non-gaap/alternative performance …swiss.cfa/lists/events...

TRANSCRIPT

NON-GAAP/ALTERNATIVE PERFORMANCE MEASURES: WHAT IS THE BIG DEAL?

Vincent Papa June 7, 2017

NGFM

• Context • Company Communication of NGFM

• Investors’ Use of NGFM

• Key Investor Concerns

• Bridging the Gap

2 CFA Institute

CONTEXT: EVOLVING CORPORATE REPORTING LANDSCAPE

EVOLVING AUDIT AND ASSURANCE SERVICES

3

Perceived Shortcomings of Traditional

financial statement information

(Country specific GAAP/IFRS)

Increased demand for Other information

(Non-GAAP, ESG, Risk Reporting, Intellectual

capital)

TECHNOLOGY TRANSFORMING THE NATURE, DELIVERY & ASSURANCE OF COMPANY INFORMATION (XBRL delivery, implications of adoption of blockchain technologies,

leveraging big data)

Corporate Information for

Capital Markets

CFA Institute

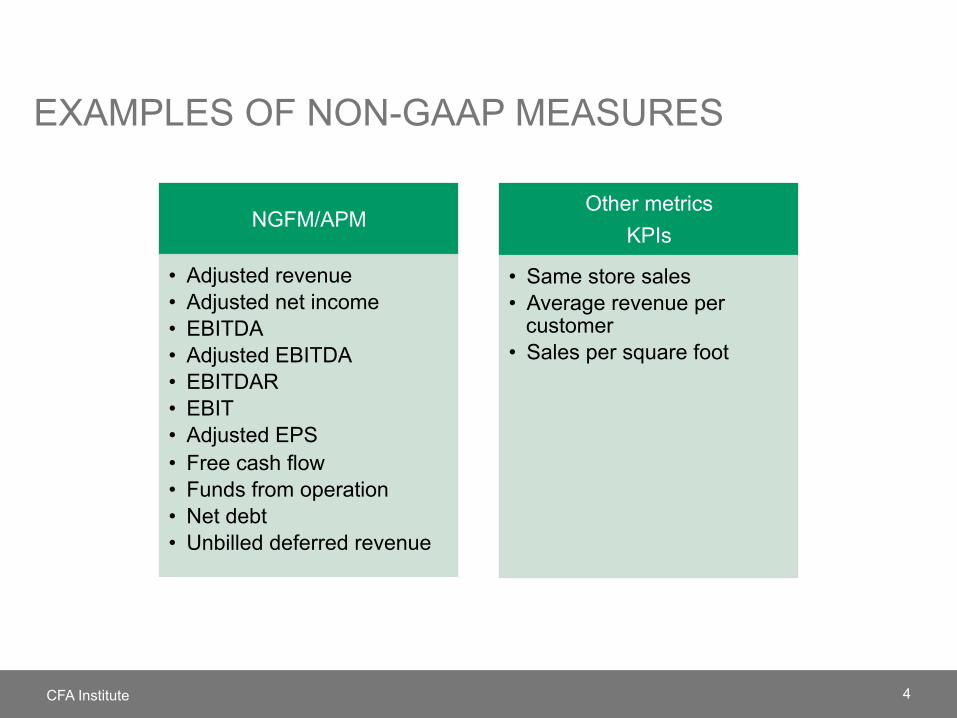

EXAMPLES OF NON-GAAP MEASURES

4 CFA Institute

NGFM/APM

• Adjusted revenue • Adjusted net income • EBITDA • Adjusted EBITDA • EBITDAR • EBIT • Adjusted EPS • Free cash flow • Funds from operation • Net debt • Unbilled deferred revenue

Other metrics KPIs

• Same store sales • Average revenue per

customer • Sales per square foot

DRIVERS OF NGFM REPORTING

SUPPLY FACTORS • Companies desire to convey relevant entity-specific information • Measures help to manage perception of performance

• Variation by country – 43% of SIX versus in 2013 >80% of US (S&P500) and UK (FTSE100) in 2015

• Prevalent in particular industries (Healthcare, technology) • Regulatory environment can determine quality of alternative performance

reporting

DEMAND FACTORS • Investor demand for supplemental information on earnings components • Institutional practices (e.g. consensus earnings) • A by-product of GAAP complexity and perceived irrelevance

