north korea: a war of words for now? - ocbc bank reports/ocbc korea outlook... · north korea: a...

TRANSCRIPT

North Korea: A war of words for now?

Barnabas Gan

Economist

Global Treasury Research & Strategy

August 2017

1

2

Executive Summary • For now, it is merely a war of words. Rhetorically, US vice-president Mike Pence has

mentioned that “all options (are) on the table”, while Trump citing “fire and fury”. Japan, a

close proximity to North Korea, has also voiced that North Korea “is a grave threat to

(Japan)… We strongly condemn such acts.” The only peace-making comment is heard from

China, given official comments that China “will absolutely not permit war or chaos on the

peninsula,” and for good reasons.

• However, if the war of words escalate into a military engagement, our estimates suggest a

derailing of global growth, led by a fall in both trade volumes and asset prices. Even in

today’s war of words, there has been an observable rise in demand for safe haven assets,

such as the JPY, UST and gold, while dragging growth-related assets like equities. As of 11th

August, the dollar has fallen to its April ‘17 low against the yen, while gold rallied to near its

$1,300/oz. Should the escalation prove to be a prolonged one, gold may rally by as much as

30% while global equities (especially Wall Street) could fall by as much as 20%. Elsewhere,

the JPY should eventually fall given the proximity of the conflict.

• Despite the recent intensification, there are no signs that the US is planning a pre-emptive

strike against North Korea, nor are there any evidences that Kim will make good on threats to

hit US shores. For war to eventually start, the US must (1) first evacuate tens of thousands of

US civilians from South Korea and Japan, (2) deploy a reinforcement of troops in the Korean

Peninsula, and (3) ensure collateral damage on Asian shores (China, South Korea, Japan) to

be limited. A pre-emptive strike by either parties is unlikely as well, as it could adversely dent

global risk-taking appetite, not mentioning the many lives lost as a result.

3

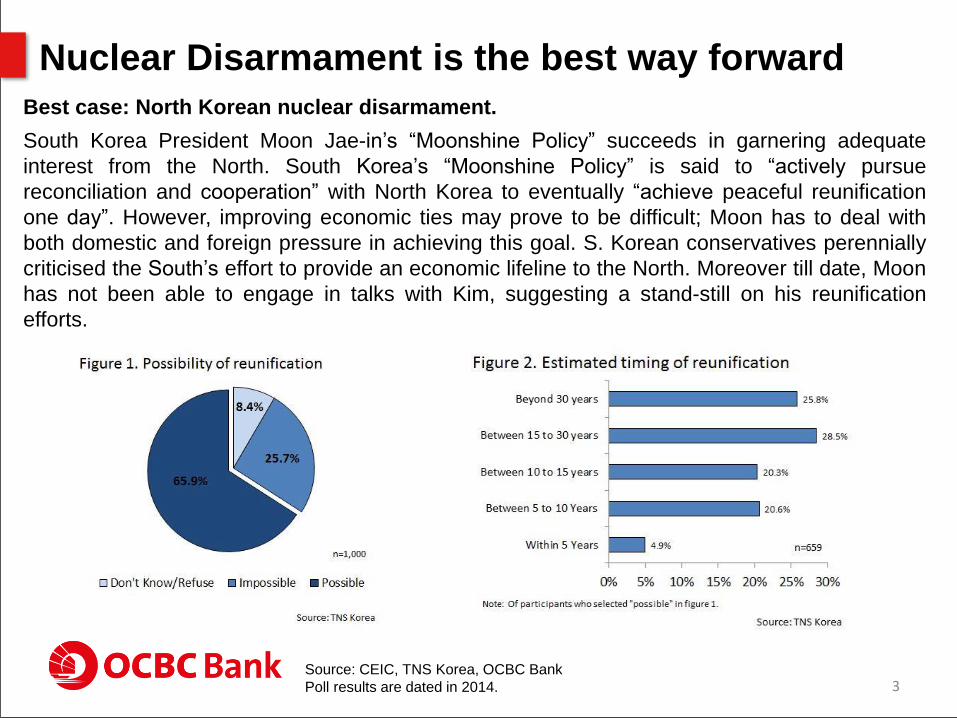

Nuclear Disarmament is the best way forward

Best case: North Korean nuclear disarmament.

