nordea 1 alpha 15 ma fund

TRANSCRIPT

Nordea 1 – Alpha 15 MA FundLU0607983383, BI-EUR

Advertising Material for professional investors only, investing for their own account – according to MiFID definition

Any investment decision in the sub-funds should be made on the basis of the current prospectus and the Key Investor Information Document (KIID).

January 2022

Open

22

NordeaA stable bank among the largest European players

Ratings:

• Standard & Poor's

• Moody's

• Fitch

AA-

Aa3

AA-

Common Equity Tier 1 capital

ratio17%

Market Capitalisation €46bn

Total assets €614bn

AuM (Asset & Wealth Management) €393bn

Source: Nordea Bank Abp. As of date: 30.09.2021

Nordea is the largest financial institution in the Nordic region

The 4 business areas are:

• Personal Banking;

• Business Banking;

• Large Corporate & Institutions; and

• Asset & Wealth Management

Personal

Customers

~9.2m

Corporate

customers

~540,000

Number of

employees

~27,000

Total operating

income YTD Sep

2021

€7,182m

Open

3

Nordea Asset ManagementAt a glance

Source: Nordea Investment Funds S.A. and Nordea Investment Management AB. Date: 30.09.2021. * © 2021 Morningstar, Inc. All Rights Reserved as of 30.09.2021. The Morningstar Rating is an assessment of a fund’s past performance —

based on both return and risk — which shows how similar investments compare with their competitors. A high rating alone is insufficient basis for an investment decision. Past performance is no guarantee of future results.

NAM in numbers Multi-boutique approach Key facts

€ 281bn

In assets under management (AUM) One platform, many specialists: alpha and outcome

solutions in one platform to serve clients in all

weather

90% AUM managed by internal boutiques

10% AUM managed by best of breed external

boutiques

12 internal boutiques covering alpha, ESG

and outcome

Nearly 50% of AUM are from third party clients

Servicing clients in 55 countries across the globe

34 Nordea 1 funds with a Morningstar rating

of 4 or 5 stars*

19 Nordea 1 funds with more than € 1bn of AUM

32 Nordea 1 funds with more than € 500m of AUM

44 Nordea 1 funds with more than € 250m of AUM

A pioneer in ESG/SRI since 1988 currently

managing € 177bn

1932

44

Open

Nordea Asset ManagementOne platform, many specialists

The Nordea multi-boutique approach

allows us to propose some of the best

investment solutions to our clients by

combining internal strengths with

exclusive external competences.

4

Open

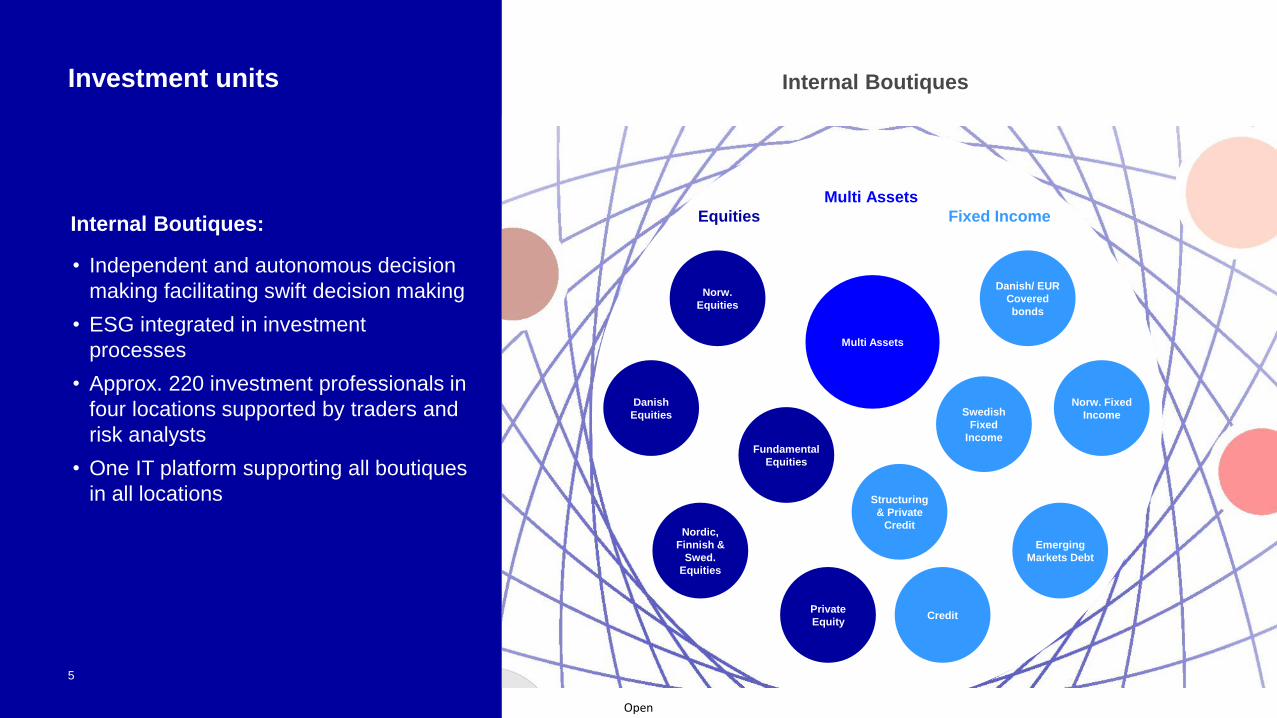

5

Investment units

Internal Boutiques:

• Independent and autonomous decision

making facilitating swift decision making

• ESG integrated in investment

processes

• Approx. 220 investment professionals in

four locations supported by traders and

risk analysts

• One IT platform supporting all boutiques

in all locations

Equities

Multi Assets

Fixed Income

Internal Boutiques

Multi Assets

Fundamental

Equities

Nordic,

Finnish &

Swed.

Equities

Norw.

Equities

Danish

Equities

Private

Equity

Danish/ EUR

Covered

bonds

Swedish

Fixed

Income

Norw. Fixed

Income

Credit

Emerging

Markets Debt

Structuring

& Private

Credit

Open

6

Nordea Asset ManagementSelected Nordea solutions to meet your needs

Note that some of the strategies listed above are only available as a sub-fund vehicle within the Nordea 1, SICAV. The Nordea 1, SICAV consists of 76 sub-funds covering the full asset spectrum out of which 58 products have more than

€100m AuM and 49 products have more than €200m AuM. Source: Nordea Investment Funds S.A. Date: 30.09.2021.

Why Liquid Alternatives and why us?

Open

8

Why liquid alternatives today?Historical vs. expected returns and risk from EUR based investor’s perspective

Source: Nordea Investment Management AB, on the basis of analyses carried out by the Multi Assets Team. Period under consideration: 31.12.2011 – 31.12.2021. Past and expected returns are unhedged, in base currency and from EUR based investor’s stance. The performance represented is historical; past performance is not a reliable indicator of future results and investors may not recover the full amount invested. The value of your investment can go up and down, and you could lose some or all of your invested money. Expected numbers are only targets. There can be no warranty that an investment objective, targeted returns and results of an investment structure is achieved.

Open

9

Source: Bloomberg. Note: The Chicago Board Options Exchange Volatility Index reflects a market estimate of future volatility, based on the weighted average of the implied volatilities for a wide range of strikes.

• Low Vol has been a key benefit in the last

years and was stemming from the strong

growth-driven market environment

• But: Macro data are worsening rapidly and

market uncertainties increase: Covid-19,

growth outlook, central bank interventions

• Net result: Market sell-offs, bumpier

markets, less calm market environment

→ Liquid alternatives are needed

to add diversification without

sacrificing returns!

Volatility is coming back to the market with forceDiversify your portfolio with liquid alternatives!

Open

Equity-like returns with limited correlations to traditional asset classes

Alpha 15 MA Strategy proposition

• An innovate, alternative solution:

‒ Objective A15 MA: cash +7-10% p.a. (gross), vol. 10-15% over

a cycle1

‒ Process: Quantitative, bottom-up risk premia approach with a

fundamental overlay

• Employs a diversified universe of risk premia:

‒ To face the low expected returns offered by traditional asset

classes and unlock additional sources of return

• Delivers true diversification:

‒Combines traditional and alternative risk premia to offer low

correlation to traditional asset classes

10

1) There can be no warranty that an investment objective, targeted returns and results of an investment structure is achieved. The value of your investment can go up and down, and you could lose some or all of your invested

money. During adverse market environments, the volatility can reach around 15% in the A15MAS. 2) Source: Nordea Investment Management AB. Based on monthly observations. The product performance represents the Alpha 15 Multi

Asset Strategy, gross of fees and in EUR. Period under consideration: 01.01.2017 - 31.12.2021. The performance represented is historical; past performance is not a reliable indicator of future results and investors may not recover

the full amount invested. The value of your investment can go up and down, and you could lose some or all of your invested money. 3) The equity index used is the MSCI World 100% Hedged to EUR NDR. 4) The bond returns are

based on the Bloomberg Barclays Series-E Germany Govt 7-10 YR in EUR. Please note the Alpha 15 MA Strategy does not have any official benchmarks and the indices are used for comparison purposes only. Internally calculated by the

investment team and produced on a best effort basis.

Attractive risk-adjusted returns and

low correlation to traditional asset classes

5 year p.a. A15MA Strategy

Return2 11.20%

Volatility 8.51%

Sharpe Ratio 1.37

Equity Correlation3,4 0.45

Bond Correlation3 0.16

Open

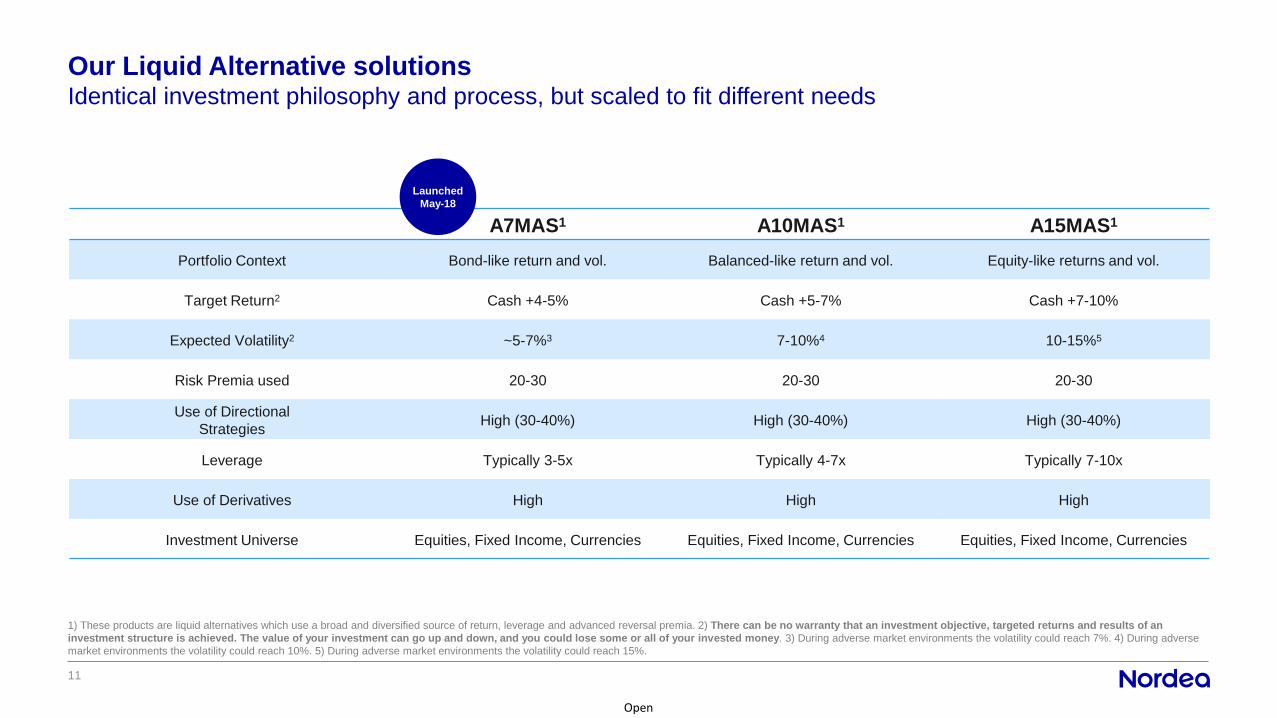

Identical investment philosophy and process, but scaled to fit different needs

Our Liquid Alternative solutions

11

1) These products are liquid alternatives which use a broad and diversified source of return, leverage and advanced reversal premia. 2) There can be no warranty that an investment objective, targeted returns and results of an

investment structure is achieved. The value of your investment can go up and down, and you could lose some or all of your invested money. 3) During adverse market environments the volatility could reach 7%. 4) During adverse

market environments the volatility could reach 10%. 5) During adverse market environments the volatility could reach 15%.

A7MAS1 A10MAS1 A15MAS1

Portfolio Context Bond-like return and vol. Balanced-like return and vol. Equity-like returns and vol.

