north jefferson county ambulance district docs/0 final packet.pdf · north jefferson county...

TRANSCRIPT

North Jefferson County Ambulance District

High Ridge, Missouri

2014-2015 Annual Budget

October 21, 2014

Table of Contents

PAGE

INTRODUCTION AND PROFILE

Cover Page ..................................................................................................................................... 1

List of Principal Officials .................................................................................................................. 2

Mission and Values Statement…………………………………………………………………………… 3

Organizational Chart........................................................................................................................ 4

Geographical Map 5

Fast Facts about the District ............................................................................................................ 6

District Statistics .............................................................................................................................. 7

BUDGET PROCESS AND POLICIES

Budget Preparation Process ........................................................................................................... 8

Budget and Financial Policies ......................................................................................................... 20

BUDGET SUMMARY

Budgeted Revenues, Expenditures and Changes in Fund Balance – All Funds ............................ 27

PENSION FUND

Budgeted Revenues, Expenditures and Changes in Fund Balance ............................................... 32

Director Position Serving Since Current Term ExpiresCarla Hloben Chairperson April 2011 April 2017Kathy Hennessey Vice-Chairperson April 2007 April 2015Julia Vessells Treasurer April 2010 April 2015Rebecca Cowley Director September 2012 April 2016Diana Davis Director April 2010 April 2016Tasha Schriewer Director January 2012 April 2017

Employee Position Serving Since Position Start DateJamie Guinn Chief August 1996 November 2011Jennifer Wilson Business Manager October 1995 October 1995Norman Corley Training Officer June 1990 2007*Laura Gunning Medical Supply Officer October 1990 January 2010William O'Hara Fleet Officer October 2005 September 2012

List of Principal Officials as of September 9, 2014

Elected Officials

Distrct Administrative Staff/Officers

102.0 Mission & Values Statements The mission of NJCAD is to provide outstanding emergency medical services and patient transportation services. We provide these services in a professional manner while maintaining the dignity of those we serve. Our staff continuously strives to learn, improve and grow in enhancing the delivery of emergency medical services to those we serve. NJCAD adheres to the following values: Commitment to Service We treat persons with illness and injury in our community with care and compassion, utilizing effective principles and practices of patient care, and we strive for excellence through ongoing evaluation and improvement. Respect We recognize the dignity of others and communicate with others in a respectful manner. Integrity We serve with honesty, loyalty and dedication. Accountability We are responsible for our actions, both positive and negative. Teamwork We practice teamwork through communication and cooperation to achieve common goals. Fair Treatment We do not discriminate against patients or personnel on the basis of race, color, national origin, ancestry, religion, sex, age, disability, political belief, military service, marital status, sexual orientation or any other legally protected characteristic.

Organizational Structure and Authority

Board of Directors

Business

Business Manager

Claims Rep

Chief Operations

Assistant Chief

A Crew Shift Officer(s)

A Crew FT Duty Crew

PT Crew

B Crew Shift Officer(s)

B Crew FT Duty Crew

PT Crew

C Crew Shift Officer(s)

