north sea decommissioning market forecast 2016-2040 leaflet and contents

TRANSCRIPT

North Sea Decommissioning Market Forecast 2016-2040energy business insight

e: [email protected] t: +44 (0)203 4799 505

www.douglas-westwood.com

Aberdeen | Faversham | Houston | London | Singapore

© 2016 Douglas-Westwood

29

North Sea Decommissioning Market Forecast 2016-2040

By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Chapter 3 : Overview of Decommissioning Process

Decommissioning – SLVs

There have been several conceptual

SLVs but only one, the Pioneering

Spirit, by Allseas has actually been

constructed.

Its first job will be the removal of the

Yme MOPU offshore Norway. It will also be removing the topsides

of the Brent platforms, which all weigh

>20,000 tonnes.Allseas is already planning to construct

another SLV with a topside lift capacity

of 72,000 tonnes. SLVs can offer significant time and cost

savings to operators. Success will depend on operator will-

ingness and competitive day rates.

Impact of Single Lift Vessels

Several SLVs have been conceptualised in

recent years, including the Pioneering Spirit

(previously ‘Pieter Shelte’) and Twin Marine

Lifter System. However, Allseas are the only

company who have firm plans to enter a

vessel into the market with the Pioneering

Spirit which already has two decommission-

ing contracts and is due to start work in

2016. Allseas are decidedly confident and

already have plans for an SLV larger than

the Pioneering Spirit, following its comple-

tion, currently named Amazing Grace.

SLVs will have a significant impact on

decommissioning times, with a correspond-

ing reduction in costs. The Pioneering Spirit

will be able to remove some of the heaviest

topsides in the world in one lift – something

that would take HLVs significantly longer at

considerably higher costs, due to the need

to use reverse installation methods. Preparation times for SLVs prior to lifts will

also be about a fifth of those required for

conventional heavy lift crane vessels.

The success of SLVs rests heavily on the Pio-

neering Spirit’s performance. If it completes

operations quickly, with no incidents and

has a day rate that appeals to operators, it

is likely a number of other companies will

build rival vessels.Should the Pioneering Spirit be a success, it

and the vessels that follow will at least ease

the demand load across the installation,

pipe laying and decommissioning sectors,

creating vessel availability and easing bot-

tlenecks.

Other concepts for SLVs have been touted, including

the Twin Marine Lifter System that would have been

the first to market had it been ordered and delivered

as expected. This has not been the case and

construction has still not begun. In 2014 the concept

was sold to Shandong Twin Marine and though a

contract to build the vessel was expected to be an-

nounced in 2015, nothing has been forthcoming. Another SLV, ‘Borealis’, was due to be delivered in

2012, however Subsea 7 bought the order in 2009

and re-designed the vessel as a pipelay and heavy

lift vessel.

Table 11: SLVs Under Construction

Vessel

Pioneering Spirit(ex. Pieter Shelte)

Amazing Grace

Twin Marine Lifter

Construction

Daewoo Shipyard

TBD – In design phase

China Petroleum Liaohe Equipment Company

Owner

Allseas

Allseas

Shandong Twin Marine

(JV between Twin Marine Heavy-Lift and Shandong Shipping Corp)

Order Date

2007

-

-

Delivery Year

2016

Expected 2021

-

Max. Lift Capacity (Topsides)

48,000 tonnes

Planned 72,000 tonnes

34,000 tonnes

Max. Lift Capacity (Jacket)

25,000 tonnes

Unknown

16,000 tonnes

Max. Speed

14 knots

Unknown

Unknown

Draft

10-25m

Unknown

Design draft 8.5 m, Submerged draft 22.75 m

Estimated Cost

3bn

> 3bn

Unknown

Notes

Allseas announced in May 2015 that Pioneering Spirit

should be ready to start its first platform removal in the

North Sea later in the year.Following the delivery of Pioneering Spirit, Allseas has

announced the construction of an even larger ship

(160m wide), which is intended for the installation and

removal of the largest vessels.As part of the unique commercial offering an insurance

package is being developed which will allow fixed-price

platform removal.

• Prospects• Technologies• Markets

© 2016 Douglas-Westwood

34

North Sea Decommissioning Market Forecast 2016-2040

By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Chapter 4 : Supply Chain

Platform Decommissioning – Infrastructure Removal & Disposal

BP

ConocoPhillips

Shell

BG

Perenco

Operators

Amec Foster Wheeler

Aker Solutions

BIS Salamais

EPC / Project Management

ABLE

Kvaerner

Peterson UK & Veolia

AF Decom Offshore

Shipyards/Ports

Veolia

Bureau Veritas

Cape

MMO ProvidersBibby Offshore

Technip

Subsea 7

Support Vessel Contractors

Operators

The Operator of the platform to be removed

may award a contract for the whole decom-

missioning process to a duty holder who will

be responsible for the engineering and project

management of the complete decommission-

ing phase including infrastructure removal.

