ngo kinh luan chemical industry natural rubber industry

TRANSCRIPT

Ngo Kinh Luan

Analyst

Chemical industry

Email: [email protected]

www.fpts.com.vn

FPT Securities Joint Stock Company, HCMC

Branch

29-31 Nguyen Cong Tru St, District1, HCMC,

Vietnam

Tel: (84) – 8 6290 8686

NATURAL RUBBER INDUSTRY

REPORT 2013

May 2013

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

www.fpts.com.vn

Report summary

Total global natural rubber production reached the amount of 11.4 mil tonnes increased by 3.97% compared with 2011. Global natural rubber consumption in 2012 was 10.9 mil tonnes, went up by 0.23% compared with 2011. Tapping productivity was 1.1 ton/hectare.

According to the statistics of Association of Natural Rubber Producing Countries (ANRPC) and Vietnam Rubber Group (VRG), in 2012, the exploitation of Vietnam was 863,600 tonnes, stood at the 5

th place of the

world. Besides that, Vietnam ranked 4th position in the world for the natural rubber export volume (1.02 mil

tonnes in 2012) and 2nd

for the natural rubber tapping productivity. In 2012, Vietnam average tapping productivity was 1.71 ton/hectare, lower than India (1.82 ton/hectare), significantly higher than the global average level of 1.1 ton/hectare.

In the domestic extent, Binh Phuoc and Binh Duong are 2 provinces that have largest arceage for rubber plantation, account for 22% and 18%, respectively, of total rubber area in Vietnam. The next provinces are Tay Ninh with 11%, Dong Nai with 6%.

Rubber consumption in domestic market was 15-18% of exploitation output, equivalent to 150,000 ton/year.

Rubber export: in 2012, Vietnam exported 1.02 mil tonnes of natural rubber, valued 2.85 bil USD, gained by

25% in terms of quantity and 11.7% in value. The import volume was about 302,000 tonnes dropped by

16.6% compared with 2011. The main import market is Cambodia (account for 59%) and main export market

is China (account for 40%). The export volume of listed companies of natural rubber industry accounts for a

very small portion of total industry from 3%-4%, about 28-30 thousand tonnes.

2013 industry outlook For the world: in 2013, rubber supply is expected to exceed demand about 179,000 tonnes, the long-term rubber price is also expected to drop. For Vietnam: the export volume is expected to reach 1 mil tonnes in 2013, slightly reduce compared with 1.02 mil tonnes in 2012. The import tax reduction for rubber of China and the increase in import and prospective tire industry development of India will boost the natural rubber export in 2013. The domestic demand will increase from 2013 onward since the radial tire plant operation of Casumina and Da Nang Rubber Company will start at the end of this year. In addition, VRG has invested in upgrading the productivity of VRG Khai Hoan Gloves Manufacturing Plant from 1.2 bil to 3.2 bil units/year, it will raise the domestic demand.

Strategy for industry development VRG has proposed the Government to boost Vietnam rubber area from 800,000 hectares to 1 mil hectares in 2015, raise the rubber planning in Northern Region from 50,000 hectares to 100,000 hectares in 2020. The Prime Minister signed the Decision No. 1782/QĐ-TTg approving the VRG restructure plan. In long-term orientation, the main function of rubber industry firms will focus on: (1) Planting and processing rubber, (2) Producing and processing wood, (3) Developing industrial park on rubber acreage.

Stocks of natural rubber company are divided into 2 groups. In which, 1st group includes: PHR, DPR, TRC

are seen as 3 companies having highest ROE and ROA (average ROE is 35% and ROA is 21%), this group has the best and the most stable profit margin. The 2

nd group includes: HRC and TNC with smaller scale in

terms of equity, total assets and rubber area. Besides that, these 2 companies have lower profit margin with ROE from 15-25% and ROA from 13-17%. With small scale and old rubber area, it results to lower efficiency of HRC and TNC than 3 other companies. In general, companies in natural rubber industry operate relatively well, healthy financial status, high dividend but quite low liquidity; they are appropriate for value investing.

The business results in 1st quarter of 2013 of almost companies in natural rubber industry are significantly

lower than the same period of 2012 (total revenue down by 33%, profit before tax down by 56%) due to lower consumption and lower selling price (output down by 24% and price down by 10-14%).

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

1

www.fpts.com.vn

Recommendation:

PHR: is the largest company among 5 companies listed in natural rubber industry at present, in 2008-2012 period, the average sales growth rate was 19.4%/year, average ROE was 35.5%/year. According to 2013 business plan, forward EPS is 4,800 VND, with the price on June 12

th, 2013 of

29,800VND the forward P/E of 2013 is 6.2 times. Dividend in 2012 was 30% in cash and that of 2013 is expected to be 30%. DPR: In 2008-2012 period, DPR had average sales growth rate about 17%/year, average ROE of 32.1%. It has had the highest profit margin in 5 listed natural rubber companies. EPS in the two recent years reached the highest level, 2011 was 18,663 VND and 2012 was 12,552 VND, this is a suitable stock for investment. According to business plan in 2013, forward EPS is 11,000 VND, with the price on June 12

th, 2013 of 50,000

VND, the forward P/E of 2013 is 4.5 times. The dividend in 2012 was 40% in cash and that of 2013 is expected to be 30%. TRC: is the 3

rd highest sales growth rate in listed natural companies, following PHR and DPR in 2008-2012

period with average sales growth rate of 14%/year, average ROE of 35%/year. According to 2013 business plan, forward EPS is 7,600 VND, with the price on June 12

th, 2013 of 49,000

VND, the forward P/E of 2013 is 6.4 times. The dividend in 2012 was 35% in cash, that of 2013 is expected

to be 30%.

With the currently declining rubber price, it shows that 2013 will be a difficult year for companies in

natural rubber industry. The investment recommendation is given for long-term basis, and limited for

short-term in this year.

Investors using this report should mention that the assessments are based on subjective opinions of FPTS

analysts. Investors take their own responsibility on investment decisions. Please read carefully the disclaimer

at the end of this report.

