ns4053 winter term 2013 latin america: country briefs

TRANSCRIPT

NS4053 Winter Term 2013

Latin America: Country Briefs

Country Briefing Overview

• Latin America: Country Briefs

• Mexico – New Wave of Reforms

• Nicaragua – Increasingly Pragmatic

• Cuba – Uncertainty over Reforms

• Bolivia – Indigenous Development

• Argentina – Unstable Expansion

• Brazil – Uncertain Future

2

Mexico: New Wave of Reforms I

Mexico’s proximity to the U.S. should have allowed it to be much more wealthy than it is:

• Country has been characterized by slow growth:• On average annual GDP growth increased 3.4%

from 1971-2010• Slowing to 2.4% from 1981-2010• Average annual GDP per capita increased only

0.5% between 1981-2010• Global recession hit hard with GDP contracting

by 6.5% in 2009 -- country will not recover to 2008 levels until later this year

• If country had maintained average growth during 1950s and 1960s

• GDP per capita would be at least twice the current level

• Above South Korea and similar to Portugal 3

Mexico: New Wave of Reforms II

Causes of decline• Numerous policy errors

• Populist policies in early 1970s – inflationary pressures

• Mismanagement of oil wealth – use of oil revenues for social programs, not reinvestment in exploration and production

• Massive external debt• Dysfunctional political system

• No new institutions since the demise of the PRI in 2000

• One term for politicians reduces accountability • Severe Structural Impediments

• Poor education system – teachers’ union blocking reforms

• Rigid labor market – high costs of hiring and firing

• Restrictions on investments make it hard to attract sufficient foreign direct investment into key sectors -- energy

4

Mexico: New Wave of Reforms III

Political elites fail to agree of structural reforms because various macroeconomic indicators give mistaken impression that the economy is doing relatively well:

• Low inflation has been the norm since mid-1990s• U.S. Slowdowns, not domestic factors explain

recessions in 2001-02 and 2009• Public finances posted small deficits and even

surplus since the 1990s• Balance of payments shows small and manageable

balances• Economy grew around 5.1% in 2010 when 3.0% was

forecast – mainly just catch-up after the severe recession.

5

Mexico: New Wave of Reforms IV

At the start of 2012 Mexico faced a number of challenges:

• Economy appeared to be developing a vicious cycle of slower growth, stagnant reforms, instability, and declining growth:

• Faster than expected declining oil production was setting in,

• Low tax base, over dependence on oil revenues could possibly lead to a fiscal crisis

• Political deadlock might make needed reforms impossible

• Likely slow recovery of the U.S economy – increased competition from China put additional stress on the economy

• Further loss of export markets due to limited competition -- creating a chronic productivity gap with other emerging countries

• Problems compounded with deteriorating security situation

• Increased violence likely to take a heavy toll on investment and tourism, further suppressing economic recovery.

6

Mexico/China I

7

Mexico/China II

8

Mexico/China III

9

Mexico: New Wave of Reforms V

• With the election of the PRI’s Enrique Pena Nieto, the country is experiencing a new sense of optimism

• On December 2 Pena Nieto signed a pact with the leading political parties to achieve major changes:

• Focused on reducing high levels of drug-related violence

• Increasing social spending to benefit the poorest and promising reforms of the fiscal and energy sectors

• Also important: reforms in labor markets and education

• The President’s Position:

• after years of relative stagnation, Mexico can surge as an important economy

• actions must be taken immediately to boost the country’s long-term growth potential. 10

Mexico: New Wave of Reforms VI

Reform process off to a very good start

•Labor Reforms

•Intended to transform the massive informal labor market that has grown at the fringes of the law

•First attempt to overhaul the labor code since 1970

•Also a departure from previous PRI stance of not making any legal change that would show a “pro-business” bias and diminish worker rights

•Reform a necessity – World Economic Forum has ranked Mexico’s labor market as highly inefficient (rank 102 out of 144) Reasons included:

• rigidities in hiring and firing (113th)

• relatively low participation of females (121st)

11

Mexico: New Wave of Reforms VII

• Mexico’s labor market is for all practical purposes dual:

• A formal sector, with cumbersome regulations and where hiring and firing is costly; and

• An informal sector, mostly populated by small and limited businesses (usually with 1-2 employees) that do not stick to the labor code

• The informal market allows quick turnaround for many people seeking work (particularly as there is no unemployment insurance)

• It may account for one half of the country’s labor force

• Major change in the labor code is that it will admit several types of new contracts

• Trial periods allowed – employers can terminate without paying severance fees

• Initial training contracts – allow workers to acquire necessary knowledge and skills can also be terminated without severence pay

12

Mexico: New Wave of Reforms VIII

• Labor reforms also extend to some union activities• Surprise because PRI traditionally seen as closer

to labor unions• Labor reform is expected to improve Mexico’s

competitiveness in a number of ways

• It will transfer jobs previously in informal sector to the formal sector

• It will create new jobs, particularly among the youngest, oldest and women, due to the new allowable contracts

• More people will be allowed to hold more than one job and therefore increase the length of time worked per day

• Speedier resolutions between businesses and unions arising from mass firings are expected.

13

Mexico: New Wave of Reforms IX

• Education Reforms

• Mexico’s education system is highly deficient

• UNESCO – in 2009 at 5.3% of GDP Mexico’s spending on education is above the regional average – Cuba spends 13.1%

• Does not translate into student achievement

• OECD’s achievement tests, Mexico 48 out of 56 countries and the worst among OECD countries

• Although expenditures above regional average, not led o investment in school infrastructure and maintenance

• Only 3.34% Ministry of Education’s 2011 allocated for fixed assets – more than 96% to teachers’ salaries and pensions

• Main beneficiaries teachers affiliated to the powerful teachers unions 14

Mexico: New Wave of Reforms X

• Reforms main goal is to weaken the influence of the teacher union

• Reforms aims to create professional career structure free from union interference

• Access to teaching positions often political

• Promotions not based on merit

• Also the reforms aim to increase the autonomy of schools regarding their own infrastructure and operations.