South Korea President Moon Jae-in’s “Moonshine Policy” succeeds in garnering adequate

interest from the North. South Korea’s “Moonshine Policy” is said to “actively pursue

reconciliation and cooperation” with North Korea to eventually “achieve peaceful reunification

one day”. However, improving economic ties may prove to be difficult; Moon has to deal with

both domestic and foreign pressure in achieving this goal. S. Korean conservatives perennially

criticised the South’s effort to provide an economic lifeline to the North. Moreover till date, Moon

has not been able to engage in talks with Kim, suggesting a stand-still on his reunification

efforts.

Source: CEIC, TNS Korea, OCBC Bank

Poll results are dated in 2014.

4

N. Korea will benefit immensely from reunification

Source: Google Images, Bank of Korea, Thomson

Reuters, CIA World Factbook, OCBC Bank

5

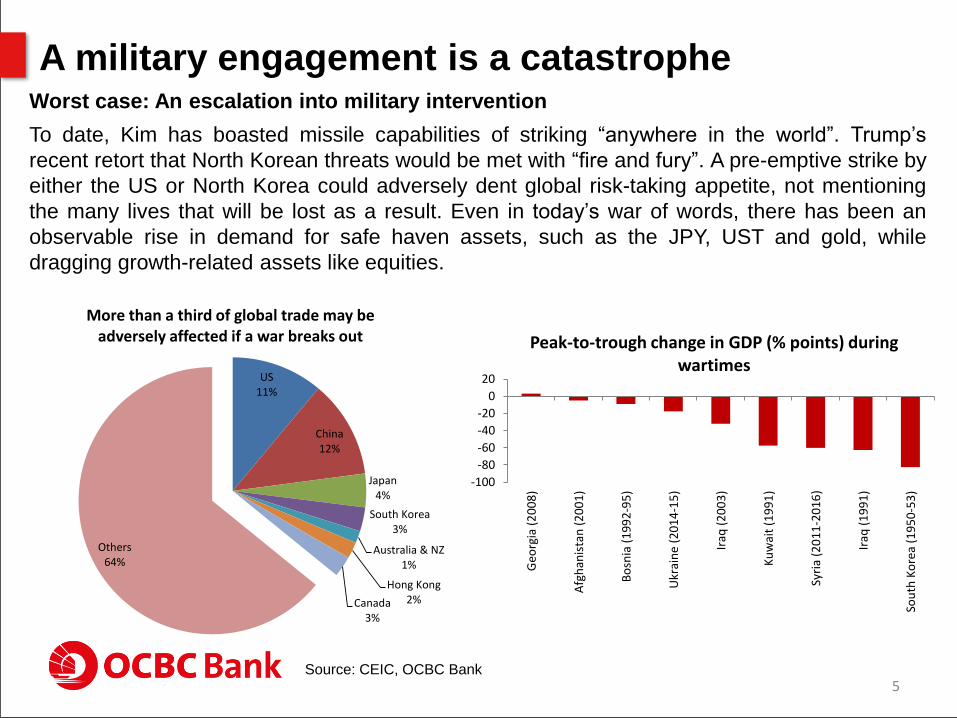

A military engagement is a catastrophe Worst case: An escalation into military intervention

To date, Kim has boasted missile capabilities of striking “anywhere in the world”. Trump’s

recent retort that North Korean threats would be met with “fire and fury”. A pre-emptive strike by

either the US or North Korea could adversely dent global risk-taking appetite, not mentioning

the many lives that will be lost as a result. Even in today’s war of words, there has been an

observable rise in demand for safe haven assets, such as the JPY, UST and gold, while

dragging growth-related assets like equities.

