northwest independent school district · · 2016-05-10northwest independent school district fort...

TRANSCRIPT

Northwest Independent School District

Fort Worth, Texas

Comprehensive Annual

Financial Report

For the Fiscal Year Ended June 30, 2007

Prepared by the Financial Services Department

Jon Graswich, CPA Chief Financial Officer

DeAnne Hatfield, CTSBO

Director of Business Services

1

THIS PAGE LEFT BLANK INTENTIONALLY

2

…

……

…

…

…

…

……

………

…

NORTHWEST INDEPENDENT SCHOOL DISTRICTCOMPREHENSIVE ANNUAL FINANCIAL REPORT

FISCAL YEAR ENDED JUNE 30, 2007

TABLE OF CONTENTS

Exhibit PageIntroductory Section Number NumberTitle Page…..…………………………………………..………………………………………………… 1 1Table of Contents………………………..…………..……………………….……………………………… 1 3Transmittal Letter………………………………………………….…………….………………………… 1 7GFOA Certificate of Achievement for Excellence in Financial Reporting….….……….……………… 1 19ASBO Certificate of Excellence in Financial Reporting………………………….……………………… 1 20Administrative Organizational Chart………………………………………………………………………. 1 21Board of Trustees………………………………………………………….………………………………… 1 22School Board and Administrators………………………………….……………………………………… 1 23Consultants and Advisors………………………………….………………………………………………… 1 24

Financial Section

Independent Auditor's Report……………………………………………………………………………… 1 26Management's Discussion and Analysis…………………………….……….…………………………… 1 28Basic Financial Statements:

Government Wide Financial Statements: Statement of Net Assets…………………………………………………………………………… A-1 35Statement of Activities………………………………………………………………………… B-1 37

Fund Financial Statements:Balance Sheet - Governmental Funds…………………………………………………………… C-1 38Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Assets…………………………………………………………………… C-2 41Statement of Revenues, Expenditures, and Changes in Fund Balance - Governmental Funds……………………………………………………… C-3 42Reconciliation of the Governmental Funds Statement of Revenues, Expenditures, and Changes in Fund Balances to the Statement of Activities……………… C-4 44

Statement of Net Assets - Proprietary Funds………...……………………………………………… D-1 45Statement of Revenues, Expenses, and Changes in Fund Net Assets -

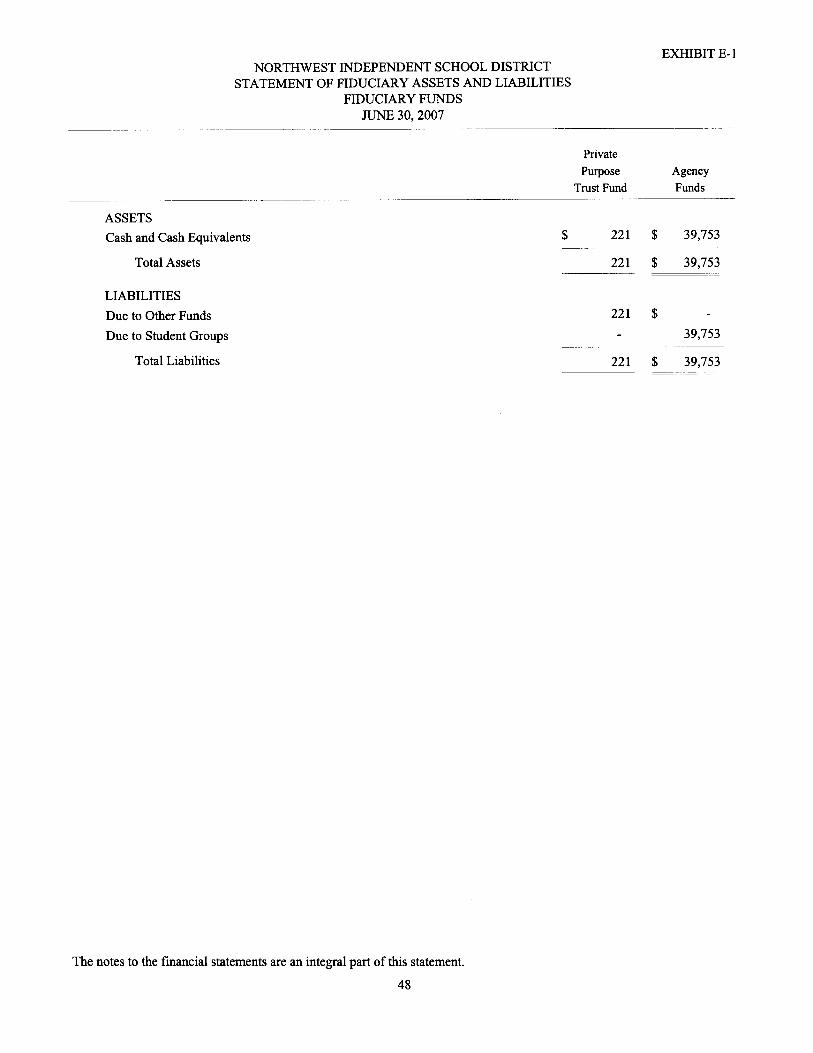

Proprietary Funds……………………………………………………………………………… D-2 46Statement of Cash Flows - Proprietary Funds……………………………………………………… D-3 47Statement of Fiduciary Assets and Liabilities……………………………………………………… E-1 48Statement of Changes in Fiduciary Fund Net Assets…………………………………………………… E-2 49Notes to the Financial Statements…………………………………………………………………… 1 50

3

… …

……

……

…

…

……

NORTHWEST INDEPENDENT SCHOOL DISTRICTCOMPREHENSIVE ANNUAL FINANCIAL REPORT

FISCAL YEAR ENDED JUNE 30, 2007

TABLE OF CONTENTS

Exhibit PageFinancial Section (Continued) Number NumberRequired Supplementary Information:Schedule of Revenues, Expenditures, and Changes in Fund Balance, Budget and

Actual - General Fund………………………………………………………………………………… G-1 65Combining and Individual Fund Statements and Schedules:

Nonmajor Governmental Funds - Special Revenue Funds………...…………………………………… 1 66Combining Balance Sheet - Nonmajor Governmental Funds…..………… ……………………… H-1 68