• Still a long way to go in reforming eduation, but a very promising start.

• Energy Reforms

• Reform of Mexico’s energy sector will be debated during the first half of 2013

• The oil sector requires major reforms to guarantee its long-term sustainability

15

Mexico: New Wave of Reforms XI

• Petroleos Mexicanos (Pemex) holds a monopoly in the oil production sector and contributes 30-35% of Mexican public budget revenues

• The dependence of government finances on Pemex’s performance has hampered the company’s ability to invest in exploration and exploitation of new oil fields

• Underinvestment is reflected in declining production

• Gasoline imports currently represent around 50% of domestic demand

• Lack of sufficient financial resources has also raised concerns over Pemex’s safety record

• Limited reforms in 2008 opened up a few areas to private participation – constructing gas pipes and exploration in mature oil fields – impact has been limited

16

Mexico: New Wave of Reforms XII

• President has said he will promote a second energy reform given the negative long-term outlook for proved oil reserves

• However many obstacles

• PRI still divided between those that are more incined to stay with a resource nationalization party and those closer to a free market position

• Ambitious energy reform requires changing Mexican constitution – but this also requires state-level congresses to approve it.

• The company’s workers union one of the most powerful in the country and will likely oppose any substantive reform

• Opposition parties, PRD, and PAN will not support reform without major political concessions

17

Mexico: New Wave of Reforms XIII

• Competition Policy – Anti-Monopoly• The “Pact of Mexico” includes proposals to boost economic

competition and end monopolistic practices• Idea is that increased competition will promote investment

growth, job creation and technological innovation• Although mexico has become a flly integrated member of

global economyover last two decades:• It is still beset by institutions and laws that were at the heart

of the country’s earlier closed economy• Situation has prevented a level paly in felds from developing

across different sectors• Has created market distortions and inefficiencies athat affect

both consumers and producers

18

Mexico: New Wave of Reforms XIV

• As a result Mexico scored very low on several WEF indicators

• Intensity of local competition – 4.8 where one is the lease and 7 the most desirable outcome – ranked 75th

• At 3.2 score for extent of market dominance – places Mexico in 113th place

• Country fares poorly with regards to effectiveness of its anti-monopoly policy with a score of 3.5 ranking it 115th

• Sectors target for more competition

• Transport sector – foreign companies can own only up to 25% of domestic air travel firms. Similar in maritime transport

• Electronic media – television is a duopoly

• Fixed line telephone sector dominated by Carlos Slim’s Telmex – 80 % of the land line market

• Banking sector also in need of more competition• Problem: Powerful groups in industry and within

PRI will try to prevent major reforms

19

Mexico: Prospects 2013• The country’s political transition is occurring very

smoothly

• Provides a good foundation for new-founded optimism

• Highest priority of new government -- reduction in violence

• Calderon’s anti-cartel policies are blamed for the violence

• The PRI led-government wants success against cartels measured mainly by a fall in violence levels rather than quantizes of drugs seized or cartel leaders captured or killed

• With monetary and fiscal policies showing little room to boost growth, main economic challenge administration faces is to push through congress reforms to boost growth potential

• The labor reform has been approved with some modifications

• Fiscal end energy reform bills will be discussed in 2013

• If approved they are unlikely to be so far reaching as to raise the growth potential significantly

• Government will be effective at over-selling them – leading too overstated growth optimism.

20

Mexico: Forecast I

21

Mexico: Forecast (2013)

22

Mexico: Risks (2013)

• Forecast Risks

23

Mexico: Favorable Labor Costs

24

Nicaragua: Increasingly Pragmatic I

• Nicaragua going through a period of great change amid high uncertainty

• With the return of Daniel Ortega and the Sandinistas to power in 2006 many changes have taken place

• Country has become testing ground for many of the revolutionary and often contradictory economic and political trends sweeping Latin America

• Ortega's increasing authoritarianism at national level while vibrant grass roots democracy at the local level

• Implementation of neo-liberal, market-driven development within confides of a leftist, state centered populist agenda

• Outcome of these economic and political contrasts will

• Have profound effect on the country’s future development

• Perhaps impact the region as a whole.

25

Nicaragua: Increasingly Pragmatic II

• Although Ortega campaigned on a platform of Christianity, socialism and solidarity with Venezuela’s Hugo Chavez:

• Regime has few similarities to other ALBA (Alianza Bolivariana) countries Cuba, Venezuela, Ecuador, Bolivia

• Ortega has been politically authoritarian, pro-business, socially populist and above all pragmatic

• Marxist slogans are mostly gone as is wide-spread government involvement in the economy

• Ortega’s economic model retains many of the legal and regulatory underpinnings of his predecessor’s neo liberal policies

• In the government’s October 2007 Agreement with the IMF was a pledge to implement free market policies linked to targets on fiscal discipline, spending on poverty and energy regulation

26

Nicaragua: Increasingly Pragmatic III

• While originally opposed to CAFTA-DR, Ortega and Sandinistas have approached the project with pragmatism and creativity

• With labor costs rising in Mexico, Nicaragua began positioning itself to capture share of rapidly expanding U.S. supply-chain, near-shoring business

• The country has lowered many restrictions on trade becoming one of the most open countries in the region

