nonresidential construction index report q3 2016

TRANSCRIPT

EXECUTIVE SUMMARY“ONE OF THE GREATEST PIECES OF ECONOMIC WISDOM IS TO KNOW WHAT YOU DO NOT KNOW.” — John Kenneth Galbraith

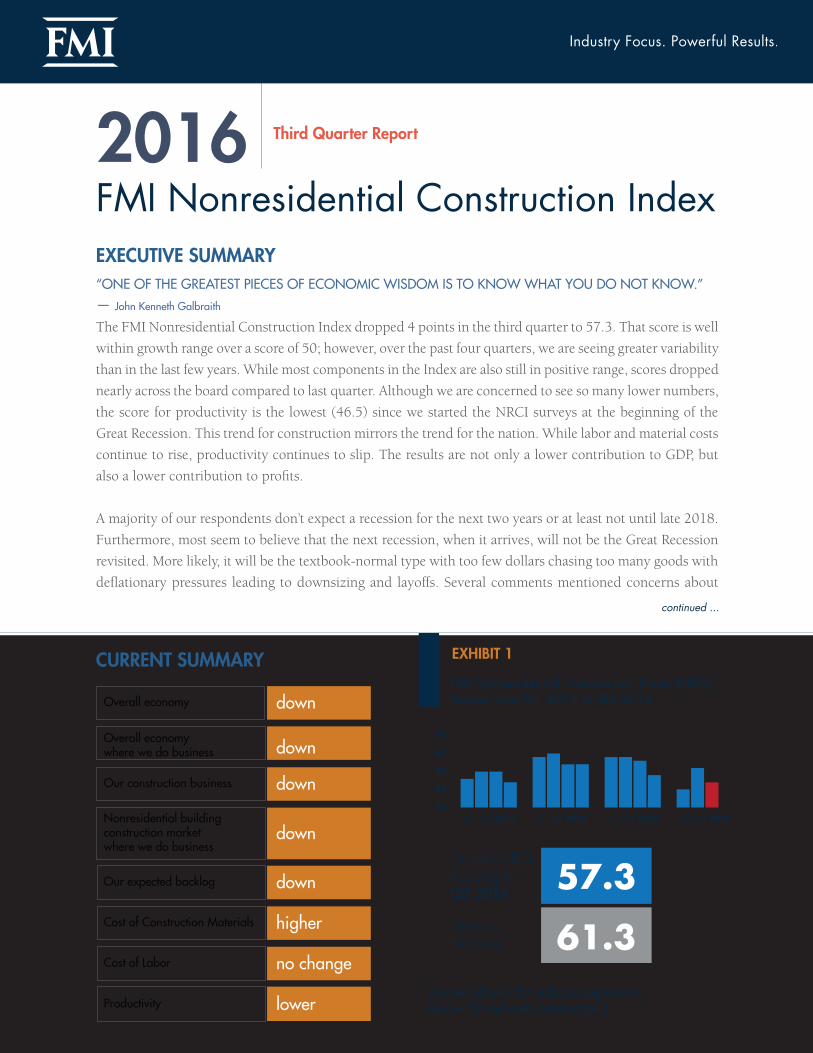

The FMI Nonresidential Construction Index dropped 4 points in the third quarter to 57.3. That score is well

within growth range over a score of 50; however, over the past four quarters, we are seeing greater variability

than in the last few years. While most components in the Index are also still in positive range, scores dropped

nearly across the board compared to last quarter. Although we are concerned to see so many lower numbers,

the score for productivity is the lowest (46.5) since we started the NRCI surveys at the beginning of the

Great Recession. This trend for construction mirrors the trend for the nation. While labor and material costs

continue to rise, productivity continues to slip. The results are not only a lower contribution to GDP, but

also a lower contribution to profits.

A majority of our respondents don’t expect a recession for the next two years or at least not until late 2018.