MMO providers

Operators must ensure the structural integrity

of their infrastructure before it is re

moved.

These services will often be sub-contracted by

the duty holder/project manager or directly by

the Operator.

Heavy lift vessel contractors

HLVs used for the removal of platforms will

usually be contracted directly by the Operator

or platform duty holder.

For reverse installation or piece small decom-

missioning methods, support vessels will

often be required to transport the removed

modules back to shore for disposal. Most HLV

contractors will have the required support

vessels and barges in their fleet.

Waste management & shipyards

The platform Operator or duty holder will

usually be responsible for awarding waste

management contracts to a waste man-

agement service provider, who will then

contract the shipyard or port to be used. The

Operator may directly contract th

e yard/port

themselves.

Shipyards will often work in partnership with

specialist decommissioning disposal and waste

management companies to establish facilities

at their yard. For example, in June 2015 JV

partners Peterson and Veolia invested in a de-

commissioning facility in Great Yarm

outh port.

The supply chain within the UK can be

considered somewhat constrained due to the

shipyard and onshore infrastructure limita-

tions. It is likely that UKCS suppliers may be

overlooked for UKCS disposal contracts due

to the capabilities of Norwegian and Dutch

yards.

Supply chain integration

In recent years there has been a call for the

supply chain to become more integrated with

the packaging of services across the supply

chain to ease the supply chain, share experi-

ence and expertise as well as managing the

risk involved.

In particular there is a call for waste manage-

ment service providers to be involved in the

decommissioning process from an earlier

stage.

HLV

Heerema

SAL

McDermott

SLV

Allseas

Shangdong Twin

Marine

Heavy Lift Vessel Contractors

Veolia

Sureclean

Waste Management

© 2016 Douglas-Westwood

41

North Sea Decommissioning Market Forecast 2016-2040

By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Chapter 5 : Market ForecastDenmark : Total Expenditure

Figure 24: Denmark – Total Cost Scenario 1

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

Expe

nditu

re (

$bn)

FPS Removal

Heavy Transport

Onshore DeconstructionPSV

Substructure RemovalTopside Removal

Well Decommissioning

Figure 25: Denmark – Total Cost Scenario 2

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

Expe

nditu

re (

$bn)

FPS Removal

Heavy Transport

Substructure RemovalOnshore Deconstruction

PSV+DSV

Topside Removal

Well Decommissioning

Denmark summaryThough smaller than both Norway and the

UK, Denmark has a number of fixed platforms

which will reach the end of their commercial

life in the next few years. Decommissioning will take place in two main

periods which are built around the abandon-

ment dates for the major hubs in the country.

Four are due to be abandoned in the forecast

period – significantly less than Norway and

the UK.

We expect the Dan and Halfdan hubs, as well

as their tieback fields, to all be abandoned in

the later years of this decade, with decommis-

sioning work running until 2023.

The Siri and Gorm hubs are the other two

that we expect to be decommissioned, with

abandonment for both expected in 2035. Gorm has a large number of platforms with

two small, six medium, one large and two

extra large platforms expected to be removed

by the end of the forecast period. The Siri hub consists of three medium and

one extra large platform. It also has three

subsea wells – % of all subsea well removals

2016-2040 in Denmark.Unlike the other two countries mentioned,

Denmark has no floating platforms, with the

vast majority of production coming from fixed

wellhead platforms.

Well decommissioning will represent only

% of the total spend in S1 and % in

S2 – far less than in other countries. This is

due to the lack of subsea wells, which cost

significantly more to P&A and remove than

surface wells.

Scenario 1Total spend in S1 for Denmark will be $ bn

over 2016-2040, % more than in S2. This

is a higher difference than both Norway and

the UK due to a higher percentage of spend

in the region being focused on platform

removals.

The entire platform removal and onshore

deconstruction process will cost $ bn, %

of total country spend, essentially a reverse of

Norway and the UK. Topside and substruc-

ture removal will lead spend, representing

% and % of the total forecast expendi-

ture respectively. Scenario 2 Total expenditure in S2 will be almost $ bn,

with onshore deconstruction accounting for

the highest proportion of spend outside of

well decommissioning ( % of the total). There is a relatively even split of spend in S2

with heavy transport accounting for % fol-

lowed by substructure removal with % and

topside removal with %. The relatively small

percentage taken up by platform removal

demonstrates the cost saving that can be

made with SLVs.

Danish decommissioning activity will

peak in two distinct periods.Virtually all Danish production comes

from fixed platforms – FPS remov-

als.

These tie into hubs, of which are

coming to the end of their commercial

life.

Dan and Halfdan hubs first to be

removed 2019-2023. Only subsea well removals – well

decommissioning will account for a

smaller proportion of spend than in

Norway and the UK.

2016-2040S1 Total Spend $ bn S2 Total Spend $ bn

© 2016 Douglas-Westwood

45

North Sea Decommissioning Market Forecast 2016-2040

By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Chapter 5 : Market Forecast

Well removals

The number of well removals in Norway

will grow significantly over the forecast

period, with the last ten years accounting

for % of all removals.

