nov17 presentation to investors atresmedia - antena3.com€¦ · presentation to investors ... iptv...

TRANSCRIPT

1Roadshow back up_Mar 2013 1Presentation to investors_Nov 17

ATRESMEDIA

Presentation to investors

Nov 2017

www.atresmediacorporacion.com

2Roadshow back up_Mar 2013 2Presentation to investors_Nov 17

Advertising market in Spain

Gross Ad market Yoy growth

+0.6%

-2.2% -7.1%

Total Ad market+2.9%

9M17 in line yoy for the Total Ad market

+5.3%

+14.0%

Source: I2p (Arcemedia)

+0.4%+2.7%

+8.9%

-0.7%

-8.5%

-0.04%

2016 9M17

2016 9M17 2016 9M17 2016 9M17 2016 9M17 2016 9M17

3Roadshow back up_Mar 2013 3Presentation to investors_Nov 17

TV: Clear leadership

Spanish Ad spending by medium Share

Advertising market in Spain

Source: Infoadex

+0.4pp

+25.6pp

-23.9pp

-0.3pp

-1.8pp

4Roadshow back up_Mar 2013 4Presentation to investors_Nov 17

Source: Infoadex and Bank of Spain

Total & TV market vs GDP is bouncing back

Total & TV ad intensity (vs GDP)

Advertising market in Spain

0.72% 0.74%

0.54%

0.41%0.46%

0.29%0.32%

0.23%

0.16% 0.19%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total Ad market

TV Ad market

2002-15 avg=0.58%

(All-time average= 0.73%)

2003-15 avg= 0.24%

(All-time average= 0.29%)

5Roadshow back up_Mar 2013 5Presentation to investors_Nov 17

72%

27%

60%

88%

Source: Internal estimates & EGM. 2016 data

9.3

6.2

1.32.5

Spanish TV: Best cost-coverage mix

Cost-coverage by mediumIn €/1,000 impacts & % penetration

CPT

Coverage

Advertising market in Spain

6Roadshow back up_Mar 2013 6Presentation to investors_Nov 17

Positive outlook for household consumption & GDP

Spanish TV industry: Main drivers

-0.5%

-2.1%

1.4% 2.6% 3.0%

4.4%

3.7%

-1.9%

-1.1%

1.0%

3.7% 3.5%

4.3%3.9%

2012 2013 2014 2015 2016 2017e 2018e

Consumption

GDP

Forecast

Source: Funcas (Sep17). In current prices

Household Consumption & GDP Yoy growth

7Roadshow back up_Mar 2013 7Presentation to investors_Nov 17

Sustainable recovery from very low historical levels

Gross TV Ad market In € mill

Source: Infoadex

Spanish TV industry: Ad market

16%10% 8% 9%

-11%

-23%

4%

-10%

-19%

-6%

11%6% 6%

2,317

3,469

2,378 2,472

1,703 1,890

2,011 2,122

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

% yoy Gross TV Ad market

Average: 2,450

-13%

-39%

8Roadshow back up_Mar 2013 8Presentation to investors_Nov 17

Spanish TV ad market vs other European countries

Source: GS & BoML

* consensus

104

119

79

121

100

92

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e*

Spanish TV Ad market is catching up with its peers

TV ad market growth by countryIn index terms. 2003=100

9Roadshow back up_Mar 2013 9Presentation to investors_Nov 17

Spanish TV industry: Ad market

Spanish TV Ad market: ≈Flat market in 2017

Gross TV Ad market Yoy growth

1%

-14%

-8%

-15%-18%

-15%

-24%-21%

-16%

-10%

-3%

6%

3%

8%

22%

13%12%

8%

3% 3%

6%

11%

1%3% 4%

-4%

3%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

FY11=-10%

FY12=-19%

FY13=-6%

FY14=+11%

Source: Infoadex.