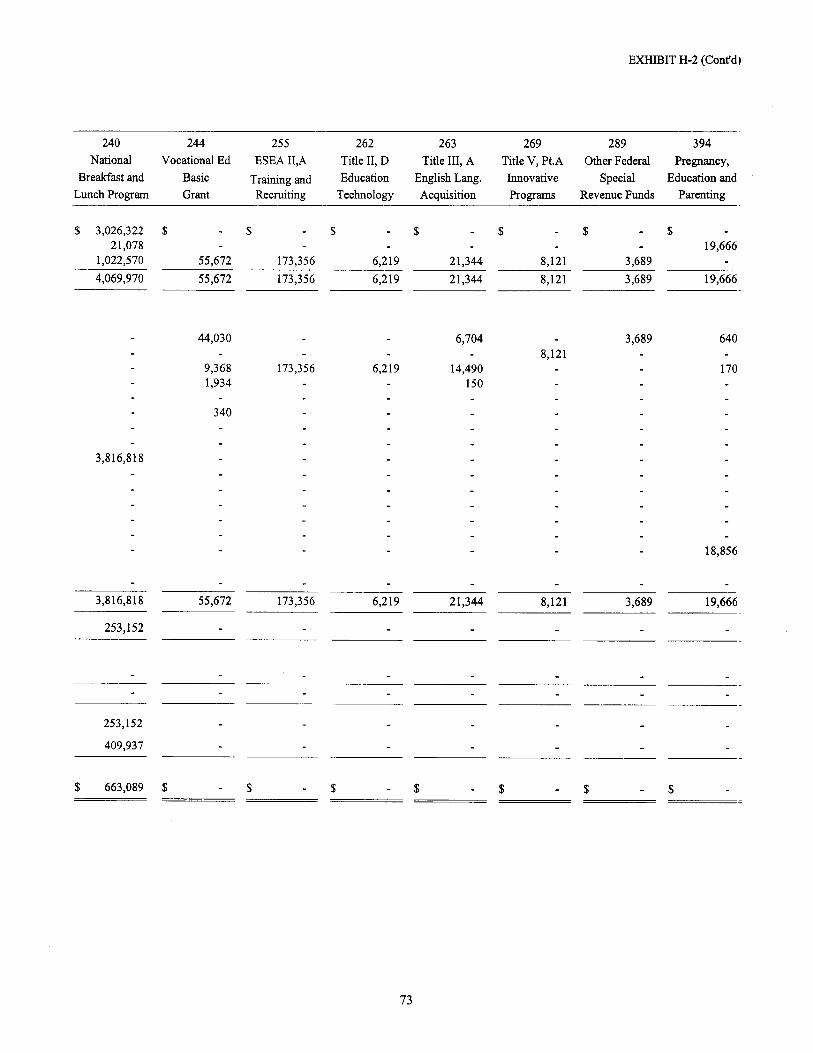

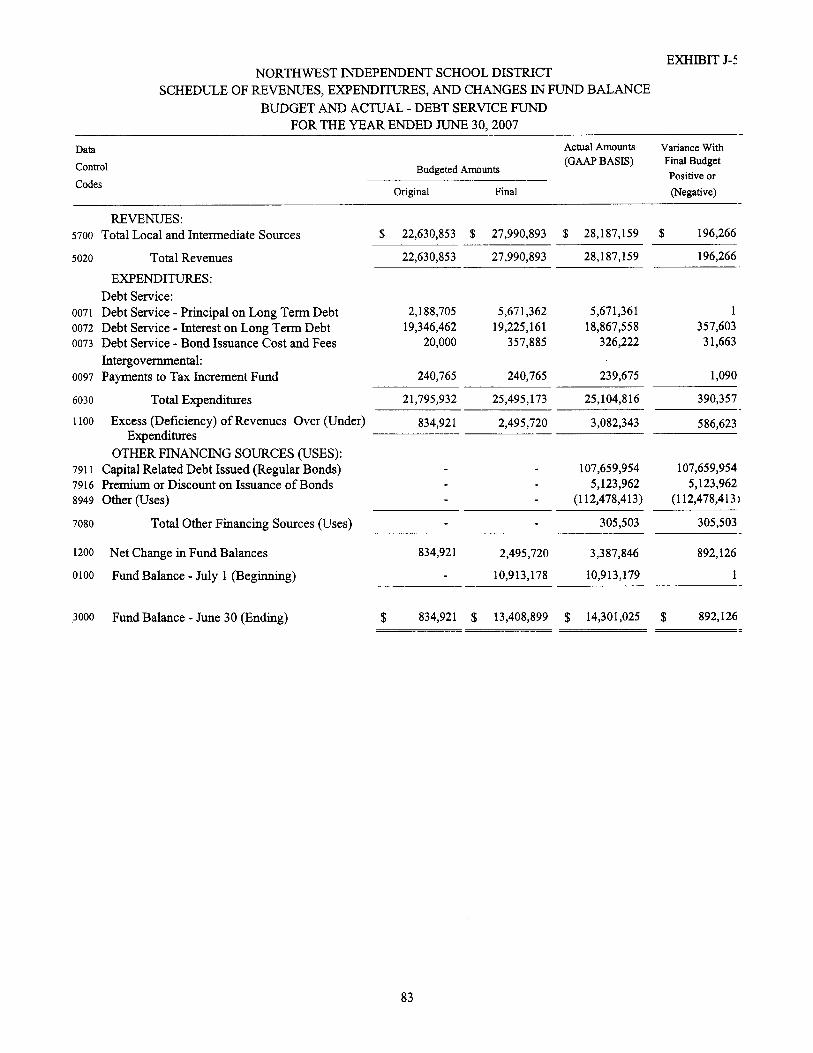

Combining Statement of Revenues, Expenditures and Changes in Fund Balances - Nonmajor Governmental Funds……………………………………………………… H-2 72Combining Statement of Net Assets - Internal Service Funds……………………………………… H-3 78Combining Statement of Revenues, Expenses and Changes in Fund Net Assets - Internal Service Funds………………..…………………………………………… H-4 79Combining Statement of Cash Flows - Internal Service Funds……………………………..……… H-5 80Combining Statement of Changes in Assets and Liabilities - All Agency Funds……………………… H-9 81Schedule of Revenues, Expenditures, and Changes in Fund Balance - Budget and Actual - Child Nutrition Program………………………………………………………………………… J-4 82Schedule of Revenues, Expenditures, and Changes in Fund Balance - Budget and Actual - Debt Service Fund………………………………………………………………………………… J-5 83

Capital Assets Used in the Operation of Governmental Funds:Schedule by Function and Activity……………….………………………………………………… 1 84Schedule of Changes by Function and Activity………………………………………………………… 1 85Schedule by Location…………………………..……….…………………………………………… 1 86

Compliance Schedules: Schedule of Delinquent Taxes Receivable…………………………………………………………… J-1 88

Schedule of Expenditures for Computations of Indirect Cost for 2008-2009………….…………… J-2 90Fund Balance and Cash Flow Calculation Worksheet……………………………………………… J-3 91

Statistical SectionNet Assets By Component Last Six Fiscal Years…………………………………………………………. Sch. 1 94Expenses, Program Revenues and Net (Expense)/Revenue Last Six Fiscal Years……………………….. Sch. 2 96

General Revenues and Total Change in Net Assets Last Six Fiscal Years……………………………….. Sch. 3 98

4

Sch. 3

NORTHWEST INDEPENDENT SCHOOL DISTRICTCOMPREHENSIVE ANNUAL FINANCIAL REPORT

FISCAL YEAR ENDED JUNE 30, 2007

TABLE OF CONTENTS

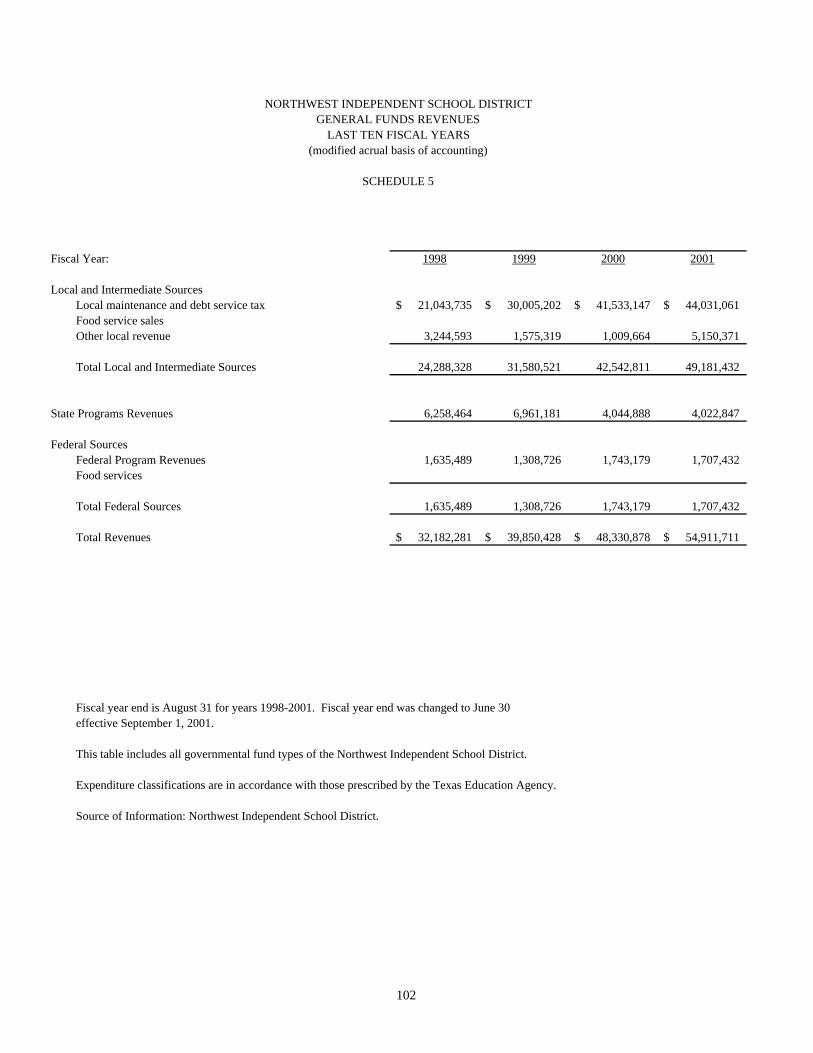

Exhibit PageStatistical Section (Continued) Number NumberFund Balances, Governmental Funds Last Six Fiscal Years……………………………………………… Sch. 4 100General Funds Revenues Last Ten Fiscal Years………………………………………………………….. Sch. 5 102Governmental Funds Expenditures and Debt Service Ratio Last Ten Fiscal Years……………………… Sch. 6 104Other Financing Sources and Uses and Net Change in Fund Balances, Governmental Funds

