november 14, 2005 anderson econ 136a midterm #2econ.ucsb.edu/~anderson/password/136a_f05_mt2.pdf ·...

TRANSCRIPT

November 14, 2005 Anderson ECON 136A MIDTERM #2 Name _________________________ Answer questions #1-25 (multiple choice) on your scantron and questions #26, 27 & 28 in your blue-book. ------------------------- ANSWER ON YOUR GREEN SCANTRON 1. Which of the following is NOT considered cash for financial reporting purposes? a. Petty cash funds and change funds b. Money orders, certified checks, and personal checks c. Coin, currency, and available funds d. Postdated checks and I.O.U.'s 2. If a company employs the gross method of recording accounts receivable from customers, then sales discounts taken should be a. reported as a deduction from sales in the income statement. b. reported as an item of "other expense" in the income statement. c. reported as a deduction from accounts receivable in determining the net realizable value of accounts receivable. d. reported as sales discounts forfeited in the cost of goods sold section of the income statement. 3. Which of the following methods of determining annual bad debt expense best achieves the matching concept? a. Percentage of sales b. Percentage of ending accounts receivable c. Percentage of average accounts receivable d. Direct write-off 4. For the year ended December 31, 2004, Colt Co. estimated its allowance for uncollectible accounts using the year-end aging of accounts receivable. The following data are available: Allowance for uncollectible accounts, 1/1/04 $51,000 Provision for uncollectible accounts during 2004 (2% on credit sales of $2,000,000) 40,000 Uncollectible accounts written off, 11/30/04 44,000 Estimated uncollectible accounts per aging, 12/31/04 74,000 After year-end adjustment, the uncollectible accounts expense for 2004 should be a. $44,000. b. $55,000. c. $74,000. d. $67,000.

MIDTERM #2--Page 2 5. In preparing its August 31, 2004 bank reconciliation, Cloud Corp. has available the following information: Balance per bank statement, 8/31/04 $25,650 Deposit in transit, 8/31/04 5,900 Return of customer's check for insufficient funds, 8/30/04 600 Outstanding checks, 8/31/04 2,750 Bank service charges for August 100 At August 31, 2004, Cloud's correct cash balance is a. $28,800. b. $28,200. c. $28,100. d. $26,500. 6. If a company's general ledger indicates that the cash balance at the end of the year is negative, this should be presented in the financial statements: a. As a current liability b. Labeled "bank overdraft" c. As cash, negative d. As a current liability labeled "bank overdraft" e. None of the above 7. A company employs the percentage of sales method for estimating the allowance for doubtful accounts. Using this method, they estimated during the year that the bad debt expense is $100,000. Also during the year, the Company dertermined that the uncollectible accounts to be written-off are $20,000. The proper amount for them to include as bad debt expense during the year is: a. $100,000 b. $120,000 c. $ 80,000 d. $ 40,000 8. According to many accountants and auditors, controls over cash are critical. Consequently,: a. Bank reconciliations serve as an important component of a company's internal control environment. b. Bank reconciliations serve only to reconcile the book cash balance to the bank balance and are not a component of the internal control environment. c. A bank reconciliation need only be performed if a company suspects fraud. d. A bank reconciliation is only necessary to gauge whether the bank has made a mistake in their records.

MIDTERM #2--Page 3 9. A company using the percentage of sales method has gone through its normal process of allowing for doubtful accounts, and written off certain accounts. Subsequently one of the balances they wrote-off has been paid by the customer! This should: a. Result in a credit to the income statement b. Reduce the allowance for bad debts c. Increase the allowance for bad debts d. Increase the bad debt expense 10. When using a perpetual inventory system, a. no Purchases account is used. b. a Cost of Goods Sold account is used. c. two entries are required to record a sale. d. all of these. 11. Goods in transit which are f.o.b. destination should be a. included in the inventory of the seller. b. included in the inventory of the buyer. c. included in the inventory of the shipping company. d. none of these. 12. Dane Co. received merchandise on consignment. As of March 31, Dane had recorded the transaction as a purchase and included the goods in inventory. The effect of this on its financial statements for March 31 would be a. no effect. b. net income was correct and current assets and current liabilities were overstated. c. net income, current assets, and current liabilities were overstated. d. net income and current liabilities were overstated. 13. Which of the following is correct? a. Selling costs are product costs. b. Manufacturing overhead costs are product costs. c. Interest costs for routine inventories are product costs. d. All of these. 14. The use of a Discounts Lost account implies that the recorded cost of a purchased inventory item is its a. invoice price. b. invoice price plus the purchase discount lost. c. invoice price less the purchase discount taken. d. invoice price less the purchase discount allowable whether taken or not. 15. An inventory pricing procedure in which the oldest costs incurred rarely have an effect on the ending inventory valuation is a. FIFO. b. LIFO. c. base stock. d. weighted-average.

