nova economics club€¦ · · 2016-07-25say‘s economics ―cosmopolitical‖ because it was...

TRANSCRIPT

John Maynard Keynes Edition

Nova Economics Club Publication #10 – June 2016

NEC TALKS

with

Mário Centeno

June 2016

Contents

Editorial p. 1

June in Review p. 2

NEC Recommends p. 3

NEC Talks with Mário Centeno p. 4

News – ―Future Leaders‖ peddy-paper p. 6

John Maynard Keynes p. 7

NEC Statistics p. 10

Subscribe to our Newsletter here

Follow us by clicking

Powered by:

Editor: Miguel Costa Matos Deputy Editor: Tiago Alves Design: Beatriz Braz Review: Miguel Costa Matos June in Review &

NEC Recommends: Miguel Costa Matos, Patrícia Filipe, Sofia Pessoa and Tiago Alves NEC Talks: João Cortes, Miguel Costa

Matos, João Matias and Márcia Silva Pereira News: João Cortes Statistics: Alexandre Carvalho, Alexandre Gouveia, Beatriz Braz,

Diogo Conceição, Francisco Gonçalves, Gonçalo D‘alte, João Cortes, João Matias, João Mendes, Lucas Silva, Margarida Martins,

Matheus Coelho, Miguel Amaro, Rodrigo Barrela, Tiago Alves and Tiago Rabaça Economist of the Month: Guilherme Azambuja

Dear reader,

First things first – let me apologize for the delay in

getting this edition to you. NEC is run by students

who volunteer and when exam season hits, we

necessarily face the crunch. Nevertheless, this

edition is quite a treat – its patron is John

Maynard Keynes, and it includes an interview

with the Portuguese Minister for Finance, Mário

Centeno. We also give continuity to our usual

sections including a review of the month‘s news

and of the top articles by leading economists that

you can catch up on.

It is worth reflecting on Keynes and his legacy 80

years from the publication of the General Theory

of Employment, Interest and Money. Far too

many pages have already been spent debating

Keynes‘ influence on economic science.

Veritably, Keynes‘ influence was crippled early on

by Paul Samuelson‘s ―neoclassical synthesis‖

which distorted Keynes‘ teachings. This tradition

of usurpation has been time-honored by New

Keynesians, who work from an essentially

neoclassical framework and add some frictions to

it. This is the realm of fact – I leave it to the

reader to judge it good or bad.

The true test of Keynes‘ influence is not that the

state has any role to play in the economy, or if it

grows counter-cyclically. It is instead whether we

admit to the existence of involuntary

unemployment, whether we accept that economic

future is really unknown, whether we understand

that demand drives and shapes supply, and

whether we comprehend that people‘s liquidity

preference can neuter markets by slowing down

money.

Keynes called his theory ‗General‘ in contrast

with the case of self-regulating, perfect-

information, perfect-competition markets taught in

economics classes. These markets are so

bizarrely implausible that one might think they

were drawn up as straw men, deliberately to be

put down, but their resilience has been

extraordinary. Keynes was not the first to point

out that classical economics was theorizing on a

market that didn‘t exist. The German school of

thought, led by Friedrich List, called Smith and

Say‘s economics ―Cosmopolitical‖ because it was

thought as if there were no nations. It is

worthwhile to consider once more whether the

economics we are taught tells us anything more

than special facts for special worlds that don‘t

exist.

Last week the EU decided to impose sanctions

on Portugal and Spain, leaving France scot-free

―because it is France‖ and Germany unpunished

for its excessive trade surplus. Keynes here too

was prescient. The Macroeconomic Imbalance

Procedure harkens back to Keynes‘ call for an

International Clearing Union that taxed trade

surpluses. It did so automatically, free from these

power games that make the European Union so

unequal in dishing out carrots and sticks.

Eight years on from the global financial crisis, we

are still in crisis. Our ‗dismal science‘ has, it

appears, not only failed to help but actively

contributed both to cause the crisis and prolong

it. 80 years later, we might begin to ask if we

might not be better off if we had listened to

Keynes after all.

Miguel Costa Matos Editor-in-Chief, NEC Newsletter

Nova Economics Club Monthly Newsletter

JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

Editorial 1

June 2016

June in Review

Nova Economics Club Monthly Newsletter

2

1st Australia‘s economy grew at its fastest pace in four years in the first quarter due to a surge in exports. A

weakening Australian dollar has prompted growth in service exports, which is also helping the economy

transition form the mining boom.

