north carolina community health center association march 3, 2011 michael holton manager...

TRANSCRIPT

Budgeting, Grants Management, and Cost Allocation

Michael HoltonManagerRSM McGladrey, [email protected]

To enhance participants’ knowledge of the grant requirements of community health centers from federal, state and other funding agencies.- Grant Revenue

- Contract Revenue

The Session Will Discuss Issues Related to:- Budgeting,

- Maximization of Grant Funding, and

- Reporting / Filing Issues

GOALS

Session Goals

DHHS GRANT REVENUE CYCLE

UDS

NGAFSR

Budget

Establishing a Grant File

Each health center should establish, maintain and, as necessary (at a minimum, on a yearly basis), update a centrally located corporate file in which the health center stores documents related to compliance with all grant requirements

- Application and Notice of Grant Award (NGA)

- HRSA/BPHC correspondence, including responses to special conditions and letters from the project officer and/or grants management

- HRSA Performance Review, JCAHO, other site review reports

- Financial Status Report (FSRs)

- Semi-annual Reports (SARs)

- Audit reports

Establishing a Grant File

Institutional file, that includes –

- Grant-related laws, regulations and policies• Grant enabling statute: Section 330 of the Public Health

Service Act (42 USC 254b), as amended by Public Law 107-251 (October 26, 2002)

• DHHS line item appropriations• Program specific regulations: 42 CFR Part 51c (community

health centers) and 42 C.F.R. Part 56 (migrant health centers)• DHHS administrative regulations: 45 C.F.R. Part 74,

incorporating OMB Circulars A-110 (as set forth in 2 CFR Part 215) and A-122

• OMB Circular A-133 – Federal Audit Guidance • PHS policies (e.g., PHS Grants Policy Statement)

Establishing a Grant File

Applicable PINs and PALs- PIN #2004-22: Service Area Competition (project

renewal)- PIN #2004-19: Non-competing Continuation (budget

renewal)- PIN #2002-01: Unified NGA for Health Center Cluster

Programs - PIN #2002-07: Scope of Project Policy- PIN #98-23: Health Center Program Expectations- PINs #97-27 & 98-24: Affiliation Policies- PAL #2005-03: Accreditation Initiative

Establishing a Grant File

Applicable PINs and PALs (cont.)- PIN #2002-18: Creating a Financial Recovery Plan- PIN #95-15: Application of Federal Cost Principles- PIN #95-02: Payment of Membership Dues to

Professional Organizations- PIN #94-34: Guidance Regarding the Implementation

of 1992 Amendments to Sections 329 and 330 of the Public Health Service Act

- PAL #99-14: Community Centers – A Review of Literature

Website: www.bphc.hrsa.gov/pinspals

Establishing a Grant File

Institutional file (cont.)- Other Federal, State and local laws

- Documents related to the internal operations of the health center• Articles of Incorporation• Bylaws• Mission statement and internal policies and

procedures • Terms and conditions of agreements between

health center and third parties

Your Key Federal Players

Establish a Meaningful and Working Relationship

• Program issues:• Assigned HRSA Project Officer

• Budget Information and other Grants Management requirements• Assigned Grants Management Specialist• Refer to attachment pages of the Notice of

Grant Award

Key Federal Contacts

Project Officer

The Project Officer, in most cases, serves as the first point of contact

• Has Federal program oversight responsibilities of the HRSA grant

• Reviews and make recommendations on continued Federal support

• Clarifies program guidance and program expectations

Grants Management Specialist

The assigned Grants Management Specialist, working in conjunction with the Project Officer, serves as the business management contact for the grant

• Reviews and make recommendations on continued federal support

• Clarifies grants regulations and requirements• Monitors compliance with grant requirements and releases

conditions of award• Issues Notices of Grant Award

Single Grant Application

Grant Application Budgeting

Preparation of Budget(s):- Departmental

- Organization-Wide

Justification of Budget Items (revenue and expenses)

