nigeria real estate industry outlook 2017 report (abridged version)

TRANSCRIPT

REAL ESTATEI N D U S T RY O U T L O O K 2 0 1 7

Market Trends, Opportuni t ies & Risks in Uncertain

Economic TimesCromwell PSI

NIGERIA

Copyright © 2017

All rights reserved

No part of this publication shall be reproduced, transmitted, shared or sold in whole or in part,without the prior written consent of Cromwell Professional Services International. Alltrademarks remain the property of the company.

Users of information in this report are advised to do their due diligence before making businessor investment decisions. Information contained in this report should be independently verifiedby a qualified professional. Nothing contained in this report should be construed as business orinvestment advice.

Thank you.

Cromwell PSI2

Introduction

3

This report is a vital tool for investors, developers, regulators and stakeholders who want to develop and execute strategies that unlock value and mitigate risk in Nigeria’s real estate market.

We are pleased to present this maiden edition of the Real Estate Industry

Outlook Report for 2017.

Over the last decade, the Nigerian real estate industry has experienced

significant growth, and has risen to become the 5th biggest contributor to

GDP. Despite the present economic challenges and a full-year recession in

2016, this report reveals the macroeconomic forces that could affect the

performance of the Nigerian real estate industry in 2017.

Nigeria’s rising international profile as Africa’s largest economy and one the

continent’s most promising emerging markets portends interesting

opportunities and possibilities in the long term for the real estate industry.

The goal of this report is to provide you with insights and information to

make the right decisions in 2017.

Happy reading!

Olusola Olalekan Enitan F.N.I.V.S, RSV, MIAM

Country LeaderCromwell Professional Services International

In this Report: page

Nigeria’s Macroeconomic Outlook 4

The Real Estate Industry in 2017 10

Industry Overview 11

Impending Legislation 16

Market Analysis 19

About Us 29

Appendices 45

4

Nigeria’s Macroeconomic Outlook

Macroeconomic Outlook

5

Sub-Saharan Africa’s growth outlook for 2017 reflects aslow comeback from weak commodity prices and multipledomestic challenges.

0.4%

3.6%

5.9%

3.6%

-1.54%

0.4%

1.2%

7.5%

6.1%

6.6%

2.2%

1.8%

Angola

Ghana

Kenya

Mozambique

Nigeria

South Africa

2017 2016

The regional outlook for Sub-Saharan Africa shows an average

GDP growth rate of 4%. However, African economies reliant on

extractive industries, especially Nigeria, South Africa and Angola

are unlikely to achieve this average in 2017 due to unstable

commodity prices and domestic challenges which include rising

inflation and plunging currencies.

With slowing economic growth in China, commodity prices

have declined sharply with oil prices plummeting from a high of

US$114 per barrel in 2014 to a low of US$28 per barrel in 2016.

This has had severe impacts on Africa’s commodity-dependent

economies, which showed modest gains immediately after the

global crisis but continue to experience slow growth in tandem

with declining commodity prices.

Unless commodity prices significantly recover in 2017, it is

unlikely that Africa’s biggest economies – South Africa and

Nigeria – will experience any considerable growth this year.

Sources: World Bank, Cromwell Research

2017 Nigerian Real Estate Industry Outlook

Macroeconomic Outlook

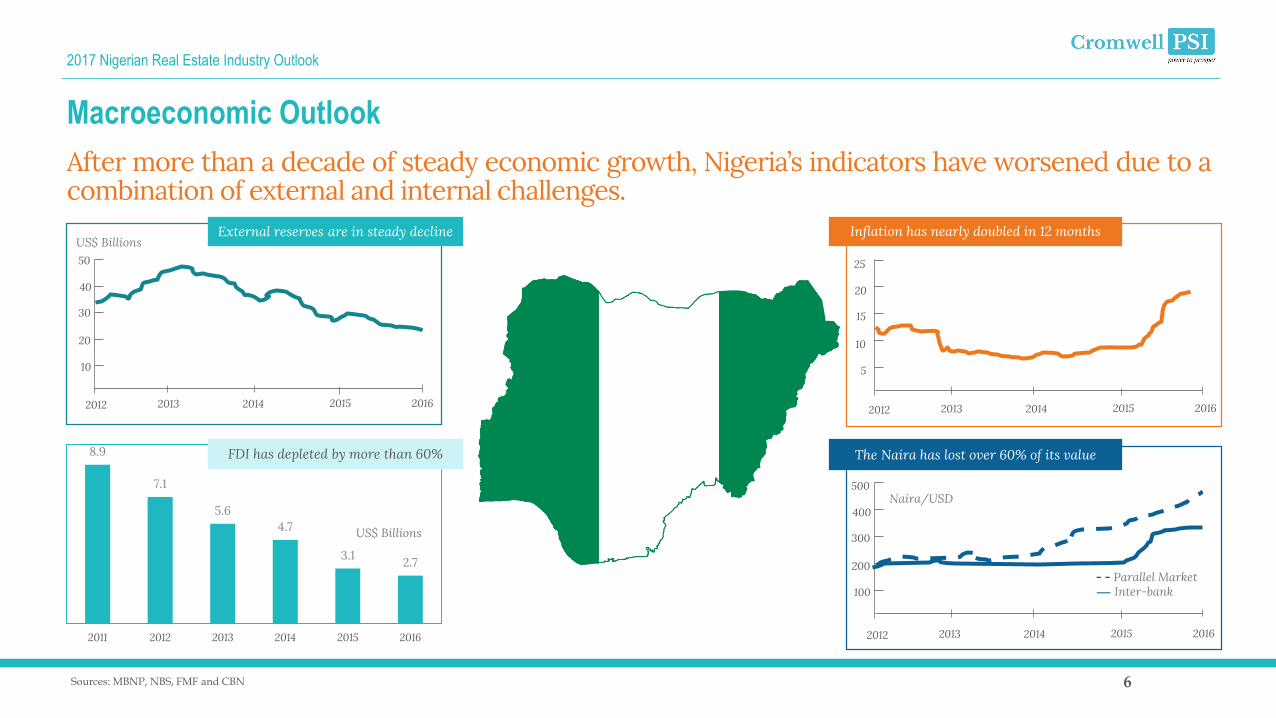

6Sources: MBNP, NBS, FMF and CBN

After more than a decade of steady economic growth, Nigeria’s indicators have worsened due to acombination of external and internal challenges.