This trend applies to both surface and

subsea wells, with the majority of fixed and

floating production units expected to come

to the end of their life at the end of the

forecast period.

With a cost of nearly $ bn and a total of

subsea wells to be removed, the im-

portance of subsea decommissioning work

is clear. This should be a major focus for the

small number of companies capable of ex-

ploiting this area of the market, particularly

as the number of wells in the UK will begin

to decline in the 2030s.

Surface wells will account for a high propor-

tion of removals at %, but this will not be

mirrored in the cost. They will only repre-

sent % of total well cost, demonstrating

the higher costs associated with subsea well

work, particularly in harsh conditions.

Despite this there are surface wells to

be removed 2016-2040, with a cost of al-

most $bn. This highlights that there is still

a large market for those companies who

specialise in the plugging and abandonment

of surface wells.

Key subsea developments that we believe

will be decommissioned over the forecast

period include tiebacks to the Norne FPSO

( wells), Alvheim FPSO ( wells) and the

Heidrun TLP ( wells).

Platform removals

The number of removals will grow almost

exponentially over the forecast period, with

a limited amount of activity in the early part

of the forecast before it ramps up later. This

is a result of the abundant reserves that a

number of the major hubs in Norway still

possess, meaning they can keep producing

economically for many years.

The dominance of large and extra large

platforms can be seen throughout the

forecast period and platforms under 1,000

tonnes will account for only % of remov-

als (platforms). None of these will

be removed until 2038 as they are part of

major hubs which are expected to produce

into the 2030s.

In comparison there are platforms that

weigh more than 5,000 tonnes, accounting

for % of the total number of platforms

to be removed. This underlines the amount

of time and cost that will be required using

HLVs and the reverse installation method.

The Yme MOPU will be the first job for the

SLV Pioneering Sprit. The platform has never

produced due to cracks in the grouting of

the platform’s legs, which was discovered

after installation. The platform will be trans-

ported straight to shore for deconstruction

after attempts to reuse it were found to be

impractical. The removal will be completed

with a single lift of the MOPU which weighs

15,000 tonnes.

Norway : Platform & Well Removals

Figure 30: Norway – Number of Platforms Removed by Size

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

Plat

form

s Rem

oved

Extra Small (Wellhead/Flare)

Small

Medium

Large

Extra Large

Figure 31: Norway – Number of Wells Removed by Surface/Subsea

0

100

200

300

400

500

600

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

Wel

ls Rem

oved

Subsea

Surface

84% of well remova ill take place

2031-2040.

Norway is dominated by heavy plat-

forms with % of platforms weighing

over 5,000 tonnes.

The Yme MOPU (15,000 tonnes) will

be the first single lift job for the Pio-

neering Spirit, scheduled for mid-2016.

Major opportunity for well removal

companies, particularly from 2031

onwards.

2016-2040

Platform Tonnage Removed m

Platforms Removed

Wells Removed

Subsea %

Surface %

© 2016 Douglas-Westwood

37

North Sea Decommissioning Market Forecast 2016-2040

By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Chapter 5 : Market ForecastMethodology

Models

Model Outputs

Assumptions (within Models)

Outputs

Data

Hub

Dat

a, C

olla

tes

Fiel

d D

ata

His

tori

cal F

ield

Pro

duct

ion

Dat

a fr

om

Gove

rnm

ent

Org

anis

atio

ns

DW

Offs

hore

Oil

& G

as D

atab

ase

DW’s North Sea Decommissioning Market Forecast is produced using a combination of

in-house databases (and external sources for verification purposes) which track projects

on an individual basis. Our in-house model forecasts weight and spend using this data and

estimated costs of decommissioning work.

Scenario 1 Cost$ Millions

Day ratesCost

Number of Platform Removals

Scenario 2 Cost$ Millions

Day ratesCost

Number of Platform Removals

Well Removal

Well Decommissioning Model Days

Tonnage Removed

Platform Decommissioning - SLV TonnageNumber of lifts

Abandonment & Decommissioning

Dates for Each Hub

Hub O&M Costs

Offshore O&M ModelField O&M Costs

Field Data:FPS UnitsPlatformsTrees

Tonnage Removed

Platform Decommissioning - HLV TonnageNumber of lifts

Forecast Field Production

D&P Model

Forecast Oil and Gas Price Hub Revenue

Forecast Hub Production

FPS ModelDays

FPS Removal

© 2016 Douglas-Westwood 21North Sea Decommissioning Market Forecast 2016-2040By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Chapter 3 : Overview of Decommissioning Process

Decommissioning Planning Phase

The decision to cease production

occurs as recoverable reserves are

exhausted and incremental recovery

costs prove financially less attractive.

Oil price, petroleum tax and O&M

costs all affect a field’s CoP date.

Sustained low oil prices will lead to

CoP for fields that are near or past

optimal lift.