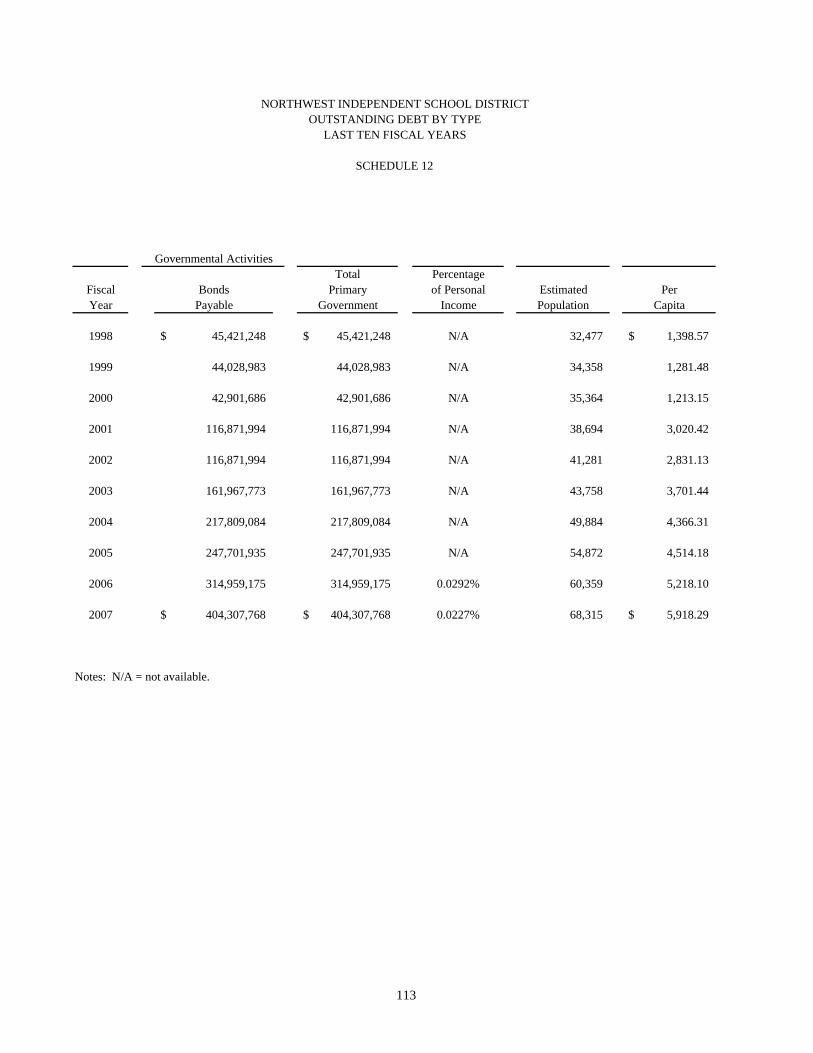

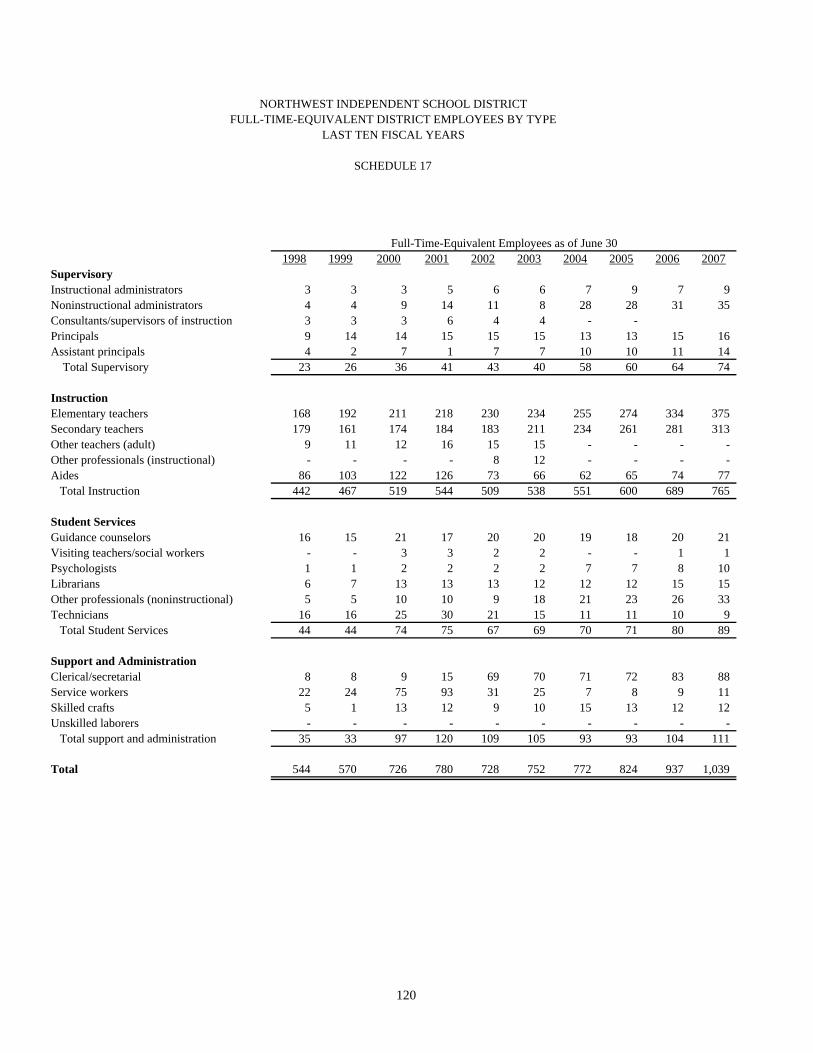

Last Ten Fiscal Years………………………………………………………………………………… Sch. 7 106Assessed Value and Actual Value of Taxable Property Last Ten Fiscal Years………………………….. Sch. 8 108Direct and Overlapping Property Tax Rates Last Ten Fiscal Years……………………………………… Sch. 9 109Principal Property Taxpayers Current Year and Nine Years Ago……………………………………….. Sch. 10 110Property Tax Levies and Collections Last Ten Fiscal Years…………………………………………….. Sch. 11 112Outstanding Debt By Type Last Ten Fiscal Years……………………………………………………….. Sch. 12 113Direct and Overlapping Governmental Activities Debt………………………………………………….. Sch. 13 114Legal Debt Margin Information Last Ten Fiscal Years………………………………………………….. Sch. 14 116Demographic and Economic Statistics Last Ten Fiscal Years…………………………………………… Sch. 15 118Principal Employers Current Year……………………………………………………………………….. Sch. 16 119Full-Time Equivalent District Employees by Type Last Ten Fiscal Years………………………………. Sch. 17 120Expenditures, Enrollment and Per Pupil Cost Last Ten Fiscal Years……………………………………. Sch. 18 121School Building Information Last Ten Fiscal Years…………………………………………………….. Sch. 19 122

Single Audit SectionReport on Compliance and on Internal Control over Financial Reporting based on an Audit of Financial Statements in Accordance with Governmental Auditing Standards…….….….....………….. 1 126Report on Compliance with Requirements Applicable to each Major Program and Internal Control Over Compliance in Accordance with OMB Circular A-133…….….…...……………………………. 1 127Schedule of Findings and Questioned Costs………….…..……..………….…..………..…..…………… 1 129Schedule of Status of Prior Findings………...….…..……..……..…….…….…..………...…………….. 1 130Schedule of Expenditures of Federal Awards……………………………………...……..………………. K-1 131Notes on Accounting Policies for Federal Awards…………………..…….……...…...…………………. 1 132

5

INTRODUCTORY SECTION

6

The independent audit of the financial statements is part of a broader, federally mandated “Single Audit” designed to meet the special need of federal grantor agencies. The standards governing Single Audit engagements require the independent auditor to report not only on the fair presentation of the financial statements, but also on the audited government’s internal controls and compliance with legal requirements, with special emphasis on internal controls and legal requirements involving the administration of federal rewards. These reports are available in the Single Audit Section of this report. GAAP require that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (MD&A). This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. The District’s MD&A can be found immediately following the report of the independent auditors. Profile of the District In the late 1800’s, schools began appearing in the area amid railroads, general stores, and livery stables. Descendants of early settlers recall tales of early schoolhouses and how in 1949 the one-school districts in Justin, Haslet, Rhome, and Roanoke joined hands to form the Northwest Independent School District. Newark was annexed in 1973. Residents of the district elect a seven-member Board of Trustees (the Board), each of which serves for three years. Monthly meetings of the Board are posted and advertised as prescribed under state law so that the Board may fulfill its charge to the students, parents, staff, and taxpayers of the District. Special meetings or study sessions are scheduled as needed. The Board has final control over all school matters except as limited by state law. Serving the communities of Haslet, Justin, Newark, Rhome, Roanoke, Trophy Club, Aurora, Avondale, Drop, New Fairview, Marshall Creek, and Northlake, along with portions of Fort Worth, Southlake, Westlake, and Flower Mound, the District’s boundaries encompass approximately 232 square miles in Denton, Tarrant, and Wise Counties. The District provides a well-rounded program of public education for children from pre-kindergarten through grade twelve. In addition to basic instructional programs, the District offers special education, gifted and talented, bilingual/ESL, remedial, college preparatory, and career and technical programs. The District is fully accredited by the Texas Education Agency (TEA). The District operates ten elementary schools, three middle schools, a high school, an alternative education program campus, and one special campus. Enrollment for the 2006-07 year was 10,334 students, an increase of approximately 18.7% over the previous year. A total of 400 seniors graduated from the District in 2007. The mission of the Northwest Independent School District, in partnership with parents and community, is to provide all students a premier education preparing them to be successful, productive citizens. A high degree of professionalism exists among our employees, and an on-going recognition of student and staff excellence contributes to this environment. The instructional program is geared toward having the student meet or exceed grade level expectations. Emphasis is placed on higher level thinking skills, including research methodologies and independent, complex and critical thinking skills. The District attracts highly qualified personnel because of its commitment to excellence. During the 2006-07 school year, the District employed 1039 employees consisting of 851 professionals, 77 educational aides, and 111 auxiliary staff. Professional employees include 688 classroom teachers with an average of 10.1 years of experience. 21.3 percent of the teaching staff has earned a master’s degree and .8 percent of the teaching staff has earned a doctorate degree. The average student/teacher ratio is 15.02 in the District. Texas law mandates that no more than 22 students can be assigned to one classroom teacher in kindergarten through fourth grade. The annual budget serves as the foundation for the District’s financial planning and control. The District budget process is instructionally driven. District budget planning begins with the senior administrative staff and the Board of Trustees holding goal setting sessions. The Budget Calendar and Five-Year Forecast are

8

reviewed with the Board of Trustees. Also, campuses annually prepare the required Campus Improvement Plans. Budget preparation begins with a training session with principals and program managers. At that time, the Budget Manual and budget worksheets are distributed and budgets are prepared on-line instead of strictly on paper submissions. The District uses site-based budgeting to enhance the ability of principals to serve as effective instructional leaders. Site-based budgeting places the principal at the center of the budget preparation process. The Campus Budget Worksheet reflects the initial campus funding allocations. These allocations address equity issues between campuses. They are designed around three cost drivers: pupils, staff, and buildings. Pupil allocations reflect both the number of students and additional funds for special needs students. Staff allocations provide for campus staff development. Building allocations are based on building size, age, and reflect past usage. The initial allocation represents 80% of the campus funding allocation based on projected enrollment. The remaining amount is distributed in November based on actual enrollment. The allocation may be revised by the Principal per the Campus Improvement Plan subject to review. After the completed campus and program budget packages have been returned, they are reviewed in detail by the Superintendent with the senior staff. The review focuses on the instructional impact. The Board of Trustees regularly receives budget updates that include any revisions to the earlier Five-Year Financial Forecast. The Texas Legislative biannual session met in 2007 and revisions to school finance were reviewed with the Board of Trustees. The Board of Trustees reviewed the budget in June and adopted the Personnel Compensation Plan. The proposed budget must be prepared by June 19th for a July 1 fiscal year start date. The board president must call a board meeting for the purpose of discussing and adopting the budget and the tax rate. A notice of this meeting is required to be published at least 10 days but no more than 30 days before the public meeting. The budget must be adopted prior to June 30th for a July 1 fiscal year start date. Budget Adoption. The Denton Central Appraisal District Projected Estimate of the 2006 Certified Appraisal roll occurred on June 5, 2006, and the Denton County Tax Assessor-Collector calculated the rollback tax rate on June 6, 2006. The required legal notices were published. The Board of Trustees adopted the budget on June 26, 2006. Tax Rate Adoption. The Denton Central Appraisal District Certification of the 2006 Appraisal Records occurred on July 25, 2006, and the Denton County Tax Assessor-Collector calculated the rollback tax rate on July 28, 2006. The required legal notices were published. The Board of Trustees held the required public meeting and adopted the tax rate on August 28, 2006. The District maintains budgetary controls throughout all of its financial systems. The objective of budgetary controls is to ensure compliance with legal provisions embodied in the official budget adopted by the Board. The Board adopts an official budget for the general fund, debt service fund, and child nutrition program (which is included in special revenue funds). In accordance with procedures prescribed by the State Board of Education, budget amendments that affect the total amount in a fund or functional spending category must be approved by the Board prior to the expenditure of funds. The functional level is specified by Board policy as the legal level of encumbrance of estimated purchase amounts prior to the release of purchase orders to vendors. Outstanding encumbrances at the end of the fiscal year are an accounts payable and are treated as expenditures in the prior year upon receipt of the goods and services. Factors Affecting Financial Condition The information presented in the financial statements is perhaps best understood when it is considered within the broader perspective of the specific environment in which the District operates.

