nexus and state income taxes: to latest developmentsmedia.straffordpub.com/.../presentation.pdf ·...

TRANSCRIPT

Presenting a live 110‐minute teleconference with interactive Q&A

Economic Nexus and State Income Taxes: Responding to Latest DevelopmentsResponding to Latest DevelopmentsAvoiding Traps Triggered by Royalty Income, Support Activities, Excess Sales and Other Indirect Presence

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, DECEMBER 8, 2011

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Mike Shaikh Reed Smith Los AngelesMike Shaikh, Reed Smith, Los Angeles

Ellen McCabe, Tax Principal, LarsonAllen, Minneapolis

Jaye Calhoun, Member, McGlinchey Stafford, New Orleans, La.

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442 and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

Economic Nexus and State Income T R di t L t t Taxes: Responding to Latest Developments Seminar

Dec. 8, 2011

Ellen McCabe, [email protected]

Mike Shaikh, Reed [email protected]

Jaye Calhoun, McGlinchey Stafford [email protected]

Today’s Program

Recent Court Developments In This Area[Mike Shaikh]

Slide 7 – Slide 15

Recent Legislative And Regulatory Developments[Ellen McCabe]

Responses For Corporate Tax Departments To Consider

Slide 16 – Slide 25

Slide 26 Slide 44Responses For Corporate Tax Departments To Consider[Jaye Calhoun]

Developments On The Horizon

Slide 26 – Slide 44

Slide 45 – Slide 46p[Mike Shaikh]

RECENT COURT Mike Shaikh, Reed Smith

RECENT COURT DEVELOPMENTS IN THIS AREA

R Li i i Of NRecent Litigation Of Note

I. KFC (Iowa)

II. W.L. Gore (Maryland)

III L L B (Ohi )III. L.L. Bean (Ohio)

IV. Telebright (New Jersey)

V BIS (New Jersey)V. BIS (New Jersey)

VI. Vestax (Michigan)

VII. Whirlpool (New Jersey)VII. Whirlpool (New Jersey)

8

KFC CKFC Corp.

• KFC Corp. licenses KFC trademarks to franchisors in several states, including Iowa.

• No physical presence is required; economic presence is sufficient.

• Physical presence does not achieve a “bright line.”

• Licensing of intangibles into the state is held to an amount to the functional equivalent of physical presence under Quill.

• Also, sufficient nexus is based on the fact that the transactions that produced income were based on the use of intangibles in Iowa.

• U.S. Supreme Court denied certiorari.U.S. Supreme Court denied certiorari.

KFC Corp. v. Iowa Department of Revenue, 792 NW2d 308 (Iowa 2010), cert denied U S S Ct Dkt No 10-1340 10/3/2011cert. denied, U.S. S. Ct. Dkt. No. 10 1340, 10/3/2011

9

WL GW.L. Gore

• Two intangible holding company (IHC) subsidiaries• IHCs received royalties and interest from the operating entity.• Tax Court held that the subsidiaries had sufficient nexus with Maryland,

because the entities were engaged in a unitary business and the IHCs had no existence separate and apart from the operating entity.

• IHCs depend on the operating entity for their existence and enjoyed functional integration and control through stock ownership. They also relied on the operating company’s personnel, office space and corporate services, d i l k f id i idemonstrating a lack of separate corporate identities.

• Court disregarded entities for nexus purposes but treated them as separate non-filers for statute of limitations purposes.

See also Nordstrom/Classics Chicago/SYL.

W.L. Gore & Assoc., Inc. v. Comptroller of the Treasury, Maryland Tax Court, Nos. 07-IN-OO-0084, 07-IN-OO-0085, 07-IN-OO-0086, Nov. 9, 2010 , , , ,

10

L L BL.L. Bean• Test of commercial activity tax (CAT) bright-line nexus standard

― Standard: More than $500,000 in annual taxable gross receipts in Ohio• Taxpayer sells apparel and other customer goods through Internet, telephone

and mail order.No physical presence in Ohio• No physical presence in Ohio

• “The highest court in most, but not all, states that have considered the issue, including Ohio, has found that Quill applies only to sales and use taxes.”

• Also, “The petitioner’s continuous, systematic, and significant solicitation and p y gexploitation of the economic marketplace in Ohio is sufficient [for substantial nexus purposes].”― The taxpayer sends thousands of catalogs to Ohio and engages in other

advertising, including print and television.advertising, including print and television.― Gross receipts from Ohio sales of TPP exceeded $100 million.