Cessation of ProductionThe decision on whether and when to

proceed with Cessation of Production

(CoP) programmes will occur as recoverable

reserves are exhausted and the incremental

recovery costs prove financially less attractive.

Oil price is one of the key sensitivities, along

with petroleum tax and O&M costs, which

have traditionally been seen as having an

impact on the timing of CoP, the abandon-

ment of the field and the subsequent begin-

ning of expenditure on decommissioning.

Three financial models have traditionally

been used to identify the optimum point in

time to cease production:

Negative net profit (NNP) is the point

where operating costs exceed revenue

from production.

A minimum margin on ongoing expendi-

ture requires an additional margin on ex-

penditure to cover allocation of operating

overheads, but like NNP this model fails

to take account of future field cash flows.

Maximising remaining Net Present Value

(NPV) incorporates into the calculation

all future cash flows, including decommis-

sioning liabilities and available tax relief

over time.

A key output from the financial analysis is to

identify the critical point that will trigger the

commencement of preparing for decommis-

sioning.

This will ordinarily be the point at which the

remaining NPV equates to approximately

150% of the estimated decommissioning

cost. At this point security provisions will be

triggered and the decommissioning project

team mobilised. In practice this is often

ignored; operators have a strong history of

ignoring the decommissioning costs which

are often deferred as long as possible, even

after the field has been abandoned.

There is a strong correlation between oil

price and abandonment, with a higher oil

price enabling field operators to deploy

enhanced oil recovery techniques. This was

seen in recent years as the stable high oil

price (around $110 a barrel) that lasted

from 2011 to mid-2014 caused numerous

fields to be extended beyond their design

life.

Nevertheless, sustained low oil prices are

likely to impact CoP for fields which are

near or past their optimal life. Numerous

small fields in the UK have had life exten-

sion work which requires a high oil price to

be economic, without it, CoP will undoubt-

edly occur soon.

Two fields have already suffered this fate

with FPS development Athena, which

only began production in 2012, as well as

the well-established Dunlin field that first

entered production in the 1970s, both

reaching their CoP point recently due to

the oil price downturn.

“If they had realistic decommissioning costs built into their balance sheet they probably should have started decommis-sioning some years ago.”

Decommissioning Company

“But the biggest issue that these guys have is the yearly expenditure to keep the platform operable. Just keeping the lights on, on some of these platforms is 20-30 million a year, so again it comes down to having a good economist on your team, who can look at the scenarios of oil price v decommissioning costs v Opex costs.”

Decommissioning Company

Figure 15: Model cash flow for a development drilling project

-200

-150

-100

-50

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17Cas

h Fl

ow (

$m)