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

2

www.fpts.com.vn

CONTENTS

I. NATURAL RUBBER INDUSTRY OVERVIEW ...................................................................... 4

1. Global natural rubber industry .................................................................................... 4

2. Domestic natural rubber industry ............................................................................... 5

2.1 The position of Vietnam natural rubber industry. ...................................................... 5

2.2 Scale and dispersion structure of Vietnam natural rubber ........................................ 7

2.3 Output, natural rubber tapping productivity in Vietnam ............................................. 9

2.4 The natural rubber import-export situation of Vietnam .............................................11

II. 2013 NATURAL RUBBER INDUSTRY OUTLOOK..............................................................14

III. SITUATION OF LISTED NATURAL RUBBER COMPANIES ..............................................16

1. Operating scale ............................................................................................................16

1.1 Listed companies in the industry .............................................................................16

1.2 Rubber area, tapping volume of companies year by year .......................................17

2. Rubber area structure of listed companies ...............................................................19

3. Product structure of listed companies .......................................................................20

4. Business plan and 2013 outlook of typical companies .............................................21

APPENDIX

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

3

www.fpts.com.vn

ABBREVIATION CATALOGUE

PHR : Phuoc Hoa Rubber Joint Stock Company

DPR : Dong Phu Rubber Joint Stock Company

TRC : Tay Ninh Rubber Joint Stock Company

HRC : Hoa Binh Rubber Joint Stock Company

TNC : Thong Nhat Rubber Joint Stock Company

JSC : Join Stock Company

LTD : Limited

VRG : Vietnam Rubber Group

MARD : The Ministry of Agriculture and Rural Development

Net profit before tax : Net PBT

Net profit after tax : Net PAT

AGROINFO : Information Center for Vietnam Agriculture and Rural Development

IRSG : International Rubber Study Group

ANRPC : Association of Natural Rubber Producing Countries

GSO : General Statistics Office

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

4

www.fpts.com.vn

I. NATURAL RUBBER INDUSTRY OVERVIEW

1. Global natural rubber industry

In 2012, total natural rubber production was 11.4 mil tonnes, increase by 3.97% yoy. In which,

Asia accounted for major portion with about 93% of the global production, the following

continents were Africa (4-5%), Latin America (2.5-3%).

According to the statistics of IRSG, the global natural rubber consumption in 2012 was 10.9 mil

tonnes, went up by 0.23% yoy. Asia had the highest natural rubber consumption in the world,

about 69.7% of the global demand, the next one was Europe (13.5%), North America (10.7%).

The 4 leaders of natural rubber production includes: Thailand, Indonesia, Malaysia, Vietnam

keeps about 82% of total production output in the world; the group with highest global

consumption includes: China (33.5%), US (9.5%), India (8.7%), Japan (6.6%), Malaysia (4.6%).

For China, the five-year average consumption volume was 32% of total natural rubber

consumption in the world and accounted up to 25% of global import. The top 4 natural rubber

exporters are: Thailand (2.8 mil tonnes), Indonesia (2.45 mil tonnes), Malaysia (1.31 mil tonnes)

and Vietnam (1.02 mil tonnes), account for about 87% of global natural rubber export volume.

Global distribution in terms of consumption

Source: Agroinfo, FPTS

Unit: Mil tonnes

Global natural rubber production and consumption

2000-2012

Global distribution in terms of production

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

5

www.fpts.com.vn

The average growth rate of plantation area in 2000-2011 period was 3.8%/year. Total natural rubber area in the world to 2012 was 9.56 mil hectares. The average volume growth rate in 2000-2012 period was 4.2%/year. The 2012 volume was 11.41 mil tonnes, increased by 4.6% compared with 2011. The tapping productivity from 2007 up to now has been dropped from 1.23 ton/hectare down to 1.14 ton/hectare. This is the lowest level in the last 6 years.

2. Domestic natural rubber industry

2.1 The position of Vietnam natural rubber industry.

To the end of 2012, Vietnam ranked the 5th in the word for the natural rubber tapping volume with

the portion of 7.6%, equivalent to 863,600 tonnes and ranked the 4th for the natural rubber export

in the world, accounted for 10.3% of the global market share, equivalent to 1.02 mil tonnes. Four

countries including: Thailand, Indonesia, Malaysia, Vietnam account for 87% of total global natural

rubber export volume. In addition, these four countries also account for 73% of total global natural

rubber production, in which: Thailand (3.55 mil tonnes), Indonesia (3.00 mil tonnes), Malaysia (0.95

mil tonnes), India (0.904 mil tonnes) and Vietnam (0.86 mil tonnes).

Global volume and tapping capacity in

2000-2012 period

Global natural rubber area in 2000-2011 period

Top 5 countries in terms of production volume

Source: Agroinfo, FPTS

Top 4 countries in terms of export volume

Source: Agroinfo, FPTS

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

6

www.fpts.com.vn

Top 5 countries of tapping volume at the end of 2012

Indicators Thailand Indonesia Malaysia India Vietnam

Total area (hectare) (*) 2,756,000 3,456,000 1,048,000 737,000 910,500

Tapping volume (tonnes)

3,500,000 3,000,000 950,000 904,000 863,600

Average productivity (ton/hectare)

1.72 1.16 1.47 1.82 1.71

In the last 2 years, Vietnam reached to the 5th

position of global rubber area, in particular, in

2012, rubber area of these countries were as

following: Thailand (2.756 mil hectares),

Indonesia (3.456 mil hectares), China (1.07 mil

hectares), Malaysia (1.048 mil hectares),

Vietnam (0.91 mil hectares), India (0.737 mil

hectares).

At the end of 2012, according to the statistics of

ANRPC and VRG, Vietnam ranked the 5th for

the global natural rubber tapping volume, with

863,600 tonnes. Moreover, Vietnam had the

highest growth rate in terms of volume and area

in the world, the average growth rates in 2000-

2012 period were 9.5%/year in production and

6.8%/year in area, respectively. According to the

end of 2012’s data, tapping volume of these

countries were as following: Thailand (3.5 mil

tonnes), Indonesia (3.0 mil tonnes), Malaysia

(0.95 mil tonnes), Vietnam (0.86 mil tonnes) and

India (0.904 mil tonnes).

About the tapping volume, Vietnam is still lower

than 4 above countries. But in terms of tapping

productivity, Vietnam ranks the 2nd in the world,

the 2012’s rubber yield was 1.71 ton/hectare,

the leader was India with 1.82 ton/hectare. The

recent 5-year average of Vietnam was 1.70

ton/hectare, in which, India was 1.82

ton/hectare, Thailand was 1.68 ton/hectare,

Indonesia was 1 ton/hectare and Malaysia was

1.46 ton/hectare.

National rubber area in 2000-2012 period

National exploitation output in 2000-2012

period

National tapping productivity in 2000-2012

period

Source: Agroinfo, IRSG, ANRPC

(*) Except for Vietnam (31/12/2012), other countries’ data is updated at the end of

February 2012

To

n/h

ecta

re

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

7

www.fpts.com.vn

In the top four countries with highest natural

rubber export volume in 2007-2012 period,

Vietnam and Malaysia were two countries with

high export growth level, in particular: Malaysia

was 12.1%/year, Vietnam was 7.5%/year, that of

Thailand was 2.8%/year and Indonesia was

0.3%/year.