In Re: L.L. Bean, 2011 WL 2118350, Ohio Department of Taxation, No. 0000000198, Aug. 10, 2010

11

T l b i h CTelebright Corp.• One employee set up a home office in New Jersey, from which she would One employee set up a home office in New Jersey, from which she would

check in with the Maryland office via email from a personal laptop.• She performed all work from her New Jersey home.• Court held this created minimum presence required to tax the employer.

― Taxpayer regularly and consistently permits the employee to work from her home in New Jersey.

― Corporation is “doing business at the place where its employees are t d t t f k h th l l i i d expected to report for work, where they are regularly receiving and

carrying out their assignments, where those employees are supervised, where they begin and end their work day, and where they deliver to their employer and customers a finished work product.”

• Minimum physical presence case

Telebright Corp. v. Division of Taxation, 25 N.J. Tax 333, NJTC No. 011066-2008 (March 24, 2010)

12

BIS LP IBIS LP, Inc.

• Taxpayer was a foreign corporation that has a 99% limited partnership interest in BISYS Information Solutions LP.

― BIS was an investment company.

― BISYS was a banking information, data processing company.

• BISYS does business in New Jersey.

• Division claimed BIS and BISYS were unitary, and thus BIS was subject Division claimed BIS and BISYS were unitary, and thus BIS was subject to tax in New Jersey

• Court held there was no unitary relationship.

• No nexus in New Jersey• No nexus in New Jersey

BIS LP, Inc. v. Director, Division of Taxation, 25 N.J. Tax 88 (2009), aff’dNo A 172 09T2 2011 WL 3667622 (App Div 2011) No. A-172-09T2, 2011 WL 3667622 (App. Div. 2011)

13

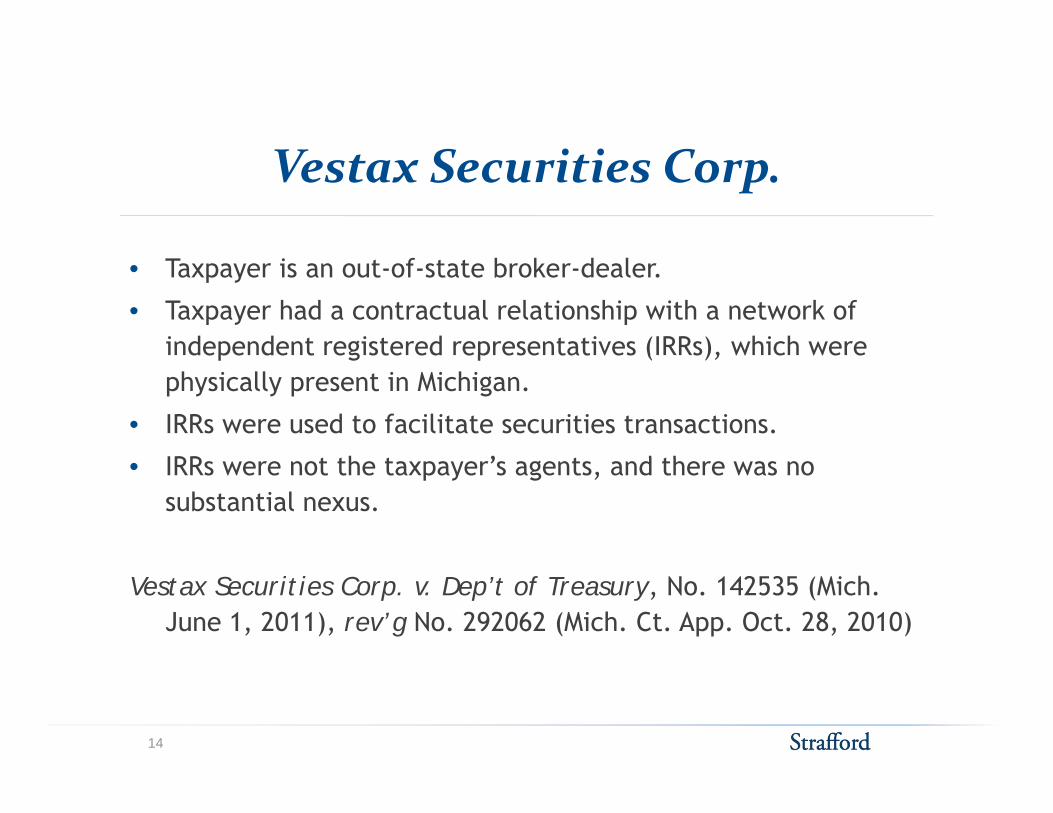

V S i i CVestax Securities Corp.