9

Introduction. The Northwest Independent School District, uniquely situated northwest of the Fort Worth/Dallas Metroplex, lies within one of the fastest growing areas in Texas. Northwest stretches across 232 square miles and is located in Denton, Tarrant and Wise Counties, Texas. Population. The population of the Northwest Independent School District in 2000 was 35,364 as compared to 68,315 in 2007. Local economy. The commercial, industrial, and residential growth of the District has kept pace with that of the Fort Worth/Dallas area, and has been aided by the District’s close proximity to both the Dallas/Forth Worth International Airport and Fort Worth’s Alliance Airport. Diversified manufacturing is responsible for the local economy with increasing growth in commercial aviation. Agriculture-oriented industries relating to livestock marketing, grain and agri-business related industry and services join with the aerospace products, food and beverage, mobile homes, auto making, and medical industries to offer numerous manufacturing jobs in the Metropolitan Area. Area Developments Alliance Industrial Park. Alliance is a joint effort of Hillwood Development, the City of Fort Worth and neighboring communities, the Federal Aviation Administration and other government and civic leaders in the development and operation of an industrial airport, business community, and international trade center. Alliance is located in the northwest corner of the Dallas/Fort Worth Metroplex, within the northern limits of the City of Fort Worth. Alliance’s access to highway, rail and air transportation offers an excellent opportunity for future commercial and industrial growth. More than 140 companies have located to Alliance, building 25 million square feet, creating 24,000 jobs and generating $26 billion economic impact to North Texas. There are five business parks within Alliance. Alliance Center. At the heart of Alliance Center is the 414 acre Alliance Airport. Over a decade ago, the City of Fort Worth, the FAA and Alliance began work on the first purely industrial airport in the Western Hemisphere. The airport officially opened December 1989, and the Spirit of Alliance took flight. Today, Alliance Airport features the full complement of flight services and is the cornerstone for the nation’s fastest growing industrial complex. Alliance Airport is one of few North Texas airports capable of accommodating heavy transport aircraft such as the DC-10 and 747. This city owned airport is managed by privately held Alliance Air Services and boasts a 9,600 foot runway (with plans to expand to 13,000 feet). Alliance Airport provides state-of-the-art infrastructure and an award winning FAA Control Tower. It is FAR Part 139 certified and operates 24/7/365. American Airlines, a Fortune 500 company, operates a $481 million aircraft maintenance and engineering center from its complex, which houses the largest single cantilever building in the world. Bell Helicopter TEXTRON operates its Customer Center within Alliance Center. The facility offers Bell Helicopter Textron 64,000 square feet of office space, 82,000 square fee of hangar space and 15,000 square feet of warehousing space. As a result of engineering and composite operations associated with the construction of the tilt-rotor vehicle V-22 Osprey, Bell/Agusta Aerospace Company in joint venture with Bell Helicopter operates a 29,225 square foot headquarters for its civilian tilt-rotor operations. At Alliance, the company develops, manufactures, and markets its BA 609, the world’s first civilian certificated tilt-rotor, as well as the AB 139, a medium twin-engine helicopter. The Federal Aviation Administration operates the Alliance Airport Air Traffic Control Tower, A Flight Standards District Office and an Airways Facilities Sector field office in Alliance Center, supervising aircraft, agencies and personnel in 30 Texas counties.

10

Federal Express, a Fortune 500 firm, is the world’s largest express transportation company. The Southwest Regional Hub at Alliance is the company’s only completely automated hub and includes seven buildings, aircraft ramp areas and parking for delivery trucks. The facility handles 175,000 packages daily. Galderma, a leading research based pharmaceutical company dedicated to developing prescription and over the counter dermatological products, established its U.S. headquarters and national distribution center at Alliance. The U.S. Drug Enforcement Agency operates a 140,000 square foot National Airwing Headquarters with 155 employees on the airport grounds. Since this facility is owned by the City, the facility is not subject to ad valorem taxation. Alliance Gateway. Alliance Gateway, with over 2.8 million square feet of distribution and manufacturing space, is home to major corporations, including Nestle Distribution Company (food and candy distribution facility), Nokia Mobile Phones (cellular phone manufacturing and distribution), Southwestern Bell Telephone (customer call center) and Zenith Electronics (consumer electronics distribution facility). The James River Paper Company has built a 375,000 square foot facility for its regional distribution center. In 1999, TD Ameritrade, an online stock brokerage firm began operations of a national call center and customer service center at Alliance Gateway. Alliance Commerce Center. Corporations operating regional and national distribution facilities at Alliance Commerce Center include Andersen Logistics, Caremark, CompuCom Systems, GWS Perlos, Motivating Graphics, Patterson Dental Company, Recaro Aircraft Seating and Valmont Electric. These companies occupy approximately 300,000 square feet and employ over 240 persons. A garden office complex of 300,000 square feet called Heritage Commons is complete and houses Hillwood Development Operations. Westport at Alliance. Burlington Northern/Santa Fe Railway Company (BNSF), a Fortune 500 firm, operates three facilities at Alliance: the BNSF Automotive Facility, the BNSF Alliance Intermodal Facility and the BNSF Rail Yard. Handling over 100,000 vehicles annually, the 55-acre Auto Facility serves as a distribution port for DaimlerChrysler, American Honda, Hyundai and Kia. The 735 acre, $115 million intermodal yard is one of the largest intermodal facilities in the country. The state-of-the-art JC Penney Alliance Logistics Center features one of the largest steel rack-supported systems in the nation. With 17 levels and 105 bays of storage space, the 145,520 load cells can store approximately 72,000 pounds of merchandise. The distribution center annually processes 10,000 to 13,000 shipping containers from international ports, taking advantage of its proximity to the intermodal yard at Alliance. Other distribution centers located in this Alliance Sector include Grainger Industrial Supply, Hyundai, Kraft Foods/AmeriCold Logistics, Michaels Stores, SC Johnson & Son, Inc., and Volkswagen. Alliance Crossing. Alliance Crossing includes corporate office, financial, healthcare, lodging, and restaurant facilities. The U.S. Postal Service operates a full-service retail outlet and the City of Fort Worth Police Department operates a police substation from the Alliance Crossing retail center. Over 100 persons work in this retail-commercial development. Burlington Northern Santa Fe Railroad. Burlington Northern has completed construction of its $100 million Network Operations Center (“NOC”) on the company’s Western Center Boulevard property in north Fort Worth. The NOC comprised of two buildings totaling more than 250,000 square feet, is a high-tech, state-of-the-art facility which serves as the control and tracking center for all of Burlington’s railroads through the United States. Cabela’s. Known as the World’s Foremost Outfitter of hunting, fishing and outdoor gear opened its eleventh retail store in Alliance. A 230,000 square foot mega store, which contains an aquarium, museum,

11

and exhibit space, in addition to the retail, opened in May 2005. Cabela’s invested approximately $50 million in the facility, which employs approximately 500 individuals. Texas Motor Speedway. Located in far north Fort Worth at the intersection of Interstate 35-W and State Highway 114, the $110 million Texas Motor Speedway was completed in the Spring of 1997. The facility includes a 1.5 mile racing oval, grandstand seating for more than 200,000 spectators and approximately 200 luxury suites. An office tower and condominiums have also been constructed on the property. Pursuant to the terms of an agreement between the speedway developer and the Fort Worth Sports Authority, Inc., Texas Motor Speedway is owned by the Authority and leased to the developer, and most of the property comprising the Speedway is exempt from ad valorem taxes. Texas Motor Speedway is the second-largest sports and entertainment facility in the nation where dual-bank turns allow for NASCAR and IRL IndyCar racing, plus every major form of American automobile racing. NASCAR Winston Cup (now known as the Nextel Cup) races have been held at the Texas Motor Speedway as well as sanctioned IRL Indy Car races. NASCAR has sanctioned two Nextel Cup races for the speedway. The facility has hosted several major music concerts and other large events since opening. Historical Employment Data.

