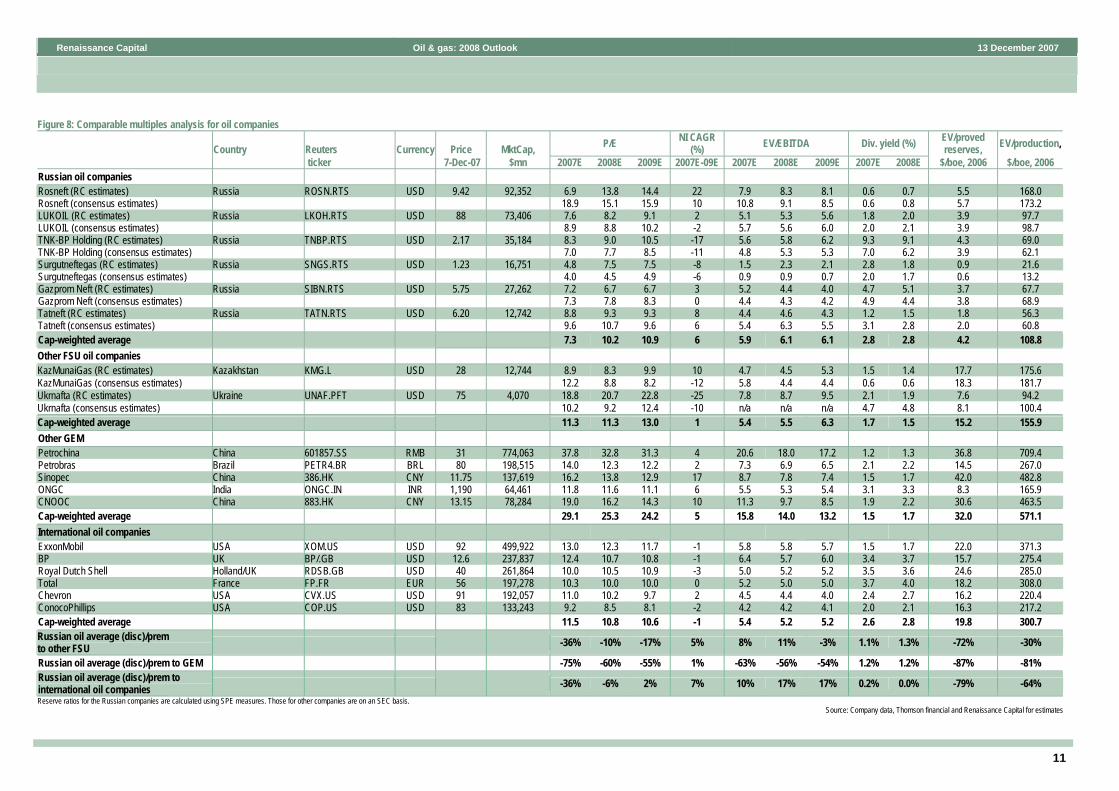

Figure 8: Comparable multiples analysis for oil companies

Reuters Price MktCap, P/E NI CAGR (%) EV/EBITDA Div. yield (%) EV/proved

reserves, EV/production,

Country

ticker Currency

7-Dec-07 $mn 2007E 2008E 2009E 2007E-09E 2007E 2008E 2009E 2007E 2008E $/boe, 2006 $/boe, 2006 Russian oil companies Rosneft (RC estimates) Russia ROSN.RTS USD 9.42 92,352 6.9 13.8 14.4 22 7.9 8.3 8.1 0.6 0.7 5.5 168.0 Rosneft (consensus estimates) 18.9 15.1 15.9 10 10.8 9.1 8.5 0.6 0.8 5.7 173.2 LUKOIL (RC estimates) Russia LKOH.RTS USD 88 73,406 7.6 8.2 9.1 2 5.1 5.3 5.6 1.8 2.0 3.9 97.7 LUKOIL (consensus estimates) 8.9 8.8 10.2 -2 5.7 5.6 6.0 2.0 2.1 3.9 98.7 TNK-BP Holding (RC estimates) Russia TNBP.RTS USD 2.17 35,184 8.3 9.0 10.5 -17 5.6 5.8 6.2 9.3 9.1 4.3 69.0 TNK-BP Holding (consensus estimates) 7.0 7.7 8.5 -11 4.8 5.3 5.3 7.0 6.2 3.9 62.1 Surgutneftegas (RC estimates) Russia SNGS.RTS USD 1.23 16,751 4.8 7.5 7.5 -8 1.5 2.3 2.1 2.8 1.8 0.9 21.6 Surgutneftegas (consensus estimates) 4.0 4.5 4.9 -6 0.9 0.9 0.7 2.0 1.7 0.6 13.2 Gazprom Neft (RC estimates) Russia SIBN.RTS USD 5.75 27,262 7.2 6.7 6.7 3 5.2 4.4 4.0 4.7 5.1 3.7 67.7 Gazprom Neft (consensus estimates) 7.3 7.8 8.3 0 4.4 4.3 4.2 4.9 4.4 3.8 68.9 Tatneft (RC estimates) Russia TATN.RTS USD 6.20 12,742 8.8 9.3 9.3 8 4.4 4.6 4.3 1.2 1.5 1.8 56.3 Tatneft (consensus estimates) 9.6 10.7 9.6 6 5.4 6.3 5.5 3.1 2.8 2.0 60.8 Cap-weighted average 7.3 10.2 10.9 6 5.9 6.1 6.1 2.8 2.8 4.2 108.8 Other FSU oil companies KazMunaiGas (RC estimates) Kazakhstan KMG.L USD 28 12,744 8.9 8.3 9.9 10 4.7 4.5 5.3 1.5 1.4 17.7 175.6 KazMunaiGas (consensus estimates) 12.2 8.8 8.2 -12 5.8 4.4 4.4 0.6 0.6 18.3 181.7 Ukrnafta (RC estimates) Ukraine UNAF.PFT USD 75 4,070 18.8 20.7 22.8 -25 7.8 8.7 9.5 2.1 1.9 7.6 94.2 Ukrnafta (consensus estimates) 10.2 9.2 12.4 -10 n/a n/a n/a 4.7 4.8 8.1 100.4 Cap-weighted average 11.3 11.3 13.0 1 5.4 5.5 6.3 1.7 1.5 15.2 155.9 Other GEM Petrochina China 601857.SS RMB 31 774,063 37.8 32.8 31.3 4 20.6 18.0 17.2 1.2 1.3 36.8 709.4 Petrobras Brazil PETR4.BR BRL 80 198,515 14.0 12.3 12.2 2 7.3 6.9 6.5 2.1 2.2 14.5 267.0 Sinopec China 386.HK CNY 11.75 137,619 16.2 13.8 12.9 17 8.7 7.8 7.4 1.5 1.7 42.0 482.8 ONGC India ONGC.IN INR 1,190 64,461 11.8 11.6 11.1 6 5.5 5.3 5.4 3.1 3.3 8.3 165.9 CNOOC China 883.HK CNY 13.15 78,284 19.0 16.2 14.3 10 11.3 9.7 8.5 1.9 2.2 30.6 463.5 Cap-weighted average 29.1 25.3 24.2 5 15.8 14.0 13.2 1.5 1.7 32.0 571.1 International oil companies ExxonMobil USA XOM.US USD 92 499,922 13.0 12.3 11.7 -1 5.8 5.8 5.7 1.5 1.7 22.0 371.3 BP UK BP/.GB USD 12.6 237,837 12.4 10.7 10.8 -1 6.4 5.7 6.0 3.4 3.7 15.7 275.4 Royal Dutch Shell Holland/UK RDSB.GB USD 40 261,864 10.0 10.5 10.9 -3 5.0 5.2 5.2 3.5 3.6 24.6 285.0 Total France FP.FR EUR 56 197,278 10.3 10.0 10.0 0 5.2 5.0 5.0 3.7 4.0 18.2 308.0 Chevron USA CVX.US USD 91 192,057 11.0 10.2 9.7 2 4.5 4.4 4.0 2.4 2.7 16.2 220.4 ConocoPhillips USA COP.US USD 83 133,243 9.2 8.5 8.1 -2 4.2 4.2 4.1 2.0 2.1 16.3 217.2 Cap-weighted average 11.5 10.8 10.6 -1 5.4 5.2 5.2 2.6 2.8 19.8 300.7 Russian oil average (disc)/prem to other FSU -36% -10% -17% 5% 8% 11% -3% 1.1% 1.3% -72% -30%

Russian oil average (disc)/prem to GEM -75% -60% -55% 1% -63% -56% -54% 1.2% 1.2% -87% -81% Russian oil average (disc)/prem to international oil companies -36% -6% 2% 7% 10% 17% 17% 0.2% 0.0% -79% -64% Reserve ratios for the Russian companies are calculated using SPE measures. Those for other companies are on an SEC basis.