Source: CEIC, OCBC Bank

US11%

China12%

Japan4%

South Korea3%

Australia & NZ1%

Hong Kong2%Canada

3%

Others64%

More than a third of global trade may be adversely affected if a war breaks out

-100

-80

-60

-40

-20

0

20

Geo

rgia

(2

00

8)

Afg

han

ista

n (

20

01

)

Bo

snia

(1

99

2-9

5)

Ukr

ain

e (

20

14

-15

)

Iraq

(2

00

3)

Ku

wai

t (1

99

1)

Syri

a (2

01

1-2

01

6)

Iraq

(1

99

1)

Sou

th K

ore

a (1

95

0-5

3)

Peak-to-trough change in GDP (% points) during wartimes

6

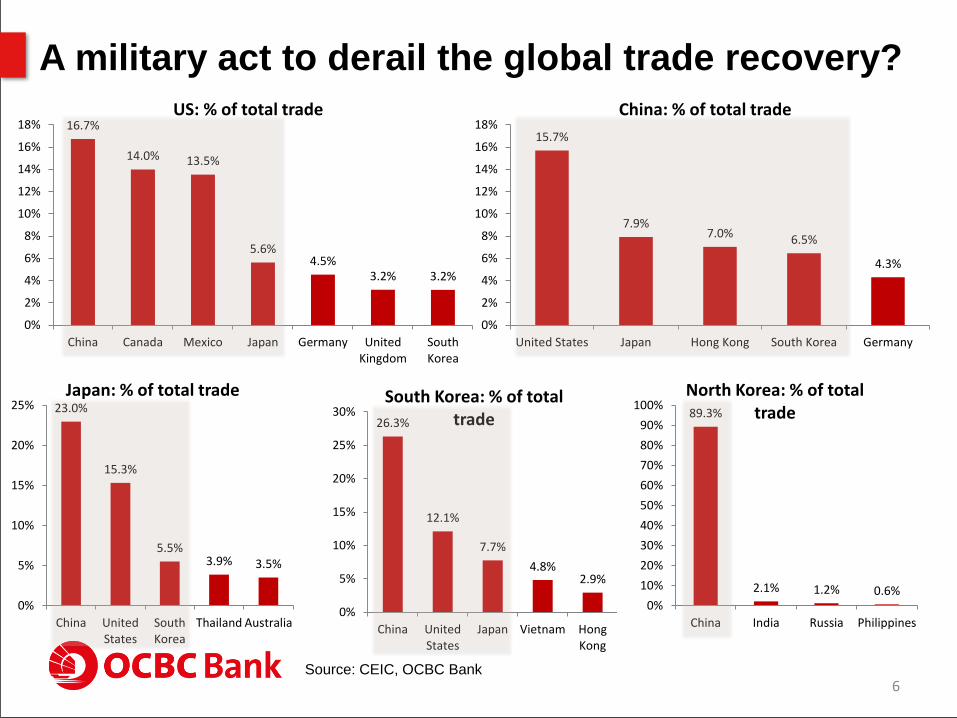

A military act to derail the global trade recovery?