Preparation of Budget Forms:- BPHC Funding Request Summary

- Standard Form 424A

- Income Analysis Format

- Personnel by Position and BPHC Program

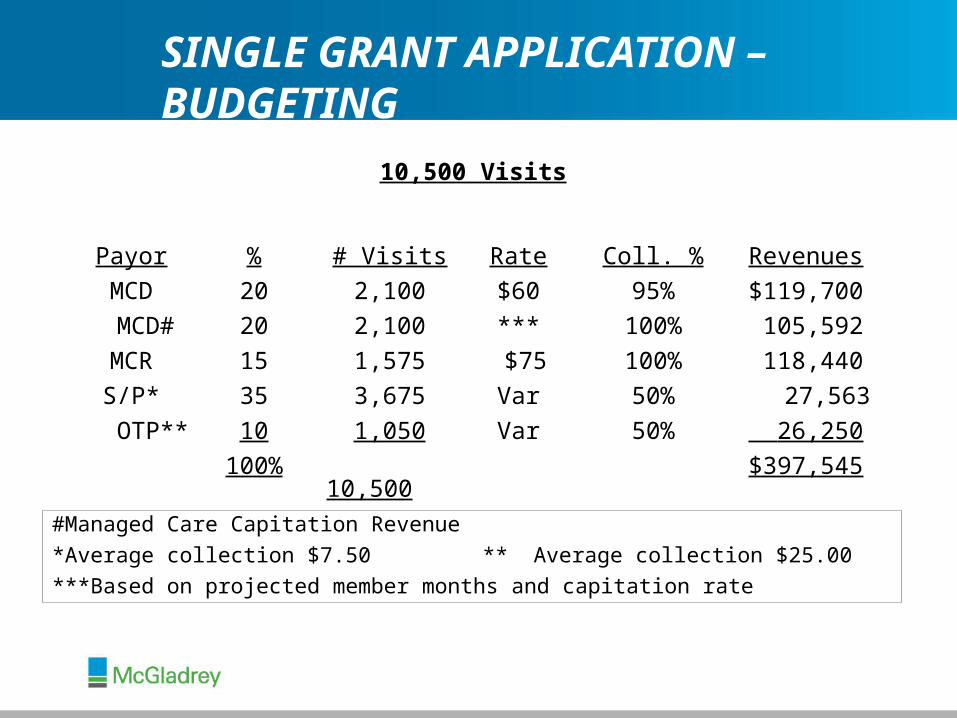

SINGLE GRANT APPLICATION – BUDGETING

Staffing Budget:- Consider:

Þ Current Payroll RegisterÞ New Program or Site Expansion

- Need Salary Cost and FTE DetailÞ Provider Versus Non-Provider Staff

- Staffing Assists in the Budgeting of Various Expenses and Visits

SINGLE GRANT APPLICATION – BUDGETING

Sample Staffing BudgetEmployee Name Position FTE SalaryDr. Steven Smith Internist 1.00 $100,000Dr. Bob Scott Internist 1.00 110,000Peggy Sue Nurse Prac. 1.00 75,000John Cooper Cashier 1.00 22,000Marie Ryan Data Process. 1.00 25,000John Schwartz Executive Dir. 1.00 125,000Steve Johnson Controller 1.00 75,000Caroline Hudson Accountant 1.00 35,000Total $567,000

SINGLE GRANT APPLICATION – BUDGETING

Calculation of Projected Visits

Estimated BudgetedEmployee Position FTE Productivity Visits

Dr. S. Smith Internist 1.00 3,950 3,950

Dr. Bob Scott Internist 1.00 3,950 3,950

Peggy Sue Nurse Prac. 1.00 2,600 2,600

Total Visits 10,500

SINGLE GRANT APPLICATION – BUDGETING

Expenditures: Review Prior Year Audited Financial Statements Review First 6 Months’ Internal Financial Statement Base Expenditures on First 6 Months’ Financial

Statement:

- Compare to Prior Year for Major Differences Þ Reconcile

- Increase or Decrease Appropriate Cost Due to Visit Volume Variance

- Increase or Decrease Due to Unit Cost Differences

SINGLE GRANT APPLICATION – BUDGETING

Budgeting of Expenditures

Salaries = Staffing Plan (FTEs)

