november 2012 perspectives on the uk retail · pdf filenovember 2012 perspectives on the uk...

TRANSCRIPT

Financial Services

NOVEMBER 2012

PERSPECTIVES ON THE UK RETAIL BANKING MARKET

AUTHORS

Jason Quarry Simon Low Greg Hill Rishi Baveja

Copyright © 2012 Oliver Wyman 2

INTRODUCTION

The UK retail banking market faces a

period of change. It is confronted with

unprecedented regulatory pressures, new

digital technologies, growing competition,

and an uncertain economic climate. Banks

will need to respond with long-overdue

work on product design, sales models, cost

structures, and customer servicing.

Through this process of change, market

shares are likely to become more fluid than

they have been in the past, both among the

Big 5 and the wide range of product specialist

and full-service challenger institutions.

This poses a threat to the incumbent

firms, yet considerable opportunities

too. Profit potential in the business is

attractive – certainly more attractive than

comparable EU retail banking markets and

many other parts of the UK banking industry.

There is also an opportunity to help rebuild

banks’ reputations in the eyes of the public.

In this context, this report highlights

five main challenges for UK retail bank

management teams:

• Adjusting product structures: Achieving a

more even and transparent distribution of

profits prompted by newly interventionist

regulators and gradually increasing

customer sophistication

• Embracing positive changes in

distribution: Getting ahead with digital;

taking the brave steps needed to reshape

branch networks

• Efficiency in the cost structure: Beyond

incremental changes, thinking more

radically and structurally about cost

deployment and areas of inefficiency

• Re-designing the savings and investment

business: Creating a meaningful role for

banks in investment product sales and

increasing the profile of the savings

product set

• Customer service and conduct: Raising

the bar across the board

This report is structured as follows:

1. MARKET OVERVIEW

2. FORCES FOR CHANGE

3. IMPLICATIONS FOR RETAIL BANKS

4. CONSIDERATIONS FOR CHALLENGERS

AND NEW ENTRANTS

5. CONCLUSIONS

Copyright © 2012 Oliver Wyman 3

1. MARKET OVERVIEW

PROFITABILITY

Leaving aside Payment Protection Insurance

(PPI) compensation provisions, banks’ core

returns in UK retail remain high and stable,

both by the standards of other European

retail markets, and by the standards of other

banking businesses in the UK. This has been

achieved in the face of strong headwinds:

a low interest rate environment and resultant

erosion of deposit income, continued

pressure on credit quality as a result of the

stagnant economy, and the regulatory,

funding, and capital pressures on

the banking industry.

ExHIBIT 1: UK RETAIL AND SMALL BUSINESS BANKING ROE, 2004-11

15%

5%

10%

20%

0%

25%

AVERAGE UK RETAIL BANKING RETURNS*,†

ROE, 2004–2011

2004 2005 2006 2007 2008 2009 2010 2011

* Market RoE weighted across banks by asset size. RoEs normalised with capital calculated as 11% of RWAs and a tax rate of

30%. Institutions included: A&L, Barclays, B&B, Co-operative Bank (pre-Verde), HBOS, HSBC, LBG, Nationwide, Northern Rock,

Northern Rock Asset Management, RBS, Santander, Tesco, YBS. Note that different banks report on different bases, therefore

inclusion and definition of small business banking dependent upon institution specific reporting structures

† Excludes exceptional items and charges (e.g. PPI charges)

Source: Company data; Oliver Wyman analysis

Copyright © 2012 Oliver Wyman 4

ExHIBIT 2: PROFIT POOLS IN CORE RETAIL BANKING PRODUCTS, UK VS. SELECTED EUROPEAN MARKETS (CORE PRODUCTS ONLY)*, †

55

45

35

15

25

FRANCE GERMANY ITALY SPAIN UK

4.3 7.2 6.4 5.5 15.1

14.0% 14.2% 22.3% 24.5% 33.3%

86.0% 85.8% 77.7% 75.5% 66.7%

REVENUES (£BN), 2011

PROFIT BEFORE TAX†† (£BN)

PROFIT/REVENUE

COST/REVENUE

Mortgages

Time deposits

Personal loans

Current accounts

Credit cards and overdrafts

Instant access savings(includes ISA's)

30.9

50.7

28.6

22.5

45.3

-5

5

0

* “Core retail banking products” are: time deposits, Instant access savings, current accounts, credit cards and overdrafts, personal loans

and mortgages

† Euros converted to GBP using Oanda 2011 average yearly exchange rate

†† Excludes exceptional items and charges (e.g. PPI charges); excludes head office costs; country-level FTP assumed

Source: Oliver Wyman analysis

Furthermore, returns are well spread across

the market. Major, full-service retail banking

providers are returning about 20% on equity

(when removing exceptional charges). Newer

supermarket banks also generate strong

returns despite their lack of operating scale

and small back-books. Successful monolines

can make very high returns when risk costs

are running at relatively low levels. Only a

minority of players generate single digit RoEs,

and many of these are institutions that are

not shareholder-owned.

Five main factors explain the comparatively

high profitability of UK banks:

• Greater ability to re-price the back-

book than in other European markets,

particularly in mortgages. Mortgages

were systematically under-priced pre-

crisis, but UK banks have been able to

re-price the majority of their back-book

due to short-term SVR reversion periods

(see Exhibit 3). This is not an option in

countries with a large number of legacy

lifetime trackers, as in Ireland, and long-

term fixed rate products, as in Germany

• Lower credit losses in the UK than many

other European economies

• More shareholder-owned banks than

other markets, with greater cost and

profit discipline

• Linked to the above, less dense and

better utilised branch networks. The

UK has about 200 branches per million

inhabitants; many European countries

have more than 400 (see Exhibit 4)

• More consistency in the regional banking

markets than other countries, with better

scale efficiencies

Copyright © 2012 Oliver Wyman 5

ExHIBIT 3: RE-PRICING IN UK MORTGAGE BOOKS

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0%

3.5%

2004 2006 20072005 2008 2009 2010 2011 2012

SPREAD OVER BASE RATE

Floating stockspread

Floating new business/flow spread

Source: Bank of England

ExHIBIT 4: BRANCH DENSITY OF THE UK VS. SELECTED EUROPEAN MARKETS

COUNTRY

BRANCHES/MM INHABITANTS

EU POSITION ANNUAL CLOSURE RATECHANGE/TREND2007 2010

Spain 1,025 940 -2.8%

France 623 603 -1.1%

Italy 563 559 -0.3%

Germany 484 484 0.0%

EU average 473 463 -0.8%

Switzerland 468 442 -1.9%

Finland 325 280 -4.9%

Sweden 220 210 -1.7%

UK 206 199 -1.1%

Netherlands 222 174 -7.7%

Rapid decline Moderate decline Neutral/limited change

Source: European Banking Federation

Copyright © 2012 Oliver Wyman 6

However, there are also some less

healthy elements to the UK profitability

picture which may be unsustainable going

forwards, particularly if subject to future

regulatory intervention.