Source: Company data, Thomson financial and Renaissance Capital for estimates

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

12

Figure 9: Comparable multiples analysis for gas companies Reuters Price MktCap, P/E NI CAGR (%) EV/EBITDA Div. yield (%) EV/proved reserves, EV/production, Country ticker Currency 7-Dec-07 $mn 2007E 2008E 2009E 2007E-09E 2007E 2008E 2009E 2007E 2008E $/boe, 2006 $/boe, 2006 Russian gas companies Gazprom (RC estimates) Russia GAZP.RTS USD 13.5 316,898 14.0 10.5 9.8 13 9.1 6.4 5.9 0.9 1.1 2.8 91.1 Gazprom (consensus estimates) 13.3 11.3 10 17 8.7 7.1 6.0 0.8 1.0 2.8 89.9 Novatek (RC estimates) Russia NVTK.RTS USD 7.1 21,482 27.4 22.5 20.4 27 17.3 14.3 13.0 1.4 1.7 4.6 115.5 Novatek (consensus estimates) 28.0 21.4 18.5 27 17.8 13.7 12.5 1.1 1.3 4.6 115.5 Cap-weighted average 14.9 11.2 10.5 14 9.6 6.9 6.4 0.9 1.2 3.0 92.7 International gas companies Ouicksilver Resources USA KWK.US USD 53 4,195 35.4 29.1 22.7 28 14.3 12.6 8.3 0.0 0.0 18.4 472.3 Murphy Oil USA MUR.US USD 75 14,280 18.7 12.6 10.6 30 8.6 5.8 4.4 0.9 0.9 40.2 425.6 Devon Energy USA DVN.US USD 88 39,143 14.0 11.9 10.9 8 5.9 5.1 4.0 0.6 0.7 18.5 205.0 Chesapeake Energy USA CHK.US USD 38 18,185 12.6 11.8 11.4 3 6.0 5.1 4.7 0.7 0.7 18.2 282.7 Encana Canada ECA.CA USD 67 50,160 12.8 14.3 17.3 n/a 6.1 6.2 n/a 1.2 1.2 17.3 206.5 Pioneer Natural Resources USA PXD.US USD 47 5,584 21.0 17.4 12.9 28 7.2 6.1 5.0 0.6 0.6 8.7 172.1 Apache USA APA.US USD 99 33,078 12.9 11.0 9.7 14 5.3 4.7 3.9 0.6 0.6 16.1 204.0 Anadarko Petroleum USA APC.US USD 61 28,653 17.3 18.4 17.5 -16 5.9 5.6 5.0 0.7 0.7 13.8 213.8 XTO Energy USA XTO.US USD 65 25,067 14.8 15.1 14.3 6 7.6 6.7 5.6 0.6 0.6 20.5 314.6 BG Group UK BG/.GB GBP 10.3 70,309 19.8 16.9 17.2 4 9.4 7.9 7.8 0.8 0.9 33.5 328.4 Cap-weighted average 16.1 14.7 14.6 5 7.2 6.3 4.6 0.8 0.8 22.2 264.7 Russian gas average (disc)/prem to international gas companies -7% -24% -28% 8% 35% 10% 38% 0.1% 0.3% -87% -65% Reserve ratios for the Russian companies are calculated using SPE measures. Those for other companies are on an SEC basis.

Source: Company data, Thomson financial and Renaissance Capital for estimates

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

13

Figure 10: Comparable multiples analysis for alternative oil and gas companies Country Reuters Current price MktCap, P/E EV/EBITDA EV/production EV/reserves (2P), EV/resources, ticker Currency 7-Dec-07 $mn 2007E 2010E 2007E 2010E 2007E 2010E $/boe $/boe Russia Imperial Energy Russia IEC.L GBP 13.44 1,394 n/a 10.2 n/a 7.2 1,104.4 102.9 1.95 1.07 Sibir Energy Russia SBE.L GBP 5.17 4,052 23.4 7.6 9.5 5.5 209.4 106.0 6.76 4.91 Urals Energy* Russia UEN.L GBP 2.10 509 n/a 4.6 68.9 3.1 283.4 64.8 1.71 1.04 West Siberian Resources Russia WSIB.SG SEK 4.84 898 19.5 7.2 9.7 2.7 103.2 33.9 3.72 2.41 Victoria Oil & Gas** Russia VOG.L GBP 0.14 32 n/a 2.4 n/a 1.5 341.8 32.6 0.71 0.08 Volga Gas Russia VGAS.L GBP 3.09 335 116.8 4.7 n/a 1.7 n/a 32.5 4.25 1.21 Cap-weighted average 21.0 7.7 11.4 5.1 365.1 89.8 4.96 3.39 Central Asia Arawak Energy Kazakhstan ABG.C CAD 2.67 479 24.3 12.6 5.0 2.3 124 53.2 6.32 2.87 Big Sky Energy Kazakhstan BSKO.US USD 0.09 14 3.6 1.2 5.3 -0.2 48 -3.0 4.33 4.33 BMB Munai Kazakhstan KAZ.US USD 5.70 256 7.9 4.9 5.3 3.1 243 108.8 2.15 1.12 Burren Energy Turkmenistan BUR.L BPN 1,245 3,601 10.5 11.5 6.5 6.0 185 128.5 13.78 7.61 Canargo Energy Georgia CNR.US USD 0.67 344 n/a n/a n/a n/a n/a n/a n/a 4.35 Caspian Energy Kazakhstan CEK.C CAD 0.39 40 n/a n/a 416.8 1.2 192 22.8 12.9 0.84 Caspian Holdings Kazakhstan CSH.L BPN 3.75 7 n/a n/a n/a 1.9 114 51.7 0.71 0.44 Dragon Oil Turkmenistan DGO.L BPN 326 3,414 12.8 7.3 7.7 3.1 275 87.1 4.91 4.36 Frontera Resources Georgia FRR.L BPN 56.50 72 n/a n/a n/a n/a n/a n/a n/a 0.35 Max Petroleum Kazakhstan MXP.L BPN 74.25 513 48.7 n/a 30.1 n/a n/a n/a n/a 0.74 Roxy Petroleum Kazakhstan RXP.L BPN 38.50 132 n/a n/a n/a 3.9 n/a 111 24.82 9.78 Tethys Petroleum Kazakhstan TPL.C CAD 2.90 135 n/a 21.7 n/a 15.2 n/a 584 14.83 2.07 Transmeridian Kazakhstan TMY.US USD 1.78 181 n/a n/a 19.8 1.5 281 31.5 1.60 1.60 Cap-weighted average 9,187 14.5 9.7 10.5 4.5 224 111 9.21 5.20 Russian (disc)/prem to Central Asia 44% -20% 8% 14% 63% -19% -46% -35% * Our model has not been yet adjusted for the acquisition of 35.3% interest in OOO Taas-Yuriakh Neftegazodobycha and the additional share issue. ** Our model has not been yet adjusted for FY07 UK GAAP results (year-end 31 May).