Target Return2 Cash +4-5% Cash +5-7% Cash +7-10%

Expected Volatility2 ~5-7%3 7-10%4 10-15%5

Risk Premia used 20-30 20-30 20-30

Use of Directional

StrategiesHigh (30-40%) High (30-40%) High (30-40%)

Leverage Typically 3-5x Typically 4-7x Typically 7-10x

Use of Derivatives High High High

Investment Universe Equities, Fixed Income, Currencies Equities, Fixed Income, Currencies Equities, Fixed Income, Currencies

Launched

May-18

Multi Assets Team

Investment philosophy + process

Open

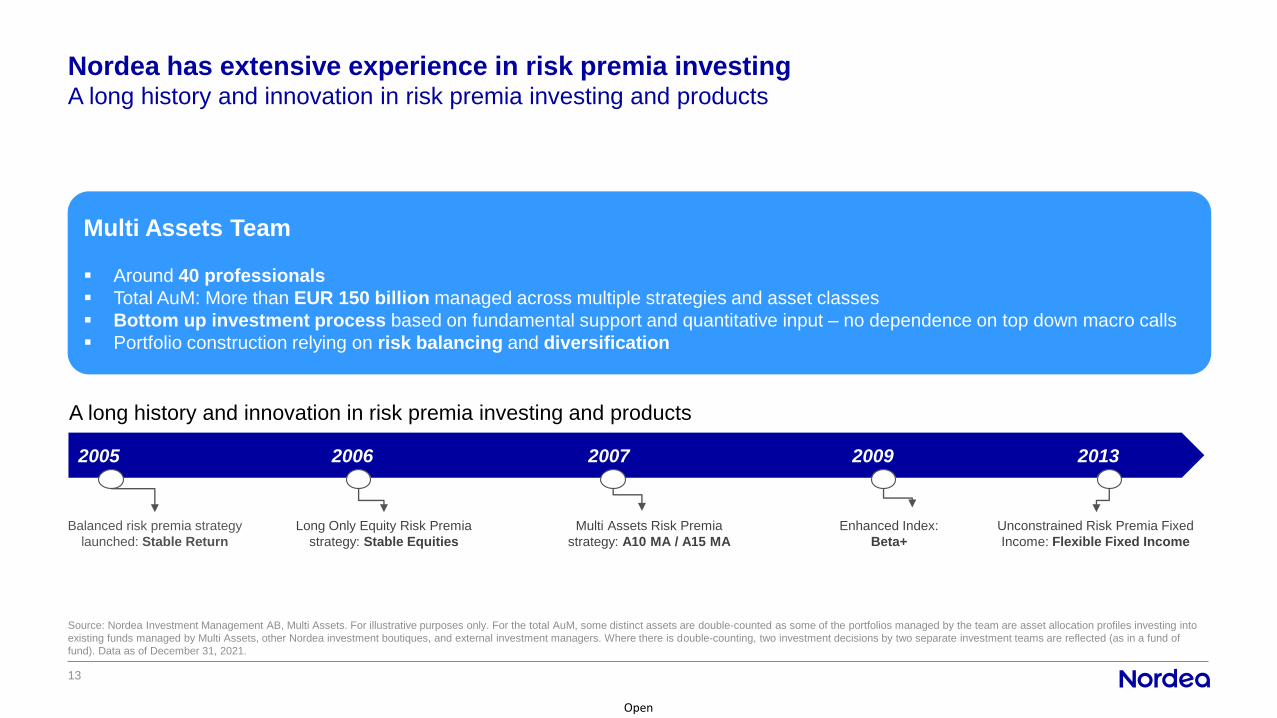

A long history and innovation in risk premia investing and products

Nordea has extensive experience in risk premia investing

13

Source: Nordea Investment Management AB, Multi Assets. For illustrative purposes only. For the total AuM, some distinct assets are double-counted as some of the portfolios managed by the team are asset allocation profiles investing into

existing funds managed by Multi Assets, other Nordea investment boutiques, and external investment managers. Where there is double-counting, two investment decisions by two separate investment teams are reflected (as in a fund of

fund). Data as of December 31, 2021.

2005 2006 2007 2009 2013

Long Only Equity Risk Premia

strategy: Stable Equities

Multi Assets Risk Premia

strategy: A10 MA / A15 MA

Unconstrained Risk Premia Fixed

Income: Flexible Fixed Income

Enhanced Index:

Beta+

Balanced risk premia strategy

launched: Stable Return

Multi Assets Team

▪ Around 40 professionals

▪ Total AuM: More than EUR 150 billion managed across multiple strategies and asset classes

▪ Bottom up investment process based on fundamental support and quantitative input – no dependence on top down macro calls

▪ Portfolio construction relying on risk balancing and diversification

A long history and innovation in risk premia investing and products

Open

14

Understanding asset class behaviour with Traditional risk premia

Example: European Corporate Bonds

Focus on returns from duration and credit risk rather than total return

• Definition of a risk premium: Excess

return required for taking a certain risk

• Risk is easier to identify when focusing

on risk premiums rather than asset classes

• Correlation analysis is more robust for

risk premiums than for asset classes

Example: European Corporate Bonds

Note: For illustrative purposes only.

Focus on risk premia rather than asset classes

Risk Free Rate

German Duration

Risk Premium

Europe IG Credit Spreads

European Corporate Bonds Total Return

Open

Note: For illustrative purposes only.

15

No need to make the correct macroeconomic call to achieve a positive total return in all periods of the

economic cycle

The Economic Cycle

Return drivers working

in periods of recession

Return drivers working

in periods of recovery

Total performance

Illustrative performance

What is unique about Nordea’s MAT Risk Premia approach?Macro-call’s independent

Open

Note: Example for illustrative purposes only. Source: Nordea Investment Management AB and Multi Assets team.

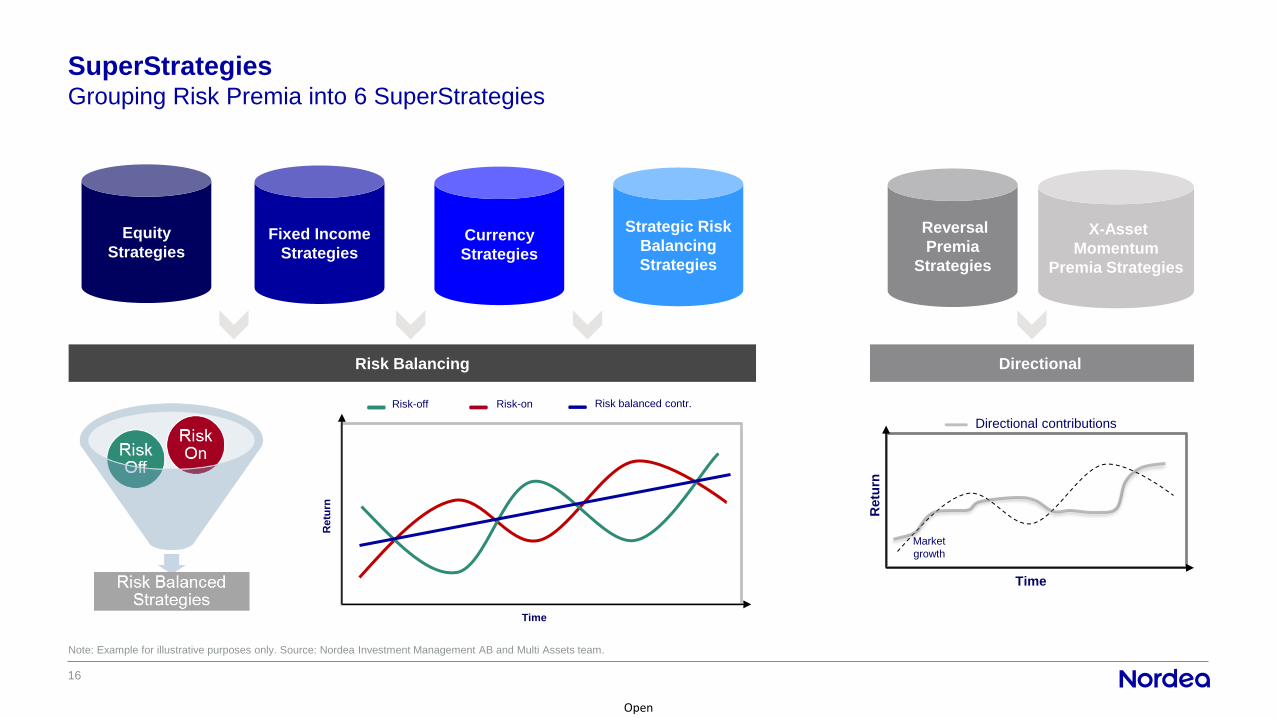

SuperStrategiesGrouping Risk Premia into 6 SuperStrategies

Risk Balancing Directional

X-Asset

Momentum

Premia Strategies

Reversal

Premia

Strategies

Strategic Risk

Balancing

Strategies

Currency

Strategies

Fixed Income

Strategies

Equity

Strategies

Time

Retu

rn

Directional contributions

Market

growth

Time

Retu

rn

Risk-off Risk-on Risk balanced contr.

16

Open

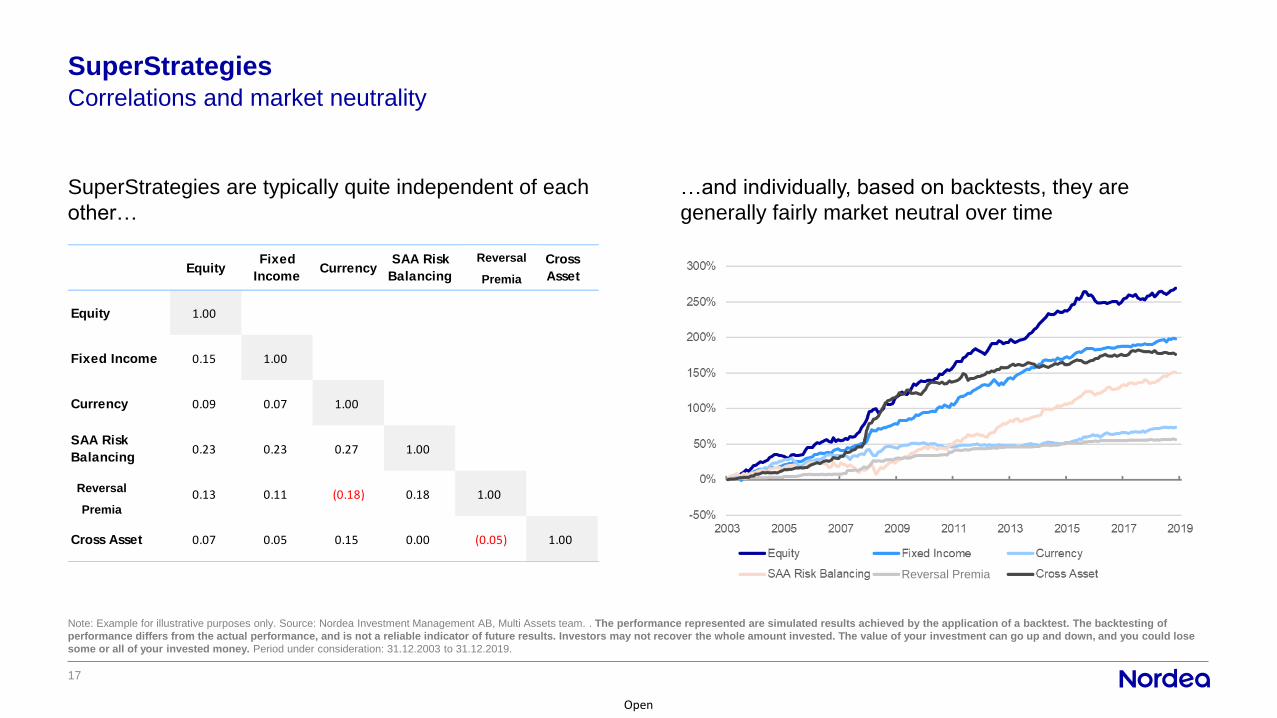

Correlations and market neutrality

SuperStrategies

17

Note: Example for illustrative purposes only. Source: Nordea Investment Management AB, Multi Assets team. . The performance represented are simulated results achieved by the application of a backtest. The backtesting of

performance differs from the actual performance, and is not a reliable indicator of future results. Investors may not recover the whole amount invested. The value of your investment can go up and down, and you could lose

some or all of your invested money. Period under consideration: 31.12.2003 to 31.12.2019.