• To address Sandinista social concerns over “sweat-shop” labor in country’s free trade zones, government designed governance program that includes labor unions as equal partners in negotiations with foreign investors

• Results have been success in creating jobs and the spectrum of products exported

27

CAFTA-DR Trade Freedom

28

1995 1997 1999 2001 2003 2005 2007 2009 201110

20

30

40

50

60

70

80

90

Tra

de

Fre

edo

m S

core

CountryNicaraguaCosta RicaHondurasEl SalvadorGuatemalaDR

Source: Heritage House Index of Economic Freedom, 2012

Nicaragua: Increasingly Pragmatic IV

• Overall the economy has done well since 2006

• Resources managed prudently

• Excessive inflation has been avoided

• Much of the crime and drug-related violence in the region is absent in Nicaragua

• Growth rates are picking up – after declining by 1.5% in the world-wide recession year of 2009, real GDP grew at 4.5% in 2010, 4.7% in 2001 and is expected to expand at 3.7% in 2012.

• According to the IMF poverty rates declined from 48.3% of population in 2005 to 42.5% in 2009 with rural areas showing the most improvement

• Poverty still a major problem

• 63% of the rural population still falls beneath the poverty level

• 15% of the overall population still lives in extreme poverty

• A sustained growth rate of 5% or greater is necessary for the country to achieve significant poverty reduction 29

Nicaragua: Increasingly Pragmatic V

• The country’s limited revenue base and close IMF budgetary scrutiny have forced government to rely heavily on international aid to finance poverty reduction programs

• Hugo Chavez has provided more then $2 billion over lat five years

• However much of Venezuela’s aid has simply gone to offset loss of aid from other sources – big cutbacks in U.S. and EU aid

• The country faces a number of challenges and – loss of Venezuelan aid would be major problem

• Venezuelan aid and trade may have added full percentage point to Nicaragua’s growth in 2010-11

• If the US suspends its annual property waver, it would jeopardize nearly $1.4 billion in development loans over next five years – economy might collapse

30

Nicaragua: Increasingly Pragmatic VI

• While growth and poverty reduction have been good under Ortega, the economy rests on a fragile institutional base.

• The economy has opened up to trade but there has been a decline in overall economic freedom

• There has been a secular decline in the critical governance indicator, voice and accountable

• While political stability has increased, only Guatemala ranks below Nicaragua

• The country has by far the lowest level of government effectiveness, and regulatory quality in the region

• On the other hand the rule of law has improved under Ortega, with only Costa Rica having a (albeit significantly) higher ranking

• Unfortunately there has been little progress in combatting corruption with Nicaragua having one of the lowest scores in the region.

31

CAFTA-DR Voice/Accountability

32

1996 2000 2003 2005 2007 2009 201120

30

40

50

60

70

80

90V

oic

e an

d A

cco

un

tab

ility

(p

erce

nti

le)

CountryNicaraguaCosta RicaHondurasEl SalvadorGuatemalaDR

Source: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the extent to which a country's citizens are able to participate in selecting their government, as well as freedom of expression, freedom of association, and a free media.

CAFTA-DR Political Stability/Absence of Violence

33

1996 2000 2003 2005 2007 2009 201110

20

30

40

50

60

70

80

90

Po

litic

al S

tab

ility

/Ab

sen

ce o

f V

iole

nce

(p

erce

nti

le)

CountryNicaraguaCosta RicaHondurasEl SalvadorGuatemalaDR

Source: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the likelihood that the government will be destabilized or overthrown by unconstitutional or violent means, including politically-motivated violence and terrorism.

CAFTA-DR Government Effectiveness

34

1996 2000 2003 2005 2007 2009 201115

20

25

30

35

40

45

50

55

60

65

70G

ove

rnm

ent

Eff

ecti

ven

ess

(p

erce

nti

le)

CountryNicaraguaCosta RicaHondurasEl SalvadorGuatemalaDR

Source: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the quality of public services, the quality of the civil service and the degree of its independence from political pressures, the quality of policy formulation and implementation, and the credibility of the government's commitment to such policies.

CAFTA-DR Regulatory Quality

35

1996 2000 2003 2005 2007 2009 201120

30

40

50

60

70

80

Reg

ula

tory

Qu

alit

y (p

erce

nti

le)

CountryNicaraguaCosta RicaHondurasEl SalvadorGuatemalaDR

Source: World Bank, Worldwide Governance Indicators, 1996-2011

Reflects perceptions of the ability of the government to formulate and implement sound policies and regulations that permit and promote private sector development.

CAFTA-DA Rule of Law

36

1996 2000 2003 2005 2007 2009 201110

20

30

40

50

60

70

80R

ule

of

Law

(p

erc

enti

le)

CountryNicaraguaCosta RicaHondurasEl SalvadorGuatemalaDR

Source: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the extent to which agents have confidence in and abide by the rules of society, and in particular the quality of contract enforcement, property rights, the police, and the courts, as well as the likelihood of crime and violence.

CAFTA-DA Control of Corruption

37

1996 2000 2003 2005 2007 2009 201110

20

30

40

50

60

70

80C

on

tro

l of

Co

rru

pti

on

(p

erce

nti

le)

CountryNicaraguaCosta RicaHondurasEl SalvadorGuatemalaDR

Source: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the extent to which public power is exercised for private gain, including both petty and grand forms of corruption, as well as "capture" of the state by elites and private interests.