First, the business continues to rely on some

revenue streams that are opaque to customers,

such as overdraft charges, net interest income on

current accounts, interchange income on credit

cards, mortgage product fees and insurance

cross-sell revenue. PPI mis-selling was an

extreme example of this. It has seriously

damaged the reputation and financial

position of the sector, with approximately

£11 billion of industry provisions, a figure

that is expected to increase further.

Second, customer profitability remains

skewed. Although such skews are inherent

to many parts of financial services and other

industries, the UK retail banking business

offers up some extreme examples. In both

current accounts and credit cards, 10-30%

of customers often make up more than 90%

of profits, with a meaningful proportion of

unprofitable customers for providers.

Finally, the back-book and associated re-pricing

constitutes a significant part of the profit

pool. This has led to complexity in product

structures, and added to the degree of customer

profitability skew described above.

As explained later in this report, these

historic sources of profit will need to be

rebalanced in response to regulator and

customer pressure: pricing will become more

transparent and profits will be extracted

more evenly across the customer base.

The end-point should be a more equitable

value-exchange between customers and

shareholders across the product set.

The extent and speed of the change here

will be heavily influenced by the scale of

regulatory intervention. There is clearly a role

for regulators here to help rein in the product

and pricing structures that have resulted

from low customer price sensitivity, but at

this stage it is unclear how much latitude

regulators will leave banks in this regard.

COMPETITION AND CONSUMER CHOICE

Retail banking customers in the UK can

choose between a wide range of suppliers,

products and channels. UK customers rely

less on branches than most continental

Europeans, with most products and services

now available via remote channels.

Despite a large variety of available suppliers,

volumes remain concentrated among the

high-street banks in many products (see

Exhibit 5) – though no more so than in

other markets. For example, in both current

account and savings products, France,

Sweden, Canada, and Australia exhibit

market concentrations that are similar to or

higher than the UK’s (though Italy, Germany,

and the US have less concentrated markets).

An important cause of this concentration is

low customer switching rates1, particularly

in current accounts (see Exhibit 6). The

stickiness of the main banking relationship

is borne out in a recent Oliver Wyman

Customer Survey which highlighted that 57%

of customers have been with their main bank

or building society for 11 or more years2.

1 Pre-crisis mortgage switching rates were high due to re-mortgaging. This is a structural feature of the UK mortgage market. Credit availability and reduced price differentials between back- and front-book products have restricted this switching post-crisis.

2 Oliver Wyman Customer Survey ( July 2012).

Copyright © 2012 Oliver Wyman 7

ExHIBIT 5: OVERVIEW OF THE UK SUPPLY-SIDE

Deposits Mortgages Unsecuredlending*

SHARE BY PLAYER TYPE, 2011

TOP 7BY SHARE

Big 5, Next 3

Big 5, Largest 2

Aspiring full service challengers

Major Building Societies/Co-operatives

Rest of market

Branchnetwork

LBG, RBS,Barclays, HSBC,

Santander, Nationwide, Co-operative

LBG, HSBC, Santander,

Nationwide, Barclays, RBS, Co-operative

LBG, Santander, Nationwide,

Barclays, RBS, HSBC, NRAM

LBG, Barclays, RBS, HSBC,

Santander, Tesco Bank, M&S

50%

100%

0%

* Includes credit cards, personal loans, overdrafts and car finance

Note: Included institutions: Big 5: Barclays, HSBC, LBG, RBS, Santander; Major Building Societies/Co-operatives: Co-operative

Bank (pre-Verde), NAB, Nationwide; Aspiring full service challengers: Metro Bank, Tesco Bank, Virgin Money

Source: Company data; Bank of England; European Banking Federation; Oliver Wyman analysis

ExHIBIT 6: CUSTOMER SWITCHING RATES

8%

4%

0%

12%

2000 2002 20032001 2004 2005 2006 2007 2008 20102009

SURVEY RESPONDENTS WHO SWITCHED ACCOUNT IN THE PREVIOUS 12 MONTHS

Savings

Main personal curent account

Mortgages

Creditcards

SME main bank relationship

Source: Independent Commission on Banking Final Report, Figure 7.3

Copyright © 2012 Oliver Wyman 8

There are several reasons for customer stickiness:

• Nationwide banking networks (cf. US regional banking structure) mean that customers do not need to change banks when re-locating

• Continued high volumes of products sold through branch networks, favouring the subset of institutions with large physical networks

• Limited consumer engagement with, or understanding of, banking compared with other goods and services they consume

• Switching is perceived to cost more in terms of effort than it is worth in terms of finding better prices or service (recent survey evidence suggests 55% of customers believe switching current accounts would be a hassle, and 51% of customers say they are more likely to switch current accounts following the introduction of the planned Q4 2013 switching service, with 16% much more likely to switch3)

3 Quadrangle Customer Survey on behalf of Independent Commission on Banking, August 2011.

Customer stickiness does not necessarily equate to satisfaction. A review of newspaper headlines over the last few years would suggest mass dissatisfaction with the banking sector. However, such headlines can be misleading. Consider the following:

• “Do I receive a good service from my bank?” typically polls much better than “do I feel the banking industry is doing a good job?”