5 CFA Institute

6 CFA Institute

ILLUSTRATION: NOVARTIS

NovartisUSDMillions 2016 2015 2014 2013 2012IFRSIncomebeforetaxes 7,817 8,134 11,921 10,496 10,925Amortizationofintangibleassets 4,097 4,132 3,073 3,159 3,045Impairments 786 369 1,575 259 356Acquisitionordivestmentrelateditems (33) 182 (647) 349 364Otherexceptionalitems 648 1,275 (1,096) 74 87Adjustedincomebeforetaxes 13,315 14,092 14,826 14,337 14,777

EPS 2.82 2.92 4.21 3.76 3.83AdjustedEPS 4.76 5.01 5.22 5.09 5.15

2016and2015onlyreflects continuingoperations

7 CFA Institute

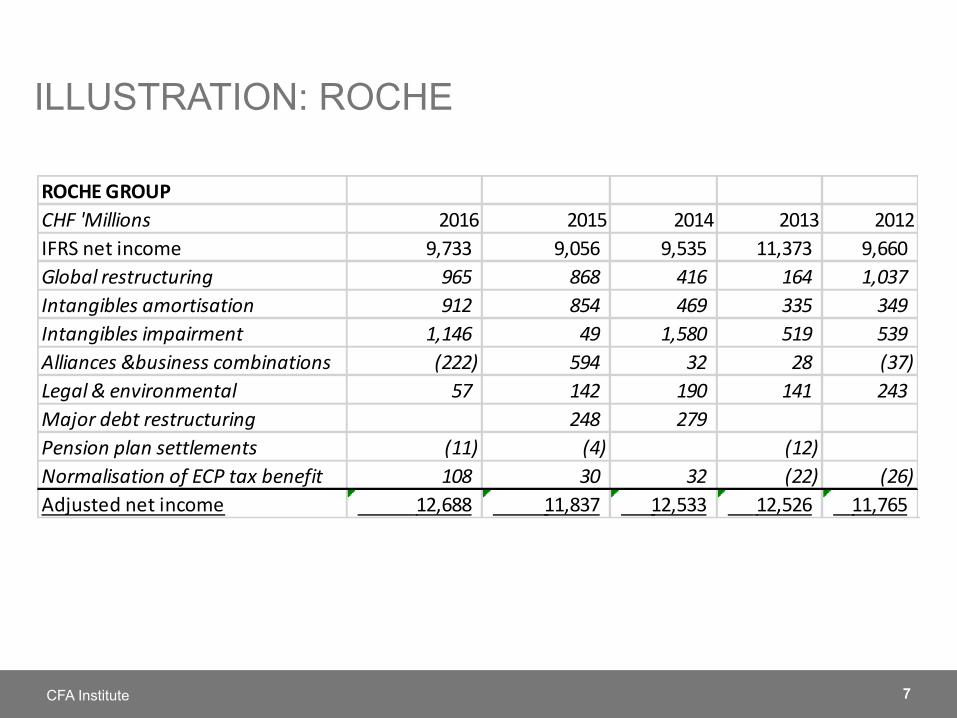

ILLUSTRATION: ROCHE

ROCHEGROUPCHF'Millions 2016 2015 2014 2013 2012IFRSnetincome 9,733 9,056 9,535 11,373 9,660Globalrestructuring 965 868 416 164 1,037Intangiblesamortisation 912 854 469 335 349Intangiblesimpairment 1,146 49 1,580 519 539Alliances&businesscombinations (222) 594 32 28 (37)Legal&environmental 57 142 190 141 243Majordebtrestructuring 248 279Pensionplansettlements (11) (4) (12)NormalisationofECPtaxbenefit 108 30 32 (22) (26)Adjustednetincome 12,688 11,837 12,533 12,526 11,765

8 CFA Institute

TYPICAL EARNING ADJUSTMENTS-SIX

Figure 4: Occurrence of Adjustments for 13 (12) SIX companies in 2013 (2012)

Source: 2014 Deloitte IAS Financial Reporting by listed companies- Spotlight on Swiss Trends