Years from Project Start

Annual Cash FlowCumulative Cash Flow

Suffering risk

Maximum exposure

Loss Profit

Net present value

Payback

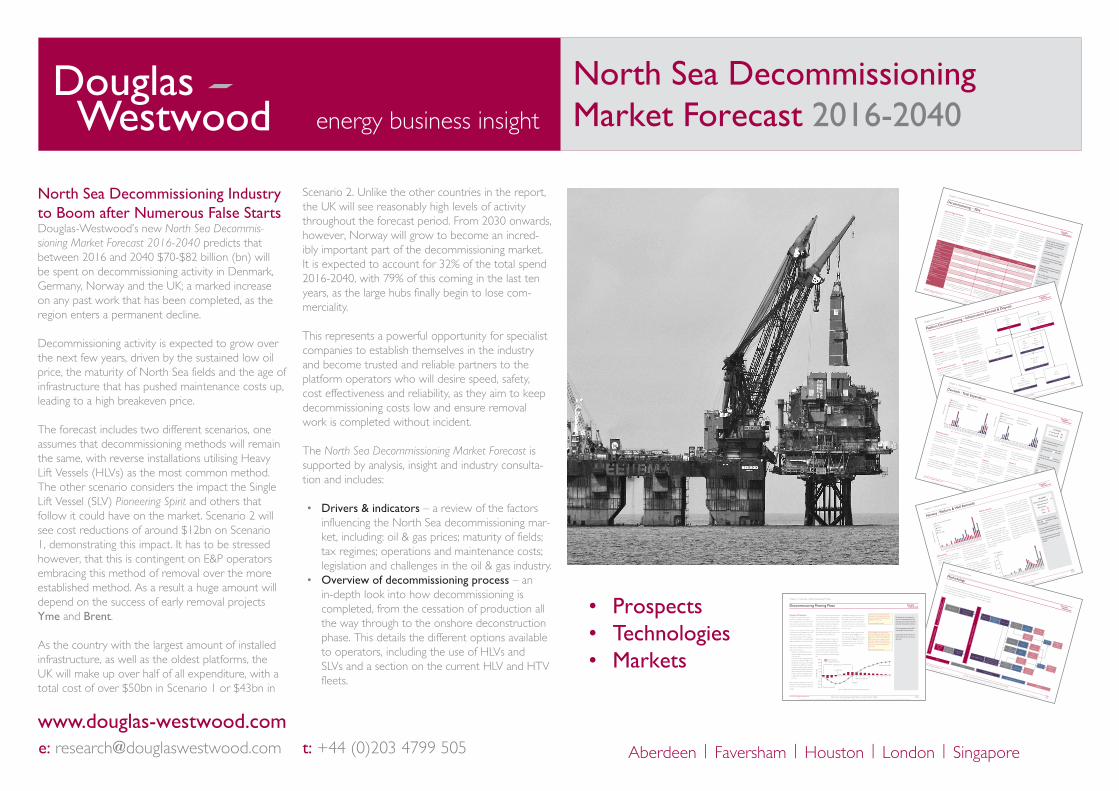

North Sea Decommissioning Industry to Boom after Numerous False StartsDouglas-Westwood’s new North Sea Decommis-sioning Market Forecast 2016-2040 predicts that between 2016 and 2040 $70-$82 billion (bn) will be spent on decommissioning activity in Denmark, Germany, Norway and the UK; a marked increase on any past work that has been completed, as the region enters a permanent decline.

Decommissioning activity is expected to grow over the next few years, driven by the sustained low oil price, the maturity of North Sea fields and the age of infrastructure that has pushed maintenance costs up, leading to a high breakeven price.

The forecast includes two different scenarios, one assumes that decommissioning methods will remain the same, with reverse installations utilising Heavy Lift Vessels (HLVs) as the most common method. The other scenario considers the impact the Single Lift Vessel (SLV) Pioneering Spirit and others that follow it could have on the market. Scenario 2 will see cost reductions of around $12bn on Scenario 1, demonstrating this impact. It has to be stressed however, that this is contingent on E&P operators embracing this method of removal over the more established method. As a result a huge amount will depend on the success of early removal projects Yme and Brent.

As the country with the largest amount of installed infrastructure, as well as the oldest platforms, the UK will make up over half of all expenditure, with a total cost of over $50bn in Scenario 1 or $43bn in

Scenario 2. Unlike the other countries in the report, the UK will see reasonably high levels of activity throughout the forecast period. From 2030 onwards, however, Norway will grow to become an incred-ibly important part of the decommissioning market. It is expected to account for 32% of the total spend 2016-2040, with 79% of this coming in the last ten years, as the large hubs finally begin to lose com-merciality.

This represents a powerful opportunity for specialist companies to establish themselves in the industry and become trusted and reliable partners to the platform operators who will desire speed, safety, cost effectiveness and reliability, as they aim to keep decommissioning costs low and ensure removal work is completed without incident.

The North Sea Decommissioning Market Forecast is supported by analysis, insight and industry consulta-tion and includes:

• Drivers & indicators – a review of the factors influencing the North Sea decommissioning mar-ket, including: oil & gas prices; maturity of fields; tax regimes; operations and maintenance costs; legislation and challenges in the oil & gas industry.

• Overview of decommissioning process – an in-depth look into how decommissioning is completed, from the cessation of production all the way through to the onshore deconstruction phase. This details the different options available to operators, including the use of HLVs and SLVs and a section on the current HLV and HTV fleets.

North Sea Decommissioning Market Forecast 2016-2040energy business insight

e: [email protected] t: +44 (0)203 4799 505

www.douglas-westwood.com

Aberdeen | Faversham | Houston | London | Singapore

To Order

Complete the order form and mail, fax or email us your details.Payment: goods will only be dispatched on receipt of payment in full. A pre-payment invoice will be issued on request. Payment must be made in UK Pounds. Payment may be by a cheque drawn on a UK bank.Credit card owners: give full name and address of the cardholder and telephone number - you will not be billed until dispatch.

Copyright: you agree that this report is the copyright of the authors; it is for use only within your own organisation, will not be made available in any form to third parties and will not be copied or transmitted electronically.Flexible outputs: the complexity and flexibility of DW’s models enables us to cut outputs in a number of different formats. DW is able to provide different segmentation or additional granularity if required at an additional cost.Databooks: Supporting databooks to accompany the charts and tables presented in our market forecasts are available in Excel format upon request, for most reports.Additional services: tailored to meet your company’s needs, include dedicated real-time analysis, on-site support and presentations. Please contact us to discuss further.

Name ........................................................................................ Job Title ..............................................................................

Company .................................................................................................................................................................................

Deliver address ......................................................................................................................................................................

Cardholders address ............................................................................................................................................................

Card Number ......................................................................... CCV number .........................Expiry date .......................

Signature .................................................................................. Email ....................................................................................

Tel no. ....................................................................................... Fax ........................................................................................

EU companies must give an EU VAT number ...................................................................................................