• Complaints volumes ex-PPI have been falling

• No retail industry has perfect service. The trade-off between cost and quality is inherent to any business, including financial services

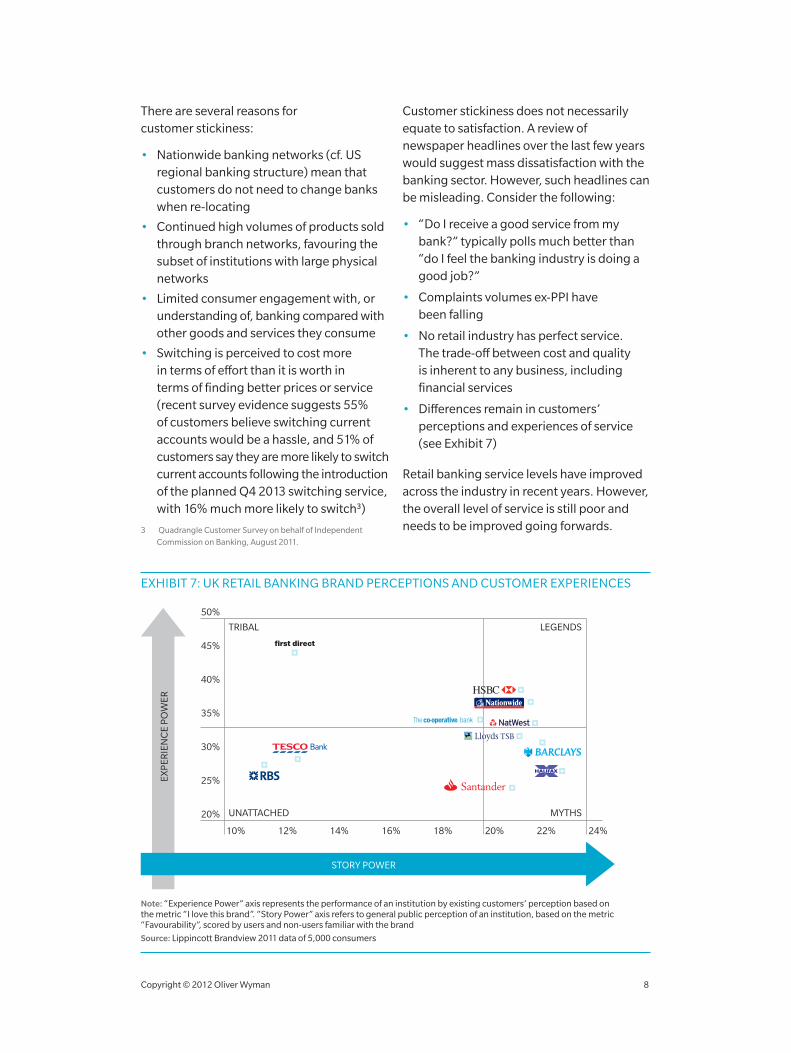

• Differences remain in customers’ perceptions and experiences of service (see Exhibit 7)

Retail banking service levels have improved across the industry in recent years. However, the overall level of service is still poor and needs to be improved going forwards.

ExHIBIT 7: UK RETAIL BANKING BRAND PERCEPTIONS AND CUSTOMER ExPERIENCES

30%

25%

45%

35%

40%

20%

50%

24%20% 22%18%16%14%12%10%

TRIBAL

UNATTACHED

LEGENDS

MYTHS

STORY POWER

EXP

ERIE

NC

E P

OW

ER

Note: “Experience Power” axis represents the performance of an institution by existing customers’ perception based on the metric “I love this brand”. “Story Power” axis refers to general public perception of an institution, based on the metric “Favourability”, scored by users and non-users familiar with the brand

Source: Lippincott Brandview 2011 data of 5,000 consumers

Copyright © 2012 Oliver Wyman 9

2. FORCES FOR CHANGE

High profitability, often opaque pricing and

dramatic customer value skews have been

features of the UK retail banking market for

many years. Significant changes have often

been predicted, but they have not occurred.

However, the forces for change are now

stronger than ever. We consider four drivers

of change in today’s market:

• Regulation

• Growing digital demand

• Competition and new management teams

• Macroeconomic adjustments

REGULATION

Post-crisis, banking has been hit by an

unprecedented amount of new and

proposed regulation. UK retail banking is

no different, with five main components:

ringfencing, capital & funding regulation,

direct government intervention, consumer

protection, and conduct risk requirements.

First, the ICB and now Liikanen make it

increasingly likely that UK banks4 will have

to “ringfence” retail activities in a separately

capitalised subsidiary. This would result

in a new dynamic of competition between

ringfenced and non-ringfenced retail players,

with structurally higher capital and funding

costs for the ringfenced entities, and a

complex and costly separation challenge for

the “universal bank” high-street players.

Second, leaving aside the ringfencing issue,

regulation is pushing up capital requirements

and funding costs. A combination of changes

to regulatory capital levels minima (Basel

4 Note that ringfencing reforms are not applicable to institutions with less than £25 billion of retail deposits.

III, ICB, G-SIFI) and potential changes to risk

weighting methodology5 will result in retail

banks holding more equity capital. At the

same time, funding costs (through liquidity

buffer costs and the now established norm of

higher funding costs for long-term assets) are

adding to financial resource costs.

Third, government intervention is biting.

Competition regulation will alter the industry,

with the large mandated sale of LBG and

RBS portfolios re-distributing market share

across the sector. The 7-day current account

switching service planned for Q4 2013 “will

be free to use and provide a guarantee that

no customer will suffer any financial loss if

any mistakes occur”6. This should reduce

barriers to current account switching and

thereby drive higher switching rates. The

government’s Funding for Lending scheme

will also influence asset-side businesses by

increasing lending volumes; and similar

future schemes may also be pushed as the

UK government looks to further boost the

macroeconomic recovery.

Fourth, consumer protection regulation

is changing the market. Two examples are

the Consumer Credit Directive and the

Retail Distribution Review (RDR). Both

increase compliance costs and the latter a

requirement to adapt the fundamentals of

the bank-intermediated saving industry.

Going forwards, other areas (e.g. the current

ongoing regulatory work on interchange

income) may also start to be affected.