MIDTERM #2--Page 4 16. In a period of rising prices, the inventory method which tends to give the highest reported net income is a. base stock. b. first-in, first-out. c. last-in, first-out. d. weighted-average. 17. Which of the following is true about lower of cost or market? a. It is inconsistent because losses are recognized but not gains. b. It usually understates assets. c. It can increase future income. d. All of these. 18. Designated market value a. is always the middle value of replacement cost, net realizable value, and net realizable value less a normal profit margin. b. should always be equal to net realizable value. c. may sometimes exceed net realizable value. d. should always be equal to net realizable value less a normal profit margin. 19. Net realizable value is a. acquisition cost plus costs to complete and sell. b. selling price. c. selling price plus costs to complete and sell. d. selling price less costs to complete and sell. 20. If a material amount of inventory has been ordered through a formal purchase contract at the balance sheet date for future delivery at firm prices, a. this fact must be disclosed. b. disclosure is required only if prices have declined since the date of the order. c. disclosure is required only if prices have since risen substantially. d. an appropriation of retained earnings is necessary. 21. Which statement is NOT true about the gross profit method of inventory valuation? a. It may be used to estimate inventories for interim statements. b. It may be used to estimate inventories for annual statements. c. It may be used by auditors. d. None of these. 22. A major advantage of the retail inventory method is that it a. provides reliable results in cases where the distribution of items in the inventory is different from that of items sold during the period. b. hides costs from competitors and customers. c. gives a more accurate statement of inventory costs than other methods. d. provides a method for inventory control and facilitates determi- nation of the periodic inventory for certain types of companies.

MIDTERM #2--Page 5 23. Which statement is true about the retail inventory method? a. It may not be used to estimate inventories for interim statements. b. It may not be used to estimate inventories for annual statements. c. It may not be used by auditors. d. None of these. 24. To produce an inventory valuation which approximates the lower of cost or market using the conventional retail inventory method, the computation of the ratio of cost to retail should a. include markups but not markdowns. b. include markups and markdowns. c. ignore both markups and markdowns. d. include markdowns but not markups. 25. Miller, Inc. estimates the cost of its physical inventory at March 31 for use in an interim financial statement. The rate of markup on cost is 25%. The following account balances are available: Inventory, March 1 $220,000 Purchases 172,000 Purchase returns 8,000 Sales during March 400,000 The estimate of the cost of inventory at March 31 would be a. $16,000. b. $64,000. c. $84,000. d. $72,000. ------------------------- ANSWER IN YOUR BLUE-BOOK 26. Waves, Inc. sold goods to customers with terms 2/10n30 and uses the gross method. The total invoice value, excluding any discounts, was $100,000. Within 10 days of the invoice, customers paid cash of $10,000 (representing $10,204 of invoice value). Present the journal entries required to record (1) the initial sale and (2) the collection of $10,000 cash within 10 days.

MIDTERM #2--Page 6

27. Windydays Inc. utilizes dollar value LIFO and has only one "pool". The following informationpertains to their computation of the inventory balance as of December 31, 2004:

Inventort at PriceDec. 31 Year-end prices Index

2001 100,000 100 2002 150,000 105 2003 170,000 110 2004 175,000 115

Compute the ending inventory using "dollar value LIFO" as of December 31, 2001, 2002, 2003 and 2004.

28. Based on the following facts, please compute the ending inventory using each of thefollowing three retail inventory methods:

(1) LCM (Conventional LIFO retail)-- hint no markdowns(2) Cost method (Average Cost)-- hint markdowns included(3) Dollar Value Retail LIFO-- Hint: Layers & Include markdowns

Cost RetailBeginning Inventory 250,000 500,000 Purchases 750,000 1,250,000 Markups, net 30,000 Markdowns, net (10,000) Net sales (1,200,000) Ending inventory at retail 570,000