Preferred format: Number of Users: PDF * Single User (1 copy) 5350 UK Pounds Hardcopy ** Multi-User (5 copies) 6350 UK Pounds

Payment Method: Pre-payment invoice AMEX / MasterCard / Visa

Order Form

I understand that the study is copyright and for use only within my organisation. It will not be copied, or otherwise circulated to third parties or distributed electronically. (please tick)

* VAT will be added when applicable** Hardcopy deliveries outside the UK will be via DHL couriers at an additional cost of UK Pounds 60

ISBN 978-1-910045-29-9

• The supply chain – detailed analysis of the supply chain, outlining the specialised well abandonment firms, system inerting companies, disconnection specialists, infrastructure removal businesses and disposal companies

• Market forecast – summary of total expendi-ture, weight removed and the number of plat-form and well removals for the four countries featured in the report, as well as a country-by-country breakdown. Expenditure is split into two different scenarios, one showing the impact SLVs could have and one assuming the market con-tinues as it previously has. In addition, for each scenario and country, expenditure is broken down into the following segments: FPS removal, heavy transport, onshore deconstruction, PSV (and DSV), substructure removal, topside re-moval and well decommissioning. There is also a separate section on the onshore deconstruction market.

• Supporting databook – the report will be released with a supporting Excel workbook that features all of the tables and charts that are included in the report.

Why purchase the North Sea Decommissioning Market Forecast?DW’s market forecasting is trusted by sector players worldwide, with clients including the world’s top-10 oil & gas companies, top-10 oilfield services compa-nies and top-10 private equity firms.

The report is essential for financial institutions, equipment manufacturers, offshore engineering, operations & maintenance companies, ROV opera-tors, cutting service companies, contractors, oil & gas companies and agencies & government depart-ments wanting to make more informed investment decisions.

Our proven approach includes:

• Unique and proprietary data – updated year-round from published sources and insight gained from industry consultation.

• Detailed methodology – analysis is based on DW’s in-house Oil & Gas database which details every field in the North Sea. The data feeds into the market model to generate forecasts of decommissioning activity on a yearly basis.

• Comprehensive analysis – comprehensive examination, analysis and 25-year coverage of decommissioning expenditure, tonnage removal and the number of platform and well removals each year.

• Concise report layout – consistent with DW’s commitment to delivering value for our clients, all our market forecasts have a concise layout consisting of industry background and supporting materials condensed to enable quick review with ‘speed-read’ summaries of key points through-out.

2016

North Sea Decommissioning

Market Forecast

Prospects, Technologies, Markets

2016-2040

© 2016 Douglas-Westwood 2North Sea Decommissioning Market Forecast 2016-2040By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Contents

Table of Contents

1 Summary & Conclusions ..........................................6Summary ......................................................................................................................................... 7

Conclusions .................................................................................................................................... 8

2 Drivers and Indicators ..............................................9Offshore Oil & Gas and the North Sea .................................................................................. 10

Oil – Supply & Demand ............................................................................................................. 11

Oil Price Volatility ....................................................................................................................... 12

Oil Price Impacts ......................................................................................................................... 13

Historical Platform Installations ............................................................................................... 14

Historical Subsea Tree Installations ......................................................................................... 15

Oil & Gas Challenges ................................................................................................................. 16

Drivers of North Sea Decommissioning ................................................................................ 17

Drivers of North Sea Decommissioning – Legislation ........................................................ 18

3 Overview of Decommissioning Process ........... 20Decommissioning Planning Phase ............................................................................................ 21

Overview of Decommissioning Process ................................................................................. 22

Well Abandonment ..................................................................................................................... 23

Infrastructure Removal .............................................................................................................. 24

Other Considerations ................................................................................................................ 26

Decommissioning – HLVs .......................................................................................................... 27

Decommissioning – HTVs ......................................................................................................... 28

Decommissioning – SLVs ........................................................................................................... 29

Decommissioning – SLV: Pioneering Spirit............................................................................. 30

4 Supply Chain ............................................................ 31Well Abandonment ..................................................................................................................... 32

Platform Decommissioning – System Inerting and Disconnection ................................... 33

Platform Decommissioning – Infrastructure Removal & Disposal .................................... 34

5 Market Forecast ...................................................... 35Methodology ................................................................................................................................ 36

Denmark, Germany, Norway & UK : Total Expenditure .................................................... 38

Denmark, Germany, Norway & UK : Total Removals ......................................................... 39

Summary : Weight ....................................................................................................................... 40

Denmark : Total Expenditure ................................................................................................... 41

Denmark : Platform & Well Removals .................................................................................... 42

Germany Summary ..................................................................................................................... 43

Norway : Total Expenditure ..................................................................................................... 44

Norway : Platform & Well Removals ...................................................................................... 45

UK : Total Expenditure .............................................................................................................. 46

UK : Platform & Well Removals ............................................................................................... 47

Onshore Deconstruction .......................................................................................................... 48

6 Appendix .................................................................. 49Data and Text Conventions ...................................................................................................... 50

© 2016 Douglas-Westwood 3North Sea Decommissioning Market Forecast 2016-2040By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Contents