FY15=+6% FY16=+6%

9M17=+0.8%

10Roadshow back up_Mar 2013 10Presentation to investors_Nov 17

Source: Internal Estimates

9M17: High dispersion among sectors

Ad spending by sectors% 9M17 yoy

Beauty &Hygiene

Food Autos Telcos Retail Finance Health Others

-7%-4%

8%

4%

-9% -7%

12%

5%

11% 12% 14% 10% 9% 9% 6% Weight30%

9M17=+0.4%

Spanish TV industry: Ad market

(Energy, Beverages, Cleaning, Home,Sports & leisure…)

11Roadshow back up_Mar 2013 11Presentation to investors_Nov 17

Source: • TV Market: Infoadex. 2016• Prices: Internal estimates. Conventional advertising. • Volumes: Internal estimates. Commercial hours: 13h-25h. Conventional advertising excluding TVE.

Steady growth in prices and volumes

2,317

3,469

1,703

1,890 2,011

2,122

100

146 147

109112 116

118

8389

9296

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Nominal Prices Volumes

TV Ad marketIn € million +

Market Prices & Volumesin index terms

TV ad market

Spanish TV industry: Prices and volumes

12Roadshow back up_Mar 2013 12Presentation to investors_Nov 17

Source: Infoadex

Stable market shares by player

Market share evolution by playerAd Share

43.3%43.3%43.4%44.2%43.7%

41.9%42.1%42.1%41.5%42.6%

5.3%6.0%6.6%6.8%7.1%5.2%4.8%4.3%4.3%4.0%4.3%3.8%3.6%3.2%2.6%

9M172016201520142013

Advertising market in Spain

Forta

Other FTAs

Pay TVs

13Roadshow back up_Mar 2013 13Presentation to investors_Nov 17

Spanish TV industry: Commercial FTA landscape

Net TV

Commercial FTA TV landscape (9M17)