CAFTA-DR Economic Freedom

38

1995 1997 1999 2001 2003 2005 2007 2009 201140

45

50

55

60

65

70

75

80

Ove

rall

Eco

no

mic

Fre

edo

m S

core

CountryNicaraguaCosta RicaHondurasEl SalvadorGuatemalaDR

Source: Heritage House Index of Economic Freedom, 2012

Nicaragua: Increasingly Pragmatic VII

• Assessment• Nicaragua’s poor record in establishing a firm institutional

setting helps explain why growth has not grown at ranges where significant reductions in poverty occur

• The institutional setting does not foster increased productivity

• The IMF has identified a declining trend in productivity starting in the 2000s.

• The one bright spot has been the country’s progress in developing trade within CAFTA-DR

• In early 2013 Managua was listed as one of the top 100 outsourcing destination

• CAFTA-DR reinforces the idea that growth in trade correlates closely with policies that promote

• economic stability,

• private investment in production,

• public investment in education, infrastructure, logistics and good governance

39

Nicaragua: Increasingly Pragmatic VIII

• The pragmatic solution for Nicaragua’s future may well be to simply let a CAFTA-DAR virtuous circle of trade reform increased productivity and growth take its course.

40

Uncertainty in Cuba I

The Cuban economy is going through a period of uncertainty

• The global crisis hit Cuba hard causing very low rates of growth in the last several years.

• The government does not have sufficient resources to maintain the old Communist system

• Since taking over from his brother Fidel, President Raul Castro has prepared Cubans for the need for economic efficiency and cutting excessive state spending.

• China has become Cuba’s top creditor – nearly $4 billion in loans, but not open ended

• Raul Castro is tying the country’s fate to an economic reform process inspired by the Chinese model

• One plan was to cut 500,000 state employees by March 2011 and another 800,000 later.

• An expanding private sector was expected to absorb these workers.

41

Uncertainty in Cuba II

Government’s private sector plans are vague• Small scale cooperatives are to be created, particularly in the

service sector• About 250,000 new licenses for self employment will be issued

– along lines during the mid-1990s crisis• Conservatives in the party see the private sector as a

necessary emergency measure – a politically dangerous evil to be kept small and eliminated when state finances allow.

• Reform forces see “market socialism” in which the private sector is a key driver of the economy

• Most likely a continuing leadership tug-of-war over the need to control and limit the private sector is more likely than an all out move to market socialism.

• In the short run, partially dismantling the paternalist state and loss of state employment will bring widespread anxiety and uncertainty which could turn into wide-spread frustration threatening to disrupt social stability 42

Uncertainty in Cuba III

To date little progress – liberalizing reforms are advancing slowly• Reform is still very piecemeal• Private sector expansion so far has been vary limited• Plans to dismiss state employees have been largely halted

until the private sector’s absorption capacity grows.• With Hugo Chavez’s health condition uncertain, country faces

prospect of loosing vital Venezuelan subsidies• Production remains sluggish, inflation is up and corruption is

eroding regime legitimacy.• Anti-corruption drive is only adding to popular cynicism about

elites rather than generating trust for the regime• Still reform approval has convinced China to increase economic

engagement in Cuba• China now key economic partner. While trade with Venezuela

has stagnated in recent years trade with China now up to 1.8 $billion

• China particularly involved in onshore oil drilling and offshore exploration along with several other international companies

• To date there have been no significant discoveries with several firms pulling out.

43

Uncertainty in Cuba IV

• Currently the country appears incapable of generating very high rates of economic growth

• Unemployment is not high – at the end of 2012 3.8% up from 3.2% in 2011, and expected to reach 4.3% in 2013

• So far the process of restructuring has yielded GDP growth of only 2.7% in 2011 and 3.1% for 2012

• Figures suggest the economy requires a new stimulus to escape from stagnation.

• The slack labor market is likely to erode support for the government’s cautious approach to reform and encourage more radical measures

• Clearly the reforms to date have not been sufficient to revive the economy

• The new non-state sector accounts for only 8% of the labor force

• Due to the lack of availability of alternative employment, the government has held back on state sector rationalization 44

Cuba: Recent Rates of Growth

45

Uncertainty in Cuba V • The main constraints on the growth of the non-state sector are

• The lack of finance and

• Supplies of essential inputs

• The government is cautious about credit because of fear of creating an unmanageable amount of bad debt and fear of fuelling inflation

• The shortage of supplies stems from the inability of either the state or non-state producers to expand capacity

• In turn this is mainly due to a lack of finance.• The problem of investment financing is the cause of the severe

decapitalization, but no sign that the government has enacted policies to bring an upturn in capital formation

• Cuba’s investment/GDP ratio has fluctuated around 11% for the past 20 years – lower than any other country in the region.

• Cuba therefore seems to be stuck in a low productivity trap with little prospects for escaping without a major shift in policy to open up access to FDI. 46

Bolivia’s Indigenous Development I

• Indigenous groups account for 66% of Bolivia’s population• Since 2005 the Bolivian government has attempted to

empower these long disenfranchised and deprived groups• An experiment in democracy and poverty reduction

• Requires complex policy trade-offs that carry potentially high costs

• Ultimate results far from certain

• Started with Evo Morales election to president

• Promised democratic coexistence, social change and national unity

• Quickly passed constitutional reforms that included changes in

• the role of the state,

• private property, and

• management of natural resources and taxes.

• Development strategy straight-forward – maximize resource exports and the redistribution of their rents

47

Bolivia’s Indigenous Development II

• First step was to begin renationalizing firms that had been privatized under the neo-liberal regimes of the 1980s and 1990s. Mainly in the areas of:

• Electricity,

• Water

• Hydrocaprons

• Railways and

• Telecoms

• Government claims to offer “fair” compensation based on an “independent” evaluation of worth

• Recently have begun to nationalize firms that were never under government ownership.