Source: Company data, Thomson financial, Renaissance Capital estimates

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

14

Figure 11: Comparable multiples analysis for oil field service companies Reuters Price MktCap, P/E NI CAGR (%) EV/EBITDA Div. yield (%) Country ticker Currency 7-Dec-07 $mn 2007E 2008E 2009E 2007E-09E 2007E 2008E 2009E 2007E 2008E Russian OFS companies CAToil (RC estimates) Russia O2C.DE EUR 15.4 1,042 26.1 12.1 10.5 40 13.5 7.1 5.8 0.0 0.0 CAToil (consensus estimates) 24.3 13.7 9.1 43 12.9 7.8 5.3 0.4 0.7 Integra (RC estimates) Russia INTEq.L USD 14.8 2,164 201.9 25.3 16.6 n/a 10.6 7.1 5.2 0.0 0.0 Integra (consensus estimates) 30.7 17.7 15.4 n/a 11.8 8.2 6.1 0.0 0.0 Cap-weighted average 144.7 21.0 14.6 40 11.5 7.1 5.4 0.0 0.0 North American OFS companies Baker Hughes Inc USA BHI.US USD 83.450 26,553 17.5 14.7 12.2 15 9.5 7.9 6.5 0.6 0.6 BJ Services Co USA BJS.US USD 24.850 7,277 8.8 8.8 n/a n/a 4.8 4.8 n/a 0.9 0.9 Calfrac Well Services Ltd Canada CFW.CA CAD 19.000 697 13.8 12.7 n/a n/a 6.7 5.2 n/a 0.5 0.5 Halliburton Co USA HAL.US USD 37.550 33,087 15.2 12.6 10.5 11 8.4 7.4 6.2 0.9 1.0 Transocean Inc USA RIG.US USD 135.070 37,720 16.2 10.3 8.4 74 14.4 7.2 5.3 0.0 0.0 Schlumberger Ltd USA SLB.US USD 97.190 116,226 23.1 19.2 16.0 27 13.7 11.3 9.4 0.7 0.8 Trican Well Service Ltd Canada TCW.CA CAD 17.180 2,075 16.1 12.4 10.3 n/a 9.2 6.0 n/a 0.6 0.6 Weatherford International Ltd USA WFT.US USD 65.650 22,143 20.0 15.2 12.1 28 11.1 9.1 7.5 0.0 0.0 Cap-weighted average 19.6 15.7 12.8 30 12.1 9.3 7.5 0.6 0.6 European OFS companies Abbot Group PLC UK ABG.GB GBP 3.348 1,575 21.8 15.6 14.0 40 11.1 9.3 5.2 1.8 2.0 Aker Kvaerner ASA Norway AKVER.NO NOK 151.750 7,575 17.1 14.6 12.1 24 9.5 8.2 6.6 2.1 2.5 Fugro NV Holland FUGR.NL EUR 53.990 5,390 17.7 14.4 12.8 30 9.9 8.1 7.1 2.1 2.6 Cie Generale de Geophysique-Veritas France GA.FR EUR 203.860 8,175 20.5 14.9 12.5 37 6.8 5.5 4.7 0.0 0.2 Petrofac Ltd UK PFC.GB USD 10.229 3,534 20.9 18.4 16.9 22 10.9 9.6 8.5 1.3 1.5 Petroleum Geo-Services ASA Norway PGS.NO USD 27.662 4,979 11.5 9.8 8.6 25 6.5 5.0 4.3 0.0 0.0 SeaDrill Ltd Norway SDRL.NO NOK 119.000 7,872 27.1 14.6 7.1 83 18.0 11.8 5.9 0.0 1.1 Saipem SpA Italy SPM.IT EUR 27.390 17,671 22.2 17.8 14.7 32 12.5 10.4 8.7 1.6 1.8 John Wood Group PLC UK WG/.GB USD 7.756 4,067 22.0 18.0 15.3 30 12.4 10.1 8.6 0.8 0.9 Cap-weighted average 20.6 15.6 12.6 37 11.2 8.9 6.9 1.1 1.4 Russian OFS average (disc)/prem to North American OFS companies 638% 34% 14% 10% -4% -24% -28% -0.6% -0.6%

Russian OFS average (disc)/prem to European OFS companies 603% 35% 16% 3% 3% -20% -22% -1.1% -1.4%

Source: Company data, Thomson financial, Renaissance Capital estimates

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

15

Figure 12: Comparable multiples analysis for Transneft Company Reuters ticker Share price MktCap EV/IC Pre-tax ROIC (%) EV/EBITDA P/E Dividend yield (%) Country Currency 7-Dec-07 $mn 2006 2006 2007E 2008E 2009E 2007E 2008E 2009E 2007E 2008E Russian comparable companies Transneft (RC estimates) Russia TRNFP.RTS USD 1,945 13,004 0.86 15 3.6 3.2 2.7 5.8 4.8 4.6 0.51 0.61 Transneft (consensus estimates) 3.9 4.0 3.5 5.2 5.1 4.6 0.4 0.4 Gazprom (RC estimates) Russia GAZP.RTS USD 13.5 316,898 2.37 20 (7*) 9.1 6.4 5.9 14.0 10.5 9.8 0.9 1.1 Gazprom (consensus estimates) 8.7 7.1 6.0 13.3 11.3 9.9 0.8 1.0 Cap-weighted average 2.31 20 8.9 6.3 5.8 13.7 10.2 9.6 0.9 1.1 International peer group Elia Belgium ELI.BR EUR 27.9 1,963 1.19 6 12.3 11.8 11.3 19.7 17.9 16.6 4.6 4.8 Red Electrica Spain REE.MC EUR 43.5 8,611 2.37 9 12.2 11.3 10.6 24.6 21.0 18.8 2.4 2.8 Terna Italy TRN.MI EUR 2.72 7,948 2.13 15 9.0 9.3 9.2 17.9 18.5 18.2 5.2 5.4 Transelectrica Romania TSEL.BX RON 36.7 902 1.34 12 9.3 n/a n/a 20.1 15.7 n/a n/a n/a Cap-weighted average 2.11 12 10.7 10.0 9.6 21.1 19.4 17.4 3.6 3.9 Transneft (disc)/prem to international peer group -59% 4% -67% -68% -72% -73% -75% -74% -3% -3% * gas transportation only

Source: Company Data, Thomson Financial, Renaissance Capital estimates

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

16

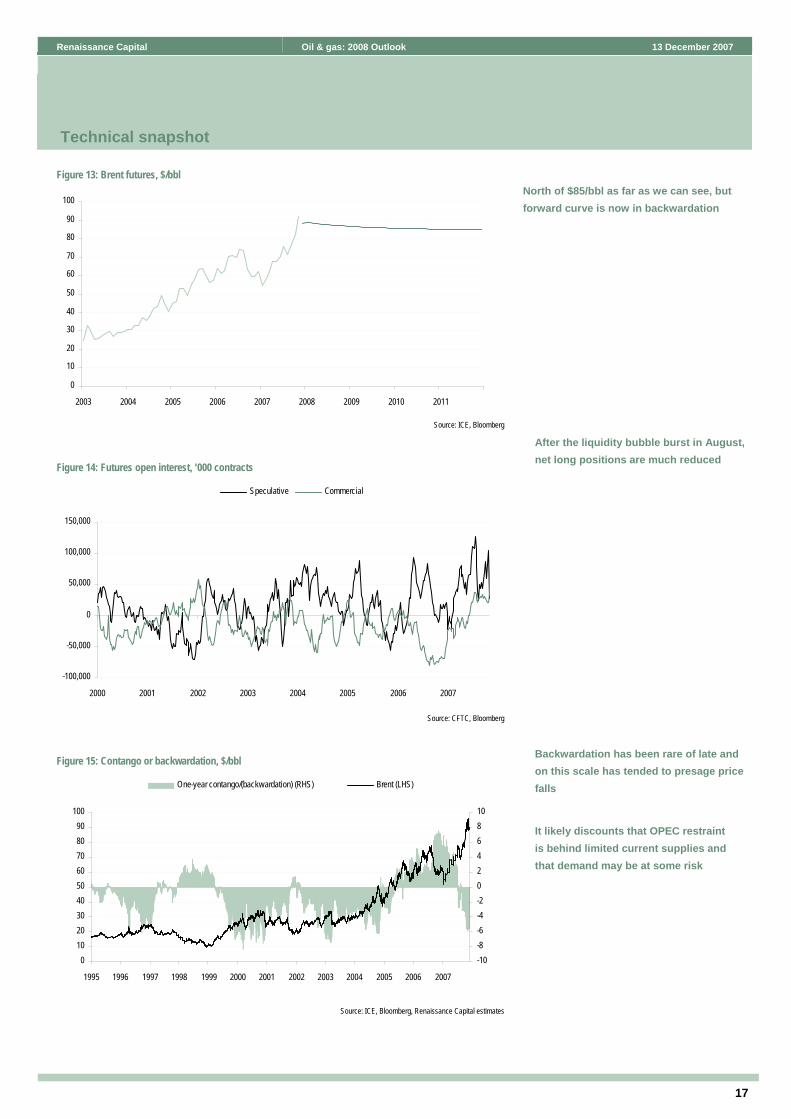

Why $100/bbl oil? We see many reasons why the crude markets have rallied this year, as supply and demand conditions have tightened. First, global economic growth has remained robust, and so has crude demand. Second, non-OPEC crude supply has been disappointing, making OPEC supply restraint dominant. Third, OECD inventories have seen severe unseasonal declines, and the trend looks decidedly downward. Fourth, worldwide refining bottlenecks, limited global (OPEC, mainly) spare production capacity and ongoing geopolitical risks have continued to seed doubts about supply availability.