0 2 4 6 8 10 12

Disposaloffixedassets

Disposalofinvestments

IAS39relateditems

Restructuring

Depreciationandamortisation

Impairment

OccurenceofAdjustments

2012 2013

9

2009 2010 2011 2012 2013 2014 Restructuring* 52.5% 45.9% 42.1% 49.0% 51.5% 48.0% Investment gains/losses* 17.6% 20.1% 19.0% 19.7% 21.0% 27.6% Acquisition* 26.1% 34.4% 31.7% 36.1% 35.2% 36.0% Stock compensation 17.6% 17.0% 17.6% 16.5% 17.0% 15.0% Amortization* 22.3% 20.5% 23.1% 22.3% 22.8% 24.0% Impairment* 29.0% 24.3% 25.5% 30.6% 27.5% 27.6% Legal 21.8% 19.7% 23.8% 22.3% 25.9% 28.2% Pension (MTM)* 1.3% 1.9% 3.1% 3.5% 0.3% 4.2% Pension (OPEB)* 2.1% 2.7% 5.2% 9.4% 7.7% 10.2% Currency 1.3% 3.1% 1.4% 1.3% 4.3% 5.4% Tax resolution/change 30.7% 40.2% 37.2% 31.3% 34.6% 35.1% Tax adjustments (NGFM) 36.1% 33.2% 35.2% 36.8% 36.7% 37.5% Debt extinguishment 10.5% 19.7% 13.4% 16.1% 14.5% 18.6% Interest revenues/costs 6.7% 6.6% 6.6% 5.2% 5.2% 4.5%

ADJUSTMENTS- S&P 500 COMPANIES

CFA Institute

CFA Institute

INVESTORS’ USE OF NGFMS

10

11

23.1%

38.0%

21.0%

13.8%

4.0%

33.5%35.2%

14.3%12.1%

4.9%

26.5%

37.1%

18.8%

13.3%

4.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Always Often Sometimes Rarely Never