• Cost – largely very low levels of FDI that the government needs to develop hydrocarbons and other resources

48

Bolivia’s Indigenous Development III

• Second, Morales has been reluctant to end coca production – a major cash crop for indigenous groups

• In response the U.S. has allowed the Andean Trade Preferences’ Act to expire

• Loss of its right to export tariff-free to the U.S. has hurt Bolivia’s manufacturing sector, especially textiles

• Has also reduced the profitability of developing the country’s fast lithium deposits through reducing the value added that can be created in Bolivia

• In early 2013 Bolivia received an exemption from the U.N. that legalizes coca chewing and production for local consumption within the country

• Concern is now that many criminal groups will step up drug manufacturing in more remote parts of the country

49

Bolivia’s Indigenous Development IV

• Ironically, despite policies favoring indigenous groups, the government has been facing increased opposition from them in a series of protests:

• Stopping highway construction linking Bolivia with Brazil and developing the vast eastern low-lands

• Slowing down hydrocarbon development – despite fact that most social programs are financed from gas exports

• Are also slowing down lithium development

• Empirically protests are reducing the country’s rate of economic growth by over one percent per annum

• Despite low levels of foreign investment, lack of favorable access to U.S. markets and the destructive effects of ongoing protests, Bolivia’s progress has been surprisingly good.

50

Bolivia’s Indigenous Development V

• Poverty reduction has been especially successful

• In 2002 about 62% of the population lived in poverty and 37% in extreme poverty

• By 2010 only 42% of Bolivians were living in poverty and 22% in extreme poverty

• Critics claim poverty reduction simply occurred as a result of Bolivia’s relatively high resource-based economic growth during this period

• ECLAC however fund that 66 percent of Bolivia’s poverty reduction was distribution-based rather than growth based

• Supported by fact that Bolivia also experienced a fairly sharp drop in income inequality during this period

• Along with Argentina, Venezuela and Nicaragua, Bolivia achieved a falling Gini coefficient of more than 2% per annum between 2002 and 2011 51

Bolivia’s Indigenous Development VI

• Despite the administration’s reputation for radicalism, macroeconomic policies have been fairly orthodox

• Control of inflation has been good – around 6%

• Foreign exchange reserves are more than adequate

• Debt has been reduced to a sustainable level

• Country was able to tap the international capital markets for the first time since 1917 – half billion dollars at very low ten year rate of 4.875

• In January 2012 IMF placed Bolivia in an elite group of LA countries as having “a relatively solid position to withstand sizeable shocks.”

• Bolivia used to be at the bottom of the Legatum Prosperity Index for Latin America – has now overtaken Guatemala and Honduras

52

Bolivia’s Indigenous Development VII

• By other measures Bolivia under Morales has not done as well

• The EIU’s 2011 Democracy Index ranks Bolivia 84the out of 167 countries – a slight drop from 81st in 2010

• Reflects poor scores for its electoral process and civil liberties

• Ranks only head of Honduras (85th), Ecuador (89th), Nicaragua (91st), Venezuela (97th), Haiti (114th) and Cuba (126th).

• The World Bank Governance Indicators show some gains in government effectiveness and regulatory quality, but little progress in other key areas.

• There has been a sharp deterioration in the country’s economic freedom index.

53

Andean Countries: Voice and Accountability

1996 2000 2003 2005 2007 2009 201120

25

30

35

40

45

50

55

60

Voic

e an

d A

cco

un

tab

ility

(p

erce

nti

le)

CountryBoliviaColombiaEcuadorPeruVenezuela

Source: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the extent to which a country's citizens are able to participate in selecting their government, as well as freedom of expression, freedom of association, and a free media.

54

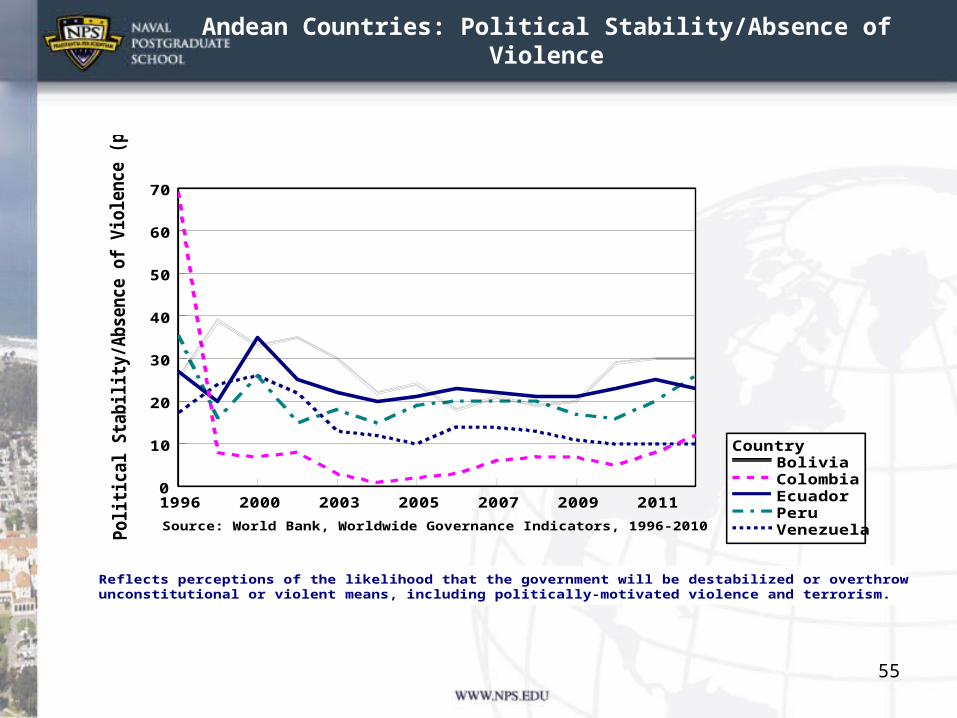

Andean Countries: Political Stability/Absence of Violence

1996 2000 2003 2005 2007 2009 20110

10

20

30

40

50

60

70

CountryBoliviaColombiaEcuadorPeruVenezuelaSource: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the likelihood that the government will be destabilized or overthrown by unconstitutional or violent means, including politically-motivated violence and terrorism.