MIDTERM #2--Page 6 November 14, 2005 ANSWER KEY Anderson ECON 136A +-------+------+--------+------+--------+--------+--------+--------+------+ | Text | Bank | Exam | | | Ques | Diff | Lrng | | |Chapter| Ref |Question|Answer| Type | Cat | Lvl | Obj | Page | +-------+------+--------+------+--------+--------+--------+--------+------+ | 7 1 1 d MChoice C 1 | | 7 8 2 a MChoice C 4 | | 7 11 3 a MChoice C 5 | | 7 43 4 d MChoice A 5 | | 7 50 5 a MChoice A 10 | | 7 52 6 d MChoice | | 7 53 7 a MChoice | | 7 54 8 a MChoice | | 7 56 9 a MChoice | | 8 1 10 d MChoice C 2 | | 8 3 11 a MChoice C 2 | | 8 8 12 b MChoice C 3 | | 8 12 13 b MChoice C 4 | | 8 15 14 d MChoice C 4 | | 8 22 15 a MChoice C 5 | | 8 25 16 b MChoice C 5 | | 9 1 17 d MChoice C 1 | | 9 5 18 a MChoice C 1 | | 9 9 19 d MChoice C 2 | | 9 12 20 a MChoice C 4 | | 9 15 21 b MChoice C 5 | | 9 16 22 d MChoice C 6 | | 9 19 23 d MChoice C 6 | | 9 21 24 a MChoice C 6 | | 9 32 25 b MChoice P 5 | | 7 56 26 Exercise | +-------------------------------------------------------------------------+

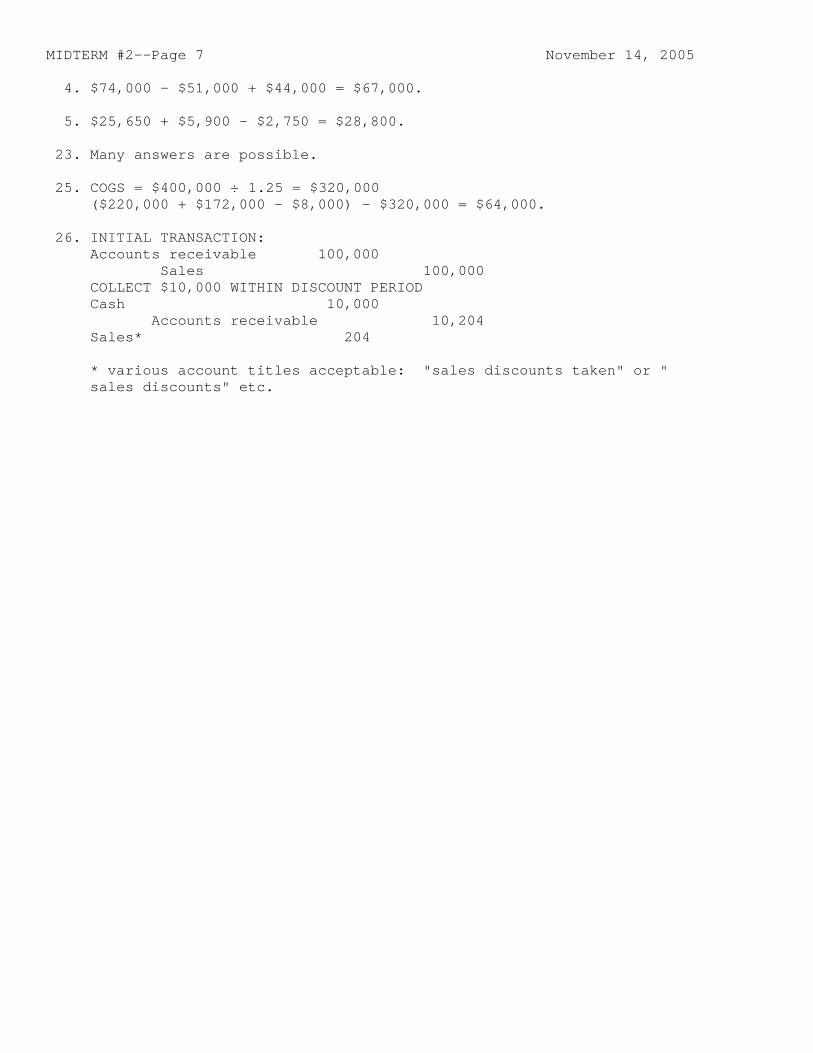

MIDTERM #2--Page 7 November 14, 2005 4. $74,000 - $51,000 + $44,000 = $67,000. 5. $25,650 + $5,900 - $2,750 = $28,800. 23. Many answers are possible. 25. COGS = $400,000 1.25 = $320,000 ($220,000 + $172,000 - $8,000) - $320,000 = $64,000. 26. INITIAL TRANSACTION: Accounts receivable 100,000 Sales 100,000 COLLECT $10,000 WITHIN DISCOUNT PERIOD Cash 10,000 Accounts receivable 10,204 Sales* 204 * various account titles acceptable: "sales discounts taken" or " sales discounts" etc.