7th

Dynamic scoring in action: Obama budget would raise taxes and increase economic growth. However, while

total growth would be higher, per capita growth would be lower since immigrants would have, on average,

lower income than existing residents.

8th

Japan‘s economy grew 1,9% in the first quarter, more than the government initially reported.

More countries within the European Union want some powers returned from Brussels, back to national

governments.

9th

Mario Draghi, European Central Bank president, stepped up his call for Europe‘s political leaders to make

root-and-branch reforms of their economies to create more jobs, warning them it was their duty to save the

region from its ageing crisis.

10th

Pedro Kuczynski, an economist, declared victory for Peru presidency after narrowly prevailing over the

populist Keiko Fujimori, the daughter of an imprisoned former president.

Barack Obama officially endorsed Hillary Clinton to succeed him as president, after Bernie Sanders

signaling that he would soon bow out of the Democratic nomination contest.

12th

A man stormed a gay nightclub, wielding an assault rifle and a pistol, and carried out the worst mass

shooting in United States history, leaving 50 people dead and 53 wounded.

16th The Bank of Canada, the country‘s central bank, revealed that it was working with the country‘s biggest

banks to develop an electronic version of the Canadian dollar.

17th British MP Jo Cox is murdered outside her surgery over her support of immigrants, just days before Britain

votes to leave the EU.

20th

The unexpected resignation of highly admired governor of the Reserve Bank of India, Raghuram Rajan,

unsettles many investors and weakens Mr Modi‘s economic credibility.

21st

Brazil‘s telecommunications giant Oi filed for bankruptcy protection, revealing the extent of the economic

crisis the country is suffering, expected to be the worst in a century, and unleashing shockwaves on the

market.

22nd

The ECB reinstates Emergency Liquidity Assistance to Greek banks, as tensions thaw. The next step

towards normal relations between Greece and the ECB is inclusion in the QE programme, expected in

September.

25th

Just 24 hours after deciding to leave the European Union, the U.K. started to absorb the financial

ramifications of its shock decision. U.S. ratings agency Moody's announced that it had lowered its outlook

on the country's credit rating from stable to negative.

27th

Trade partners must consider how the current political realities of trade can be managed more effectively,

since the era of transactional trade-centric globalization is coming to a close and a more sustainable,

investment-focused chapter is set to begin.

28th

Mario Draghi says central banks around the world should align their monetary policies to help prevent

"destabilizing spillovers" between economies growing at different paces.

Although in the short run this change will bring some important negative consequences, in the long run,

there will be more winners than losers. The country should eventually end up richer and disparities of wealth

will be less extreme.

June 2016 JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

Nova Economics Club Monthly Newsletter

A guide to the ECB’s corporate bond purchases In June, the European Central Bank launched its latest bid to stimulate the eurozone economy and lift inflation by buying corporate bonds. Use this guide to understand the latest escalation of the aggressive monetary policy easing from central banks worldwide since the 2008 financial crisis.

China’s New Silk Road Into Europe Is About More Than Money Beijing‘s multibillion-dollar plans to build overland and maritime links across Central and South Asia — whether that means huge investments in Pakistan or gas pipeline deals in places like Kazakhstan and Uzbekistan — grab the lion‘s share of attention. This report assures that the ultimate prize in the Silk Road plan — also known in China as the ―One Belt, One Road‖ initiative — is someplace else: Europe. Evolution Not Revolution: Rethinking Policy at the IMF This interview with new IMF Chief Economist, Maurice Obstfeld puts the evolving policy perspectives of the IMF into the limelight. Long gone are the days of the Washington Consensus, it appears, with evidence-backed policy being the driving tone for this pleasant and insightful read. Fragile States Index 2016 For 12 years, the Fragile States Index, created by the Fund for Peace and published by Foreign Policy, has taken stock of the year's events, using 12 social, economic, and political indicators to analyze how wars, peace accords, environmental calamities, and political movements have pushed countries toward stability or closer to the brink of collapse. The full results of this year‘s index can be found here. Innovation is not enough Dani Rodrik is intensely concerned with making countries grow, especially in the developing world. Here, Rodrik gives us a survey of how technological innovation might be hampering growth not just in the developing world but in advanced economies. An issue worth mulling over. Economics Struggles to Cope with Reality Noah Smith discusses the various types of macroeconomics being used lately and how they have becomes less able to cope with reality. His solution isn‘t new or uncontroversial – more macro-focused micro that reveals insights into how markets work in reality. A good place to get a glimpse of how Macro is changing. Market disintegration as a pre-cursor to the Great Divergence Despite being credited with many inventions of the early