Fringe benefits = Percent of Salaries and Wages

Supplies = Based on Visits

Rent = Based on Current Leases

Interest = Based on Current Loan Payments

SINGLE GRANT APPLICATION – BUDGETING

Budgeting of Expenditures

Salaries = $ 567,000

Fringe Benefits (25%) = 141,750

Supplies ($10 per visit) = 105,000

Rent = 75,000

Interest = 50,000

Other = 203,240

Total Expenses $1,141,990

SINGLE GRANT APPLICATION – BUDGETING

10,500 Visits

Payor

MCD

MCD#

MCR

S/P*

OTP**

%

20

20

15

35

10

100%

# Visits

2,100

2,100

1,575

3,675

1,050

10,500

Rate

$60

***

$75

Var

Var

Coll. %

95%

100%

100%

50%

50%

Revenues

$119,700

105,592

118,440

27,563

26,250

$397,545

#Managed Care Capitation Revenue

*Average collection $7.50 ** Average collection $25.00

***Based on projected member months and capitation rate

SINGLE GRANT APPLICATION – BUDGETING

Projected Revenue

DHHS Grant $494,426

Program Income 397,545

Contract Services 237,195 Interest Income 4,180

Miscellaneous 8,644

Total Revenue $1,141,990

BUDGETING SUMMARY

Projected Expenses

Total Projected Expenses $1,141,990Excess of Projected Expenses Over Projected Revenue $ 0***

*** CHCs must always submit a balanced budget when submitting a grant application.

BUDGET SUMMARY

Make Certain the Budget Balances!!!!!!- Review Patient Revenue Factors

- Review Staffing

BE CONSERVATIVE WHEN PROJECTING PATIENT SERVICES REVENUE!!!!

(If overly aggressive projections are used, an unobligated balance (UOB) of Federal funds could result when the FSR is filed)

SINGLE GRANT APPLICATION – BUDGETING

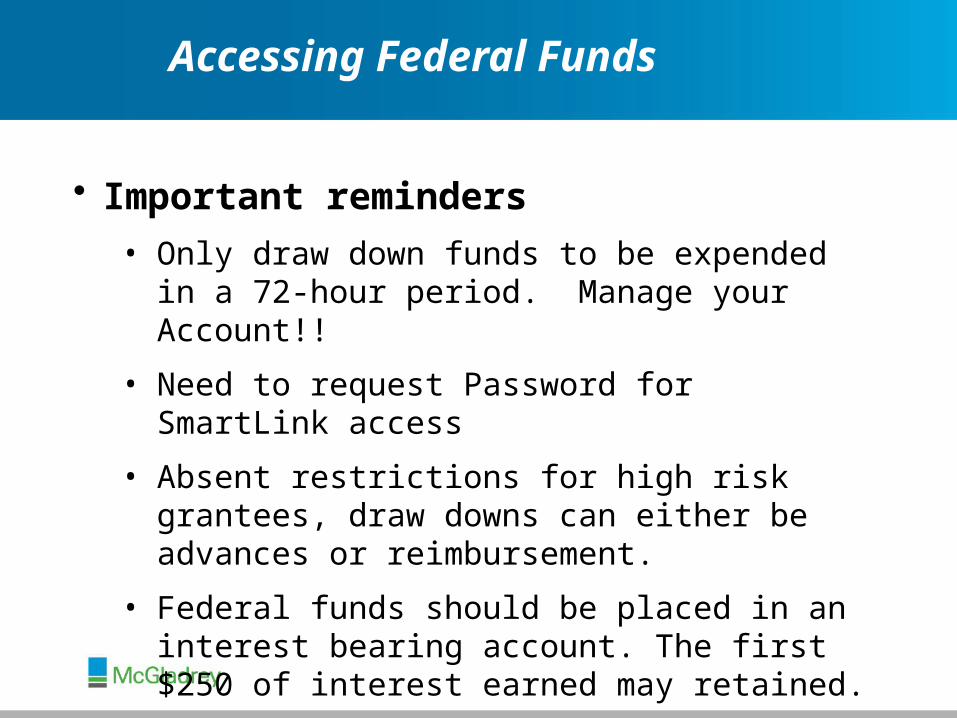

Accessing Federal Funds

• Payments for grants award by HRSA are made through the Division of Payment Management.

Division of Payment Management

P. O. Box 6021

Rockville, MD 20852

(301) 443-1661

http://www.dpm.psc.gov/Default.aspx

Accessing Federal Funds

• Important reminders

• Only draw down funds to be expended in a 72-hour period. Manage your Account!!

• Need to request Password for SmartLink access

• Absent restrictions for high risk grantees, draw downs can either be advances or reimbursement.

• Federal funds should be placed in an interest bearing account. The first $250 of interest earned may retained.