Average Annual

2006

Average Annual

2005

Average Annual

2004

Average Annual

2003

Average Annual

2002 Denton County Civilian Labor Force 326,387 309,312 280,271 276,295 278,937 Unemployed 13,821 13,174 11,560 13,042 13,980 Percent of Unemployment 4.23% 4.26% 4.12% 4.72% 5.01% State of Texas Civilian Labor Force 11,487,496 11,225,882 10,963,014 11,004,878 10,750,664 Unemployed 565,823 596,276 651,679 728,459 680,864 Percent of Unemployment 4.93% 5.31% 5.94% 6.62% 6.33%

Health Services. The Metroplex area, including the District, is served by more than 70 hospitals which offer specialized services such as organ transplantation, major trauma care, cancer treatment, kidney dialysis and chemical dependency treatment. Air Transport and Airline Industry. The Dallas/Fort Worth International Airport (the “Airport”) is the fourth busiest airport in the United States in terms of operations and passengers. The Airport is the principal air carrier facility serving the Dallas/Fort Worth metropolitan area, providing service to national and international destinations. The Airport provides nonstop services to Europe, the Far East, Canada, Mexico, Central and South America, the Caribbean and the Bahamas. The September 11, 2001 terrorist attacks, in combination with the general economic downturn in the airline industry, have had a significantly adverse effect on the airline industry. Since the attacks, most major U.S. airlines, including those servicing the Airport, have significantly reduced flight schedules and instituted extensive job cuts in an attempt to stem mounting losses. American Airlines is the predominant airline servicing the Airport, and is among the top ten taxpayers of the County. In January 2005, Delta Airlines, a former top ten taxpayer of the County, eliminated the use of the Airport as a national hub. Meacham International Airport, a Fort Worth municipally owned and operated general aviation airport, located in northern Fort Worth is a fixed based operation for private and commercial services equipped with a 7,500 foot runway. Meacham provides sophisticated instrument approach facilities, lighted

12

runways, terminal facilities and fuel and maintenance services. Fort Worth Spinks Airport, a general aviation airport located in the southwestern portion of the City is equipped with a 6,000 foot runway and two taxiways. Alliance Airport serves the needs of industrial, business, and general aviation users and is currently equipped with a 9,600 foot runway. Surface Transport. Three interstate highways (Interstate 20, Interstate 30 and Interstate 35), five federal and four state highways provide all-weather routes within Fort Worth and to and from the rest of the nation. Interstate 820, which encircles the City, allows quick access to all parts of the Fort Worth area. The Texas Highway Commission has completed a master highway construction plan for Tarrant County to provide for transportation needs through the foreseeable future, including relocation of Interstate 30 from a point just east of downtown to several miles west. This project is underway and will promote redevelopment of the south end of the Central Business District and the Hospital District southwest of downtown. Fort Worth is served by six major railroad systems. Burlington Northern/Santa Fe Railroad has its corporate headquarters in Fort Worth. Rail passenger service is provided through Fort Worth, including AMTRAK service between Houston and Chicago. Fort Worth’s position as a major southwest distribution center is supported by the presence of 75 regular route motor carriers with over 750 schedules. Local transit service is provided by The T, operated by the Fort Worth Transportation Authority. Trinity Railway Express provides service for the Metroplex. Greyhound/Trailways Bus Lines furnish Fort Worth with transcontinental passenger service; intrastate bus service is provided by Transportation Enterprises and Texas Bus Lines. State Funding. Demographic predictions indicate that the District’s enrollment will reach 17,158 by the 2010-11 school year as outlined below. The State of Texas provides funding for public education via a financing formula which weighs student attendance levels, property value per student, the District’s tax effort and regional variations in payroll and other costs. The District is actually considered a “property-rich” school district because the assessed value of property (“wealth”) in the District per student is higher than the statewide recapture of $319,500. The statewide taxable value per student for 2006-07 was $319,500 while the comparable value for the District was approximately $500,000. Enrollment Projections - Methodology Enrollment projections are provided through a contract with Population and Survey Analysts (“PASA”). PASA integrates school district information with its proprietary new home census information and specific neighborhood forecasts to create specific enrollment projections by attendance zone for the District. The projections are updated annually and PASA presents quarterly reports to the Board of Trustees and administration to explain the findings, provide comments on new and potential housing developments and create an understanding of future residential development's impact on the school district. This allows the District to take a proactive stance with regard to new school locations so that sites can be targeted not only where the need is greatest, but also far enough in advance of actual new home construction to minimize acquisition costs. This methodology provides significantly greater accuracy than the traditional cohort survival method employed in past years by the District. The District is rapidly growing and has large areas of undeveloped land. The quarterly reports help the District keep abreast of the area development as the October 1, 2005, voter approved $224.5 million bond issue is implemented over an estimated three year planning horizon.

13

Demographics

Year

Total

Elementary (EC-5th)

Middle (6th-8th)

High School (9th-12th)

Actual: 2002-03 6,177 2,981 1,507 1,689 2003-04 6,870 3,359 1,663 1,848 2004-05 7,563 3,723 1,831 2,009 2005-06 8,705 4,439 2,015 2,251 2006-07 10,334 5,311 2,367 2,656 Budget: 2007-08 11,818 6,110 2,685 3,023 Projections: 2008-09 13,463 7,111 3,101 3,251 2009-10 15,204 8,067 3,595 3,542 2010-11 17,158 9,144 4,105 3,909 2011-12 19,477 10,396 4,737 4,344

Cash Management. Cash available in excess of cash requirements was invested in the Texas Local Government Investment Pool, and government securities throughout the year. The average yield on investments at June 30, 2007 was 5.291 percent. The District’s investment policy is to minimize risk while maintaining a competitive yield on its portfolio. The District’s deposits were entirely covered by Federal Deposit Insurance Corporation (FDIC) insurance, pledged collateral or corporate surety bond for the fiscal year ended June 30, 2007. Risk Management. The District strives to maintain employee benefit programs designed to enhance the quality of life for employees. To achieve this, the District has created a self-funded insurance program that provides, medical, dental, disability, and hospital indemnity coverage to employees along with other insured programs at competitive rates effective September 1, 2002. Prior years coverage was offered through a Health Management Organization (“HMO”). The District also maintains adequate protection from property and casualty risk exposures through insured coverage and fully funded workers’ compensation coverage with a strict emphasis on cost control of claims. The Risk Management Department routinely reviews all insurance programs of the District to assess risk exposure and the appropriate levels of coverage being maintained. Major Initiatives and Accomplishments The Northwest Independent School District has consistently received a rating of “Superior Achievement” under the State of Texas School FIRST – financial accountability rating system. The Superior Achievement rating is the state’s highest, demonstrating the quality of the District’s financial management and reporting system. Northwest Independent School District’s Schools FIRST rating shows that the District is making the most of the taxpayers’ dollars and that Northwest’s schools are accountable not only for student learning, but also for achieving these results cost-effectively and efficiently. This is the fifth year of School FIRST (Financial Integrity Rating System of Texas), a financial accountability system of Texas school districts developed by the Texas Education Agency in response to Senate Bill 875 of the 76th Texas Legislature in 1999. The primary goal of Schools FIRST is to achieve quality performance in the management of school districts’ financial resources, a goal made more significant due to the complexity of accounting associated with Texas’ school finance system.

14

Competency in basic skills such as reading, writing and mathematics formerly has been measured by performance on the Texas Assessment of Academic Skills ("TAAS"). The TAAS and other standardized achievement tests were used to measure the quality of education provided in the district. The primary assessment instrument was the TAAS test, which provided the basis of the Texas Accountability System. Overall, the District individual campus accountability ratings and District TAAS performance steadily improved. Northwest High School received the National Blue Ribbon Award of Excellence, a highly prestigious award given by the U. S. Department of Education in May, 2002. Samuel Beck Elementary received the 2006 Blue Ribbon Lighthouse School Award. The Texas Assessment of Knowledge and Skills (“TAKS”) measures the statewide curriculum of specific subjects at specific grade levels and is a completely reconceived testing program. In comparison to the previous state assessment the Texas Assessment of Academic Skills or TAAS, the TAKS includes a more broad assessment of the Texas Essential Knowledge and Skills (“TEKS”), which is the statewide curriculum. The TAKS is a more rigorous assessment and questions are asked in a more authentic manner to measure student knowledge of the TEKS. The 2002-2003 school year was the first year for the TAKS to be administered and is considered somewhat of a transition year for accountability purposes. The District’s 2002 accountability ratings were carried forward to the 2003 school year. Campus 2002 ratings were not carried forward to 2003, but school performance data has been reported on the annual Academic Excellence Indicator System (“AEIS”) Report and School Report Card. The 2006-2007 accountability ratings were released and the ratings show gains in all areas of student achievement. It is the District goal for the District and all campuses to endeavor to reach exemplary status.

Texas Accountability System Campus Rating

Transition TAKS TAKS TAKS TAAS

DescriptionActual

2002-03Actual

2003-04Actual

2004-05Actual

2005-06Actual

2006-07Exemplary -- 2 3 1 1 Recognized -- 6 7 11 11 Acceptable -- 4 2 2 2 District Rating Recognized Recognized Recognized Acceptable Acceptable

Texas Assessment of Knowledge and Skills (“TAKS”)

DescriptionActual 2002-03

Actual 2003-04

Actual 2004-05

Actual 2005-06

Actual 2006-07

Reading/English Language Arts 82.0% 91.0% 91.0% 93.0% 95.0% Writing 88.0% 94.0% 94.0% 95.0% 94.0% Social Studies 88.0% 96.0% 94.0% 93.0% 94.0% Mathematics 73.0% 82.0% 80.0% 81.0% 86.0% Science 67.0% 84.0% 83.0% 81.0% 82.0% District Rating Recognized Recognized Recognized Acceptable Acceptable

District Student and Staff Accomplishments. Samuel Beck Elementary was named a 2006 Blue Ribbon Lighthouse School Award winner. Beck’s selection was based on the campus being a successful, comprehensive school exhibiting a strong commitment to educational excellence for all students. Blue Ribbon Lighthouse schools commit to sharing expertise and exemplary practices with other schools on a