What has not contributed? Rather importantly, activity in the futures markets does not seem to have played a major part in the August-December crude rally, although it was a significant contributor after the near-$50/bbl recent low episode that was seen in Jan 2007. Since August, commercial net long positions are flat while speculative net long interest has more than halved. On the other hand, we are uncertain as to whether the weaker US dollar is the cause or the effect of higher crude prices, but there is no denying that the directional correlation has been strong and OPEC, for better or for worse, has seemed more preoccupied with the exchange rate than with the crude price.

New paradigm Although inventories are falling, OECD crude inventories are adequate and days of forward cover reasonable. Crude prices remain unusually high given these conditions, signalling that there is still a large supply risk premium built into prices. Yet we see no reason for this to dissipate any time soon. Demand from developing economies remains robust, and will go on for quite some time. There are plenty of resources, but these are in the wrong (ie risky) locations. The call on OPEC thus grows over time. While we believe the cartel is focused on adding capacity, this is a slow process. Moreover, outside of OPEC, service cost inflation and the shift to unconventional supplies is forcing development costs upward.

Revised forecasts We still believe that we are in the midst of an extended oil cycle, although we accept that it will see considerably higher prices than previously anticipated and that the long-term oil price needed to deliver marginal supply has increased very significantly over recent years. Thus, our 2007 Brent forecast rises from $70 to $73/bbl (roughly the YtD average plus the price inferred from the futures strip). We are raising our 2008 forecast from $65/bbl to $75/bbl, and then foresee price declines of $5/bbl in each of the next three years. Given the state of the futures market, this continues to look conservative. Our long-term Brent model input (meaning from 2011 onward) rises from $50/bbl to $60/bbl, in nominal terms.

What are the risks? We think that crude prices could easily surpass $100/bbl on any threat to supplies. However, crude markets look equally vulnerable to a number of factors. First, slowing demand growth would certainly get OPEC’s attention. Signs point to slowing demand, surely the effect of the high prices. Second, financial interest remains net long while the scale of the current backwardation presages a sizeable price fall. Third, a reduction in geopolitical tensions would also hurt oil. Iraq has been quieter, and its crude output rising, while Israel and the Palestinian Authority are back in talking mode.

Oil price: fundamentals stronger…

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

17

Figure 13: Brent futures, $/bbl

0

10

20

30

40

50

60

70

80

90

100

2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: ICE, Bloomberg

Figure 14: Futures open interest, ‘000 contracts

-100,000

-50,000

0

50,000

100,000

150,000

2000 2001 2002 2003 2004 2005 2006 2007

Speculative Commercial

Source: CFTC, Bloomberg

Figure 15: Contango or backwardation, $/bbl

0102030405060708090

100

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

-10-8-6-4-20246810

One-year contango/(backwardation) (RHS) Brent (LHS)

Source: ICE, Bloomberg, Renaissance Capital estimates

Technical snapshot

North of $85/bbl as far as we can see, but forward curve is now in backwardation

After the liquidity bubble burst in August, net long positions are much reduced

Backwardation has been rare of late and on this scale has tended to presage price falls

It likely discounts that OPEC restraint is behind limited current supplies and that demand may be at some risk

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

18

Forecasts for crude demand in 2007 from the International Energy Agency (IEA), the US Department of Energy’s Energy Information Administration (EIA) and OPEC now foresee 1.3% growth (1.113mn bpd), somewhat lower than in September after upward reviews to 1H07 demand offset by lower expectations for 2H07. Growth of 1.9% (1.587mn bpd) is now foreseen for 2008. This larger growth mainly reflects the expectation of average winter weather conditions in contrast to the very mild ones experienced the last time around. We continue to believe that the 2008 forecasts are vulnerable to any global growth setback brought about by the financial market turmoil and demand destruction by high crude prices.

Non-OPEC supply growth estimates have remained stable over recent months, after expectations were lowered during the summer months. This leaves demand growth expectations amply exceeding forecast non-OPEC supply growth, in rather sharp contrast to the expectations in late 2006, although Angola joining OPEC earlier this year explains some of this phenomenon.

Current non-OPEC supply growth expectations are for 1.3% (0.667mn bpd) this year and 2.1% (1.037mn bpd) next year. FSU supply growth represents a huge 79% of the expected growth in 2007, meaning an optimistic 0.523mn bpd, in our opinion. Although the ratio is a more modest 49% of total non-OPEC supply growth in 2008, this still represents 0.503mn bpd, which seems a real stretch given trends in Russia and growing resource nationalism in the likes of Kazakhstan.

Taking the above demand and non-OPEC supply forecasts at face value, as well as IEA, EIA and OPEC forecasts of 4.1% (0.180mn bpd) growth in OPEC NGLs supply this year, and a striking, and therefore suspect, 10.2% (0.467mn bpd) in 2008, balanced markets require 0.9% (0.267mn bpd) more OPEC crude (and stock draws) in 2007 than in 2006, and a further 0.3% (0.083mn bpd) in 2008.

We note (from Figure 17) that OPEC’s own view of the market is less sanguine. Specifically, the cartel’s own numbers foresee a 0.3% (0.100mn bpd) higher call on OPEC and stocks in 2007 and 1.0% (0.300mn bpd) less in 2008, perhaps explaining its reluctance to increase production.

In summary, we believe that crude markets have tightened further over recent months and are now considerably more in OPEC’s control. End-2006 estimates of non-OPEC supply growth had set the stage for price weakness in 2007, but these conditions faded as the year advanced. OPEC looks in as much control in 2008, in spite of the wave of investment going into the global industry right now.

This is a very important issue, as shown in Figure 16. Arguably insufficient non-OPEC supply growth has been behind the price strength that has been seen over the past three years. These conditions are now expected to continue at least until 3Q08, assuming, of course, that bullish non-OPEC supply growth estimates for the second half of 2008 actually hold.

Supply/demand balance

19

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

Figure 16: Non-OPEC supply growth fails to meet demand growth, mn bpd

-2

-1

0

1

2

3

4

1Q04 3Q04 1Q05 3Q05 1Q06 3Q06 1Q07 3Q07 1Q08E 3Q08E

-10

0

10

20

30

Demand (mnbpd, LHS)Non-OPEC supply (mnbpd, LHS)Brent, $/bbl higher YoY (RHS)

Note: Non-OPEC production includes OPEC NGLs.

Source: IEA Monthly Oil Report, US DOE EIA’s Short Term Energy Outlook, OPEC Monthly Oil Market Report, Renaissance Capital estimates