• PMS Application Support Group = 877-614-5533

Financial and Program Management

45 CFR Part 74

- Transactions/activities conducted by nonprofit grantees (including health centers) that are paid for in whole or in part by Federal funds are subject to administrative requirements in 45 CFR Part 74, incorporating –

• OMB Circular A-110 (as set forth in 2 CFR Part 215) – Administrative standards

• OMB Circular A-122 – Cost principles

DHHS Administrative Regulations and Requirements

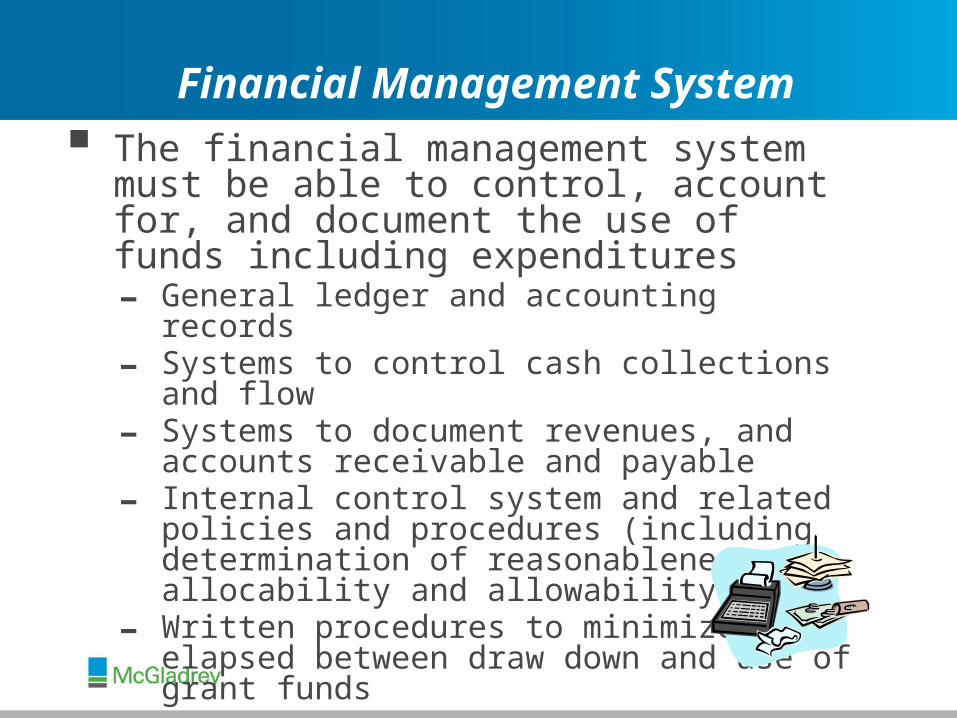

The financial management system must be able to control, account for, and document the use of funds including expenditures- General ledger and accounting records- Systems to control cash collections and flow- Systems to document revenues, and accounts

receivable and payable- Internal control system and related policies and

procedures (including determination of reasonableness, allocability and allowability)

- Written procedures to minimize time elapsed between draw down and use of grant funds

Financial Management System

The financial management system should be capable of generating monthly financial reports and statements- Budget comparative – monthly and yearly

- Productivity analyses

- Cost center allocations

Financial Management System

Allowability: to be allowable, costs must meet the criteria set forth in OMB Circular A-122- Reasonable: “[A] cost is reasonable if, in its nature and

amount, it does not exceed that which would be incurred by a prudent person under the circumstances prevailing at the time the decision was made to incur the costs”

- Conform to the limitations and exclusions regarding particular cost items

- Be adequately documented

- Be treated consistent under generally accepted accounting principles (GAAP) and the grantee’s policies and procedures

Federal Cost Principles

Allocability: costs are allocable to a Federal grant if they –

- Are allocated to a grant/project based on the relative benefits received by that project

- Are treated consistent to similar costs- Are incurred specifically for an award- Benefit the grant and can be distributed proportionately- Are necessary to the overall operation even if there is

no direct relationship to a particular cost objective

Federal Cost Principles

Costs borne, in whole or in part, by the Section 330 grant are “project costs” and subject to Federal cost principles

Federal cost principles (and procurement standards) do not apply to expenditures of program income and non-grant funds, so long as they are consistent with Section 330 purposes and there is sufficient program income and non-grant funds to cover unallowable costs

- (PIN #95-15) Specific problem areas include lobbying, fundraising,

reserves, travel and entertainment

Federal Cost Principles

Total project costs = allowable direct costs incident to grant activities plus the allocable portion of indirect costs, less any applicable credits