• Taxpayer is an out-of-state broker-dealer.

• Taxpayer had a contractual relationship with a network of independent registered representatives (IRRs), which were depe de t eg ste ed ep ese tat ves ( s), w c we e physically present in Michigan.

• IRRs were used to facilitate securities transactions.

IRR t th t ’ t d th • IRRs were not the taxpayer’s agents, and there was no substantial nexus.

Vestax Securities Corp. v. Dep’t of Treasury, No. 142535 (Mich. June 1, 2011), rev’g No. 292062 (Mich. Ct. App. Oct. 28, 2010)

14

Whi l lWhirlpool

• New Jersey throw-out rule

• Sales are thrown out if a state lacks “jurisdiction to tax” the corporation.co po at o .

• New Jersey applies economic nexus principles; thus, there was no throw-out of sales made in any other state.

86 272 i• 86-272 issues

Whirlpool Properties, Inc. v. Director, Division of Taxation, 208 NJ p p , , f ,141 (2011).

15

RECENT LEGISLATIVE AND Ellen McCabe, LarsonAllen

RECENT LEGISLATIVE AND REGULATORY DEVELOPMENTS

California Economic Nexus Standard

• Beginning 1/1/11, a taxpayer is considered ”doing business” in California if any of the following conditions are satisfied:

A. Taxpayer is actively engaging in any transaction in California for the purpose of financial or pecuniary gain or profit.

B. It is organized or commercially domiciled in California.

C Its sales in California exceed the lesser of $500 000 or 25% of the C. Its sales in California exceed the lesser of $500,000 or 25% of the taxpayer’s total sales, or

D. Its real property and tangible personal property in California d th l f $50 000 25% f th t ' t t l l exceed the lesser of $50,000 or 25% of the taxpayer's total real

property and tangible personal property.

E. Its California payroll exceeds the lesser of $50,000 or 25% of the total compensation paid by the taxpayer.

17

California Economic Nexus Standard (Cont.)