Figures and Tables

Figure 1: Tonnage Removed by Country ............................................................................................................7

Figure 2: Capex Comparison S1 and S2 .............................................................................................................8

Figure 3: Global Onshore vs Offshore Oil & Gas Production, 2005-2021.................................... 10

Figure 4: Regional Offshore Oil & Gas Production, 2000-2015 .......................................................... 10

Figure 5: Oil Price & Demand,1990-2015 ....................................................................................................... 11

Figure 6: World Liquids Production Growth, 2005-2015 ..................................................................... 11

Figure 7: Historical Brent and WTI Oil Prices, January 2010 -January 2016 ................................ 12

Figure 8: Average Annual Brent Spot Price Forecasts, 2010-2020 .................................................... 12

Figure 9: O&G Sector Average Stock Performance Index, June 2014-Dec 2015 .................... 13

Figure 10: Quarterly Visible Subsea Production Tree Orders, Q1 2008-Q3 2015 ................... 13

Figure 11: Fixed Platform Installations 1990-2015 ...................................................................................... 14

Figure 12: Subsea Tree Installations 1990-2015 ........................................................................................... 15

Figure 13: Oil & Gas Production versus E&P Spend, 2000-2016 ....................................................... 16

Figure 14: Skilled Workers by Age Category, 2014 ................................................................................... 16

Figure 15: Model cash flow for a development drilling project ........................................................... 21

Figure 16: Allseas Pioneering Spirit ..................................................................................................................... 30

Figure 17: North Sea Total Cost Scenario 1 .................................................................................................. 38

Figure 18: North Sea Total Cost Scenario 2 .................................................................................................. 38

Figure 19: Number of Platforms Removed by Country .......................................................................... 39

Figure 20: Number of Wells Removed by Country................................................................................... 39

Figure 21: Substructure Tonnage Removed by Country ......................................................................... 40

Figure 22: Topside Tonnage Removed by Country .................................................................................... 40

Figure 23: Tonnage Removed by Size 2016-2040....................................................................................... 40

Figure 24: Denmark – Total Cost Scenario 1 ................................................................................................ 41

Figure 25: Denmark – Total Cost Scenario 2 ................................................................................................ 41

Figure 26: Denmark – Number of Platforms Removed by Size .......................................................... 42

Figure 27: Denmark – Number of Wells Removed by Surface/Subsea .......................................... 42

Figure 28: Norway – Total Cost Scenario 1 ................................................................................................. 44

Figure 29: Norway – Total Cost Scenario 2 ................................................................................................... 44

Figure 30: Norway – Number of Platforms Removed by Size ............................................................ 45

Figure 31: Norway – Number of Wells Removed by Surface/Subsea ............................................. 45

Figure 32: UK – Total Cost Scenario 1 ............................................................................................................. 46

Figure 33: UK – Total Cost Scenario 2 ............................................................................................................. 46

Figure 34: UK – Number of Platforms Removed by Size ....................................................................... 47

Figure 35: UK – Number of Wells Removed by Surface/Subsea ........................................................ 47

Figure 36: Onshore Deconstruction Expenditure Comparison ........................................................... 48

Table 1: Tax Rates ....................................................................................................................................................... 17

Table 2: Number of Platforms by Size Category ......................................................................................... 17

Table 3: Average Age of Platforms by Size Category ................................................................................ 17

Table 4: Key OSPAR Terms ..................................................................................................................................... 18

Table 5: Re-use and Disposal of Platform Components .......................................................................... 22

Table 6: Forms of Topside Removal.................................................................................................................... 24

Table 7: Forms of Steel Jacket Removal ........................................................................................................... 25

Table 8: Heavy Lift Barge Fleet .............................................................................................................................. 27

Table 9: Heavy Lift/Crane Vessel Fleet .............................................................................................................. 27

Table 10: Heavy Transport Fleet >5,000t Deadweight Capacity, by Operator ........................... 28

Table 11: SLVs Under Construction ................................................................................................................... 29

Table 12: Fixed Platform Size Categories ........................................................................................................ 36

Table 13: History of Platforms Offshore Germany ..................................................................................... 43

Table 14: Onshore Cost by Country ................................................................................................................. 48

Figures

Tables

© 2016 Douglas-Westwood 4North Sea Decommissioning Market Forecast 2016-2040By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Notes & Acknowledgements

Report Details

Disclaimer

This report is a Douglas-Westwood (DW)

study and all rights are reserved, whether

this pertains to the body of the report or any

information contained within. The information

contained in this document is believed to be

accurate, but no representation or warranty,

express or implied, is made by Douglas-West-

wood as to the completeness, accuracy or

fairness of any information contained in it, and

we do not accept any responsibility in relation

to such information whether fact, opinion or

conclusion that the reader may draw. The

views expressed are those of the individual

authors and do not necessarily represent those

of the publisher.