modern era, China failed to develop in line with Western Europe at the start of the 19th century. This column suggests that one reason for this was that China‘s economy was more fragmented than that of Europe. Data from 1740-1820 shows that, in terms of market integration, the Great Divergence was well under way decades before the start of the 19th century. Inequality in Germany: How it differs from the US This column debates the main differences between inequality in Germany and in the US, showing data from 1990 on and offering some explanations for the facts. Brexit: The Morning After Nobel Prize winner Paul Krugman argues that Brexit consequences will be bad, but not as bad as many are claiming. This column discusses the main economic, financial and political costs of Britain leaving the EU. Capital hill Jeb Hensarling, chairman of the Financial Services Committee, wants to replace the Dodd-Frank act, the sprawling overhaul of America‘s financial system instituted in the wake of the crisis of 2007-08, with something much simpler. Read more about the Republicans alternative to America‘s convoluted bank regulation in here. Credibility of central bank(er)s Both the Fed and the ECB appear to have been effective in the way they have applied policy during the financial crisis. However, the environment in which the two have operated is quite different. Read more about the implication of the macroeconomic mixes applied on the credibility of the central bank(er)s, their ability to stimulate aggregate demand, and prevent it from achieving its inflation objective, in this column. Bail-in versus bail-out: the Atlante example from a systemic risk perspective ―In a bail-in scenario, the troubled bank‘s default affects its neighbours through a shock in their default probabilities derived from contagion effects. However, after a while, the bank system reaches a new equilibrium without the defaulted bank and, thus, is affected by less contagion risk. In a bail-out scenario, the troubled bank does not default and, thus, does not affect its neighbours through a shock in their default probabilities. However, it continues to be part of the system, so that all the other banks in the network will still be affected by the high contagion tisk derived from its presence.‖ If you want to know more about which banks benefit more from a bail-in or bail-out scenario, read it here.

NEC Recommends Articles and Trends to watch

3

June 2016 JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

4

Nova Economics Club Monthly Newsletter

NEC TALKS

Mário Centeno

Cortes, Matias, Matos e Pereira What economic

impact does Brexit have for Portugal and Europe?

What policies does Portugal have planned to react

to this circumstance?

Centeno Brexit constitutes a structural change in

the European Union. In this way, beyond its

immediate impact on the stock markets, which was

greater in many cases than the Lehman Brothers

crisis, there will be a long period of adjustment. The

European and British economies will watch a

redefinition of business operating in these two

economic spaces. With displacements, new

investments and a strong impact on trade flows.

Portugal‘s reaction must be thought in the context of

the European Union.

Cortes, Matias, Matos e Pereira Should there be

more flexibility for European countries to have their

own fiscal policies? Should we treat equally what is

different?

Centeno Each countries‘ fiscal policy should

contribute to reducing the area‘s aggregate risk.

This policy should be complemented by other

measures of risk-sharing. This is the big debate in

Europe today. Up until now we‘ve made headway

on regulating risk reduction and very little on the

second dimension [risk sharing]. The existence of a

larger European budget that covered some of the

national risks, like unemployment, could be a first

policy towards that objective.

Cortes, Matias, Matos e Pereira The Portuguese

banking sector demonstrates some fragility. What is

the main challenge – lack of capital, low spreads,

negative interest rates, or anemic demand for

credit? And what is the solution?

Centeno The Portuguese banking sector is not

immune to the difficulties faced by Europe‘s entire

banking sector. Among these difficulties is a

business model that did not adapt to low interest

rates. Our economies are not designed to live for

prolonged periods in this interest rate regimen.

Beyond this, our banking sector needs to keep

adjusting its capital levels and seek new business

models, but none of these problems are particularly

or exclusively Portuguese.

Cortes, Matias, Matos e Pereira The budget has

been enacted for 3 months now, and preparations

for the next one are underway. What lessons do you

take forward for future budgets?

Centeno Budgets are always very demanding

exercises, which require Public Administration to be

conscious of the permanent need to adjust to the

constraints that are binding on the Portuguese

economy. The 2016 budget reflects that and the

2017 budget will do the same. With the experience

of 2016, we learnt that we need to conduct a

spending review to help better define policy

measures and their budgetary needs. We have

begun this exercise in many sectors of the Public

Administration already.