One noteworthy point of Indonesia and Malaysia is the most of their rubber area focusing on small

regions (smallholder farming), in particular, 85% rubber area in Indonesia belongs to minor

production area; this rate of Malaysia is 93%. According to the survey, this rate of Vietnam is more

balanced, in particular, the major holder farming (Government Company, JSC of VRG) accounts

for 44.36%, that of smallholder farming is 49.28% and private sector is 6.36%. With current plant

for rubber area expansion, in the future, the area for major holder farming will quickly surpass the

smallholder farm to obtain the highest portion in Vietnam.

2.2 Scale and dispersion structure of Vietnam natural rubber

Total rubber area and rubber tapping area in Vietnam

in 2005-2012 period

Source: GSO

Natural rubber export volume of Thailand, Malaysia,

Indonesia and Vietnam in 2007-2012 period

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

8

www.fpts.com.vn

Rubber area dispersion in terms of region

According to the regulation in Decision No. 750/QĐ-TTG and No. 124/QĐ-TTg of Prime Minister

to 2015 and 2020 vision, total domestic rubber acreage will be stable at the level of 800,000

hectares. However, to the end of 2012, according to the statistics of MARD, total area planned

for rubber plantation was 910,500 hectares, surpassed the planning for 2015. In which, rubber

tapping area accounted for about 55.55%, equivalent to 505,800 hectares. Total volume to the

end of 2012 was 863,600 tonnes, average productivity was 1.71 ton/hectare, slightly lower than

the 1.72 ton/hectare level of 2011.

The probability that Vietnam will have more than 1 mil hectares of rubber in 2015-2020 period is

very high. Accordingly, the South-eastern Region will be 390,000 hectares, the Highland Region

will be 280,000 hectares and the Southern Central Coast will be 40,000 hectares, the Northern

Central Region will be 80,000 hectares, and provinces in North-western Region will be 50,000

hectares and 200,000 hectares in Laos and Cambodia.

Regarding mainly key provinces, Binh Phuoc and Binh Duong are currently having the largest

area for rubber plantation. In which, Binh Phuoc accounts for 22% of total country area and 36%

of total area of the South-eastern Region. Binh Duong accounts for about 18%, the next

provinces are Tay Minh 10%, Gia Lai 11%, Dong Nai 6% of total country area.

Source: Decision No. 750/QĐ-TTg of Prime Minister and GSO, MARD

Rubber area in 2010-2012 period

Source : FPTS’s gathering

Rubber area dispersion in Vietnam Rubber area dispersion in key provinces

Unit: hectare

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

9

www.fpts.com.vn

According to planning data of VRG, to the end of 2012, the South-eastern Region will have the

largest rubber area in Vietnam. Total VRG rubber area will be 358,000 hectares, 273,000

hectares domestically planted and about 85,000 hectares abroad. To the end of 2012, total

rubber area of listed companies only accounted for about 6% of total country area and

accounted for 15% of total VRG area (including area planted overseas).

2.3 Output, natural rubber tapping productivity in Vietnam

In the last 12 years, Vietnam rubber area grew

relatively well, averaged at about 6.8%/year

from 413,000 hectares in 2000 to 910,500

hectares in 2012.

To 2012, Vietnam rubber exploitation output

was 863,600 tonnes, up 6.4% yoy. Average

output growth rate in 2000-2012 period was

9.5%/year.

In 2000, Vietnam rubber tapping productivity

was only 1.25 ton/hectare, to 2012, this level

grew to 1.71 ton/hectare. This number has

been stable in the last 3 years and at the

highest level in the last 10 years. It was the

second highest figure in the world, only after

India, that of India was 1.82 ton/hectare, and it

was approximately the same with Thailand level

of 1.72 ton/hectare, significantly outstripped the

global average level and higher than two

leaders in natural rubber production, Malaysia

(1.47 ton/hectare) and Indonesia (1.16

ton/hectare).

At present, in terms of exploitation volume,

listed companies are only accounting for about

6% of total domestic volume, 19% of VRG

(267,000 tonnes). Dong Nai Rubber General

Company is currently the biggest company with

volume of 35,000 tonnes. Total exploitation

volume of listed companies in 2012 was 51,038

Output, natural rubber tapping productivity

in Vietnam in 2000-2012 period

Source: Agroinfo

The exploitation volume in 2010-2012 period

Unit: Ton

Unit: ton

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

10

www.fpts.com.vn

tonnes, in which Phuoc Hoa JSC had the

highest number of 19,954 tonnes. More than

77.15% of total domestic exploitation belongs to

other subsidiaries in VRG, smallholder farming

and private companies.

In terms of key regions, Tay Ninh has the

highest tapping productivity in Vietnam with the

level of 2.10 tonnes/hectare, following by Binh

Phuoc with 1.98 ton/hectare and Binh Duong

with 1.85 ton/hectare.

In order to obtain this achievement, VRG and

Vietnam Rubber Association have made effort

continuously. The overall planning of the rubber

plantation area throughout the country

accompanies with advanced plantation method

and new plant hybridization, they have resulted

to the leading position of Vietnam in terms of

productivity among the top natural rubber

producing countries in the world.

The Vietnam rubber consumption position

in the recent years

In 2008-2012 period, the natural rubber

consumption growth rate averaged at about

11%/year, average consumption was about

132,000 tonnes/year, the average

consumption/exploitation ratio was about 17-

18%. In particular, it was 100,000 tonnes in

2008 and up to 150,000 tonnes in 2012.

The uses of natural rubber in Vietnam are

primarily for tire, medical glove, pillow,…

Additionally, natural rubber consumption is

mainly contributed by temporary import and re-

export activity.

The low domestic consumption is the result of

small domestic production scale, rubber export

companies focus on export to achieve higher

efficiency and profit level. The current

consumption is reflected by the trading form

among commercial companies in Vietnam,

afterward, these companies also export. In fact,

in consumption structure of listed companies,

The exploitation and consumption volume in

2002-2012 period

Tapping productivity in key regions

Unit:Ton/hectare

Unit: Thousand tonnes

Source: Agroinfo, FPTS

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

11

www.fpts.com.vn

there is about 40-50% for domestic

consumption but eventually this amount is

exported through commercial companies.

Therefore, the natural rubber supply actually

outnumbers the domestic demand very

significantly, average level of about 5-6 times in

the last 3 years.

2.4 The natural rubber import-export situation of Vietnam

2.4.1 The import situation

In 2012, the natural rubber import volume was

about 302,000 tonnes, decreased by 16.6%

compared with 2011; import value was 803.29

mil USD, dropped by 14.9% yoy. Every year,

the rubber import portion still maintains at high

level due to compensation for some materials

for domestic production that are inadequate or

not produced such as: RSS, Skim, CSR10…

Besides that, the temporary import and re-

export activity has boosted the import volume.