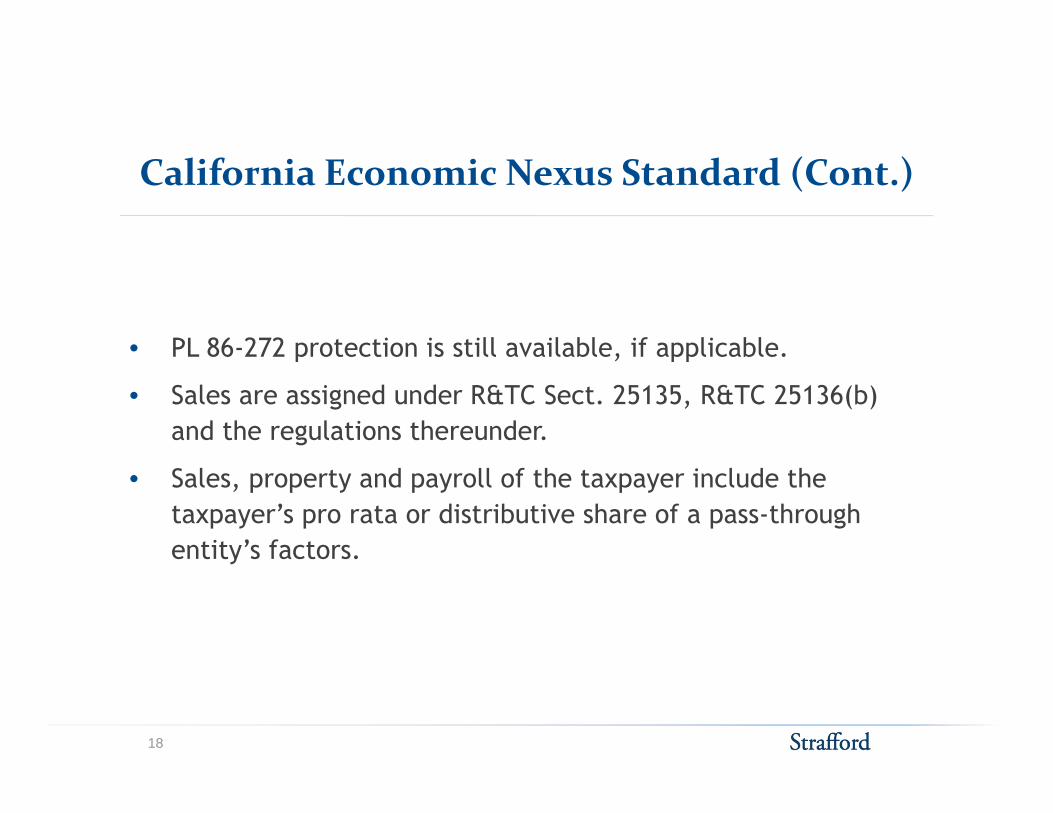

• PL 86-272 protection is still available, if applicable.PL 86 272 protection is still available, if applicable.

• Sales are assigned under R&TC Sect. 25135, R&TC 25136(b) and the regulations thereunder.

• Sales, property and payroll of the taxpayer include the taxpayer’s pro rata or distributive share of a pass-through entity’s factors.y

18

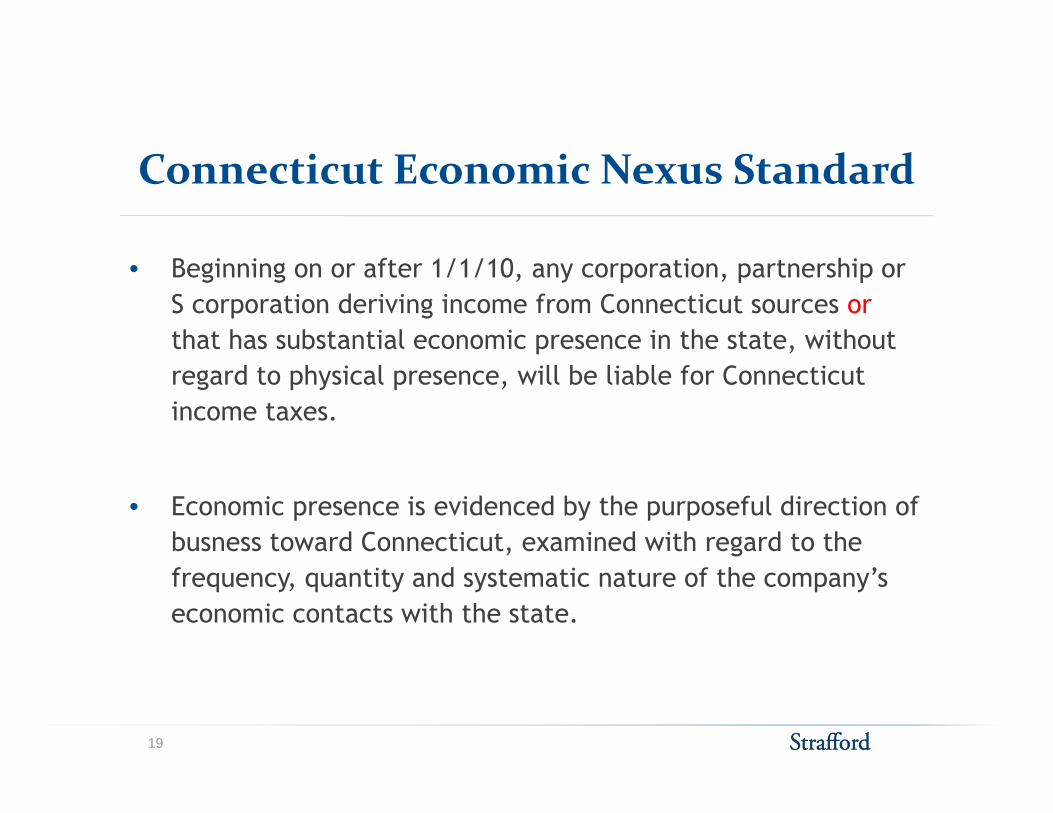

Connecticut Economic Nexus Standard

• Beginning on or after 1/1/10, any corporation, partnership or S corporation deriving income from Connecticut sources orthat has substantial economic presence in the state, without regard to physical presence, will be liable for Connecticut income taxes.