(continues on the next page)

June 2016 JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

Nova Economics Club Monthly Newsletter

NEC TALKS

Mário Centeno

June 2016

Cortes, Matias, Matos e Pereira Currently, we observe that firms invest in financial products instead of investing in productive capacity – a phenomenon many call financialization. Do you consider this problematic, as it may lead to profits not materializing in increased demand? Centeno In modern societies and economies, the capacity and speed of financial integration brought huge possibilities for regions and sectors to finance themselves when they otherwise would remain excluded from this process. However, this occurred without us taking into account the risks, which brought with it more frequent financial crises, though these are nonetheless far from a novelty. With each crisis, we learn a little more and we are now more able to reestablish growth in more solid foundations. We should pay attention to what microeconomics teach us about incentives and agent‘s information so that we can protect ourselves from these risks. If we do this, we ascertain the conditions for demand to be enhanced in a sustainable way. Cortes, Matias, Matos e Pereira You were a researcher and now you‘re a Minister. What advice would you give to young economists, both those who want to do research and those who want to do policy?

Centeno Research and policy should be intimate

with each other. Two words of warning: there is no

good policy without 1) good data; or 2) good

economic theory. In Portugal, we underrate the first

a lot and glorify too much the latter. We must have a

more balanced approach.

A culture of statistical analysis begins, for instance,

when we see a football match, and should be

extended to the way we analyze the labour market.

With the same instruments. After, we add to this

economic theory. Essential. But we ought not to

want our articles‘ abstracts to be transposed into

law. We must challenge them incessantly against

data and the social and economic reality to which

they apply. Always with lots of modesty, translated

in the idea that sometimes it is better to have an

excellent compromise than an excellent theorem. In

policy, not in theory.

Questions by

João Cortes

João Matias

Miguel Costa Matos

Márcia Silva Pereira

Edited by

Miguel Costa Matos

5

JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

Nova Economics Club Monthly Newsletter

News

Peddy-Paper ―Future Leaders‖

June 2016

6

In the past 4th of July, Nova Economics Club organized a peddy-paper dedicated to the ―Future Leaders‖, led by

NEC members João Cortes and Beatriz Braz. Thanks to the support of more than 20 current Nova SBE students it

became possible to make this experience reality.

The peddy-paper was formed by 10 groups, each group with a different path and a ―Group Leader‖, current Nova

SBE student volunteering in the activity, who knew nothing, just as they did, except perhaps a little further the rules.

The groups had to find the 10 posts spread throughout the campus. Each post had another volunteer, the ―Post

Guardian‖, who would give an economical question and a hint for the next post.

It remains for us now only to thank once more all those who could make this dream a reality and hope that the future

leaders don‘t forget this experience and keep it with the same happiness we do. NEC and our organizers members

give thanks for the help in organizing the event to Beatriz Frazão, Beatriz Gonçalves, Diogo Firme, Diogo Saul,

Filipe Baião, Francisco Caldeira Fernandes, Gonçalo Bacelar Lopes, Gonçalo Mendes, Henrique Gameiro, Leonor

Zôrro Gonçalves, Maria Margarida Cruz, Mariana Anastácio, Mariana Pires, Matilde Simões, Pedro Mota, Raquel

Carvalho, Ricardo Tavira, Rita Marques and Tiago Bernardino.

JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

“The introduction of a substantial Government transfer tax on all transactions might prove the most serviceable reform available” 1936

It wasn‘t until the end of the Great Depression that one

of the most influential economists of the 20th century

became a household name in fields such as

macroeconomics, public spending and monetary policy

among others.

John Maynard Keynes was a bright mind from

Cambridge, born in 1883 in a middle class family. He

graduated from Kings College in Cambridge, with a

degree in mathematics and went on to serve in

government as a civil servant, where he gathered data

that would later be used in ―Indian Currency and

Finance‖, published in 1913.

He returned to Cambridge very shortly in 1908 as a

lecturer, before taking up a role at the Ministry of

Treasury, where his reputation and ideas would grow in

support. By 1919 Keynes was the main Treasury

representative at the peace conference in Versailles.