UseofNGFM;N=558

Portfoliomanagers+buy-sideanalysts=376 Other+Sell-sideanalysts=182 All=558

WIDESPREAD USE

12

32.3%

40.8%

16.5%

8.3%

2.1%

33.5% 34.6%

17.0%

11.0%

3.8%

32.7%

38.8%

16.7%

9.2%

2.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

Always Often Sometimes Rarely Never

UseofGAAP/IFRS;N=557

Portfoliomanagers+buy-sideanalysts=375 Other+Sell-sideanalysts=182 All=557

CFA Institute

GAAP/IFRS STILL IMPORTANT

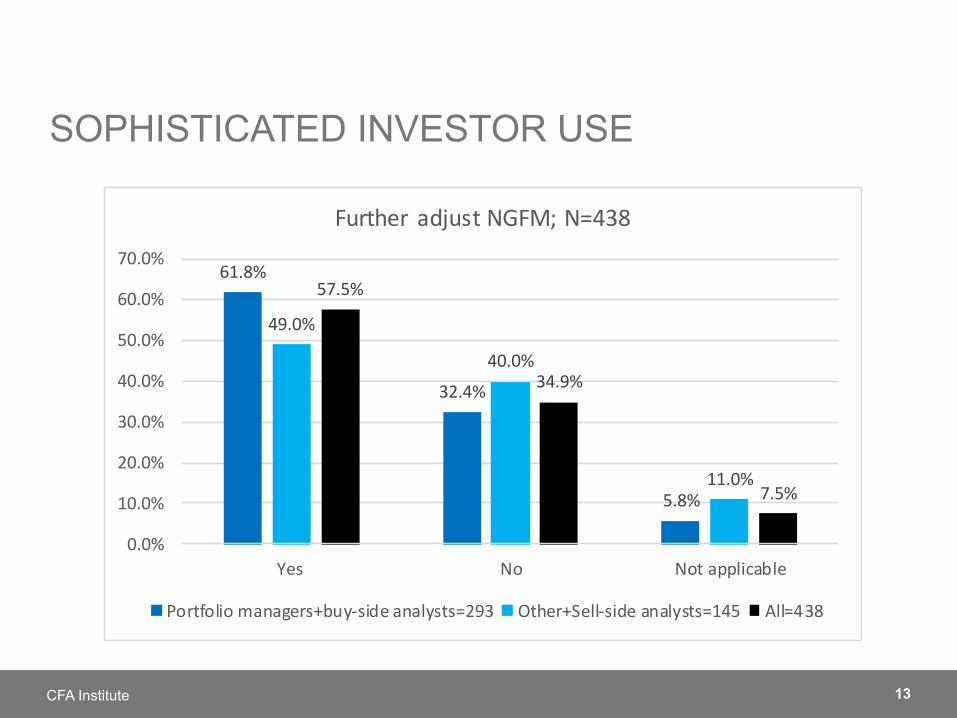

13

61.8%

32.4%

5.8%

49.0%

40.0%

11.0%

57.5%

34.9%

7.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Yes No Notapplicable

Further adjustNGFM;N=438

Portfoliomanagers+buy-sideanalysts=293 Other+Sell-sideanalysts=145 All=438

CFA Institute

SOPHISTICATED INVESTOR USE

14

78.4%

68.6%64.5%

57.1%

50.2% 49.1%

40.1%

67.4%72.2%

68.8%

55.6%52.1%

39.6%

47.9%

74.7%69.8%

65.9%

56.6%50.8%

45.9%42.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Freecashflow EBITDA AdjustedEBITDA

Netdebt AdjustedEPS EBIT Adjustedearnings

"Top-Half"UseofNGFM;N=431

Portfoliomanagers+buy-sideanalysts=287 Other+Sell-sideanalysts=144 All=431

CFA Institute

INVESTORS: COMMONLY USED NGFMS

15

39.0% 38.7%35.9%

17.4%

13.2%

8.0%

36.8%

46.5%

42.4%

18.1%

9.7%6.9%

38.3%41.3%

38.1%

17.6%

12.1%

7.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

AdjustedEBIT Adjustedoperatingprofit

Fundsfromoperations

AdjustedrevenueUnbilleddeferredrevenue

Other

"Bottom-half"- UseofNGFM;N=431

Portfoliomanagers+buy-sideanalysts=287 Other+Sell-sideanalysts=144 All=431

CFA Institute

INVESTORS: COMMONLY USED NGFMS

16

63.4%

56.9%53.1%

50.0%

38.6%

57.6% 58.3%63.2%

45.1%47.9%

61.5%57.4% 56.5%

48.4%

41.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Toassessearningsquality

Tofacilitateperiodtoperiodtrendanalysis

Tofacilitateforecastingoffuture

earnings

DisagreewithparticularGAAP

treatment

Understandperformancethrougheyesofmanagement

Top5reasonsforUseofNGFMs;N=434

Portfoliomanagers+buy-sideanalysts=290 Other+Sell-sideanalysts=144 All=434

CFA Institute

REASONS FOR USE

17

32.4% 31.7%28.3%

24.8%

10.3%

29.2%

42.4%

36.1%

31.3%

6.9%

31.3%35.3%

30.9%27.0%

9.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

Identifymanagementmisreportingincentivesand

choices

Suitableformyvaluationmodel

Tomakeforecaststhatarecomparabletootheranalysts

Toconformtoconsensusearnings

Other

OtherreasonsforuseofNGFM;N=434

Portfoliomanagers+buy-sideanalysts=290 Other+Sell-sideanalysts=144 All=434

CFA Institute

REASONS FOR USE- CONTINUED

CFA Institute

DARK SIDE OF NON_GAAP MEASURES: INVESTOR CONCERNS

18

19

For 380 S&P 500 firms reporting on a non-GAAP net income basis in 2015 and included in the S&P 500 from 2009 onward.

CFA Institute CFA Institute and R.G. Associates, Inc.

MANAGING PERCEPTION OF PERFORMANCE

20

• Lack of comparability across companies & across reporting periods • Questionable exclusions that can mislead investors on entity’s performance

• Excluding recurring restructuring costs • Excluding stock option expenses- (i.e. real expenses) • Lumping recurring expenses into “other”

• Inappropriate application during executive compensation determination

• Inadequacies of reconciliation and disclosure of NGFM adjustments • Instances of inadequate disaggregation to specific line items • Instances where reconciliation is not prominently located • Boiler plate and inadequate explanations

• Lack of assurance on NGFM

• Risks Associated with Greater Prominence of NGFM relative GAAP/IFRS measures

• Mispricing of equities • Misleading ROE, ROIC

PRIMARY CONCERNS

CFA Institute

21

UNDUE PROMINENCE: RISK OF COMPARING APPLES TO ORANGES

CFA Institute

FacebookPerformance2016 2015

OperatingMarginNon-GAAP 60% 56%OperatingMarginGAAP 45% 35%

InvestorsBusinessDaily-15thFebruary20176-TopRatedStockswith50%PlusProfitMarginsAnnualpre-taxMarginFacebook 60.0%UnitedTherapeutics 59.3%Phillips-66Partners 55.7%BOFIHoldings 53.4%Alibaba 52.9%Mobileye 51.8%