…and individually, based on backtests, they are

generally fairly market neutral over time

SuperStrategies are typically quite independent of each

other…

EquityFixed

IncomeCurrency

SAA Risk

BalancingTrading

Cross

Asset

Equity 1.00

Fixed Income 0.15 1.00

Currency 0.09 0.07 1.00

SAA Risk

Balancing0.23 0.23 0.27 1.00

Trading 0.13 0.11 (0.18) 0.18 1.00

Cross Asset 0.07 0.05 0.15 0.00 (0.05) 1.00

Reversal Premia

Reversal

Premia

Reversal

Premia

Open

18

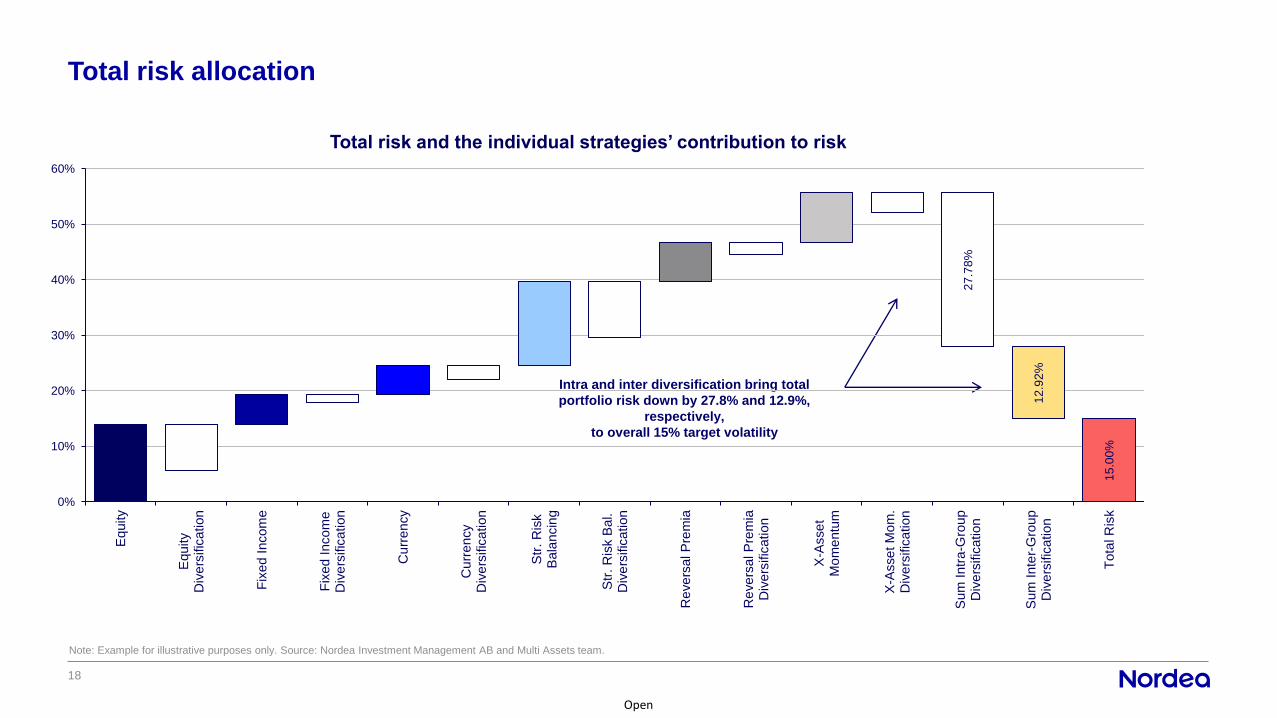

Total risk allocation

Note: Example for illustrative purposes only. Source: Nordea Investment Management AB and Multi Assets team.

Intra and inter diversification bring total

portfolio risk down by 27.8% and 12.9%,

respectively,

to overall 15% target volatility

27

.78

%

12

.92

%

15

.00

%

0%

10%

20%

30%

40%

50%

60%

Equity

Equity

Div

ers

ific

ation

Fix

ed

Incom

e

Fix

ed

Incom

eD

ive

rsific

ation

Cu

rren

cy

Cu

rren

cy

Div

ers

ific

ation

Str

. R

isk

Bala

ncin

g

Str

. R

isk B

al.

Div

ers

ific

ation

Re

ve

rsal P

rem

ia

Re

ve

rsal P

rem

iaD

ive

rsific

ation

X-A

sse

tM

om

entu

m

X-A

sse

t M

om

.D

ive

rsific

ation

Sum

Intr

a-G

roup

Div

ers

ific

ation

Sum

Inte

r-G

roup

Div

ers

ific

ation

Tota

l R

isk

Total risk and the individual strategies’ contribution to risk

Open

19

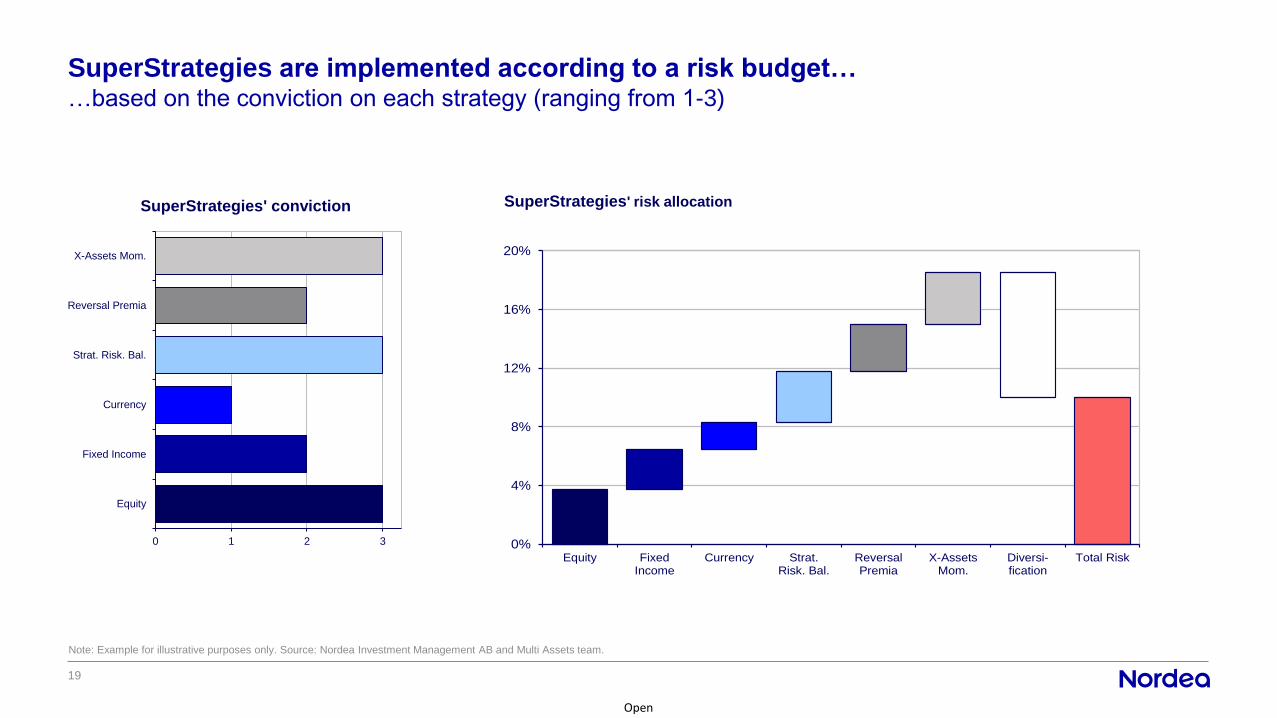

SuperStrategies are implemented according to a risk budget……based on the conviction on each strategy (ranging from 1-3)

Note: Example for illustrative purposes only. Source: Nordea Investment Management AB and Multi Assets team.

SuperStrategies' risk allocation

0 1 2 3

Equity

Fixed Income

Currency

Strat. Risk. Bal.

Reversal Premia

X-Assets Mom.

SuperStrategies' conviction

0%

4%

8%

12%

16%

20%

Equity FixedIncome

Currency Strat.Risk. Bal.

ReversalPremia

X-AssetsMom.

Diversi-fication

Total Risk

Nordea 1 – Alpha 15 MA Fund

Why invest?

Open

21

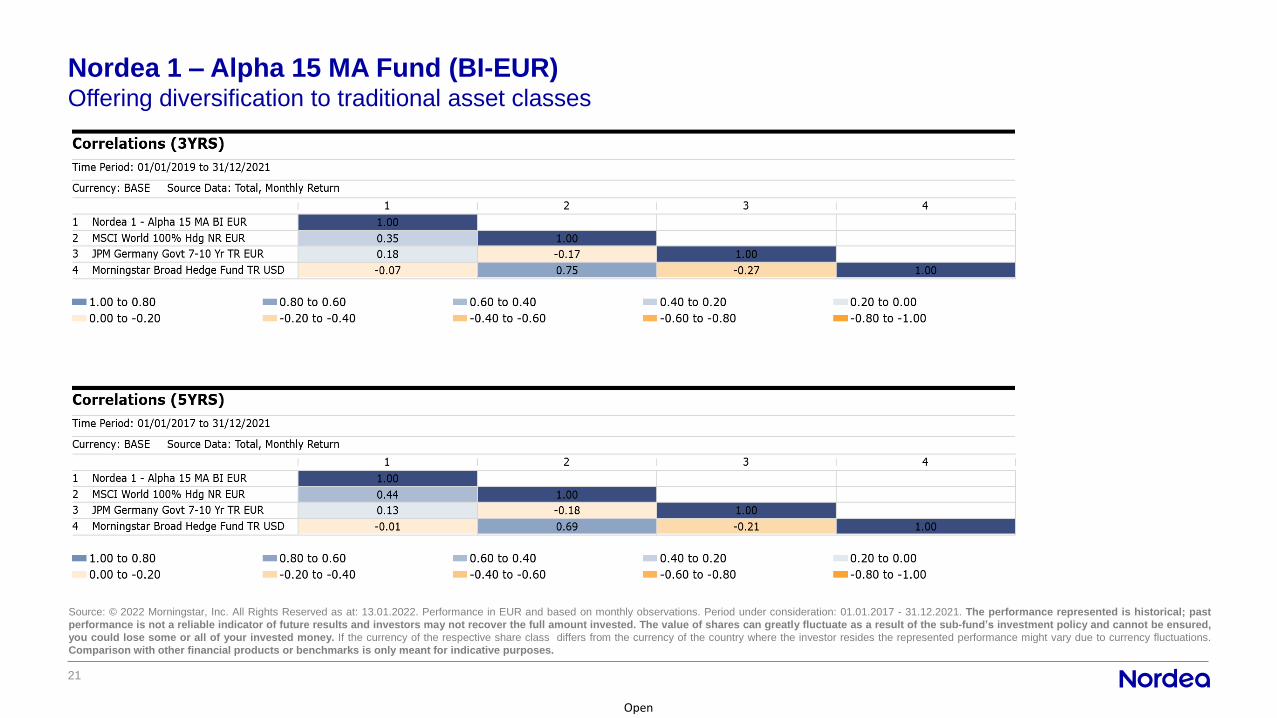

Nordea 1 – Alpha 15 MA Fund (BI-EUR)Offering diversification to traditional asset classes

Source: © 2022 Morningstar, Inc. All Rights Reserved as at: 13.01.2022. Performance in EUR and based on monthly observations. Period under consideration: 01.01.2017 - 31.12.2021. The performance represented is historical; past

performance is not a reliable indicator of future results and investors may not recover the full amount invested. The value of shares can greatly fluctuate as a result of the sub-fund’s investment policy and cannot be ensured,

you could lose some or all of your invested money. If the currency of the respective share class differs from the currency of the country where the investor resides the represented performance might vary due to currency fluctuations.

Comparison with other financial products or benchmarks is only meant for indicative purposes.

Open

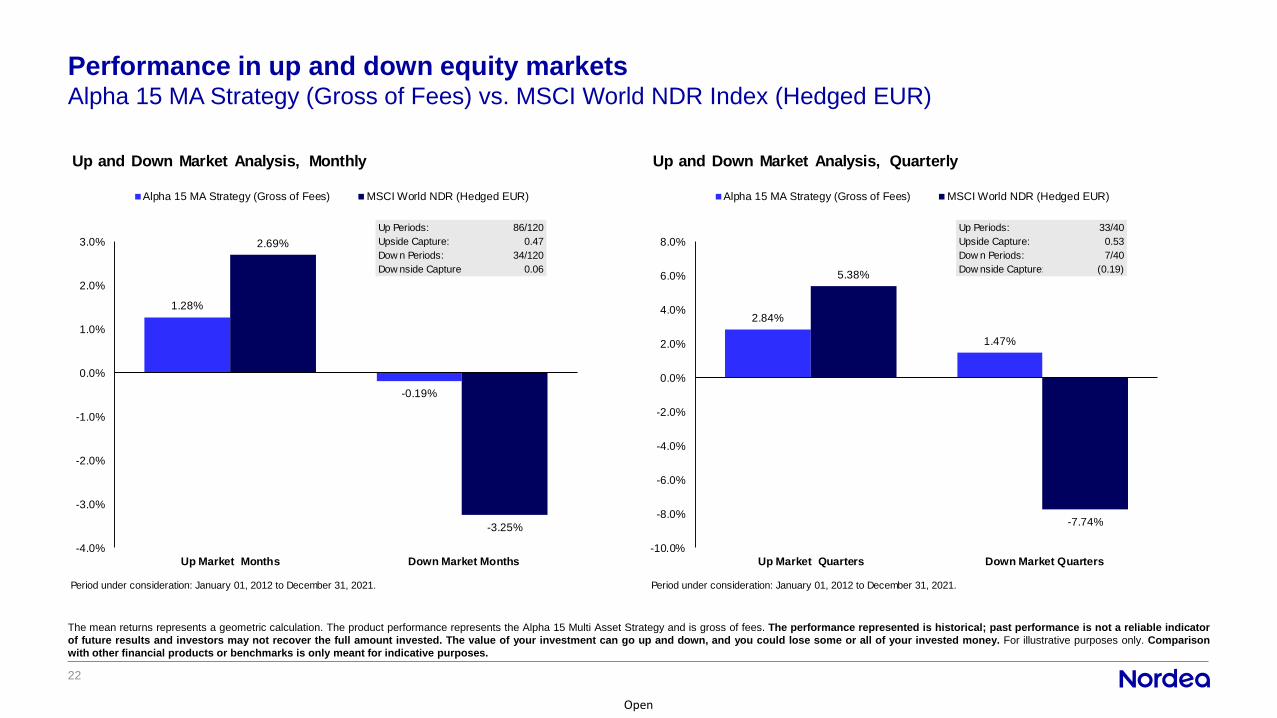

Performance in up and down equity markets

22

The mean returns represents a geometric calculation. The product performance represents the Alpha 15 Multi Asset Strategy and is gross of fees. The performance represented is historical; past performance is not a reliable indicator

of future results and investors may not recover the full amount invested. The value of your investment can go up and down, and you could lose some or all of your invested money. For illustrative purposes only. Comparison

with other financial products or benchmarks is only meant for indicative purposes.