15

local, regional and national level, as well as providing mentoring and networking opportunities to schools seeking guidance and assistance in school improvement initiatives. Gene Pike and Medlin Middle Schools were named two of the top schools in the state, according to an article in Texas Monthly. The schools were among the best of 574 public schools for academic performance, participation rates and Adequate Yearly Progress status. Northwest ISD Superintendent Karen G. Rue, Ed.D. was one of only six Texas superintendents invited to attend the BellSouth Superintendent Leadership Network Conference in January 2006 in Atlanta, Georgia. The Northwest High School softball team finished the season ranked 21st in the nation, according to the USA Today/National Fastpitch Coaches Association (NFCA) poll. The team was led by pitcher Brittany Barnhill who received a number of honors, including being named the NFCA All-American Team. More than 40 students from Gene Pike Middle School were part of the Polar First Experience in December when two pilots embarked on a world-record journey around the world via two Polar Regions. Gene Pike Middle School was one of 28 schools in the world participating in this education experience. ARAMARK Chef Jack Aspinall, representing Northwest ISD, was the winner of the International Culinary Showcase held at the Pennsylvania Convention Center in October 2006, Aspinall was one of 26 chefs around the world who were a part of ARAMARK’s 12th Annual International Guest Chef Exchange, the highest honor awarded to the company’s culinarians. Aspinall also spent more than a week in Ireland as part of the guest chef program. The Northwest High School Band welcomed home more than 30 marines from a tour in Iraq. The band played several patriotic songs to welcome the marines who were transported on the plane of Mavericks owner Mark Cuban to the Fort Worth Alliance Airport. Also, the Northwest High School UIL Marching Band advanced to state. Recent Northwest High School graduates, Whitney Norris and Kristy Young received the American FFA Degree at the 79th National FFA Convention in Indianapolis, Indiana on October 28. The American FFA is the highest degree awarded by the National FFA Organization, and recognizes these students’ demonstrated leadership abilities and outstanding achievements in agricultural business, production, processing, and service programs. Awards GFOA Certificate of Achievement. The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to Northwest Independent School District for its comprehensive annual financial report for the ten months ended June 30, 2002 and for fiscal year ended June 30, 2003, June 30, 2004, June 30, 2005 and June 30, 2006. In order to be awarded a Certificate of Achievement, a government must publish an easily readable and efficiently organized comprehensive annual financial report. This report satisfied both generally accepted accounting principles and applicable legal requirements. ASBO Certificate of Excellence. The Association of School Business Officials International (ASBO) awarded a Certificate of Excellence in Financial Reporting to Northwest Independent School District for its comprehensive annual financial report for fiscal year ended June 30, 2003, June 30, 2004, June 30, 2005 and June 30, 2006. This award is for school districts whose comprehensive annual financial reports substantially conform to the recommended principles and standards of financial reporting adopted by that organization. The award is granted only after an intensive review of financial reports by an expert panel of certified public accountants and practicing school business officials.

16

THIS PAGE LEFT BLANK INTENTIONALLY

18

19

20

NORTHWEST INDEPENDENT SCHOOL DISTRICT

Administrative Organizational Chart

Outsourced Operations• Print Shop • Food Service

SUPERINTENDENT OF

SCHOOLS

Executive Assistant to the Superintendent & Records Management

Officer

Chief FinancialOfficer

Ex. Director for Business Services • Accounts Payable • Payroll • Elections

Asst. Superintendent forFacilities, Planning &

Construction

Purchasing

Warehouse Manager• Shipping • Receiving

Director for Maintenance • • Electrical • Mechanical • Plumbing • Custodial • Groundskeeping

Asst. Superintendent for Curriculum & Instruction

Principals • 11 Elementary • 6 Secondary

Ex. Director for Student Services

• Federal/State Programs • Testing Administration • Family Outreach/Parent Partners • DEIC/CIP • Nurses

Ex. Director for Curriculum and Staff Dev. • Curriculum Coordinators (7) • Staff Development • Research/Development

Ex. Director for Instruction and

Campus Support • CATE • Advanced Academics • Textbooks • Instructional Technology • Fine Arts • Counselors

Athletic Director

Sp. Assistant to the Superintendent • Community/Government Relations • Governance/Legal

Director forCommunications

• Media Relations • Public Information • Communications

Webmaster/Graphic Designer Events Coordinator

• Construction Management • Construction Supervisor (2)

Asst. Superintendent forAdministrative Services

Director forHuman Resources

• H.R. Specialist • Substitutes

Director forPersonnel Services

• Benefits • Risk Management

Director forSafety and Security

• Emergency Op. Plans (EOP) (District/Campus) • School Resource Officers

Director forTechnology

• Network Systems • Instruction Infrastructure • Construction Infrastructure • Telephones

Data Management• Pentamation

Coordinators (2) • Pentamation Specialist

Director for Corporate & Community

Development • NEF • Partners in Education • Volunteers • Alumni Relations

Outsourced Operations• Transportation

21

NORTHWEST INDEPENDENT SCHOOL DISTRICT Board of Trustees

Mark Schluter Place 2

Elected in May 2006 Term expires in 2009

Davis Palmer President Place 6

Elected in May 1998 Term expires in 2008

Jeannette Leong Place 4

Elected in May 2001 Term expires in 2007

Lynn Gamron Vice President

Place 5 Elected in May 1999 Term expires in 2008

Stephanie Trietsch Secretary Place 7

Elected in May 2002 Term expires in 2008

Debbie Thomas Place 1

Elected in May 1997 Term expires in 2009

Dr. Daryl Laney Place 3

Elected in May 1998 Term expires in 2007

Karen G. Rue, Ed.D. Superintendent of

Schools

Board Meetings: All Northwest ISD board meetings are open to the public. Regular meetings will be held at 7 p.m. on the second and fourth Monday of each month in the board room located at the NISD Administration Building at 2001 Texan Drive. With public notice, trustees will also hold special meetings and work sessions as needed. Within the limits of the Texas Open Meetings Act, parts of the board meetings may be closed to the public for topics including, but not limited to, these: real estate transactions, personnel matters, student hearings, and legal matters.

If You Wish to Address the Board: The public may address the board during the public participation portion of the board meeting. Remarks may be related to any topic, whether agenda items or non-agenda items, and are usually limited to three minutes. Those wishing to speak during public participation may sign the roster in the room within the hour preceding the meeting.

www.nisdtx.org

22

NORTHWEST INDEPENDENT SCHOOL DISTRICT School Board and Administrators

Board of Trustees Davis Palmer................................................................................................................................................................... President Lynn Gamron..........................................................................................................................................................Vice President Stephanie Trietsch ..........................................................................................................................................................Secretary Jeannette Leong ............................................................................................................................................................... Member Dr. Daryl Laney ............................................................................................................................................................... Member Mark Schluter .................................................................................................................................................................. Member Debbie Thomas................................................................................................................................................................ Member

Administration Karen G. Rue, Ed.D............................................................................................................................. Superintendent of Schools Lowell H. Strike, Ph.D............................................................................ Assistant Superintendent for Curriculum & Instruction Mona Benotti. ............................................................................................Assistant Superintendent for Administrative Services Dennis McCreary.....................................................................Assistant Superintendent for Facilities, Planning & Construction Jon Graswich, CPA...................................................................................................................................Chief Financial Officer Jerhea Nail .......................................................................................................................Special Assistant to the Superintendent

Principals Gene Suttle .............................................................................................................................................. Northwest High School Monty Brown...........................................................................................................................................................Denton Creek Paula Sanders............................................................................................................................... Alternative Education Program Robin Ellis .................................................................................................................................................Medlin Middle School Damon Edwards.................................................................................................................................... Gene Pike Middle School Dr. Philo Waters ........................................................................................................................... Chisholm Trail Middle School Julie Nerby........................................................................................................................................................Haslet Elementary Anita Chaney .................................................................................................................................................... Justin Elementary Vicki Hardy ................................................................................................................................................ Lakeview Elementary Debbie Merki ................................................................................................................................................Roanoke Elementary Mary Dunlevy.......................................................................................................................................... Seven Hills Elementary Deborah McCune...................................................................................................................................Samuel Beck Elementary Cathy Sager.......................................................................................................................................... W.R. Hatfield Elementary Fran Brown .............................................................................................................................................Prairie View Elementary Suzie McNeese ...............................................................................................................................J. Lyndal Hughes Elementary Connie Finley ...................................................................................................................... Sonny & Allegra Nance Elementary It’s Fast, Free, and Designed to Keep You Informed: If you have an email address, NISD is offering an easy and free way to get the latest district information. Subscribe to the electronic mail list and stay informed about district activities and urgent news such as school closings. Join today by completing the NISD News registration form on the District’s homepage at

www.nisdtx.org

23

NORTHWEST INDEPENDENT SCHOOL DISTRICT Consultants and Advisors

ARCHITECTS OFFICIAL DEPOSITORY Corgan Associates, Inc Woodhaven National Bank - Rhome 501 Elm Street, Suite 500 800 Highway 287, Suite A Dallas, Texas 75202 Rhome, Texas 76078 VLK Architects 1161 Corporate Drive, West, Suite 300 TAX COLLECTION COUNSEL Arlington, Texas 76006 Linebarger Goggan Blair & Sampson, LLP 309 W. 7th Street SHW Group, Inc. Fort Worth, Texas 76102-5113 P.O. Box 650155 Dallas, Texas 75265 BOND FISCAL AGENTS ACCOUNTANTS SERIES 1990 Haynes and Associates, P.C. The Bank of New York Trust Company, N.A. 405 North Oak Street Highwoods Center, 3rd Floor Roanoke, Texas 76262 10161 Centurion Parkway Jacksonville, Florida 32256 BOND COUNSEL SERIES 1997, 2001 and 2002 McCall, Parkhurst & Horton, LLP JP Morgan Trust Company, N.A. 717 North Harwood Institutional Trust Services Dallas, Texas 75201 P.O. Box 2320 2001 Bryan Street, Floor 10 Dallas, Texas 75221 FINANCIAL ADVISORS First Southwest Company SERIES 2004 AND 2005 777 Main Street, Suite 1200 Wachovia Bank, N.A. Fort Worth, Texas 76102 Corporate Trust Operations 1525 West W.T. Harris Blvd., 3C3 Charlotte, North Carolina 28262-8522 GENERAL COUNSEL Abernathy, Roeder, Boyd & Joplin U. S. Bank Corporate Trust Services P.O. Box 1210 683 West Fifth Street, Floor 24 1700 Redbud Boulevard, Suite 300 Los Angeles, California 90071 McKinney, Texas 75069 U.S. Bank Corporate Trust Services Henslee, Fowler, Hepworth & Schwartz LLP P. O. Box 86 816 Congress Avenue, Suite 800 Minneapolis, Minnesota 55486 Austin, Texas 78701-2443 SERIES 2006 Buechler & Associates, P.C Regions Bank Corporate Trust 3660 Stoneridge Road, Suite D-101 1717 St. James Place, Suite 500 Austin, Texas 78746 Houston, Texas 77056

24

FINANCIAL SECTION

25

NORTHWEST INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS FOR THE FISCAL YEAR ENDED JUNE 30, 2007

In this section of the Annual Financial and Compliance Report, we, the managers of Northwest Independent School District, discuss and analyze the District’s financial performance for the fiscal year ended June 30, 2007. Please read it in conjunction with our independent auditors’ report on pages 26 and 27, and the District’s Basic Financial Statements which begin on page 35. FINANCIAL HIGHLIGHTS • During the fiscal year, the District had expenses that were $3,245,260 more than the $165,314,207

million generated in tax and other revenues for governmental programs (before special items). These expenditures include $25,794,215 of construction expenses for capital projects, as shown on page 42-43. After considering this $25,794,215 of construction expense the total revenues exceeded total expenses by $22,548,955. The previous year expenses exceeded revenues by $9,761,111.

