nuclear fleet approach 121112 - pwc uk blogs · the report was commissioned by areva, and...

TRANSCRIPT

www.pwc.co.uk

The fleet effect:

The economic benefits ofadopting a fleet approachto nuclear new build inthe UK

November 2012

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC Contents

Contents

1. Introduction 4

2. Executive summary 5

3. The energy challenge 7

4. Approach and methodology 12

5. Enhanced certainty 16

6. Reduced cost of UK nuclear new build 19

7. Enhanced local content of UK nuclear new build 21

8. Reduced cost of electricity to consumers 25

9. Longer term benefits of strengthened UK industrial base 28

10. Risks associated with a nuclear fleet and their mitigation 30

11. Conclusions 33

Appendices 34

Appendix A: Model structure, data sources and assumptions 35

Appendix B: Model results and sensitivity analysis 39

Appendix C: Summary of EMR 44

Appendix D: References 45

Appendix E: Acronyms 47

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 2

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 3

Acknowledgements

The report was commissioned by Areva, and independently researched and written by PwC, with theparticipation of the following companies:

Nuclear supply chain companiesAreva S.A. Nuclear Engineering Services Limited

WS Atkins Plc Rolls Royce Plc

BAE Systems Plc Sheffield Forgemasters International Ltd

Balfour Beatty Plc Siemens AG

Bendalls Engineering Siempelkamp Nukleartechnik GmbH

Clyde Union Ltd Sir Robert McAlpine Ltd

Costain Group Plc SPX Balcke Duerr GmbH

Darchem Engineering Ltd Sulzer Pumps Ltd

Delta Controls Ltd Ultra Electronics Limited

Doosan Babcock Ltd Wellman Booth

Eaton Electric Ltd Wier Group Plc

Flowserve Corporation Wyman Gordon Ltd

Independent Forgings and Alloys Limited

UK nuclear stakeholdersNational Nuclear Skills AcademyDepartment of Energy and Climate Change (DECC)Department for Business, Innovations and Skills (BIS)

Third party reportsWe reviewed over 50 studies and articles on the nuclear and wider energy sector that addressed issues ofrelevance to our report including the development of national supply chains, economics of generation, policydrivers, skills requirements and the global nuclear sector. These are listed in Appendix D.

DisclaimerThis publication has been prepared for general guidance on matters of interest only, and does not constituteprofessional advice. You should not act upon the information contained in this publication without obtainingspecific professional advice. No representation or warranty (express or implied) is given as to the accuracy orcompleteness of the information contained in this publication, and, to the extent permitted by law,PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability,responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in relianceon the information contained in this publication or for any decision based on it.

© 2012 PricewaterhouseCoopers LLP. All rights reserved. In this document, ‘PwC’ refers toPricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom), which is a member firmof PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 4

It is the context of major change within the electricitysector and Government focus on economic growththat characterises the landscape within whichPricewaterhouseCoopers LLP (PwC) has undertaken astudy on the benefits to UK industry of adopting afleet approach to nuclear new build.

Our report addresses whether there are advantages toadopting a fleet approach to a nuclear new buildprogramme through the use of a single technology. Itaddresses whether these advantages can bedemonstrated through increases in sustainablemanufacturing and construction jobs, investment infacilities and skills development in the nuclear supplychain, and in wider economic benefits1. We considerthe extent to which it is possible to identify theadditional benefits from a fleet approach due tolearning and sharing of best practice, optimisingstrategic stocks of components, staff utilisation andthe economics of seeking regulatory approvals. Weassess the potential for these benefits to flow throughto a lower cost of electricity for consumers andincreased export opportunities for the supply chain.

At the outset, it is important to define what we meanby a fleet approach to nuclear new build. For thepurposes of our analysis, we define a fleet approach ashaving two key characteristics: all the nuclear reactorsrely on a common reactor technology and all have acommon design of the associated Conventional Island(CI) and the Balance of Plant (BOP). For simplicity,we consider a new nuclear portfolio from a minimumof four reactors up to eight reactors (which operate asfour pairs), assumed to be built at regular intervals inthe period to 2030. Our definition of the fleet does notassume either a common commercialmodel/operating consortia structure or a commonowner/operator.

1 Throughout the report we do not refer to specific sites for nuclearnew build but assume all sites that have been nominated for newnuclear power stations could potentially be utilised up to 2030.

Our report:

provides an overview of the context underpinningour study;

summarises the approach taken to investigatingour hypothesis and the methodology adopted forour model;

outlines the benefits of a fleet approach to newnuclear build;

considers the impact of a fleet approach on the UKnuclear supply chain through enhanced certainty;

discusses the impact of how a new nuclear fleetcan reduce the cost of UK nuclear new build;

describes the fleet impact on the local content ofUK nuclear new build;

assesses the impact of a new nuclear fleet on thecost of electricity to consumers;

describes the impact of a fleet approach on the UKindustrial base;

discusses the risks associated with a nuclear fleetapproach and their mitigation;

summarises the conclusions reached; and

provides further details regarding themethodology, references and acronyms in theappendices.

1. Introduction

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 5

2.1. IntroductionPricewaterhouseCoopers LLP (PwC) has undertaken astudy to assess the potential benefits to the UKeconomy of adopting a fleet approach to nuclear newbuild. For the purposes of this report, a ‘fleet’ isdefined as two or more pairs of reactors which rely onthe same reactor technology and common design ofthe CI and BOP. We consider fleet sizes of four, sixand eight reactors and our data ranges refer to fleetsizes from four to eight reactors.

We studied the benefits of a fleet approach to newnuclear build compared to diversified reactortechnologies over the period to 2030 by looking at:

the importance of certainty for the UK’s supplychain and the impact of a fleet effect on it;

the advantages in terms of investment in the UKindustrial base and the economic benefits to theUK; and

the benefits that a fleet effect can deliver toelectricity users through reduced costs.

We examined implications for the supply chain of afleet approach, pre-requisites for investmentdecisions and impacts on companies further down thesupply chain. We interviewed 26 companies fromacross the nuclear supply chain as well as key nuclearstakeholders and used the outcomes in developing aneconomic model to quantify the benefits. Our modelconsidered direct, indirect and induced effects of afleet approach and expressed them in terms of theirimpact on both jobs and GDP. We developed a rangeof scenarios to assess the robustness of our analysis,based on the key drivers of cost, timescales, UKcontribution and certainty.

Our report does not consider the technical capabilitiesof different reactor types, but focuses on genericreactors that would be built in pairs on a single site.We assume that these generic reactors would meet therequirements of the Generic Design Assessment(GDA) process. We do not address cost differentialsbetween generic reactor types but assume that costsremain constant for a non-fleet approach so that wefocus on the incremental benefits of a fleet approach.

Current investment plans based on the acquisition ofnuclear licensed sites suggest that there could be up toeight reactors (ignoring differences in capacity acrosstechnologies) across four sites providing up to13.2GW of additional capacity by 2030. Adopting afleet approach to new nuclear build could provide theUK with three additional key benefits which wouldnot otherwise be realised through nuclear new build.

2.2. CertaintyA strong theme throughout the study is the urgentneed for much greater certainty on the make-up of theUK’s nuclear programme. Without certainty of timingand volume, companies are reluctant to invest in thefacilities, training and accreditation necessary toparticipate in new nuclear. Commitment to a fleet isseen as a key factor underpinning investmentdecisions and one of the most important levers inrevitalising and enhancing the UK’s nuclear supplychain. At present many smaller firms with thecapability to deliver in the nuclear supply chain areopting to apply their capabilities to other sectors suchas oil and gas, where the barriers to entry are lowerand the certainty of orders is greater. This leakage oftop end skills and experience, starting from arelatively low base given the period since the UK’s lastnuclear build project, is damaging the UK’s industrialbase. The impact of certainty is quantified within theeconomic model that underpins this report.

2.3. Strengthened industrialbase

The lack of recent experience of large scale newnuclear build in the UK suggests that UK basedsuppliers would provide only a limited share of theengineering and manufacturing inputs required for asingle pair of reactors since the expertise and therelationships would be largely with non-UK supplychain companies. With a fleet approach, however, thescope for increasing the UK content becomes easier toidentify and more commercially viable. In addition, ifUK content were to be used as a lever in commercialnegotiations through implementation of an industrialstrategy that imposed localisation targets, there couldbe a significant increase in the proportion of supplychain contracts awarded to UK companies.

2. Executive summary

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 6

2.4. Reduced consumer costs ofelectricity

A fleet approach to new nuclear build has thepotential to reduce significantly the cost of designingand building nuclear generation capacity. This wouldbe achieved through the economies of scale achievedby having common components and throughsignificant reductions in design and licensing effort,construction risk and contingency. The effect of sucha reduction in costs would be to reduce the costs ofelectricity to business and consumers. Consumers’disposable income would be increased directlythrough lower electricity bills. Business users wouldbenefit from lower electricity costs, which would betranslated into lower product prices, improvinginternational competitiveness.