5 Potential reforms not yet agreed, although recent Financial Policy Committee comments have called for a re-examination of risk weights.

6 HM Treasury; Banking Reform: Delivering Stability and Supporting a Sustainable Economy (2011).

Copyright © 2012 Oliver Wyman 10

ExHIBIT 8: ROLES OF AND CHALLENGES FOR THE FCA

CREATION OF FCA SIGNIFIES A CLEAR CHANGE IN REGULATORY APPROACH…

…WILL REQUIRE SYSTEMATIC AND RIGOROUS CONDUCT RISK MANAGEMENT…

…WITH SOME SPECIFIC AREAS OF SHORT-TERM REGULATORY FOCUS LIKELY

• FCA established to “protect and enhance confidence in UK financial system”

• Early indications are that the FCA will be more interventionist and pro-active than the FSA

− Increased thematic reviews

− Reviews of business models and strategy in relation to conduct risk

− Increased intervention where risks have not yet materialised

• FCA have begun to “firm up” definition of conduct risk, with much broader scope than TCF

− Measurement and control much earlier in value chain

− Customer detriment includes potential monetary loss and customer suitability

• Conduct risk is prevalent throughout a Bank’s activities – it is driven by principles and a “spirit” of good conduct throughout the organisation

• Requires development and articulation of conduct risk management approach – broader than just upgrading compliance function

• Embed in organisation, governance and policies with suitable MI and metrics

• Significant implications for front-to-end product design process – likely push towards simplification and transparency

• Re-focussing of channel management to ensure appropriate sales processes and supporting infrastructure

• PPI and swaps mis-selling: Orderly and efficient continuation of the clean up

• Incentives: Announced strong outcomes from review of sales incentives practices at 22 banks in September 2012

• Current accounts: Portability and “free banking”

• Packaged accounts: New rules published in July 2012 regarding package suitability and claim eligibility – expect market to continue to grow

• Interest Only mortgages: Potential focus on repayment vehicles and sales practices

Last, after more than £12 billion in fines and

compensation claims in 2011-2012 – much

of it PPI related – conduct risk and the newly

created FCA will be a major force in retail

banking. The advent of the FCA is likely to

result in more interventionist and pro-active

regulation. If implemented along the lines

currently outlined, we expect the FCA to play

a role in shifting profitability towards a more

balanced model (see Exhibit 8).

GROWING DIGITAL DEMAND

Consumer preferences are changing. This

is most visible in the growing use of the

internet (with supporting mobile technology)

as a sales and service channel. There are now

almost 45 million internet accounts in the

UK7. For many types of transaction, certain

consumer segments are no longer reverting

to branches. In the future, we expect two

types of products (see Exhibit 9):

• Digital products: savings, cards and loans,

shifting from current levels of ~30% digital

sales to ~50% by 2020

• Face-to-face products: mortgages and

current accounts, with lower digital sales

rates and continued use of face-to-face

channels as the primary sales channel

We also expect consumers will be

increasingly willing to consider alternative

banking providers. While convenient

branch location is still an important driver

of new bank selection, recent Oliver Wyman

research shows that price, online banking

services and reputation are now of similar

importance to customers (see Exhibit 10).

7 BBA, as at 2011.

Copyright © 2012 Oliver Wyman 11

ExHIBIT 9: CHANNEL USAGE VARIANCE ACROSS PRODUCTS

50%

2011

Currentaccounts

Mortgages Savings Creditcards

Personalloans

2020 2011 2020 2011 2020 2011 20112020 2020

100%

SHARE OF PRODUCT SALES BY CHANNEL2011 AND 2020

Branch

Call centre

Digital

Intermediary

“DIGITAL” PRODUCTS“FACE-TO-FACE”PRODUCTS

0%

Source: Oliver Wyman analysis

ExHIBIT 10: CUSTOMER SURVEY – INFLUENCES ON BANK SELECTION

40%

60%

20%

80%

Interest rate/price of

productsand service

Quality ofonline

banking

Reputation Convenientlocation of

branch

Recommendationfrom current

customers

Other Availabilityof mobile app

0%

DRIVERS OF NEW BANK SELECTION*

* % of respondents

Source: Oliver Wyman Customer Survey ( July 2012)

Copyright © 2012 Oliver Wyman 12

COMPETITION AND NEW MANAGEMENT TEAMS

A combination of regulation and recognition

of profit potential in the sector are increasing

competition in UK banking. The continued

growth of Santander, the proposed Co-

operative acquisition of Verde, the enlarged

and growing Virgin Money business, the

development of fuller-service supermarket

banks and the expansion of Metro Bank

are contributing to a meaningful increase

in competition.

Another important factor will be the

influence of new senior management

teams in the UK’s retail banks. Several

of the Big 5 have shaken up their senior

management teams in retail banking

and injected new leadership. Many are

looking to make changes to their business

and have several common agenda items:

notably cost management, branch network

re-shaping and digital sales focus, and

product simplification.

MACROECONOMIC ADJUSTMENTS

Retail banking profitability is dependent on

macroeconomic conditions. In particular,

consumer credit quality and underlying base

rates are key drivers. A spike in credit losses

remains possible given the fragility of the

UK and broader European economy today.

However, in the medium-term a gradual

economic recovery and a slow improvement

in credit quality are most likely. Similarly,

medium-term interest rises (likely 2014+) have

the potential to increase current account and

savings profitability, which have been eroded

by the very low interest rates maintained by

the Bank of England since the financial crisis.

As Exhibit 11 illustrates, there has historically been

a clear relationship between savings pricing and

LIBOR8. We expect this directional trend to persist,

although – given the increased importance of

deposit funding – the relationship will likely not

hold to the degree that it has done historically.

8 The relationship is shown here for instant access savings accounts. A similar relationship can be observed historically for fixed term savings accounts.