Veo TV

Atresmedia has a key position in a wide commercial FTA TV offer

Channels

13TV

Secuoya

Real

Madrid TV

Kiss TV

AudienceMkt share Power ratio

26.4%41.9% 1.6x

29.1%43.3% 1.5x

3.1%

2.8%

2.0%

5.2% 0.5x

Source: Kantar Media, Infoadex

0.4%

0.4%

0.9%

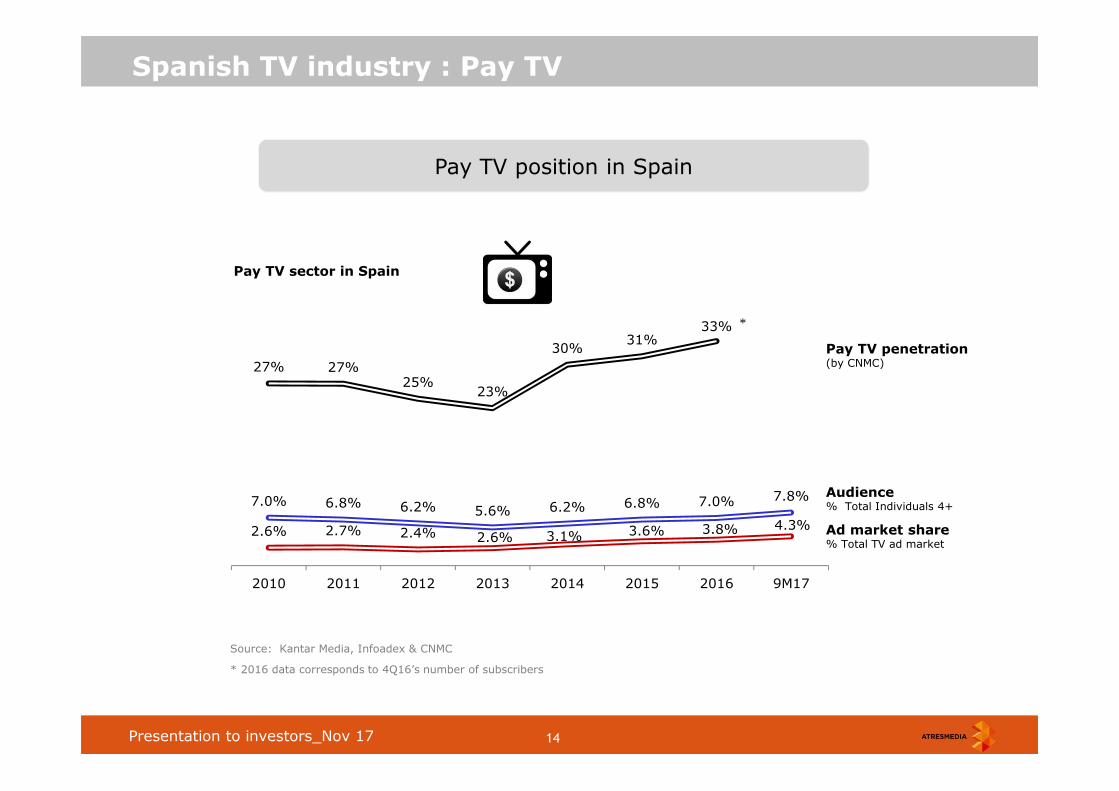

14Roadshow back up_Mar 2013 14Presentation to investors_Nov 17

Spanish TV industry : Pay TV

Pay TV position in Spain

Pay TV sector in Spain

Source: Kantar Media, Infoadex & CNMC

* 2016 data corresponds to 4Q16’s number of subscribers

Pay TV sector in Spain

Pay TV penetration (by CNMC)

Audience% Total Individuals 4+

Ad market share% Total TV ad market

7.0% 6.8% 6.2% 5.6% 6.2% 6.8% 7.0% 7.8%

27% 27%25%

23%

30%31%

33%

2.6% 2.7% 2.4% 2.6% 3.1% 3.6% 3.8% 4.3%

2010 2011 2012 2013 2014 2015 2016 9M17

*

15Roadshow back up_Mar 2013 15Presentation to investors_Nov 17

Spanish TV industry : Pay TV

Pay TV by platform type and player

Source: CNMC

Pay TV sector in Q1 17% Total connections (6.0 mill)

Satellite14%

Cable25%

IPTV57%

Others4%

Telefonica 59%

Vodafone 21%

Orange 9%

Others 11%

16Roadshow back up_Mar 2013 16Presentation to investors_Nov 17

Spanish TV industry : OTT TV

Source: Household panels. CNMC 2Q 17

OTT consumption is marginal

TV on demandQ2 17

18.4 mill households

15.9 millhouseholds

internet connected

4 millhouseholds

consume OTT

of which:

of which:

2.01 mill 0.41 mill1.16 mill

OTT

0.17 mill 0.13 mill0.19 mill

≈

17Roadshow back up_Mar 2013 17Presentation to investors_Nov 17

TV viewing

Source: Kantar Media. Non linear TV viewing includes +7 days viewing through TV set (TV viewing on desktops, tablet or mobile devices not included)

* Data from Feb 15

Average daily TV viewing In min

Linear TV viewing remains very strong

226 234 239 246 244 239 234 230

2009 2010 2011 2012 2013 2014 2015* 2016

Linear + Non linear

Linear237 233

87%

11%

1% 2%Online video

Linear TV

264 min2016

Average daily viewing In %

VoDTime shift

Source: Kantar Media & Comscore

18Roadshow back up_Mar 2013 18Presentation to investors_Nov 17

Average daily viewing In min

213233

Ind 4+

13 to 24

4 to 12

25 to 44

45 to 64

>65

TV viewing remains at very high levels

Source: Kantar Media

Age groups

Spanish TV industry: Audiences

230

Ind 4+ (+7 days)

351

302280

253

182191

126146

120143

19Roadshow back up_Mar 2013 19Presentation to investors_Nov 17

TV is by far the best media to reach brand awareness

Source: Kantar Media & Comscore Jan 17

Spanish TV vs Online Video Audiences

33.8

30.2

TV Top 5 onlinevideo platforms

In 1 day

In 1 month

Avg coverage in mill viewers

7.6

0.8

TV Video online

In 1 minute

Avg coverage in mill viewers

20Roadshow back up_Mar 2013 20Presentation to investors_Nov 17

Atresmedia: A leading communication group

Solid and clear group structure

OTHERS

ADVERTISING

Marketshare42%

Marketshare18%

Total Ad market

share19%

21Roadshow back up_Mar 2013 21Presentation to investors_Nov 17

TV & Radio as main source of revenues

Source: Infoadex & internal estimates

Atresmedia: Market positioning

ANTENA 3

NEOX

NOVA

Onda CeroEuropa FMOnda Melodía

Atresmedia CineAtresmedia Digital

Atresmedia Diversification

Radio

Others

TV

Planeta-De Agostini:RTL:Imagina:Treasury stock:Free-float:

41.7%18.7%4.1%0.4%

35.2%

89%

8%

3%

LA SEXTA

MEGAATRESERIES

2016 Net

Revenues

€ 1,021m92%

8%

Revenues by division Revenues by origin

Non ad revenues

Ad revenues2016 Net

Revenues

€ 1,021m

22Roadshow back up_Mar 2013 22Presentation to investors_Nov 17

In 2016, Total revenues and TV revenues higher than ever

Atresmedia’s Total Net Revenues & TV Net RevenuesIn € mill

Source: Atresmedia’s financial statements

Spanish TV industry: Ad market

668

1,016

704 741

1,021

539

879

604 639

909

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

23Roadshow back up_Mar 2013 23Presentation to investors_Nov 17

830883

970 1,021

High single digit growth in Rev while low single digit in OPEX

2013 2014 2015 2016 2017e guidance

750 756805 819 ≈+2%

Atresmedia: Revenues & OPEX evolution

CAGR +2.6%

Total Net Revenues

CAGR +7.7%

OPEX

In € euros

24Roadshow back up_Mar 2013 24Presentation to investors_Nov 17

65% of ∆ rev drops at the EBITDA

Atresmedia’s operating leverageIn € mill

2013 Revenue 2013 EBITDA 2016 EBITDA 2016 Revenue

830

80

≈65%operating leverage

202

1,021

Atresmedia: Operating leverage

+191 mill rev

+122 mill EBITDA

25Roadshow back up_Mar 2013 25Presentation to investors_Nov 17

Balanced and varied TV offer

Atresmedia Television: Positioning

Male Female

55-64

4-12

Age

9M17

2.1%

1.8%

1.1%

26.4%

2.4%

6.4%

12.4%

26Roadshow back up_Mar 2013 26Presentation to investors_Nov 17

13.4 13.6 13.512.8

12.4

13.514.5 14.8

14.4

13.4

10.210.0 9.8 10.1 10.3

2013 2014 2015 2016 2017YTD

13.413.8

13.512.8

12.212.2

13.6

14.1 13.5

12.5

8.2 7.97.8

8.8 8.5

2013 2014 2015 2016* 2017YTD

Antena 3: Stable audience ratings

Total Individuals24h

Commercial Target24h

Source: Kantar Media. Total Individuals (4y+)

Atresmedia Television: TV audiences by core channel

Source: Kantar Media• 2012-2015: Commercial Target (16-54 y)• *As of 2016: Commercial Target (25-59 y)

27Roadshow back up_Mar 2013 27Presentation to investors_Nov 17

6.0

7.2 7.47.1 6.6

6.0

6.7

7.2

6.56.2

8.5

7.87.3 7.2 7.2

2013 2014 2015 2016 2017YTD

6.6

7.9 8.1

8.1

7.37.4

8.2 8.4

7.6 7.2

5.8

5.2

4.8

5.35.6

2013 2014 2015 2016* 2017YTD

La Sexta: Leading Commercial Target

Total Individuals24h

Commercial Target24h

Source: Kantar Media. Total Individuals (4y+)

Atresmedia Television: TV audiences by second channel

Source: Kantar Media• 2012-2015: Commercial Target (16-54 y)• *As of 2016: Commercial Target (25-59 y)

28Roadshow back up_Mar 2013 28Presentation to investors_Nov 17

16.7 16.7 16.7 16.8 16.6

29.030.7 31.0

30.228.9

28.8 27.7 26.8 27.1 26.5

2013 2014 2015 2016 2017YTD

13.8 13.6 13.4 14.4 13.6

31.433.3 33.6

31.030.1

31.030.0 29.2 29.7

28.6

2013 2014 2015 2016* 2017YTD

Atresmedia TV: Solid ratings despite competing withless channels since 2014

Total Individuals24h

Commercial Target24h

Source: Kantar Media. Total Individuals (4y+)