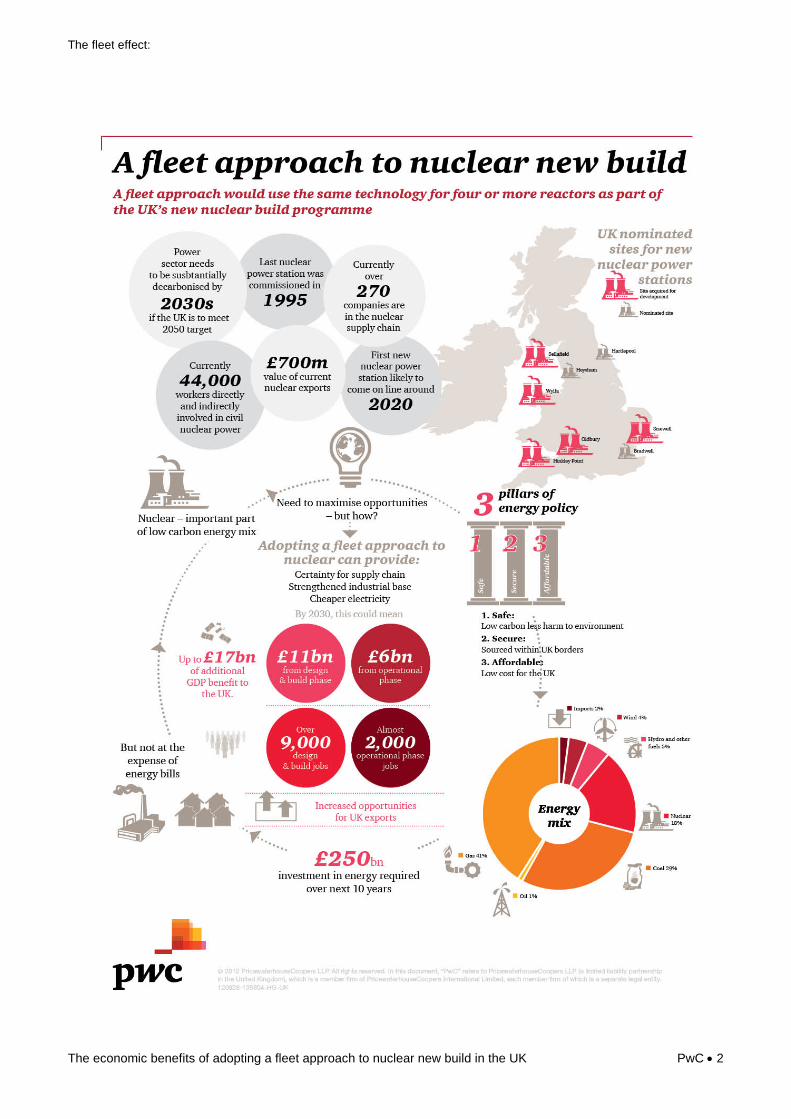

2.5. Key findingsA fleet approach to new nuclear build could deliver upto £17 billion of additional contribution toGDP (equivalent to about 1% of UK GDP in 2011), asshown in Figure 1, based upon the following:

The overall development of a fleet of four pairs ofnew nuclear reactors in the UK could result in asignificant additional direct boost to the UKmanufacturing sector, increasing GDP byapproximately £4.6bn expressed as a presentvalue in 2012 prices. This would be equivalent toan additional 68,000 man years of employmentover the design and build period up to 2030,equating to over 4,200 extra jobs over the buildperiod.

The indirect and induced effects could lead to afurther 82,000 man years of employment or 5,200extra jobs over the same period, equivalent to anaddition to UK GDP of £6.5bn expressed as apresent value in 2012 prices as compared to theeffects from diversified reactor technologies.

The lifetime costs of nuclear electricity generationfrom a fleet of four pairs of reactors could bereduced by 10.3% compared to a non-fleetapproach. The impact of the cost reduction wouldbe manifested in two ways;

first through a reduction in the costs ofElectricity Market Reform (EMR) support toGovernment, achieved through lower strikeprices for the Contracts for Difference (CfDs)for the second , third and fourth pairs ofreactors and

secondly, through a reduction in the wholesaleelectricity price.

The reduction in costs would feed through to apotential reduction in the price of electricity chargedto domestic and industrial users of up to 2.6% by2030 and an overall lifetime cost reduction in the costof generating electricity from the new nuclear fleet of10.3%, thereby reducing the costs for business andconsumers. Consumers’ disposable income would beincreased directly through lower electricity bills.Lower costs for businesses would contribute to lowerproduct prices which would improve internationalcompetitiveness. This could be equivalent to about44,000 man years of employment in sectors of theeconomy outside electricity generation over the EMRCfD durations or 1,700 extra jobs. We estimate thiswould be equivalent to a boost to UK GDP of about£6bn expressed as a present value using 2012 prices.

The incremental benefits of a fleet effect for nuclearnew build are largest with construction of the secondpair of reactors. Ending up with two or three isolatedpairs of reactors of different technologies across theUK would not maximise the industrial benefits of theprogramme and lead to the highest costs. A strategic,programmatic approach to nuclear new build cansupport the development of a sustainable nuclearsupply chain and deliver the most cost effective sourceof low carbon base load generation of electricityavailable.

Figure 1: Benefits of a fleet effect

68,000 4,2004.6

82,0005,200

6.5

44,0001,700

6

Man years Jobs GDP (£bn)

Reducedcost ofelectricity

Indirectandinducedimpacts

Directimpacts

Ov

er

CfD

pe

rio

dU

pto

203

0

194,000 1711,100

The risks associated with a fleet approach, and theirmitigations, are addressed in Section 10. We have notconsidered the potential ongoing savings once theCfDs have expired, or the potential for furtherinvestment in new nuclear post 2030 to capitalise onthe cost benefits in preference to other technologies.Both of these areas could provide further upsides.

In addition, our conclusions on the economic impactsof a fleet approach could be applied to other low-carbon technologies.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 7

3.1. The energy landscapeThe UK Government has set out ambitious plans tomeet its decarbonisation targets, with current policybuilt upon three key pillars:

reduction of CO2 and GHG emissions;

ensuring safe low carbon sources of energy; and

ensuring secure energy supplies within our ownborders.

Significant investments of around £250bn arerequired in energy sector infrastructure to deliver alow-carbon economy, particularly with the need toreplace a quarter of the UK’s existing power stationsby 2020 and to extend the transmission network toaccommodate a wider range of low-carbongeneration. The scale of investment required offersopportunities for the development of new skills andfacilities in the UK workforce and an expansion ofsustainable jobs in the manufacturing andconstruction sectors to meet the forecast demand inthe sector over the next 20 years. Added to this, thecurrent economic and financial pressures have led toa Government emphasis on enablers of growth tosupport employment. The low carbon agendaprovides the potential for real benefits for the UK interms of both jobs and GDP.

Since privatisation in the 1990s, investment in newelectricity generation has been undertaken by privatecompanies, based on their assessment of market risksand returns. As the low carbon focus has intensified,concerns about the risk/return balance for electricitygeneration assets with high capital costs andsignificant construction risks has increased, resultingin a reluctance for companies to invest without somerevenue certainty. Whilst the current coalitiongovernment has stated that the UK’s future supply of

2 DECC ‘Planning our electric future: a white paper for secure,affordable and low carbon electricity (cm8009)’, July 2011.

nuclear energy will be determined by marketmechanisms, the Government’s EMR package willdeliver some incentives. The EMR proposals3 seek tofacilitate investment in low carbon electricitygeneration through the agreement of CfDs. These willguarantee a price for electricity over an initial periodof time thus creating stable financial incentives forinvestment in all forms of low carbon electricitygeneration, including nuclear.

Our report looks at whether the benefits ofmoving from first of a kind (FOAK) in the UKto nth of a kind (NOAK) for nuclear plant differdepending on whether a fleet of the samereactor technology or diversified reactortechnologies are adopted. We seek to identifythe extent to which benefits accrue to UKnuclear supply chain companies and theoverall benefit to UK consumers.

Current uncertainties around the details of the EMRmechanisms have led to delays in the sanctioning ofnew projects and nuclear plant are no exception.Uncertainty feeds through to the supply chain and theUK manufacturing sector is feeling the impact. Itrecognises that there are opportunities to participatein new nuclear build but is seeking signals that thereis a tangible pipeline of projects to justify investmentsin facilities and training. There remains anunderstandable concern based on the history ofnuclear electricity generation in the UK that the newnuclear programme could result in the developmentof only a single station. Our report seeks to identifythe signals that would provide comfort to differentsections of the UK supply chain, the timescales inwhich they would be required and the resulting scaleof investments that would arise.