C Crew FT Duty Crew

PT Crew

W

PP

MM

21

30

Byrnes Mill

Parkdale

Scotsdale

Village of Peaceful VillageNorth Jefferson

Big River

Rock Township

Eureka Fire/Ambulance

Sugar Cree

k

Big R

iver

Antir

e Cree

k

Saline Creek

Bear

CreekHeads Creek

Rock Creek

Bour

ne C

reek

Dulin Creek

Romaine Creek

Williams C

reek

Kneff Road Tributary

Unnamed Tributary to Big River

Meram

ec R

iver

Saline Creek

Rock

Creek

Rock

Cree

k

Rock

Creek

Heads Creek

Dulin

Cree

k

Williams C

reekState

Route 30

State Road MM

State Route 2

1 North

State

Rou

te 21

Sou

th

State Road W

State Road PP

Gravois Road

Hunning Rd

Old State Rt. 21

Antir

e Rd

Saline Rd

Hunning Rd

Old S

ugar

Cre

ek R

d

East Swaller Rd

Schumacher Rd

Duda Rd

Twin River Rd

Dillon Rd

Caro

l Par

k Rd

Rock

Cre

ek Va

lley R

d

Gravois (Schumacher) Rd

Dry Fork (East) Rd

Lions Den Rd

Hillsboro House Springs Rd

Blecha Rd

East

Romain

e Cree

k

Coil Rd

Miller (off Hwy MM ) Rd

Brennan Rd

Burgan Grove Gravois(N

orthwest School) R

d

John Swaller Rd

Meadow Drive

Biltmore Dr

Little

Bre

nnan

Rd

Bear Creek Rd

Northwest Blvd

Diehl Rd

Delor

es D

r

Golda

Ln

Singing Hills Rd

Hawkins Rd

Valley

Dr

Franks Road

Byrn

es M

ill Ro

ad

Lower Byrnes Mill Road

Gravois RdRosewood Lane

Fawn Woods Drive

Scotsdale Blvd

Vogt Road

L Street

Wild

Valle

y Driv

e

Lewi

s Roa

d

Fairway Drive

Glik Road

Kley Lane

Werner Road

Butler Valley

Gail Drive

Hickory Lane

Chot

t Driv

e

River Bend Drive

Ravinia

Way

Lang Valley Drive

Ulrich Lane

Main

Drive

Glen Haven Road

Della Drive

JC Lane

Birch Drive

Terrace Drive

Country Road

Country Club Drive

Waybridge LaneWallach Drive

Ottomeyer Road

Irish S

ea Driv

e

Brosh Farm Rd

Green Valley Drive

Parkedge Drive

Glendale Road

E Lake Road

Rim Ro

ad

Kley Road

Cente

r Driv

e

Bent Oak Drive

Wilbert Road

Hill Drive

Wilderne

ss Lan

e

River Bend Acres Rd

Lally Drive

Music Mountain

Emerson Road

Echo Lake Circle

Gem Drive

Katrina D

rive

Mano

r Cre

st Dr

ive

Whitby Lane

Dellwood Lane

Donn

a Driv

e

Diehl Lane

Suns

wept

Lane

Kovarik Lane

Inland Drive

Anise Lane

Blue Springs R

oad

Lions Den Spur

Hilge

rt Driv

e

Patti Lane

West

Drive

Ridge Drive

Crest Drive

Anna Lee Drive

Lisand Drive

Saline Lane

Rose Park Road

Davis Drive

Oakc

rest

Drive

Belmont Drive

Olde Mill DriveWindswept Lane

Maple Drive

Rainbow Drive

Pogu

e Driv

eGreenway Drive

Terry Drive

Darren Drive

Ron-El Drive

Timberline Drive

Saline Point

Brinridge Drive

Laverne Drive

Oak Tre

e Lane

Will Drive

Pike T

rail

Tiffiny Lane

Trails

Drive

Hopp

e Hill

Drive

Ozark

Lane

Schumacher Road

W Fork Drive

Ron Driv

eVince Ann Lane

Harter Farm Road

Traci

Drive

Arlow

Driv

e

Ginger Root Drive

Ottomeyer Lane

Spavale Drive

Rainbow Trail

Dogwood Lane

Fores

t Lan

e

Fisher Way

Duda

Rd

Erb Ind Drive

Parkway Drive

Patrick Drive

Cold Springs Ridge

Walnu

t View

Roads End Acres

Thunder Road

River Road

King T

erra D

rive

Monti

cello

Cou

rt

Dana Drive

Sprin

gview

Drive

Wildw

ind La

ne

Elijah

Driv

e

Spring Valley Road

Hendricks Road

Caro

l Lan

e

Stacey Lane

Hickory Ridge Lane

Ridge Road

Gloucester Road

Sunset Drive

Windy Hill Lane

Hawthorn Drive

Cedar Glade Road

Linnus Drive

Henry Drive

Vista View

Drive

Golden Court

Wren Drive

Frontier Trail

Straathaven Drive

Kirchoff Lane

Carol Street

Hunte

r Lan

e

Mill Lake Court

Came

lot La

ne

Cherry Hill Drive

Quint

ana D

rive

Fisher Road

Pitcher D

rive

Memory Lane

Patricia Place

Land

Rus

h Driv

e

Pioneer Drive

Ruth

Driv

e

Eldon

Driv

e

Lois Lane

Cardinal Lane

Elizabeth

Drive

Camelot Court

Debb

ie Dr

ive

Rio Drive

Bush Road

Sunr

ise D

rive

Lost Road

Weil Lane

Islamora

da Driv

e

Robin Drive

Meadow Lane

Cotton Lane

Cambridge Lane

Al's Lane

Twin Trails Court

Pono

toc L

ane

High Trace

Toot

er La

ne

Treetop Lane

Mikel Lane

Roberta Drive

Verdant Drive

Phil's

Driv

e

Fawn Lane

Ridge

Point

Dr

Wildwoo

d Lan

eBl

ack O

ak Te

rrace

Lake Road

Dale Drive

Laur

el Dr

ive

Sassafras Lane

Park Drive

Trails Court

Pine Road

Diana Drive

Estates Drive

Stonehill Manor

Sycamore Lane

Nutmeg Lane

Brosh Lane

Virginia Drive

Velma Drive

Kruger Lane

Matts Manor

Hope Lane

Rosemary

Lane

Brighton Court

Keith Drive

Doris

Driv

e

Demare

e Cou

rt

S Golden Circle

Newcas

tle Court

Werner Drive

Cedar DriveJanet Lane

Ruby

Driv

e

Oakwood Road

Spur Drive

Belle Lane

Orchard Drive

Vasel Drive

Calico Lane

Miller Drive

Holly Place

Westwood Drive

Glas

s Lan

e

Mockingbird Drive

Jewel Court

Hy Drive

Stieren Court

Mae Court

Leona Lane

Maxwell Lane

Tyrer Lane

Alley Drive

Country

Club Drive

North Jefferson Ambulance District

®Legend

Rivers, Creeks, Streams

Interstate

State HighwaysCounty RoadsFestus Special RoadsCity Streets

US Highways

Private Streets

§̈¦

21

£¤67

55 MunicipalitiesBig RiverEureka Fire/AmbulanceJoachim-PlattinMeramecNorth JeffersonRock TownshipValle

0 0.5 10.25Miles

1 inch = 2,000 feet1:24,000Scale:

Map Created By: Planning DivisionDate of Map Creation: 11 September 2014Data Sources: Jefferson County Assessor's Office, ESRIJefferson County Planning Division, Jefferson County Public Works Department

District Statistics

The growth of the District is best depicted by the following statistics:

Year Number of Calls Number of Bases Number of Units 1976 * 1 *

2000 1890 * *

2005 2043 1 *

2010 2223 1 4

2013 2349 1 4

Fast Facts about the District

Area Served: 32 Square Miles

Area Make-Up: Rural, light industrial and agricultural

Population Served: 40,000 (2012)

Governing Body: Elected Board of Directors (6)

Calls per Year: 2349 (2013)

Type of Service: Emergency

Ambulances: 4 Advanced Life Support

Facilities: 1 Headquarters

EMS Dispatching: Jefferson County 911 Dispatch

Service Area: High Ridge and parts of Byrnes Mill, Eureka, Fenton and House Springs

Budget Preparation Process Understanding the Budget Process:

This guide is a resource for the governing body and officials who are responsible for preparing, developing, and monitoring the annual budget. The information contained in this guide will be helpful to chief executive officers, budget officers, business officials, finance officers, department heads, board members, and the public. This guide provides the groundwork for the development, preparation, and monitoring of the annual budget.

An annual budget, sometimes referred to as the operating budget, is the document that details the financial plan of the district for a fiscal year. The annual budget is perhaps an entity’s most vital document and should be developed using all of the most current and accurate information available. The budget is not just a financial plan; it also has legal implications, which are delineated in the “Implementing the Budget” section of this guide. Furthermore, the budget process does not end with the adoption of the budget. Instead, the budget is a document that must be monitored and amended from time to time, as needed.

The following is an overview of the information contained in this guide:

• Who is Responsible? • Information Used to Prepare the Budget • Budget Preparation Process • Putting the Tentative Budget Together • Implementing the Budget • Monitoring the Budget

In addition, the appendices to this guide include the following important information: designation of the budget officer (Appendix A), budget calendars (Appendix B), and definition of terms (Appendix C).

Who is Responsible?

Budget development is not a “one-person show.” Instead, it is a team effort with the budget officer

leading the charge. While the budget officer is responsible for preparing the final budget document, the budget officer needs to work closely with the planning team, officers and the designated board officer to develop a realistic blueprint for the upcoming fiscal year. The budget officer generally is responsible for the preparation of the tentative/proposed budget and presenting it to the governing board. The governing board generally has the authority and responsibility to adopt realistic, structurally balanced budgets and to monitor the budget continually. The designated board officer is responsible for providing accurate financial information to the budget officer. Officers are responsible for providing the budget officer with accurate financial information relevant to the operation of their department. Employees are responsible for providing input to the officers about the operation of their individual departments.

In our district, the Chief Financial Officer (CFO) is typically designated by the board as the budget officer and is responsible for developing the annual budget. The CFO is generally assisted by the planning team and board official in preparing the budget. With the board of directors approving the budget, therefore, district residents are ultimately responsible for approving district budgets.