As the estimate in total of import volume, it is

about 60% for temporary import and re-export

activity and 40% for domestic consumption.

This shows that the actual domestic

consumption/exploitation ratio is relatively

modest, about 17-18%.

In 2012, Vietnam imported natural rubber from

more than 40 countries around the world,

mostly from: Cambodia, Thailand, Myanmar,

Laos and Korea.

From 2010 till now, Cambodia is the largest

rubber supplier of Vietnam, about 59% in terms

of quantity and 60% in terms of value. The next

one is Thailand with 17% in terms of quantity

and 18% in terms of value. They have

geographical advantage and appealing price for

import.

The import volume and value in

2010-2012 period

Source: General Department of Customs

Import market portion in terms of

quantity - 2012

Import market portion in terms of

value - 2012

Th

ousand

to

nn

es

Th

ousand

dolla

rs

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

12

www.fpts.com.vn

2.4.2 The export situation

Rubber is one of three major agricultural

products for export in Vietnam. In 2011,

rubber accounted for 24% of total

agricultural product export value.

The average natural rubber export growth

rate of Vietnam in 5 years was 11.9% in

terms of volume and 15.5% in terms of

value.

In 2012, according to the Statistics

Department, Vietnam’s natural rubber export

volume was 1.02 mil tonnes, valued 2.85 bil

USD; increase by 25% in volume and

declined by 11.7% in value yoy. Export

surplus in 2012 was 721,000 tonnes, valued

2.05 bil USD; increased 57.8% in volume

and decreased 13.6% in value. The cause

was over 16.6% decrease in importing

natural rubber. The higher volume was not

enough to offset for the decrease in rubber

price. In particular, the average export price

reduced by 29% compared with 2011, from

3,961 USD/ton to 2,795 USD/ton.

If we just consider the listed companies,

their export volume accounts for a very

small portion of total industry, from 3%-4%

equivalent to 28-30 thousand tonnes. About

three largest listed companies: PHR, DPR,

TRC, their export volume in 2012 dropped

by only 0.5% but export revenue dropped by

up to 29% compared yoy, it was the result of

rapid decrease last year.

The main exporters of Vietnam are: China,

Malaysia, Taiwan, Korea, German, India,

U.S....In which, China is the largest market

accounting for about 40% of total natural

rubber export value of Vietnam in 2012. Last

year, natural rubber export to it was 408

thousand tonnes, valued 1.17 bil USD,

reduced by 19% in terms of volume and

39% in terms of value compared with 2011.

Portion of rubber and major commodities

export in 2011

Volume and value of natural rubber

export in 2010-2012 period

Th

ousand

dolla

rs

Th

ousand

to

nn

es

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

13

www.fpts.com.vn

Although, China is major market and highly

potential, Vietnamese companies have

attempted to diversify the export market to

reduce the excessive dependence on China

to limit the risk of selling price fluctuation

and export order. In particular, in 2011,

Chinese market accounted for 60% of total

Vietnam natural rubber export value but in

2012 this number was only 40-41% both in

volume and value. This is a beneficial

direction for natural rubber exporters; it will

enable the natural rubber trading activity

and product from rubber to be more stable

and better development.

In terms of volume, Vietnam accounts for a

relatively large portion in natural rubber

import structure of countries in the area and

in the world, in particular: India (11-15%),

China (8.6%), Korea (10%), Malaysia (7%)

and US (2%).

About listed natural rubber companies, in

recent years, these companies often did not

directly export to China but through to the

sales to domestic commercial companies

and they exported to China. Therefore,

these companies only bear the indirect

affect from China. The major export markets

for these listed companies are Europe and

some Asian countries (except for China).

Besides that, they also have found major

customers with high credibility in other

potential overseas market to expand their

export market, to limit the risk for their

products.

Source: General Department of Customs

Export portion in terms of volume

in 2012

Export portion in terms of value

in 2012

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

14

www.fpts.com.vn

II. 2013 NATURAL RUBBER INDUSTRY OUTLOOK

1. Industry outlook

For the world: the natural rubber output in 2013 is expected to grow slowly due to the

oversupply along with weak demand. According to the forecast of IRSG, the expected global

rubber output will be 11.77 mil tonnes and demand will be 11.59 mil tonnes, oversupply will

be 179,000 tonnes. However, the Governments from Thailand, Indonesia and Malaysia also

agreed to reduce the export volume of 300,000 tonnes to constraint the decrease in price of

this product, this action will prevent from the oversupply situation in 2013.

The forecast on exploitation volume growth rate in 2013 of major rubber producers in the

world: Thailand increase by 3.4%, Indonesia decrease by 8.9%, Malaysia increase by 6.5%,

India increase by 3.8%, Vietnam increase by 10% (for VRG).

At present, to April 2013, the total natural rubber inventory at two general warehouses:

Shanghai and Qingdao of China was 480,000 tonnes, at the 3-year highest level, accounted

for more than 16% of import in 2013. With high inventory as well as import rubber demand for

China automobile tire manufacturing is expected to grow by only 0.9% in 2013, additionally,

the pressure from Chinese Yuan appreciation to reduce export surplus, European sovereign

debt crisis does not have improvement sign, they will constraint the increase of rubber price

in the near future. According to industry specialists, in 2013, the rubber price will reduce in

the first half year and will endure the decrease in the next period if there is no sign of

recovery from major economies like: US, China and Japan.

Natural rubber price movement in 2008-2012 period

Source: FPTS’s gathering

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

15

www.fpts.com.vn

For Vietnam:

About export:

The forecast on China import demand (the biggest export market of Vietnam) shows that

there will be a slight growth of 0.9%. In the meanwhile, as the cautious estimate of MARD,

the natural rubber export in 2013 will be approximately 1 mil tonnes, slightly lower than 1.02

mil tonnes of 2012.

Furthermore, on December 17th, 2012, the Chinese Ministry of Finance stated that it will cut

back the tax on natural rubber import in 2013. This is a good signal for domestic

manufacturing and trading companies in 2013.

Besides that, for India (the 3rd largest natural rubber importer of Vietnam), the 17% depreciation of Rupee will encourage the India tire export industry, it will grow by from 8-10% in 2013. Consequently, it will lift up the demand for import natural rubber for manufacturing, it is estimated that India will in need of about 225,000 tonnes in 2013, increase by 9.7% compared with 2012.