He wasn‘t satisfied with the treaty and shortly after

resigned and returned to Cambridge to teach. Later

that year he published ―The Economic Consequence of

Peace‖ where he expresses his take on the peace

negotiations and what should have been different.

In the 1920s, Keynes was a firm believer in the quantity

theory of money. His writings on the topic were

essentially built on the principles he had learned from

his mentors, Marshall and Pigou, summarised in his

1923 ―Tract in Monetary Reform‖ and 7 years later in

the ―Treatise on Money‖. He strongly believed in the

central bank‘s control of interest rates as a way to

stabilize price levels, based on the principle that people

often save more than is actually being invested.

In 1933 at the height of the Great Depression, Keynes

made another publication titled ―The Means to

Prosperity‖ which provided policy recommendations to

tackle unemployment in times of global recession. This

was definitely a huge contribution to the world of

economics bearing in mind rampant unemployment at

the time, and its wider effects on the economy.

Keynes‘ general theory of employment, interest and

money came to be published in 1936. According to

Keynes teachings, the best thing to do during

depressions was either to come up with public

substitutes for deficiencies of private investment or to

enlarge private investment. As Minsky puts it, Keynes‘

main message was that during a depression, there is

no wage low enough to eliminate unemployment.

Instead, unemployment had to be resolved by

stimulating aggregate demand.

The contributions of John Maynard Keynes did not end

there. As World War II began to wind down, he played

a significant role in the Bretton Woods negotiations in

1944. Along with others, Keynes advocated for the

establishment of a world central bank and an

international currency regulation body, and he was

instrumental in the formation of what would become the

World Bank and the International Monetary Fund.

It was at Bretton Woods that he proposed Bancor, a

global currency to encourage the stabilization of

commodity prices and achieve global trade balance

through taxation of current account surpluses, and not

just penalizing trade deficits. Although not adopted, this

idea – as well as many other of Keynes‘ ideas - have

periodically bubbled back to the surface for renewed

discussion up to the present day. His ideas have had a

lasting impact and remain one of the most influential to

date.

Guilherme Azambuja

NEC member

John Maynard Keynes Economist of the Month - June

Nova Economics Club Monthly Newsletter

7

June 2016 JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

June 2016

Nova Economics Club Monthly Newsletter

John Maynard Keynes Economist of the Month - June

“The completeness of the [orthodox] victory is something of a curiosity and a mystery. It must have been due to a complex of suitabilities in the doctrine to the environment into which it was projected. That it reached conclusions quite different from what the ordinary uninstructed person would expect, added, I suppose, to its intellectual prestige. That its teaching, translated into practice, was austere and often unpalatable, lent it virtue. That it was adapted to carry a vast and consistent logical superstructure, gave it beauty. That it could explain much social injustice and apparent cruelty as an inevitable incident in the scheme of progress, [with] the attempt to change such things as likely on the whole to do more harm than good, commended it to authority. That it afforded a measure of justification to the free activities of the individual capitalist attracted the support of the dominant social authority. But although the doctrine itself has remained unquestioned by orthodox economists up to a late date, its signal failure for purposes of scientific prediction has greatly impaired, over the course of time, the prestige of its practitioners. For professional economists…were apparently unmoved by the lack of correspondence between the results of their theory and the facts of observation; a discrepancy which the ordinary man has not failed to observe, with the result of his growing unwillingness to accord to economists that measure of respect which he gives to other groups of scientists.”

8

JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

June 2016

Nova Economics Club Monthly Newsletter

John Maynard Keynes Economist of the Month - June

“If, however, we are tempted to assert that money is the drink which stimulates the system to activity, we must remind ourselves that there may be several slips between the cup and the lip.”

“The whole of the labor of the unemployed is available to increase the national wealth. It is crazy to believe that we shall ruin ourselves financially by trying to find means for using it and that safety lies in continuing to maintain idleness.”

“But this long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us that when the storm is long past the ocean is flat again.”