Furthermore, most seem to believe that the next recession, when it arrives, will not be the Great Recession

revisited. More likely, it will be the textbook-normal type with too few dollars chasing too many goods with

deflationary pressures leading to downsizing and layoffs. Several comments mentioned concerns about

FMI Nonresidential Construction Index

Third Quarter Report2016

CURRENT SUMMARY

(Scores above 50 indicate expansion, below 50 indicate contraction.)

continued ...

downOverall economy

Overall economywhere we do business

Our construction business

Nonresidential buildingconstruction marketwhere we do business

Our expected backlog

Cost of Construction Materials higher

Cost of Labor no change

Productivity lower

down

down

down

down

EXHIBIT 1

FMI Nonresidential Construction Index2

Executive Summary

markets that are beginning to be overbuilt in this latest expansion. However, as one respondent describes,

there are still many things we do not know:

Uncertainty is a word that a lot of people are using to describe our world today. Uncertainty

of: the current election and politics in general, Brexit, monetary policy, the longest bull-market

in history, the length of the current economic expansion, the total debt and deficit spending,

etc. The one thing that is certain is that we will eventually have a recession, and I hope this

time it is shallow to the point that we are out of it before the economists even measure and

announce the two down quarters!

See more detailed responses in this report to discover what we do and do not know. There will be another

recession. That is one thing we can say with great confidence.

A special thank you to all of the panelists who help make the NRCI a useful gauge of nonresidential construction activity. We value your opinions and appreciate your taking the time to share your experience.

FMI Nonresidential Construction Index3

Overall Economy: NRCI respondents’ view of the overall economy

dropped 7.3 points in the third quarter. While

this is a sharp drop from the second quarter

results, the second quarter spiked 8.9 points from

the first quarter..

Overall Economy Where Panelists Do Business: As with the overall economy, respondents’

optimism in the second quarter seems to have

pulled back to what we have seen in previous

quarters. Now at 60.4, this NRCI component

continues in a positive range.

Respondents’ Construction Business:Respondents reported that their outlook for their

own business slowed somewhat this quarter,

dropping 5.1 points to 70.9. A few actually

welcome the change, since some markets have

been “overheated.”

Nonresidential Building Construction Market Where Panelists Do Business: At 67.3, the nonresidential market that

respondents work in is still registering high on

the component scale, but 7.0 points lower than

last quarter.

NRCI Third Quarter 2016 Highlights

Expected Change in Backlog: The Index component for expected change in

backlog dropped 7.2 points in the third quarter

to a still positive 58.9. The median backlog for all

respondents was 10 months for the third quarter,

which is a drop from the last three quarters but

on par with the past two years, where backlog

hovered between nine and 10 months.

Cost of Construction Materials and Labor: The Index for cost of materials dropped 2.9 points,

indicating materials prices are still rising. Likewise,

the labor cost component, although unchanged

from last quarter, continues to indicate higher costs

for labor that is still scarce in many areas.

Productivity: Productivity continues to be a big concern as

the component Index slipped to 46.5, or 5.9

points lower than last quarter. This is the lowest

score for productivity since we began publishing

the NRCI report in 2008. Likely, the drop is

mostly indicative of the continuing difficulty

of finding skilled employees in a tight market;

however, there are many other reasons for loss of

productivity.

FMI Nonresidential Construction Index4

EXHIBIT 2

(Scores higher than 50 indicate expansion, below 50 indicate contraction.)

Predicting the recession: We asked respondents to give their estimated opinion about when they think the next recession will begin,

particularly as concerns the construction industry. Overall, 78% didn’t expect a recession until at least the

first half of 2018, and 38% of those respondents don’t expect a recession for at least two years.

Predicting continued growth during the current expansion: Most people expect a recession sometime, given the cyclical nature of construction and the economy in

general, so we asked what kind of growth in construction to expect until the “inevitable” recession occurs.

Thirty-five percent of respondents expect 1 to 2% growth (CAGR) during the remaining expansionary period,

while 32% expect 3 to 4% growth.