Source: CEIC, OCBC Bank

16.7%

14.0% 13.5%

5.6%4.5%

3.2% 3.2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

China Canada Mexico Japan Germany UnitedKingdom

SouthKorea

US: % of total trade

15.7%

7.9%7.0% 6.5%

4.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

United States Japan Hong Kong South Korea Germany

China: % of total trade

23.0%

15.3%

5.5%3.9% 3.5%

0%

5%

10%

15%

20%

25%

China UnitedStates

SouthKorea

Thailand Australia

Japan: % of total trade

26.3%

12.1%

7.7%

4.8%2.9%

0%

5%

10%

15%

20%

25%

30%

China UnitedStates

Japan Vietnam HongKong

South Korea: % of total trade 89.3%

2.1% 1.2% 0.6%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

China India Russia Philippines

North Korea: % of total trade

7

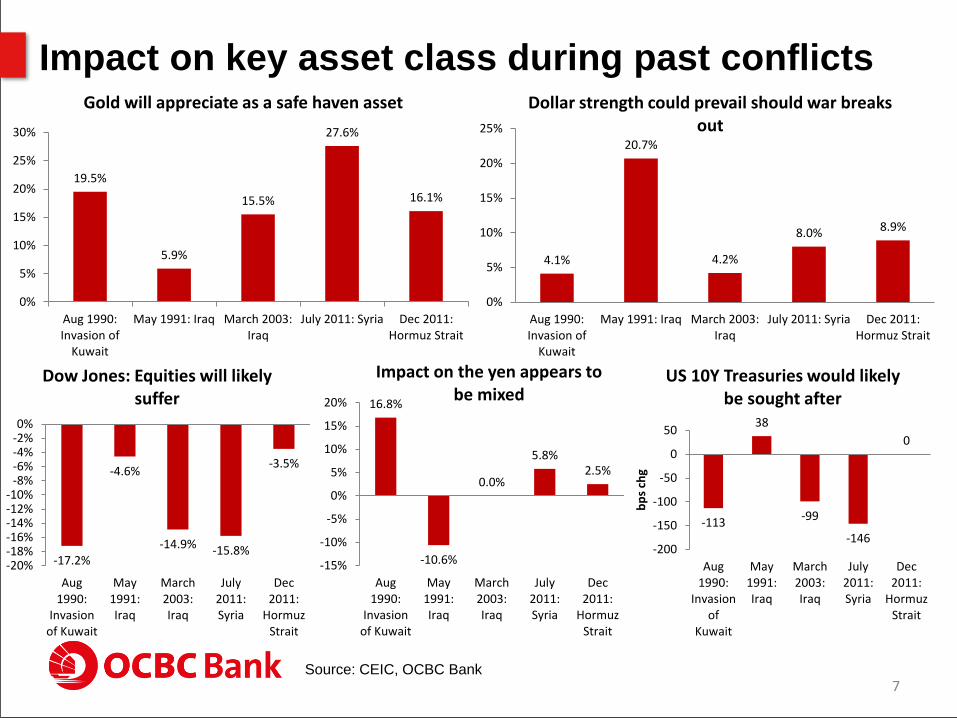

Impact on key asset class during past conflicts

Source: CEIC, OCBC Bank

19.5%

5.9%

15.5%

27.6%

16.1%

0%

5%

10%

15%

20%

25%

30%

Aug 1990:Invasion of

Kuwait

May 1991: Iraq March 2003:Iraq

July 2011: Syria Dec 2011:Hormuz Strait

Gold will appreciate as a safe haven asset

4.1%

20.7%

4.2%

8.0% 8.9%

0%

5%

10%

15%

20%

25%

Aug 1990:Invasion of

Kuwait

May 1991: Iraq March 2003:Iraq

July 2011: Syria Dec 2011:Hormuz Strait

Dollar strength could prevail should war breaks out

-17.2%

-4.6%

-14.9% -15.8%

-3.5%

-20%-18%-16%-14%-12%-10%

-8%-6%-4%-2%0%

Aug1990:

Invasionof Kuwait

May1991:Iraq

March2003:Iraq

July2011:Syria

Dec2011:

HormuzStrait

Dow Jones: Equities will likely suffer 16.8%

-10.6%

0.0%

5.8%2.5%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Aug1990:

Invasionof Kuwait

May1991:Iraq

March2003:Iraq

July2011:Syria

Dec2011:

HormuzStrait

Impact on the yen appears to be mixed

-113

38

-99

-146

0

-200

-150

-100

-50

0

50

Aug1990:

Invasionof

Kuwait

May1991:Iraq

March2003:Iraq

July2011:Syria

Dec2011:

HormuzStrait

bp

s ch

g

US 10Y Treasuries would likely be sought after

8

Referencing history: Should a military conflict

occur

Source: Bloomberg, CEIC, OCBC Bank

Current

(11th Aug

2017)

Aug 1990:

Invasion of

Kuwait

May

1991: Iraq

March

2003: Iraq

July 2011:

Syria

Dec 2011:

Hormuz

Strait

Escalation of

military

conflict?