ExHIBIT 11: HISTORICAL RELATIONSHIP BETWEEN INSTANT ACCESS SAVINGS SPREAD AND LIBOR (1995-2010)

-3%

-2%

-4%

2%

-1%

1%

0%

-5%

3%

RATE – 3M LIBOR

3M LIBOR

9% 7% 8% 6% 5% 4% 3% 2% 1% 0%

Higher interest rates historically resulted in higher margins on savings accounts

Average instant access accounts

Competitive online players*

* Online banking data from 2003-2010

Source: Bank of England; Oliver Wyman analysis

Copyright © 2012 Oliver Wyman 13

To this end, as base rates rise, deposits

become more profitable. While mortgage

margins will narrow, we expect them to move

disproportionally, and slowly, relative to base

rate movements given duration and SVR

stickiness. The net effect is therefore likely to be

positive, as illustrated in Exhibit 12. We would

expect large gains to industry profitability in

significant base rate rise scenarios, noting

that gains in liability-side income will also

be somewhat offset by increased credit risk

losses in mortgage products.

ExHIBIT 12: PROFIT POOL SENSITIVITY TO INTEREST RATES (CORE PRODUCTS ONLY)

ESTIMATED IMPACT OF CHANGE IN BOE BASE RATESON UK RETAIL BANKING PROFITABILITY 2013

CHANGE IN PRE TAX PROFIT (£BN)

2.50

3.75

1.25

0.00

5.00

0.5% 1.5% 2.0%1.0% 2.5% 3.0%

CHANGE IN BOE BASE RATE

Note: Estimated impact reflects steady state, single year impact of a base rate rise on profitability. Reactions to base rate changes

have been estimated taking into account historical pass through rates, adjusting for expected competitor dynamics (e.g. higher

competition for deposits). A range of outcomes have been assumed reflecting the uncertainty of future market dynamics

Source: Oliver Wyman analysis

THE NET EFFECT ON PROFIT POOLS

Our base case outcome would see the

benefits of macroeconomic recovery

largely offset by the compliance costs of

new regulation and margin erosion from

increased competition and regulatory-

driven product changes. More specifically,

we expect the main influences on bank

profitability and RoE to be:

+ Deposit gains with modest medium-term

interest rate rises

+ Continued credit loss improvements

due to macroeconomic stabilisation

+ Further cost reductions

− Modest margin erosion from

increased competition

− Loss of some revenue streams

from product re-design

− Higher capital and funding costs

Our base case outcome would suggest

a similar industry-wide RoE in 2014-5 to

today, but on a larger profit pool, as shown

in Exhibit 13.

Copyright © 2012 Oliver Wyman 14

ExHIBIT 13: BASE CASE UK RETAIL PROFIT POOL FORECASTS (CORE PRODUCTS ONLY)

2011

REVENUE (£BN)

PROFIT BEFORETAX* (£BN)

ROE

Operatingcosts

Profitbefore tax

RoE

Riskcosts

41.9

2012E 2013E 2014E 2015E

15.1 15.6 15.8 16.0 17.0

PROFIT/REVENUE 33.3% 36.5% 37.7% 38.1% 39.3%

COST/REVENUE 66.7% 63.5% 62.3% 61.9% 60.7%

30 12%

40 16%

60 24%

50 20%

10 4%

20 8%

43.345.3

42.042.7

REVENUE AND ROE FORECASTS (2011-2015)

0 0%

* Excludes exceptional items and charges (e.g. PPI charges); excludes head office costs

Source: Oliver Wyman analysis

However, there are major downside risks to this picture. Notably:

• Continued low interest rate environment

and resultant dampened profitability

• Medium-term economic stagnation and

declining credit quality

• Regulatory overshoot on ringfencing

“toughness” and/or capital and funding

requirements

• Failure on the part of the banks to deliver

cost efficiencies, particularly in branch

network management and IT/operations

• Future provisions against as-yet-unknown

historic conduct & standards issues

• Harsher than expected competitive

environment significantly damaging

profit margins in core profit-generating

products today

In aggregate this could put ~10% RoE

“at risk” for the industry as a whole.

Copyright © 2012 Oliver Wyman 15

3. IMPLICATIONS FOR RETAIL BANKS

A large-scale shift in market share away

from the Big 5 is unlikely in the near future.

However, we believe that there is potential

for market share to materially shift within

this group and that now is a uniquely

positive time for smaller challengers to win

market share.

Banks’ management teams should apply

themselves to five main issues:

• Adjusting product structures: Achieving a

more even and transparent distribution of

profits prompted by newly interventionist

regulators and gradually increasing

customer sophistication

• Embracing positive changes in

distribution: Getting ahead with digital;

taking the brave steps needed to reshape

branch networks

• Efficiency in the cost structure: Beyond

incremental changes, thinking more

radically and structurally about cost

deployment and potential areas

of inefficiency

• Re-designing the savings and asset-

gathering business: Creating a meaningful

role for banks in investment product sales

and increasing the profile of the savings

product set

• Customer service, banking standards, and

conduct: Raising the bar across the board

ADJUSTING PRODUCT STRUCTURES

Banks’ product structures have evolved

in response to customer behaviour. Large

differences between front- and back-book

pricing take advantage of low customer

switching rates, and opaque charging

mechanisms are a reaction to customers’

reluctance to pay simple fees.

This pricing model is becoming less

sustainable. Customers are gradually becoming

more sophisticated in their purchasing and a

newly interventionist regulator is more likely

to take action around “appropriateness” of

product and pricing structures.

This must mean a simpler and more

transparently priced product set, and a fairer

distribution of banks’ costs and revenues across

their customer base as a result. We see several

areas where banks should act proactively:

current account pricing and fees-for-service

(an area where many banks are already

starting to evolve in ways that benefit both

customers and shareholders); the structure

of overdraft charges; back-book/front-book

pricing differentials in savings and mortgages;

interchange structures; mortgage fees; and

approaches to cross-sell of insurance products.

The experience of other markets – for

example, the US experience in current

account fee introductions – is that the

process of product restructuring can result

in meaningful shifts in market share between

banks who embrace change positively and

thoughtfully and banks that are merely

reactive and remain resistant to changes.