The Government’s economic policy objective is toachieve strong, sustainable and balanced growth. As

3 DECC ‘Draft Energy Bill CM 8362’ May 2012.

3. The energy challenge

Over £250bn2 investment required in energy infrastructure.

Centred on ensuring safe low carbon and secure supply of energy.

Nuclear key to the energy mix for UK.

Uncertainties surrounding EMR have led to delays in nuclear build.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 8

part of the Growth Review launched in November20104, it aims to make the UK an attractive place tostart or grow a business, to encourage investment andto create a flexible, appropriately skilled workforce asreferenced in the Industrial Strategy in September20115. The investment requirements in the electricityindustry means that electricity generation is a keysector for achieving such growth.

There is a wide range of nuclear sector expertise in theUK currently, but much of it is focused on other partsof the nuclear value chain (outside of new nuclearbuild), including existing nuclear generation,decommissioning and defence. Those companies thathave experience in supplying parts and services fornew nuclear in other countries have already madeinvestments in quality assurance, qualificationrequirements and skills training. They see the UKnuclear new build programme as a major opportunity.

Our report seeks to identify the signals that wouldencourage overseas companies to invest in the UK, thelessons learnt from those UK companies with newnuclear build experience and the support andincentives that the UK supply chain is seeking toexpand its capabilities and skill base in a timelymanner to benefit from new nuclear buildopportunities.

The success of the nuclear new build programme inthe UK will be dependent, in part, on its ability todemonstrate a broader range of economic benefitsthan a contribution to low carbon electricitygeneration and security of supply. The nuclearindustry, has, and always will, present a nuclearhurdle to potential suppliers and investors in terms ofinvestment in capability and resources.

Over time the barriers to entry can be reduced as thelevel of experience of developing nuclear new build inthe UK improves, which should lead to increasedinward investment and the realisation of greatereconomies of scale and scope for companies withinthe supply chain. Increased scope and volume ofservices should in turn lead to increases in theperformance of regional economies, both throughindirect and induced benefits.

4 The path to strong, sustainable and balanced growth, BIS,November 2010

5 BIS ‘Industrial Strategy: UK Sector Analysis’, 2012

3.2. Future energy needsOver the next decade, a quarter of the UK’s electricitygenerating capacity is expected to close, with all butone of the existing nuclear plants scheduled to reachthe end of their operating life by 2025. The challenge ofreplacing this infrastructure is increased further by theneed to reduce CO2 emissions, implement safe lowcarbon sources of energy and maintain secure energysupplies within our own borders. This is set against thepotential doubling of demand for energy as thetransport and heating sectors become increasinglydependent on electricity.

Compliance with the EU Large Combustion Plant andIndustrial Emissions Directives means that themajority of the new plant to be developed over theperiod to 2030 will be nuclear or wind, with newer lowcarbon technologies gradually increasing in importanceas their technology challenges are overcome (and theircosts fall). The role of combined cycle gas turbines(CCGTs), the new electricity generation of choice todate, will increasingly move to that of fast responseplant to balance input from wind and otherintermittent generation. Investing in diversifiedsources of energy is key to preserving and enhancingthe UK’s security of supply, but must comply with theGovernment’s low carbon commitments andaffordability objectives.

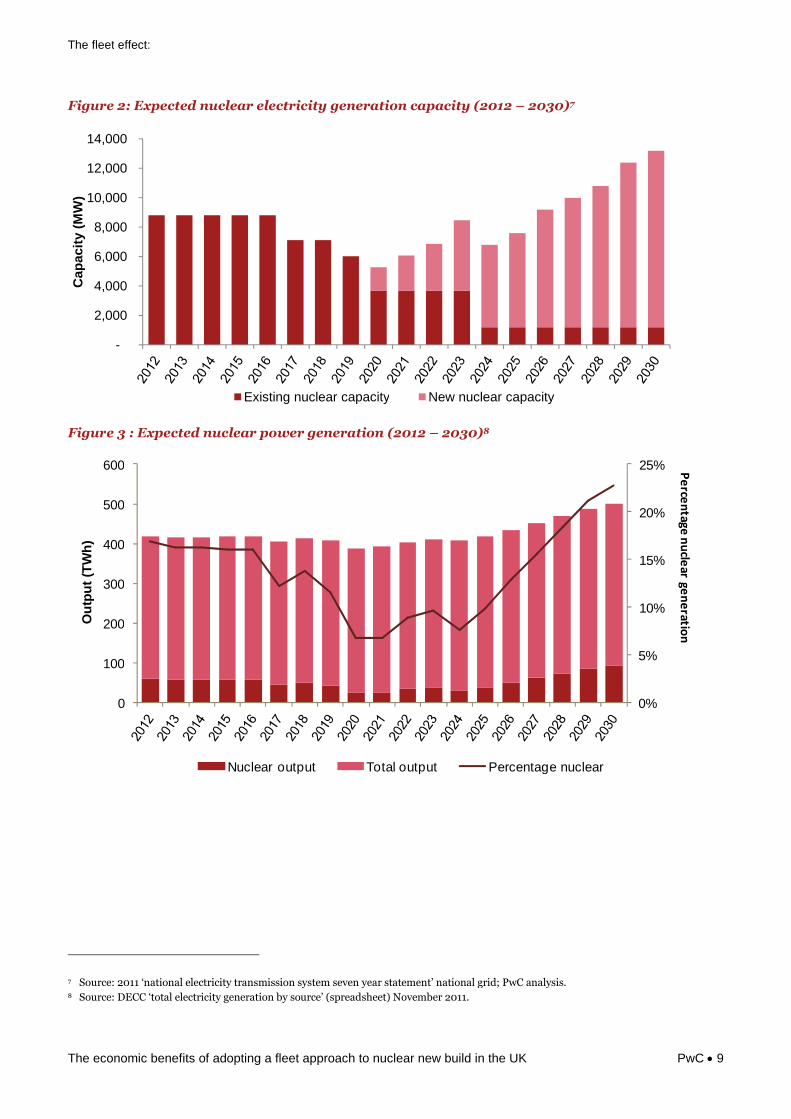

Within this policy context, new nuclear plant isassumed to be the primary low carbon baseload plant,playing a crucial role in the UK’s ability to maintain itssecurity of supply. Current investment plansbased on the acquisition of nuclear licensedsites suggest that there could be up to eightreactors (ignoring differences in capacityacross technologies) across four sites providingup to some 13.2GW of additional capacity by2030 (as shown in Figure 2).We assume that anynuclear development on the fifth acquired site or thethree additional nominated sites would not commenceuntil after 2030 and so have not included any potentialbenefits within our analysis.

National Grid currently projects peak electricitydemand to rise from around 57GW in 2020 to around60GW by 2030 at a relatively stable rate under its‘Gone Green’ scenario6. The contribution of nuclearelectricity generation to meeting this demand falls to alow of around 7% in 2020 under DECCs centralscenario and as new nuclear electricity generation iscommissioned rises to around 23% by 2030 ascompared with around 18% today as shown in Figure 3.

6 National Grid ‘UK future energy scenarios’ November 2011.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 9

Figure 2: Expected nuclear electricity generation capacity (2012 – 2030)7

Figure 3 : Expected nuclear power generation (2012 – 2030)8

7 Source: 2011 ‘national electricity transmission system seven year statement’ national grid; PwC analysis.8 Source: DECC ‘total electricity generation by source’ (spreadsheet) November 2011.

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Cap

acit

y(M

W)

Existing nuclear capacity New nuclear capacity

0%

5%

10%

15%

20%

25%

0

100

200

300

400

500

600

Ou

tpu

t(T

Wh

)

Nuclear output Total output Percentage nuclear

Pe

rcen

tagen

ucle

arge

ne

ration

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 10

The contribution of new nuclear power to the UK’ssecurity of supply underpins the importance of timelyinvestment decisions, both for developers and thesupply chain. The earliest timescale for the commercialoperation of new nuclear is assumed to be 2018 underDECC’s 2011 indicative timeline9, but manycommentators assume commercial operationdates of around 2020.

The uncertainty over timing of investment decisions bydevelopers feeds through into uncertainty for thesupply chain and uncertainty over commercialoperation dates. New nuclear is assumed to provide anincreasing contribution to meeting demand throughoutthe 2020’s which means that a continuous programmeof new build is required, with a correspondingrequirement for resources to design and construct theplant.

3.3. The UK supply chainThe last nuclear plant developed in the UK wasSizewell B, which was commissioned in 1995 and isdue to operate until 2035. Since then, UK nuclearskills have been concentrated in supportingoperations and maintenance of the Magnox andBritish Energy (now EDF) nuclear fleet, waste anddecommissioning at Sellafield and other sites and themilitary nuclear sector.

The challenges faced due to an ageing workforce, aneed to encourage graduates and craftsmen to enterthe nuclear industry, and the realisation that the skillsto support a new nuclear build programme in the UKwere insufficient and have led to a range ofGovernment, regional and company-led initiatives.However, the nuclear sector faces competition forskilled engineering and construction resources fromother infrastructure projects and safety critical sectorsincluding oil & gas and aerospace, highlighting theneed to expand both the number of workers and thetraining facilities to support skills transfer.