22

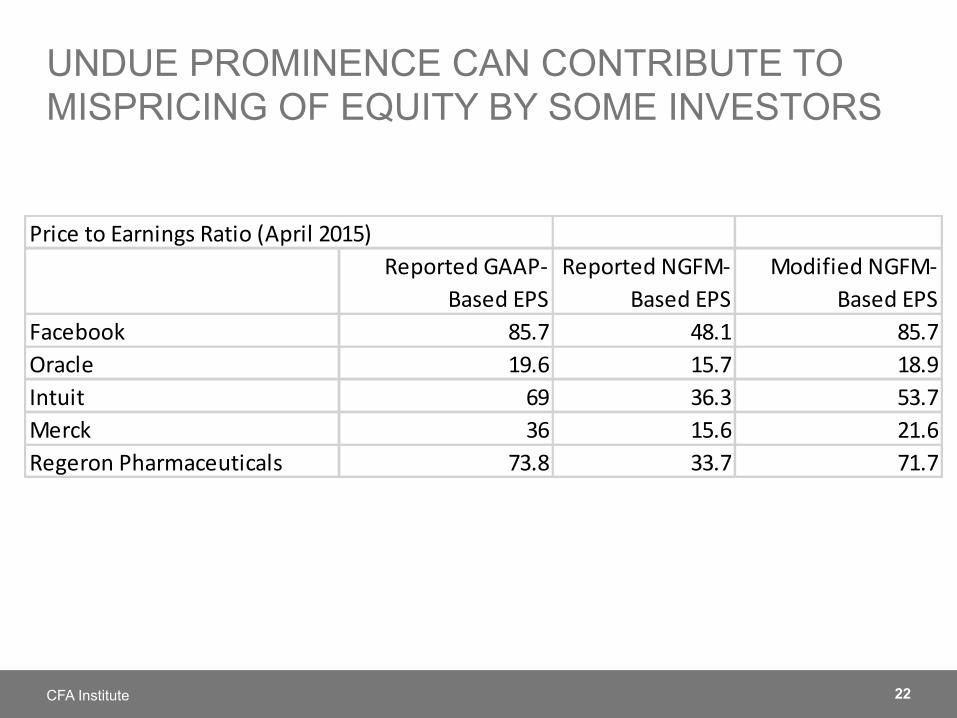

UNDUE PROMINENCE CAN CONTRIBUTE TO MISPRICING OF EQUITY BY SOME INVESTORS

CFA Institute

PricetoEarningsRatio(April2015)ReportedGAAP-

BasedEPSReportedNGFM-

BasedEPSModifiedNGFM-

BasedEPSFacebook 85.7 48.1 85.7Oracle 19.6 15.7 18.9Intuit 69 36.3 53.7Merck 36 15.6 21.6RegeronPharmaceuticals 73.8 33.7 71.7