Atresmedia Television: TV group audiences

Source: Kantar Media• 2012-2015: Commercial Target (16-54 y)• * As of 2016: Commercial Target (25-59 y)

29Roadshow back up_Mar 2013 29Presentation to investors_Nov 17

Audience: In-house vs external production

90% of most viewed contents are in-house, excl. sports

In-house 56%

3rd parties

44%

In-house vs externalTop 50 programmes (2016)

In-house 90%

3rd parties

10%

Including sports Excluding sports

30Roadshow back up_Mar 2013 30Presentation to investors_Nov 17

Programming costs: In-house vs external production

In-house 25%

3rd parties

75%

2/3 of the programming costs are internally produced

In-house 75%

3rd parties

25%

In-house vs external programming costsIn broadcasting hours

In-

house

64%

3rd parties

36%

Weighted average(based on audience per channel)

31Roadshow back up_Mar 2013 31Presentation to investors_Nov 17

Programming costs: In-house production

Direct sales to Broadcasters

In-house production: Velvet, a case study

FTA TV

Online

>100 countries

Atresmedia’s seriesReleased in 20144 seasons to date54 episodes

Production company:Bambú Producciones

Plot summary: Lovestories around GaleríasVelvet, one of the mostprestigious fashionstores in the Spain ofthe late 1950s.

Atresmedia’sPay TV channels

>24mill potential

households

3.8 mill viewers avg20.9% audience (+4 yrs)

>20 mill videos downloaded

32Roadshow back up_Mar 2013 32Presentation to investors_Nov 17

Atresmedia Radio: 18% market share

Atresmedia Radio: Positioning & Strategy

# 3 talk radio1.9 mill listeners

# 3 music radio1.9 mill listeners

#3 radio player in Spain

4.1 million listeners

18% market share

Source: EGM Q2 17 yearly averageMarket Share: Infoadex & internal estimates

New music radio

298k listeners

33Roadshow back up_Mar 2013 33Presentation to investors_Nov 17

Sound recovery from 2013 levels but still far behind fromaverage and peak levels

Gross Radio Ad market In € mill

Source: Infoadex

Spanish Radio industry: Ad market

6%13%

4% 7%

-5%

-16%

2%

-4%

-14% -11%

4%8%

1%

508

678

537 549

404 420

454 458

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

% yoy Gross Radio Ad market

Average: 530

-14%

-32%

34Roadshow back up_Mar 2013 34Presentation to investors_Nov 17

Atresmedia Radio: 4.1 million listeners

Atresmedia Radio: Audiences

Source: EGM Surveys Monday to Friday (.000) ( Moving average).

Thousand of listeners

4,954 4,8374,552

4,3194,119 4,153 4,106 4,091

2,662 2,6032,368

2,136

1,902 1,920 1,910

1,922

2,024 1,981 1,954 1,943

1,943 1,947 1,912

1,871

268 253 230 240 274 286 284 298

1st 15 2nd 15 3rd 15 1st 16 2nd 16 3rd 16 1st 17 2nd 17

35Roadshow back up_Mar 2013 35Presentation to investors_Nov 17

Atresmedia Digital: Positioning & Strategy

Websites & Verticals

• TV/Radio/News• > 18 mill unique

users /month• 12 verticals

ATRESPLAYER

• Long form video platform

• 10.0 mill app downloads

• 5.0 mill registeredusers

• AVoD and SVoD

MCNs

• Short form video platform

• Atrestube• Flooxer

Present in any possible source of audience & revenues

36Roadshow back up_Mar 2013 36Presentation to investors_Nov 17

Atresmedia Digital

Source: ComScore

7.9

9.6

12.2

2015

2014

+54%

Top 100 Spain Ranking(Monthly avg)

Source: ComScore 100 top properties MPMMX

#29th

#17th#11th

#11th

2013 2014 2015

4.3 mill uu

7.7 mill uu

9.6 mill uu

Unique users(Monthly avg)