• Total cost of all of the District’s federal programs increased during the period, with two old programs

deleted in this fiscal year and one new program being added. • The District is defined by Chapter 41 of the Texas Education Code (TEC) as a high wealth district;

therefore, during 2007 the District paid $35,630,381 in contracted instructional services between schools as part of the state wealth equalization requirements.

• The general fund ended the fiscal year with a fund balance of $51,278,806 million. USING THIS ANNUAL REPORT This fiscal year report consists of a series of financial statements. The government-wide financial statements include the Statement of Net Assets and the Statement of Activities (on pages 35 and 37). These provide information about the activities of the District as a whole and present a longer-term view of the District’s property and debt obligations and other financial matters. They reflect the flow of total economic resources in a manner similar to the financial reports of a business enterprise. Fund financial statements (starting on page 38) report the District’s operations in more detail than the government-wide statements by providing information about the District’s most significant funds. For governmental activities, these statements tell how services were financed in the short term as well as what resources remain for future spending. They reflect the flow of current financial resources, and supply the basis for tax levies and the appropriations budget. The Statement of Fiduciary Assets and Liabilities (shown on page 48), provide financial information about activities for which the District acts solely as an agent for the benefit of certain student groups of the district. The notes to the financial statements (starting on page 50) provide narrative explanations or additional data needed for full disclosure in the government-wide statements or the fund financial statements. The combining statements for non-major funds contain even more information about the District’s individual funds. These are not required by TEA. The sections labeled TEA Required Schedules and Federal Awards Section contain data used by monitoring or regulatory agencies for assurance that the District is using funds supplied in compliance with the terms of grants.

28

Reporting the District as a Whole The Statement of Net Assets and the Statement of Activities The analysis of the District’s overall financial condition and operations begins of page 35. Its primary purpose is to show whether the District is better off or worse off as a result of the fiscal year period’s activities. The Statement of Net Assets includes all the District’s assets and liabilities at the end of the fiscal year while the Statement of Activities includes all the revenues and expenses generated by the District’s operations during the fiscal year. These apply the accrual basis of accounting, which is the basis used by private sector companies. All of the current year’s revenues and expenses are taken into account regardless of when cash is received or paid. The District’s revenues are divided into those provided by outside parties who share the costs of some programs, such as tuition received from students from outside the district and grants provided by the U.S. Department of Education to assist children with disabilities from disadvantaged backgrounds (program revenues), and revenues provided by the taxpayers or by TEA in equalization funding processes (general revenues). All the District’s assets are reported whether they serve the current year or future years. Liabilities are considered regardless of whether they must be paid in the current or future years. These two statements report the District’s net assets and changes in them. The District’s net assets (the difference between assets and liabilities) provide one measure of the District’s financial health, or financial position. Over time, increases or decreases in the District’s net assets are one indicator of whether its financial health is improving or deteriorating. To fully assess the overall health of the District, however, you should consider nonfinancial factors as well, such as changes in the District’s average daily attendance or its property tax base and the condition of the District’s facilities. In the Statement of Net Assets and the Statement of Activities, we reflect the District in one kind of activity: • Governmental Activities - All of the District’s basic services are reported here, including the

instruction, counseling, co-curricular activities, child nutrition, transportation, maintenance, community services, and general administration. Property taxes, tuition, fees and state and federal grants finance most of these activities.

• Proprietary Funds - The District’s Internal Service Funds which include Print Shop, Facilities

Rental/Usage and Self-Insurance are reported within this fund. Reporting the District’s Most Significant Funds Fund Financial Statements The fund financial statements begin on page 38 and provide detailed information about the most significant funds - not the District as a whole. Laws and contracts require the District to establish some funds, such as grants received under the No Child Left Behind Act from the U.S. Department of Education. The District’s administration establishes many other funds to help it control and manage money for particular purposes (like campus activities). The District’s governmental fund uses the following accounting approach.

• Governmental Funds - Most of the District’s basic services are reported in governmental funds. These use modified accrual accounting (a method that measures the receipt and disbursement of cash and all other financial assets that can be readily converted to cash) and report balances that are available for future spending. The governmental fund statements provide a detailed short-term view of the District’s general operations and the basic services it provides. We describe the differences between governmental activities (reported in the Statement of Net Assets and the Statement of Activities) and governmental funds in reconciliation schedule following each of the fund financial statements.

29

The District as Fiduciary Reporting the District’s Fiduciary Responsibilities The District is the fiduciary for money raised by student activities. All of the District’s fiduciary activities are reported in a separate Statement of Fiduciary Assets and Liabilities on page 48 and the Statement of Changes in Fiduciary Fund Net Assets on page 49. These resources are excluded from the District’s other financial statements because the District cannot use these assets to finance its operations. The District is only responsible for ensuring that the assets reported in these funds are used for their intended purposes. GOVERNMENT-WIDE FINANCIAL ANALYSIS We will present both current and prior year data and discuss significant changes in the accounts. The analysis focuses on the net assets (Table I) and changes in net assets (Table II) of the District’s governmental activities. Net assets of the District’s governmental activities are $63,427,163. Unrestricted net assets-the part of net assets that can be used to finance day-to-day operations without constraints established by debt covenants, enabling legislation, or other legal requirements was $(138,834,103) at June 30, 2007. The District’s net assets increased in the amount of $17,069,350. This increase in governmental net assets was the result of the following factors, general revenues increased approximately $30,000,000, with operating grants also increasing approximately $5,000,000, total expenses increased by $17,328,182. Although expenses did increase, the increase in revenues far exceeded the expense increase. The District expended $25,794,215 on construction of capital projects.

Table I Northwest Independent School District

NET ASSETS In thousands

Governmental Activities

2007

Governmental Activities

2006 Current and other assets $261,325 $158,922Capital assets 245,934 237,615 Total Assets 507,259 396,537 Other liabilities

443,832 28,142

Total Liabilities 443,832 350,179 Net assets:

Invested in capital assets net of related debt 29,232 (86,171)Restricted 173,029 90,266Unrestricted (138,834) 42,263 Total Net Assets $63,427 $46,358

30

Table II

Northwest Independent School District CHANGES IN NET ASSETS

In thousands

Governmental Activities

2007

Governmental Activities

2006 Revenues:

Program Revenues: Charges for Services $5,311 $ 4,475 Operating grants and contributions 11,654 6,797 General Revenues: Maintenance and operations taxes 109,214 93,845 Debt service taxes 28,391 20,016 Grants and contributions not restricted To specific functions 12,400 3,704 Investment Earnings 9,868 4,011 Miscellaneous - 7,654 Total Revenue 176,838 140,502 Expenses:

Instruction, Curriculum and media services

52,263 44,775

Instruction and school leadership 3,979 3,653 Student support services 7,083 6,533 Child nutrition 3,995 3,378 Co curricular activities 3,740 3,452 General administration 8,660 7,654 Plant maintenance, security & data 23,784 18,191 Processing Community services 239 197 Debt services 19,194 17,555 Facilities acquisition and Construction Other business-type activities

0

36,832

0

37,053 Total Expenses 159,769 142,441

Increase (decrease) in net assets before transfers and special items

17,069 (1,939)

Special Items -Net Assets at 6/30/06 46,358 48,297Net Assets at 6/30/07 $63,427 $46,358 The District’s total revenues increased by 25.86 percent ($36.3 million). The total cost of many programs and services was substantially higher than last year, with total expenses increasing by $17.328 million. The change in net assets for the current fiscal year was $17,069,350. Also, general fund balance increased in the current fiscal year by $14.447 million with an ending balance of $51,278,806 million. The District took actions this year to compensate for some increases in cost and avoid the loss of state revenue due to changes in the provisions related to accelerated, intensive, compensatory education (State Comp Ed) and student attendance accounting (Leavers).