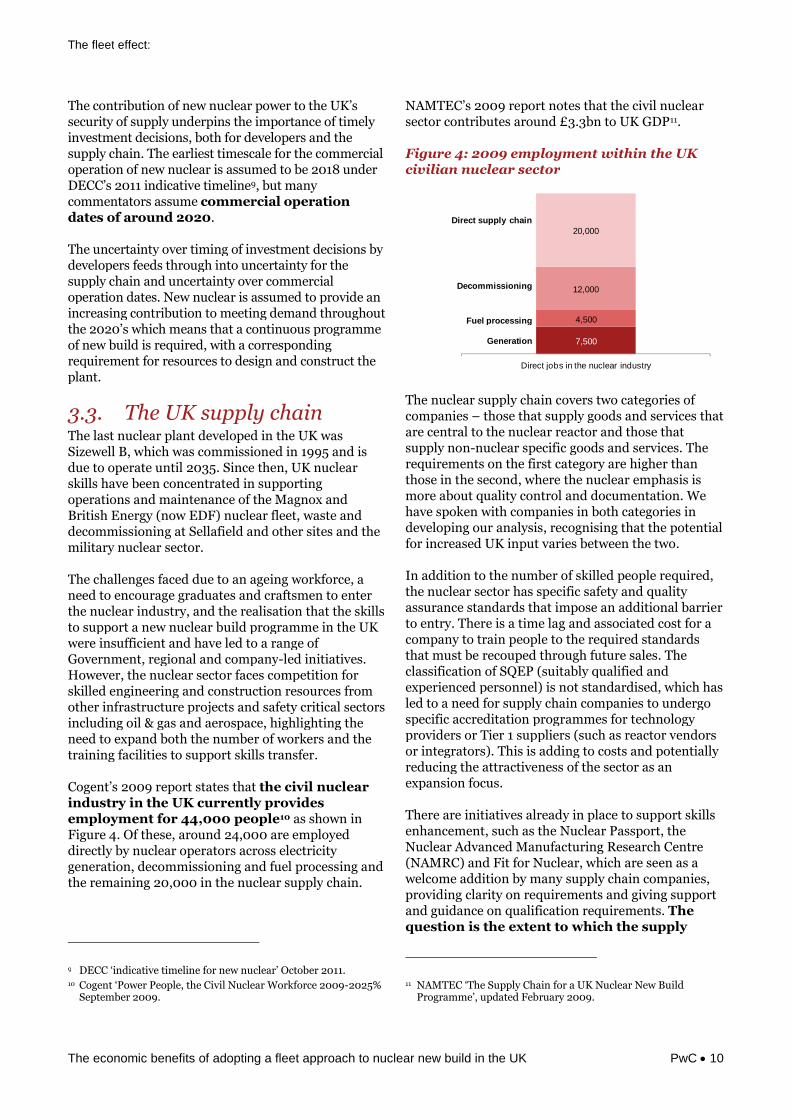

Cogent’s 2009 report states that the civil nuclearindustry in the UK currently providesemployment for 44,000 people10 as shown inFigure 4. Of these, around 24,000 are employeddirectly by nuclear operators across electricitygeneration, decommissioning and fuel processing andthe remaining 20,000 in the nuclear supply chain.

9 DECC ‘indicative timeline for new nuclear’ October 2011.10 Cogent ‘Power People, the Civil Nuclear Workforce 2009-2025%

September 2009.

NAMTEC’s 2009 report notes that the civil nuclearsector contributes around £3.3bn to UK GDP11.

Figure 4: 2009 employment within the UKcivilian nuclear sector

The nuclear supply chain covers two categories ofcompanies – those that supply goods and services thatare central to the nuclear reactor and those thatsupply non-nuclear specific goods and services. Therequirements on the first category are higher thanthose in the second, where the nuclear emphasis ismore about quality control and documentation. Wehave spoken with companies in both categories indeveloping our analysis, recognising that the potentialfor increased UK input varies between the two.

In addition to the number of skilled people required,the nuclear sector has specific safety and qualityassurance standards that impose an additional barrierto entry. There is a time lag and associated cost for acompany to train people to the required standardsthat must be recouped through future sales. Theclassification of SQEP (suitably qualified andexperienced personnel) is not standardised, which hasled to a need for supply chain companies to undergospecific accreditation programmes for technologyproviders or Tier 1 suppliers (such as reactor vendorsor integrators). This is adding to costs and potentiallyreducing the attractiveness of the sector as anexpansion focus.

There are initiatives already in place to support skillsenhancement, such as the Nuclear Passport, theNuclear Advanced Manufacturing Research Centre(NAMRC) and Fit for Nuclear, which are seen as awelcome addition by many supply chain companies,providing clarity on requirements and giving supportand guidance on qualification requirements. Thequestion is the extent to which the supply

11 NAMTEC ‘The Supply Chain for a UK Nuclear New BuildProgramme’, updated February 2009.

7,500

4,500

12,000

20,000

Direct jobs in the nuclear industry

Direct supply chain

Decommissioning

Fuel processing

Generation

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 11

chain is prepared to participate in suchschemes without certainty on the timing andthe future of the new nuclear programme andthe risk that their own role might be limited tosupport on a single plant.

Some UK companies have entered into joint ventures(JVs) with companies already in the new nuclearsupply chain such as Atkins’ JV with Assystem knownas n.triple.a which aims to provide globalopportunities but also to support activities in the twocompanies’ home markets.

Where UK companies are a subsidiary of aninternational company with an established trackrecord in new nuclear supply chains (e.g. ClydeUnion, Doosan Babcock) they have more ready accessto skilled resources, established contacts andprocesses for accreditation. Other categories withinthe supply chain are those with relevant nuclearexperience but who have not yet participated innuclear new build and those who operate in safetycritical industries but without nuclear experience.Both of these could, if appropriate incentives andsupport were to be made available, seize thisopportunity to support the growth of the UK nuclearnew build sector.

The challenge for all UK companies to capture theopportunities from a new nuclear build programme inthe UK is to determine the addressable part of themarket, the investments required in qualification andaccreditation (and their associated timescales) andthe costs of bidding for and delivering the work. Theythen need to develop business cases to invest andsecure acceptable volumes of work over predictabletimescales. We discussed with our interviewees thesignals that would encourage them to commit to suchinvestment programmes, and the impact ofdifferences between a fleet and a non-fleet approach.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 12

Comprehensive literature review of material relating to nuclear reactor construction.

Developed a set of hypotheses about the expected impacts of a fleet approach.

Undertook a series of interviews with companies in, or potentially part of, the nuclear supplychain.

Created an economic model to assess the potential impact on GDP and jobs from a fleetapproach to nuclear new build.

Model designed to estimate the direct, indirect and induced benefits of a fleet approach.

4.1. IntroductionIn this section, we describe how we have assessed theexpected benefits of a fleet approach to nuclear newbuild as compared with a non-fleet approach. We alsoprovide a brief overview of the methodology we haveused to estimate the expected benefits of a fleetapproach: further details of the model can be found inAppendix A.

We consider a new nuclear portfolio of up toeight reactors (which operate as four pairs).The interval between reactor builds is asshown in Figure 5, over a 16 year period. Thisassumption is derived from expected constructionintervals between the first and second reactors on asingle site, a rhythm of site development activity thatwould support continuity of employment, and theentry into commercial operation of sufficient nuclearcapacity to meet forecast contributions to security ofsupply by 2030. As already stated in Chapter 1, wehave not considered site specific new build.

Figure 5: Illustration of a fleet approach tonuclear new build

4.2. Approach to assessmentOur approach to assessing the economic benefits ofadopting a fleet approach to nuclear new build in theUK has been based on four key elements:

We reviewed earlier third party reports whichanalysed diverse aspects of the potential impact ofa nuclear new build programme within the UK aswell as the lessons from international experienceof the construction and operation of nuclear plant.These reports cover the nuclear supply chain, skillsrequirements, drivers of risk, reward andinvestment decisions and the downstream andupstream impact of nuclear generation. A list ofthe key reports reviewed can be found at AppendixD.

Based on our review of existing reports and ourknowledge of the UK nuclear sector, we developedan initial set of hypotheses about the expectedimpacts of a fleet approach to the delivery of newnuclear power compared to a non-fleet approach.These hypotheses effectively provided a frameworkfor the model we developed to assess the expectedbenefits of a fleet approach to a nuclear new buildprogramme.