• Economic presence is evidenced by the purposeful direction of busness toward Connecticut, examined with regard to the frequency, quantity and systematic nature of the company’s economic contacts with the state.

19

Connecticut Economic Nexus Standard (Cont.)

A. A bright-line test was established to determine if the frequency, quantity and systematic nature of the contacts result in nexus. Test consists of the following:the following:

1. If receipts from Connecticut sources are less than $500,000, then a company will be deemed to not have nexus with the state.

2 Income arriving from passive investment activity will not create 2. Income arriving from passive investment activity will not create economic nexus.

3. Licensing of intangible property, if the licensor derives receipts in excess of $500,000 under the license agreement with the licensee excess of $500,000 under the license agreement with the licensee corporation, will result in nexus. Transactions with related members (other than licensing activity) will not create nexus.

4. Public Law 86-272 will still provide protection to businesses that p phave economic nexus.

20

Connecticut House Bill 6652:Economic Nexus Revisions

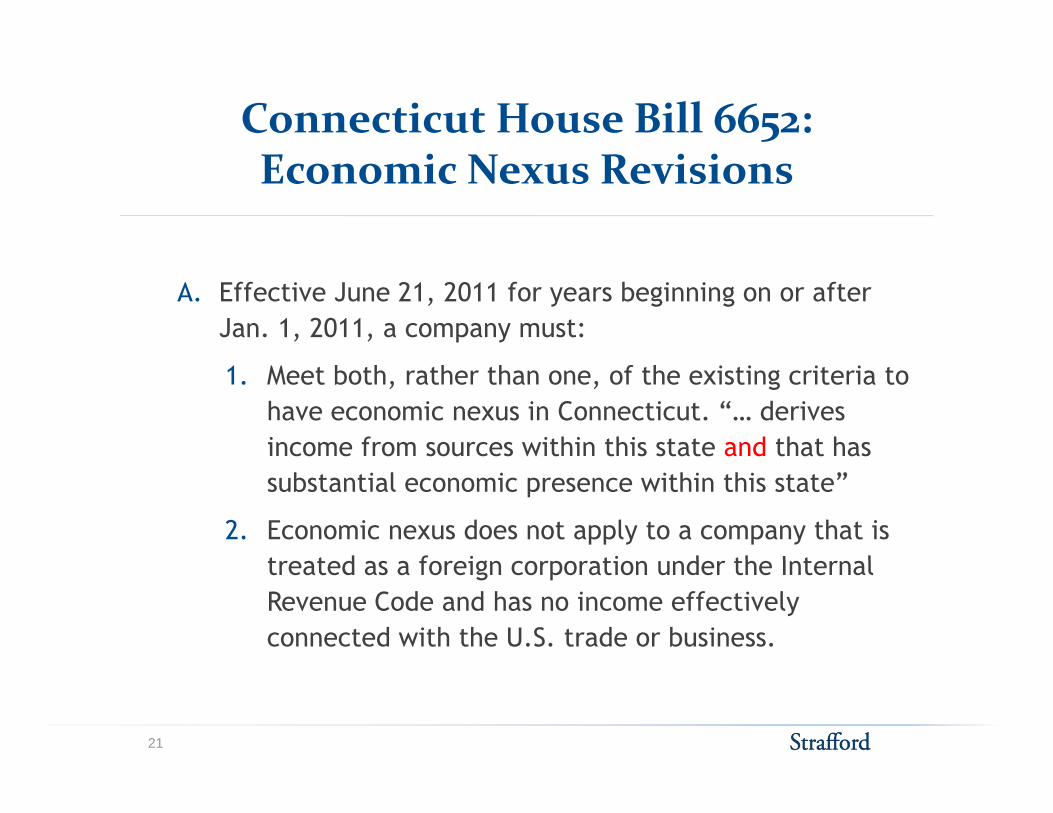

A. Effective June 21, 2011 for years beginning on or after Jan. 1, 2011, a company must:

1. Meet both, rather than one, of the existing criteria to have economic nexus in Connecticut. “… derives income from sources within this state and that has substantial economic presence within this state”

2. Economic nexus does not apply to a company that is t t d f ig ti d th I t l treated as a foreign corporation under the Internal Revenue Code and has no income effectively connected with the U.S. trade or business.