Copyright © 2012 Oliver Wyman 16

ExHIBIT 14: CASE STUDY OF BRANCH RESHAPING

1. LIBERATION OF TIMEIN THE BRANCH

• Activity study in the branch (Activity identification, Time-and-Motion)

• Classification of activities according to migratibility to the middle/back office

• Liberation of ~2,800 FTE worth of seller time (various seller roles)

• Development of detailed migration plan and piloting

• Segmentation of customer base according to profitability and channel usage behaviour

• Development of segment specific migration techniques aligned with the brand of the client

• Development and implementation of detailed campaign sequences

• Migration of ~100 million transactions with associatedtime liberation

• Improvement of the market data environment to focus sales activities on market potential

• Alignment of incentive systems on market specific value potential

• Implementation of sales support unit to provide relevant data

• Training of sales in new data and incentive system environment

• 16% YoY sales productivity lift

2. MIGRATION OF CUSTOMERS TO THE RIGHT CHANNEL

3. CONVERSION OF FREED TIME INTO SALES RESULTS

EMBRACING POSITIVE CHANGES IN DISTRIBUTION

We estimate that shifts in channel usage

behaviours will lead to at least £2 billion of

potential cost savings for the industry by

2020. Branch and telephone channels will

be less important in future because of a

reduction in over-the-counter cheque and

cash transactions and a shift to self-servicing

in digital and ATM channels.

Branches will remain critical to the

distribution of core products and services.

But the structure and role of branches will

change. Banks have begun to react to this

challenge, but we believe that there is

significant further change required.

Branch closure is not the only lever to

be pulled in network management. To

date, many banks have focussed on

branch closures, capacity optimisation,

traffic optimisation and organisational

streamlining. The focus is now shifting

towards freeing up seller time, ensuring

customers are using the most effective

channel and using the time saved to boost

sales. A final wave of development will be

needed, including process re-engineering

and automation, capacity optimisation via

hybrid staff roles (e.g. sales roles at peak

hours, processing roles off-peak), value-

aligned service propositions, and branch

format mix optimisation.

Below is an example of a recent client

engagement in a top-tier European bank

where we tackled the second wave of the

branch optimisation challenge.

Beyond the branch network, the evolution of

the digital offering will also be a key theme in

distribution. Customers now consistently

Copyright © 2012 Oliver Wyman 17

see the digital offering as one of the top 3

drivers for choosing banking providers.

Banks today tend to excel in different areas:

some have distinguished themselves through

product availability; others through digital

account servicing innovations; others

have worked harder on integrating digital

customer touch points with phone and

branch channels; others have started to

use digital data more smartly. No bank has

excelled across the board and all remain at an

early stage of development in understanding

and managing the profitability of the digital

business. Looking forward, most banks

are rightly looking to improve in this area,

through rounding out digital capabilities and

looking harder at the current and potential

impacts of digital on profitability and

customer behaviours.

EFFICIENCY IN THE COST STRUCTURE

Cost efficiency in retail banking has a dual value:

improved overall economics, and an ability to

better deliver aggressive pricing and service

strategies to win market share when needed.

Most UK banks – particularly the large

incumbents – have focussed on cost cutting

in the past two years. Particular attention

has been paid to tactical cost cutting and

reducing head office costs by removing

layers of management.

The goal should not just be lower costs, but

making the right trade-offs between cost and

customer service/product offerings. Our

view on the main cost levers for the industry

is shown in Exhibit 16.

ExHIBIT 15: TYPICAL UK RETAIL BANKING COST STRUCTURE

KEY COSTSPROPORTION TOTAL COST BASE

Distribution• Branch ~75% of distribution costs (physical and sta� costs)• Digital • Call centres• ATM• Marketing

IT• Systems (hardware and software)• Support/maintenance• Shared services• Web and mobile investment

Head O�ce• Senior and mid-management• Support functions (e.g. Risk, Finance, HR)• Administrative costs

Operations• Payments• Account servicing• Collections

Other• Central costs from Group• Programmes and investment

100%

80%

60%

40%

20%

0%

Source: Oliver Wyman analysis

Copyright © 2012 Oliver Wyman 18

ExHIBIT 16: COST LEVERS IN RETAIL BANKING

LEVER TYPICAL ACTIONSEXTENT TAPPED IN THE UK MARKET

Tactical actions • Cut marginal underperforming staff across the business

• Stop discretionary projects

• Cut contractor levels

• Tactical infrastructure cost reductions

• Sharpen marketing spend – fewer top priority initiatives – and track success/return on spend

High

Branch network reshaping

• Branch closures in marginal locations

• “Machining” branches

• Centralise services

• Increase use of remote video advisory

• Increase use of mobile advisory

• Shift to mixed tier 1/2 real estate – big signage but staff on 2/3rd floors

Medium

Organisational simplification

• Spans and layers; remove unneeded management roles

• Simplify product/channel/region matrices

• Business manager/COO consolidation

• Simplification/reduction of “luxury” innovation/product development/customer experience groups

Low

Staff productivity • Process re-engineering in operations

• Sales effectiveness and incentives work

• Hybrid roles (sales and operational roles) for staff in branches

Medium

(Large scale) Infrastructure reductions

• Investment-driven IT cuts; all attempting to “clean the slate” and simplify in a particular area

• Offshoring/outsourcing operations

• Re-assess Group allocations and re-align shared services (particularly around payments platforms, IT, elements of Finance)

• Adjust (lower) unnecessarily high service timings

Medium

Legacy business reductions

• Rationalise the product register

• Exit sub-scale legacy products

Low

Strategic footprint • Explore fundamental decisions on market participation and depth across products/regions

• Particular focus on foreign businesses

Low until recently

Demand management • Cut unvalued services, encouraging efficient customer behaviours

• Most common focus around current accounts, payments choices, SME services

Low

Copyright © 2012 Oliver Wyman 19

RE-DESIGNING THE SAVINGS AND INVESTMENT BUSINESS

The RDR is forcing banks to reconsider this

business. UK retail banks have historically

struggled to make the economics work as

revenue generating products are regulated

and so require expensive distribution.

Following the RDR, major incumbents have

further scaled back on advised offerings

as these concerns have magnified, with

Barclays, HSBC and most recently LBG

exiting the mass-market advisory market.