Direct costs- Costs identified specifically with a particular final

cost objective

Indirect costs- Costs incurred for common or joint objectives and

that cannot be readily identified with a particular cost objective (e.g., facilities, administration)

Federal Cost Principles

DHHS-approved indirect cost rate

- Cost principles require grantees with multiple sources of funding or lines of business outside of the Section 330 scope to consider utilizing an indirect cost approach, otherwise it is hard to justify cost allocation of overhead and staff to the various sources

- DHHS approved indirect cost rates assign an approved percentage of overhead/staff to each source of funding

- May require substantial communications with auditors to agree on certain fundamental principles of allocation

- Division of Cost Allocation – Apply for indirect cost rate

Federal Cost Principles

Even if a grantee does not need a DHHS-approved indirect cost rate, the grantee will need an allocation system if it is involved in activities that it wants to keep separate from the health center project

Federal Cost Principles

Time allocation

- For employees working on multiple projects, salary and benefit charges should be allocated to each project based on the proportion of time expended

- Unless assigned to specific management or professional staff, the time of clerical employees should be allocated based on either the volume or type of work performed, or, if all projects generate similar volume/type of work, based on total project expenditures

Federal Cost Principles

Grantees must maintain financial records, supporting documents, statistical records and all other records pertaining to the expenditure of grant funds to purchase real property/equipment for a period of 3 years after the final disposition of the asset

Real Property and Equipment

Grantees must maintain records for equipment acquired or improved with grant funds that –- Adequately describe the equipment- Identify the equipment by serial, model or other ID

number- Identify it by source, including award number- Note whether title vests in grantee or government- Provide the acquisition date and cost- Set forth information that can be used to calculate the

Federal share- Federal reversionary interest

Real Property and Equipment

Equipment records (cont.)- Identify the equipment’s location and condition and

the reporting date

- Provide the unit acquisition cost

- Provide the ultimate disposition data, including date of disposal, sale price, method to determine fair market value

At least every two years, the grantee must inventory its equipment and reconcile results with prior inventories

Real Property and Equipment

Record Keeping and Reporting Obligations

General record-keeping requirements

- Grantees are responsible for monitoring and oversight of all activities supported (in whole or in part) by Federal funds

- Grantees must submit to DHHS financial and programmatic records and reports pertaining (directly or indirectly) to the grant-supported project, in such form and the frequency as prescribed by DHHS

Financial and Programmatic Records

Retention

- Financial records, supporting documents, statistical records and all other records pertaining to the grant-supported project should be retained for 3 years (or other period required by applicable law) from the date of submission of final report

- If an audit, litigation, or other action involving the records is started before the end of the appropriate retention period, the records should be maintained until the end of the appropriate retention period or until the audit, litigation, or other action is completed, whichever is later

Financial and Programmatic Records

Access

- For as long as records are retained, DHHS, the Comptroller General, or any of their duly authorized representatives has the right to• Timely and unrestricted access to records, reports,

books, documents, and papers pertaining to the grant-supported project, as may be necessary for audit, examination, excerpt, transcription, and copy purposes

• Timely and reasonable access to the grantee’s personnel for the purpose of interview and discussion related to the documents

Financial and Programmatic Records

Audit requirements

- If total Federal expenditures are greater than $500,000, must complete an annual audit in accordance with the requirements of OMB Circular A-133 and the most current compliance supplement for health centers

- Costs of performing the audit can be charged to the Federal grant, unless the audit is deficient and rejected by the government

- Due 9 months after the end of fiscal year or 30 days after receipt from the auditor, whichever is earlier

- Preferably, the audit will result in an unqualified opinion with the following characteristics: gross charges exceed billable expenses, acceptable financial ratios, and minimal (or no) material audit findings

Federal Audit Requirements

Scope of the audit

- Determination that financial statements are presented fairly in all material respects in conformity with GAAP

- Review of internal controls over Federal programs to support a determination of a low level of risk for major programs

- Determination as to whether the grantee has complied with applicable laws, regulations and provisions of grant agreements that could have a direct and material effect on Federal programs

Federal Audit Requirements

Auditors are precluded from performing both A-133 audit and providing certain non-audit management consulting services, including – - Implementing accounting systems- Determining account balances- Developing internal control systems- Establishing capitalization criteria- Processing payroll- Posting of transactions- Evaluating assets- Designing or implementing IT systems- Performing actuarial studies