21

Michigan Nexus Guidance:Corporate Income Tax

A Eff ti J 1 2012 Mi hi B i T ill b l d b A. Effective Jan. 1, 2012 Michigan Business Tax will be replaced by a corporate income tax (on C corporations only). The corporate income tax is imposed on taxpayers with business activity within Michigan or that have an ownership interest or beneficial Michigan, or that have an ownership interest or beneficial interest in a flow-through entity that has business activity in Michigan. Public Law 86-272 protection can apply.

1 “B i ti it ” th t f f l g l it bl 1. “Business activity” means the transfer of legal or equitable title to or rental of property, whether real, personal or mixed, tangible or intangible, or the performance of services or a combination thereof made or engaged in or services, or a combination thereof, made or engaged in, or caused to be made or engaged in, whether in intrastate, interstate, or foreign commerce, with the object of gain, benefit, or advantage, whether direct or indirect, to the benefit, or advantage, whether direct or indirect, to the taxpayer or to others.

22

Michigan Nexus Guidance: CorporateIncome Tax – Bright‐Line Test

A Substantial nexus: A taxpayer has substantial nexus in Michigan and is A. Substantial nexus: A taxpayer has substantial nexus in Michigan and is subject to the corporate income tax if it:

1. Has in-state physical presence more than 1 day during the tax year.

2 Actively solicits sales in Michigan (meaning either 1 speech 2. Actively solicits sales in Michigan (meaning either 1. speech, conduct or activity that is purposefully directed at or intended to reach persons within Michigan and that explicitly or implicitly invites an order for a purchase or sale; or 2. speech, conduct or activity purposefully directed at or intended to reach persons within Michigan that neither explicitly nor implicitly invites an order but is entirely ancillary to requests for purchase or sale order)

3 H i t f $350 000 d t Mi hi 3. Has gross receipts of $350,000 or more sourced to Michigan, or

4. Has an ownership or beneficial interest in a flow-through entity (either directly or indirectly through one or more other flow-through entities) that has substantial nexus in Michiganthrough entities) that has substantial nexus in Michigan

23

Business Activity Tax Nexus Bill (BATSA)

A. Creates a physical presence requirement before a state could assert jurisdiction and impose a tax on a business

B. Expands upon PL 86-272 by applying the solicitation exemption B. Expands upon PL 86 272 by applying the solicitation exemption to companies performing services and dealing in intangibles

C. There are a number of nexus “safe harbors,” such as an unlimited amount of employees and property in a state without unlimited amount of employees and property in a state without creating nexus, so long as neither is present in the state for more than 21 days within a particular year.

D Pro ides clarit to companies D. Provides clarity to companies

E. State administrators are opposed. The National Governors Association has estimated that the bill's enactment would lead to

$ $state revenue losses of $4.7 billion to $8 billion annually.

24

New Jersey: Expansion Of NexusOn Foreign Corporations

A N J Admin Code 18:7-1 8: Foreign corporations subject A. N.J. Admin. Code 18:7-1.8: Foreign corporations subject to corporation business tax; expanded in 2011 to impose tax on any corporation that solicits business or derives gross receipts from sources within the stategross receipts from sources within the state

B. Financial business corporations, banking corporations, credit card companies or similar businesses that have their commercial domicile in another state are subject to tax if they solicit business or receive gross receipts from sources within the state.

C. Retroactive application: For privilege periods beginning on or after Jan. 1, 2002

D. See Technical Advisory Memorandum 6, issued 1-10-11

25

RESPONSES FOR CORPORATE Jaye Calhoun, McGlinchey Stafford

TAX DEPARTMENTS TO CONSIDERCONSIDER

N R iNexus Reviews

1. Nexus review – Be proactive - Don’t wait until you receive a nexus survey, a letter from an auditor or a call from a remote state’s tax department asking why you haven’t filed.

2. Not your grandparents’ nexus standard – When can a seller/service provider/business operating over the Internet seller/service provider/business operating over the Internet be subject to a remote state’s business activity taxes or be required to collect the remote state’s use taxes? Are Due Process and Commerce Clause principles still relevant? What Process and Commerce Clause principles still relevant? What about PL 86-272?