Alpha 15 MA Strategy (Gross of Fees) vs. MSCI World NDR Index (Hedged EUR)

Up Periods: 86/120

Upside Capture: 0.47

Dow n Periods: 34/120

Dow nside Capture: 0.06

Period under consideration: January 01, 2012 to December 31, 2021.

1.28%

-0.19%

2.69%

-3.25%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

Up Market Months Down Market Months

Up and Down Market Analysis, Monthly

Alpha 15 MA Strategy (Gross of Fees) MSCI World NDR (Hedged EUR)

Up Periods: 33/40

Upside Capture: 0.53

Dow n Periods: 7/40

Dow nside Capture: (0.19)

Period under consideration: January 01, 2012 to December 31, 2021.

2.84%

1.47%

5.38%

-7.74%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Up Market Quarters Down Market Quarters

Up and Down Market Analysis, Quarterly

Alpha 15 MA Strategy (Gross of Fees) MSCI World NDR (Hedged EUR)

Open

Performance in up and down bond markets

23

The mean returns represents a geometric calculation. The product performance represents the Alpha 15 Multi Asset Strategy and is gross of fees. The performance represented is historical; past performance is not a reliable indicator

of future results and investors may not recover the full amount invested. The value of your investment can go up and down, and you could lose some or all of your invested money. For illustrative purposes only. Comparison

with other financial products or benchmarks is only meant for indicative purposes.

Alpha 15 MA Strategy (Gross of Fees) vs. 7-10 YR GER Bunds

Up Periods: 70/120

Upside Capture: 1.09

Dow n Periods: 50/120

Dow nside Capture: (0.42)

Period under consideration: January 01, 2012 to December 31, 2021.

1.19%

0.40%

1.09%

-0.96%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

Up Market Months Down Market Months

Up and Down Market Analysis, Monthly

Alpha 15 MA Strategy (Gross of Fees) BB Germany Govt 7-10 YR

Up Periods: 27/40

Upside Capture: 1.77

Dow n Periods: 13/40

Dow nside Capture: (1.28)

Period under consideration: January 01, 2012 to December 31, 2021.

3.00%

1.77%1.70%

-1.38%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Up Market Quarters Down Market Quarters

Up and Down Market Analysis, Quarterly

Alpha 15 MA Strategy (Gross of Fees) BB Germany Govt 7-10 YR

Open

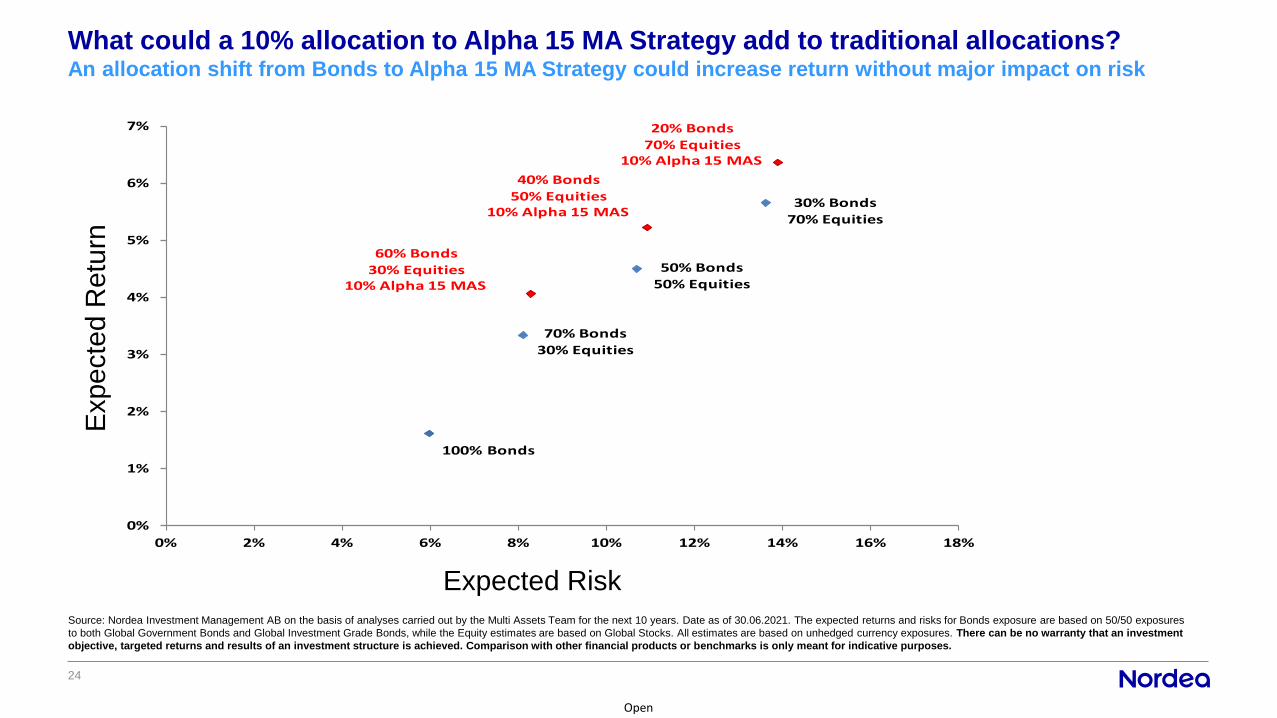

What could a 10% allocation to Alpha 15 MA Strategy add to traditional allocations?An allocation shift from Bonds to Alpha 15 MA Strategy could increase return without major impact on risk

24

Expected Risk

Expe

cte

d R

etu

rn

Source: Nordea Investment Management AB on the basis of analyses carried out by the Multi Assets Team for the next 10 years. Date as of 30.06.2021. The expected returns and risks for Bonds exposure are based on 50/50 exposures

to both Global Government Bonds and Global Investment Grade Bonds, while the Equity estimates are based on Global Stocks. All estimates are based on unhedged currency exposures. There can be no warranty that an investment

objective, targeted returns and results of an investment structure is achieved. Comparison with other financial products or benchmarks is only meant for indicative purposes.

100% Bonds

70% Bonds

30% Equities

50% Bonds50% Equities

30% Bonds70% Equities

60% Bonds30% Equities

10% Alpha 15 MAS

40% Bonds

50% Equities10% Alpha 15 MAS

20% Bonds70% Equities

10% Alpha 15 MAS

0%

1%

2%

3%

4%

5%

6%

7%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Open

25

Why invest in the Nordea Alpha 10 MA Strategy?Attractive returns with a limited correlation to equities

1) Expected return numbers are only targets. There can be no warranty that an investment objective, targeted returns or results of an investment structure are achieved. The value of shares can greatly fluctuate as a

result of the sub-fund’s investment policy and cannot be ensured, you could lose some or all of your invested money. Source: Nordea Investment Management AB, on the basis of analyses carried out by the Multi Assets

Team. Data as of 30.06.2021. 2) Sources: Nordea Investments Fund S.A. and Datastream. Period under consideration: 01.07.2016 – 30.06.2021.

Cash

European Govies

US Treasuries

EU IG

US IGEU HY

US HY

EM Govies

EM Equities

Global Equities

A15 MAS

A10 MAS

A7 MAS (Since May 2018)

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

-0.50 -0.30 -0.10 0.10 0.30 0.50 0.70 0.90

Ex

pe

cte

d r

etu

rns o

ve

r 1

0 y

ea

rs1

Historical Correlation vs Global Equities2

Open

26

Nordea 1 – Alpha 15 MA Fund (BI-EUR)Performance*

* Up until March 18th, 2016, the sub-fund’s performance comprised performance fees.

Source (unless otherwise stated): Nordea Investment Funds S.A. Period under consideration (unless otherwise stated):

30/12/2011 - 31/12/2021. Performance calculated NAV to NAV (net of fees and Luxembourg taxes) in the currency of the

respective share class, gross income and dividends reinvested, excluding initial and exit charges as per 31/12/2021. Initial and

exit charges could affect the value of the performance. The performance represented is historical; past performance is not

a reliable indicator of future results and investors may not recover the full amount invested. The value of shares can

greatly fluctuate as a result of the sub-fund’s investment policy and cannot be ensured , you could lose some or all of

your invested money. If the currency of the respective share class differs from the currency of the country where the investor

resides the represented performance might vary due to currency fluctuations.

With effect from 14/12/2020, the official reference index of the fund is EURIBOR 1M. Prior to this date, the fund did not have an

official reference index. The fund performance since launch is measured against EURIBOR 1M. This reference index is used for

performance comparison purposes.

With effect as of 23/10/2017 the sub-fund is renamed from Nordea 1 - Alpha 15 to Nordea 1 - Alpha 15 MA Fund.**Inception date: 15.06.2011.

Calendar Year Returns in % Fund Reference index

2011

2012 10.14% 0.33%

2013 -3.26% 0.13%

2014 3.41% 0.13%

2015 9.61% -0.07%

2016 13.94% -0.34%

2017 12.76% -0.37%

2018 -4.38% -0.37%

2019 11.52% -0.40%

2020 12.66% -0.50%

YTD 16.58% -0.56%

Cumulative Returns in % Fund Reference index

YTD 16.58% -0.56%

1 month 4.21% -0.05%

3 months 4.79% -0.14%

6 months 8.49% -0.29%

1 year 16.58% -0.56%

3 years 46.47% -1.46%

5 years 57.93% -2.19%

Since inception 114.34% -1.31%**

Open

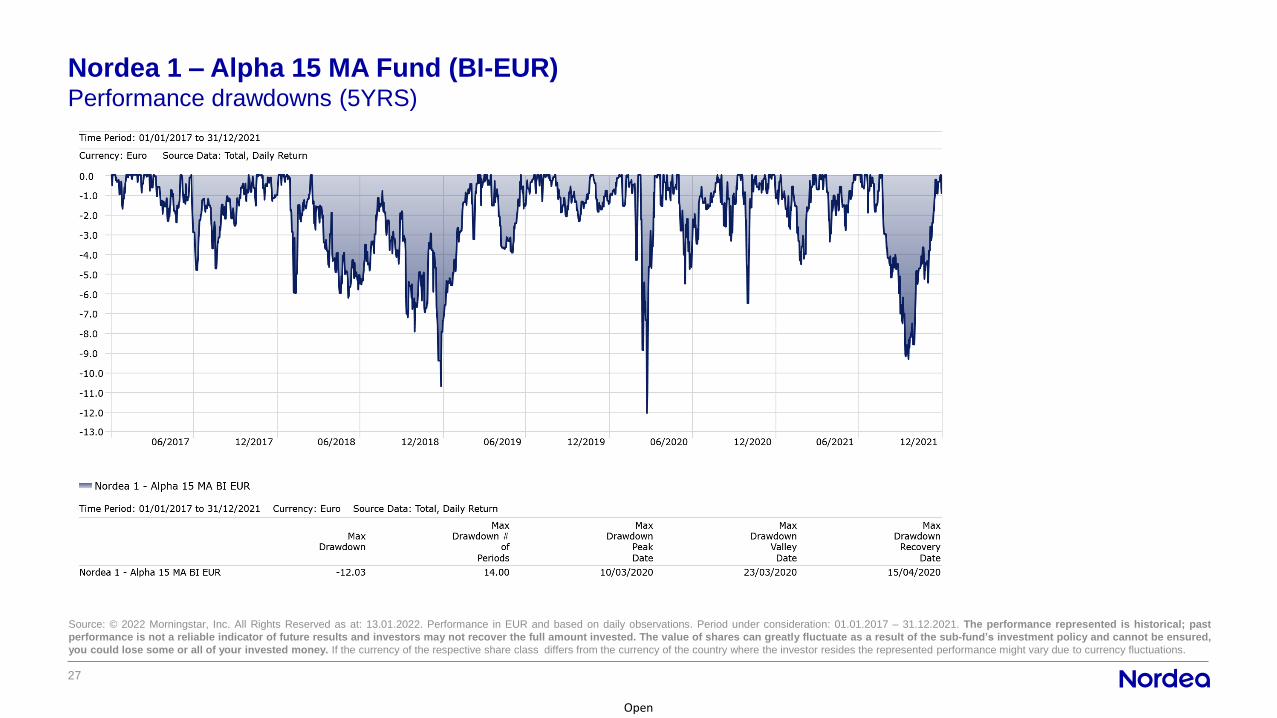

27

Nordea 1 – Alpha 15 MA Fund (BI-EUR)Performance drawdowns (5YRS)

Source: © 2022 Morningstar, Inc. All Rights Reserved as at: 13.01.2022. Performance in EUR and based on daily observations. Period under consideration: 01.01.2017 – 31.12.2021. The performance represented is historical; past

performance is not a reliable indicator of future results and investors may not recover the full amount invested. The value of shares can greatly fluctuate as a result of the sub-fund’s investment policy and cannot be ensured,

you could lose some or all of your invested money. If the currency of the respective share class differs from the currency of the country where the investor resides the represented performance might vary due to currency fluctuations.