Information Used to Prepare the Budget

A good annual budget begins with sound estimates and well-supported budgetary assumptions. Spending levels and financial resources must be accurately gauged at budget preparation time to ensure that planned services are properly funded. To develop sound estimates, budget officers should avail themselves of as much pertinent data as possible. While valuable information is available from a number of sources, the budget officer should also work closely with officers to develop a realistic annual budget.

Sources of information used in preparing the budget:

• Modified budgets for prior and current year • Prior year’s financial reports • Current year revenue and expenditure information to date • Debt service requirements, contracts, and other commitments • Current economic conditions affecting revenue generation • Cash flow reports and revenue projections • State and federal aid information • Collective bargaining agreements • Service contracts with other governments • Multiyear capital plans • New and pending legislation • Rate of inflation • Current interest rates • Tax and debt limit information – if applicable • Strategic plans • Input from labor, taxpayers and other interested groups

Budget Preparation Process

These are the steps that are typical to the budget processes.

1. The budget preparation process starts with the setting forth of the budget calendar.

2. The budget officer distributes budget forms and instructions to all the officers of the district. The forms should include all revenue and expenditure account codes used in the previous two years along with the actual and budgeted estimates for the previous fiscal year and year-to-date totals for the current year. The form should also contain space for the manager to explain or justify new types of proposed revenues or expenditures or to further explain large increases or decreases in the amounts proposed for the following year.

3. Officers submit their estimates and discuss their requests with the budget officer.

4. The budget officer uses the information from the budget forms to prepare the tentative/proposed budget. This will generally involve assessing whether the total departmental estimates of appropriations are greater than the estimated financial resources and then developing a tentative/proposed budget that provides necessary appropriations within the limits of those resources. The budget officer should also ensure that the tentative/proposed budget meets all legal requirements, consulting with the district’s legal counsel as necessary.

5. The budget officer presents the tentative/proposed budget to the governing board for its consideration and approval. At this time, it may be necessary for the budget officer to provide backup documentation for some of the estimated appropriation and revenue figures. Alterations and revisions may be necessary before approving the budget. The budget that is finally approved needs to be balanced: the total financing sources from estimated revenues, appropriated fund balance, and appropriated reserves equaling the amount of appropriations for expenditures.

6. The district publishes a notice, and a public hearing on the budget is held. Again, alterations and revisions to the budget may be necessary after completion of the public hearing.

7. The governing board adopts the final budget by majority vote. If the governing board fails to adopt a final budget by the deadline date set forth in the County Law, respectively, the preliminary budget or the tentative budget, with such changes, alterations, and revisions as may have been made by the board will constitute the final budget for the following fiscal year. If the board rejects the original budget, the district may present the original budget or a revised budget to the board a second time for approval. If the second vote is not approved or the board decides not to present the budget a second time, the district must operate under a “contingency budget.”

8. The final step of the budget preparation process is the calculation of the real & personal property tax levy.

Putting the Tentative Budget Together

Because the budget is such a key instrument in the day-to-day operations of the district, it is essential that it is properly constructed. A significant error contained within the document could have severe consequences. For example, overestimating revenues and/ or underestimating expenditures could result in shortfalls that threaten the delivery of essential services. Underestimating revenues and/or overestimating expenditures could result in the collection of more real property taxes than are necessary. Using non-recurring, one-shot revenues to support recurring expenditures may appear to offer a solution to establish a balanced budget; however, the strategy is a short-term solution and only temporarily defers the need to address structural budget imbalances. Therefore, it is important to prepare the budget using realistic estimates based on the most current and accurate information available and not to rely on one-shot revenues to support recurring expenditures.

Expenditure Estimates

After the various departments have submitted an estimate of their costs of operations for the next fiscal year, the budget officer should review them to ensure they are complete, reasonable, and mathematically accurate. If a program is being offered for the first time or a major change to an existing program is anticipated, the manager should provide sufficient documentation for the governing board to consider when approving or disapproving the change. Based upon the governing board’s decision, the board may need to approve the imposition of a new fee or the addition/ deletion of services.

In addition to the department estimates and requests, there are certain items that can affect an entire fund and may or may not have been specifically addressed by a department.

• Debt Service – Debt service schedules should be reviewed to determine the principal and interest expenditures for the upcoming year. In addition, recent governing board resolutions regarding current or pending debt issuances should also be reviewed, so that all debt service costs can be incorporated in the budget.

• Employee Salaries – The payroll or human resources department should provide a listing of current employees with their salary estimates. When reviewing employee listings, the budget officer should verify that all employees and positions are included. Salary schedules and collective bargaining agreements will generally determine the rates of pay for the upcoming year. Similarly, the employer’s share of Social Security costs can be estimated by applying the applicable rate to the anticipated personal service costs for next year..

• Employee Benefits – In order to estimate the cost of employee benefits, the budget officer must first review the various collective bargaining agreements and personnel policies adopted by the governing board to determine what employee benefits must be funded. Health care benefit costs can be estimated by reviewing current policies and programs and applying projected rates to the probable make-up of next year’s workforce. Retirement benefit costs can be estimated by using projected rates for employer contributions received from the Retirement Program. Workers’ Compensation costs can best be projected by reviewing current policies and past history.

Other expenditures that districts should take into consideration include fuel and energy costs and contractual payments due to employees in the upcoming year for compensated absences, retirement, or separation from service.

Appropriations for Contingencies

Because budgeting is not an exact science, most local governments are authorized to include an amount in their budget for unforeseen circumstances. This amount is referred to as the contingency account and is subject to limitations established by various laws. No direct expenditure can be charged to this account. Instead, the balance is transferred to other appropriation accounts that are at risk of becoming overdrawn as needed. A breakdown of contingency limits by type of local government is included in Appendix C.

Revenue Estimates

The budget officer and the designated board officer, in consultation with appropriate personnel, will have the task of forecasting many of the revenue estimates. For this reason, knowledge of the local economy, State and federal aid programs, contracts with other governments, and any other information on revenue generation is essential. With current and accurate information from these key sources and an understanding of the nature of the district’s revenues, the budget officer can develop realistic estimates. In addition, officers should provide estimates of revenue derived from the activities of their departments to help in the budget process.

The process of estimating revenues usually begins with a historical analysis. Looking at revenues over time often is a fair indicator of future results, a three- to five-year period is usually sufficient. The district should be able to provide accurate historical data to start the estimating process. In addition, accurate year-to-date numbers with estimates to year end are necessary for the process.

Non-Property Taxes Non-property taxes, such as sales and use taxes, utility gross receipts taxes, mortgage recording taxes, and various other relatively volatile taxes are difficult to predict. Although rates rarely change, the revenue base can be highly erratic. Many of these items are based on consumer usage and therefore dependent on the state of the local, regional, and national economies. Past experience can provide some guidance, but current and future economic trends are better to use in estimating these revenues.