2012 2013 2014 2015 2016

2012 2013 2014 2015 2016

8.9

7.1

5.64.7

3.1 2.7

2011 2012 2013 2014 2015 2016

100

200

300

400

500

5

10

15

20

25

FDI has depleted by more than 60%

Inflation has nearly doubled in 12 months

The Naira has lost over 60% of its value

2012 2013 2014 2015 2016

10

20

30

40

50

US$ Billions

US$ Billions

Naira/USD

- - Parallel Market Inter-bank

External reserves are in steady decline

2017 Nigerian Real Estate Industry Outlook

Macroeconomic Outlook

7

Despite a negative growth of -1.54% in 2016, Nigeria’s Real GDP is projected to grow and improveslightly to 2.19% in 2017.

Nigeria’s economy is expected to be on the road to recovery in 2017. Real

GDP is projected to grow and improve slightly from an estimated negative

growth of -1.54 percent in 2016 to 2.19 percent in 2017. This growth will be

driven by a fiscal stimulus facilitated by an expected increase in oil prices, an

increase in non-oil federal receipts, an increase in oil production, and

resolution of payment arrears especially joint venture cash calls.

In addition to expected economic recovery due to positive growth in the oil

sector, increased growth in the non-oil sector especially agriculture,

manufacturing, services and light industries will be central in overall GDP

growth.

While crude oil output is forecast to rise from an average of 1.8 mbpd in 2016

to 2.2 mbpd in 2017, depressed global oil prices could lead to a continuation

of the government’s structural adjustments and devaluation of the Naira.

However, the average price of crude oil is expected to rise by 11.8% from

US$38 in 2016 to US$42.50 in 2017.

Inflation jumped from 9.5% (December 2015) to 18.5% (November 2016)

due to the combined effects of currency depreciation, higher energy prices

and high cost of inputs.

Key Macroeconomic indicators

2016 (Est.) 2017 (Outlook)

Real GDP Growth % -1.54 2.19

Non-oil GDP % Oil GDP %

-0.07-15.41

0.2024.30

Gross Domestic Investment 13.95 13.90

Inflation Rate % 18.55 15.74

Oil Price Benchmark, US$ 38.00 42.50

Oil Production (mbpd) 1.8 2.2

External Trade Balance 0.31 1.80

Consumer Price index 213.60 247.22

Unemployment rate 14.20 16.32

World Bank Doing Business Index

169/190 169/190

Sources: MBNP, NBS, FMF and CBN

2017 Nigerian Real Estate Industry Outlook

10,709

8,623

4,417

4,391

3,514

2,030

1,898

1,837

1,592

1,291

1,139

1,037

Crop Production

Trade

Oil & Gas

Telecoms & ICT

Real Estate

Food, Beverage & Tobacco

Construction

Professional Services

Other Services

Financial Institutions

Public Administration

Education

Macroeconomic Outlook

8

Seven sub-sectors contribute more than 70 per cent of Nigeria’s GDP. It is very unlikely thecountry’s GDP profile would change significantly in 2017.

Sources: MBNP, NBS, FMF and CBN

Services(53.2%)

Agriculture(23.1%)

Manufacturing(9.5%)

Oil & Gas(9.6%)

Real Estate & Construction(3.9%)

Utilities (0.5%)

Solid minerals (0.1%)The oil sector accounts for less than 10% of

Nigeria’s GDP but remains the largest contributor of

export earnings and government revenues. The

sector experienced negative growth in 2016, with an

estimated contraction of -15.4%.

The biggest contributors to GDP are services(including retail and wholesale trade), agriculture,

manufacturing and construction and real estate).

While the oil and gas sector contribution to GDP

continues to decline, the non-oil contributors have

grown steadily at an average rate of 6.2% between

2010 and 2015, and are largely responsible for the

growth of Nigeria’s GDP (avg. 4.8%) during that

period.

In light of their historical growth rates, Nigeria’s

non-oil sector could provide resilience and modest

recovery to the economy in 2017.

2017 Nigerian Real Estate Industry Outlook

Macroeconomic Outlook

9

Our outlook presents three potential macroeconomic scenarios for 2017 with significant positiveand negative implications for Nigeria.

Scenario 1 Scenario 2 Scenario 3

Status Quo Best Case Worst Case

Description Nigeria does not pursue macroeconomic or structural reforms and continues to conduct business as usual in the hope that oil prices recover.

Nigeria implements macroeconomic and structural reforms, and makes a big push to significantly diversify the economy.

The economic contraction worsens due to a combination of domestic and external factors, especially a precipitous fall in oil prices and incapable leadership.

Possible Implications

The economy would continue to

contract in the short term and GDP

could decline by -0.5% in 2017.

Income per capita would decline as

total GDP stays relatively flat while

the population grows.

Low FDI, continued exchange rate

volatility and low market

confidence.

The economy would recover

strongly and GDP growth could

reach 2.2% in 2017, driven by

strong non-oil sector growth.

Increased public and private

investment, higher FDI, stable

exchange rate, reduced obstacles

to doing business, and high market

confidence.

The economy could deteriorate

significantly, leading to a GDP

contraction below -2% in 2017.

Financial sector meltdown, wildly

volatile exchange rate, hyper-

inflation, capital flight and

significant loss of confidence in

the Nigerian economy.