9

JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

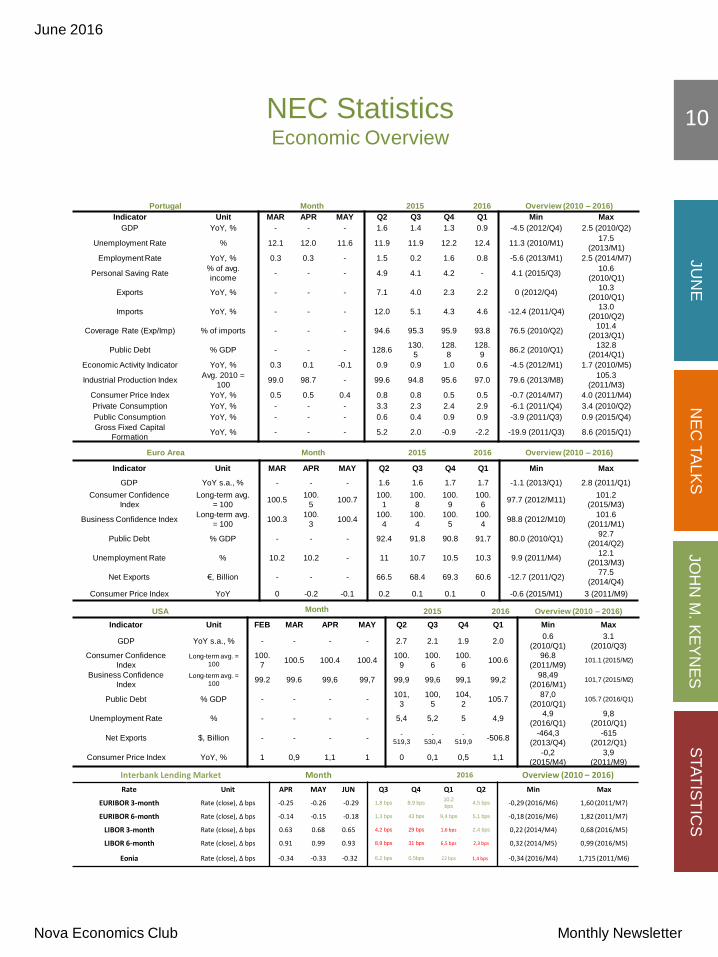

NEC Statistics Economic Overview

Nova Economics Club Monthly Newsletter

10

Interbank Lending Market Month 2016 Overview (2010 – 2016)

Rate Unit APR MAY JUN Q3 Q4 Q1 Q2 Min Max

EURIBOR 3-month Rate (close), ∆ bps -0.25 -0.26 -0.29 1,8 bps 8,9 bps 10,2

bps 4,5 bps -0,29 (2016/M6) 1,60 (2011/M7)

EURIBOR 6-month Rate (close), ∆ bps -0.14 -0.15 -0.18 1,3 bps 43 bps 9,4 bps 5,1 bps -0,18 (2016/M6) 1,82 (2011/M7)

LIBOR 3-month Rate (close), ∆ bps 0.63 0.68 0.65 4,2 bps 29 bps 1,6 bps 2,4 bps 0,22 (2014/M4) 0,68 (2016/M5)

LIBOR 6-month Rate (close), ∆ bps 0.91 0.99 0.93 8,9 bps 31 bps 6,5 bps 2,3 bps 0,32 (2014/M5) 0,99 (2016/M5)

Eonia Rate (close), ∆ bps -0.34 -0.33 -0.32 6,2 bps 0,5bps 22 bps 1,4 bps -0,34 (2016/M4) 1,715 (2011/M6)

Portugal Month 2015 2016 Overview (2010 – 2016)

Indicator Unit MAR APR MAY Q2 Q3 Q4 Q1 Min Max

GDP YoY, % - - - 1.6 1.4 1.3 0.9 -4.5 (2012/Q4) 2.5 (2010/Q2)

Unemployment Rate % 12.1 12.0 11.6 11.9 11.9 12.2 12.4 11.3 (2010/M1) 17.5

(2013/M1)

Employment Rate YoY, % 0.3 0.3 - 1.5 0.2 1.6 0.8 -5.6 (2013/M1) 2.5 (2014/M7)

Personal Saving Rate % of avg.

income - - - 4.9 4.1 4.2 - 4.1 (2015/Q3)

10.6

(2010/Q1)

Exports YoY, % - - - 7.1 4.0 2.3 2.2 0 (2012/Q4) 10.3

(2010/Q1)

Imports YoY, % - - - 12.0 5.1 4.3 4.6 -12.4 (2011/Q4) 13.0

(2010/Q2)

Coverage Rate (Exp/Imp) % of imports - - - 94.6 95.3 95.9 93.8 76.5 (2010/Q2) 101.4

(2013/Q1)

Public Debt % GDP - - - 128.6 130.

5 128.

8 128.