Figure 17: World oil supply/demand balance, mn bpd 2006 2007E 2008E FY 1Q 2Q 3Q 4QE FYE 1QE 2QE 3QE 4QE FY Demand 84.6 85.7 84.6 85.4 87.2 85.7 87.7 86.0 86.8 88.7 87.3 IEA 84.7 85.8 84.7 85.3 87.1 85.7 88.2 86.5 87.2 88.9 87.7 US DOE 84.7 85.6 84.5 85.6 87.5 85.8 87.7 86.0 86.9 88.5 87.3 OPEC 84.5 85.8 84.6 85.4 87.0 85.7 87.3 85.6 86.4 88.6 87.0 Supply 84.7 84.7 84.7 84.8 86.2 85.0 87.3 87.3 87.9 92.2 87.8 Non-OPEC 49.4 50.1 50.0 49.7 50.5 50.1 51.0 50.8 50.9 55.0 51.1 IEA 49.5 50.4 50.1 49.6 50.4 50.1 51.4 51.0 50.9 61.5 51.2 US DOE 49.3 49.7 49.9 49.7 50.3 49.9 50.2 50.6 51.1 51.4 50.8 OPEC 49.4 50.3 50.0 49.8 50.8 50.2 51.3 50.8 50.8 52.1 51.3 Of which FSU 12.1 12.6 12.6 12.6 12.8 12.6 12.9 13.0 13.2 13.1 13.1 IEA 12.2 12.7 12.7 12.7 12.8 12.7 13.0 13.2 13.3 12.5 13.3 US DOE 12.2 12.6 12.6 12.5 12.8 12.6 12.8 12.9 13.2 13.3 13.0 OPEC 12.0 12.5 12.4 12.5 12.8 12.6 12.9 13.0 13.1 13.4 13.1 OPEC NGLs 4.4 4.5 4.5 4.6 4.7 4.6 4.8 4.9 5.1 5.3 5.0 IEA 4.6 4.8 4.8 4.8 5.0 4.8 5.1 5.3 5.5 5.8 5.4 US DOE 4.5 4.6 4.5 4.5 4.6 4.5 4.7 4.7 4.9 5.0 4.8 OPEC 4.1 4.2 4.3 4.4 4.6 4.4 4.7 4.8 4.9 5.1 4.9 OPEC crude 30.8 31.1 30.1 31.2 32.0 31.1 31.9 30.3 30.8 28.3 31.2 IEA 30.6 30.6 29.8 30.9 31.7 30.8 31.7 30.2 30.8 21.6 31.1 US DOE 30.9 31.4 30.1 31.4 32.6 31.4 32.8 30.7 30.9 32.0 31.6 OPEC 31.0 31.3 30.3 31.2 31.6 31.1 31.3 30.0 30.7 31.4 30.8 Call on OPEC crude and stocks 30.9 30.0 30.1 30.5 31.0 30.4 31.5 31.5 31.8 31.9 31.7 IEA 31.1 30.2 30.2 30.6 - - - - - - - US DOE 30.8 29.9 30.1 30.4 31.0 30.4 31.5 31.5 31.8 31.9 31.7 OPEC 30.9 30.0 30.1 30.5 - - - - - - - Stock-build/(draw) 0.1 (1.1) 0.1 (0.7) (1.6) (1.0) (1.3) 0.8 0.9 (0.1) 0.1 IEA 0.5 (0.4) 0.4 (0.3) - - - - - - - US DOE (0.1) (1.4) (0.0) (1.0) (1.6) (1.0) (1.3) 0.8 0.9 (0.1) 0.1 OPEC (0.1) (1.3) (0.2) (0.7) - - - - - - - Notes: The IEA and OPEC numbers do not project OPEC crude supply. Processing volumetric gains, losses and biofuels are included in non-OPEC supply.

Source: IEA Monthly Oil Report, US DOE EIA’s Short Term Energy Outlook and OPEC Monthly Oil Market Report, all from Nov 2007

Non-OPEC cannot meet demand growth.

Prices rise!

Non-OPEC cannot meet demand growth.

Prices rise!

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

20

OPEC’s compliance (Figure 18) slipped somewhat following the Oct 2006 and Feb 2007 production ceiling (quota) reductions, but it has remained very good by historical standards. OPEC has been highly disciplined of late, in our opinion.

Figure 18: OPEC output, mn bpd

-5

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007

Non-compliance OPEC Ex -Iraq and ex -Angola Quota

Source: Bloomberg, Renaissance Capital estimates

Meanwhile, the supply/demand balance portrayed in Figure 17 indicates that OPEC’s production would have to increase fairly substantially from 3Q07 levels in order to keep crude markets in balance in 4Q07 and 1Q08, when there is a seasonal upswing in demand due to the onset of winter in the northern hemisphere. The call on OPEC crude (and stocks) is anticipated to rise by 0.8mn bpd between 3Q07 and 4Q07. Normally, this is partly met with a stock-draw offsetting-inventory build in 2Q and 3Q of the year. This time around, however, 3Q closed with a large and unseasonal stock draw of around 0.7mn bpd, according to forecasts from the IEA, EIA and OPEC.

Against this background, OPEC convened in Vienna on 11 Sep 2007 and agreed to increase the production ceiling (excluding Iraqi and Angolan output) by 0.5mn bpd from 1 Nov 2007. OPEC explained the move by the higher needs in the winter season. OPEC also alluded to the shift of the forward market into backwardation around that time, which would imply a further reduction in stocks, and that higher supplies would alleviate this.

However, OPEC observed in its September communiqué that output increases in prior years had led to comfortable inventory levels, especially of crude. We tend to concur with this view. In addition, OPEC noted the ongoing tightness in the US products market and acknowledged that this continued to affect the level of product stocks and prices. The cartel’s view on this is long established. Basically, the failure of customers (and implicitly their governments) to encourage downstream investment is not the cartel’s problem to fix. Many in the market judged the September quota increase to be insufficient and crude markets rallied in the aftermath.

More recently, as crude prices retreated from near $100/bbl, hurt by worries about global growth, OPEC's decision to leave output unchanged at its 5 Dec 2007 meeting in Abu Dhabi provided strong short-term support for oil prices‚ in our view.

OPEC watch

21

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

Crude markets came off the boil in the latter stages of 2006, and they started 2007 on a rather weak note. We think these price setbacks were a delayed response to faltering demand as well as lower geopolitical tensions.

We actually believe that the principal driver was a rise in oil inventories. Both US inventories, which are regularly reported and tracked, and OECD ones (shown in Figure 19 and Figure 20, respectively) trended upward from early 2003 through mid-2006.

Since then, however, inventories have contracted due to the upswing in demand into the winter season, non-OPEC supply growth faltering and OPEC restraining supply. This trend will continue through 1Q08, at the very least.

Figure 19: US inventories and total product supply

600

650

700

750

800

850

1990 1992 1994 1996 1998 2000 2002 2004 2006

14

15

16

17

18

19

20

21

22

Inventories (LHS, mn bbls) Supply (RHS, mn bpd)

Source: US Department of Energy’s EIA, Renaissance Capital estimates

Figure 20: OECD stocks and forward demand cover

3,600

3,700

3,800

3,900

4,000

4,100

4,200

4,300

1990 1992 1994 1996 1998 2000 2002 2004 2006

70

75

80

85

90

95

100

OECD stocks (LHS, mn bbls) Days of forward cover (RHS)

Source: US Department of Energy’s EIA, Renaissance Capital estimates

Inventories falling

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

22

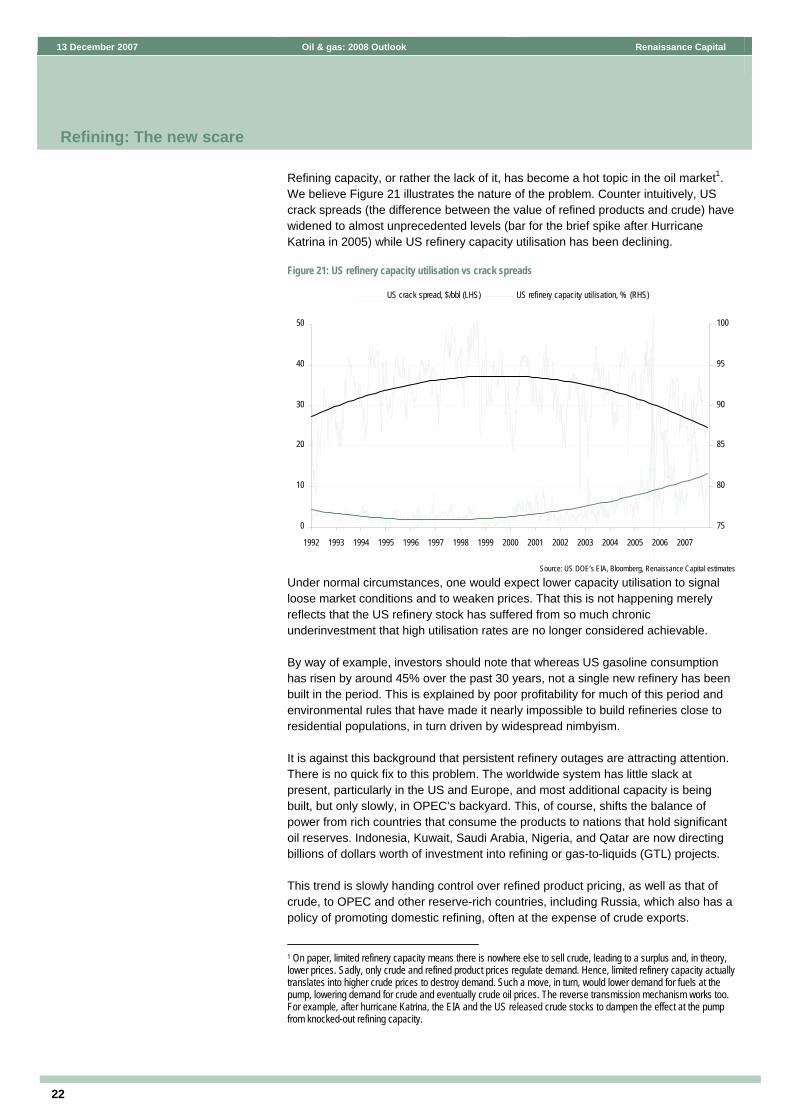

Refining capacity, or rather the lack of it, has become a hot topic in the oil market1. We believe Figure 21 illustrates the nature of the problem. Counter intuitively, US crack spreads (the difference between the value of refined products and crude) have widened to almost unprecedented levels (bar for the brief spike after Hurricane Katrina in 2005) while US refinery capacity utilisation has been declining.