2017 Nigerian Real Estate Industry Outlook

10

The Nigerian Real Estate Industry in 2017

11

Industry Overview

12

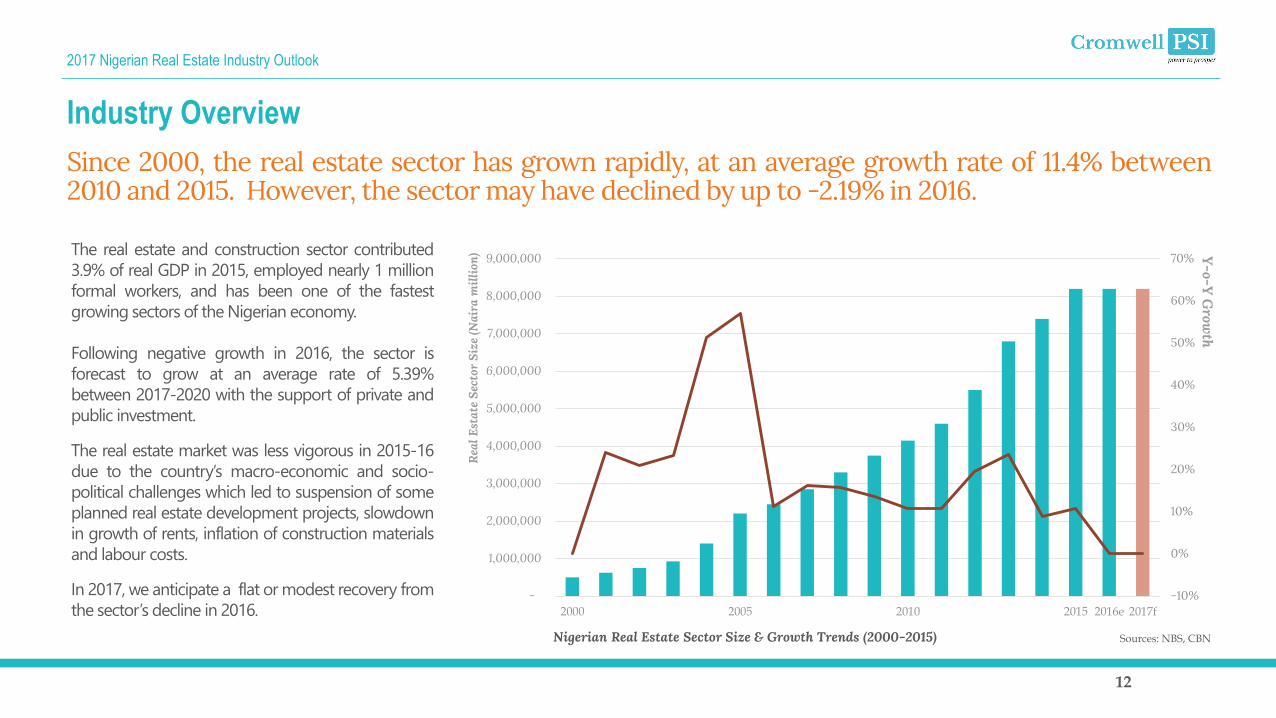

Since 2000, the real estate sector has grown rapidly, at an average growth rate of 11.4% between2010 and 2015. However, the sector may have declined by up to -2.19% in 2016.

Sources: NBS, CBN

Industry Overview

-10%

0%

10%

20%

30%

40%

50%

60%

70%

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

2000 2005 2010 2015 2016e 2017f

Y-o-Y

Grow

th

Rea

l Est

ate

Sect

or S

ize

(Nai

ra m

illio

n)

Nigerian Real Estate Sector Size & Growth Trends (2000-2015)

The real estate and construction sector contributed

3.9% of real GDP in 2015, employed nearly 1 million

formal workers, and has been one of the fastest

growing sectors of the Nigerian economy.

Following negative growth in 2016, the sector is

forecast to grow at an average rate of 5.39%

between 2017-2020 with the support of private and

public investment.

The real estate market was less vigorous in 2015-16

due to the country’s macro-economic and socio-

political challenges which led to suspension of some

planned real estate development projects, slowdown

in growth of rents, inflation of construction materials

and labour costs.

In 2017, we anticipate a flat or modest recovery from

the sector’s decline in 2016.

2017 Nigerian Real Estate Industry Outlook

13

Despite its current challenges, the medium to long term outlook for the real estate sector suggestsstrong growth due to several favourable socio-economic factors.

Sources: MBNP, NBS, FMF and CBN

Nigeria’s population, currently over 180 million and growing at an

average annual rate of 3%, remains a major driver of growth for the

real estate industry.

Other major growth drivers are rising urbanisation, a growing

middle class, increasing investment from local participants,

including Pension funds and Mutual funds; the growing number of

High Net Worth Individuals (HNWIs) investing in real estate, and

targeted intervention by the Federal Government in the housing

finance sector.

Increased foreign and domestic investment is another significant

driver of growth for the real estate industry. In the long term, we

expect the industry to experience an increasing entry of foreign

developers, investors and service firms; increased joint venture

arrangements between local sponsors and financial as well as

strategic partners; and development expansion into secondary (Tier

2) cities such as Ibadan, Owerri, Abeokuta, Enugu and Kano,

among others.

Real Estate Market Growth

Foreign direct investment (FDI)

flows

Institutional participation and

investment from local PFAs and mutual

funds

Growing number of high net worth

individuals (HNWIs) investing in RE

Population shift to urban areas (47%

urbanised)

Growing middle class driving demand for

residential RE

Federal government intervention in the

housing finance sector

Industry Overview

2017 Nigerian Real Estate Industry Outlook

14

The residential and retail real estate market segments are driven by Nigeria’s growing population,increasing rural-urban migration, rising consumption and a growing middle class.

Industry Overview

Residential Segment Retail Segment Nigeria has an affordable housing deficit of 17 million houses estimated at

US$363 billion. This number is expected to increase by 2 million houses per year

at the current population growth of 2.8% per year.

The mortgage market remains small, underdeveloped and costly, with interest

rates ranging from 18-30%, and tenors of 1-6 years. Ratio of outstanding

mortgages to GDP stands at 0.6%* compared to 50% in Europe.

The high-end luxury residential segment has been a key revenue generator for

developers, and prime developments are clustered in a handful of

neighbourhoods in Lagos, Abuja and Port Harcourt. However this segment of the

market is expected to continue lagging in 2017 due to macroeconomic

uncertainty.

Since 2012, a growing number of developers have pivoted towards the largely

underserved mid-range market. This trend is expected to continue in 2017.

The Nigeria Mortgage Refinance Company (NMRC), the Federal Mortgage Bank

of Nigeria will lead the government’s efforts to improve the availability and

affordability of mortgage loans to Nigerians in 2017.

In the current retail real estate market, estimates show there is 1m2 of

retail space per 1,000 people in Nigeria, compared to South Africa’s

480m2 retail space per 1,000 people.^ This translates into significant

opportunities, given the current and future size of Nigeria’s large

population.

Nigeria is considered one of Africa’s leading destinations for retail

property investors due to strong socio-economic fundamentals that

fuel the growing demand for consumer products.

In addition to successful retail developments like the Palms Mall and

Ikeja City Mall, plans are in the pipeline to spend up to US$3.5billion

on 25 new destination malls in Nigeria in 2017.

Supermarket brands such as South Africa’s Shoprite chain and Game,

a subsidiary of Wal-Mart, have proved popular as anchor tenants,

while high-street fashion and lifestyle brands have snapped up retail

space across the country.

2017 Nigerian Real Estate Industry Outlook

15

The long-term growth of the commercial, industrial and hospitality real estate segments will bedriven by growing economic activity and FDI inflows.

Industry Overview

Commercial Industrial Hospitality Nigeria’s growing reputation as Africa’s largest

economy and a gateway to the sub-Saharan

regional market has led to strong demand for

Grade-A office space and commercial real estate in

recent years.

The supply-demand gap has raised prices, and

rental figures in Lagos remain among the highest

in the world, with achievable rents at more than

US$85/m2 per month (2014).

Notable commercial real estate developments that

could stimulate the sector in coming years include

the Wings project and Eko Atlantic City project in

Lagos, and the World Trade Centre project in Abuja

-- a mixed-use eight-tower complex development

with AAA office towers, luxury residences and up-

scale shopping that is estimated to cost US$26

billion.