9 86.2 (2010/Q1)

132.8

(2014/Q1)

Economic Activity Indicator YoY, % 0.3 0.1 -0.1 0.9 0.9 1.0 0.6 -4.5 (2012/M1) 1.7 (2010/M5)

Industrial Production Index Avg. 2010 =

100 99.0 98.7 - 99.6 94.8 95.6 97.0 79.6 (2013/M8)

105.3

(2011/M3)

Consumer Price Index YoY, % 0.5 0.5 0.4 0.8 0.8 0.5 0.5 -0.7 (2014/M7) 4.0 (2011/M4)

Private Consumption YoY, % - - - 3.3 2.3 2.4 2.9 -6.1 (2011/Q4) 3.4 (2010/Q2)

Public Consumption YoY, % - - - 0.6 0.4 0.9 0.9 -3.9 (2011/Q3) 0.9 (2015/Q4)

Gross Fixed Capital

Formation YoY, % - - - 5.2 2.0 -0.9 -2.2 -19.9 (2011/Q3) 8.6 (2015/Q1)

Euro Area Month 2015 2016 Overview (2010 – 2016)

Indicator Unit MAR APR MAY Q2 Q3 Q4 Q1 Min Max

GDP YoY s.a., % - - - 1.6 1.6 1.7 1.7 -1.1 (2013/Q1) 2.8 (2011/Q1)

Consumer Confidence

Index Long-term avg.

= 100 100.5

100.

5 100.7

100.

1 100.

8 100.

9 100.

6 97.7 (2012/M11)

101.2

(2015/M3)

Business Confidence Index Long-term avg.

= 100 100.3

100.

3 100.4

100.

4 100.

4 100.

5 100.

4 98.8 (2012/M10)

101.6

(2011/M1)

Public Debt % GDP - - - 92.4 91.8 90.8 91.7 80.0 (2010/Q1) 92.7

(2014/Q2)

Unemployment Rate % 10.2 10.2 - 11 10.7 10.5 10.3 9.9 (2011/M4) 12.1

(2013/M3)

Net Exports €, Billion - - - 66.5 68.4 69.3 60.6 -12.7 (2011/Q2) 77.5

(2014/Q4)

Consumer Price Index YoY 0 -0.2 -0.1 0.2 0.1 0.1 0 -0.6 (2015/M1) 3 (2011/M9)

USA Month 2015 2016 Overview (2010 – 2016)

Indicator Unit FEB MAR APR MAY Q2 Q3 Q4 Q1 Min Max

GDP YoY s.a., % - - - - 2.7 2.1 1.9 2.0 0.6

(2010/Q1) 3.1

(2010/Q3) Consumer Confidence

Index Long-term avg. =

100 100.

7 100.5 100.4 100.4

100.

9 100.

6 100.

6 100.6

96.8

(2011/M9) 101.1 (2015/M2)

Business Confidence

Index Long-term avg. =

100 99.2 99.6 99,6 99,7 99,9 99,6 99,1 99,2

98,49

(2016/M1) 101,7 (2015/M2)

Public Debt % GDP - - - - 101,

3 100,

5 104,

2 105.7

87,0

(2010/Q1) 105.7 (2016/Q1)

Unemployment Rate % - - - - 5,4 5,2 5 4,9 4,9

(2016/Q1) 9,8

(2010/Q1)

Net Exports $, Billion - - - - -

519,3 -

530,4 -

519,9 -506.8

-464,3

(2013/Q4) -615

(2012/Q1)

Consumer Price Index YoY, % 1 0,9 1,1 1 0 0,1 0,5 1,1 -0,2

(2015/M4) 3,9

(2011/M9)

June 2016 JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S

NEC Statistics Financial Markets Overview

Nova Economics Club Monthly Newsletter

11

June 2016

Currency Pairs Month 2015 2016 Overview (2010 – 2016)

Pair (Spot) Unit APR MAY JUN Q3 Q4 Q1 Q2 Min Max

EUR/USD Close price 1.145 1.113 1.110 0,35% 2,82% 4,84% 2.43% 1,046 (2015/M3) 1,494 (2011/M5)

EUR/GBP Close price 0.784 0.769 0.833 4,09% 0,37% 7,89% 5.15% 0,694 (2015/M7) 0,908 (2011/M7)

EUR/JPY Close price 121.9 123.2 114.5 1,75% 2,47% 1,94% 10.60% 94,1 (2012/M7) 150 (2014/M12)