4. Approach and methodology

Reactor 1

Reactor 2

Reactor 3

Reactor 4

Reactor 5

Reactor 6

Reactor 7

Reactor 8

2029 20302024 2025 2026 2027 20282019 2020 2021 2022 20232013 2014 2015 2016 2017 2018

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 13

We then undertook a series of 26interviews with a sample of organisations12

which are either in existing nuclear supply chainsor might potentially be part of the UK nuclearsupply chain. Our interviewees includedcompanies from across different parts of thenuclear supply chain, large and small companies,those with existing nuclear new build experienceand those without, UK based companies and thosethat are subsidiaries of international companies.We asked the companies a series of questionsdesigned to elicit qualitative and quantitativeinformation about:

the opportunities presented by nuclear newbuild in the UK;

the implications on their specific business of afleet approach to nuclear new build in the UK;

how commitment to a fleet approach to nuclearnew build would affect their investmentdecisions; and

the impact on their own supply chains of a fleetapproach in the UK.

In addition, we discussed a similar range of topicswith key stakeholders , namely the Department forBusiness, Innovation and Skills (BIS), the Departmentof Energy and Climate Change (DECC) and theNational Nuclear Skills Academy.

Using results from the preceding elements, wedeveloped an economic model to assess thepotential impact on GDP and jobs from afleet approach to nuclear build compared to anon-fleet approach for the UK. The model wasdesigned to estimate the direct, indirect andinduced benefits of a fleet approach, where:

direct benefits are the employment and GrossValue Added (GVA13) generated by expenditureon suppliers of the nuclear island, civil works,conventional island and balance of plant;

indirect benefits are the employment and GVAgenerated by greater supply chain spending as aresult of the first round of expenditure; and

induced benefits are the employment and GVAgenerated by greater employee wages, whichresults from the increased revenue of suppliersand their supply chains.

12 See acknowledgements for list of companies and stakeholdersinterviewed.

13 GVA is the difference between revenue and intermediateconsumption, and a contributor to GDP.

4.3. MethodologyA critical part of our approach was the developmentand application of an economic model with which toassess the expected incremental benefits of a fleetapproach to nuclear new build. This involved threekey steps:

development of a series of logic chains whichdescribe how the expected incremental impacts ofa fleet approach to nuclear new build are expectedto arise, including the articulation of what isassumed to happen in the absence of a fleetapproach (the counterfactual or non-fleetapproach);

identification and collection of the data needed topopulate the economic model and determinationof the additional assumptions required; and

construction, testing and running of the economicmodel, including sensitivity testing to understandthe significance of the key assumptions anduncertainties.

An explanation of the steps can be found below.

4.3.1. Development of logic chainsfor benefit categorisation

Our logic chains assumed that a fleet approach tonuclear new build has the potential to deliverincremental economic benefits for the UK throughfour key mechanisms by:

reducing the cost of designing, building andoperating (including decommissioning) up to fournuclear plant comprising eight reactors of thesame technology and design;

increasing the share of UK content in the UK’snuclear new build programme;

reducing the average cost of electricity toconsumers in the UK; and

developing UK capability so it can be exploited inthe longer term in the nuclear supply chain, bothwithin the UK and globally. This capability couldthen be additionally deployed in other sectors withhigh quality and safety requirements.

Figure 6 shows schematically the key expectedbenefits of a fleet approach in chronological orderbased upon when they would be expected to arise.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 14

Figure 6: Expected benefits of a fleet approach

An integral part of assessing the potential incrementalbenefits of a fleet approach was to define thecounterfactual – an alternative view of what wouldhappen without a fleet approach. Our counterfactualassumed that the same volume of additional nuclearcapacity would be provided in the UK as part of thenuclear new build programme but reactor technologywere not common and the design of the CI and BOPwere not the same. Otherwise, under thecounterfactual, we assumed that the features of eachplant were the same.

We combined the underlying logic model with theavailable data to construct, run and test our economicmodel to estimate the scale of the potential benefits ofa fleet approach to new nuclear build. Details of themodel structure can be found in Appendix A.

4.3.2. Data sources and assumptionsEach of the logic chains required different data and,where reliable data were not available, assumptionswere made in order to estimate the scale of thepotential benefit. The key data sources andassumptions used for each element of our model aredescribed in Appendix A and summarised in Table 1below.

Table 1: Key data sources and assumptions

Category of assumptions Sources

Expenditure groupings withinthe design and build phase of anuclear reactor

Supply chain interviews,third party reports,PwC analysis

Timescales Supply chain interviews

Economic assumptions PwC assumptions,Government statistics

Financial assumptions PwC assumptions

Electricity pricing assumptions(cost for consumers)

DECC, National Grid, thirdparty reports

Our analysis of reductions in electricity prices startsfrom assumptions on the CfD strike price achieved foreach pair of nuclear reactors. These are sourced frompublicly available sources and do not represent PwC’sview on appropriate or achievable strike prices fornuclear plant. Any cost savings are assumed to applyto CfDs for subsequent pairs of reactors – i.e. thesecond, third and fourth pairs only.

4.3.3. Sensitivity analysisWe undertook a range of sensitivity analyses on thefollowing parameters:

reduction in the design and build cost of a reactor;

increase in the proportion of design and buildcontent achieved by UK companies; and

reductions in the cost of electricity.

Through these, we aimed to assess the robustness ofour hypotheses. Details are found in Appendix B.

Our sensitivity assessment associated with thecost of electricity for consumers uses a rangeof CfD strike prices from £75/MWh to£135/MWh (2012 prices) taken from publicsources. The lower end of the range is a round figurebased on the £74.10/MWh proposed by PB Power intheir 2011 report for DECC14. The upper range is around figure that is lower than the £140/MWh quotedas an offshore wind price cap by Vincent de Rivaz,Chief Executive Officer, EDF in his August 2012interview with the Daily Telegraph15.

14 Parsons Brinckerhoff “Electricity Generation Cost Model” 201115 Daily Telegraph

‘http://www.telegraph.co.uk/finance/newsbysector/energy/9471193/EDF-Energy-puts-price-cap-on-Hinkley-Point-nuclear-plant.html’

• Greater certainty

Investmentdecisions

• Economies ofscale

• Local (UK)

Design and build

• Lower electricityprices forcustomers

Operation

• Strengthened UKindustrial base

• Increasedexports

Legacy

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 15

4.4. Overview of resultsIn Chapters 5-10 we analyse the expected potentialbenefits of a nuclear new build programme focusing,in particular, on the incremental benefits that a fleetapproach to nuclear new build could be expected tobring (compared with the alternative of a non-fleetapproach – where the volume, technology/design andtiming of the programme is not known withcertainty).

We also consider the potential risks associated witheach category of benefit, reviewing the evidence inrelation to each category of expected benefit in turnand following a broadly common structure for eachcategory:

We describe (qualitatively) the mechanismsthrough which the UK is expected to deriveeconomic benefits from a fleet approachdrawing on our interviews with key stakeholders,especially those potentially involved in the deliveryof the programme, and our review of recentrelevant studies.

We present the results of our economicmodelling of each benefit. This includes anoverview of the key steps in our analysis as well asa summary of the sensitivity of our results to thekey assumptions we made.

We summarise our assessment of the keyrisks and uncertainties associated with eachbenefit.

Table 2: Summary of expected benefits andrisks of new nuclear build

Chapter Benefit Estimated fleet benefits

5 Enhancedcertainty

Quantified through measuresbelow

6 Reduced costof design andbuild

Up to 18% reduction for a fourthpair of reactors

7 Enhancedlocal content

Up to £11bn of additional GVA andan additional 150,000 man yearsof employment

8 Reduced costof electricity

Wholesale electricity prices downby up to 2.6% by 2030, resulting inup to £6bn of additional GVA and44,000 additional man years ofemployment

9 StrengthenedUKindustrialbase

Not directly quantified

10 Key risks anduncertainties

Qualitative mitigation measuresidentified

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 16

Nuclear supply chains need enhanced certainty about the make-up of the UK’s nuclear newbuild programme.

At present only Hinkley C is seen as secure.

Commitment to a fleet provides confidence and clarity on timescales and work volumes.

A fleet approach can reduce actual and perceived risk in programme.

The over-riding feedback from our discussions withthe supply chain is the need for enhanced certaintyabout the direction, timing and scale of the UK newnuclear build programme. The level of nuclear buildskills and experience within the UK is at a relativelylow base given the period since the development ofSizewell C and the limited involvement of UKcompanies in other global nuclear new buildinitiatives. A programme of UK nuclear newbuild is not seen as a reality at present:although Hinkley Point C is seen as probable, otherreactors are viewed as no more than likely at themoment.

Figure 7: The components of certainty

Whilst it can be argued that achieving certainty istechnology agnostic, there are strong arguments thatpoint to a fleet approach enhancing certainty. A fleetbased on common technology and design can reduceboth actual and perceived risks, unlocking thepotential for supply chain investments throughimproving the risk/reward balance and enabling the

realisation of economies of scale and increased UKindustrial capability.

5.1. Certainty throughcommitment

We identified a number of themes relating tocommitment to new nuclear industrial strategies toprovide certainty to the supply chain on the role itcould play.