55

Andean Countries: Government Effectiveness

56

1996 2000 2003 2005 2007 2009 201110

20

30

40

50

60

70G

ove

rnm

ent

Eff

ecti

ven

ess

(per

cen

tile

)

CountryBoliviaColombiaEcuadorPeruVenezuelaSource: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the quality of public services, the quality of the civil service and the degree of its independence from political pressures, the quality of policy formulation and implementation, and the credibility of the government's commitment to such policies.

Andean Countries: Regulatory Quality

1996 2000 2003 2005 2007 2009 20110

10

20

30

40

50

60

70

80

Reg

ula

tory

Qu

alit

y (p

erce

nti

le)

CountryBoliviaColombiaEcuadorPeruVenezuela

Source: World Bank, Worldwide Governance Indicators, 1996-2011

Reflects perceptions of the ability of the government to formulate and implement sound policies and regulations that permit and promote private sector development.

57

Andean Countries: Rule of Law

1996 2000 2003 2005 2007 2009 20110

5

10

15

20

25

30

35

40

45

50

Ru

le o

f L

aw (

per

cen

tile

)

CountryBoliviaColombiaEcuadorPeruVenezuelaSource: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the extent to which agents have confidence in and abide by the rules of society, and in particular the quality of contract enforcement, property rights, the police, and the courts, as well as the likelihood of crime and violence.

58

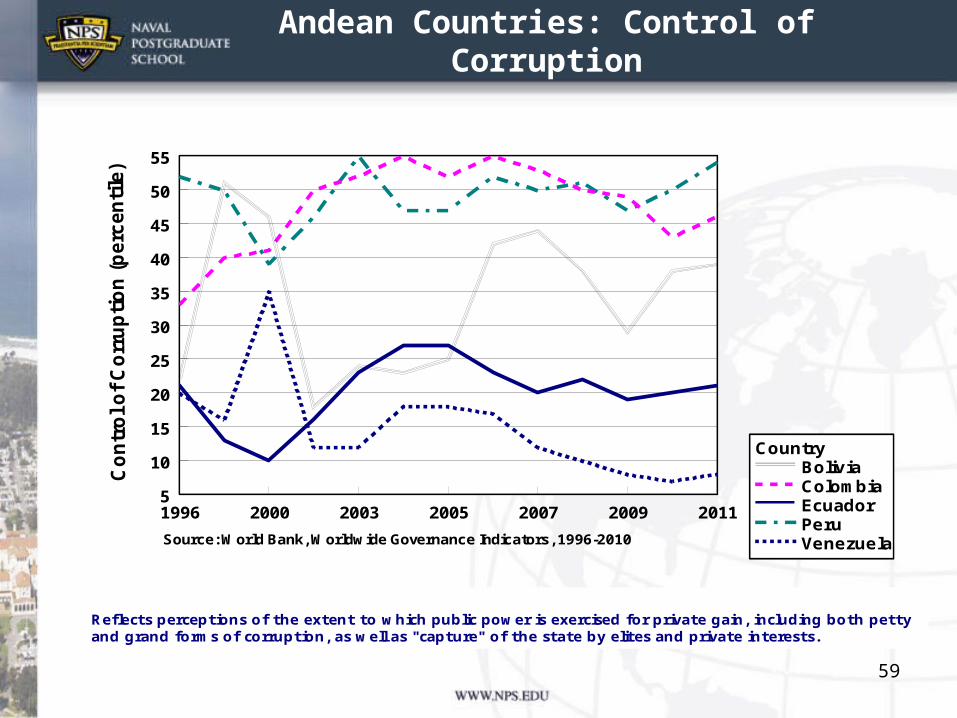

Andean Countries: Control of Corruption

1996 2000 2003 2005 2007 2009 20115

10

15

20

25

30

35

40

45

50

55

Co

ntr

ol o

f C

orr

up

tio

n (

perc

en

tile

)

CountryBoliviaColombiaEcuadorPeruVenezuelaSource: World Bank, Worldwide Governance Indicators, 1996-2010

Reflects perceptions of the extent to which public power is exercised for private gain, including both petty and grand forms of corruption, as well as "capture" of the state by elites and private interests.

59

Andean Countries: Overall Economic Freedom

60

1995 1997 1999 2001 2003 2005 2007 2009 2011 201335

40

45

50

55

60

65

70

Ove

rall

Eco

no

mic

Fre

edo

m S

core

CountryBoliviaColombiaEcuadorPeruVenezuela

Source: Heritage House Index of Economic Freedom, 2013

Andean Countries: Trade Freedom

1995 1997 1999 2001 2003 2005 2007 2009 2011 201350

55

60

65

70

75

80

85

90

Tra

de

Fre

edo

m S

core

CountryBoliviaColombiaEcuadorPeruVenezuela

Source: Heritage House Index of Economic Freedom, 2013

61

Bolivia’s Indigenous Development VIII

Questions for the future:

•How much of the country’s good performance under Morales due to very favorable commodity boom during most years?

•How might the situation change with falling export revenues?

•Will competing social claims overwhelm the government?