Gold 1290 +19.5% +5.9% +15.5% +27.6% +16.1% +6% to +30%

DJIA 21800 -17.20% -4.60% -14.90% -15.80% -3.50% -4% to -20%

JPY 109 +16.8% -10.60% Flat +5.8% +2.5% -5% to -15%

UST 10Y Yield 2.19%-113bps

(-12.5%)

+38bps

(+4.4%)

-99bps

(-24.2%)

-146bps

(-46.0%)Flat

0 to -60bps

(0% to -27%)

DXY 93.36 +4.1% +20.7% +4.2% +8.0% +8.9% 0% to +20%

9

How asset classes react during missile launches

Source: CEIC, OCBC Bank

Dates refer to recent North Korean missile launches

97

98

99

100

101

102

103

t-3

0

t-2

7

t-2

4

t-2

1

t-1

8

t-1

5

t-1

2

t-9

t-6

t-3 t

t+3

t+6

t+9

t+1

2

t+1

5

t+1

8

t+2

1

t+2

4

t+2

7

t+3

0

Dow Jones Industrial Average

Jul-28 Jul-04 May-13

84

89

94

99

104

109

114

t-3

0

t-2

7

t-2

4

t-2

1

t-1

8

t-1

5

t-1

2

t-9

t-6

t-3 t

t+3

t+6

t+9

t+1

2

t+1

5

t+1

8

t+2

1

t+2

4

t+2

7

t+3

0

S. Korea CDS

Jul-28 Jul-04 May-13

94

96

98

100

102

104

106

108

t-3

0

t-2

7

t-2

4

t-2

1

t-1

8

t-1

5

t-1

2

t-9

t-6

t-3 t

t+3

t+6

t+9

t+1

2

t+1

5

t+1

8

t+2

1

t+2

4

t+2

7

t+3

0

Gold

Jul-28 Jul-04 May-13

96

97

98

99

100

101

102

103

104

t-3

0

t-2

7

t-2

4

t-2

1

t-1

8

t-1

5

t-1

2

t-9

t-6

t-3 t

t+3

t+6

t+9

t+1

2

t+1

5

t+1

8

t+2

1

t+2

4

t+2

7

t+3

0

USDKRW

Jul-28 Jul-04 May-13

10

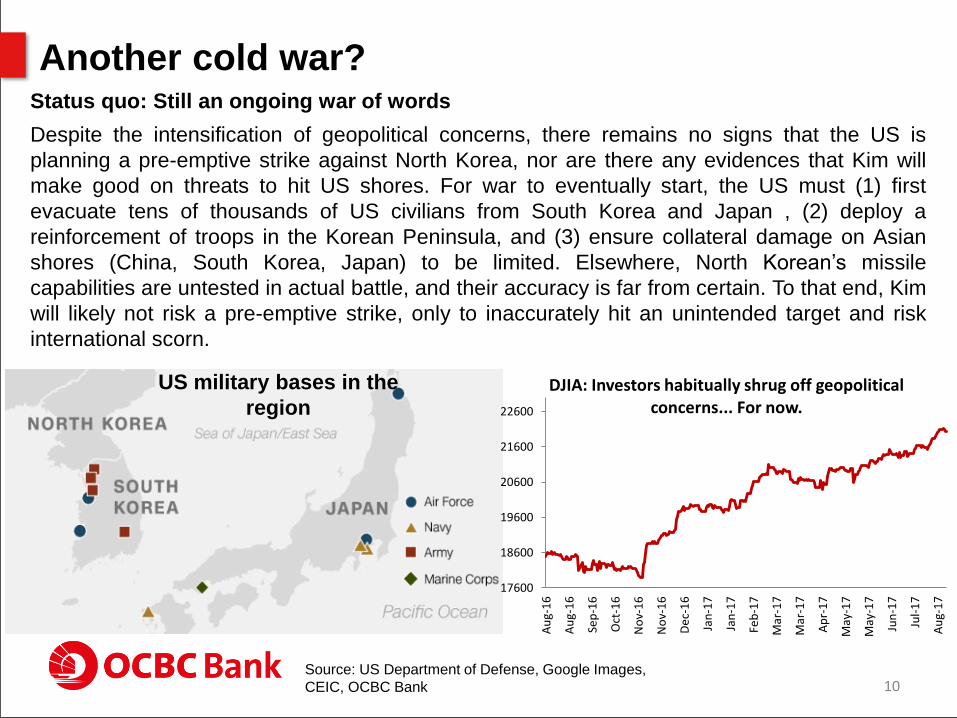

Another cold war? Status quo: Still an ongoing war of words

Despite the intensification of geopolitical concerns, there remains no signs that the US is