The lack of clarity over the structure of theprogramme, delays in the programme itself anduncertainty over the technologies to be adoptedare resulting in parts of the supply chain:

delaying investment decisions to enhance skilllevels or improve facilities;

opting to apply their capabilities to othersectors such as the wider power and utilitiesmarket, or oil and gas, where the barriers toentry are lower, investment decisions are lowerrisk and the certainty of orders is greater; and

focusing nuclear skills abroad on other newnuclear programmes such as in Asia, CentralEurope and the Middle East.

The commercial supply chain strategies for Tier 1and 2 supply chain companies reflect theuncertainty in the new build programme.Commitment would enable the firming upof commercial strategies and provide clarityfor the supply chain on steps required to supportdelivery.

Orders for four or more reactors of a singletechnology would be a ‘game changer’ formany supply chain companies weinterviewed. It would justify investments ininnovation through automation or expansion ofwork along the value chain into fabrication anddesign, improving quality and cost-effectiveness.

Commitment to

Volumes that support investment

Confidenceand

certainty

Timescales to support continuity of workload

The nuclear new build programme

results in

5. Enhanced certainty

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 17

Our interviewees told us that the reduction inconstruction risk resulting from thecertainty of a fleet programme would leadto cost and timescale reductions throughmore efficient use of capacity, reduced trainingrequirements and better implementation oflessons learned.

The supply chain recognises that accreditationrequirements for nuclear new build (‘N’ Stamp orRCC-M) are onerous and time-consuming. A fleetapproach would provide companies with agreater degree of certainty that they wouldachieve acceptable returns on theirinvestments.

Commitment to contracts for multiplereactors would enable supply chaincompanies to demonstrate secure revenuesto underpin financing support for investmentin facilities.

For supply chain companies active in a range ofindustries, commitment to multiple reactorswould allow businesses to invest to meetknown demand and take investment risksin other sectors.

Moving from memoranda of understanding to firmcontract placement depends on investors takingFinal Investment Decisions (FIDs), which in turnneed successful CfD negotiations that gives ownersa known commercial basis for their investment,based on the expected cost of building andoperating proposed plant and clarity to the supplychain.

5.2. Certainty throughcontinuity

Discussions with the supply chain identified clearmessages on the need for a sustained programme ofwork to support supply chain investment in facilities,accreditation and people:

Continuity of work is more readilyachievable with one technology providerable to coordinate the placing of orders inand across the supply chain. If intervalsbetween reactor builds are too long, the supplychain will have underutilised manpower and runsthe risk of losing specialist skills, but if intervalsare too short, manpower capacity requirementswill increase significantly, providing challenges forthe supply chain and suggesting that the balance ofrequirements might be met from the overseassupply chain. A consensus appears to be buildingaround an interval of around 18 months betweenreactor builds.

Continuity through the use of a consistentdesign and supply chain would be a majorcontributor in maximising processeffectiveness.

Confidence in the continuity of the nuclearnew build fleet programme will enable thesupply chain to invest in capability building– through additional recruitment of apprentices,development of career plans for ongoing skillstraining over time, recruitment of skilled engineersand graduate trainees – to support their ability toearn the required levels of return on theirinvestment.

Greater maturity of the design and mutualunderstanding of the costs of deliverywould reduce the risks of delay andimprove the certainty of outcome, therebyreducing overall construction risk. Thebenefits of learning from previous experience,increasing expertise and familiarity with therequired processes would result in cost andschedule savings in design, construction andcontingency requirements.

As the technology develops a track recordwith the regulator, licensing risks will bereduced.

Development of a fleet would lead to anincreased level of trust and understandingacross the supply chain from Tier 1 to Tier 4 asthe level of maturity and expertise in the nuclearnew build sector expands.

5.3. Certainty through volumeFor many companies in the supply chain, the businesscase for investment in new nuclear build is dependenton the volume of services or components requiredover time, such that investment is sustainable:

Certainty in volumes provides confidenceto smaller supply chain companies that thecosts and timescales of achieving nuclear qualityaccreditations is a worthwhile investment.

Some specialist supply chain companies are theonly, or one of a few remaining, manufacturers oftheir product in the UK. Certainty throughvolume will support their continuedoperations.

Commitment to volumes means that the additionalcosts associated with nuclear quality requirementscan be recovered over a larger number of productsor longer timescale, leading to lower unit costsand increased competitiveness of UK supplychain companies.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 18

Commitment to multiple reactors and anassociated timing provides the supply chain withcertainty over future orders and sufficient securityand confidence to put in place the multi-yeartraining programmes required to deliver thenecessary numbers of apprentices and designengineers and to develop career progression plansto provide opportunities over the duration of thenew nuclear build programme.

Increased volumes of standard componentswould enable minimal retooling, common qualityassurance regimes, increased innovation andboosts R&D to provide more efficient, lowercost, higher quality solutions. Onceoperational, additional volumes would be requiredto support O&M services.

The quantification of the impact of certainty isdiscussed in Chapters 6-9, through the impact onreduced costs, increased jobs and impact on GDP.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 19

Reduction in total design and build costs of approximately 11% between first and secondpairs of reactors.

Further 4% saving between second and third pairs of reactors.

Overall saving of 18% between first and fourth pairs of reactors.

Total saving for design and build of a fleet of eight reactors of 10% against thecounterfactual.

6.1. Nature of benefitsThe construction of a fleet of nuclear reactorsgenerates cost efficiencies through a variety ofsources, which differ according to the type of supplierand their position in the value chain. Supply chaininterviews identified the economies of scalegenerated by a volume of reactors withidentical technology and design as the mostcommon driver of cost savings.

The improved certainty associated with a fleetapproach was identified as an important contributorto lower financing costs, supporting early investmentin supply chain capability. The continuity of ordersresulting from certainty was also expected to besignificant, allowing the supply chain to optimise theiruse of resources. We include the cost savings fromcertainty in the benefits discussed below.

The specific sources of cost savings identified bystakeholder interviews as the most significant:

volume discounts through bulk purchasing;

absorbing one-off fixed costs – such as thoseassociated with design, set-up, procurement andaccreditation;

learning effects, leading to new or improvedproduction techniques;

reduced financing costs; and

improved resource planning.

Our analysis has assessed the potential scale of thesecost savings (compared to a non-fleet approach) foreach key element of spend: in total, we haveconsidered around 20 separate elements of spendassociated with the design and build of new nuclear

plant, split across the nuclear island, nuclear islandcivil works, balance of plant and conventional island.

6.2. Scale of benefitsThe quantification of these savings is displayed inFigure 8, with a reduction in total design and buildcosts of approximately 11% between the first andsecond pairs of reactors. There is an incrementalsaving of approximately 4% between the second andthird pairs of reactors, which is repeated between thethird and fourth pairs of reactors. Hence, the designand build cost of the fourth pair of reactors isapproximately 18% less than that of the firstpair, under a fleet approach of building fourpairs of reactors. The total design and build costfor the eight reactors under a fleet approach results ina 10% saving against a non-fleet approach. In 2011Parsons Brinckerhoff’s study for DECC16 estimated asaving of 15% for the total capital costs of a nuclearpower station with multiple reactors, as constructionmoves from FOAK to NOAK in the UK, which iscomparable to the savings in Figure 8.

Figure 8: Expected cost savings during designand build phase with a fleet approach

16 Parsons Brinckerhoff ‘Electricity generation costs’ 2011

0%

20%

40%

60%

80%

100%

Reactors 1 & 2 Reactors 3 & 4 Reactors 5 & 6 Reactors 7 & 8

Pe

rce

nta

geco

stre

du

ctio

ns

Nuclear island - non civil works Nuclear island civil worksConventional island Balance of plant

6. Reduced cost of UK nuclearnew build

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 20

6.3. Sensitivity analysisTwo key sensitivities were identified for design andbuild cost savings based on the responses provided inour supply chain interviews. The first is the level ofcost savings considered achievable with a fleetapproach, where we considered the quantitativeimpacts of conservative and optimistic scenarios tocompare with our base case saving of 18%:

a conservative view on design and build costsavings led to a saving of 9% for the fourth pair ofreactors when compared with the first; and

an optimistic view on design and build cost savingsled to a saving of 28% for the fourth pair ofreactors when compared with the first.

The second is the timing of the new build programme,which we dealt with qualitatively due to the difficultyof quantifying its impact. Stakeholder interviewsrevealed that for many companies in the supply chain,the cost saving from a fleet approach was sensitive tothe phasing of reactors. A significant proportion ofsavings could be lost if the gap between theconstruction of reactors was noticeably increased ordecreased. A phasing of around 18 months appearedto suit the majority of companies.

Further details are contained in Appendix B.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 21

Increased UK content in the nuclear supply chain could provide an additional £5bn in directGDP and an additional £6bn in indirect and induced GDP.

The UK nuclear supply chain could be boosted by up to 4,200 additional direct jobs duringdesign and build and a further 5,200 additional indirect/induced jobs.