31

The cost of all governmental activities this year was $159.7 million compared to $142.4 million last year. However, as shown in the Statement of Activities on pages 37, the amount that the taxpayers ultimately financed for these activities through District taxes was only $137.606 million because some of the costs were paid by those who directly benefited from the programs ($16.96 million). THE DISTRICT’S FUNDS As the District completed the year, its governmental funds (as presented in the balance sheet on pages 38-39) reported a combined fund balance of $223.9 million, which is greater than last year’s total of $126.7 million. Over the course of the fiscal year, the Board of Trustees revised the District’s budget several times. These budget amendments fall into three categories. The first category includes amendments and supplemental appropriations that were approved shortly after the beginning of the year and reflect the actual beginning balances (versus the amounts we estimated in June 2006). The second category includes changes that the Board made during the third quarter to take into account the mid-year hiring and overtime freeze and some of the District’s staff restructuring efforts. The principal amendment in this case was to eliminate the original budget contingency appropriation used in the past to cover employee overtime and charges associated with staff turnover. The third category involved amendments moving funds from programs that did not need all the resources originally appropriated to them to programs with resource needs. The District’s General Fund balance of $51.3 million reported on page 38 differs from the General Fund’s budgetary fund balance of $43.6 million reported in the budgetary comparison schedule on page 65. This is principally due to cost savings and added revenues described above. Capital Assets At the end of 2007, the District had $281.8 million invested in a broad range of capital assets, including facilities and equipment for instruction, transportation, athletics, administration, and maintenance. This amount represents a net addition of just over $12.8 million, or 4.76 percent, above last year. This year’s major additions included:

Land $ 1,304,629 Building Improvements 15,179,862 Construction in Progress (4,220,069) Furniture and Equipment 542,950

Total $12,807,372

More detailed information about the District’s capital assets is presented in Note II C – Capital Assets to the financial statements. Debt At June 30, 2007, the District had over $404 million in bonds outstanding. In addition, the District has $8.9 million in accreted interest related to the bonds outstanding. In May 2007, the Board of Trustees authorized issuing $95.02 million in School Building Bonds. The District had two bond refundings during the fiscal year in the amount of $107,659,954. This provided financing for the construction of new school facilities within the District. More detailed information about the District’s long-term liabilities is presented in Note II E – Long-term debt. Other obligations include accrued vacation pay and sick leave. More detailed information about the District’s long-term liabilities is presented in Note I D4 – Compensated Absences to the financial statements.

32

ECONOMIC FACTORS AND NEXT YEAR’S BUDGETS AND RATES The District’s elected officials considered many factors when setting the fiscal year 2008 budget and tax rates. One of those factors is the economy. The District’s population growth during 2000-2007 averaged annual gains of 13.18 percent. Unemployment has lowered slightly and now stands at 4.23 percent. This compares with the State’s unemployment rate of 4.93 percent and the national rate of 4.7 percent. These indicators were taken into account when adopting the General Fund budget for 2008. Amounts available for appropriation in the General Fund budget are $115,545,186, an increase of 0.35 percent over the final 2007 budget of $115.1 million. The District will use its revenues to finance programs currently offered. Budgeted expenditures are expected to rise nearly 4.95 percent to $115.5 million from $110.06 million in 2008. Increased Chapter 41 and Tax Increment Fund expenditures cause virtually all of the increase. The District has added no major new programs or initiatives to the 2008 budget. If these estimates are realized, the District’s budgetary General Fund balance is expected to stay the same at the close of 2008. CONTACTING THE DISTRICT’S FINANCIAL MANAGEMENT This financial report is designed to provide the citizens, taxpayers, customers, investors and creditors with a general overview of the District’s finances and to show the District’s accountability for the money it receives. If you have questions about this report or need additional financial information, contact the District’s Business Office, at Northwest Independent School District, P.O. Box 77070, Fort Worth, TX, 76177-0070.

33

THIS PAGE LEFT BLANK INTENTIONALLY

34

THIS PAGE LEFT BLANK INTENTIONALLY

36

THIS PAGE LEFT BLANK INTENTIONALLY

40

NORTHWEST INDEPENDENT SCHOOL DISTRICT NOTES TO THE FINANCIAL STATEMENTS

JUNE 30, 2007

I. Summary of significant accounting policies The Northwest Independent School District (District) is a public educational agency operating under the applicable laws and regulations of the State of Texas. It is governed by a seven member Board of Trustees that are elected by registered voters of the District. The District prepares its basic financial statements in conformity with Generally Accepted Accounting Principles (GAAP) promulgated by the Governmental Accounting Standards Board (GASB) and other authoritative sources identified in Statement of Auditing Standards No. 69 of the American Institute of Certified Public Accountants. Additionally, the District complies with the requirements of the appropriate version of the Texas Education Agency (TEA) Financial Accountability System Resource Guide (FASRG) and the requirements of contracts and grants of agencies from which it receives funds. In 2002, the District implemented GASB Statement No. 34, Basic Financial Statements-and Management’s Discussion and Analysis-for State and Local Governments (GASB Statement No. 34), GASB Statement No. 37, Basic Financial Statements-and Management’s Discussion and Analysis-for State and Local Governments: Omnibus which provides additional guidance for the implementation of GASB Statement No. 34, and GASB Statement No. 38, Certain Financial Statement Note Disclosures which changes note disclosure requirements for governmental entities. GASB Statement No. 34 established a new financial reporting model for state and local governments that included the addition of management’s discussion and analysis, government-wide financial statements, required supplementary information and the elimination of the effects of internal service activities and the use of account groups to the already required fund financial statements and notes. The GASB determined that fund accounting has and will continue to be essential in helping governments to achieve fiscal accountability and should, therefore, be retained. The GASB also determined that government-wide financial statements are needed to allow user’s of financial reports to assess a government’s operational accountability. The new GASB model integrates fund-based financial reporting and government-wide financial reporting as complementary components of a single comprehensive financial reporting model. A. Reporting entity The Board of the District is elected by the public; has the authority to make decisions, appoint administrators and managers; significantly influence operations; and has the primary accountability for fiscal matters. Therefore, the District is a financial reporting entity as defined by the Governmental Accounting Standards Board (GASB) in its Statement No. 14, “The Financial Reporting Entity.” Based upon our review under the GASB Statement No. 39, there are no component units included within the reporting entity. The criteria used included whether the component unit was a legally separate tax entity from the District and there were no significant revenues that were material to the District. B. Government-wide and fund financial statements The government-wide financial statements (i.e., the statement of net assets and the statement of changes in net assets) report information on all of the nonfiduciary activities of the primary government. Interfund services provided and used are not eliminated in the process of consolidation. The governmental activities are supported by tax revenues and intergovernmental revenues.

50

The statement of activities demonstrates the degree to which the direct expenses of a given function are offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function. Program revenues include 1) charges to customers or applicants who purchase, use or directly benefit from goods, services, or privileges provided by a given function and 2) grants and contributions that are restricted to meeting operational or capital requirements of a particular function. Taxes and other items not properly included among program revenues are reported instead as general revenues. Separate financial statements are provided for governmental funds and fiduciary funds, even though the latter are excluded from the government-wide financial statements. Major individual governmental funds are reported as separate columns in the fund financial statements. C. Measurement focus, basis of accounting, and financial statement presentation The government-wide financial statements are reported using the economic resources measurement focus and the accrual basis of accounting, the agency funds have no measurement focus. Revenues are recorded, when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Property taxes are recognized as revenues in the year for which they are levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by the provider have been met. Governmental fund financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose, the government considers revenues to be available if they are collected within 60 days of the end of the current fiscal period. Expenditures generally are recorded when a liability is incurred, as under accrual accounting. However, debt service expenditures, as well as expenditures related to compensated absences and claims and judgments, are recorded only when payment is due. Revenues from local sources consist primarily of property taxes. Property tax revenues and revenues received from the State of Texas are recognized under the susceptible-to-accrual concept. Miscellaneous revenues are recorded as revenue when received in cash because they are generally not measurable until actually received. Investment earnings are recorded as earned, since they are both measurable and available. Grant funds are considered earned to the extent of the expenditures made under the provisions of the grant. Accordingly, when such funds are received, they are recorded as deferred revenues until the related and authorized expenditures have been made. If balances have not been expended by the end of the project period, grantors sometimes require the District to refund all or part of the unused amount. The District reports the following major governmental funds:

The general fund is the government’s primary operating fund. It accounts for all financial resources of the District, except those required to be accounted for in another fund. Major revenue sources include local property taxes, state funding under the Available School Fund and interest earnings. Expenditures include all costs associated with the daily operations of the District except for specific programs funded by the federal or state government, child nutrition, debt service, and capital projects. This is a budgeted fund. The debt service fund accounts for the resources accumulated and payments made for principal and interest on long-term general obligation debt of governmental funds. This is a budgeted fund.

51

The capital projects fund accounts for proceeds from long-term debt financing (including the sale of bonds) and revenues and expenditures related to authorized construction and other capital asset acquisitions.

The District reports the following non-major governmental fund:

The special revenue funds account for resources restricted to, or designated for, specific purposes by a grantor. Federal and state financial assistance generally is accounted for in a special revenue fund. Child Nutrition Program adopts an annual budget.

The District reports the following proprietary funds:

The internal service funds account for revenues and expenses related to services provided to organizations inside the District on a cost reimbursement basis. The District’s Internal Service Funds are Self Insurance, Facility Rental/Usage and Print Shop.

Additionally, the District reports the following fiduciary funds:

The agency fund accounts for resources held in a custodial capacity by the District, and consists of funds that are the property of students or others. The District’s Agency Funds are the Student Activity Account and the High School Student Activity Account. The private-purpose trust fund accounts for resources held and administered by the District, acting in a fiduciary capacity for private organizations, or governments.

Legal requirements for school district budgets are formulated by the state, TEA, and the local district. The Board adopts an “appropriated budget” on a basis consistent with GAAP for the general fund, debt service fund and child nutrition program (which is included in special revenue funds). At a minimum, the District is required to present the original and the final amended budgets for revenues and expenditures compared to actual revenues and expenditures for these three funds.

The following procedures are followed in establishing the budgetary data reflected in the general purpose financial statements: • Prior to June 19th, the District prepares a budget based on the planning-programming

budgeting method for the next succeeding fiscal year. The operating budget includes proposed expenditures and the means of financing them.

• After one or more budget workshops with the Board, a meeting is called for the purpose of

adopting the proposed budget. At least ten days but not more than 30 days public notice of the meeting is required.

• Prior to June 30th the Board of Trustees legally adopts the budget for the general fund, debt

service fund and child nutrition program.

• After the budget for the above listed funds is approved, any amendment that causes an increase or decrease in a fund or functional spending category or total revenue or other resources object category requires Board approval prior to the fact. These amendments are presented to the Board at its regular monthly meeting and are reflected in the official minutes. Because the District has a policy of careful budgetary control, several budgetary amendments were necessary throughout the year. Budget amendments throughout the year were not significant.

• Expenditure budgets are controlled at the expenditure functional and object level by the

appropriate budget manager (principal, department director or divisional administrator).

52