Open

28

Key takeaways

• Extensive research: Relies on MAT’s

extensive research capabilities and experience

• Diversified source of returns: To offer higher

returns with lower risk than traditional asset

classes

• Risk Management: At the center of and

starting point for asset allocation

• Diversification: Low correlation to traditional

asset classes

• Liquid alternative with no performance fees

There can be no warranty that an investment objective, targeted returns and results of an investment structure is achieved. The value of your investment can go up and down, and you could lose some or all of your invested

money.

Appendix

Open

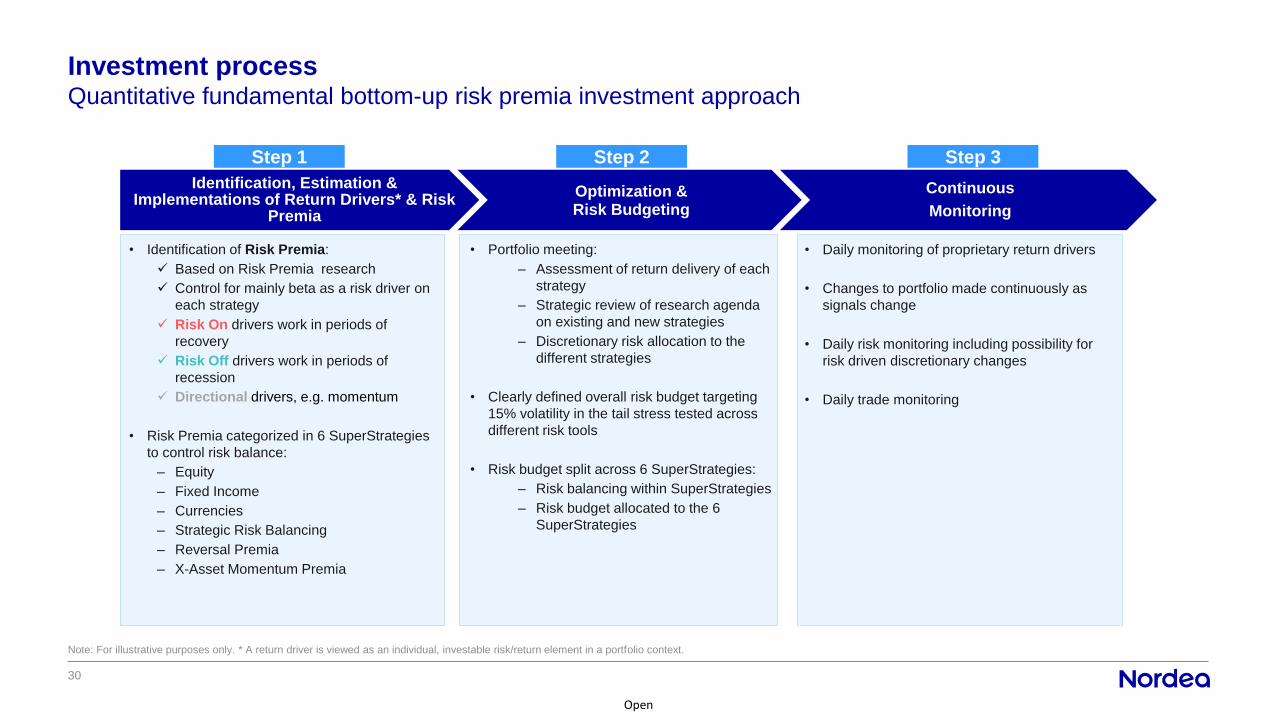

Quantitative fundamental bottom-up risk premia investment approach

Investment process

30

Note: For illustrative purposes only. * A return driver is viewed as an individual, investable risk/return element in a portfolio context.

Identification, Estimation & Implementations of Return Drivers* & Risk

Premia

Optimization & Risk Budgeting

Continuous

Monitoring

Step 1 Step 2 Step 3

• Portfolio meeting:

– Assessment of return delivery of each

strategy

– Strategic review of research agenda

on existing and new strategies

– Discretionary risk allocation to the

different strategies

• Clearly defined overall risk budget targeting

15% volatility in the tail stress tested across

different risk tools

• Risk budget split across 6 SuperStrategies:

– Risk balancing within SuperStrategies

– Risk budget allocated to the 6

SuperStrategies

• Daily monitoring of proprietary return drivers

• Changes to portfolio made continuously as

signals change

• Daily risk monitoring including possibility for

risk driven discretionary changes

• Daily trade monitoring

• Identification of Risk Premia:

✓ Based on Risk Premia research

✓ Control for mainly beta as a risk driver on

each strategy

✓ Risk On drivers work in periods of

recovery

✓ Risk Off drivers work in periods of

recession

✓ Directional drivers, e.g. momentum

• Risk Premia categorized in 6 SuperStrategies

to control risk balance:

– Equity

– Fixed Income

– Currencies

– Strategic Risk Balancing

– Reversal Premia

– X-Asset Momentum Premia

Open

31

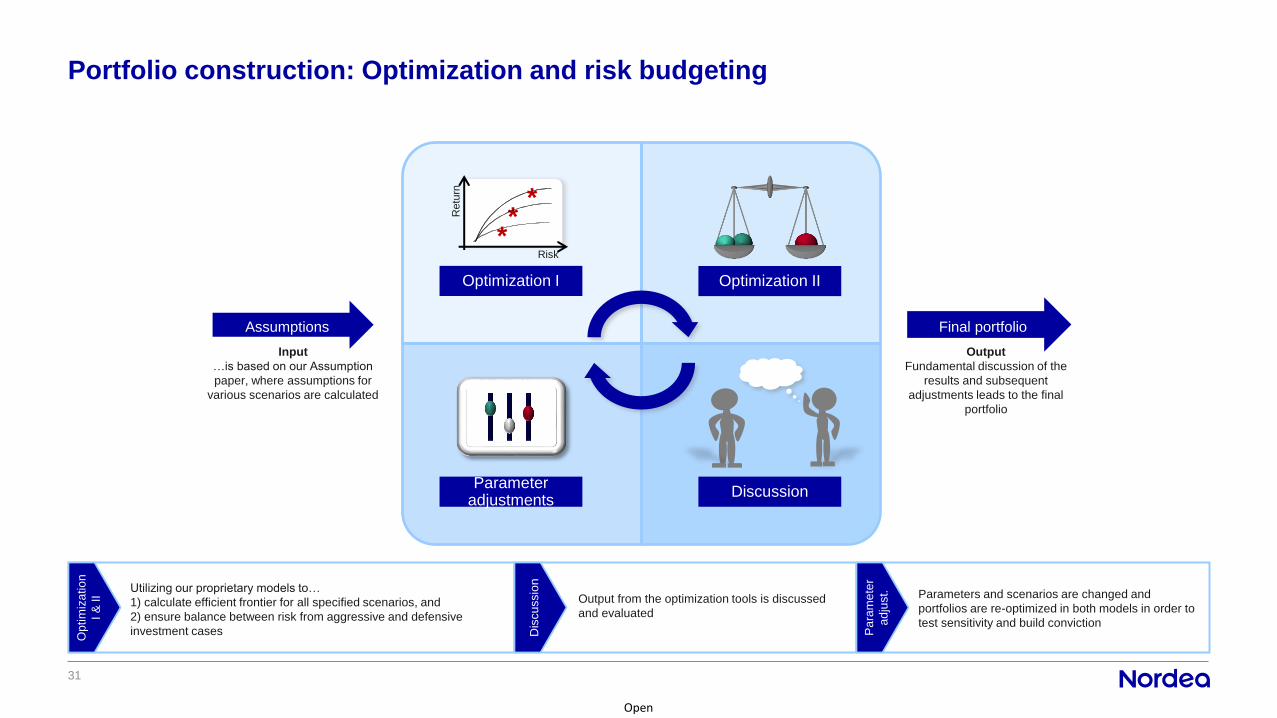

Portfolio construction: Optimization and risk budgeting

Assumptions

Input

…is based on our Assumption

paper, where assumptions for

various scenarios are calculated

Final portfolio

Output

Fundamental discussion of the

results and subsequent

adjustments leads to the final

portfolio

*

Risk

Retu

rn

*

*

Optimization IIOptimization I

Parameter adjustments

Discussion

Utilizing our proprietary models to…

1) calculate efficient frontier for all specified scenarios, and

2) ensure balance between risk from aggressive and defensive

investment cases

Output from the optimization tools is discussed

and evaluated

Parameters and scenarios are changed and

portfolios are re-optimized in both models in order to

test sensitivity and build conviction

Dis

cu

ssio

n

Op

tim

iza

tio

n

I &

II

Pa

ram

ete

r

ad

just.

Open

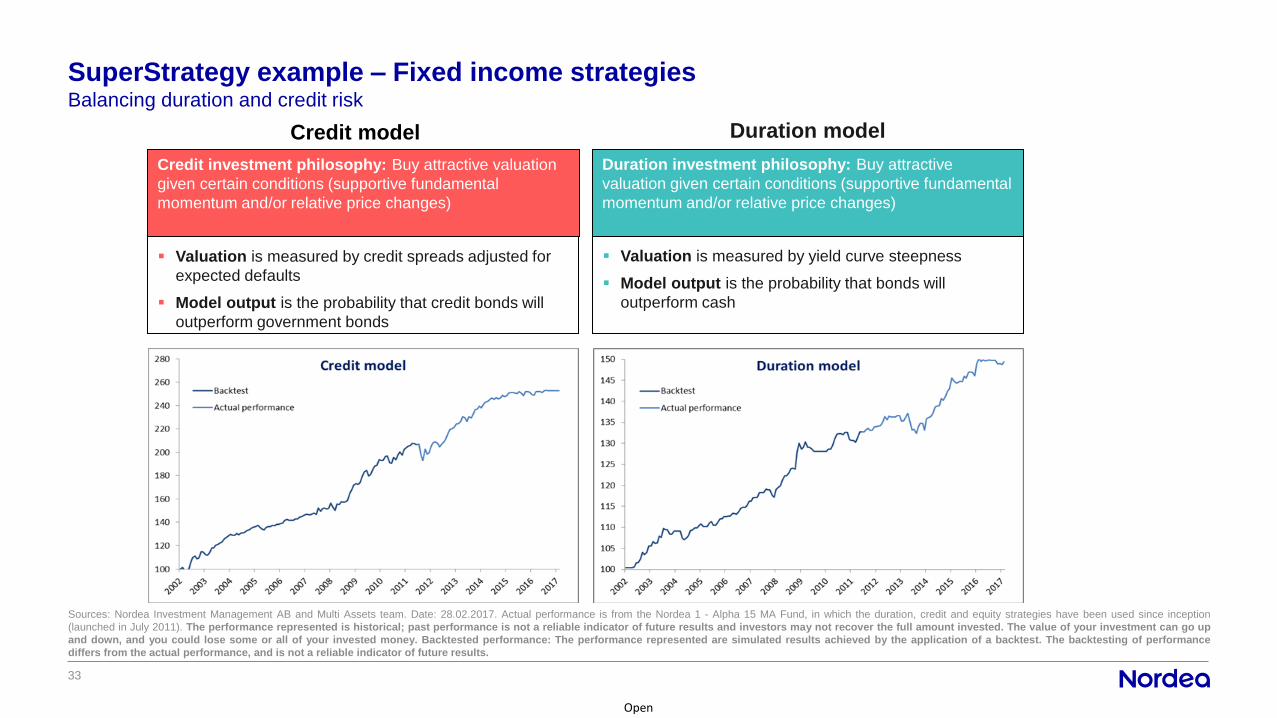

SuperStrategy example – Equity strategiesBalancing risk on and risk off equity strategies

-30%

-20%

-10%

0%

10%

20%

30%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Risk free rate Equity Beta Premium Low. Vol. Premium

▪ Premium: Equity country

▪ Trade: Long high Risk Premia equity country indices and sell low Risk Premia

equity country indices

▪ Risk/Return Control: Earnings momentum, sector deviation

▪ Instruments used: Equity Index Futures

Equity country strategy Low risk anomaly strategy

Beta positive: Exploiting relative equity risk premiums based on country

valuation and fundamental support; going long cheap and shorting expensive.

Anti-Beta: Isolating and exploiting the low risk anomaly premia; buying

relatively stable/low risk equities and hedging out the equity beta.

Low Risk Anomaly

premium

Equity Beta

premium

(0.7 beta)

Risk free rate

Low Risk

Equities

Sources: Nordea Investment Management AB. The performance for this composite represents all portfoliosmanaged as Global Stable Equities. Period under consideration: 01.01.2006 – 31.12.2016. There can be nowarranty that an investment objective, targeted returns and results of an investment structure is achieved.The value of your investment can go up and down, and you could lose some or all of your invested money.