A fleet approach strengthens the incentives for the supply chain to invest in nuclear newbuild capability (facilities, accreditation and training).

The potential volume of work will lower barriers of entry for UK nuclear new build supplychain.

A fleet approach increases the likelihood of additional inward investment from non-UKcompanies.

7.1. Nature of benefitsConstruction of a fleet of nuclear reactors as part ofthe UK nuclear new build programme is also expectedto enable increased UK industrial and manufacturingcontent in the nuclear new build programme(compared with what it might otherwise be) for tworeasons:

it would encourage more existing UK basedsuppliers to invest in developing their capability tomeet the needs of the operators; and

it could incentivise more international (non-UKbased) suppliers to invest in new or additionalcapacity in the UK (facilities and jobs) so that theycould compete more effectively to supply the UKnuclear new build programme.

Both of these effects have the potential to increase UKbased suppliers’ share of spend on the nuclear newbuild programme. This, in turn, could be expected toenhance the direct contribution of new nuclear buildto the UK economy. This can be measured asadditional GVA and as an increase in employment.

There would also be knock-on effects of any increasein UK output as the direct value added flowed throughthe economy. There would be indirect impacts on theeconomy through the spending of UK suppliers ontheir own supply chains and induced impacts on theeconomy through the spending of the suppliers’employees (and the employees in the supply chains).The indirect and induced impacts have beenestimated using GVA and employment multipliers as

defined in ONS input/output tables and PwC analysis.Combining these impacts with the direct impact givesthe total change in GDP and jobs resulting fromincreased UK content.

Delivery of a fleet of new nuclear reactors couldsignificantly strengthen the UK’s industrial base,specifically the capacity and skills to supplycomponents to new nuclear plants. This would haveincreased value at present as this capability iscurrently at risk from a lack of certainty. There couldalso be additional benefits from the creation ofnuclear know-how that could be applied across thewider UK generation sector.

While a proportion of the UK’s nuclear new buildprogramme must by definition be localised (e.g. civilworks for construction, operation and maintenance),the lack of recent UK experience in new nuclearsuggests that domestic suppliers may provide only alimited share of the design and build value. However,the certainty and volume brought about by a fleetapproach has the potential to affect the behaviour ofthe new nuclear supply chain, increasing the scope forUK content. These impacts vary across the differentcategories of expenditure in the design and buildphase and so the scale of the addressable market forcompanies in the UK nuclear supply chain differs,with each category considered separately:

For UK suppliers, the enhanced certaintyassociated with a fleet strengthens the incentivesto invest in nuclear new build capability, as areturn on their investment is more likely. This may

7. Enhanced local content of UKnuclear new build

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 22

take the form of investment in specific capitalequipment, recruitment of apprentices andnuclear-qualified staff, or training programmes tomeet nuclear standards. The capability of UKsuppliers would also improve over the fleet buildprogramme as they benefit from experience andlearning effects in delivering the same reactortechnology.

In addition, the potential volume associated with afleet of nuclear reactors lowers the barriers toentry into the UK nuclear new build supply chain.The entry barriers to the nuclear industry areparticularly high, consisting of sunk costs such asaccreditation, quality control procedures andtendering. The timescale required to achieveaccreditation coupled with uncertainty over ordervolumes, technology differences and deliverytimings made smaller companies in our interviewprogramme reluctant to commit to the costs ofinvestment. Commitment to a fleet approach andthe greater opportunity for repeat contracts wouldallow the potential for costs to be recovered over agreater number of units or timescales.

For non-UK suppliers, greater volume andcertainty of reactors with identical technologywould increase the viability of transferringmanufacturing operations into the UK, withadditional confidence being provided by a clearindustrial strategy. Our interviewees made clearthat, with a global supply chain, the business casefor investment must be strong. The increasedquantity of orders from a fleet approach wouldmake it more cost-effective to make inwardinvestment. Such investments have already beenseen in the UK offshore wind sector such asSamsung’s deal with David Brown Gear Systems17,Gamesa’s investment in an R&D facility inStrathclyde18 and Siemens’ £80m investment in awind turbine factory in Hull19.

Prime contractors are expected to employ globalsupply chains, using the optimum combination ofcost and quality criteria. The increased capabilityof the UK supply chain described above increasesthe likelihood that prime contractors would electto use UK content.

These reasons show the scope for increasing the UKindustrial and manufacturing contribution to nuclearnew build becomes more commercially viable when a

17 http://www.ft.com/cms/s/0/da0bf1b6-4c15-11e1-98dd-00144feabdc0.html#axzz28w21HjpO.

18 http://www.guardian.co.uk/environment/2012/mar/23/gamesa-offshore-windfarm.

19 http://www.bbc.co.uk/news/uk-england-humber-17993593.

fleet approach is adopted. However, without positiveaction to utilise UK capacity, there is a risk that thelevel of UK content will remain relatively small giventhe maturity of existing global supply chains andmodern logistics. The benefits of a fleet approachis likely to be maximised when supported by aclear industrial strategy that supports UKcontent, which would allow the proportion ofwork undertaken in the UK to increasesignificantly.

7.2. Scale of benefitsIn the context of utilising a fleet approach to drivedomestic content, Figure 9 demonstrates there isscope to almost double the UK’s involvement in thenuclear new build programme, when compared to thenon-fleet approach. In the absence of a fleet approachthe value of UK content is estimated to remain below50%, with over half of the available work undertakenby companies outside the UK. Our analysis of theresults of our interview programme concludes that thescope for UK content under a fleet approach increasesas the size of the fleet increases, with the greatestlocalisation potential for a fleet of eight reactorsestimated at approximately 85%20.

Figure 9: Potential for UK content evolutionwith and without a fleet

Economic benefits are generated for the UK in termsof GVA and employment, shown in Figure 10,increasing with the size of a fleet. There would be:

direct economic impacts for the nuclear supplychain as they generated greater profits, wage billsand employment;

indirect impacts when those businesses increasedtheir own supply chain spending; and

induced impacts when the employees of all ofthese businesses spent their increased wages in theeconomy.

20 See Appendix B for details.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Fleet of 2 Fleet of 4 Fleet of 6 Fleet of 8

%U

Kco

nte

nt

UK content - non-f leet approach UK content - f leet approach

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 23

For a fleet of eight reactors, approximately £4.6bn ofdirect additional GVA could be generated from theincrease in UK content, with additional indirect andinduced impacts of £3.5bn and £3.0bn respectively.This total additional GVA of more than £11bntranslates into approximately 150,000 manyears of employment (or around 9,400 jobs),which consists of:

a direct impact of 68,000 man years (equivalent to4,200 jobs);

an indirect impact of 45,000 man years(equivalent to 2,800 jobs); and

an induced impact of 38,000 man years(equivalent to 2,400 jobs).

The impacts on the UK supply chain are the net resultof the:

reduction in the total value of work available to UKcompanies due to the reduced design and buildcosts of a fleet; and

increase in the total share of design and build workdue to the fleet effect encouraging inwardinvestment and increased competitiveness of UKcompanies.

Figure 10 and Figure 11 take into account the trade-offs between the two effects, and demonstrate theeconomic impacts of increased UK content assumingthat the projected cost savings in Chapter 6 areachieved.

Figure 10: Additional direct, indirect andinduced GVA generated by a fleet approach

Figure 11: Additional direct, indirect andinduced employment generated by a fleetapproach

Figure 12 below shows how the magnitude ofeconomic impact for a fleet of eight reactors variesover the lifetime of the nuclear new build programme,which has been assumed to be completed by 2030.

The fleet benefit of UK content follows the timeprofile of construction activity, reaching its peak in2022 when the design and build of six reactors isunderway simultaneously, and tailing down as theconstruction of each reactor is completed. The peakeconomic impact will arise in 2022 when we estimatethat 14,900 people will be employed to meet thedemand for UK support to the new nuclearprogramme. This will generate additional GVA of£1.6bn in 2022.

Figure 12: Additional employment and GVAimpacts over time (fleet of eight reactors)

£0

£2

£4

£6

£8

£10

£12

Fleet of 4 Fleet of 6 Fleet of 8

Ad

dit

ion

alG

VA

(NP

V£

bn

)

Direct GVA (£bn) Indirect GVA (£bn) Induced GVA (£bn)

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Fleet of 4 Fleet of 6 Fleet of 8

Em

plo

ym

en

t(m

an

years

)

Direct man years Indirect man years Induced man years

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 24

7.3. Sensitivity analysisThree sensitivities were quantitatively tested in oursensitivity analysis against our base case estimate of£11.1bn of additional GVA and an additional 150,000man years of employment (9,400 jobs) for a fleet ofeight reactors:

A conservative scenario on the level of costreduction possible over the design and build of afleet produces an estimate of an additional £5.8bnof GVA and an additional employment estimate of57,000 man years or 4,000 jobs.