Sound growth in unique users yoy

12.2 mill uu

2016

2016

37Roadshow back up_Mar 2013 37Presentation to investors_Nov 17

Atresmedia Digital: Atresplayer

Atresplayer: Atresmedia’s OTT offer

38Roadshow back up_Mar 2013 38Presentation to investors_Nov 17

Developing new non ad-based media initiatives

Atresmedia Diversification: Positioning & Strategy

39Roadshow back up_Mar 2013 39Presentation to investors_Nov 17

Atresmedia Diversification: International

≈19

x2.7

≈51

1422

5

20

9

9M 14 9M17

In mill suscribers

International division increased penetration by x2.7 in 3 years

40Roadshow back up_Mar 2013 40Presentation to investors_Nov 17

Atresmedia Diversification: Media for Equity

Media for Equity: Exploring new business models

Media for Equity

Exit in 2016

41Roadshow back up_Mar 2013 41Presentation to investors_Nov 17

Medium term goals: TV & Radio

Television and Radio’s EBITDA margin on track

EBITDA Margin EBITDA Margin

2013

404

Market Gross Ad revenues (€ mill) & EBITDA Margin

2013

1,703

2014

1,890

7%15%

17%19%

25%

2014

420

21%22%

24% 24%27%

Source: Infoadex & Atresmedia’s financial results

2015

2,0112015

454

≈2,400

/2,500 ≈500/

5252016

2,122 2016

458

42Roadshow back up_Mar 2013 42Presentation to investors_Nov 17

Other non-ad based revenues to double

≈10%

2017

≈5%

2014

x2

Medium term goals: Other revenues

≈7%

2015

Non-Ad revenuesas % of Total Revenues

≈8%

2016

43Roadshow back up_Mar 2013 43Presentation to investors_Nov 17

Debt at target level and dividend policy according to plan

Dividend policyTotal Net Debt Target (€ mill)

€ 150 mill

Payout ratio ≥80%185

134

158

179

148

2014 dividend: 0.20 €/sh96% payout ratio

2015 dividend: 0.36 €/sh82% payout ratio

2016 dividend: 0.92 €/sh100% payout ratio

• Ordinary: 0.47 €/sh- 0.22 €/sh (dec-16)- 0.25 €/sh (jun-17)

• Special: 0.45 €/sh- 0.45 €/sh (dec-17)

Long termtarget

Medium term goals: Financials

44Roadshow back up_Mar 2013 44Presentation to investors_Nov 17

Back up: 2016 & 9M17 Financial Results

Back up

45Roadshow back up_Mar 2013 45Presentation to investors_Nov 17

Net Revenues 1,021.1 970,2

EBITDA 202.0 165.7

Net profit 129.1 99.2

FY16 FY15

+5.2%

+21.9%

YoY

+30.1%

OPEX 819.1 804.5 +1.8%

Atresmedia

2016 Results in € mill: P&L

EBITDA Margin 19.8% 17.1%

Net profit Margin 12.6% 10.2%

Source: Atresmedia’s financial statements

EBIT 184.4 144.6 +27.6%

EBIT Margin 18.1% 14.9%

46Roadshow back up_Mar 2013 46Presentation to investors_Nov 17

Total Net Rev. 909.5 857.4

EBITDA 169.4 133.5

EBIT 154.1 118.7

FY 16 FY 15

+6.1%

+26.9%

YoY

+29.7%

OPEX 740.2 723.9 +2.2%

Atresmedia Television

FY16 Results in € mill: P&L

EBITDA Margin 18.6% 15.6%

EBIT Margin 16.9% 13.8%

Source: Atresmedia`s financial statements

47Roadshow back up_Mar 2013 47Presentation to investors_Nov 17

Net Revenues 82.2 89.9

EBITDA 19.7 21.8

EBIT 17.7 20.0

FY 16 FY 15

-8.6%

-9.8%

YoY

-11.1%

OPEX 62.5 68.0 -8.2%

Atresmedia Radio

FY 16 Results in € mill: P&L

EBITDA Margin 24.0% 24.3%

EBIT Margin 21.6% 22.2%

Source: Atresmedia’s financial statements

48Roadshow back up_Mar 2013 48Presentation to investors_Nov 17

Financials

Contribution to consolidated group

Atresmedia: “Others” Division

Net Revenues 29.4

EBITDA 12.9

FY 16 FY 15€ mill

22.9

10.4

Net revenues split

Source: Atresmedia’s financial statements

Others* 56%Films

23%

Events 21%

*Others (Internet, Editorial, new initiatives…)