A growing middle class population and retail

activity are driving demand for warehousing

space as well as infrastructure-enabled

industrial clusters and free zones. This can be

attributed to manufacturers and suppliers

seeking premises from which to meet growing

consumer demand.

Nigeria currently has about 25 approved free

zones (schemes set up to strategically improve

the investment climate by stimulating export

oriented business activities), although less than

half of these are operational.

While the industrial real estate segment has a

lot of potential, it remains largely unorganised

and opaque in terms of real estate

development.

The hospitality real estate segment has

experienced growth in recent years due to the

entry of various boutique and luxurious

hospitality players in Nigeria’s major cities.

Notable developments in this segment include

the upgrading of Starwood’s Le Meridien Hotels

into a 7-star suite, Marriott International’s

proposed multi-million dollar investments in the

subsector, the entry of Sheraton’s Four Points

into Akwa Ibom State, and the incursion of

Hilton into several cities in the country.

Although penetration of global hospitality

brands is increasing (with about 20% of total

room supply), local and regional brands will

continue to play an important role.

2017 Nigerian Real Estate Industry Outlook

16

Impending Legislation

17

Several new bills introduced to the Nigerian federal legislature in 2016 could successfully pass intolaw in 2017 with considerable implications for the real estate industry.

Impending Legislation

Bill Title Description Stage

1 HB 521 National Housing Fund Act (Amendment) Bill, 2016

This Bill seeks to update and strengthen the National Housing Fund

Act with the view to reflect present day realities and stiffen

punishment for violators of the National Housing Fund Act.

1st reading

2 SB 285 Nigerian Assets Management Agency (Establishment and Regulatory) Bill, 2016

This Bill seeks to establish and regulate the Nigerian Assets

Management Agency charged with the responsibility of managing all

Government Assets including those seized, forfeited or taken over by

Federal Government bodies such as the EFCC, ICPC, Police, Customs,

Nigerian Security and Civil Defence Corps among others

1st reading

3 SB 280 Nigeria Industrial Development and Zones Bill, 2016

This Bill seeks to repeal the Nigeria Export Processing Zone Authority

Act LFN CAP NI07 2004, and enact the Nigeria Industrial Development

and Zones Commission to manage, control and co-ordinate all

activities within the Zones. The Commission will also have control over

all goods deposited or manufactured in the Zones and power to

demarcate areas within the Zones as Customs territory.

1st reading

2017 Nigerian Real Estate Industry Outlook

18

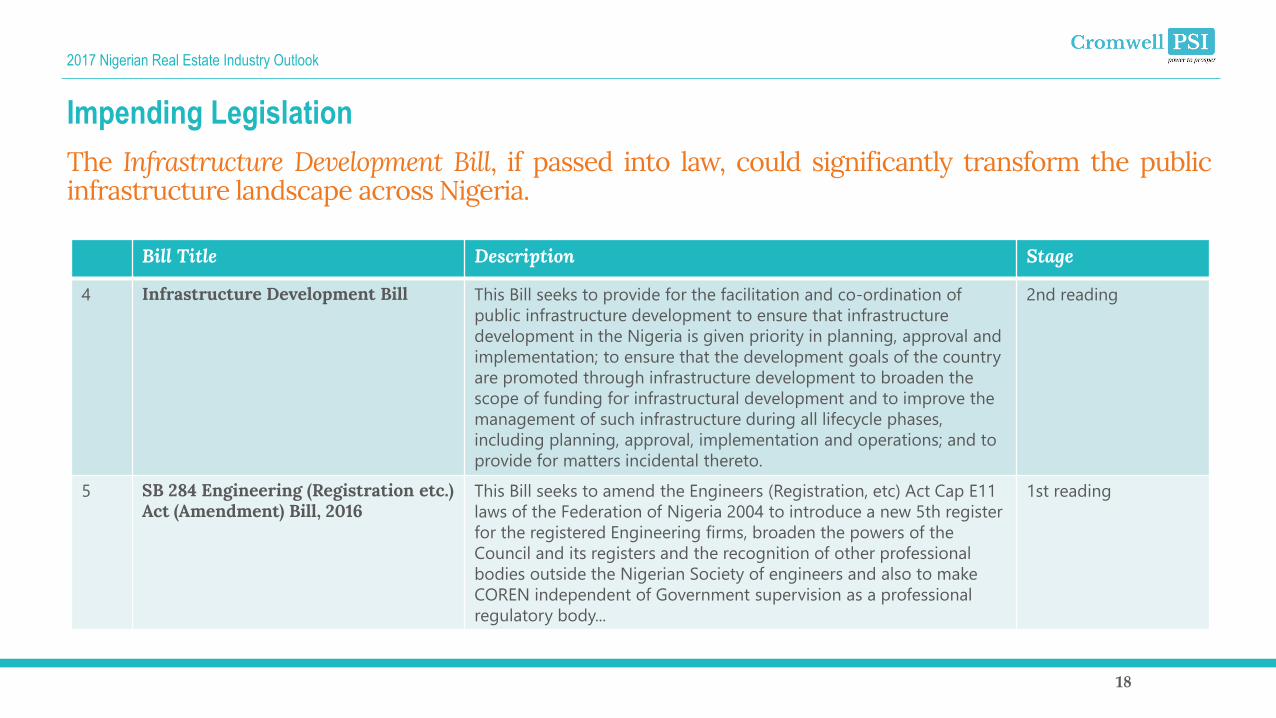

The Infrastructure Development Bill, if passed into law, could significantly transform the publicinfrastructure landscape across Nigeria.

Impending Legislation

Bill Title Description Stage

4 Infrastructure Development Bill This Bill seeks to provide for the facilitation and co-ordination of

public infrastructure development to ensure that infrastructure

development in the Nigeria is given priority in planning, approval and

implementation; to ensure that the development goals of the country

are promoted through infrastructure development to broaden the

scope of funding for infrastructural development and to improve the

management of such infrastructure during all lifecycle phases,

including planning, approval, implementation and operations; and to

provide for matters incidental thereto.

2nd reading

5 SB 284 Engineering (Registration etc.) Act (Amendment) Bill, 2016

This Bill seeks to amend the Engineers (Registration, etc) Act Cap E11

laws of the Federation of Nigeria 2004 to introduce a new 5th register

for the registered Engineering firms, broaden the powers of the

Council and its registers and the recognition of other professional

bodies outside the Nigerian Society of engineers and also to make

COREN independent of Government supervision as a professional

regulatory body...

1st reading

2017 Nigerian Real Estate Industry Outlook

19

Market Analysis

20

We conducted a national survey and analysis of the real estate market to understand the state andevolution of trends across Nigeria.