It will be unfortunate if banks choose to simply

ignore large parts of the investment market

(i.e. pensions and other long-term savings), no

longer playing the role of the “savings prompt”

for mass-market retail customers, not only for

the informed consumers but for the broader

economy. However, there is a real risk of this

because mass-market customers are unlikely

to pay fees inflated by RDR and so banks are

unlikely to sell advised products.

At the same time, deposits are increasing

in importance as a source of bank funding,

and as a future profit generator (assuming

medium-term interest rates rise). Banks should

take bold moves with their deposit gathering

businesses. Specifically, they should:

• Provide mass-market consumers with

clear options in self-directed investment

products and “savings prompts”, with

smart usage of digital channels

• Design an advisory service for the affluent

segment that clients will pay for; too

often these roles add little value and are

treated with suspicion. Ensuring a credible

affluent proposition is a major challenge

that most in the UK have yet to crack

• Make a push to win share in the savings

account market in advance of medium-

term rate rises; reconsidering pricing

strategies to achieve this

• Take a holistic view of deposit gathering at

Group level – decide where deposits can best

be gathered at any particular time and reflect

this in pricing and marketing, rather than

leaving these decisions at business unit level

CUSTOMER SERVICE, BANKING STANDARDS, AND CONDUCT

Service standards and conduct have become

the focus of political and regulatory attention,

for example, the ongoing Parliamentary

Commission on Banking Standards. As a

result, compliance costs have increased

and are likely to increase further. However,

beyond this, we expect banks will need

to more fundamentally change their

approaches in both service and conduct.

Management should have three priorities

for service:

• Raise awareness of the importance of

customer satisfaction across the board:

improve quality and accuracy of service

MI, higher prioritisation of service issues

on management agenda

• Integrate service considerations into

proposition design and pricing strategies:

differentiate high-quality service offerings,

either for an optional fee or for high value

clients, offer a higher standard of service

(e.g. same day card replacement, call centre

responses within 3 rings, faster mortgage

processing times etc.) while ensuring that

base standards are not compromised

• Improve underlying service quality via

fundamental operational re-design

incorporating management best practice

techniques (lean, six sigma, TQM, etc.)

Copyright © 2012 Oliver Wyman 20

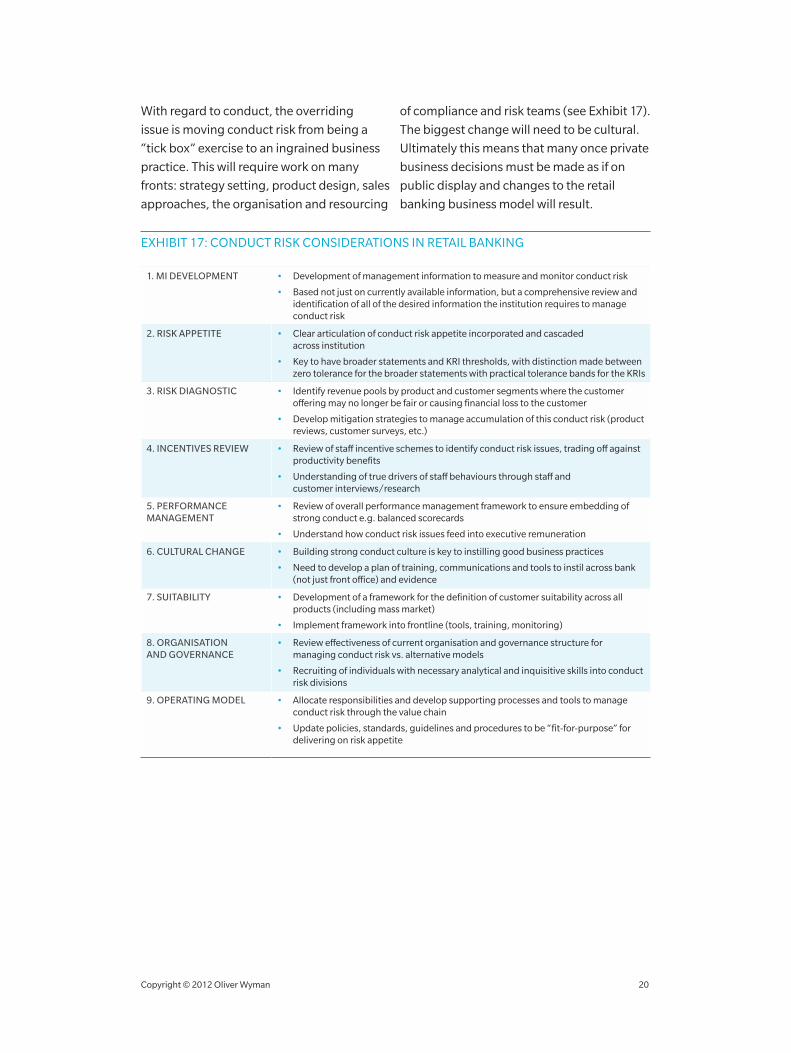

With regard to conduct, the overriding

issue is moving conduct risk from being a

“tick box” exercise to an ingrained business

practice. This will require work on many

fronts: strategy setting, product design, sales

approaches, the organisation and resourcing

of compliance and risk teams (see Exhibit 17).

The biggest change will need to be cultural.

Ultimately this means that many once private

business decisions must be made as if on

public display and changes to the retail

banking business model will result.

ExHIBIT 17: CONDUCT RISK CONSIDERATIONS IN RETAIL BANKING

1. MI DEVELOPMENT • Development of management information to measure and monitor conduct risk

• Based not just on currently available information, but a comprehensive review and identification of all of the desired information the institution requires to manage conduct risk

2. RISK APPETITE • Clear articulation of conduct risk appetite incorporated and cascaded across institution

• Key to have broader statements and KRI thresholds, with distinction made between zero tolerance for the broader statements with practical tolerance bands for the KRIs

3. RISK DIAGNOSTIC • Identify revenue pools by product and customer segments where the customer offering may no longer be fair or causing financial loss to the customer

• Develop mitigation strategies to manage accumulation of this conduct risk (product reviews, customer surveys, etc.)