However, the drop in rubber price is one of the barriers of domestic rubber companies. The

natural rubber price is forecast to be in downtrend in the first half of this year. The recovery in

the rest of the year is still no answer, but the majority of specialists and research agencies

suppose that rubber price will be decrease in long term. Therefore, the growth of natural

rubber industry in the next period will depend on the volume growth.

About the domestic market:

According to the latest data, the domestic demand in the last 3 years accounted for about 17-

18% of total domestic supply. This rate will be improved from 2013 when Da Nang Rubber

JSC and Casumina launch two entire-steel radial tire plants. Besides that, in 2012, VRG has

invested in upgrading the productivity of VRG Khai Hoan Glove Manufacturing Plant from 1.2

bil to 3.2 bil units/year, this will be promising for the higher domestic demand in the near

future.

2. The development strategy

In 2013, VRG will exploit the first 600 hectares of rubber in Cambodia. To the end of 2012, VRG planted 63,000 hectares of rubber in Cambodia. It plans to complete 100,000 hectares in 2014.

To 2015, it is expected to have stable rubber area of 800,000 hectares, the productivity will be 1.2 mil ton/year. Nevertheless, to the end of 2012, total Vietnam rubber area was 910,500 hectares, higher than the 2015 plan figure. As a result, VRG is proposing the Government for a higher adjustment to 1 mil hectares in 2015. In 2020-2030 period, the rubber volume of Vietnam is expected to be about 1-1.1 mil ton/year, account for about 10% of global volume, it will be a favourable advantage of Vietnam natural rubber industry.

The Government has had the plan to expand the rubber area to the Northern provinces. According to the plan, to 2020, there will be 50,000 hectares of rubber area planted in the North-western provinces. After many years of implementation, at present, MARD announces that the North-western provinces have 19,707 hectares of rubber planted, that fulfils 39% the plan. In which, Son La has 6,664 hectares, Dien Bien has 3,468 hectares, Lai Chau has 8,986 hectares. In the demand of development and the land support from farmers of the Northern mountainous area, MARD has asked the Prime Minister for the

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

16

www.fpts.com.vn

adjustment for the rubber development plan in the North-western Region from 50,000 hectares to 100,000 hectares to 2020.

On November 23rd, 2012, the Prime Minister signed the Decision No. 1782/QĐ-TTg regarding the Vietnam Rubber Group Restructure Plan. Accordingly, it is planned to withdraw capital from the investment outside of core industry in 2012-2020 period. For long-term orientation, the main activities of companies in industry will focus on: (1) Rubber plantation and processing, (2) Wood production and processing, (3) Industrial park development on rubber planting area. According to the capital withdraw plan, it will partial affect the listed companies. In particular, PHR will on the 2012-2015 road map to withdraw capital from the hydropower and other industry sectors such as: Gruco Gon River Hydropower, VRG Ngoc Linh Hydropower, VRG Sai Gon Investment JSC. HRC and DPR also withdrawal from Viet Long Investment Fund, TRC has planned to withdraw capital from Rubber Commercial Services and Tourism JSC, VRG Infrastructure Investment Ltd Company... Furthermore, in the future, the major companies in industry being in the form of Single Member Ltd Company will be equitized to attract investment and improve the competition in industry.

According to the plan, VRG will keep 100% capital of 22 Single Member Ltd Companies; hold more than 50% of 18 JSC; less than 50% of 20 other companies.

In general, this capital withdrawal plan will be a strategic step for long-term development of

entire industry. This will foster financial capital and human resources concentration for the whole

industry to improve the strength and core business for future sustainable development.

III. SITUATION OF LISTED COMPANY IN NATURAL RUBBER INDUSTRY

1. Operating scale

1.1 Listed companies in the industry:

Indicators on March 31st

, 2013 PHR DPR TRC HRC TNC

Stock exchange HOSE HOSE HOSE HOSE HOSE

Chartered capital (mil VND) 813,000 430,000 300,000 172,610 192,500

Total assets (mil VND) 3,101,131 2,821,172 1,484,791 656,835 379,867

Owners’ equity (mil VND) 2,024,148 2,179,990 1,308,986 484,351 329,669

Outstanding shares (shares) 78,490,047 43,000,000 29,125,000 17,260,976 19,250,000

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

17

www.fpts.com.vn

Name

Dec 31st

,2012 Rubber area

(hectares)

Tapping area

(hectares)

Productivity (Ton/hectare)

Tapping output

(Tonnes)

Phuoc Hoa Rubber Joint Stock Company - PHR

22,489 11,000 2.00 19,954

Dong Phu Rubber Joint Stock Company – DPR

15,925 7,121 2.30 16,368

Tay Ninh Rubber Joint Stock Company – TRC

7,300 5,407 2.15 11,602

Hoa Binh Rubber Joint Stock Company – HRC

5,101 1,812 0.88 1,700

Thong Nhat Rubber Joint Stock Company – TNC

2,075 1,298 1.09 1,414

1.2 Rubber area, tapping volume of companies year by year

Source: FPTS’s gathering

Area

Tapping volume

Unit: hectare

Unit: ton

The rubber acreage of almost

companies increased in 2012. The

main factor for year by year area

growth is the rubber plantation in

Laos and Cambodia. In specific, in

2012, PHR added 2,278 hectares

in KamphongThom - Cambodia;

DPR added 1,300 hectares in

Kratie - Cambodia; TRC added

473 hectares in SiemRiep -

Cambodia, HRC is currently

replanting in large scale, resulting

to significant fall in tapping area, it

is only 2,241 hectares at present,

TNC in 2012 maintained the

productive area of 1,344 hectares.