EUR/CHF Close price 1.099 1.106 1.084 4,43% 0,15% 0,66% 0.87% 0,843 (2015/M1) 1,489 (2010/M1)

EUR/AUD Close price 1.506 1.539 1.491 10,14% 6,71% 0,28% 0.49% 1,160 (2012/M8) 1,659 (2015/M8)

USD/JPY Close price 106.4 110.6 103.1 2,07% 0,35% 6,48% 8.37% 75,57 (2011/M10) 125,9 (2015/M6)

USD/CAD Close price 1.256 1.308 1.296 6,72% 4,09% 6,20% 0.24% 0,941 (2011/M7) 1,386 (2015/M12)

GBP/USD Close price 1.461 1.448 1.333 3,60% 2,47% 2,82% 7.20% 1,384 (2016/M2) 1,719 (2014/M7)

AUD/USD Close price 0761 0.724 0.745 8,89% 4,01% 5,19% 2.90% 0,683 (2016/M1) 1,108 (2011/M7)

Commodities Month 2015 2016 Overview (2010 – 2016)

Future 05/16 Unit APR MAY JUN Q3 Q4 Q1 Q2 Min Max

Brent Oil $ p. barrel, close 47.4 50.5 49.7 25,6% 23,6% 8,2% 23.3% 28,0 (2016/M1) 126,6 (2014/M6)

Natural Gas $ p. MMBtu,

close 2.18 2.32 2.92 12,0% 16,9% 16,2% 49.2% 1,69 (2016/M3) 8,97 (2010/M1)

Aluminum $ p. ton, close 1673 1546 1646 4,9% 4,5% 0,7% 8.5% 1444 (2015/M11) 2764 (2011/M4)

Copper $ p. lb., close 2.28 2.10 2.20 10,5% 9,0% 2,3% 0.7% 1,94 (2016/M1) 4,71 (2011/M2)

Nickel $ p. ton, close 9417 8399 9410 13,1% 15,3% 3,3% 10.7% 8393 (2016/M5) 28977 (2011/M2)

Zinc $ p. ton, close 1934 1920 2102 15,6% 4,8% 13,2% 16.1% 1552 (2015/M11) 2499 (2011/M2)

Gold $ p. ounce,

close 1291 1218 1321 4,9% 4,9% 16,6% 6.8% 1045 (2015/M12) 1953 (2011/M9)

Silver $ p. ounce,

close 17.8 16.0 18.6 6,9% 4,9% 12,3% 20.1% 13,6 (2015/M12) 50,9 (2011/M4)

Platinum $ p. ounce,

close 1078 983 1024 15,8% 1,8% 9,5% 4.7% 811 (2016/M1) 1938 (2011/M8)

Government Bonds Month 2015 2016 Overview (2010 – 2016)

Bond Unit APR MAY JUN Q3 Q4 Q1 Q2 Min Max

Portugal 2-Year Gov. Bond Yield (close), ∆ bps 0,69 0.52 0,61 1 bps 21 bps 23 bps 21 bps -0,01 (2015/M6) 21,7 (2012/M1)

Portugal 10-Year Gov.

Bond Yield (close), ∆ bps 3,16 3.08 3,09

58

bps 14 bps 24 bps 31 bps 1,51 (2015/M3) 16,5 (2012/M1)

Germany 2-Year Gov. Bond Yield (close), ∆ bps -0,48 -0.51 -0,65 2 bps 9 bps 13 bps 16 bps -0,58 (2016/M3) 1,96 (2011/M5)

Germany 10-Year Gov.

Bond Yield (close), ∆ bps 0,27 0.15 -0,13

18

bps 4 bps 48 bps 28 bps 0,05 (2015/M4) 3,51 (2011/M4)

US 2-Year Gov. Bond Yield (close), ∆ bps 0,78 0.88 0,57 2 bps 41 bps 34 bps 15 bps 0,15 (2011/M9) 1,18 (2010/M4)

US 10-Year Gov. Bond Yield (close), ∆ bps 1,84 1.85 1,48 34

bps 23 bps 50 bps 32 bps 1,38 (2012/M7) 4,01 (2010/M4)

Thank you for reading! Enjoy your summer!

Nova Economics Club – Newsletter team

JU

NE

N

EC

TA

LK

S

JO

HN

M. K

EY

NE

S

STA

TIS

TIC

S