Market Analysis

Zones Constituent states

1 North East Taraba, Adamawa, Borno, Yobe, Bauchi and Gombe

2 North West Sokoto, Zamfara, Kebbi, Kaduna, Katsina, Kano and Jigawa

3 North Central Kwara, Kogi, Plateau, Nassarawa, Benue, Niger, FCT Abuja

4 South West Lagos, Ogun, Oyo, Osun, Ondo and Ekiti

5 South East Imo, Anambra, Ebonyi, Enugu and Abia

6 South South Edo, Delta, Rivers, Cross River, Akwa Ibom and Bayelsa

Nigeria is a diverse country made up of over 400 ethnic groups and 450 languages, and

administered according to 36 states and a federal capital territory.

In order to streamline the market data collection exercise, and to best understand the market

trends, this survey was divided along the six geo-political zones of Nigeria – a grouping of states

with similar cultures, ethnic groups, and common history.

2017 Nigerian Real Estate Industry Outlook

21

Key Findings: The general trend across Nigeria reveals a real estate market weakened by socio-economic challenges. However, some states and regions have remained resilient.

The data collected and analysed presents several insights about the Nigerian real estate market

over the last five years, and projections for 2017. Our key findings are as follows:

a) There is a pervasive slowdown in the major real estate markets, starting in 2015 and

expected to continue in 2017. This is largely due to the economic recession which severely

impacted the demand side of the market, leading to high vacancy rates, especially in the

prime and luxury property market segments.

b) While the property market in the Federal Capital Territory, Abuja has been on a downtrend

and has seen a considerable drop in property values, the Lagos market has remained

resilient and has experienced marginal appreciation, especially in the mid-market segments.

c) States such as Borno, Yobe, Adamawa, Bauchi, and Gombe which are affected by the

instability and insecurity caused by the Boko Haram insurgency in the North East and parts

of the North West have suffered significant erosions of property values due to negative

market perceptions and weak demand.

d) The displacement of inhabitants from the conflict zones in the North East has favourably

impacted property values, not just in neighbouring states (like Niger, Zamfara, Kaduna and

Jigawa), but in the South East and South South as indigenes relocate to these areas.

Market Analysis

e) Property values across all states in Nigeria are significantly

influenced by levels of economic activity, a vibrant formal

private sector (industry and services), and degree of

urbanisation.

f) The appreciation in property values is more substantial for

undeveloped land compared to developed properties.

This is due to the growing demand and activities of

property developers and investors taking up land as an

investment, or exploring opportunities to develop

projects for residential, commercial, industrial, hospitality

and retail use.

All the collected data is presented according to Nigeria's

geopolitical zones, and on a state-by-state basis in the

following pages.

2017 Nigerian Real Estate Industry Outlook

2012 2013 2014 2015 2016

1.0

2.0

3.0

4.0

5.0

Naira (Millions) JIGAWABuildings Land

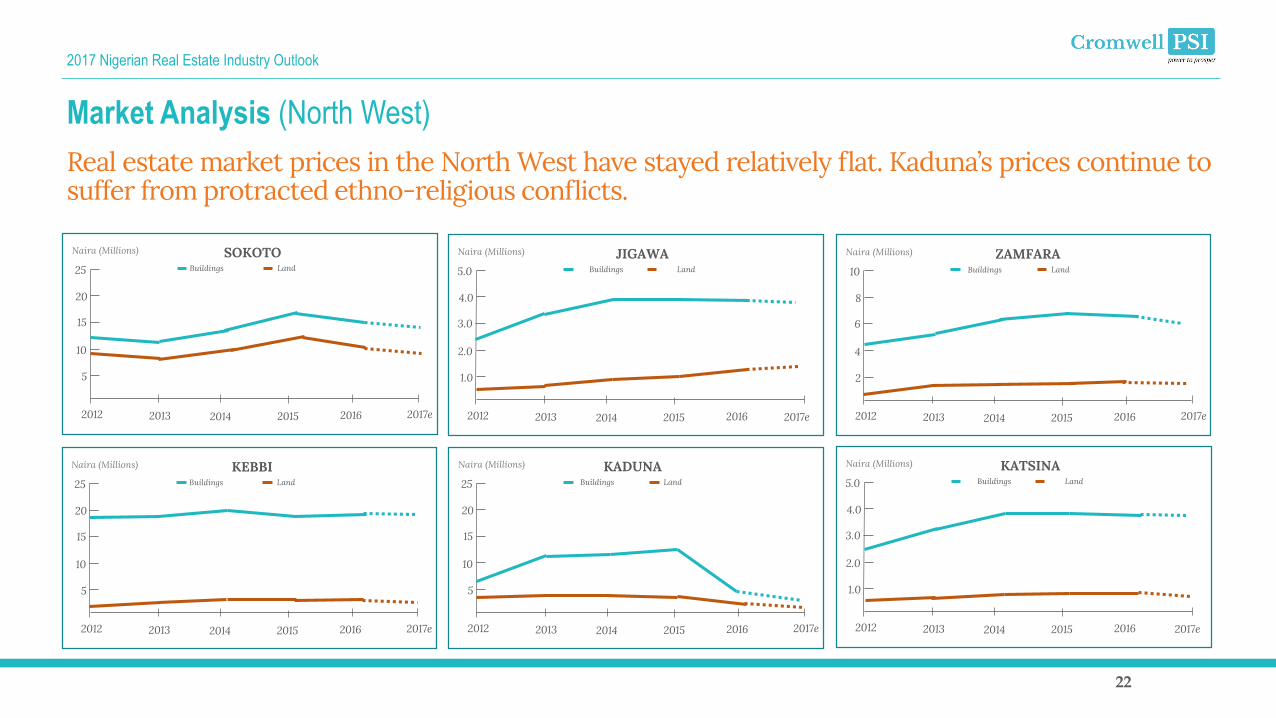

Market Analysis (North West)

22

Real estate market prices in the North West have stayed relatively flat. Kaduna’s prices continue tosuffer from protracted ethno-religious conflicts.

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

SOKOTOBuildings Land

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

KADUNABuildings Land

2012 2013 2014 2015 2016

2

4

6

8

10

Naira (Millions)

2017e

ZAMFARABuildings Land

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

KEBBIBuildings Land

2017e

2012 2013 2014 2015 2016

1.0

2.0

3.0

4.0

5.0

Naira (Millions) KATSINABuildings Land

2017e

2017 Nigerian Real Estate Industry Outlook

2012 2013 2014 2015 2016

1.0

2.0

3.0

4.0

5.0

Naira (Millions) BAUCHIBuildings Land

Market Analysis (North East)

23

The instability, destruction and human displacement caused by the Boko Haram conflict in theNorth East has led to a slump in real estate market prices.