Current IssuesN

RCI S

core

0

10

20

30

40

50

60

70

Q1-Q42011

Q1-Q42012

Q1-Q42013

Q1-Q42014

Q1-Q42015

Q1-Q32016

57.3

Current NRCIReading forQ3 2016

57.3Previous Reading 61.3

FMI Nonresidential Construction Index (NRCI) Scores | Q1 2011 to Q3 2016

FMI Nonresidential Construction Index5

Predicting the Recession: Predicting the next economic recession has long been

a cottage industry in economic reporting. These days

it seems to be a growing concern with many online

pundits sending out dire warnings, hoping that you will

buy something they are selling or gain fame and credit

for being the one lone wolf who successfully predicted

economic demise. The noise in the media tends to crowd

out the level-headed economists genuinely attempting to

calculate the ongoing chances for growth or recession.

For the purpose of our questions on predicting the next

recession, we used the standard applied by the National

Bureau of Economic Research (NBER):

A recession is a period between a peak and a trough, and an expansion is a period between

a trough and a peak. During a recession, a significant decline in economic activity spreads

across the economy and can last from a few months to more than a year. Similarly, during an

expansion, economic activity rises substantially, spreads across the economy and usually lasts

for several years.

In addition to the formal definition of a recession, we asked respondents to focus their responses on the

potential for the recession to affect the construction industry. Seventy-eight percent do not expect a recession

until at least the first half of 2018, and 38% of those responding do not expect a recession for at least two years

(Exhibit 2). Since the responses to this question are based on reasoned opinions and experience, we further

handicapped the results by asking respondents to estimate the certainty of their responses. Although most

responses clustered around the 50/50 level, the longer-term predictions were also the stronger predictions

according to respondents’ degree of certainty—where 10 equals the highest degree of certainty. (There were

no 10s.)

For the first quarter NRCI report, we asked respondents to estimate construction put in place for 2016. To

provide a counterpoint to the recession predictions above, we asked respondents what growth level they

expected for the design and construction industry during the current expansion. Although the questions

are not directly compatible, the answers were similar. Thirty-five percent of respondents expect 1% to

2% growth during the remaining expansionary period, while 32% expect 3% to 4% growth until the next

recession occurs. (In the first quarter, 31% expected construction for 2016 to grow between 0.5% and 5%.

Thirty-nine percent expected growth from 2.6% to 5.0%.)

Current Issues

FMI Nonresidential Construction Index6

We also asked executives responding to our survey this quarter what they thought might be the top-three

reasons or causes. We have depicted those responses in a “word cloud” graphic format to indicate the number

of mentions of key words. Although not a highly scientific representation of the data, the graphic shows the

larger concerns are not only economic, but also political and global. The economy is, of course, the focus

here, and the large print for the economy includes several comments concerning the business cycle and the

feeling that “we are due” or overdue for a recession. The presidential race, uncertainty and even low confidence

levels in the government’s ability to help prevent a severe recession are also big concerns. Falling demand

in the face of overbuilding in some markets is a concern also reflected in the open-ended responses below

(Exhibit 5). In the open-ended responses, we can get the sense that this isn’t the first time NRCI industry

executives thought about these issues and when the recession might hit. There is uncertainty behind many

responses, but most seem to agree (or hope) that the next recession might be more of the “normal” type

with no major bubble bursting like the securities markets or residential markets as in the beginning of the

Great Recession. There are some who not only feel we are due for a correction, but also think it might be a

necessary change from some of the overheated markets faced today.

Word Cloud: Key word responses for reasons and causes of the next recession. (Font size represents number of mentions.)

EXHIBIT 3

FMI Nonresidential Construction Index7

What is your best estimate of when a recession will next affect the economy, specifically the design and construction industry?

EXHIBIT 4

How do you expect the design and construction industry to perform during the expansion period from now up to the next recession? (CAGR, Compound Annual Growth Rate)

EXHIBIT 5

FMI Nonresidential Construction Index8

Selected comments on the chance and causes of potential recession or expansion for the construction economy:

EXHIBIT 6

� 75% overbuilding and rising labor and material costs.

� Costs increases are spotty, so overall, not sure what heavy increases there might be. There are many needs such as infrastructure, flat office building market, education reform, bigger than normal cultural changes that increase the obsolescence of old buildings, thus new buildings are required. Our dominant market, Memphis, is growing with an energy like never before, and that creates construction potential.