4. INCENTIVES REVIEW • Review of staff incentive schemes to identify conduct risk issues, trading off against productivity benefits

• Understanding of true drivers of staff behaviours through staff and customer interviews/research

5. PERFORMANCE MANAGEMENT

• Review of overall performance management framework to ensure embedding of strong conduct e.g. balanced scorecards

• Understand how conduct risk issues feed into executive remuneration

6. CULTURAL CHANGE • Building strong conduct culture is key to instilling good business practices

• Need to develop a plan of training, communications and tools to instil across bank (not just front office) and evidence

7. SUITABILITY • Development of a framework for the definition of customer suitability across all products (including mass market)

• Implement framework into frontline (tools, training, monitoring)

8. ORGANISATION AND GOVERNANCE

• Review effectiveness of current organisation and governance structure for managing conduct risk vs. alternative models

• Recruiting of individuals with necessary analytical and inquisitive skills into conduct risk divisions

9. OPERATING MODEL • Allocate responsibilities and develop supporting processes and tools to manage conduct risk through the value chain

• Update policies, standards, guidelines and procedures to be “fit-for-purpose” for delivering on risk appetite

Copyright © 2012 Oliver Wyman 21

4. CONSIDERATIONS FOR CHALLENGERS AND NEW ENTRANTS

Challengers can adapt to changes more

easily and more quickly than large

incumbents. However, the lesson from

history is that a bold and focussed approach

is required to win share in a market where

customer switching rates remain low in

many products.

Challengers and new entrants enjoy the best

opportunities in the following areas:

ExPLOITING ALTERNATIVE BUSINESS MODELS

• Alliances with other retail firms: Alliances

with retailers is not a new concept in UK

retail banking. To date, supermarkets

have been the main operators via white

labelled offerings with banks. However,

the landscape is changing. Tesco

Bank is evolving towards a full service

independent bank and M&S Money has

announced the launch of 50 branches.

Scale has yet to be reached, particularly in

vanilla banking products, but we believe

that retailers can win share, particularly

by taking advantage of existing physical

and digital footflow and leveraging the

customer purchasing data at their disposal

• Direct Banking: Some see the Direct

Banking model as flawed, pointing to

customer resistance to cross-sell, low

margins and limited growth potential.

However, First Direct has proved that

share can be acquired in the UK (albeit

with some branch access), and we have

shown in previous research9 that some

European Direct Banks generate similar

levels of profitability per customer as

traditional bricks and mortar banks.

We believe internet sales will grow

rapidly – particularly in savings and

consumer lending products – giving

Direct Banking models the opportunity to

win market share

• Positioning of branch networks: Given

their small branch networks, challengers

are well positioned to adapt to changing

consumer preferences and build

distribution networks that better serve

customer needs

• IT platforms: Legacy IT platforms – often a

combination of multiple systems resulting

from mergers and acquisitions – are a

significant burden for retail banks. Newer,

smaller and more nimble institutions have

the opportunity to use IT and systems as

a competitive advantage. Investment in

newer, better quality systems can provide

major advantages: significant medium-

term cost savings, a reduced likelihood

of service breakdowns, and the ability to

use data to improve customer targeting

and servicing

9 Direct Banking Revisited, Oliver Wyman, November 2011.

Copyright © 2012 Oliver Wyman 22

SELECTING TARGET MARKETS

• Affluent segment: Many of the larger

incumbents have historically struggled to

build a profitable and clearly differentiated

affluent segment proposition. In this

context (and also given the RDR pressures

on the investment business), challengers

can win share here with a proposition that

more clearly tailors products and service

levels to this difficult part of the market

• Small business banking: Although a

potentially risky segment at this point

in the cycle, SME banking is a profitable

market in the medium-term which needs

more competition between suppliers.

With the recent breakdown of the RBS-

Santander transaction (~£12 billion of

Commercial loans), this sector is likely to

evolve rapidly in the coming two years,

providing opportunities to grow organically

and inorganically

MOVING PRODUCTS • Current account re-design: The

opportunity is clear: to create new, more

transparent product structures. Being

an early mover could be advantageous

for a low-share challenger, capitalising

on the opportunity to position a unique,

customer friendly offering which

challenges the ‘free banking’ paradigm

• Savings pricing: Aggressive and

transparent price strategies, looking to

benefit longer term from interest rate rises

Bold strategies have high potential upsides,

but such strategies are not risk-free. They

are all costly – in terms of either upfront or

contingent costs – and the risk/return trade-

off clearly needs to be considered carefully.

Copyright © 2012 Oliver Wyman 23

5. CONCLUSIONS

The UK retail banking market remains

attractive. There is potential for the industry

to change significantly in the coming years

due to the cocktail of regulatory change,

shifting customer demand, increased

competition, management changes and

changing economic conditions.

Coming out of the crisis, banks need to be

leaner, with re-focussed distribution models.

This will be especially important in the face

of bold challengers who have a greater

opportunity to disrupt than ever before.

More fundamentally, regulatory pressures

will necessitate a broader industry shift

towards simpler, more transparent products

and services. We think that this may come

sooner rather than later. Facing up to this

challenge and embracing change positively

and thoughtfully will be a key driver of

future success.

Oliver Wyman is a global leader in management consulting that combines deep industry knowledge with specialised expertise in strategy, operations, risk management, organisational transformation, and leadership development.

For more information please contact the marketing department by email at [email protected] or by phone at one of the following locations:

EMEA

+44 20 7333 8333

AMERICAS

+1 212 541 8100

ASIA PACIFIC

+65 6510 9700

Copyright © 2012 Oliver Wyman

All rights reserved. This report may not be reproduced or redistributed, in whole or in part, without the written permission of Oliver Wyman and Oliver Wyman accepts no liability whatsoever for the actions of third parties in this respect.

The information and opinions in this report were prepared by Oliver Wyman. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisors. Oliver Wyman has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Oliver Wyman disclaims any responsibility to update the information or conclusions in this report. Oliver Wyman accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages. The report is not an offer to buy or sell securities or a solicitation of an offer to buy or sell securities. This report may not be sold without the written consent of Oliver Wyman.

www.oliverwyman.com