3. Don’t let your guard down – Watch for new developments.

27

Due Process Clause(F i C )(Fairness Concerns)

• No state “shall deprive any person of life, liberty or property without due process of law.”

• Requires “some definite link, some minimum connection, between a state and the person property or transaction it between a state and the person, property or transaction it seeks to tax.”

• Quill Corp. v. N.D. (1992): Due process embodies “traditional notions of fair play and substantial justice.”

28

Commerce Clause(S t i C )(Systemic Concerns)

The Constitution was intended to address the problems that arose under the • The Constitution was intended to address the problems that arose under the Articles of Confederation (1778) whereby each state was essentially a sovereign nation under the Treaty of Paris (1783).

― Particularly the propensity of the states to erect protectionist trade barriersy p p y p

― Created a national free-trade zone

• The Constitution gives Congress the power to “regulate Commerce … among the several States.” Article 1, Section 8, Clause 3

• Taxation is regulation.• Complete Auto (1977): State taxes sustained if:

― Applied to activity with substantial nexusFairly apportioned― Fairly apportioned

― Do not discriminate against interstate commerce― Fairly related to services provided by the state

• Quill (1992): Requires at least some physical presence

29

Wh A S d d ?What Are Standards?• Public Law 86-272Public Law 86 272

― Brown-Forman Distillers Corp. v. Collector of Revenue(La. 1958, denied cert. 1959)― “Missionary men” who assisted with displays

Northwestern States Portland Cement Co v Minnesota (1959) ― Northwestern States Portland Cement Co. v. Minnesota (1959) ― Solicited orders, accepted outside state, leased office space in-state

― Business lobbied Congress, arguing administrative burden was undue for insignificant level of activity. Congress reacted quickly, passing a law intended as a stop-gap measure and providing for a study known as the Willis Reportas a stop-gap measure and providing for a study known as the Willis Report.

― Willis Report recommended quantitative rule, based on volume

• Complete Auto (1977): State taxes sustained if:― Applied to activity with substantial nexus― Fairly apportioned― Do not discriminate against interstate commerce― Fairly related to services provided by the statey p y

30

Quill Corp. v. North Dakota, U S 8 ( )504 U.S. 298 (1992)

― Commerce Clause requires a physical presence in the state before a state may impose a use-tax collection responsibility.

No such physical presence requirement applies for Due ― No such physical presence requirement applies, for Due Process purposes

― Principles applicable to taxes other than use tax?