� Election results could cripple the U.S. economy for further growth. Too many entitlement promises would further shift spending to programs that do not improve infrastructure or entice business development. States will not be able to support themselves, thus no incentives for business.

� Everything always comes to an end. The economy is on an eight-year uptick since the start of the Great Recession and typically runs max out at eight years. This one will probably run a little longer because of interest rates being kept so low for so long. Everything is cyclical.

� Expansion because indicators still show increased need and demand. People resources are hindering growth.

� Flight to safety in the U.S.A., which should lead to increased investment in buildings and infrastructure.

� I think we will continue to see steady growth in our industry. There may be some bumps in the road, but I do not believe there will be anything like what happened in 2008.

� If the rising cost of construction continues, owners are going to begin shelving projects until the cost comes back down. We are already seeing this happen in the Miami (South Florida) market with condos. We will also face a slowdown with the general election this year. If another democratic president gets elected, the construction industry will suffer.

� In our markets, the engineering and architectural firms are reporting to be very busy. We will be very busy for at least two years after they slow down.

� Industry is currently building too much to sustain the level of activity. We are over-building some segments of the market due to low cost of money. And with the rising cost of construction due to the amount of work in the pipeline and scarcity of labor, some projects no longer pencil.

� Instability overseas. Either a crash in the Japanese yen or the failure of a major bank in Europe.

� It will not be another financial meltdown. It will be something geopolitical if there is a big recession. The next recession will be a market correction where developers have overbuilt an area of the market, and the market does not sustain the demand. It will be a more typical recession.

� Locally, we see many apartments, hospitals and breweries springing up and expanding. Housing sales just exceeded pre-recession levels. There are state and local bonds for schools. We are in a boom for another year or two (it took almost two years for the recession to hit us locally, and then it hit hard). It looks like a very similar boom/bust

FMI Nonresidential Construction Index9

cycle, and I have no confidence that either presidential candidate will be good for the economy long term.

� No recession in sight. There always is a slowdown but for different reasons. The world climate is unsettling, but we have not been able to identify a specific cause for the next downturn,

� Overbuilding of multifamily and health care. Stress of the coal, oil and gas industry.

� Overbuilding is a significant risk, particularly in multifamily.

� Prodigious talent loss at the bottom of the last trough has not and will not be replaced in a stagnant (less than 2%) growth economy. This is a problem for the design, construction and civil authorities’ fields and will persist until the replacement employees gain experience. Further, the people who enter the industry at this time are not same caliber as we saw in earlier expansions, which will exacerbate the talent drain. Technology leaps are being implemented in an industry that has traditionally skimped on training,

utilizing on-the-job experience as a substitute for instruction. Increasing labor costs will be combined with diminished productivity.

� Slight expansion because of pent-up demand and low interest rates.

� Some geopolitical event that cannot be predicted.

� The Bay Area office market is strong but declining to the zero side (net leases) with 20% sublease space vacancy competing with normal office turnover and another 3 million to 4 million feet of new site space coming on market within 12-18 months. Classic oversupply dynamics forming, coupled with overvalued, pre-IPO tech firms that are having their funding cut or reduced will lead to headcount layoffs. In addition, lack of sales growth for large firms, along with the dollar costing them money outside the U.S., leads to M&As to grow and layoffs to show profits. We have seen RFP requests downtrend for six months to what would appear to be normalized levels, but, in fact, they continue to downtrend monthly and quarterly. For now, it all looks like a normal

FMI Nonresidential Construction Index10

cycle downturn recession of 10-30%, but if credit markets begin to show pain in the form of defaults on corporate bond debt or commercial real estate defaults due to valuation adjustments, look out; 2018-2020 could be really bad. For now, we see a mid-2017 normal recession call lasting two to three years as supply versus demand normalizes.

� The November presidential election results will impact the overall national economy. If a Republican wins the election, I expect that the economy will expand. If a Democrat wins the election, I expect that the economy will grow at a slower pace and may turn toward recession.

� Uncertainty is a word that a lot of people are using to describe our world today. Uncertainty of: the current election and politics in general, Brexit, monetary policy, the longest bull market in history, the length of the current economic expansion, the total debt and deficit spending, etc. The one thing that is certain is that we will eventually have a recession, and I hope this time it is shallow to the point that we are out of it before the economists even measure and announce the two down quarters!