2012 2013 2014 2015 2016

2

4

6

8

10

Naira (Millions)

2017e

ADAMAWABuildings Land

2012 2013 2014 2015 2016

2

4

6

8

10

Naira (Millions)

2017e

BORNOBuildings Land

2012 2013 2014 2015 2016

2

4

6

8

10

Naira (Millions)

2017e

TARABABuildings Land

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

GOMBEBuildings Land

2017e

2012 2013 2014 2015 2016

1.0

2.0

3.0

4.0

5.0

Naira (Millions) YOBEBuildings Land

2017e

2017 Nigerian Real Estate Industry Outlook

Market Analysis (South East)

24

Property prices in the South East market continue to experience steady appreciation buoyed byincreasing market participation.

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

ABIABuildings Land

2012 2013 2014 2015 2016

0.5

1.0

1.5

2.0

2.5

Naira (Millions)

2017e

EBONYIBuildings Land

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

ENUGUBuildings Land

2012 2013 2014 2015 2016

10

20

30

40

50

Naira (Millions)

2017e

ANAMBRABuildings Land

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

IMOBuildings Land

2017 Nigerian Real Estate Industry Outlook

2012 2013 2014 2015 2016

1.0

2.0

3.0

4.0

5.0

Naira (Millions) KOGIBuildings Land

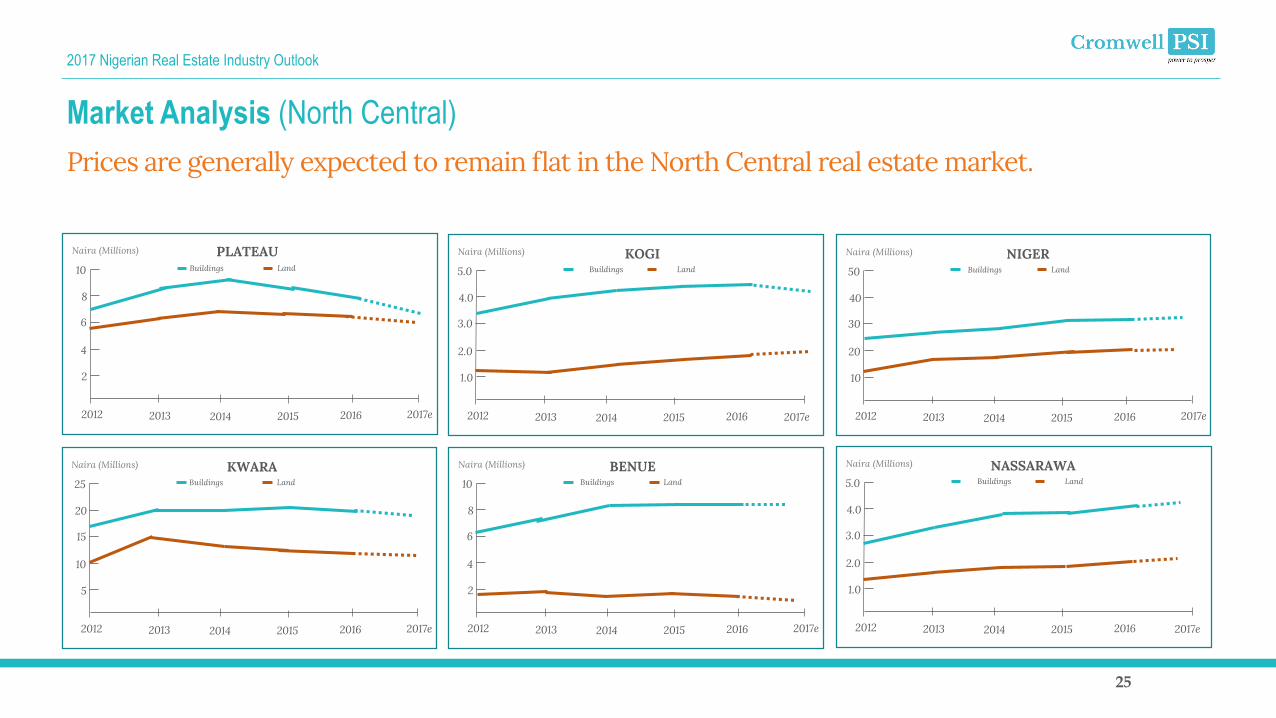

Market Analysis (North Central)

25

Prices are generally expected to remain flat in the North Central real estate market.

2012 2013 2014 2015 2016

2

4

6

8

10

Naira (Millions)

2017e

PLATEAUBuildings Land

2012 2013 2014 2015 2016

2

4

6

8

10

Naira (Millions)

2017e

BENUEBuildings Land

2012 2013 2014 2015 2016

10

20

30

40

50

Naira (Millions)

2017e

NIGERBuildings Land

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

KWARABuildings Land

2017e

2012 2013 2014 2015 2016

1.0

2.0

3.0

4.0

5.0

Naira (Millions) NASSARAWABuildings Land

2017e

2017 Nigerian Real Estate Industry Outlook

Market Analysis (Lagos & Abuja)

26

2012 2013 2014 2015 2016

25

50

75

100

125

Naira (Millions)

2017e

ABUJABuildings Land

2017 Nigerian Real Estate Industry Outlook

2012 2013 2014 2015 2016

25

50

75

100

125

Naira (Millions)

2017e

LAGOSBuildings Land

The Federal Capital Territory also has one of the highest property values in Nigeria and

one of the widest variances in value from one location to another within the same

state/territory.

Between 2011 and 2015, the average CAGR of property values within the FCT was 8%.

However, this figure varied significantly between the performance of residential

property, commercial property and undeveloped land.

The effects of the economic recession have adversely affected property values in the

FCT with high vacancy rates, especially in the prime real estate segment. This is

especially obvious in the poor year-on-year return for 2016 as evidenced by the data

below.

Lagos State has one of the highest property values in Nigeria and one of the

widest variances in value from one location to another within the same

state/territory.

Between 2011 and 2015, the Cumulative Average Growth Rate (CAGR) of

property values within Lagos ranged from as high as 39%, especially in

locations like Banana Island, and as low as 1% in places like Alagbado and

Festac.

The effects of the economic recession have affected the prime and luxury

segments of the property market. However, overall property values remained

robust, especially in the mid-market segments.

2012 2013 2014 2015 2016

3

6

9

12

15

Naira (Millions) OSUNBuildings Land

Market Analysis (South West)

27

Property prices in the South West market have remained resilient in the face of economicchallenges. This trend is expected to continue in 2017.