Federal Audit Requirements

Financial reporting requirements

- Federal Financial Report (FFR – SF425) (replaces the SF 272 PSC Federal cash transactions report and SF269 Financial Status Report)• Old SF 272 PSC

1. Monitors the timing of cash advances and disbursements2. Submitted quarterly, within 45 days of the end of the

quarter• Old SF 269 FSR

1. Reports the status of grant fund expenditures 2. Submitted annually, within 90 days after the budget period

ends

Reporting Requirements

What is the Federal Financial Report (FFR)?

The FFR, also known as SF-425/SF425A, combines and replaces both the Federal Cash Transactions Report (PSC/SF-272) and the Financial Status Report (SF-269) into a single electronic report

Certain federal agencies are required to transition to using the FFR beginning with 1st Quarter Fiscal Year 2010 Reports (Quarter 1: October 1–December 31, 2009)

Until further notice, the FSR-269 will not be accessible for HHS Grantees through the FFR

HHS Grantees

PSC 272 Submit through PMS

FSR-269 Submit through EHB

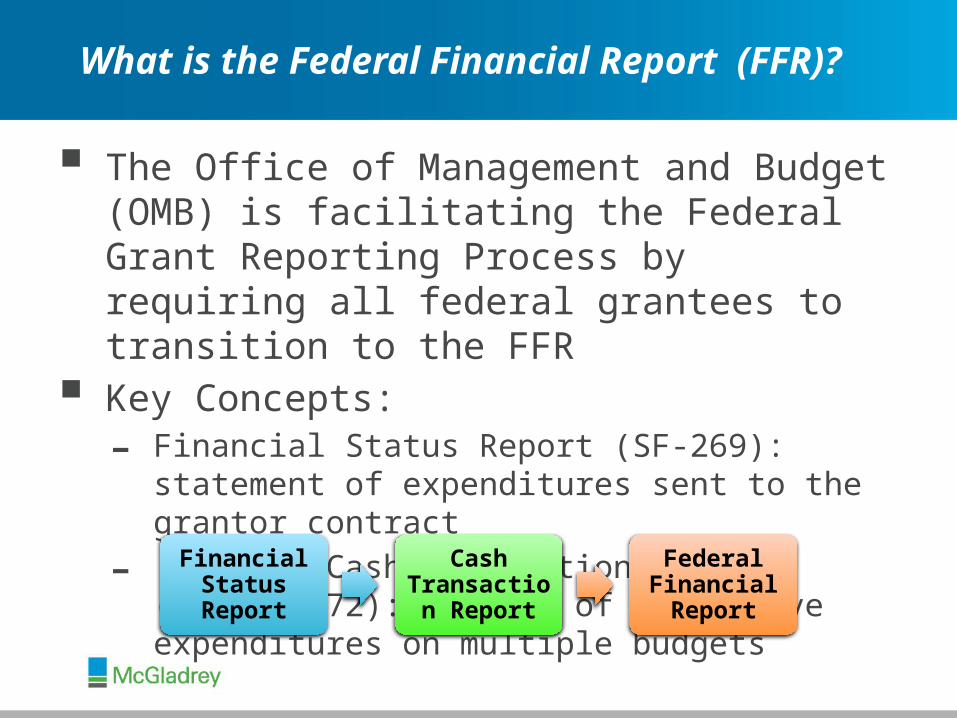

The Office of Management and Budget (OMB) is facilitating the Federal Grant Reporting Process by requiring all federal grantees to transition to the FFR

Key Concepts:- Financial Status Report (SF-269): statement of

expenditures sent to the grantor contract

- Federal Cash Transactions Report (PSC/SF 272): report of cumulative expenditures on multiple budgets

Financial Status Report

Cash Transaction

Report

Federal Financial Report

What is the Federal Financial Report (FFR)?

How will the FFR affect Health Centers’ Current Reporting Requirements?