� We are anticipating a mild to moderate recession within the design and construction industry in late 2019. Expecting to see signs at the consumer retail level of the economy to appear in late 2018, which will be an early indicator of recession of nonresidential construction approximately 12 months following a slowdown in early indicator industries, such as retail, housing and automobiles. The next recession will likely be induced by government policy. As the economy improves globally in 2017, interest rates (should) rise. As interest rates rise, governments will be forced to face looming deficits and aging population demographics. Europe, Japan and North America are included in this situation. Belt tightening in

the form of reduced government spending stimulus or increased taxation will cause headwinds for global GDP, pushing us into our next recession, which we are expecting should be mild to moderate, as we find our way forward.

� We believe there is no long-term confidence in the industrial market clients. They will plan or budget a project but don’t have a definite schedule. When they choose to do a project, it starts immediately, and they compress the schedule. They are in a reactionary mode.

� We don’t have the capacity to expand as an industry. A recession would help us catch our breath and function more normally than we are now. We are keeping an unsustainable pace now. Let’s slow it down for all our sakes.

� We need a change in Washington to get our economy to grow. Not sure Republicans in the House can get organized and work with the Senate to get something done. Just not optimistic about our federal government.

� We need to get back to a normal economy with slightly higher interest rates so banks can become more profitable and not so conservative when lending to small businesses.

� What goes up must come down. By the time we have the next significant recession, it might be about 10 years from the beginning of the Great Recession. The Bay Area is white-hot and has been for the past year, will be for the next year (I hope), so I expect a drop off sometime in 2018 due to all the above.

� Who controls the federal government?

FMI Nonresidential Construction Index11

* A note on the use of the diffusion index: Do not interpret diffusion index values in the same manner as averages, because a simple increase or decrease in a diffusion index does not necessarily imply an improving or declining result. For example, if a diffusion index moves from 31 last quarter to 35 this quarter, it does not imply the market has improved. A reading above 50 indicates improving or expansion, 50 indicates remaining the same, and below 50 indicates worse or contracting. Therefore, if a reading goes from 31 to 35, then the result still implies a decline from the previous quarter because 35 is below 50; but the decline is not as great as the previous decline because 35 is above 31. As another example, if the diffusion index changes from 31 to 65, it implies improvement over the previous quarter, not because 65 is above 31, but because 65 is above 50.

NRCI Scores> 50 indicates growth (better)< 50 indicates slowing (worse)

FMI Nonresidential Construction Index Detailed Results by Market Sector

EXHIBIT 7

NRCI Component Results Q2 2016

NRCI Component Results Q3 2016

Improving over last quarter

Remains the same as last

quarter

Worse compared with

last quarter

Improving over last quarter

Remains the same as last

quarter

Worse compared with last quarter

Commercial 45.3% 53.8% 0.9% 72.2 44.9% 51.7% 3.4% 70.8Education 40.0% 53.0% 7.0% 66.5 35.4% 53.5% 11.1% 62.1

Health care 41.9% 52.1% 6.0% 67.9 37.1% 53.3% 9.5% 63.8Lodging 44.9% 53.1% 2.0% 71.4 44.6% 47.3% 8.1% 68.2

Manufacturing 24.1% 69.0% 6.9% 58.6 36.5% 52.7% 10.8% 62.8Office 33.1% 64.5% 2.4% 65.3 25.0% 69.6% 5.4% 59.8Other 41.7% 58.3% 0.0% 70.8 52.4% 33.3% 14.3% 69.0

Commercial 37.1% 56.2% 6.7% 65.2 44.9% 48.3% 6.7% 69.1Education 39.5% 50.0% 10.5% 64.5 33.3% 54.5% 12.1% 60.6

Health care 52.6% 38.8% 8.6% 72.0 43.8% 46.7% 9.5% 67.1Lodging 34.4% 54.2% 11.5% 61.5 29.3% 57.3% 13.3% 58.0