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

OYOBuildings Land

2012 2013 2014 2015 2016

3

6

9

12

15

Naira (Millions)

2017e

ONDOBuildings Land

2012 2013 2014 2015 2016

3

6

9

12

15

Naira (Millions)

2017e

EKITIBuildings Land

2012 2013 2014 2015 2016

5

10

15

20

25

Naira (Millions)

2017e

OGUNBuildings Land

2017e

2017 Nigerian Real Estate Industry Outlook

2012 2013 2014 2015 2016

3

6

9

12

15

Naira (Millions) BAYELSABuildings Land

Market Analysis (South South)

28

Real estate market prices in the South-South will likely continue to experience moderate growthin 2017.

2012 2013 2014 2015 2016

3

6

9

12

15

Naira (Millions)

2017e

EDOBuildings Land

2012 2013 2014 2015 2016

3

6

9

12

15

Naira (Millions)

2017e

AKWA IBOMBuildings Land

2012 2013 2014 2015 2016

1

2

3

4

5

Naira (Millions)

2017e

CROSS RIVERBuildings Land

2012 2013 2014 2015 2016

3

6

9

12

15

Naira (Millions)

2017e

DELTABuildings Land

2017e

2012 2013 2014 2015 2016

25

50

75

100

120

Naira (Millions) RIVERSBuildings Land

2017e

2017 Nigerian Real Estate Industry Outlook

29

About Us

An introduction to Cromwell Professional Services International.

30

Who We Are

About Us

Cromwell PSI is an aggregation of indigenous,experienced and highly motivated talent who arechanging the landscape of strategic outsourcing andprofessional services in Africa.Our extensive industry experience, combined with the broad competencies of our

specialists and network of global partners, allow us to provide technical expertise

and professional support to clients in a wide range of sectors in Nigeria and across

the African continent.

We are in the business of creatively solving demanding business problems, and

delivering solutions that help to realise the operational and strategic objectives of

the organisations we serve.

We are a fast-emerging indigenous firm on the African continent that helps clients

tackle serious business problems and challenges that affect their strategic

objectives. Our service delivery is unique because we strive to understand our

clients’ problems better than they do.

Our success stems from a fundamental understanding of our target industries and

the needs of the markets we serve. Cromwell PSI has proven its commitment to

improvement and growth, and is building a reputation for long-term, mutually

profitable client relationships.

“Enhance value through innovative solutions ”We work with clients to enhance value through innovative solutions

in strategic outsourcing, real estate, business performance,

decision-critical research, training and industry events.

“Be the dominant, home-grown global player in strategic outsourcing and professional services.Cromwell PSI wants to serve Africa’s most successful organisations

in the public and private sector landscape. We will grow from a

regional firm into a transcontinental brand that delivers a wide

range of professional services that support the operations, strategy,

growth and profitability of clients in the industries we serve.

Our Mission

Our Vision

31

Our ‘VALUE’ Principles

About Us

Value InnovationWe always go further than others to create a

leap in value for our clients. Our business is

founded on an entrepreneurial spirit and

passion to explore new ideas and welcome

new opportunities in exceeding our clients’

expectations.

LeadershipThrough our thinking, character and actions, we set bold and positive

examples for others to follow. We always act with transparency and

integrity because our clients rely on us as a critical part of their success.

AgilityWe adapt and respond rapidly to changes

and challenges without losing momentum or

vision. This principle makes us strive to

exemplify a passionate and personal service

to our clients.

UniversalityWe are everywhere, and always leave a mark of quality on everything we

do. Our firm belief in diversity, collaboration and synergy gives us the

unique ability to solve a wide range of problems for clients in several

different industries.

EmpathyWe always put ourselves in our clients’ shoes. This quality allows us to

gain a deep understanding of their needs and challenges, so we can

deliver fitting results.

Our VALUE code governs the way we do business at Cromwell PSI, and defines the corepillars of our brand.

32

What We Do

About Us

Real Estate Advisory Property Development

& Management

Facilities Management Urban & Infrastructure

Development

Professional Services Market Research Training & Capacity Development Industry Events

33

Real Estate Advisory

What We Do

About Us

Due Diligence & Audits We provide pre- and post-investment due diligence and audit services

including background checks, legal and compliance reviews, property analysis,

portfolio audits, data assessments, deal reviews and underwriting services

that facilitate informed investing, identify unrecognised opportunities and

reduce risks.

Transaction Advisory

We provide strategic support and advice during all phases of real estate

transactions for acquisitions, dispositions, design-build consultation, sale

leasebacks, lease renewal and negotiations, and corporate relocations.

Real EstateAdvisory

We support clients to realise value from real estate development projects

through market feasibility and demand analysis, highest and best use

evaluations, economic development and impact analysis, and real estate

development and implementation strategies.

Valuation & Investment Advisory

We provide independent real estate valuations, appraisals, reviews and

investment advisory for real estate funds, including international investors,

institutions, developers, and corporations. This service also covers feasibility

and pre-investment studies, portfolio analysis and lease advisory.

Commercial Real Estate Brokerage Services

We act on behalf of corporations, institutions, and individuals to acquire, sell

or lease commercial real estate. This service also provides access to an

expansive database of commercial real estate listings, including office,

industrial, retail, land, medical, institutional, investment and mixed-use.

34

What We Do

About Us

Commercial, Industrial & Residential Property Development Support

We provide integrated property development services that enhance

investment returns through strategic advice, pre-purchase feasibility studies

and development analysis, market analysis, profit and cost assessments,

property law advice, design and construction support, project management,

risk and security advisory, project financing and joint venture partnerships.

Property Management Services

We manage residential and commercial property in all sectors covering retail,

office space, leisure and industrial assets.

We also provide asset management services, coordinate property

maintenance and repairs, handle tenant communication and correspondence,

rent collection, financial management and statutory compliance, lease

management, and insurance and risk management.

Property Development

& Management

35

What We Do

About Us

Energy Design Planning and Management

We develop and execute strategies to reduce energy consumption and utilities

costs for residential and commercial facilities, and manage and monitor the energy

efficiency performance of the facilities.

Asset Replacement Planning

We develop and execute strategies to ensure current and future capital assets are

well maintained and a financial plan is in place to ensure their replacement. This

service ensures that no replacement needs and problems occur which could

interfere with operations of the facility.

Plant Services & Maintenance

We manage facility operations, construction, renovation, maintenance, repairs of

buildings, grounds, utilities and installed building systems.

Electrical & Mechanical Systems

We support the design, construction, maintenance and repair of electrical and

mechanical systems including HVAC systems, communications systems, power and

lighting systems, and building controls technology.

Fuel & Liquids Facilities Management

We develop and execute programs for the management and maintenance of fuel

facilities and installations that ensure regulation compliance and operational

efficiency.