Ambulance User Fee Income Ambulance user fee income generally involves fees charged to patients for various services provided and should be included in the revenue estimates received from the billing supervisor. These revenues can be significant, although user fee revenue is based on consumer demand for the applicable service and the district’s ability to supply it. Consumer demand may fluctuate based on current economic conditions as well as the quality of the services provided. Past trends can provide useful data and the billing supervisor predictions are also helpful. Changes in fee schedules should also be considered, particularly if the services are intended to be self-sustaining. Any changes in local conditions may also impact these revenue items.

Use of Money and Property This category includes interest earnings on investments and income from rental property or equipment. Estimated interest earnings should be based on current yield rates and expected investment amounts. Estimated rental income should be based on rental agreements.

Sale of Property and Compensation for Loss These revenues are highly volatile. Amounts received can range from insignificant to substantial. The good news is that they are relatively controllable by the district. Minor sales of unneeded

supplies and equipment are generally not significant, while sales of unneeded land or buildings can generate significant revenues. The selling price and the timing of the sale can often be negotiated. The budget officer should confirm sales information. Generally, insurance recoveries for damage to property are not included in the initial budgets because the losses are usually sustained from unexpected events. For the district, the proceeds may be appropriated to repair or replace the loss when the money is received. Because of the sporadic nature of this class of revenues, care should be taken when budgeting for them. These one-time revenues, particularly larger amounts generated from the sale of real property, should not be used to finance day-to-day operations. Instead, they should be restricted to one-time expenditures, such as capital acquisitions or contributions to debt reduction. In some cases, the amounts may be required to be restricted for debt service or other specified uses.

Miscellaneous Miscellaneous revenues include refunds of prior year expenditures, gifts and donations, and certain other revenues not classified elsewhere. Generally, such revenues are insignificant and vary from year to year. Reviewing and identifying amounts realized in prior years can also be helpful.

Interfund Transfers Interfund transfers represent contributions of resources from one fund to another, generally for expenditure in the receiving fund. These operating transfers, although included in estimated revenues, are considered a financing source. Transfers should be based on management’s decisions and be within applicable legal authority. They should be easily quantified for budgetary purposes. In total, transfers in should equal transfers out. When budgeting for these revenues, keep in mind that taxpayer equity and fairness should be maintained when applicable, and that not making approved transfers can have negative financial consequences for the intended receiving fund.

When estimating revenue, conservatism is the key. It is far better to underestimate a particular revenue by a small amount, than to plan on a revenue that does not materialize.

Estimates of Available Fund Balance

Another important financing source for the annual budget is available fund balance. The key to using this as a funding source is the proper estimation of its value. At budget time, the challenge for the district budget officer is to calculate year-end fund balance months in advance.

The calculation of year-end fund balance is as follows: start with fund balance at the beginning of the year, add revenues to date, and subtract expenditures to date. This calculated amount represents the fund balance as of the last completed month. To this amount, add projected revenues and subtract projected expenditures for the remainder of the fiscal year. The final figure is a reasonable estimate of fund balance available at year-end. The same procedure should also be used to determine the amount of any reserve balances available at year-end for each applicable fund.

Real & Personal Property Taxes

The final piece of the budget process, the piece often generating the most interest to governing board members and taxpayers alike, is the determination of the amount of real & personal property taxes that will be necessary to balance the budget. A balanced budget is intended to ensure that the district does not spend beyond its means. At this point, a preparation of a preliminary tax rate summary (Pro Forma) is completed and submitted to the County Clerk.

The amount to be raised by taxation is called the tax levy. In general, the amount of the tax levy is raised by computing a tax rate and then applying that tax rate to the assessed value of real property subject to taxation. The tax rate is computed by dividing the amount of the tax levy by the total taxable assessed value of the real and personal property, and is usually expressed as an amount per thousand dollars of assessed value. The taxable assessed value of most types of real property is determined by the Jefferson County Assessor. The basic formula for the tax levy is as follows:

General Tax Levy (2013) is assessed at a rate of .04947 per $100 of assessed valuation (total proposed tax would be $1,630,309.08). This will be for the 2013-2014 fiscal year General Revenue Budget.

Pension Tax Levy (2013) is assessed at a rate of .00500 per $100 of assessed valuation (total proposed tax would be $164,777.55. This will be for the 2013-2014 fiscal year Pension Budget.

Implementing the Budget

Once the budget has been adopted there must be a systematic accounting process in place to determine that sufficient revenues are realized and money is available for expenditure for each purpose enumerated in the budget. Without properly accounting for revenues and expenditures, officials cannot be reasonably assured that the budget that they approved is, in fact, being complied with.

Listed below are recommended accounting procedures and, in some cases, legal requirements for implementing the budget. These may not be applicable to all local entities:

• A separate account should be kept for each appropriation showing the amount appropriated, the amount encumbered, the amounts expended, and the unencumbered balance.

• A separate account should be kept for each revenue item showing the amount estimated to be earned and recognized as revenue, the actual amounts recorded to date, and the balance expected to be realized.

• As a rule, no expenditure may be made, or any liability incurred, unless an amount has been appropriated for the particular purpose and is available or is authorized to be borrowed pursuant to the Local Finance Law.

• Whenever it appears that resources will not be sufficient to meet appropriations, the budget officer should notify the governing board stating the probable amount of the deficiency. The budget officer should provide recommendations regarding possible actions to be taken.

• If, during the fiscal year, the governing board determines that sufficient revenues will not be generated to finance the total appropriations provided for in the original budget, the governing board generally may reduce appropriations to prevent making expenditures in excess of money available. An appropriation may not be reduced below the minimum amount required by law, nor generally be reduced by more than the unexpended balance less outstanding and unpaid claims chargeable to it.

• As a general rule, the governing board may make supplemental appropriations. These may be provided by transfer from the unexpended balance of an appropriation, from the appropriation for contingencies within a fund, or by borrowing pursuant to the Local Finance Law. For towns, villages and counties, the unappropriated, unreserved fund balance may be utilized for this purpose only to the extent that the total of all revenues of a fund, recognized or reasonably expected to be recognized in the current fiscal year, together with unappropriated, unreserved fund balance, exceeds the total of all revenues of the fund and appropriated fund balance as estimated in the budgets.

• Under certain statutes, the governing board may appropriate certain revenues that were not included in the original budget at any time for the applicable objects or purposes. These revenues include grants received from the State and federal governments, gifts that are required to be expended for particular objects or purposes, and certain insurance proceeds.

