nonprofit financial management college of public and community service university of massachusetts...

TRANSCRIPT

Nonprofit Financial ManagementCollege of Public and Community Service

University of Massachusetts at Boston©2010 William Holmes

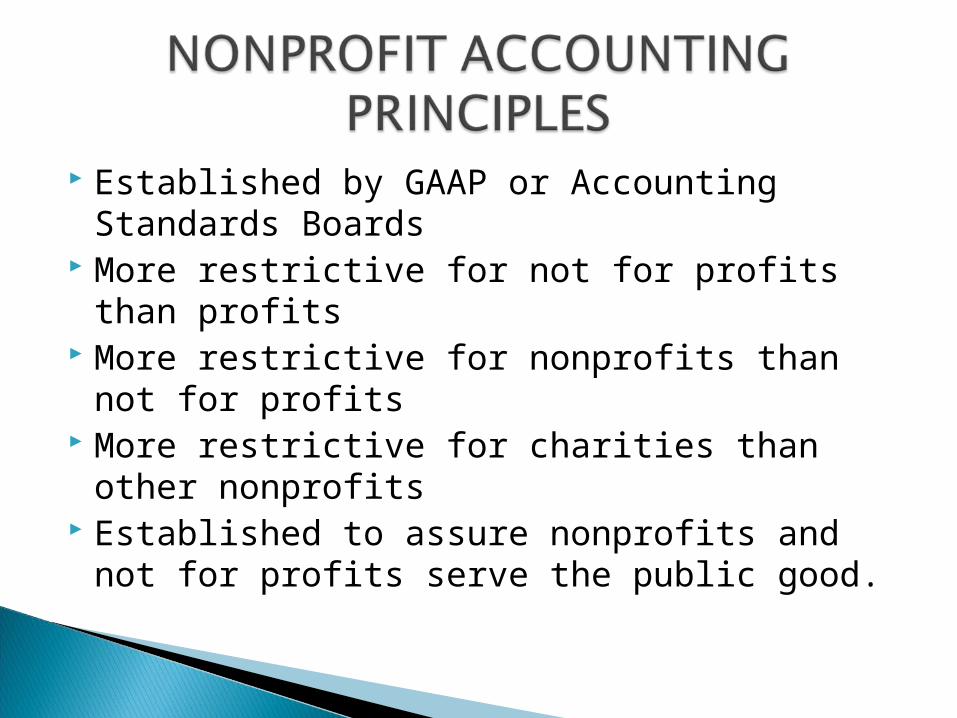

Established by GAAP or Accounting Standards Boards

More restrictive for not for profits than profits

More restrictive for nonprofits than not for profits

More restrictive for charities than other nonprofits

Established to assure nonprofits and not for profits serve the public good.

1. Income categorized as unrestricted or restricted assets

2. Restricted assets must be donor imposed3. Expenses may be categorized as

unrestricted or restricted4. Donations or gains or loss in investments

may be unrestricted or restricted5. Income reported separate from

expenditures6. Separation of unrestricted, temporary

restricted, and permanently restricted

1. Assets not separated as current vs. long-term or variable vs. fixed

2. Assets ordered by liquidity, most liquidity first (or specify in notes)

3. May break down categories in to specific funds, but must give aggregate total

4. May not comingle restricted and unrestricted assets, except for cash

5. Notes should identify temporary and permanent restrictions

6. Restricted accounts are fungible7. Donor imposed restrictions

separated from self-imposed restrictions, permanent vs. temporary restrictions

Expenses listed by functional class and by natural category

Functional classes are programs, types of service, or types of products

Fundraising is a functional category Natural categories include salaries,

supplies, rent, professional fees, bad debts, and depreciation.

1. Expenses separated from revenue2. Expenses broken into detail3. Expenses reported by functional class4. Expenses given by natural categories5. Statement in matrix form (expense

categories by functional classes)6. Critiqued by low overhead: program-

spending ratio and the fundraising efficiency ratio