Custodial, Janitorial & Cleaning Services

We provide commercial, retail, industrial, specialist and flexible contract custodial,

janitorial and cleaning support that meets the operational needs of the facilities we

oversee. We oversee regular inspection, care, cleaning, operations, repairs and

maintenance of the facility.

Facilities Management

36

What We Do

About Us

Sewage & Waste Management

We provide a comprehensive range of domestic, commercial and industrial waste

management services covering CCTV surveys, blocked drains, sewer/drain

cleaning, flood response, waste disposal and recycling.

Procurement Consulting & Contract Management

We address all aspects of procurement, sourcing and contract management

operations to achieve savings and improved supplier relationships through

strategic sourcing, spend analysis and custom benchmarking.

Landscaping & Horticulture Services

We provide horticultural, arboriculture and landscaping support, including

landscaping design and construction, garden and grounds maintenance, tree

surveys, vegetation management and interior landscape projects.

Security/ Surveillance Planning & Management

We provide a broad range of security services that respond to demands for site

surveys, manned guarding, CViT and cash management, surveillance and CCTV

systems, and security consultancy.

Space Planning & Design

We assist clients with planning and design solutions for residential, commercial,

retail and industrial spaces that lead to minimal expenditure and disruption,

optimal space use and density.

Public Buildings and Secured Facilities Management

We provide facilities management services for government-owned real estate

assets, including public buildings, public shared spaces, and critical and secure

facilities like courts, airports, utilities, prisons and banks.

Facilities Management

37

What We Do

About Us

Urban Housing Development, Cities & Mega Projects

We provide a comprehensive range of services across all aspects of the urban

planning and development process, including master planning, project visioning,

urban design strategies, land capability studies, community needs assessments and

independent reviews for all sizes of urban renewal and greenfield development

projects.

Social Infrastructure Development Support Services

We provide design, project management, construction and procurement support

for social infrastructure development projects, including the health, education,

housing, civic and utilities, corrections and justice sectors.

Transportation Systems Development

We provide design, ground engineering, environmental and construction services

support for transportation infrastructure development and rehabilitation, including

railways, roads, mass transit, marine transport and ports, and airports.

Policy, Strategy & Social Advocacy

We formulate and develop plans, policies and strategies that guide and address

the growth, development and management of economic, urban form and social

infrastructure issues.

Asset Replacement & Sunk Fund Management

We assist governments and infrastructure authorities to develop strategies and

manage resources allocated to address asset management and replacement issues

with a view to optimising the life of existing assets and accurately planning for

their replacement if required in future years.

Urban & Infrastructure

Development

38

What We Do

About Us

Management Consulting & General Business Advisory

We provide consulting services that focus on the most critical issues and

opportunities facing businesses, especially with strategy, marketing, organization,

operations, technology, transformation, mergers & acquisitions and sustainability

across all industries.

Accounting, Audit & Assurance Services

We provide key audit and assurance services, including statutory and non-

statutory audits, internal audits, corporate reporting, IFRS reporting, regulatory

compliance, capital markets, corporate treasury solutions, accounting advisory,

actuarial insurance, IT risk assurance, and governance and risk assurance.

Tax, Legal & Compliance Support

We support client organisations with legal, compliance and tax services around

local and international tax, general legal service, mergers & acquisitions, regulatory

compliance, tax reporting & strategy, tax controversy and dispute resolution, tax

policy & administration, and transfer pricing.

Human ResourcesSupport

Provide a broad spectrum of HR solutions that take care of workplace

investigations, recruitment, workforce planning, compensation, performance

issues, HR transformations, regulatory compliance, employee administration and

other HR needs.

Information Technology & Enterprise Solutions

We help clients become high-performance businesses by maximizing the value of

technology through end-to-end enterprise solutions, software, databases,

analytics, mobility and cloud infrastructure that enable the storage, retrieval,

analysis, presentation and dissemination of mission-critical data.

Professional Services

39

What We Do

About Us

Market & Industry Research Reports

We publish reports with important statistical and analytical information on

consumer markets, commercial industries, key economic sectors, performance

profiles and outlooks, current and future trends, competitor insights, and critical

international developments relevant to the market. Our on-demand and scheduled

report releases feature country and regional reports, industry profiles and

outlooks, consumer market reports, and indexes.

Custom Research & Surveys

We assist organisations with customised and cost-effective research and survey

projects for market entry, business development, competitive insight, and strategic

planning purposes.

Market Intelligence Databases

We provide online subscription database access to market and industry-related

data, statistics, analyses, reports and surveys from global, regional, country and

company perspectives that provide strategic insights to help clients achieve their

key business objectives.

Market Research

40

What We Do

About Us

Competency Management

Our extensive competency management frameworks allow companies to more

rapidly and efficiently assure the competency of every personnel by identifying

skill and knowledge gaps that may be limiting performance and compliance.

Performance Consulting

We work with companies to analyse operations and identify opportunities for

improving operational efficiency and implement programs designed to improve

personnel performance. By combining business, technical, and learning expertise,

we help our clients understand how to achieve sustainable competency

management to improve operations and profits.

Executive Training Programs

We offer a wide variety of scheduled and bespoke executive training programs that

cover functional business areas – Finance & Accounting, Human Resources,

Information Technology, Facilities Management – management, leadership and

organizational development, and other courses that help business professionals

advance their careers, and support organisations to grow and improve

performance.

Workforce Development Programs

Our workforce Development programs develop effective, competent technical

professionals for our clients in the shortest time possible. We lean on our deep

industry experience and competency building expertise of our partners to provide

a program tailored to our clients’ specific challenges and business needs. Our

programs typically include workforce planning, capability testing, competency

assessment, gap analysis, career ladders, and instructor-led training.

Training & Capacity Development

41

What We Do

About Us

Industry Events –Summits, Conferences, Retreats & Exhibitions

We organise and host strategic industry summits, conferences, retreats and

exhibitions that promote interaction, collaborations and partnerships between key

influencers, major industry players, and governments on country, regional and

global levels.

These events are held around the world and while some are open to all, others are

exclusive, member-only gatherings.

A selection of these industry-leading conferences and events is periodically

released on the Cromwell PSI website.Industry Events

42

We Want To Serve You

Cromwell Professional Services InternationalRC 1359897

Strategic Outsourcing -- Real Estate -- Professional Services -- Market Research –

Training & Events

Address: Plot H3, No. 10 Obafemi Awolowo Way, CBD,

Alausa, Ikeja, Lagos

Phone: +234 905 555 6698 – +234 807 504 8968

Email: [email protected]

Web: www.cromwellpsi.com

44

AppendicesNote: The appendices to this report include the comprehensive data tables from our national survey of property trends, and an analysis of the real estate market on a state-by-state basis.

If you are interested in receiving a copy of the full report, please send us an email at [email protected]

Thank you.