Non HHS Grantees

Beginning January 4, 2010, grantees will not be permitted to file cash transactions using PSC-272

Cash Transactions Reports for the quarter ending on December 31, 2009 and beyond must use the new FFR in PMS

Reports are due 30 days after reporting period has ended

The Financial Status Report will now be provided through the FFR

HHS Grantees

Report Cash Transactions the Payment Management System’s (PMS) website using the automated FFR Cash Transaction Report

Should continue to use the SF-269/SF-269A to report expenditures through 3/31/2010 on HRSA’s EHB

Transition to FFR (SF425) on HRSA’s EHB beginning 4/1/2010 for the FSR

The Electronic 272 System will no longer be available

Reports are due 30 days after reporting period has ended

Health and Human Services (HHS) will advise the Office of Management & Budget (OMB) how the FSR will be incorporated into the FFR for HHS grantees

Eventually, OMB anticipates the FFR to become identical for all programs

Total Recipient Share required: must now report on the cumulative recipient share and disbursements of the grant funds based on the amounts entered in the approved budgets

What Are the Changes Included in the FFR?

The New Federal Financial Report Process

The filling requirements remain the same as for filing the PSC-272 in FFR

The filing requirements remain the same as indicated in the Terms and Conditions of the Notice of Grant Awards (NGA) for the FSR

A FFR attachment will be used for reporting multiple grants The FFR establishes government-wide standards for reporting

periods & due dates

- Reporting period end dates must fall on the end of a calendar quarter

- Reports are due 30 days after reporting period end date instead of 45 days

To submit the FFR, you must access the Division of Payment Management Website (DPM) at http://www.dpm.psc.gov.

Select Payment System and Login - If you are a current PMS user, you will continue to have

the same user permissions for the FFR Cash Transaction Report as you did for the Electronic 272 System.

- If you are not a current PMS User but had used the Electronic 272 System, on Jan. 4, 2010, DPM sent an email to you with a temporary username and password, as well as instructions to access the FFR Cash Transaction Report

Accessing and Completing the FFR

Once you enter your account number, you must choose either 1) the Federal Cash Transaction Report or 2) the Financial Status Report.

- Note : if you choose the Financial Status Report, it will be “grayed out” for HHS Grantees

There is also a selection for reporting FFR interest income. The assumption is that you will report any interest earned above $250.00 per grant period, per grant.

Certain information will be pre-populated on the report, i.e., the federal agency, recipient organization, DUNS number, the grant period. Check to be sure information is accurate.

There is a separate area for reporting on multiple grants on a FFR attachment screen.

Must now verify cumulative disbursements for each active grant (since the inception of the grant).

Accessing and Completing the FFR

10a. –10c. o You will report these values to PMSo Fields will be disabled in the EHBs

FFR –Transactions Section

If you have disbursements on inactive grants, you will need to enter the disbursement amount. If inactive grants show on your account, and there will be no more activity on them, you should delete them from the FFR.

Once disbursements have been completed, the FFR will populate fields showing cash receipts and cash disbursements. You must enter an amount in the “cash on hand” field.

Once the report is complete and ready to be Certified, the authorized certifier must log into the FFR, scroll to the bottom of the page and complete steps 1-5

You will have the ability to print, save and/or view the report once it is certified. Recommend that a copy be saved for your records.

Accessing and Completing the FFR

Have a separate, interest-bearing checking account for each federal award:

- Draw downs and expenditures are easily traced for each grant.

- There is no co-mingling of grant funds that may be for different purposes, and it is easier to determine interest earned on the federal funds.

- The FFR report can be completed simply by gathering the bank statements on each federal grant account, which will show receipts and disbursements activity.

Keep copies of each quarterly report Keep a log of draw-downs for each grant, including a perpetual log

on the 330 grant

Suggestions for FFR Reporting

Resources & References for the FFR

Division of Payment Management:

- http://www.dpm.psc.gov/

- http://www.dpm.psc.gov/grant_recipient/ffr_info_hhs.aspx

Grants.gov: http://www.grants.gov/

Recipient Instructions for completing the FFR in the Payment Management System (PMS)

Always contact your grant specialist or your payment management account representative for any questions or concerns

Key Definitions• Program Income – Patient Services Revenue and State, local

and other assistance.• Patient Services Revenue - The amount of fees, premiums,

and third party reimbursements accrued from center operations during the budget period, after adjustments for uncollectibles.

• State, Local, and Other assistance - all resources for the approved project that are NOT:

– Fees, premiums and third party reimbursement, or– Section 330 Federal financial assistance.