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

18

www.fpts.com.vn

Source: FPTS’s gathering

Unit: t

on/h

ecta

re

Unit: h

ecta

re

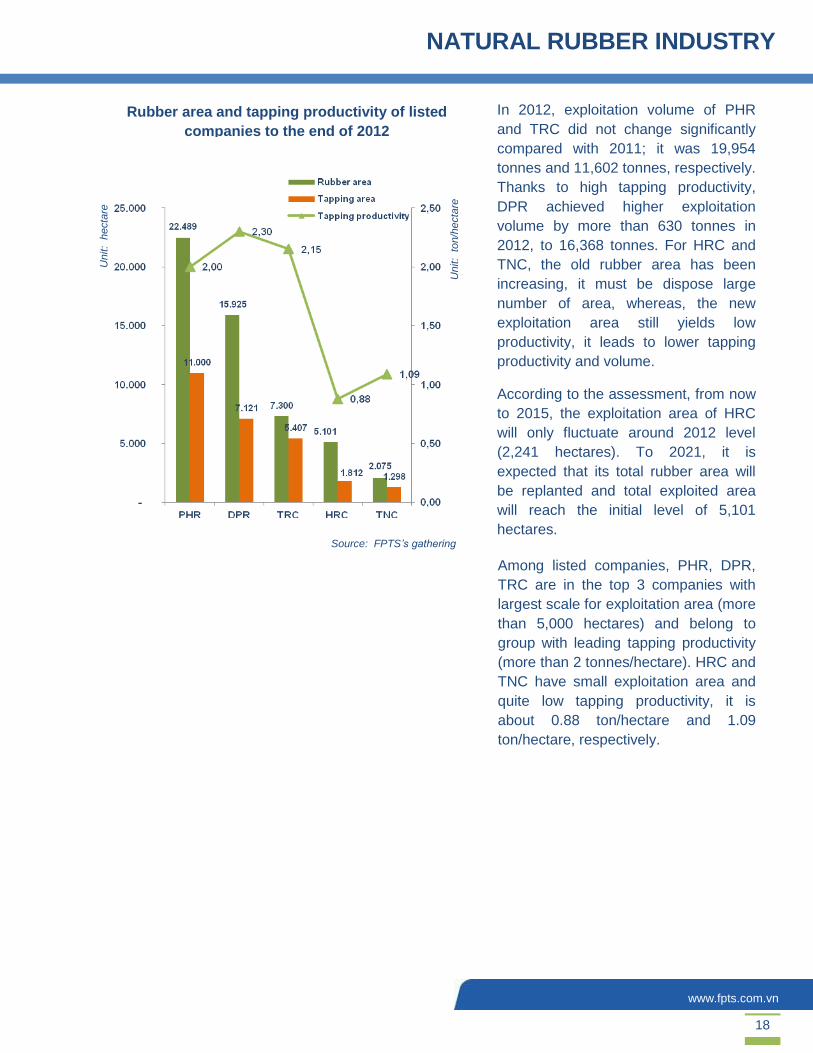

Rubber area and tapping productivity of listed

companies to the end of 2012

Among listed companies, PHR, DPR,

TRC are in the top 3 companies with

largest scale for exploitation area (more

than 5,000 hectares) and belong to

group with leading tapping productivity

(more than 2 tonnes/hectare). HRC and

TNC have small exploitation area and

quite low tapping productivity, it is

about 0.88 ton/hectare and 1.09

ton/hectare, respectively.

In 2012, exploitation volume of PHR

and TRC did not change significantly

compared with 2011; it was 19,954

tonnes and 11,602 tonnes, respectively.

Thanks to high tapping productivity,

DPR achieved higher exploitation

volume by more than 630 tonnes in

2012, to 16,368 tonnes. For HRC and

TNC, the old rubber area has been

increasing, it must be dispose large

number of area, whereas, the new

exploitation area still yields low

productivity, it leads to lower tapping

productivity and volume.

According to the assessment, from now

to 2015, the exploitation area of HRC

will only fluctuate around 2012 level

(2,241 hectares). To 2021, it is

expected that its total rubber area will

be replanted and total exploited area

will reach the initial level of 5,101

hectares.

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

19

www.fpts.com.vn

2. Rubber area structure of listed companies

At present, among listed companies, HRC has highest portion of old rubber area, HRC has up

to 50% of rubber area more than 24 years old and is currently replanting about 47% by new

area. It leads to lower exploitation efficiency and lift the exploitation expense of HRC in

comparison with other companies in the industry.

PHR currently has 22% of rubber area more than 25 years old, 42% of area from 11-25 years

old but it is compensated by about 29% of area in basic construction stage to replace old area.

DPR has 15% of rubber area more than 25 years old, however it has up to 70% of area in the

period of yielding high productivity. TRC has 13% of area more than 25 years old and 71% of

area in energetic period with high ability to produce latex. TNC has about 18% of area more

than 25 years old, 39% from 11-25 years old and it is replanting in large rate with more than

32% of area from 0-6 years old.

DPR

a DPR

TRC PHR

a DPR

HRC

a DPR

TNC

a DPR

Source: Listed company data, FPTS’s gathering

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

20

www.fpts.com.vn

3. Product structure of listed companies

The product structure of listed companies in natural rubber industry implies that almost the

companies produce SVR and Latex. In which, SVR dominates; this is also the advantageous

product of Vietnam. In the structure of natural rubber product export, this product accounts for

roughly 75-80%. PHR and HRC mainly focus on high value SVR CV50, 60; DPR focuses on

SVR3L, SVR10, 20; TRC has the strength in Latex and TNC has RSS which creating

competitive advantage over the rest listed companies.

PHR

TRC DPR

Source: Listed company data and VRG

HRC

PHR

TNC

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

21

www.fpts.com.vn

4. Business plan and 2013 outlook of typical companies

Indicators Unit PHR DPR TRC

Market price (12/06/2013) VND/share 29,800 50,000 49,000

Average 3-month trading volume Share/day 67,171 15,614 2,580

Gross profit margin % 29.48 39.96 32.42

Net PBT margin % 33.96 42.52 42.59

2012 ROE % 31.78 26.39 28.60

2013E EPS VND/share 4,800 11,000 7,600

P/E forward Times 6.2 4.5 6.4

Source : Listed companies’ consolidated financial statement

and FPTS’s gathering

PHR

PHR is the largest company among 5 listed natural rubber companies with average revenue

growth rate of 19.4% in 2008-2012 period, average ROE of 35.5%/year. With large scale of

rubber area and large portion of high-value and diverse products, it has created competitive

advantage over other listed companies. One noteworthy point about PHR is that the corporate

tax rate imposed on PHR is 25% while other companies such as DPR, TRC are granted with the

tax rate of 15% and reduced by 50% (according to the provision of Circular No. 134/2007/TT-

BTC issued by the Ministry of Finance on November 23rd, 2011 about equitization of State

enterprises). This undermines the operating efficiency of PHR compared with other companies

in industry.

According to the 2013 business plan: consumption volume will decrease by 17%,

revenue will decrease by 20%, Net PBT will decrease by 32% compared with 2012 result.

Expected dividend is 30%.

According to 2013 plan, PHR sets the consumption of about 26,000 tonnes of rubber, decrease

by 17% compared with 2012. This substantial drop is caused by the reason that the company

will exploit new rubber area with low productivity in first period; average tapping productivity is

2013 Plan Unit PHR DPR TRC

Total area Hectare 22,733 16,907 7,773

Tapping area Hectare 10,636 7,121 5,011

%FY2012 100% 100% 93%

Consumption Tonnes 26,000 20,000 12,602

%FY2012 83% 104% 91%

Average selling price Mil

VND/Ton 62 62 62

%FY2012 95% 97% 100%

Revenue Bil VND 1,857 1,434 901.3

%FY2012 80% 103,6% 98%

Net PBT Bil VND 504 515 256.9

%FY2012 68% 87% 67%

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

22

www.fpts.com.vn

estimated to be only 1.84 ton/hectare compared with 2 tonnes/hectare of 2012. With the

temporary selling price appointed by VRG of 62 mil VND, reduced by 20% compared with 2012,

Net PBT is forecast to be 504 bil VND, reduced by 32% compared with 2012. At the moment,

PHR has signed about 60% of orders for 2013.