Example of trades:

Sources: Nordea Investment Management AB. Date: 24.02.2016.

Largest Longs Largest Shorts

DAX INDEX FUTURE 3/2016 AMSTERDAM IDX FUT 3/2016

HANG SENG IDX FUT 3/2016 OMXS30 IND FUTURE 3/2016

CAC40 10 EURO FUT 3/2016 SPI 200 FUTURES 3/2016

2/24/2016

32

Open

33

SuperStrategy example – Fixed income strategiesBalancing duration and credit risk

Sources: Nordea Investment Management AB and Multi Assets team. Date: 28.02.2017. Actual performance is from the Nordea 1 - Alpha 15 MA Fund, in which the duration, credit and equity strategies have been used since inception

(launched in July 2011). The performance represented is historical; past performance is not a reliable indicator of future results and investors may not recover the full amount invested. The value of your investment can go up

and down, and you could lose some or all of your invested money. Backtested performance: The performance represented are simulated results achieved by the application of a backtest. The backtesting of performance

differs from the actual performance, and is not a reliable indicator of future results.

▪ Valuation is measured by yield curve steepness

▪ Model output is the probability that bonds will

outperform cash

▪ Valuation is measured by credit spreads adjusted for

expected defaults

▪ Model output is the probability that credit bonds will

outperform government bonds

Credit model Duration model

Credit investment philosophy: Buy attractive valuation

given certain conditions (supportive fundamental

momentum and/or relative price changes)

Duration investment philosophy: Buy attractive

valuation given certain conditions (supportive fundamental

momentum and/or relative price changes)

Open

34

SuperStrategy example – Currency strategiesBalancing FX carry and valuation

Sources: Nordea Investment Management AB. Date: 24.02.2016.

Beta positive: Relative yield; borrowing in a lower rate currency and

investing in a higher rate currency

Carry trade strategy FX valuation strategy

Anti-Beta: Benefiting from the relative FX valuation premiums based on the

fair value of currency crosses; going long cheap and shorting expensive

▪ Premium: Currency carry (attractive differential

between lower and higher rate currencies)

▪ Trade: Long high yield currencies and short low yield

currencies

▪ Risk/Return Control: Country fundamentals

▪ Instruments used: FX forwards

▪ Premium: Currency pairs exhibiting anti-beta

behavior (provides protection in stressed

market conditions)

▪ Trade: Long undervalued currencies and short

overvalued currencies that are negatively

correlated to equity markets

▪ Instruments used: FX forwards

▪ Typically performs well when risky assets are

struggling

Example of trades:

Largest Long

MXN

CLP

ZAR

Largest Short

ILS

CAD

CHF

Example of trades:

Largest Long

JPY

SEK

CAD

Largest Short

CHF

NZD

AUD

Open

35

SuperStrategy example – Strategic Risk Balancing strategiesRisk balancing the premia of the Assumption Paper

SAA Research & Analysis

Return Drivers & Risk Characteristics

Risk On DriversRisk Off Drivers

• Equity low volatility

• Duration region

• Covered bonds

• Credit low risk

• FX valuation (Purchasing

Power Parity principles)

• Equity beta

• Equity region

• Equity industry

• Equity size

• Equity style

• Credit risk premium

(EM, IG, HY)

Identification of all Return Drivers

Factor Risk Screening

Selection of relevant

Return Drivers

Note: For illustrative purposes only.

Open

36

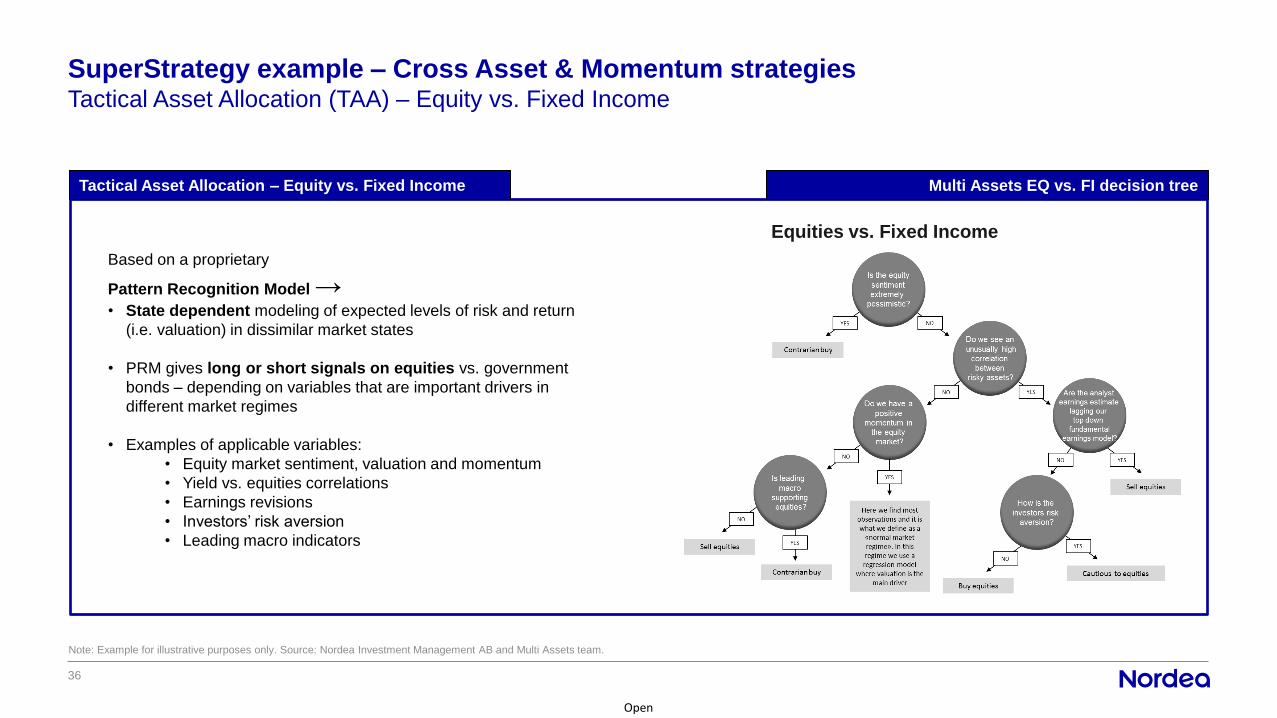

SuperStrategy example – Cross Asset & Momentum strategiesTactical Asset Allocation (TAA) – Equity vs. Fixed Income

Note: Example for illustrative purposes only. Source: Nordea Investment Management AB and Multi Assets team.

Tactical Asset Allocation – Equity vs. Fixed Income Multi Assets EQ vs. FI decision tree

Equities vs. Fixed Income

Based on a proprietary

Pattern Recognition Model →• State dependent modeling of expected levels of risk and return

(i.e. valuation) in dissimilar market states

• PRM gives long or short signals on equities vs. government

bonds – depending on variables that are important drivers in

different market regimes

• Examples of applicable variables:

• Equity market sentiment, valuation and momentum

• Yield vs. equities correlations

• Earnings revisions

• Investors’ risk aversion

• Leading macro indicators

Open

37

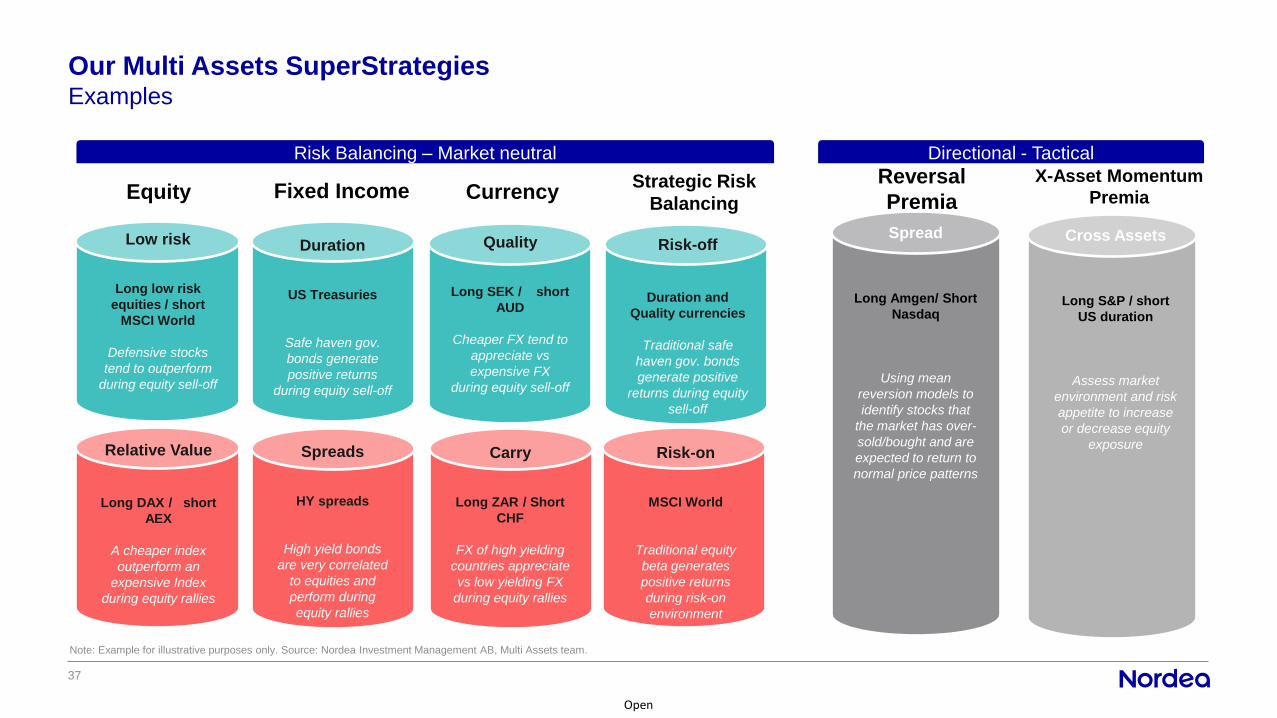

Our Multi Assets SuperStrategiesExamples

Note: Example for illustrative purposes only. Source: Nordea Investment Management AB, Multi Assets team.

Directional - TacticalRisk Balancing – Market neutral

Trading

Equity

Low risk

Long low risk

equities / short

MSCI World

Defensive stocks

tend to outperform

during equity sell-off

Fixed Income

Duration

US Treasuries

Safe haven gov.

bonds generate

positive returns

during equity sell-off

Currency

Quality

Long SEK / short

AUD

Cheaper FX tend to

appreciate vs

expensive FX

during equity sell-off

Strategic Risk

Balancing

Risk-off

Duration and

Quality currencies

Traditional safe

haven gov. bonds

generate positive

returns during equity

sell-off

Relative Value

Long DAX / short

AEX

A cheaper index

outperform an

expensive Index

during equity rallies

Spreads

HY spreads

High yield bonds

are very correlated

to equities and

perform during

equity rallies

Carry

Long ZAR / Short

CHF

FX of high yielding

countries appreciate

vs low yielding FX

during equity rallies

Risk-on

MSCI World

Traditional equity

beta generates

positive returns

during risk-on

environment

Reversal

Premia

Spread

Long Amgen/ Short

Nasdaq

Using mean

reversion models to

identify stocks that

the market has over-

sold/bought and are

expected to return to

normal price patterns

X-Asset Momentum

Premia

Cross Assets

Long S&P / short

US duration

Assess market

environment and risk

appetite to increase

or decrease equity

exposure

Open

38

Alpha 15 MA – Performance contributions (gross of fees)Calendar year & YTD

Note: Illustrative example based on the Alpha 15 MA Strategy (gross of fees). Source: Nordea Investment Management AB. The performance represented is historical; past performance is not a reliable indicator of future results and

investors may not recover the full amount invested. The value of your investment can go up and down, and you could lose some or all of your invested money.