•Will the government’s poor progress in governance and economic reforms severely limit its ability to efficiently manage nationalized firms?

•How will Bolivia’s coca policies play out?

•Will the anger demonstrated in wide based protests be effectively channeled into constructive demands for better democracy and governance?

62

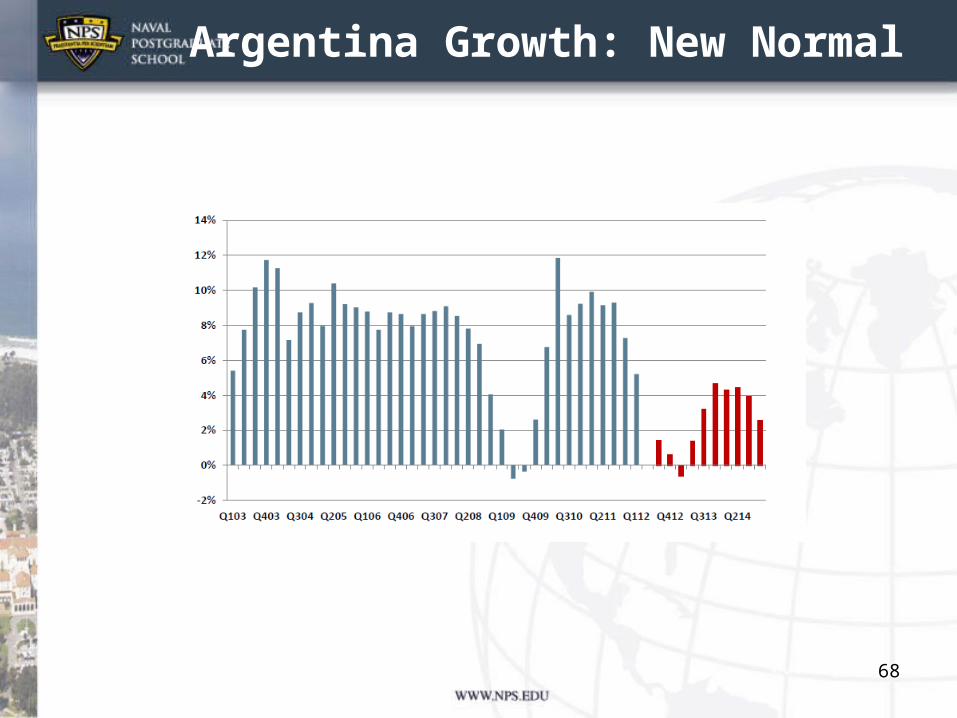

Argentina’s Unsustainable Expansion I

Argentina has been held up as a model for Greece:• Instead of the usual prescription of austerity, the

government has pursued expansionary monetary and fiscal policies.

• Fortunate to hit a commodity boom which brought in windfall foreign exchange earnings used to build up reserves.

• Rapid rates of growth (7.6% per annum) since devaluating its currency and defaulting on its debts after the 2001-02 crisis

• However because of its debt defaults the country has been frozen out of international capital markets

• Because international borrowing is not an option the country had to maintain large levels of F/X reserves through balance of payments surpluses

• Meant keeping a weak currency to maintain competitiveness in export markets 63

Argentina’s Unsustainable Expansion II

Growth model is hitting diminishing returns• Attempts to keep very competitive with overvalued

exchange rate meant buying up dollars, but could not prevent the resulting growth in money supply

• Inflationary pressures building up, suppressed by price controls and misleading estimates of the price index.

• Price controls on energy have reduced productive supplies as have export taxes on agricultural commodities.

• Diversion of resources from agriculture to industry has led to declining productivity.

• In the last several years increasing protectionism and capital controls introduced to conserve foreign exchange reserves

• Uncertainty over government policy and increased controls have resulted in capital flight and a sharp fall in foreign exchange reserves

• Massive subsidies for energy users reached US 8 billion or 2% of GDP

64

Argentina’s Unsustainable Expansion III

Country on verge of sharp contraction:• Days of public spending growth rates of 40%, real

wage increases and negative interest rates are over.• Government now up against a binding constraint –

very limited in its ability to finance further spending• Has started cutting subsidies for fiscal reasons• Facing increased wage demands from strong unions• Concerned that any slowdown in Chinese economy

will result in commodity price declines• Potential crisis in Europe will also have a major

impact on the economy• The recent slow-down in the Brazilian economy is

also taking a heavy toll on manufactured exports.• Country likely to find growth declines to considerably

less than half that over the last 10 years.

65

Argentina: Forecast

66

Argentina: Risk Assessment

67

Argentina Growth: New Normal

68

Brazilian Take-Off The country has emerged as one of the BRICs – Brazil, Russia,

India and China. Enablers:• Sound macroeconomic policies – fiscal responsibility• Reasonably open trade and domestic polices• Political transitions that don’t disrupt the growth process• New growth phase began under Fernando Henrique Cardoso

and the inflation busting Real Plan of 1994

• Began enacting long list of strategic reforms enabling sustainable faster rates of economic growth

• Enabled the country to come out of the crisis much more rapidly than anticipated – taking advantage of trade with China

• Major oil discoveries in addition to a new commodity boom should help accelerate growth

• Since 2003 more than 32 million people (total population 198 million) entered middle class with 20 million rising above poverty

• May use increased economic strength to counter-balance U.S. influence in the region, especially in trade

• However recent developments have raised questions as to the country’s future growth

69

Brazilian UnderperformanceAfter recovering quickly from the 2008-09 crisis, growing at

7.5% in 2010, the economy has declined rapidly• The economy experienced a sharp deceleration in 2011

with depressed demand• As consumer and business confidence remain depressed,

private sector credit has also reversed and growth rates are diminishing

• Although the exchange rate has weakened, it is still to strong, putting manufacturing at a distinct disadvantage – variant of the Dutch Disease.