A more optimistic scenario on the level of costreduction possible over the design and build of afleet produces an estimate of an additional £11.4bnof GVA and an additional employment estimate of153,000 man years or 10,000 jobs.

A scenario assuming output per worker ratiosbased on UK nuclear literature (representing anindustry with lower labour-intensity) does notimpact the GVA estimates but provides anadditional employment estimate of 98,000 manyears or 6,000 jobs.

A scenario assuming output per worker ratiosbased on ONS input-output tables (representinghigher labour intensity) provides a total additionalemployment estimate of 388,000 man yearsrespectively or 24,000 jobs.

A scenario assuming economic multipliers basedon UK nuclear literature representing an under-developed nuclear supply chain provides anestimate of £7.4bn of additional GVA and 162,000additional man years of employment (10,000jobs).

A scenario assuming economic multipliers basedon the 2011 PwC study of the nuclear industry inFrance21 representing a well-developed nuclearsupply chain provides an estimate of £13.2bn ofadditional GVA and 209,000 additional man yearsof employment (13,000 jobs).

Full details and figures on our sensitivity analysis areto be found in Appendix B.

21 PricewaterhouseCoopers ‘The Socio-Economic Impact of theNuclear Power Industry in France’ 2011.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 25

8.1. Nature of benefitsOur research and analysis indicates that a fleetapproach to nuclear new build has the potential toreduce significantly the cost of designing and buildingnuclear generation capacity. This would be achievedthrough the economies of scale achieved by havingcommon components and through significantreductions in design effort, construction risk andcontingency, as described in Chapter 6.

Any reduction in the expected cost ofdeveloping, operating and decommissioning afleet of nuclear reactors could be anticipatedto feed through to lower electricity prices,through a reduction in the wholesale price ofelectricity and/or a reduction in the EMRsupport costs23. These lower prices would benefitdomestic and non-domestic customers, includingenergy intensive businesses:

Domestic customers would benefit from reducedelectricity costs leading to greater disposableincome, which would benefit the UK economythrough increased spending. This benefit can beestimated through increased GDP.

Commercial and industrial consumers would gainfrom lower electricity costs and hence improvedcompetitiveness leading to increased productivity.This benefit can also be estimated throughincreased GDP.

22 Lifetime costs take account of costs incurred over the operationaland decommissioning period, recovered over the duration of theEMR CfD.

23 EMR support costs is the term used by DECC in its document“Estimation of households’ demand for gas and electricity” torepresent the costs associated with CfDs under the EMR.

Companies active in export markets would alsopotentially benefit from an increase ininternational competitiveness, leading to increasedsales and increased GDP.

8.2. Scale of benefitsOverall, we estimate that the lifetime costs ofnuclear electricity generation from a fleet ofeight reactors could be reduced by 10.3%through improvements in planning, regulation,efficiency and regulatory approvals.

Our analysis suggests that the reduction incosts would feed through to a potentialreduction in the price of electricity charged todomestic, commercial and industrial users ofup to 2.6% by 2030.

Consumers’ disposable income would be increaseddirectly through lower electricity bills.

Commercial and industrial users would benefitfrom lower costs of businesses, which wouldtranslate into lower product prices, improvinginternational competitiveness. This could lead toincreased exports, reduced imports and higherlevels of investment.

Taken together, these effects are estimated to increaseUK GDP by about £700m (undiscounted) in 2030,when all the new nuclear capacity is assumed to beoperating. This is equivalent to about 2,400additional man years of employment in sectors of theeconomy outside electricity generation. We estimatethat this is equivalent to an additional boost toUK GDP of about £6bn expressed as a presentvalue using 2012 prices.

The reduced costs of delivering nuclear power due toa fleet approach are estimated to reduce the consumerprice of electricity by up to 2.6% at the peak of itsimpact around 2030, for a fleet of eight reactors as

8. Reduced cost of electricityto consumers

Analysis concludes that the lifetime costs22 of nuclear electricity generation from a fleet couldbe reduced by 10.3% for a fleet of eight reactors.

Domestic customers will benefit as well as commercial and industrial users, potentiallyleading to reduction in electricity prices of 2.6% in 2030.

Benefits equivalent to £6bn GDP boost and 44,000 man years of employment or 1,700 jobs.

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 26

shown in Figure 13. We limited our analysis toaddressing the benefits to be gained during the initialCfD period for each reactor, so our charts show adiminishing impact over time. In practice, we wouldexpect that there would be price benefits in the post-CfD period and additional benefits from thedevelopment of further nuclear plants post-2030.

Figure 13: Reduction in electricity prices byfleet size in base case scenario, 2020-2055

We assessed the sensitivity of the electricity priceimpact through developing scenarios that consideredalternative CfD strike prices, pass-through of costsavings, operational savings and the duration of CfDs.These are described in Table A4 in Appendix A andrepresent:

illustrative scenarios designed to illustrate lowerand higher impacts;

a lower scenario based on a £75/MWh CfD strikeprice, risk allocation agreements that limit thepass-through of design and build cost savings, nooperational savings (perhaps due to indexationoffsetting efficiency savings) and a 15 year CfD;

an upper scenario based on a £135/MWh CfDstrike price, full pass-through of design and buildcost savings and operational cost savings and a 25year CfD; and

a base case scenario based on £105/MWh CfD (thearithmetical average), risk allocation agreementsthat limit the pass-through of design and buildcost savings, operational savings and a 20 yearCfD.

The reductions in electricity price over the threescenarios are shown for a fleet of eight reactors inFigure 14.

Figure 14: Reduction in electricity prices byscenario for a fleet of eight reactors, 2020-2055

The fall in electricity prices due to a fleet of nuclearreactors feeds through to increased GDP andemployment through the mechanism described inAppendix A.

In our base case scenario, the fall in energy pricesbased on a fleet of four reactors translates into anincrease in £1.7bn of GDP and 12,000 additionalman years of employment or 500 jobs.

The economic impacts accumulate for additionalpairs of reactors as the cost savings build up,leading to increases of £5.9bn in GDP and 44,000man years of employment or 1,700 jobs for a fleetof eight reactors in our base case scenario.

Under our lower scenario, the economic impact fora fleet of eight reactors is estimated to provide anadditional £1.8bn of GDP and 12,000 man years ofadditional employment or 500 jobs.

Under our upper scenario the economic impact fora fleet of eight reactors is estimated to provide anadditional £10.9bn of GDP and 86,000 man yearsof employment or 3,300 jobs.

The sensitivities are shown in Figure 15 and Figure 16and described more fully in Appendix B.

Figure 15: Impact on GDP from reduced costof electricity

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Red

ucti

on

inele

ctr

icit

yp

rice

(%)

Fleet of 4 Fleet of 6 Fleet of 8

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Red

ucti

on

inele

ctr

icit

yp

rice

(%)

Lower scenario Central scenario Upper scenario

£0.0

£2.0

£4.0

£6.0

£8.0

£10.0

£12.0

Fleet of 4 Fleet of 6 Fleet of 8

GD

P(N

PV

£b

n)

Lower scenario Central scenario Upper scenario

The fleet effect:

The economic benefits of adopting a fleet approach to nuclear new build in the UK PwC 27

Figure 16: Impact on employment fromreduced cost of electricity

The time profile of economic impacts has beenconstrained to the period covered by the EMR CfDs solargely follows that of the fall in electricity prices inFigure 13. In our base case scenario, the impact onGDP and employment spans 26 years from 2023 until2049, with an average 1,700 additional jobs as shownin Figure 17.

Figure 17: Employment impact of reducedcost of electricity over time

8.3. Sensitivity analysisThree additional sensitivities are quantitatively testedagainst our base case assumptions for a fleet of eightreactors with respect to the impact on the cost ofelectricity. Compared to our base case results for afleet of eight reactors - an additional £6bn of GDP and44,000 additional man years of employment or 1,700jobs:

Conservative views on the level of cost reductionachievable produce additional GDP contributionsof £3bn, and an additional 26,000 man years ofemployment or 1,000 additional jobs.

optimistic views on the level of cost reductionachievable produce additional GDP contributionsof £8bn and an additional 59,000 man years ofemployment or 2,300 jobs.

In a scenario where total electricity generationproduced after 2030 continues to increaseaccording to the rate of increase forecast for the

latter half of the 2020’s24, the impact of a newnuclear fleet on electricity prices would lead to inan increase in GDP of £5.6bn and an additional41,000 man years of employment or 1,600 jobs.

In a scenario where wholesale electricity pricesremain constant after 2030, the impact of a newnuclear fleet on electricity prices would result in anincrease in GDP of£6.4bn and an additional49,000 man years of employment or 1,900additional jobs.

Further details are contained in Appendix B.

24 DECC “Fossil fuel wholesale and retail prices: Annex F” 2011

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Fleet of 4 Fleet of 6 Fleet of 8

Em

plo

ym

en

t(m

an

years

)