While we have made every attempt to ensure

the information contained in this document

has been obtained from reliable sources,

Douglas-Westwood is not responsible for any

errors or omissions, or for the results obtained

from the use of this information. All informa-

tion in this document is provided “as is”,

with no guarantee of completeness, accuracy,

timeliness or of the results obtained from the

use of this information, and without warranty

of any kind, express or implied, including, but

not limited to warranties of performance, mer-

chantability and fitness for a particular purpose.

Nothing herein shall to any extent substitute

for the independent investigations and the

sound technical and business judgment of the

reader. Laws and regulations are continually

changing, and can be interpreted only in light

of particular factual situations.

North Sea Decommissioning

Market Forecast

is published by:

Douglas-Westwood Limited,

20 East Street

Faversham

Kent

ME13 8AS, UK

tel: +44 203 4799 505

fax: +44 1795 594748

© Copyright Douglas-Westwood

Limited 2016

By purchasing this document, your

organisation agrees that it will not

copy or allow to be copied in part or

whole or otherwise circulated in any

form any of the contents without the

written permission of the publishers.

DW report number 570-16

ISBN 978-1-910045-29-9

Production Team

Editor

Steve Robertson

Assistant Editor

Hannah Lewendon

Report Author

Ben Wilby

Layout & Graphic Design

Oliver Solly

A supporting databook to accompany the charts and tables presented in this report

is available in Excel format upon request.

Date of publication: 15xx February 2016

© 2016 Douglas-Westwood 5North Sea Decommissioning Market Forecast 2016-2040By purchasing this document, your organisation agrees that it will not copy or allow to be copied in part or whole or otherwise circulated in any form any of the contents without the written permission of Douglas-Westwood

Douglas-Westwood’s Offerings

Notes & Acknowledgements

About Us

Established in 1990, Douglas-Westwood is

a leading provider of market research and

consulting services to the energy industry

worldwide. We have completed over 1,100

projects for clients in more than 70 different

countries and in some 250 niche energy

segments. Our clients range from the oil &

gas majors and their contractors to financial

houses and governments. Our research is

supported by proprietary data, insight and

knowledge. Our international reach is backed

up by one of the largest sector-focused teams

in offices in the Americas, Europe and Asia.

Douglas-Westwood is a member of the

Energy Software Intelligence Analytics group

of companies.

Douglas-Westwood clients include the world’s:

Top-10 oil & gas companies

Top-10 oilfield services companies

“Energy experts Douglas-Westwood”

The Guardian

Consultancy

With an extensive advisory team spanning

three continents, Douglas-Westwood deliv-

ers energy business consultancy services

across the globe. DW consultancy services

are focused on the strategic planning pro-

cess, helping our clients to make investment

decisions, develop and test advanced com-

petitive strategies for new products, new

business streams, mergers and acquisitions,

We provide consultancy services through

advanced market insight, modelling and

simulation to a client base which includes

players in oil & gas E&P, oilfield services,

conventional & renewable energy and the

public sector.

Douglas-Westwood has supplied con-

sultancy services to over 250 companies

worldwide.

“Foremost oilfield services

market consultant”

Hong Kong client

Transactions

Douglas-Westwood provides sector-

focused commercial due-diligence and

transactions services to major and mid-tier

private equity firms, investment banks

and debt providers. We have industry-

leading credentials including both buy-side

and sell-side mandates, public-to-private

transactions, re-financing, IPOs and project

financing ranging in enterprise value from

$5 million technology firms to $1 billion

oilfield service, engineering and equipment

companies.

Douglas-Westwood clients include the

world’s:

Top-10 private equity firms

Top-10 investment banks

“Douglas-Westwood provides

great value to us”

Perth client

Research

Business research, analysis and market

forecasting is our core activity. Over the

years we have built a huge knowledge base

of both sectors and players. Our experience

of researching the oilfield services sector

(OFS) is unparalleled worldwide. We spe-

cialise in emerging markets and technolo-

gies, from offshore windpower to subsea

processing and difficult to access markets

and geographies including Russia and the

Middle East. Our custom research offerings

include: gathering & analysis of market data,

independent marketing and forecasting,

measurement & analysis of competitive po-

sitions and industry consultation & in-depth

perception surveys.

Douglas-Westwood have researched some

250 different business sectors to wide

international acclaim.

“Top energy research group

Douglas-Westwood”

Financial Times

Publications

Douglas-Westwood produces original en-

ergy business market studies and forecasts,

now highly acclaimed and used worldwide.

In oil & gas we were the first firm to

forecast & value the growth of key offshore

markets such as deepwater, subsea produc-

tion, global onshore drilling, pipelines and

offshore wind power.

Our reports are geared to meet senior

executives’ needs in business planning and

decision-making and assume no previous

reader knowledge of the subject area. Each

offers a concise, region by region format.

Analysis is based on our extensive in-house

project databases and models combined

with forecasting expertise developed over

many years.

Douglas-Westwood has over 20 energy

sector market forecast titles in print.

“An excellent report in all areas”

Houston client