Monitoring the Budget

After the budget has been approved, it is generally the responsibility of the governing board, budget officer, and department heads to see that services are delivered within the limits provided in the budget. They should closely monitor the progress of actual revenues and expenditures throughout the year, and identify any variances that might cause the district to end the year with a significant surplus or deficit.

The preparation of budget reports facilitates the monitoring of the adopted and amended budget. A budget report shows the original budget, any authorized amendments, actual transactions to date (i.e., revenues, expenditures, and encumbrances listed by account code) and the differences between the amended budget and actual transactions (shown as variances). Budget reports should be prepared and reviewed as of the end of each month during the fiscal year. The reports can also be enhanced with information that compares the amended budget to a projected estimate of actual revenues and expenditures through the end of the year. These projections can be prepared using historical data from prior years, quarterly estimates contained in the original budget, input from department heads, or any other relevant and reliable information.

The budget officer can also prepare a narrative explaining the numbers in the budget report and recommending corrective actions if shortfalls are indicated. By using these reports, the board of directors can identify financial trouble spots in advance. Such reports also help them to assess the performance of departments and activities. To help monitor the progress of individual departments, it might also be desirable to develop quarterly expenditure plans for major departments based on the department’s budget and historical patterns.

The timely detection of projected budget shortfalls allows actions to be taken early to address the shortfall, when only relatively small adjustments may be required. Waiting until the close of year, after the situation has deteriorated significantly, can result in the need to take more drastic action with fewer options available. Timely detection can also lead to the taking of appropriate action in the succeeding year’s budget if the shortfall is seen to be an ongoing problem and not just a temporary situation.

The following actions (although not appropriate for all entities) should be considered if a problem arises:

• Transfer between appropriations, where appropriate • Use of contingency funds, where allowed • Appropriation of fund balance, when appropriate • Use of budget notes

Conclusion

A significant amount of time and effort is expended in preparing the annual budget. It is often a very busy and stressful time. Often, computer-generated information is used. Although technology is ever evolving, it is still prudent to double check the numbers that you are presenting. For example, sit and read the final document to see if it makes sense. Then, get an adding machine and manually add the columns and the rows—making sure that the final product is accurate, realistic and makes sense. The additional effort spent on preparing an accurate and realistic budget generally reduces the risk of having to make adjustments later in the year or in future years.

Appendix A – Budget Officer Designation

Appendix B – Budget Calendar

Appendix C – Terminology

Appendix A Missouri Revised Statutes Chapter 67 Political Subdivisions, Miscellaneous Powers Section 67.020 Budget officer, designation, duties--submission of budget.

67.020. 1. The budget shall be prepared under the direction of a budget officer. Except as otherwise provided by law, charter, or ordinance, the budget officer shall be designated by the governing body of the political subdivision. All officers and employees shall cooperate with and provide to the budget officer such information and such records as he shall require in developing the budget. The budget officer shall review all the expenditure requests and revenue estimates, after which he shall prepare the proposed budget as defined herein.

2. After the budget officer has prepared the proposed budget, he shall submit it, along with such supporting schedules, exhibits, and other explanatory material as may be necessary for the proper understanding of the financial needs and position of the political subdivision, to the governing body. He shall submit at the same time complete drafts of such orders, motions, resolutions, or ordinances as may be required to authorize the proposed expenditures and produce the revenues necessary to balance the proposed budget.

Appendix B – Budget Calendar

The budgeting process takes several months so the Budget Calendar summarizes the schedule of critical due dates. January 15 Conflict of Interest Resolution updated March 1 Distribution of Budget Calendar March 5 Financial status meeting with Budget

Committee to discuss budget goals March 12 Meeting to discuss and distribute

assignments with to Officers March 9 Contract negotiation meeting April 9 Assignments due from Officers April 16 Meeting of Budget Committee to

discuss and review specific budget needs

May 1 Financial disclosure reports due to Ethics Commission

May 7 Draft budget completed and distributed to Board of Directors

May 15 Budget Workshop with Board of Directors

June 15 Preliminary budget completed and distributed to the Board of Directors & Budget Committee

August 18 Set property tax levy (Due by September 1)

September 8 Proposed 2014-2015FY Budget presented to Board of Directors

September 12 Proposed 2014-2015FY Budget presented to public

September 15 Adoption of Proposed 2014-2015FY Budget at Board Meeting

October 20 Final Public Hearing and Adoption of Proposed 2014-2015FY Budget

Appendix C – Terminology

The following explanations are presented to aid in understanding the terminology generally used in governmental accounting, auditing, financial reporting and budgeting.

Term Definition Appropriations

An allocation or designation of money by the governing board to be spent on a particular type of item. Appropriations are often referred to as expenditure line items in the annual budget.

Appropriated Fund Balance The portion of fund balance estimated to be available that is designated to help finance operations of that fund for the subsequent year.

Appropriated Reserves The portion of amounts reserved for stated purposes estimated to be available and designated to finance specific, authorized budgetary appropriations.

Assessed Value The estimated value of property for tax purposes. Assessed value is approximately equal to market value, ideally within 10%.

Budget A plan of financial activity for a specified period of time indicating all planned revenues and expense for the period.

Budget Calendar The schedule of key events or dates which a government follows in preparation and adoption of the budget.

Estimated Revenues All sources of funds estimated to be earned and recognized as revenue during a fiscal year to finance appropriations contained in the annual budget.

Cash Basis of Accounting A basis of accounting in which transactions are recognized only when cash is increased or decreased.

Current Budget Year The budget year in which a local government is operating.

Ensuing Budget Year The next upcoming budget year that runs from November 1 to October 31. Also known as the “incoming” budget year.

Fiscal Body Local government council or board. The body with budget approval authority.

Fiscal Year One complete 12-month cycle of financial activity. For towns, most counties, and most cities, the fiscal year coincides with the calendar

year, January 1st to December 31st. For our District, the fiscal year begins November 1st and ends October 31st.

Fund A set of self-balancing accounts containing both revenues and expenses that are segregated for the purpose of carrying out a specific purpose or activity.

Fund Balance The excess of cash and investments attributed to a fund over that funds liabilities and obligations.

General Fund The fund used to account for all revenues and expenditures applicable to the general operations of the government that are not required to be accounted for in another fund.

Levy The amount of revenue generated by a tax rate. Also, the amount of tax charged by a government.

Reserve A reserve account where budget surpluses can be transferred from undedicated funds so the funds are held for future purposes.

Tentative/Proposed Budget The budget as prepared by the budget officer and initially presented to the governing board.

Unappropriated Unreserved Fund Balance A portion of fund balance that is not reserved or appropriated to finance operations of that fund in the subsequent year.