1st quarter of 2013 business result: net sales was 331.6 bil VND, accomplished 17.8% of

2013 plan; Net PBT was 65.69 bil VND, accomplished 13% of 2013 plan, reduced by 71%

compared with the same period of 2012. Average selling price in 1st quarter of 2013 was 62.3

mil VND/ton.

Revenue and profit figures plummeted compared with the same period of 2012 due to: (1) 2,327 tonnes reduction in consumption; (2) 10.36 mil VND/ton reduction in selling price; (3) 119.64 hectares reduction in rubber disposal area. If the price maintains at present level, it will accomplish and even exceed the 2013 plan set by Annual General Meeting’s decision.

Rubber plantation plan

KamthongThom Project: to 2013, it is expected to plant the last 300 hectares to achieve the

plan of 7,600 hectares of rubber area. At the end of 2014, the first 500 hectares will be tapped

(planted in 2009).

Daklak Project: PHR only planted 113 hectares. In 2013, it is expected to plant 1,000 hectares

additionally and complete 8,000 hectares to 2017.

2012 ROE was 31.78%, the highest of 5 listed companies.

According to the 2013 business plan, forward EPS is 4,800 VND, as the price of 29,800

VND on June 12th, 2013 the forward P/E will be 6.2 times. Under the rapid decrease in

rubber price circumstance at present, it is recommended for long-term investment, and

limiting short-term investment in this year.

DPR

In 2008-2012 period, DPR had the average sales growth rate of 17%/year, average ROE of 32.1%/year. In terms of profit to sales ratio, DPR has the most effective business result among 5 listed

companies. The EPS of 2 recent years were very high, they were 18,663 VND and 12,552 VND

in 2011 and 2012, respectively, this is good stock for investment.

According to 2013 plan: consumption volume increase by 4%, sales increase by 3.6%

and Net PBT will be equal 87% of 2012 result. Expected dividend is 30%.

According to 2013 plan, tapping area of DPR will unchanged, consumption output is expected

to be 20,000 tonnes, 4% higher than 2012 result and sales target is 1,434 bil VND, increase by

3.6% compared with 2012. Net PBT will be 515 bil VND, down by 13% compared with 2012.

1st quarter of 2013 business result: it got 228 bil VND of net revenue, accomplished 15.9%

of 2013 plan, 24% lower than the same period last year. Net PBT was 78.3 bil VND,

accomplished 15.2% of 2013 plan, reduced by 31% compared with same period of 2012.

Sales and profit figures lower than the same period were caused by low consumption in 1st

quarter, more than 660 tonnes (down by 24%), selling price reduced by more than 8.4 mil

VND/ton compared with 1st quarter of 2012.

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

23

www.fpts.com.vn

Rubber plantation project:

Dong Phu Kratie Project: to 2013, DPR plans to plant the last 300 hectares, completes 6,500

hectares of rubber area. At the end of 2014, it will exploit the first 1,100 hectares (planted in

2009).

Daknong Project: 946 hectares already planted. In 2013, it will plant 54 hectares more. At the

end of 2013, it will exploit 180 hectares (planted in 2007).

According to 2013 business plan, forward EPS is 11,000 VND; as the price on June 12th,

2013 of 50,000VND then the 2013 forward P/E is 4.5 times. Under the rapid decrease in

rubber price circumstance at present, it is recommended for long-term investment, and

limiting short-term investment in this year.

TRC

TRC is the listed company ranking the 3rd for sales growth rate after PHR and DPR in 2008-2012 period, sales growth rate was 14%/year. Average ROE was 35%/year.

2013 plan: consumption volume will go down by 9%; sales down by 12% and Net PBT

down by 33% compared with 2012. Expected dividend is 30%.

In this year, TRC will dispose the old rubber area, exploitation area will be decrease by about

500 hectares, it will lead to the lower output in 2013 as well as the lower selling price, down to

62 mil VND/ton, according to the plan and direction of VRG. TRC has set a relatively cautious

target.

1st quarter of 2013 business result: net sales was 183.8 bil VND, accomplished 20% of 2013

plan, decrease by 27% compared with the same period; Net PBT was 54.5 bil VND, completed

21% of 2013 plan, decrease by 7% compared with same period. Sales and profit went down as

the result of consumption dropped by more than 402 tonnes and selling price fell by about 7 mil

VND/ton compared with 2012.

Rubber plantation project: at present, TRC is fully drawing attention to the Tay Ninh Rubber

Siem Riep Project in Cambodia with total area of 7,600 hectares. In comparison with TRC’s

5,407 hectares currently exploited in Vietnam over total rubber area of 7,300 hectares, this

project plays a critical role in the long-term development of TRC. At the moment, 100% land of

this project has been granted by Cambodia Government, but it is awaiting the investment

license from Vietnam Government. Therefore, the company is facing the trouble of transferring

direct capital investment from Vietnam to Cambodia. However, according to the plan, to 2015,

7,250 hectares of rubber will be completely planted. Until now, there has been 473 hectares of

rubber planted, in 2013, the company is on schedule to plant 2,000 hectares more.

According to 2013 business plan, forward EPS is 7,600VND, as the market price on June

12th, 2013 of 49,000VND, then the 2013 forward P/E is 6.4 times. Under the rapid decrease

in rubber price circumstance at present, it is recommended for long-term investment,

and limiting short-term investment in this year.

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

24

www.fpts.com.vn

Liquidity of listed natural rubber company shares in 3 months

(Average volume over one trading session)

Source: FPTS’s gathering

Table of financial indicators of listed companies in natural rubber industry

P/E – P/B of companies compared with industry average ratio

Unit:Share/day

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

25

www.fpts.com.vn

APPENDIX

Year Total area Tapping Area Volume Tapping

productivity

2000 413,000 232,000 291,000 1.25

2001 416,000 241,000 313,000 1.30

2002 429,000 243,000 298,000 1.23

2003 441,000 267,000 364,000 1.36

2004 454,000 301,000 419,000 1.39

2005 483,000 334,000 482,000 1.44

2006 522,000 356,000 555,000 1.56

2007 556,000 373,000 602,000 1.61

2008 631,000 399,000 660,000 1.65

2009 678,000 422,000 724,000 1.72

2010 749,000 439,000 752,000 1.71

2011 834,000 472,000 812,000 1.72

2012 910,500 505,800 863,600 1.707

References

Ministry of Agriculture and Rural Development

Vietnam Rubber Group - VRG

Specialized information of Vietnam Rubber Group

Agroinfo statistics

IRSG statistics

Materials from International Rubber Conference in China

Material from Natural rubber market report of Industry and Commerce information Center of Ministry of Industry and Commerce

General Department of Customs data

General Statistics Office data

Data from websites: Thitruongcaosu.net, Tocom, AFET, Malaysian Rubber Board, Indexmundi, Thuvienphapluat và website doanh nghiệp.