OPEX 16.5 12.6

49Roadshow back up_Mar 2013 49Presentation to investors_Nov 17

Net Revenues 755.1 740.2

EBITDA 148.6 151.5

Net profit 103.5 101.5

9M 17 9M 16

+2.0%

-1.9%

YoY

+1.9%

OPEX 606.5 588.7 +3.0%

Atresmedia

9M 17 Results in € mill: P&L

EBITDA Margin 19.7% 20.5%

Net profit Margin 13.7% 13.7%

Source: Atresmedia’s financial statements

EBIT 135.6 138.1 -1.8%

EBIT Margin 18.0% 18.7%

50Roadshow back up_Mar 2013 50Presentation to investors_Nov 17

Total Net Rev. 664.9 661.0

EBITDA 127.0 128.9

EBIT 116.0 117.3

9M 17 9M 16

+0.6%

-1.4%

YoY

-1.2%

OPEX 537.8 532.1 +1.1%

Atresmedia Television

9M 17 Results in € mill: P&L

EBITDA Margin 19.1% 19.5%

EBIT Margin 17.4% 17.8%

Source: Atresmedia`s financial statements

51Roadshow back up_Mar 2013 51Presentation to investors_Nov 17

Net Revenues 60.0 58.8

EBITDA 12.1 14.6

EBIT 10.5 13.1

9M 17 9M 16

+2.2%

-17.2%

YoY

-19.6%

OPEX 48.0 44.2 +8.6%

Atresmedia Radio

9M 17 Results in € mill: P&L

EBITDA Margin 20.1% 24.8%

EBIT Margin 17.5% 22.3%

Source: Atresmedia’s financial statements

52Roadshow back up_Mar 2013 52Presentation to investors_Nov 17

Financials

Contribution to consolidated group net of eliminations

Atresmedia: Others Division

Net Revenues 30.2

EBITDA 9.5

9M 17 9M 16€ mill

20.5

8.0

Net revenues split

Source: Atresmedia’s financial statements

Others* 53%Films

26%

Events 21%

*Others (Internet (also Smartclip), Editorial…)

53Roadshow back up_Mar 2013 53Presentation to investors_Nov 17

Legal Notice

The information contained in this presentation has not been independently verified and is, in any case, subject to

negotiation, changes and modifications.

None of the Company, its shareholders or any of their respective affiliates shall be liable for the accuracy or completeness

of the information or statements included in this presentation, and in no event may its content be construed as any type of

explicit or implicit representation or warranty made by the Company, its shareholders or any other such person. Likewise,

none of the Company, its shareholders or any of their respective affiliates shall be liable in any respect whatsoever

(whether in negligence or otherwise) for any loss or damage that may arise from the use of this presentation or of any

content therein or otherwise arising in connection with the information contained in this presentation. You may not copy or

distribute this presentation to any person.

The Company does not undertake to publish any possible modifications or revisions of the information, data or statements

contained herein should there be any change in the strategy or intentions of the Company, or occurrence of unforeseeable

facts or events that affect the Company’s strategy or intentions.

This presentation may contain forward-looking statements with respect to the business, investments, financial condition,

results of operations, dividends, strategy, plans and objectives of the Company. By their nature, forward-looking

statements involve risk and uncertainty because they reflect the Company’s current expectations and assumptions as to

future events and circumstances that may not prove accurate. A number of factors, including political, economic and

regulatory developments in Spain and the European Union, could cause actual results and developments to differ materially

from those expressed or implied in any forward-looking statements contained herein.

The information contained in this presentation does not constitute an offer or invitation to purchase or subscribe for any

ordinary shares, and neither it nor any part of it shall form the basis of or be relied upon in connection with any contract or

commitment whatsoever.

Investor Relations Department

Additional information

Phone: +34 91 623 46 14

E-mail: [email protected]

Web: www.atresmediacorporacion.com