Budget and Financial Policies Introduction North Jefferson County Ambulance District functions under Missouri Revised Statutes, Chapter 190, as a political subdivision of the State of Missouri. The District provides basic and advanced life support emergency medical services as well as public education to the community.

The 2014-2015FY budget has been prepared after analyzing, evaluating, and justifying requests from all departments. The District maintains budgetary controls to ensure compliance with legal provisions embodied in the appropriated budget approved by the District’s Board of Directors. The level of budgetary control (that is, the level at which expenditures cannot legally exceed the appropriated amount) is at the fund level. There is flexibility in the use of monies within various line items, so long as the total appropriated at the fund level is maintained. During the year, revenues and expenditures are closely monitored to ensure compliance with the adopted budget and state law. Monthly budget comparisons are distributed to management and the Board of Directors. Annually, an audit is performed by an independent certified public accountant. Fund Accounting The accounts of the District are organized on the basis of funds. A fund is an independent fiscal and accounting entity with a self-balancing set of accounts. Fund accounting segregates funds according to their intended purpose and is used to aid management in demonstrating compliance with finance related legal and contractual provisions. The District has adopted a budget for the following major governmental funds: The General Fund – This is the District’s primary operating fund, which accounts for all the financial resources and the legally authorized activities of the District except those required to be accounted for in other specialized funds.

The Pension Fund- The District uses this fund to account for property taxes that are assessed specifically for the payment of employee retirement funds

Revenue Projections Property Taxes Approximately 57% of the District’s general fund revenue is comprised of property taxes. The District is subject to Missouri State Hancock Amendment. The amendment limits the rate of increase and the total amount of taxes on property which may be imposed in any year without voter approval. If the assessed valuation of property, excluding the value of new construction and improvements, increases by a larger percentage than the increase in the general price level from the previous year, the maximum authorized current levy must be reduced to yield the same gross revenue from existing property, adjusted for changes in the general price level, as could have been collected at the existing authorized levy on the prior assessed value. Conversely, if assessed

valuation decreases, then the property tax rate may increase (up to the maximum levy allowed by law) in order to yield the same gross revenue from existing property. State law also dictates that the assessor shall annually assess all real property in the following manner: new assessed values shall be determined in each odd-numbered year; those same assessed values shall apply in the following even-numbered year, except for new construction and property improvements which shall be valued as though they had been completed in the preceding odd-numbered year.

Year Total Real Total Personal Total Combined Aggregate

2007 242,903,764 76,811,856 $319,717,627

2008 250,781,259 79,165,809 $329,949,076

2009 254,644,492 74,578,102 $329,224,603

2010 259,334,604 70,638,036 $329,974,650

2011 259,607,597 74,089,236 $333,698,844

2012 261,408,971 73,693,380 $335,104,363

2013 266,381,378 73,553,883 $339,937,274

2014* 269,601,656 69,406,198 $335,538,253

The District’s combined tax rate for the past ten years is as follows:

Year General

Fund Tax Rate

Property Tax

Revenues

Pension Fund Tax Rate

Pension Tax Revenues

Net Ambulance Revenues

2005 $0.3947 1,253,707 $0.050 416,163

2006 $0.4447 1,445,965 $0.050 429,319

2007 $0.4947 1,738,915 $0.048 480,510

2008 $0.4947 1,647,349 $0.048 159,840 447,918

2009 $0.4947 1,620,609 $0.0489 159,201 535,415

2010 $0.4947 1,645,953 $0.0489 160,884 561,856

2011 $0.4947 1,643,876 $0.0493 160,321 591,025

2012 $0.4947 1,668,169 $0.0494 166,085 659,877

2013 $0.4947 1,658,298 $0.050 168,0634 516,820 (625,000)

2014 (estimated) $0.4932* 1,671,987 $0.0498* 168,326 625,000*

Ambulance User Fee Income For 2014-2015, there will be no increase in rates. In addition, the 2014-2015 budget reflects a 0% increase in billable call volume for expected emergency calls. Therefore, it is not expected to have an impact on the ‘net’ ambulance fees for 2014-2015.

Ambulance rates charged by the District including Medicare and Medicaid reimbursement rates are as follows:

District

Ambulance Rate

Medicare Allowable

Medicare Adjustmen

t

Medicaid Allowable

Medicaid Adjustmen

t

Resident Rates (Emergency) Basic Life Support $ 600.00 $ 346.37 $ 253.63 $ 147.52 $ 452.48 Advanced Life Support $ 750.00 $ 411.31 $ 338.69 $ 239.79 $ 510.21 Advanced Life Support Level 2 $1,000.00 $ 595.32 $ 404.68 $ 208.89 $ 791.11 Mileage-Per Loaded Mile $ 7.50 $ 7.16 $ 0.34 $ 3.50 $ 4.00

Non-Resident Rates (Emergency) Basic Life Support $ 800.00 $ 346.37 $ 453.63 $ 147.52 $ 652.48 Advanced Life Support $ 950.00 $ 411.31 $ 538.69 $ 239.79 $ 710.21 Advanced Life Support Level 2 $ 1,200.00 $ 595.32 $ 604.68 $ 208.89 $ 991.11 Mileage-Per Loaded Mile $ 9.00 $ 7.16 $ 1.84 $ 3.50 $ 5.50

Other Rates Non-covered mileage $ 9.00 $ 0.00 $ 9.00 $ 0.00 $ 9.00

PCR Duplication Fees $ 21.36

PCR Copy Fee Per Page $ 0.50

PCR Notary Fee $ 2.00

Other Revenue This category includes interest earnings on investments and income from sale of property or equipment. Estimated interest earnings should be based on current yield rates and expected investment amounts. Estimated sale of property or equipment is based on submitted proposals.

Cash Management and Investing The District maintains separate accountability by fund for cash and investment accounts. In accordance with District policy, the District’s Chief Financial Officer is authorized to invest funds which are not immediately needed, in obligations of the United States Treasury, United States Government Agencies and Instrumentalities, Repurchase Agreements, and Certificates of Deposit.

Financial institutions are required to fully collateralize deposits with federal depository insurance and/or securities pledged to the District. As a means of managing exposure to fair value loss arising from increasing interest rates, the District’s governmental funds investment policies limit maturities to 12 months or less.