Other materials

Vietnam natural rubber statistics

Source: Agroinfo

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

26

www.fpts.com.vn

5-year business result of listed companies in industry

PHR 2008 2009 2010 2011 2012 Average/CAGR

Revenue 1,091,577 1,067,844 2,030,099 2,583,186 2,218,195 19.38%

Gross profit 354,260 282,903 709,436 1,021,833 653,981 20.60%

Gross profit margin 32.45% 26.49% 34.95% 39.56% 29.48% 33.61%

Net PBT 388,939 351,095 661,578 1,003,389 753,204 17.97%

Net PBT margin 35.63% 32.88% 32.59% 38.84% 33.96% 35.12%

ROA 16.81% 14.48% 24.11% 30.65% 19.44% 21.06%

ROE 28.71% 28.71% 28.71% 28.71% 31.78% 35.54%

DPR 2008 2009 2010 2011 2012 Average/CAGR

Revenue 728,795 648,310 1,028,421 1,837,202 1,384,643 17.40%

Gross profit 252,024 233,460 463,062 866,224 553,307 21.73%

Gross profit margin 34.58% 36.01% 45.03% 47.15% 39.96% 42.08%

Net PBT 234,044 220,723 433,410 871,211 588,719 25.94%

Net PBT margin 32.11% 34.05% 42.14% 47.42% 42.52% 41.73%

ROA 21.48% 18.40% 27.00% 39.11% 20.56% 23.66%

ROE 36.67% 28.59% 38.37% 51.19% 26.39% 32.11%

TRC 2008 2009 2010 2011 2012 Average/CAGR

Revenue 549,115 440,353 757,982 1,195,284 915,510 13.60%

Gross profit 206,499 150,558 325,501 494,546 296,806 9.50%

Gross profit margin 37.61% 34.19% 42.94% 41.37% 32.42% 38.20%

Net PBT 198,220 162,510 304,993 568,058 389,933 18.43%

Net PBT margin 36.10% 36.90% 40.24% 47.52% 42.59% 42.08%

ROA 26.83% 21.12% 29.75% 40.78% 23.57% 27.27%

ROE 42.18% 28.25% 39.98% 54.38% 28.60% 34.73%

HRC 2008 2009 2010 2011 2012 Average/CAGR

Revenue 289,976 202,645 411,801 688,411 494,477 14.27%

Gross profit 98,951 50,816 105,668 134,112 40,139 -20.19%

Gross profit margin 34.12% 25.08% 25.66% 19.48% 8.12% 20.59%

Net PBT 88,025 71,523 106,512 142,537 110,502 5.85%

Net PBT margin 30.36% 35.29% 25.86% 20.71% 22.35% 24.87%

ROA 22.15% 15.88% 20.28% 22.83% 13.91% 17.88%

ROE 26.95% 19.37% 24.68% 29.55% 18.88% 22.97%

TNC (*) 2008 2009 2010 2011 2012 Average/CAGR

Revenue 181,765 171,590 181,156 144,666 191,088 3.65%

Gross profit 13,782 38,944 62,068 70,499 55,042 12.22%

Gross profit margin 7.58% 22.70% 34.26% 48.73% 28.80% 32.91%

Net PBT 8,393 34,402 60,427 82,403 79,429 32.17%

Net PBT margin 4.62% 20.05% 33.36% 56.96% 41.57% 37.28%

ROA 3.10% 11.06% 17.98% 22.10% 19.44% 17.21%

ROE 3.90% 12.80% 20.11% 24.80% 22.04% 19.40%

Source:Listed companies’ audited financial statements (*) Growth rate data of TNC was taken from 2009 to 2012 because in 2008,

there was an extraordinary change due to the economic recession.

NATURAL RUBBER INDUSTRY

09/05/2011

09/05/2011

27

www.fpts.com.vn

Disclaimers

The information and statements contained herein, including any expression of opinion, are based upon sources believed to be reliable but their accuracy, completeness or correctness is not guaranteed.

Expressions of opinion herein were arrived at after due and careful consideration and they were based upon the best information then known to us, and in our opinion are fair and reasonable in the circumstances prevailing at the time. Expressions of opinion contained herein are subject to change without notice.

This document is not and should not be construed as, an offer or the solicitation of an offer to buy or sell any securities. FPTS and other related companies and/or their officers, directors and employees may have positions and may have affect transactions in securities of companies mentioned herein and may also perform or seek to perform investment banking services for these companies.

No person is authorized to give any information or to make any representation not contained in this document and any information or representation not contained in this document must not be relied upon as having been authorized by or on behalf of FPTS. This document is private circulation only and is not for publication in the press or elsewhere.

FPTS accepts no liabilities whatsoever for any direct or consequential loss arising from any use of this document or its contents. The use of any information, statements forecasts and projection contained herein shall be at the sole discretion and risk of the users. This document is confidential and is intended solely for the use of its recipient. Any duplication or redistribution of this document is prohibited.

At the time of writing this analytic report, FPTS hold 4 shares of this enterprise and FPTS’ analysts do not hold.

The information related to other stocks or other information related this stock can be viewed at

https://ezsearch.fpts.com.vn or will be provided upon official request

Copyright © 2010 FPT Securities Corporation

FPT Securities Joint-stock

company

Head office

Floor 2 – Tower 71 Nguyen Chi

Thanh,

Dong Đa district, Hanoi, Vietnam

Phone: (84.4) 3 773 7070 / 271

7171

Fax: (84.4) 3 773 9058

FPT Securities Joint-stock

company

Ho Chi Minh city branch

29-31 Nguyen Cong Tru, Nguyen

Thai Binh ward, HCMC, Vietnam

Phone: (84.8) 6 290 8686

Fax: (84.8) 6 291 0607

FPT Securities Joint-stock

company

Da Nang branch

124 Nguyen Thi Minh Khai, Hai Châu

district, Da Nang city, Vietnam

Phone: (84.511) 3553 666

Fax: (84.511) 3553 888