Federal Financial Report (Formerly the FSR)

Determination of Outlays • Start with: Accrual based expenses, reconciled to audited

financial statements.• Minus: All non-cash outlays (depreciation, bad debt, etc.).• Plus: Fixed asset additions (less proceeds from long term debt)

and payments of long-term debt obligations. – Only capital lease and loan payments for capital

expenditures can be included in total outlays. • Plus: Establishment of Reserves• Equals = Total Outlays

Financial Status Report

The “Order of Spending” for CHC Grant Awards is:

1. Program Income:

a) Patient Services Revenue

b) State, Local and Other Dollars:– Contracts – Contributions– Miscellaneous – Donated

2. Federal Grant (up to amount recognized)

3. Current Program Income Over Budget

Financial Status Report

FFR Transactions – By Field Line 10

d. Federal funds authorized Populated from EHBs

e. Federal share of expenditures Previously reported = pre-populated

f. Federal share of unliquidated obligations Enter cumulative value

g. Total Federal share EHBs will calculate value

h. Unobligated balance of Fed funds EHBs will calculate value

i. Total recipient share required Previously reported – pre-populated

j. Recipient share of expenditures Previously reported = pre-populated

k. Remaining recipient share to be provided EHBs will calculate values

l. Total Federal program income earned Enter cumulative value only (last column)

m. Program income expended – deduction alt Enter cumulative value only (last column)

n. Program income expended – addition alt Enter cumulative value only (last column)

o. Unexpended program income Enter cumulative value only (last column)

Federal Financial Report

Budget: Grant $ 494,426Program Income

647,564

$ 1,141,990

Actual: Grant $ 494,426Program Income

740,574 Total Revenue

1,235,000Outlays

1,150,000 Surplus

$ 85,000

Financial Status Report

Example:

Order of Spending:Program Income, Up to Budget 647,564Federal Grant 494,426Current Program Income Over Budget 8,010

$1,150,000

Excess Program Income ($740,574 - $647,564 - $8,010) $85,000

Financial Status Report

Federal Financial Report Example

Federal Financial Report Example

Federal Expenditures and Unobligated BalanceI. II. III.

Line # Description Previously This CumulativeReported Period

10 d. Total Federal funds authorized 494,426 494,426 10 e. Federal share of expenditures 494,426 494,426 10 f. Federal share of unliquidated obligations10 g. Total Federal share (sum of lines e and f) 494,426 494,426 10 h. Unobligated balance of Federal funds (line d minus g) 0 0

Recipient Share10 i. Total recipient share required 0 0 10 j. Recipient share of expenditures 0 0 10 k. Remianing recipient share to be provided (line I minus j) 0 0

Program Income10 l. Total Federal program income earned 740,574 740,574 10 m. Program income expended in accordance with the deduction 0 0 alternative 10 n. Program income expended in accordance with the addition 647,564 647,564

alternative10. o Unexpended program income (line l minus line m or line n) 85,000 85,000

Lines i, j and k are for reporting on cost sharing or matching requirements, only. When Health Centers report on the FFR, lines i., j., and k. should remain blank.

Financial Status Report ScenariosBudgeted Revenue

CHC 1 CHC 2 CHC 3 CHC4Federal grant $ 1,200,000 $1,200,000 $ 1,200,000 $ 1,200,000State, Local & Other 1,800,000 1,800,000 1,800,000 1,800,000Patient Revenue 4,500,000 4,500,000 4,500,000 4,500,000Total Budget $7,500,000 $7,500,000 $7,500,000 7,500,000Actual RevenueFederal grant $1,200,000 $1,200,000 $1,200,000 $1,200,000State, Local & Other 1,800,000 1,700,000 2,000,000 1,900,000Patient Revenue 4,500,000 4,600,000 5,000,000 4,600,000Total Revenue $7,500,000 $7,500,000 $8,200,000 $7,700,000

Total Outlays ($7,400,000) ($7,300,000) ($7,900,000) ($7,400,000)Order of Dollars Spent1) Program income $6,300,000 $6,300,000 $6,300,000 $6,300,0002) Federal grant 1,100,000 1,000,000 1,200,000 1,100,0003) Program income above budget --- --- 400,000 --- Total Expenditures $7,400,000 $7,300,000 $7,900,000 $7,400,000Unspent DollarsExcess Program Income --- --- $300,000 $200,000Unobligated Federal Grants $100,000 $200,000 ---- 100,000 Total Unspent Dollars $100,000 $200,000 $300,000 $300,000

Any Questions???