December 31, 2010 - December 31, 2021

Sum of Contributions 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Currencies Premia -2.34% -0.46% -3.09% -2.57% 1.55% 1.73% 1.81% 1.42% 1.22% -2.86% -0.02%

Equity Premia 8.12% -4.89% -2.32% 8.34% 0.81% -1.38% 3.07% 2.56% 3.08% -1.35% 12.02%

Fixed Income Premia -2.01% 14.29% 4.84% 10.88% 3.48% 2.63% 2.49% 2.14% 1.08% 3.65% -0.42%

Strategic Risk Balancing Premia 0.77% 0.17% 7.02% 8.03% -1.56% 11.08% 12.26% 5.17%

Cross Asset and Momentum Premia -2.69% 5.77% 6.21% -8.87% 1.24% 4.61% 1.58% -1.85% -2.75% 5.39% 2.85%

Reversal Premia -3.26% 0.96% -5.01% -1.88% 7.28% 1.68% -1.15% -3.09% 0.47% -2.27% -1.27%

Cash and Implementation 1.98% -0.44% -0.45% -0.11% -0.17% 0.42% -1.33% -1.38% -2.02% -0.12% -0.91%

Grand Total -0.20% 15.24% 0.18% 6.56% 14.37% 16.71% 14.49% -1.77% 12.17% 14.70% 17.41%

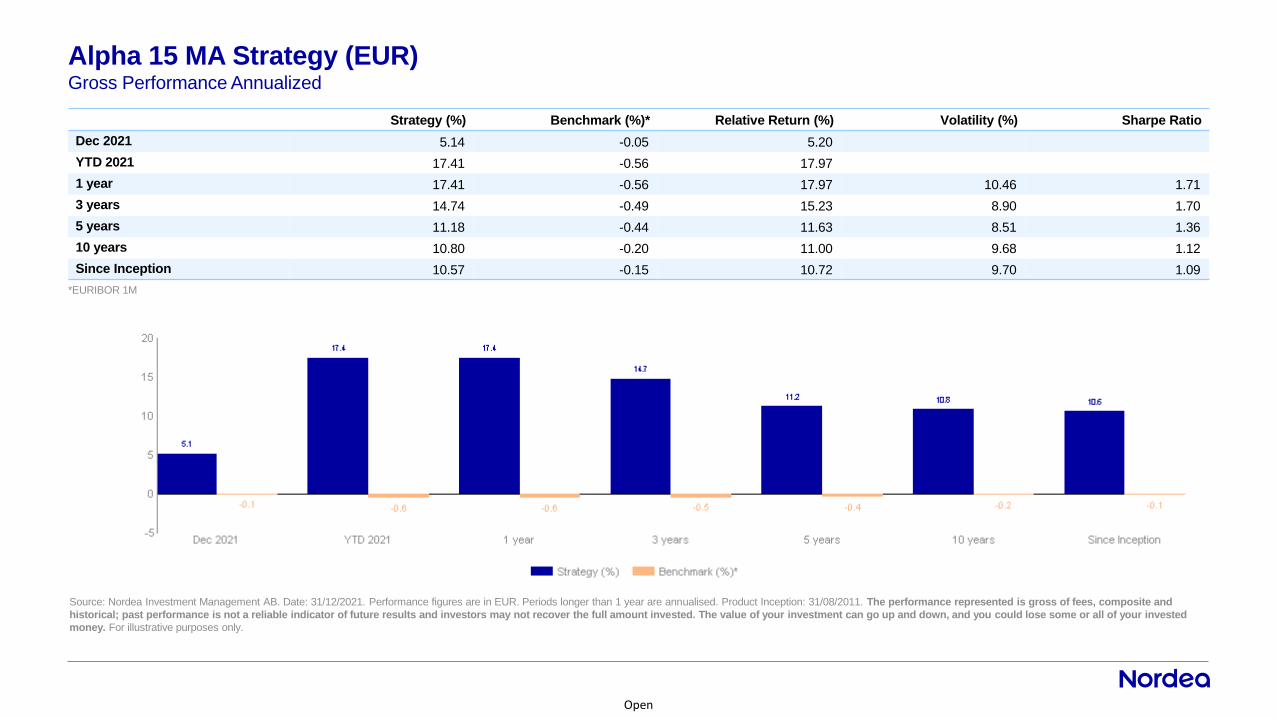

Open

Strategy (%) Benchmark (%)* Relative Return (%) Volatility (%) Sharpe Ratio

Dec 2021 5.14 -0.05 5.20

YTD 2021 17.41 -0.56 17.97

1 year 17.41 -0.56 17.97 10.46 1.71

3 years 14.74 -0.49 15.23 8.90 1.70

5 years 11.18 -0.44 11.63 8.51 1.36

10 years 10.80 -0.20 11.00 9.68 1.12

Since Inception 10.57 -0.15 10.72 9.70 1.09

*EURIBOR 1M

Source: Nordea Investment Management AB. Date: 31/12/2021. Performance figures are in EUR. Periods longer than 1 year are annualised. Product Inception: 31/08/2011. The performance represented is gross of fees, composite and

historical; past performance is not a reliable indicator of future results and investors may not recover the full amount invested. The value of your investment can go up and down, and you could lose some or all of your invested

money. For illustrative purposes only.

Gross Performance Annualized

Alpha 15 MA Strategy (EUR)

Open

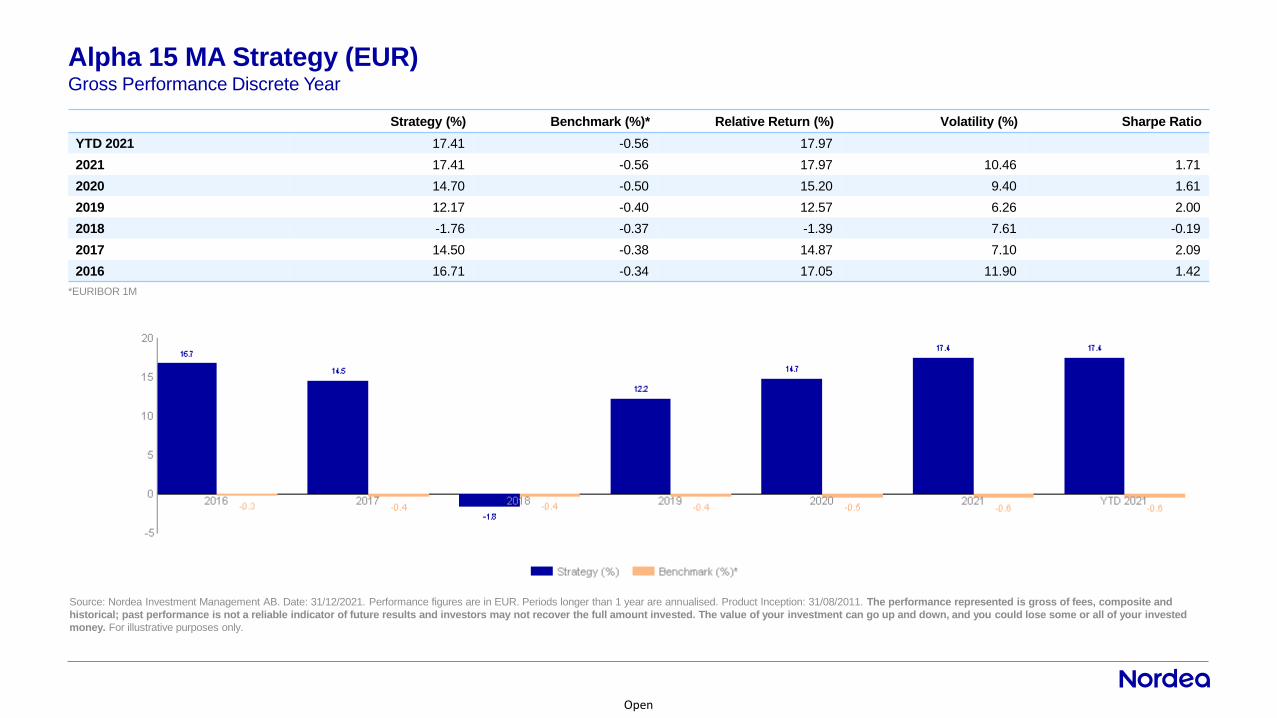

Strategy (%) Benchmark (%)* Relative Return (%) Volatility (%) Sharpe Ratio

YTD 2021 17.41 -0.56 17.97

2021 17.41 -0.56 17.97 10.46 1.71

2020 14.70 -0.50 15.20 9.40 1.61

2019 12.17 -0.40 12.57 6.26 2.00

2018 -1.76 -0.37 -1.39 7.61 -0.19

2017 14.50 -0.38 14.87 7.10 2.09

2016 16.71 -0.34 17.05 11.90 1.42

*EURIBOR 1M

Source: Nordea Investment Management AB. Date: 31/12/2021. Performance figures are in EUR. Periods longer than 1 year are annualised. Product Inception: 31/08/2011. The performance represented is gross of fees, composite and

historical; past performance is not a reliable indicator of future results and investors may not recover the full amount invested. The value of your investment can go up and down, and you could lose some or all of your invested

money. For illustrative purposes only.

Alpha 15 MA Strategy (EUR)Gross Performance Discrete Year

Open

41

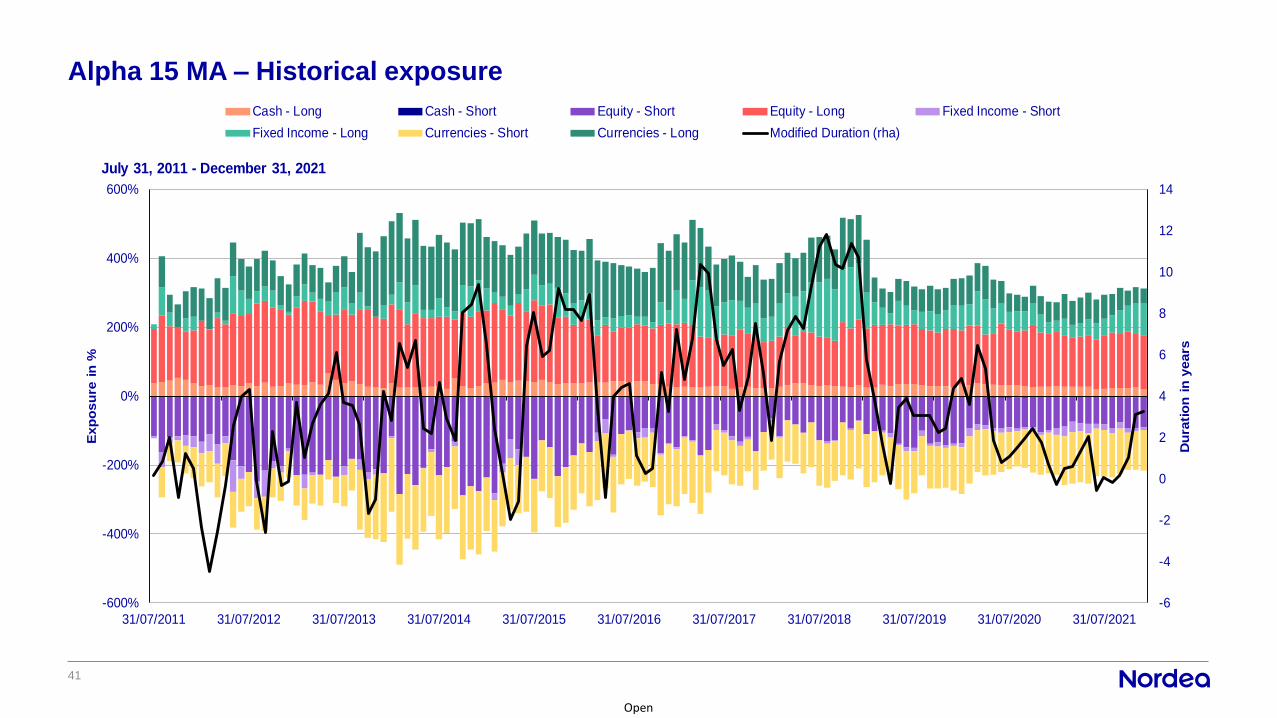

Alpha 15 MA – Historical exposure

-6

-4

-2

0

2

4

6

8

10

12

14

-600%

-400%

-200%

0%

200%

400%

600%

31/07/2011 31/07/2012 31/07/2013 31/07/2014 31/07/2015 31/07/2016 31/07/2017 31/07/2018 31/07/2019 31/07/2020 31/07/2021

Du

rati

on

in

years

Exp

osu

re i

n %

July 31, 2011 - December 31, 2021

Cash - Long Cash - Short Equity - Short Equity - Long Fixed Income - Short

Fixed Income - Long Currencies - Short Currencies - Long Modified Duration (rha)

Open

42

Alpha 15 MA – Historical exposure

-6

-4

-2

0

2

4

6

8

10

12

14

-400%

-200%

0%

200%

400%

600%

800%

1000%

1200%

31/07/2011 31/07/2012 31/07/2013 31/07/2014 31/07/2015 31/07/2016 31/07/2017 31/07/2018 31/07/2019 31/07/2020 31/07/2021

Du

rati

on

in

years

Exp

osu

re i

n %

July 31, 2011 - December 31, 2021

Total Gross Exposure Net Equity Exposure Modified Duration (rha)

Open

43

Alpha 15 MA – Historical net equity exposure

-100%

-50%

0%

50%

100%

150%

31/07/2011 31/07/2012 31/07/2013 31/07/2014 31/07/2015 31/07/2016 31/07/2017 31/07/2018 31/07/2019 31/07/2020 31/07/2021

Net

Eq

uit

y E

xp

osu

re i

n %

July 31, 2011 - December 31, 2021

Open

44

Nordea 1 – Alpha 15 MA Fund (BI-EUR)Fund information

Source: Nordea Investment Funds S.A. Date:

Sub-fund's name Nordea 1 - Alpha 15 MA Fund

Fund Manager Multi Assets Team

Fund Domicile 562, rue de Neudorf, 2220 Luxembourg, Luxembourg

Share class BI-EUR

Annual Man. Fee 1.200%

Security number (ISIN) LU0607983383

Security number (WKN) A1JHT2

Fund Size in millions 4,968.66

Currency EUR

Reference index EURIBOR 1M

No. of holdings 169

Launch date 15/06/2011

Minimum investment (EUR) 75,000

31.12.2021

Appendix

Open

NAM level Responsible Investment approaches – applicable to ALL our funds

46

NAM level ESG approaches

Active

Ownership

Norms-based

Screening

Exclusion

List

ESG

Integration

All holdings screened for

breaches of international

norms and conventions

We exercise our formal

voting rights and engage

with companies

Exclusion list publicly

available, as well as our RI

Policy which defines the

exclusion criteria

→ See next slide

ESG data made available for

all the portfolio managers to

integrate into the investment

decisions

Open

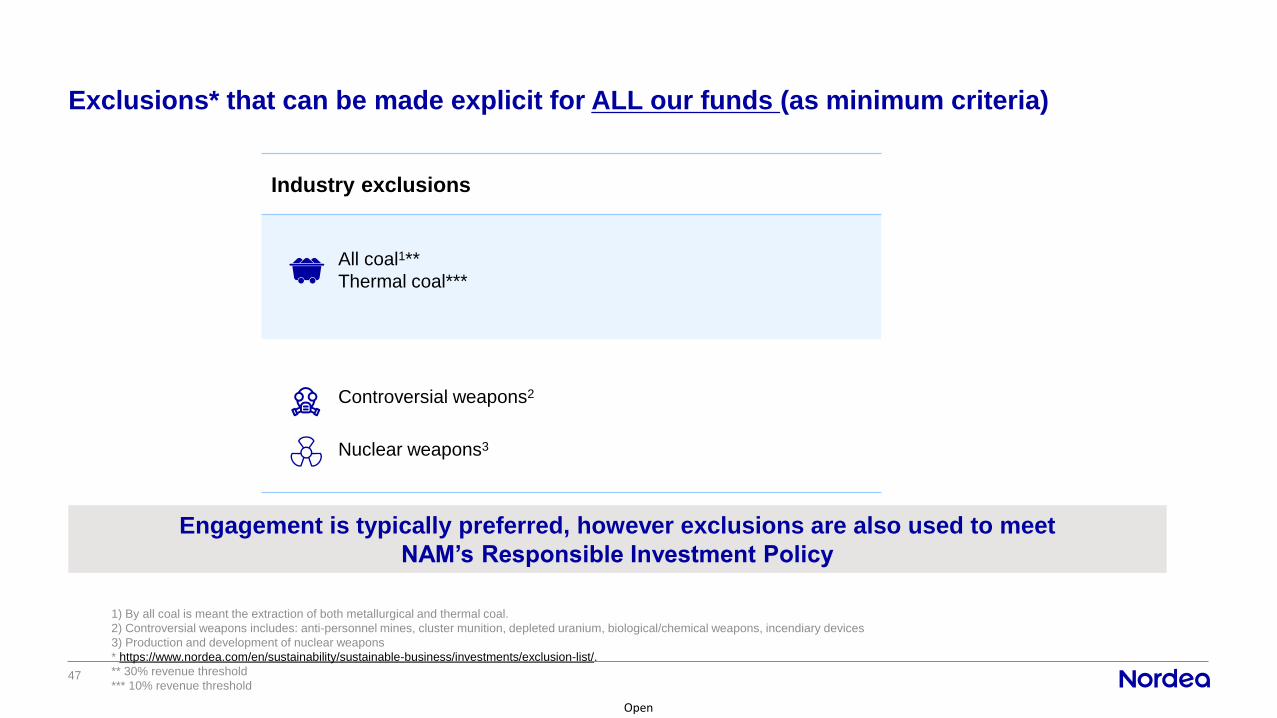

Exclusions* that can be made explicit for ALL our funds (as minimum criteria)

47

Industry exclusions

All coal1**

Thermal coal***

Controversial weapons2

Nuclear weapons3

Engagement is typically preferred, however exclusions are also used to meet

NAM’s Responsible Investment Policy

1) By all coal is meant the extraction of both metallurgical and thermal coal.

2) Controversial weapons includes: anti-personnel mines, cluster munition, depleted uranium, biological/chemical weapons, incendiary devices

3) Production and development of nuclear weapons

* https://www.nordea.com/en/sustainability/sustainable-business/investments/exclusion-list/.

** 30% revenue threshold

*** 10% revenue threshold

Open

48

The sub-funds mentioned are part of Nordea 1, SICAV, an open-ended Luxembourg-based investment company (Société d'Investissement à Capital Variable), validly formed and existing in accordance with the laws of Luxembourg and with

European Council Directive 2009/65/EC of 13 July 2009. This document is advertising material and does not disclose all relevant information concerning the presented sub-funds. Any investment decision in the sub-funds should be

made on the basis of the current prospectus and the Key Investor Information Document (KIID), which are available, along with the current annual and semi-annual reports, electronically in English and in the local language of the market

where the mentioned SICAV is authorised for distribution, without charge upon request from Nordea Investment Funds S.A., 562, rue de Neudorf, P.O. Box 782, L-2017 Luxembourg, from the local representatives or information agents, or

from our distributors as well as on www.nordea.lu. Investments in derivative and foreign exchange transactions may be subject to significant fluctuations which may affect the value of an investment. Investments in Emerging Markets

involve a higher element of risk. The value of shares can greatly fluctuate as a result of the sub-fund’s investment policy and cannot be ensured. Investments in equity and debt instruments issued by banks could bear the

risk of being subject to the bail-in mechanism (meaning that equity and debt instruments could be written down in order to ensure that most unsecured creditors of an institution bear appropriate losses) as foreseen in EU

Directive 2014/59/EU. For further details of investment risks associated with these sub-funds, please refer to the relevant Key Investor Information Document (KIID), available as described above. Nordea Investment Funds S.A.

has decided to bear the cost for research, i.e. such cost is covered by existing fee arrangements (Management-/Administration-Fee). Nordea Investment Funds S.A. only publishes product-related information and does not make any

investment recommendations. A summary of investor rights is available in English through the following link: https://www.nordea.lu/documents/engagement-policy/EP_eng_INT.pdf/. Nordea Investment Funds S.A. may decide to terminate the

arrangements made for the marketing of its sub-funds in any respective EU-country of distribution in accordance with Article 93a of Directive 2009/65/EC. Published by Nordea Investment Funds S.A., 562, rue de Neudorf, P.O. Box 782, L-

2017 Luxembourg, which is authorized by the Commission de Surveillance du Secteur Financier in Luxembourg. Further information can be obtained from your financial advisor. He/she can advise you independently of Nordea Investment

Funds S.A. Please note that all sub funds and share classes might not be available in your country of jurisdiction. Additional information for investors in Switzerland: The Swiss Representative and Paying Agent is BNP Paribas

Securities Services, Paris, Succursale de Zurich, Selnaustrasse 16, 8002 Zurich, Switzerland. Additional information for investors in Germany: The Information Agent in Germany is Société Générale S.A. Frankfurt Branch, Neue Mainzer

Straße 46-50, 60311 Frankfurt am Main, Germany. A hard copy of the above-mentioned fund documentation is also available here. Additional information for investors in Austria: The Information and Paying Agent in Austria is Erste Bank

der österreichischen Sparkassen AG, Am Belvedere 1, 1100 Vienna, Austria. Additional information for investors in the Netherlands: Nordea 1, SICAV is a Luxembourg Undertaking for Collective Investment in Transferable Securities

(UCITS) registered in the Netherlands in the register kept by the AFM, and as such is allowed to offer its shares in the Netherlands. The AFM register can be consulted via www.afm.nl/register. Additional information for investors in

France: With the authorisation of the AMF the shares of the sub-funds of Nordea 1, SICAV may be distributed in France. Centralising Correspondent in France is CACEIS Bank, located at 1-3, place Valhubert, 75206 Paris cedex 13, France.

Investors are advised to conduct thorough research before making any investment decision. Additional information for investors in Belgium: The Financial Service Agent in Belgium is BNP Paribas Securities Services S.C.A.,

Brussels Branch, Rue de Loxum, 25, 1000-Brussels, Belgium. A hard copy of the above-mentioned fund documentation is available upon demand free of charge. Additional information for investors in Spain: Nordea 1, SICAV is duly

registered in the CNMV official registry of foreign collective investment institutions (entry no. 340) as authorised to be marketed to the public in Spain. The Depositary of the SICAV’s assets is, J.P. Morgan Bank Luxembourg S.A. In Spain, any

investment must be made through the authorised distributors and on the basis of the information contained in the mandatory documentation that must be received from the SICAV’s authorised distributor prior to any subscription. The

Representative Agent is Allfunds Bank S.A.U., C/ de los Padres Dominicos, 7, 28050 Madrid, Spain. A complete list of the authorised distributors is available in the CNMV’s webpage (www.cnmv.es). Additional information for investors in

Portugal: The Management Company of the SICAV, Nordea Investment Funds S.A., and the Depositary of the SICAV’s assets, J.P. Morgan Bank Luxembourg S.A., are validly formed and existing in accordance with the laws of Luxembourg

and authorized by the Commission de Surveillance du Secteur Financier in Luxembourg. The Paying Agent in Portugal is BEST - Banco Electrónico de Serviço Total, S.A., duly incorporated under the laws of Portugal and registered with the

CMVM as a financial intermediary. Additional information for investors in Italy: Fund documentation as listed above is also available in Italy from the distributors and on the website www.nordea.it. The updated list of distribution agents in

Italy, grouped by homogenous category, is available from the distributors themselves or from the Paying Agents: State Street Bank International GmbH – Succursale Italia, Allfunds Bank S.A.U. – Succursale di Milano, Société Générale

Securities Services S.p.A., Banca Sella Holding S.p.A, Banca Monte dei Paschi di Siena S.p.A., CACEIS Bank S.A.,Italian Branch and on the website www.nordea.it. Any requests for additional information should be sent to the distributors.

Before investing, please read the prospectus and the KIID carefully. We recommend that you read the most recent annual financial statement in order to be better informed about the fund's investment policy. The prospectus and KIID

for the sub-funds have been published with Consob. For the risk profile of the mentioned sub-funds, please refer to the fund prospectus. Additional information for investors in the United Kingdom: The Facilities Agent is FE Fundinfo

(UK) Limited., 3rd Floor, Hollywood House, Church Street East, Woking GU21 6HJ, United Kingdom. Additional information for investors in Ireland: The Facilities Agent is Maples Fund Services (Ireland) Limited, 32 Molesworth Street,

D02 Y512 Dublin 2, Ireland. Additional information for investors in Sweden: The Paying Agent is Nordea Bank Abp, Swedish Branch, Smålandsgatan 17, 105 71 Stockholm, Sweden. Additional information for investors in Denmark:

The Representative Agent is Nordea Danmark, Filial af Nordea Bank Abp, Finland, Grønjordsvej 10, Postbox 850 0900 CopenhagenC, Denmark. A hard copy of the above-mentioned fund documentation is available here. Additional

information for investors in Norway: The Nordea 1, SICAV is registered in Norway. Additional information for investors in Finland: The Nordea 1, SICAV is registered in Finland. Additional information for investors in Latvia: The

Representative Agent is Luminor Bank AS, 62 Skanstes iela 12, 1013 Riga, Latvia. Additional information for investors in Estonia: The Representative Agent in Estonia is Luminor Bank AS, Liivalaia 45, 10145 Tallinn, Estonia. Additional

information for investors in Lithuania: The Representative Agent in Lithuania is Luminor Bank AB, Konstitucijos pr. 21 A, 03601 Vilnius, Lithuania. Shareholders must evaluate possible investment risks and take this into consideration

when making investment decisions. Additional information for investors in Brazil: This is a strictly privileged and confidential document for the purposes of a potential investment in foreign securities on a one-on-one basis with potential

investors with a pre-existing relationship with Nordea Investment Funds S.A. This document contains information addressed only to a specific individual and is not intended for distribution to, or use by, any other person. This document (i) is

provided for informational purposes only, (ii) should not be construed in any manner as any solicitation or offer to buy or sell any securities or any related financial instruments, (iii) should not be construed in any manner as a public offer of any

securities or any related financial instruments, and (iv) and will be addressed to a potential investor with restrict access of information. Neither Nordea Investment Funds S.A nor Nordea 1, SICAV have been, and will not be, registered with the

Brazilian Securities Commission (Comissão de Valores Mobiliários - CVM). Nordea 1, SICAV must not be offered or sold in Brazil except in circumstances which do not constitute a public offering or distribution under Brazilian laws and

regulations. Any public offering, placement or distribution, as defined under Brazilian laws and regulations, of securities in Brazil, is not legal without prior registration under Law No. 6,385 of December 7, 1976, as amended. Documents

relating to the offering of the Nordea 1, SICAV, as well as information contained therein, must not be supplied to the general public in Brazil (as the offering of the Nordea 1, SICAV is not a public offering of securities in Brazil) or used in

connection with any offer for subscription or sale of the Nordea 1, SICAV to the general public in Brazil. Investors within Brazil should consult with their own counsel as to the applicability of these laws and regulations or any exemption there

from. Source (unless otherwise stated): Nordea Investment Funds S.A. Unless otherwise stated, all views expressed are those of Nordea Investment Funds S.A. This document may not be reproduced or circulated without prior permission

and must not be passed to private investors. This document contains information only intended for professional investors and financial advisers and is not intended for general publication. Reference to companies or other investments

mentioned within this document should not be construed as a recommendation to the investor to buy or sell the same but is included for the purpose of illustration. The level of tax benefits and liabilities will depend on individual

circumstances and may be subject to change in the future.