Budgeted Expenditures

General District Operations 366,400

Building/Grounds 56,663

EMS Operations 51,150

Personnel Wages & Benefits 1,765,986

Public Relations 13,700

Vehicle Operations 74,138

Total Expenditures: 2,328,037 General Operations The 24% increase in GO costs for 2014-2015 relates primarily to changes in Service Agreements and IT Maintenance/Support. The Billing staff will be implementing a patient portal that patients will have secure online access to paying their bills as well as added functionality for the billing staff. In 2015, the District has two possible board member seats open in April. The District is responsible for paying the Jefferson County Election Authority to hold these elections and the estimated cost for 2015 is $18,000 (up from $15,258 in 2014). The District will be adding a Breach Insurance for 2015 and received a discount for completing additional training. Capital Purchases/Expenditures Capital assets are defined by the District policy as assets with an initial individual cost of $5,000 or more and an estimated useful life in excess of one year. These capital expenditures are budgeted in the General Fund. The cost of normal replacement, maintenance and repairs that is less than $5,000 and does not add to the value of the asset or materially extend the asset’s life is not capitalized. Major capital expenditures for 2014-2015 include the following: one ambulance is due for remount. A remount is the process of removing the box from an existing ambulance and putting a new chassis underneath. $126,893.50 has been allocated for this line item. $50,000 has been allocated for the purchase of a new 6800 vehicle and $53,441 allocated for contingency. Building and Grounds Building and Grounds expenditures include insurance, utilities as well as the replacement and/or repairs of buildings, furniture and certain equipment. These accounts also include

$3,000 for supplies relating to the general operations and upkeep of District facilities (i.e. toiletries, consumables, cleaning supplies, insecticides, etc.). Major repairs budgeted for 2014 include the following: nothing scheduled at this time. EMS Operations Total EMS Operations expenditures are budgeted at $51,150 of which patient medical supplies comprise $39,800 (or 78%) and the repair and replacement of medical equipment maintenance and repairs comprise $6,000 (or 12%). This year’s budget also includes $0.00 in contingency for radio equipment/programming or replacement of medical equipment..

Personnel Wages and Benefits Wages and Benefits comprise 61% of the District’s total operating expenditures. Being in the service industry, the District’s primary expenditures are wages and benefits. The District currently employs 16 full-time employees and 23 part-time employees, of which 33 are licensed paramedics. The District currently operates and staffs 3 ambulances (no changes have been made since 2008). Due to budget constraints, the District has no plans for additional staffing during 2015. In addition, the one Assistant Chief vacancy will not be filled at this time. The full-time paramedics and office staff are members of the International Association of Firefighters Local 2665. The District has entered into labor agreements covering the period May 21, 2013 through May 21, 2016. The labor agreements cover the District’s full-time paramedics and the three administrative staff positions. As of September 4, 2014 there have been no meetings with labor to discuss any changes to existing agreements. Until such time as a new agreement is reached, the current agreement shall remain in effect. The 2014-2015FY budget reflects a 1.5% COLA increase to existing wages and benefits. The District’s group insurance (health, dental, vision, life, and disability) is due for renewal on November 1, 2014. The budget reflects a 4% increase in health insurance, a 12% increase in disability insurance, and a 12% increase in all other lines. The amount budgeted for group insurance anticipates changes in individual elections, as well as the increase in premium. Education and Training As mentioned previously, the District provides education and training to its employees as well as to citizens of Jefferson County and surrounding communities. The cost of holding classes includes several types of expenditures which are budgeted in the Education and Training category, except for teaching and training wages which are budgeted in wages and benefits. Classes, trainings and conference fees are the most expensive costs of the programs at $17,922 (or 53% of the total education and training expenditures). The next highest are Education Allowance at $9,500 (or 28%). Public Relations Public Relations line items cover public relations expenses, community education, staff recognition and community newsletters. Programs include our VIAL of Life program, car seat installations, community movie nights, helmet fittings, Halloween glow bracelet program, and other brochures and handouts. Total Public Relations expenditures for 2014 are $13,700.

Vehicle Operations The District relies on an outside service center for maintaining its fleet of vehicles. Vehicle Operations expenditures are projected at $74,138 and include all purchases of goods and services related to maintaining our fleet. Maintenance and Repairs are budgeted at $30,000 and comprise 40% of the total vehicle operations cost with fuel costs also totaling $30,000 (or 40%). The next highest line item is insurance premium at 7,838 for 2015.

2012-2013 Fuel by Unit Unit Net Cost Gallons

6800 $2,845.15 811.027 6802 $990.29 303.965 6817 $8,370.79 2432.047 6827 $3,894.75 1137.343 6837 $7,666.84 2232.731 6847 $5,222.32 1505.939 Total $28,990.14 8,423.052

Vehicle Number

Service Budgeted

Chassis Year & Make

Box Year, Type & Mfr

Current Miles

Budgeted Amount Disposition

6827 Remount 2006 Ford 2005 Type II Medtec

113,597 $126,893.50 Retire chassis

6817 None 2007 Ford 2005 Type II Medtec

88,300 $ -

6837 None 2012 Ford 2006 Type II Medtec

30,743 $ -

6847 None 2012 Ford 2006 Type II Medtec

88,335 $ -

6802 Replacement 2007 Ford Crown Victoria

N/A $ - Sale and replace with 2006 Silverado

6800 Replacement 2006 Chevrolet Silverado

N/A 113,792 $50,000.00 Replacement in

2013-2014FY

$126,893.50

Nov '14 - Oct 15Ordinary Income/Expense

IncomeBeginning Fund Balance 665,250REVENUES 2,301,837OTHER FUNDING SOURCES 1,200

Total Income 2,968,287

Gross Profit 2,968,287

ExpenseGENERAL DISTRICT OPERATIO... 366,400BUILDING/GROUNDS 56,663EMS OPERATIONS 51,150PERSONNEL WAGES & BENEFI... 1,765,986PUBLIC RELATIONS 13,700VEHICLE OPERATIONS 74,138Ending Fund Balance 515,250Reserve Operating Funds 125,000

Total Expense 2,968,287

Net Ordinary Income 0

Net Income 0

1:56 PM North Jefferson County Ambulance District10/09/14 BudgetCash Basis November 2014 through October 2015

Page 1

Nov '14 - Oct 15Ordinary Income/Expense

IncomeBeginning Fund Balance 665,250REVENUES

Ambulance Net Income 625,000Education and Training Fees 3,300Interest Income 1,500Sale of Bicycle Helmets 50Taxes 1,671,987

Total REVENUES 2,301,837

OTHER FUNDING SOURCESGrant Funding 0Proceeds from Insurance 0Proceeds from Sale of Assets 1,200

Total OTHER FUNDING SOURCES 1,200

Total Income 2,968,287

Gross Profit 2,968,287

ExpenseGENERAL DISTRICT OPERATIONS

Administrative CostsEquipment 500Licensing/Professional Fees 0Phone System Maint/Programming 500Postage 3,126Service Agreements 4,500Supplies 2,500

Total Administrative Costs 11,126

Capital Purchases 230,334Computer/IT

Equipment Replacement/New 2,000IT Maintenance/Support 44,814

Total Computer/IT 46,814

Election of Board Director(s) 18,000Employer Liability Insurance 10,987Grant Allocation 0Lease Payments 0Professional Services