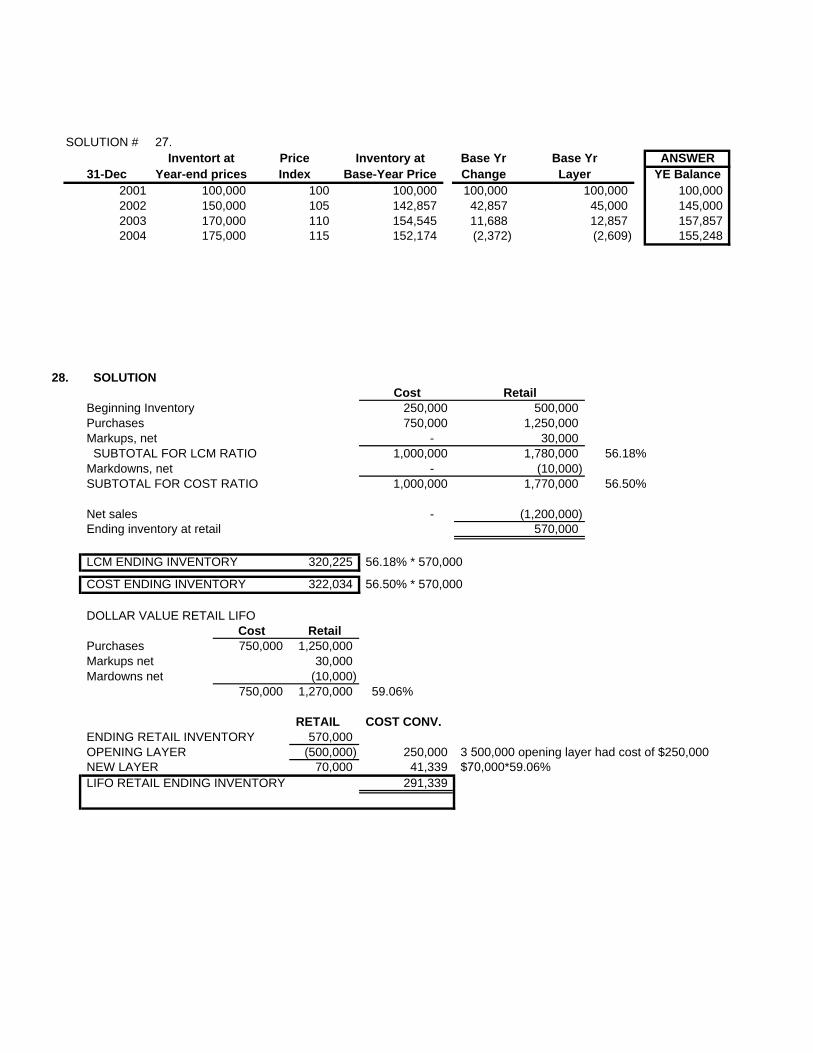

SOLUTION # 27.Inventort at Price Inventory at Base Yr Base Yr ANSWER

31-Dec Year-end prices Index Base-Year Price Change Layer YE Balance2001 100,000 100 100,000 100,000 100,000 100,000 2002 150,000 105 142,857 42,857 45,000 145,000 2003 170,000 110 154,545 11,688 12,857 157,857 2004 175,000 115 152,174 (2,372) (2,609) 155,248

28. SOLUTIONCost Retail

Beginning Inventory 250,000 500,000 Purchases 750,000 1,250,000 Markups, net - 30,000 SUBTOTAL FOR LCM RATIO 1,000,000 1,780,000 56.18%Markdowns, net - (10,000) SUBTOTAL FOR COST RATIO 1,000,000 1,770,000 56.50%

Net sales - (1,200,000) Ending inventory at retail 570,000

LCM ENDING INVENTORY 320,225 56.18% * 570,000

COST ENDING INVENTORY 322,034 56.50% * 570,000

DOLLAR VALUE RETAIL LIFOCost Retail

Purchases 750,000 1,250,000 Markups net 30,000 Mardowns net (10,000)

750,000 1,270,000 59.06%

RETAIL COST CONV.ENDING RETAIL INVENTORY 570,000 OPENING LAYER (500,000) 250,000 3 500,000 opening layer had cost of $250,000NEW LAYER 70,000 41,339 $70,000*59.06%LIFO RETAIL ENDING INVENTORY 291,339