planning a pre-emptive strike against North Korea, nor are there any evidences that Kim will

make good on threats to hit US shores. For war to eventually start, the US must (1) first

evacuate tens of thousands of US civilians from South Korea and Japan , (2) deploy a

reinforcement of troops in the Korean Peninsula, and (3) ensure collateral damage on Asian

shores (China, South Korea, Japan) to be limited. Elsewhere, North Korean’s missile

capabilities are untested in actual battle, and their accuracy is far from certain. To that end, Kim

will likely not risk a pre-emptive strike, only to inaccurately hit an unintended target and risk

international scorn.

Source: US Department of Defense, Google Images,

CEIC, OCBC Bank

US military bases in the

region

17600

18600

19600

20600

21600

22600

Au

g-1

6

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

No

v-1

6

De

c-1

6

Jan

-17

Jan

-17

Feb

-17

Mar

-17

Mar

-17

Ap

r-1

7

May

-17

May

-17

Jun

-17

Jul-

17

Au

g-1

7

DJIA: Investors habitually shrug off geopolitical concerns... For now.

Thank You

11

12

This publication is solely for information purposes only and may not be published, circulated, reproduced or distributed in whole or in part to any other person without

our prior written consent. This publication should not be construed as an offer or solicitation for the subscription, purchase or sale of the securities/instruments

mentioned herein. Any forecast on the economy, stock market, bond market and economic trends of the markets provided is not necessarily indicative of the future or

likely performance of the securities/instruments. Whilst the information contained herein has been compiled from sources believed to be reliable and we have taken all

reasonable care to ensure that the information contained in this publication is not untrue or misleading at the time of publication, we cannot guarantee and we make no

representation as to its accuracy or completeness, and you should not act on it without first independently verifying its contents. The securities/instruments mentioned

in this publication may not be suitable for investment by all investors. Any opinion or estimate contained in this report is subject to change without notice. We have not

given any consideration to and we have not made any investigation of the investment objectives, financial situation or particular needs of the recipient or any class of

persons, and accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of the

recipient or any class of persons acting on such information or opinion or estimate. This publication may cover a wide range of topics and is not intended to be a

comprehensive study or to provide any recommendation or advice on personal investing or financial planning. Accordingly, they should not be relied on or treated as a

substitute for specific advice concerning individual situations. Please seek advice from a financial adviser regarding the suitability of any investment product taking

into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. OCBC

and/or its related and affiliated corporations may at any time make markets in the securities/instruments mentioned in this publication and together with their respective

directors and officers, may have or take positions in the securities/instruments mentioned in this publication and may be engaged in purchasing or selling the same for

themselves or their clients, and may also perform or seek to perform broking and other investment or securities-related services for the corporations whose securities

are mentioned in this publication as well as other parties generally.

Co.Reg.no.:193200032W

Disclaimer Treasury Market Research & Strategy

Selena Ling ([email protected]) Tel : (65) 6530 4887

Emmanuel Ng ([email protected]) Tel : (65) 6530 4073

Wellian Wiranto ([email protected]) Tel : (65) 6530 5949

Tommy Xie Dongming ([email protected]) Tel : (65) 6530 7256

Barnabas Gan ([email protected]) Tel : (65) 6530 1778

Terence Wu ([email protected]) Tel : (65) 6530 4367

OCBC Credit Research

Andrew Wong ([email protected]) Tel : (65) 6530 4736

Wong Liang Mian ([email protected]) Tel : (65) 6530 7348

Ezien Hoo ([email protected]) Tel : (65) 6722 2215

Wong Hong Wei ([email protected]) Tel: (65) 6722 2533