Figure 21: US refinery capacity utilisation vs crack spreads

0

10

20

30

40

50

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

75

80

85

90

95

100

US crack spread, $/bbl (LHS) US refinery capacity utilisation, % (RHS)

Source: US DOE’s EIA, Bloomberg, Renaissance Capital estimates

Under normal circumstances, one would expect lower capacity utilisation to signal loose market conditions and to weaken prices. That this is not happening merely reflects that the US refinery stock has suffered from so much chronic underinvestment that high utilisation rates are no longer considered achievable.

By way of example, investors should note that whereas US gasoline consumption has risen by around 45% over the past 30 years, not a single new refinery has been built in the period. This is explained by poor profitability for much of this period and environmental rules that have made it nearly impossible to build refineries close to residential populations, in turn driven by widespread nimbyism.

It is against this background that persistent refinery outages are attracting attention. There is no quick fix to this problem. The worldwide system has little slack at present, particularly in the US and Europe, and most additional capacity is being built, but only slowly, in OPEC’s backyard. This, of course, shifts the balance of power from rich countries that consume the products to nations that hold significant oil reserves. Indonesia, Kuwait, Saudi Arabia, Nigeria, and Qatar are now directing billions of dollars worth of investment into refining or gas-to-liquids (GTL) projects.

This trend is slowly handing control over refined product pricing, as well as that of crude, to OPEC and other reserve-rich countries, including Russia, which also has a policy of promoting domestic refining, often at the expense of crude exports.

1 On paper, limited refinery capacity means there is nowhere else to sell crude, leading to a surplus and, in theory, lower prices. Sadly, only crude and refined product prices regulate demand. Hence, limited refinery capacity actually translates into higher crude prices to destroy demand. Such a move, in turn, would lower demand for fuels at the pump, lowering demand for crude and eventually crude oil prices. The reverse transmission mechanism works too. For example, after hurricane Katrina, the EIA and the US released crude stocks to dampen the effect at the pump from knocked-out refining capacity.

Refining: The new scare

23

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

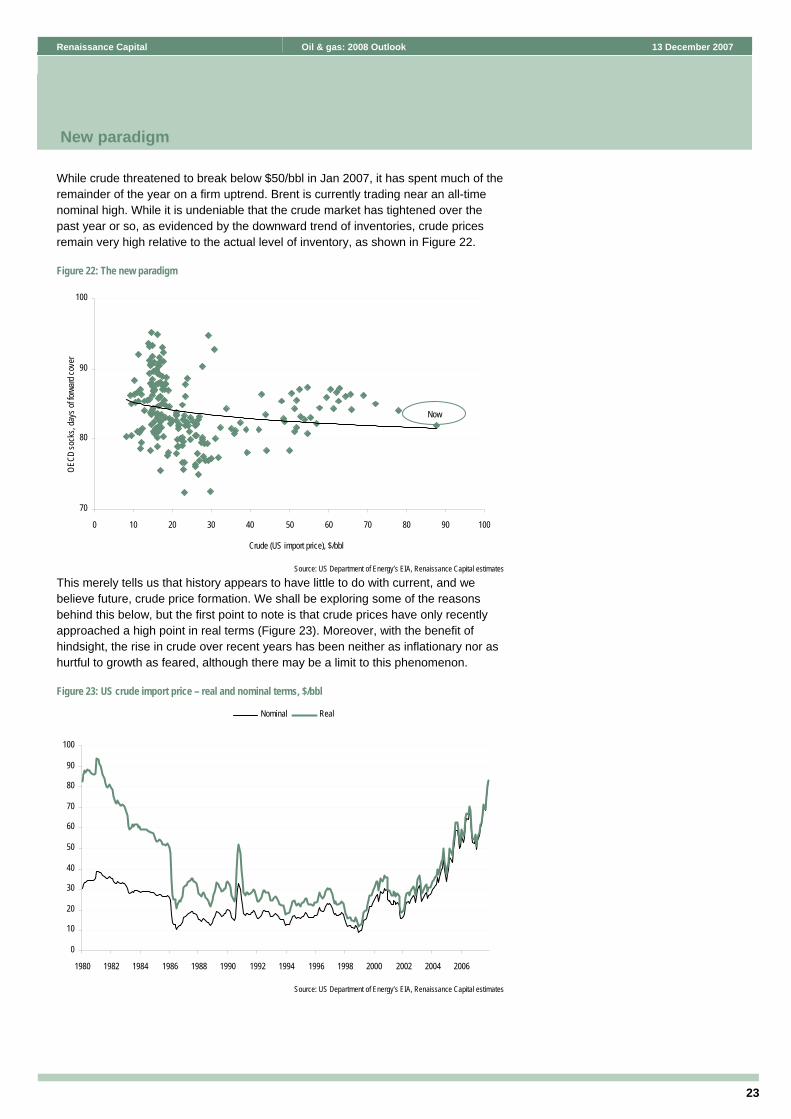

While crude threatened to break below $50/bbl in Jan 2007, it has spent much of the remainder of the year on a firm uptrend. Brent is currently trading near an all-time nominal high. While it is undeniable that the crude market has tightened over the past year or so, as evidenced by the downward trend of inventories, crude prices remain very high relative to the actual level of inventory, as shown in Figure 22.

Figure 22: The new paradigm

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100

Crude (US import price), $/bbl

OECD

sock

s, da

ys of

forw

ard co

ver

Now

Source: US Department of Energy’s EIA, Renaissance Capital estimates

This merely tells us that history appears to have little to do with current, and we believe future, crude price formation. We shall be exploring some of the reasons behind this below, but the first point to note is that crude prices have only recently approached a high point in real terms (Figure 23). Moreover, with the benefit of hindsight, the rise in crude over recent years has been neither as inflationary nor as hurtful to growth as feared, although there may be a limit to this phenomenon.

Figure 23: US crude import price – real and nominal terms, $/bbl

0

10

20

30

40

50

60

70

80

90

100

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

Nominal Real

Source: US Department of Energy’s EIA, Renaissance Capital estimates

New paradigm

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

24

Demand is rising, fuelled by developing economies

Figure 24 through Figure 26 show the inexorable rise of crude demand from developing economies. This phenomenon will continue for a considerable period of time, we believe.

Figure 24: Demand, mn bpd

0

10

20

30

40

50

60

1965 1970 1975 1980 1985 1990 1995 2000 2005

Non-OECD OECD

Source: US Department of Energy’s EIA

Figure 25: Share of demand, %

0

10

20

30

40

50

60

1965 1970 1975 1980 1985 1990 1995 2000 2005

Non-OECD OECD

Source: US Department of Energy’s EIA

Figure 26: Demand growth, % YoY

-8-6-4-202468

1012

1965 1970 1975 1980 1985 1990 1995 2000 2005

Non-OECD OECD

Source: US Department of Energy’s EIA

Global production capacity is limited

OPEC, which holds the world’s entire spare crude production capacity, has been operating at 90%-plus utilisation rates since 2003. This leaves very little room for error should non-OPEC supply falter through project delays or accidents, or OPEC supply be disrupted or held back due to internal strife (eg Nigeria), policy malaise (eg Venezuela or Iran) or geopolitical risks (eg affecting the whole of the Middle East, we would say). While spare capacity is forecast to rise this year and next, it will remain low in absolute terms. This calls for a continuing risk premium in crude markets.

Figure 27: OPEC capacity utilisation

75%

80%

85%

90%

95%

100%

2000 2001 2002 2003 2004 2005 2006 2007

Source: Bloomberg

Figure 28: Global spare crude production capacity, mn bpd

0

1

2

3

4

5

6

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007E2008E

Source: US Department of Energy’s EIA

25

Renaissance Capital Oil & gas: 2008 Outlook 13 December 2007

Resources overall are adequate, but in the wrong kind of place

We do not have much time for Malthusian peak-oil theories. Any focus on discoveries vs demand can lead to such concerns, but these views disregard the effect of economics and technology on reserves. Bearing these two factors in mind, which Figure 29 does, the world’s reserve-to-production ratio has undoubtedly kept up with the relentless rise in demand.