Manufacturing 29.5% 62.5% 8.0% 60.8 37.0% 50.7% 12.3% 62.3Office 33.3% 58.5% 8.1% 62.6 25.9% 58.0% 16.1% 54.9Other 50.0% 47.2% 2.8% 73.6 54.5% 40.9% 4.5% 75.0

Commercial 19.6% 52.0% 28.4% 45.6 29.1% 34.9% 36.0% 46.5Education 35.1% 38.7% 26.1% 54.5 27.6% 51.0% 21.4% 53.1

Health care 41.7% 45.2% 13.0% 64.3 41.7% 41.7% 16.5% 62.6Lodging 21.1% 45.3% 33.7% 43.7 17.3% 36.0% 46.7% 35.3

Manufacturing 28.7% 48.3% 23.0% 52.9 33.3% 36.1% 30.6% 51.4Office 17.6% 53.8% 28.6% 44.5 16.1% 48.2% 35.7% 40.2Other 32.4% 50.0% 17.6% 57.4 31.8% 54.5% 13.6% 59.1

Business Outlook - One Year

Business Outlook - Three Years

Business OutlookThree Months

Business OutlookThree Months

Business Outlook - One Year

Business Outlook - Three Years

Overall Second Quarter 2016 Overall Third Quarter 2016

FMI Nonresidential Construction Index12

Note: NRCI scores and component scores are based on a diffusion index where scores above 50 represent improving or expanding, a score of 50 represents remaining the same, and a score below 50 represents worse than last quarter or contraction.

EXHIBIT 9

Size of the Organization in Annual Revenue

NRCI Component Indexes — Comparisons of Results: Q4 2015 to Q3 2016EXHIBIT 8

NRCI components Q4 2015

NRCI components Q1 2016

NRCI components Q2 2016

NRCI components Q3 2016

The overall economy 58.3 56.5 65.4 58.1

The overall economy where panelists do business 64.8 57.3 69.9 60.4

Panelists' construction businesses 69.9 64.1 76.0 70.9

Nonresidential building construction market where panelists do business 65.3 60.6 74.3 67.3

Cost of construction materials 30.6 38.1 25.2 22.3

Cost of labor 18.9 18.8 12.0 12.0

Productivity 47.9 49.1 52.4 46.5

Expected change in backlog 62.2 59.7 66.1 58.9

Median Median Median Median

Approximate current signed backlog in months 12.0 11.0 11.0 10.0

$201M to $1B27%

Greater than $1B8%

$50M or Less23%

$51M to $200M42%

FMI Nonresidential Construction Index13

CommercialGeneral Building

Contractor43%

Roofing0%

Painting1%

Masonry2% Concrete

2%

Electrical2%

Other11%

Mechanical/HVAC12%

Construction Manager16%

EXHIBIT 10

Type ofContracting Business

EXHIBIT 11

Primary Region in Which Panelists Work

South34%

National Contractors

9%

West26%

Midwest20%

Northeast11%

FMI Nonresidential Construction Index14

* A note on the use of the diffusion index: Do not interpret diffusion index values in the same manner as averages, because a simple increase or decrease in a diffusion index does not necessarily imply an improving or declining result. For example, if a diffusion index moves from 31 last quarter to 35 this quarter, it does not imply the market has improved. A reading above 50 indicates improving or expansion, 50 indicates remaining the same, and below 50 indicates worse or contracting. Therefore, if a reading goes from 31 to 35, then the result still implies a decline from the previous quarter because 35 is below 50; but the decline is not as great as the previous decline because 35 is above 31. As another example, if the diffusion index changes from 31 to 65, it implies improvement over the previous quarter, not because 65 is above 31, but because 65 is above 50.