Accounting Services 10,275

1:56 PM North Jefferson County Ambulance District10/09/14 BudgetCash Basis November 2014 through October 2015

Page 1

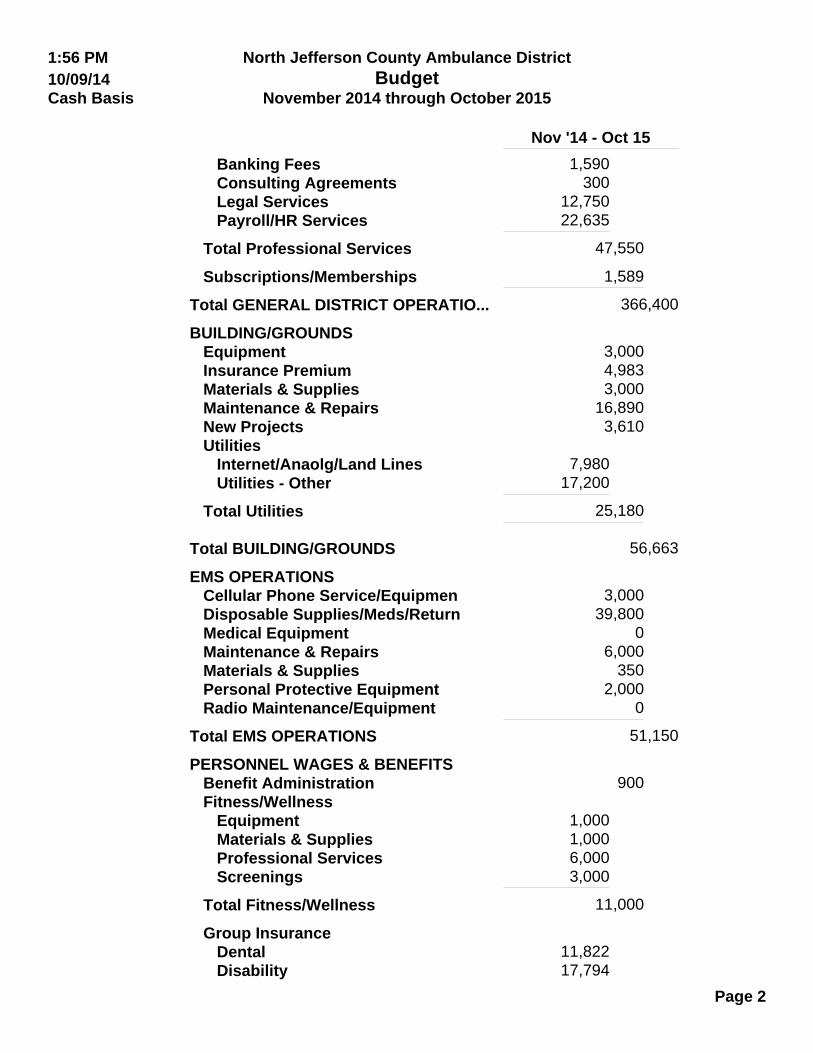

Nov '14 - Oct 15Banking Fees 1,590Consulting Agreements 300Legal Services 12,750Payroll/HR Services 22,635

Total Professional Services 47,550

Subscriptions/Memberships 1,589

Total GENERAL DISTRICT OPERATIO... 366,400

BUILDING/GROUNDSEquipment 3,000Insurance Premium 4,983Materials & Supplies 3,000Maintenance & Repairs 16,890New Projects 3,610Utilities

Internet/Anaolg/Land Lines 7,980Utilities - Other 17,200

Total Utilities 25,180

Total BUILDING/GROUNDS 56,663

EMS OPERATIONSCellular Phone Service/Equipmen 3,000Disposable Supplies/Meds/Return 39,800Medical Equipment 0Maintenance & Repairs 6,000Materials & Supplies 350Personal Protective Equipment 2,000Radio Maintenance/Equipment 0

Total EMS OPERATIONS 51,150

PERSONNEL WAGES & BENEFITSBenefit Administration 900Fitness/Wellness

Equipment 1,000Materials & Supplies 1,000Professional Services 6,000Screenings 3,000

Total Fitness/Wellness 11,000

Group InsuranceDental 11,822Disability 17,794

1:56 PM North Jefferson County Ambulance District10/09/14 BudgetCash Basis November 2014 through October 2015

Page 2

Nov '14 - Oct 15Medical 150,000Pharmacy 28,638Vision 2,449

Total Group Insurance 210,703

Professional HealthMedical Claims >1000 2,000Immunizations/Drug Testing 4,000

Total Professional Health 6,000

Recuitment/Procurement 5,000Training & Education

Classes /Trainings/Conferences 17,922Education Allowance 9,500Equipment 800Materials & Supplies 450Meal Service 0Travel 5,257

Total Training & Education 33,929

Wages & BenefitsBoard Director Reimbursement 3,000Duty Pay 6,240FICA Tax 95,570Holiday Pay 4,500Longevity 19,600Trainings/Meetings 23,971Teaching Overtime 4,008Uniform Allowance 12,600Wages (FT) 988,701Wages (PT) 203,264Workers Compensation 137,000

Total Wages & Benefits 1,498,454

Total PERSONNEL WAGES & BENEFI... 1,765,986

PUBLIC RELATIONSEducation/Training 500Community Outreach 5,800Materials & Supplies 3,800Staff Appreciation/Recognition 3,600

Total PUBLIC RELATIONS 13,700

VEHICLE OPERATIONS

1:56 PM North Jefferson County Ambulance District10/09/14 BudgetCash Basis November 2014 through October 2015

Page 3

Nov '14 - Oct 15Equipment 6,000Fuel 30,000Insurance Premium 7,838Maintenance & Repairs 30,000Materials & Supplies 300

Total VEHICLE OPERATIONS 74,138

Ending Fund Balance 515,250Reserve Operating Funds 125,000

Total Expense 2,968,287

Net Ordinary Income 0

Net Income 0

1:56 PM North Jefferson County Ambulance District10/09/14 BudgetCash Basis November 2014 through October 2015

Page 4

Nov '14 - Oct 15 Budget $ Over Budget

IncomeTaxes, penalties & interest 0.00 168,825.91 -168,825.91

Total Income 0.00 168,825.91 -168,825.91

ExpenseAdministrative Fees 0.00 500.00 -500.00

Total Expense 0.00 500.00 -500.00

Net Income 0.00 168,325.91 -168,325.91

2:34 PM North Jefferson County Ambulance District-Pension09/09/14 Profit & Loss Budget vs. ActualAccrual Basis November 2014 through October 2015

Page 1