Figure 29: Global reserve additions (bn bbls) and R/P ratio (years)

0

50

100

150

200

250

1980 1985 1990 1995 2000 2005

0

5

10

15

20

25

30

35

40

45

50

Reserve additions Production R/P ratio (RHS)

Source: BP Statistical Review of World Energy, June 2007, US Department of Energy’s EIA, Renaissance Capital estimates

Having said the above, the lion’s share of global reserves is held by OPEC, with most (55%) concentrated in the Middle East. To many, this is a source of systemic supply risk. Moreover, while the economic ‘proving’ of Canada’s oil sands boosted the non-OPEC share, these resources are costly to develop and slow to produce.

Figure 30: Reserves location, %

0%

20%

40%

60%

80%

100%

1980 1985 1990 1995 2000 2005

OPEC Non-OPEC

Source: US Department of Energy’s EIA

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

26

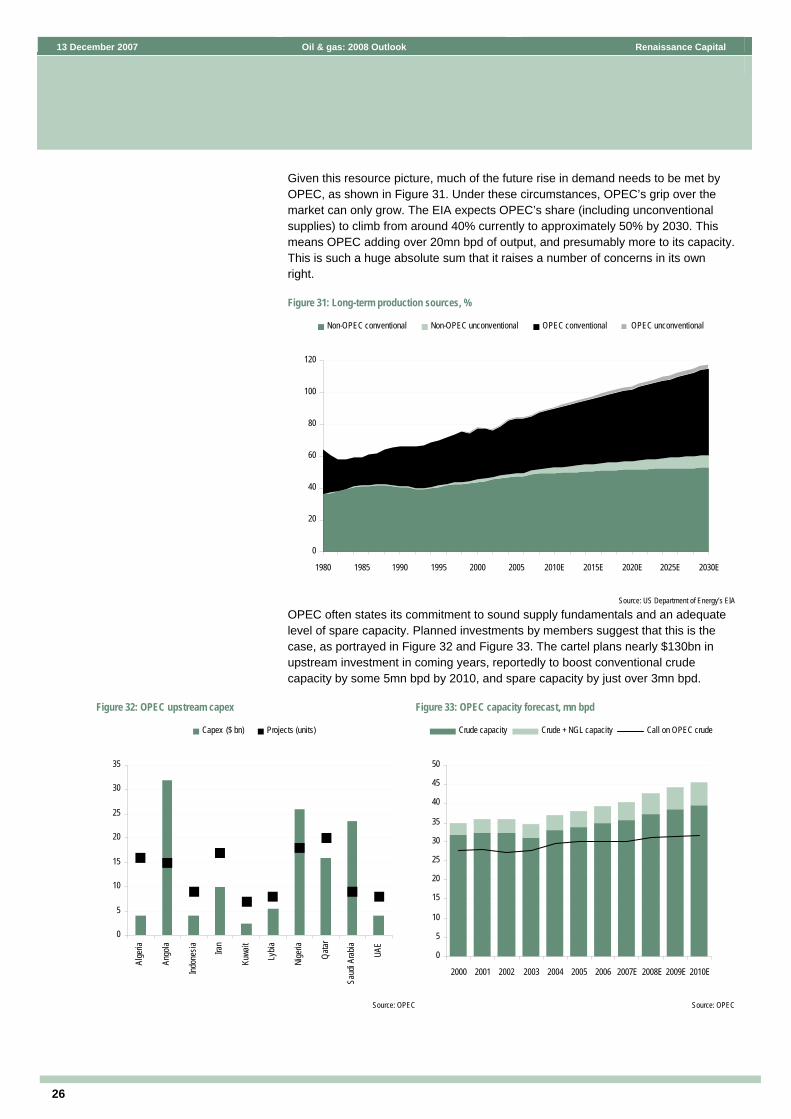

Given this resource picture, much of the future rise in demand needs to be met by OPEC, as shown in Figure 31. Under these circumstances, OPEC’s grip over the market can only grow. The EIA expects OPEC’s share (including unconventional supplies) to climb from around 40% currently to approximately 50% by 2030. This means OPEC adding over 20mn bpd of output, and presumably more to its capacity. This is such a huge absolute sum that it raises a number of concerns in its own right.

Figure 31: Long-term production sources, %

0

20

40

60

80

100

120

1980 1985 1990 1995 2000 2005 2010E 2015E 2020E 2025E 2030E

Non-OPEC conventional Non-OPEC unconventional OPEC conventional OPEC unconventional

Source: US Department of Energy’s EIA

OPEC often states its commitment to sound supply fundamentals and an adequate level of spare capacity. Planned investments by members suggest that this is the case, as portrayed in Figure 32 and Figure 33. The cartel plans nearly $130bn in upstream investment in coming years, reportedly to boost conventional crude capacity by some 5mn bpd by 2010, and spare capacity by just over 3mn bpd.

Figure 32: OPEC upstream capex

0

5

10

15

20

25

30

35

Alge

ria

Ango

la

Indon

esia Iran

Kuwa

it

Lybia

Nige

ria

Qatar

Saud

i Arab

ia

UAE

Capex ($ bn) Projects (units)

Source: OPEC

Figure 33: OPEC capacity forecast, mn bpd

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007E 2008E 2009E 2010E

Crude capacity Crude + NGL capacity Call on OPEC crude

Source: OPEC

27

Renaissance Capital Oil & Gas 13 December 2007

Cost of adding production is rising

The rising cost of development is a source of great concern. Capital costs, alongside taxes, are among the most significant expenses borne by the industry. Figure 34 portrays three-year averages for unit finding and development costs (F&DC, measured in dollars of capital spent to prove a barrel of oil equivalent). For the super-majors, they more than quadrupled between 2000 and 2006.

Figure 34: Three-year finding and development cost, $/boe

0

2

4

6

8

10

12

14

16

18

20

2000 2001 2002 2003 2004 2005 2006

Super-majors Russian companies Other GEM oils

Source: Companies’ US GAAP SFAS No. 69 disclosures, Renaissance Capital estimates

High service price inflation is mainly to blame for rising F&DC, although ever-more challenging geology is a factor too. In addition, the growing role of unconventional oil is also adding to the cost of replacing production. Figure 35 shows this. It excludes deep offshore plays as nowadays these are considered a conventional source.

Figure 35: Growing non-conventional supply, mn bpd

0

2

4

6

8

10

12

1980 1990 2000 2004 2010E 2015E 2020E 2025E 2030E

Canadian oil sands Ultra-heavy crudes Biofuels Coal-to-liquids Gas-to-liquids Other

Source: US Department of Energy’s EIA

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

28

Crude production

Russia’s crude production turned very disappointing in 2007, with our growth forecasts having been cut twice to the current level of 2.3% (from 3.7% at the start of the year). This was mainly driven by a delayed drilling campaign in 1Q07, when unusually warm weather held back winter-road building, pad construction and rig mobilisation. We had hoped for performance to catch up subsequent to this, but the renewed vigour of development-drilling metrics, up 22% YoY through September (last reported), appears to have had little visible effect on output from Russia’s core producing basins. Excluding the Sakhalin projects and Rosneft’s upstream assets, the daily crude output growth from the remaining VICs was fairly insignificant or even negative YoY since May. Preliminary output figures for November indicated further deterioration of the YoY growth rate which shrank to merely 0.9%, while December is normally a modest down month as Sakhalin-2 closes for winter. For 2007 as a whole, we forecast Russia will produce 491.4mnt (or 9.828mn bpd), representing 0.4% YoY growth from Russia’s core producers, with the ramp-up of production at Sakhalin-1 earlier in the year contributing the rest.

We do not expect the reverse of this trend in 2008. Spending remains focused on greenfield projects, which should take some time to contribute. On current trends we expect Russia to be producing flat to less crude YoY through Apr 2008, with some seasonal recovery thereafter. However, as we expect no growth at all for the core producers next year, we forecast Russia’s overall crude output growth in 2008 of just 0.5% YoY, measured in tonnes, and 0.2% YoY in bpd terms, once adjusted for leap year effects. We believe this Russian supply outturn is considerably weaker than current market thinking.