FMI Nonresidential Construction Index (NRCI) Component Results Q2 2016 to Q3 2016EXHIBIT 12

NRCI Scores> 50 indicates growth (better)< 50 indicates slowing (worse)

Improving over

last quarter

Staying the same as last

quarter

Worse compared with

last quarter

NRCI components Q2 2016

Improving over last quarter

Staying the same as last

quarter

Worse compared with

last quarter

NRCI components Q3 2016

Overall Economy 31.5% 67.8% 0.7% 65.4 23.8% 68.5% 7.7% 58.1

Overall Economy Where Panelists Do Business

40.4% 58.9% 0.7% 69.9 28.5% 63.8% 7.7% 60.4

Panelists' Construction Business 56.2% 39.7% 4.1% 76.0 49.6% 42.6% 7.8% 70.9

Nonresidential Building Construction Market Where Panelists Do Business

50.0% 48.6% 1.4% 74.3 43.8% 46.9% 9.2% 67.3

Backlog in Months High Median Low High Median Low

Approximate Current Signed Backlog 34.0 11.0 3.0 40.0 10.0 3.0

Grow faster

than last quarter

Stay about the same as last quarter

Shrink compared to last quarter

Grow faster than last quarter

Stay about the same as last quarter

Shrink compared to last quarter

Expected Change in Backlog 37.7% 56.8% 5.5% 66.1 31.0% 55.8% 13.2% 58.9

Higher than last quarter

Same as last quarter

Lower than last quarter

Higher than last quarter

Same as last quarter

Lower than last quarter

Cost of Construction Materials 51.0% 47.6% 1.4% 25.2 56.9% 41.5% 1.5% 22.3

Cost of Labor 76.0% 24.0% 0.0% 12.0 76.0% 24.0% 0.0% 12.0

Improving over last quarter

Same as last quarter

Declining compared to last quarter

Improving over last quarter

Same as last quarter

Declining compared to last quarter

Productivity 11.6% 81.5% 6.8% 52.4 6.2% 80.6% 13.2% 46.5

NRCI Component Results Q2 2016 NRCI Component Results Q3 2016

All individual responses to this survey will be confidential

and shared outside of FMI only in the aggregate.

All names of individuals responding to this survey will

remain confidential to FMI.

H O W T O B E C O M E A N N R C I P A N E L I S T

If you are an executive for a construction firm in nonresidential building markets and would

like to become a panelist for the “FMI Nonresidential Construction Index,” please send your

information or questions about this survey to Phil Warner at [email protected]. The survey

is sent to panelists quarterly and should take approximately 10 minutes to complete. Panelists

will receive the full quarterly report free of charge.

CONFIDENTIALITY

A B O U T T H I S R E P O R T

The data in this report is presented as a sampling of

construction industry executives voluntarily serving

as panelists for this survey. The responses are based

on their experience and opinions, and the analysis is

based on FMI’s interpretation of the aggregate results.

All trends are based on a limited series of data that

may or may not represent the larger population. We

must caution that major decisions should not be

made without additional investigation and research of

specific geographic and construction market segments.

About FMIFor over 60 years, FMI has been the leading management consulting and investment banking† firm dedicated exclusively to

engineering and construction, infrastructure and the built environment.

FMI serves all sectors of the engineering and construction, infrastructure and built environment industries as a trusted advisor.

More than six decades of industry context, connections and leading insights result in transformational outcomes for our clients

and the industry.

FMI helps you build your foundation for tomorrow and optimize your business for today. Industry Focus. Powerful Results.

� A/E and Environmental

� General Contractors/CM

� Heavy civil

� Industrial

� Specialty Trades

� Utility T&D

Sector Expertise

† Investment banking services provided by FMI Capital Advisors, Inc., a registered broker-dealer and wholly owned subsidiary of FMI.

Raleigh (headquarters) 5171 Glenwood AvenueSuite 200Raleigh, NC 27612919.787.8400

Denver210 University BoulevardSuite 800Denver, CO 80206303.377.4740

Tampa308 South BoulevardTampa, FL 33606813.636.1364

Houston9303 New Trails DriveSuite 350The Woodlands, TX 77381713.936.5400

Phoenix 7639 East Pinnacle Peak RoadSuite 100Scottsdale, AZ 85255602.381.8108

www.fminet.com

Copyright © 2016 FMI Corporation

Notice of Rights: No part of this publication may be reproduced or transmitted in any form, or by any means, without permission from the publisher.

� Clean Tech and Energy Services

� Construction Materials

� Building Products

� Oil and Gas

� Private Equity

� Owners