23

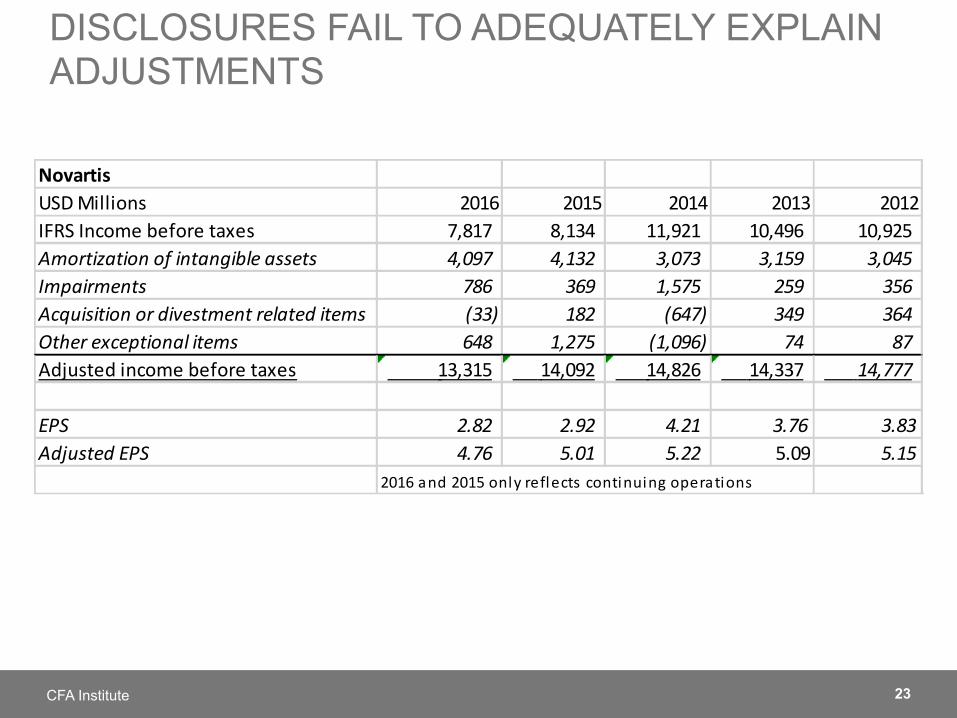

DISCLOSURES FAIL TO ADEQUATELY EXPLAIN ADJUSTMENTS

CFA Institute

NovartisUSDMillions 2016 2015 2014 2013 2012IFRSIncomebeforetaxes 7,817 8,134 11,921 10,496 10,925Amortizationofintangibleassets 4,097 4,132 3,073 3,159 3,045Impairments 786 369 1,575 259 356Acquisitionordivestmentrelateditems (33) 182 (647) 349 364Otherexceptionalitems 648 1,275 (1,096) 74 87Adjustedincomebeforetaxes 13,315 14,092 14,826 14,337 14,777

EPS 2.82 2.92 4.21 3.76 3.83AdjustedEPS 4.76 5.01 5.22 5.09 5.15

2016and2015onlyreflects continuingoperations

24

DISCLOSURES FAIL TO ADEQUATELY EXPLAIN ADJUSTMENTS – NOVARTIS ANNUAL REPORT

CFA Institute

1Amor%za%onofintangibleassets:Costofgoodssoldincludesrecurringamor%za%onofacquiredrightstoin-marketproductsandotherproduc%on-relatedintangibleassets;Research&Developmentincludestherecurringamor%za%onofacquiredrightsfortechnologyplaBorms;IncomefromassociatedcompaniesincludesUSD296millionfortheNovar%sshareofthees%matedRochecoreitems.

2Impairments:CostofgoodssoldandResearch&Developmentincludeimpairmentchargesrelatedtointangibleassets;Otherincomeincludesimpairmentreversalsofproperty,plantandequipment;Otherexpenseincludesimpairmentchargesrelatedtoproperty,plantandequipment,andfinancialassets.

3 Acquisition or divestment related items, including restructuring and integration charges: Other income and Other expense include transitional service-fee income and expenses, and other items related to the portfolio transformation; Other income also includes a gain from the revaluation of a previously held financial investment in a newly acquired company.

25

DISCLOSURES FAIL TO ADEQUATELY EXPLAIN ADJUSTMENTS – NOVARTIS ANNUAL REPORT

CFA Institute

4 Other items: Other revenues include an early release of deferred income associated with a collaboration agreement; Cost of goods sold, Other income and Other expense include net restructuring and other charges related to the Group-wide rationalization of manufacturing sites; Research & Development, Marketing & Sales, Other income and Other expense include other restructuring income and charges; Cost of goods sold and Research & Development include adjustments of contingent considerations; General & Administration, Other income and Other expense include items related to setup costs for Novartis Business Services; Other income and Other expense also include legal settlements and changes in provisions; Other income also includes gains from product divestments, other income related to the portfolio transformation and a gain related to the sale of real estate; Other expense also includes a charge as a result of a pension plan amendment, a charge for an indirect tax settlement and other costs; Income from associated companies includes USD 135 million for the Novartis share of the estimated GSK Consumer Healthcare Holdings Ltd. core items; Other financial income and expense relates mainly to devaluation losses in Venezuela

CFA Institute

INVESTOR PROTECTION- WHAT IS REQUIRED?

26

BRIDGING THE GAP: CREATING A DEPENDABLE PERFORMANCE REPORTING FRAMEWORK

27 CFA Institute

CFA Institute

THANKS FOR LISTENING!

28