Figure 36: Russian crude production growth, % YoY

-2

0

2

4

6

8

10

12

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: InfoTEK, Reuters, Renaissance Capital estimates

The Central Asian and Caspian region has been outperforming Russia in terms of production growth over 2005-2006. In our view, 2007 will not be an exception with estimated production growth of 12.4% to 125.6mnt (2.5mn bpd), accelerating further by 16.5% in 2008 to 146.3mnt.

Fundamentals watch

29

Renaissance Capital Oil & Gas 13 December 2007

Azerbaijan has been the largest single contributor to this growth with the 2007 increase forecast at 30% fuelled by Azerbaijan International Operating Company (AIOC) and its largest project Azeri-Chirag-Guneshli. Kazakhstan lagged behind with just 3.9%, 5.5% and 5.1% production growth in 2005, 2006 and 2007, respectively. From 2008, however, we expect production in Kazakhstan to start growing with double-digit rates mainly due to the ramp-up of the Tengiz and Karachaganak fields. Kashagan is to contribute from 2010 only, in our view.

Turkmenistan has been a marginal producer until recently but promises to catch up quickly, reaching a 2.5x increase over the next decade. The major hopes rest on offshore development, the Yeloten group of fields, and the implementation of enhanced recovery methods, still quite underutilised in the country. Uzbekistan is unlikely, in our view, to demonstrate any liquids production growth in the next 10 years, given its traditional focus on gas resources and limited liquids opportunities.

Ukraine remains a marginal producer with future growth rates likely to fall given an unfriendly taxation regime, in our view.

Figure 37: Central Asia crude production, mnt

0.0

50.0

100.0

150.0

200.0

250.0

1996 1999 2002 2005 2008 2011 2014

0

5

10

15

20

Kazakhstan, RHS Turkmenistan, RHS Azerbaijan, RHS

Uzbekistan, RHS growth % , LRS

Source: Renaissance Capital estimates

Figure 38: Ukraine crude production, mnt

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Ukraine, RHS growth % , LHS

Source: Renaissance Capital estimates

Investment-led growth

Figure 36 provides a clear indication that Russia’s so-called brownfield miracle has been exhausted. This means that the ratio of mature and highly depleted reserves is increasing, as is the ratio of hard-to-recover reserves. While crude and gas production from brownfield assets will continue to be the largest contributor to overall production for the foreseeable future, the transition from brownfield to greenfield is evidently happening.

These newer developments incorporate much improved capital inputs, entailing higher capital spending by producers, while the growing maturity of the brownfields

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

30

sites, as well as regulatory pressure to lower the idle well stock, also call for increased capital costs associated with maintaining production.

Figure 39: Upstream capital spending by Russian VICs, $mn

-

2,000

4,000

6,000

8,000

10,000

12,000

2005 2006 9m 2007

Drilling capex Other capex

Source: NGV, Neftyanaya Torgovlya, Renaissance Capital estimates

The capex spend of Russia’s main VICs expanded 37% in the first nine months of 2007, following the growth of some 45% in the whole of last year. This translated to around $1.2bn/month of upstream capital spending, including $0.5bn/month of drilling capex. Although this is partially driven by firmer pricing, there is also a strong volume pick-up. Specifically, development drilling footage for VICs rose 22% in first nine month of 2007, while exploration drilling increased 26% in the same period (vs 26% and 17% FY06 growth, respectively).

Figure 40: Exploration and development drilling volumes by Russian VICS, km

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2005 2006 9m 2007

Development drilling Ex ploration drilling

Source: NGV, Neftyanaya Torgovlya, Renaissance Capital estimates

31

Renaissance Capital Oil & Gas 13 December 2007

We expect this trend for accelerated capital spending to continue in 2008, in part fuelled by high commodity prices, but also administrative support for the development of the new frontier regions (such as East Siberia) via fiscal incentives.

We also see development drilling growth all over the Central Asia/Caspian region and Ukraine. In Kazakhstan the trend is not as strong as in Turkmenistan (where a significant part of drilling is for gas rather than oil). Aggressive drilling growth in Turkmenistan, we believe, will help to deliver sizable growth in the near future, while Kazakhstan and Azerbaijan are switching towards productivity improvement rather than pure expansion. In exploration drilling, the story looks different with Ukraine lacking the incentives to invest and Azerbaijan focusing on production growth but not reserves replacement.

Figure 41: Drilling (km) and production in Kazakhstan

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07

1.000

1.100

1.200

1.300

1.400

ex ploration development production, mn bpd

Source: RPI, InfoTEK, NGV

Figure 12: Drilling (km) and production in Ukraine

0

50

100

150

200

250

300

2004 2005 2006 2007E

0.08

0.08

0.08

0.08

0.09

0.09

0.09

0.09

0.09

ex ploration development production, mn bpd

Source: RPI, InfoTEK, NGV

Figure 43: Drilling (km) and production in Azerbaijan

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2000 2001 2002 2003 2004 2005 2006

0.20

0.30

0.40

0.50

0.60

0.70

0.80

ex ploration development production, mn bpd

Source: RPI, InfoTEK, NGV

Figure 44: Drilling (km) and production in Turkmenistan

0

50,000

100,000

150,000

200,000

250,000

300,000

1999 2000 2001 2002 2003 2004 2005

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

ex ploration development production, mn boepd

Source: RPI, InfoTEK, NGV

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

32

Crude netback parity

Following the fiscal incentive to refine that was introduced in Russia in Aug 2004, when crude export duties shot up, the traditional crude export premium has disappeared. In fact, crude export margins (vs wellhead sales) have been negative for most of 2006, but have since grown significantly (reaching nearly $10/bbl last month). We associate this recent strength with the time-lag on export duties, which has a temporary positive effect on export margin when the oil price is rising, and we do not think this will be sustained. Domestic refining margins remain very strong with both diesel and gasoline trading at 5-20% premiums to export netbacks, as is the export margin on fuel oil (Figure 45), increasing the attractiveness of local refining vs crude exports. This is an area of some concern, as either market forces (more products staying at home) or political interference (either via coercion or raising product export duties) could adversely affect these rather benign trading conditions.

Figure 45: Russia: Oil products netbacks

(35)

(30)

(25)

(20)

(15)

(10)

(5)

0

5

10

15

Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07

Gasoline Diesel Fuel o il

Source: Renaissance Capital estimates

None of the Central Asia/Caspian crude-long countries has a domestic market for crude oil. Domestic product prices are normally regulated, and state-controlled companies are burdened with the duty to supply local refineries at prices, which are significantly below international netbacks. We do not envisage this will change any time soon.

Ukraine, however, is different with regular crude oil auctions allowing Ukrainian producers to sell oil at unregulated domestic prices. For most of 2005, this was trading at a premium to the price that Ukrainian refineries paid for Russian crude (see Figure 46). From Nov 2005, however, this started to change as a result of decreased demand from local refineries, some of which closed for modernisation or signed direct crude delivery contracts with Central Asian producers.

33

Renaissance Capital Oil & Gas 13 December 2007

Figure 46: Ukrainian domestic crude market trends, $/bbl

25

30

35

40

45

50

55

60

65

70

75

80

Dec-04 Mar-05 Jun-05 Sep-05 Dec-05 Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07

Urals (Ukraine) Auction price

Source: Petroleum Argus, UKRSE, UICE, Renaissance Capital estimates

13 December 2007 Oil & gas: 2008 Outlook Renaissance Capital

34

Oil taxation in Russia

The lacklustre performance of the Russian oil stocks over the past 12 months – which saw the oil price growing 42% and the Bloomberg World Oil and Gas Index appreciating 21% – is widely attributed to the specifics of the Russian oil taxation system, which makes pure upstream producers fairly insensitive to the oil price. We estimate that at $100/bbl oil, marginal tax amounts to 90% (split as 22% UNRPT, 65% export duty and 3% income tax), significantly reducing the incentives for incremental investments upstream. However, vertically integrated companies benefit from higher oil prices disproportionately, as the Russian refining margin is directly linked to the oil price (via the tax subsidy on the export of oil products). We estimate that the average gross refining margin in Russia will be $16.4/bbl in 2008 (using a $75/bbl Brent), and that it would go up to $19.3/bbl under the $85/bbl oil price assumption. Most of this growth is related to the tax subsidy on the export of fuel oil, thus reducing the incentives for the oil companies to increase the refining depth.