• Slack growth in manufacturing at same time high demand for services has created a type of stagflation --

• Inflation will continue to be a problem due to structural factors – low productivity rates, elevated salary increases, infrastructure bottlenecks and import restrictions

• While the economy has picked up a bit forecasts put growth in 2012 at 3.5% maximum or possibly 2.9%

• How fast Brazil can grow and for how long remains a question due to a number of structural impediments that will constrain the economy unless addressed.

70

Brazil: Structural Problems• Because savers do not view Brazilian and non-Brazilian

assets as perfect substitutes, low domestic savings mean perennially very high (nominal and real) interest rates.

• To offset the impact on investment of high capital costs, the state-owned Brazilian Development Bank offers tens of billions of dollars in long term loans at zero or negative interest rates – unfortunately those who receive the loans are not necessarily the most productive

• Both public and private sector under save, but the government’s dearth savings is the bigger problem

• Not do to lack of revenue – tax receipts as a share of GDP are the highest in Latin America

• Problem is state invests little because it has to many inflexible current expenditures

• Public sector pensions account for 6.8% GDP and are 2.5 times higher than private pensions

• Leaves little for infrastructure needed to create new exports and the higher paying jobs essential in reducing the country’s great income inequalities.

• Will require major reforms, but the political will may not be there.

71

Brazil: Sharp Deceleration in Demand

72

Brazil’s Uncertain FutureMajor concerns for the future• The key constraint is lack of domestic savings. • If Brazil raises its investment rate to 23% of GDP from

today’s 19% (as it must to build World Cup infrastructure) it will have to run a current account deficit and rely on external savings equivalent to 3-4% GDP for years.

• That gap can be easily financed with today’s abundant liquidity, but a disorderly European default or eventual US monetary tightening could change that.

• There is a good possibility that the country’s recent commodity boom is an aberration which will soon shift as soon as China shifts transitions from its resource intensive growth model or as the economy begins to slow-down its growth

• A permanent decline in commodity prices would lead to currency depreciation and trigger negative wealth and income effects which would in turn adversely affect economic growth.

73

Brazil: Forecast I

74

Brazil Forecast II

75

Brazil Forecast Risks

76

Brazil: Gradual Recovery

77

Latin America-China Economic Relations I

Trade between China and LAC has been booming for a decade• Within last 5 years bilateral trade has increased by over 160

percent• In period since financial crisis, China has become the number

one trading partner of Brazil, Chile and Peru.• Relationship not limited to trade: Chinese firms have

dramatically stepped up FDI in the region• In last two years China has become the top source of FDI in

Brazil and Peru• Pattern has been primarily driven by China’s expanding for

Latin American mineral, agricultural and energy resources. • Chinese manufactures to the region have grown dramatically • Boom in trade and investment has not had an equal impact

throughout. Exports to China largely concentrated in a small number of raw materials (copper, iron ore, soy and oil) from core group of countries (Argentina, Brazil, Chile, and Peru).

78

China’s Share of LAC Exports: 2002, 2008 (%)

79

Latin America-China Economic Relations II

• Other countries like Mexico have a less complementary and more competitive relationship

• Even Brazil has found domestic manufacturers have come under heavy pressure from Chinese competition

• Relationship with China has produced high expectations but is giving way to rising anxieties

• During financial crisis China a ray of hope – China weathered the crisis much better than traditional markets.

• Now as China slows down, concerns are expressed over falling into pattern of boom and bust commodity boom cycles, deindustrialization, rising currencies (Dutch-Disease) and overdependence on a single market like China

• Surge in investment from China also encountering local sensitivities about foreign ownership of agricultural land

• Initial hopes of manufactured exports to China largely disappointed.

• Much of initial excitement about increased interaction with China based on negative view of U.S. – this is now changing.

80

Future ConcernsFuture problems for the region center around the fact that LAC’s

economies are notoriously illicit and under taxed:• Leaves governments without the fiscal resources necessary to

invest in a better future

• China’s thirst for raw materials means the region will remain highly vulnerable to boom and bust cycles and external shocks

• Continuing low taxes and underinvestment in education, infrastructure, public services and technology means Latin America will fall further behind other regions – remain a second tier region.

• Economic crisis has exacerbated the difficulties in reaching a consensus for establishing long term goals and associated necessary reforms to break out of the resource cycle

• Illicit networks centered around drug trafficking are, in a vicious cycle of illegality, increasingly contaminating political and judicial systems in the region – prevent consensus building around long-term goals

• Painful cuts in public services and increasing crime and social tensions have made coalition building all the more challenging

• Result in many countries may be a vicious cycle of short term political optimization resulting in sub-par, unstable growth and development

Summing UpKey Points• Emerging economies will outpace the growth of the

advanced economies. This disparity in growth has only been exacerbated by the financial crisis

• Slow growth in the US and Eurozone will cause a continued shift in Latin American trade to Asia

• Latin America’s recent improved growth performance is encouraging , but largely based on favorable commodity prices – most countries still very vulnerable to external shocks.

• LAC grow growth prospects are relatively favorable providing they can move ahead with improvements in governance and economic reforms

• China’s role in Latin America has the potential to contribute significantly to growth through providing expanded investment – China state banks have lent more than $75 billion to the region since 2005.

• China’s rise in the region provides more competition for the U.S., but the US still has a number of long run advantages such as security assistance, cultural ties and market for many Latin American non-commodity exports.

82