31

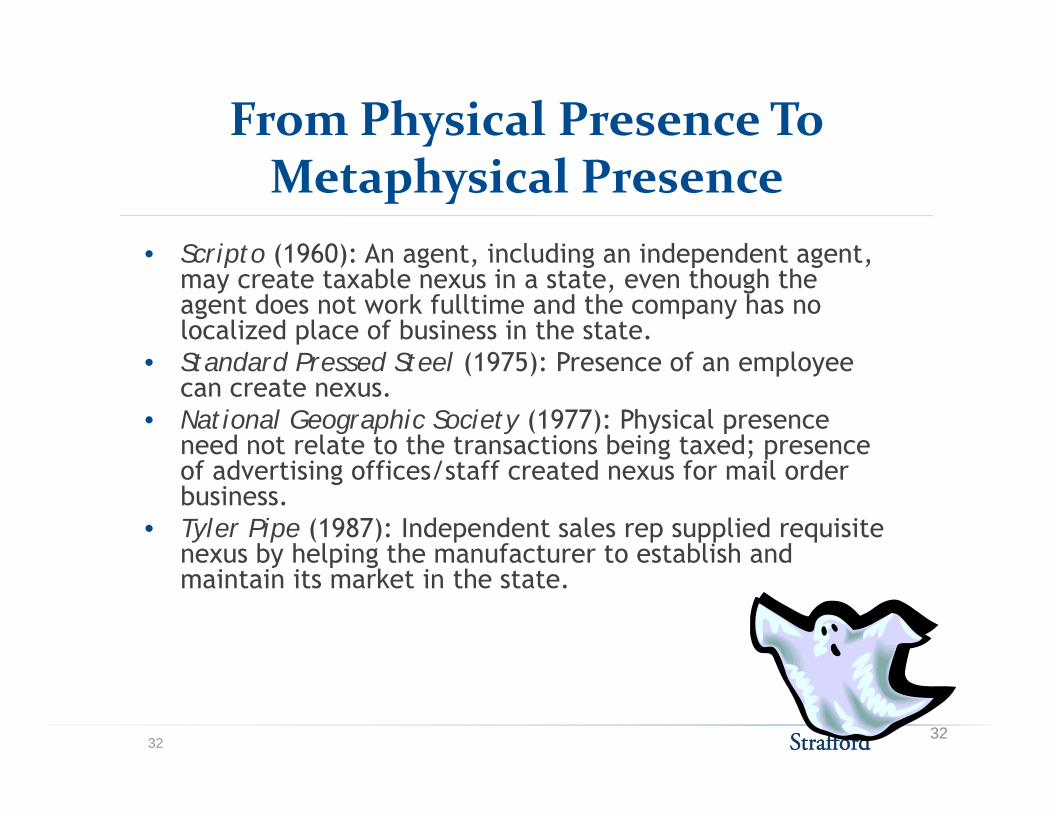

From Physical Presence ToMetaphysical Presence

• Scripto (1960): An agent including an independent agent • Scripto (1960): An agent, including an independent agent, may create taxable nexus in a state, even though the agent does not work fulltime and the company has no localized place of business in the state. St d d P d St l (1975) P f l • Standard Pressed Steel (1975): Presence of an employee can create nexus.

• National Geographic Society (1977): Physical presence need not relate to the transactions being taxed; presence g ; pof advertising offices/staff created nexus for mail order business.

• Tyler Pipe (1987): Independent sales rep supplied requisite nexus by helping the manufacturer to establish and nexus by helping the manufacturer to establish and maintain its market in the state.

3232

Royalty CompaniesRoyalty Companies• Geoffrey, Inc. v. South Carolina Tax Comm, 437 S.E. 2d 13 (S.C. 1993),

cert. denied, 510 U.S. 992 (1993)

― The licensing of a trade name or trademark creates sufficient nexus between an out-of-state licenser and the state to meet both the “minimum connection” standard required by the Due Process Clause and the “substantial nexus” requirement of the Commerce Clause.

• Lanco, Inc. v. Director, Division of Taxation

― Corporation business tax applied to income derived by an out-of-state intangible holding company from licensing fees attributable to New Jersey.

― Follows Geoffrey rationale

― Quill does not apply to income taxes.Quill does not apply to income taxes.

― U.S. Sup. Ct. Denied Cert. on June 18, 2007.

33

Credit Card And Financial Institutions

J C P N ti l B k J h A l N M1998 00497 COA R3• J. C. Penney National Bank v. Johnson, Appeal No. M1998-00497-COA-R3-CV (Tenn. Ct. App. Dec. 17, 1999), appeal denied, Tenn. Sup. Ct. (May 8, 2000)

― Tax did not violate the "minimum contacts" standard of the Due ― Tax did not violate the minimum contacts standard of the Due Process Clause.

― National Bellas Hess and Quill should apply.

• Tax Comm'r of W. Va. v. MBNA Am. Bank

― Out-of-state credit card bank has substantial nexus with West Virginia even though it does not have a physical presence in the stateeven though it does not have a physical presence in the state.

― Court adopts economic nexus standard.

― Quill does not apply to income taxes.

U S Supreme Court Denied Cert on June 18 2007― U.S. Supreme Court Denied Cert. on June 18, 2007.

34

Credit Card And Financial Institutions (Cont.)

• MBNA America Bank, N.A. & Affiliates v. Indiana Dept. of Rev. (2008)

― Economic presence was sufficient to establish substantial nexus f t f t t dit d b k Q ill d t t d b d for an out-of-state credit card bank. Quill does not extend beyond sales and use taxes.

― U.S. Supreme Court – cert. denied

• Capital One Bank v. Commissioner of Revenue (MA 2009)

― Out-of-state intangible holding company/credit card bank have substantial nexus with MA, based on economic presence.

― U.S. Supreme Court – cert. denied

35

Economic Presence Nexus Standards:Factor Presence Standard

A t f t t t d i b i i t t ill h • An out-of-state taxpayer doing business in a state will have substantial nexus with the state and be subject to the state’s franchise and income tax if any of the following thresholds are exceeded in the state during the tax period:

― $50,000 or 25% of the total property

― $50,000 or 25% of the total payroll$50,000 or 25% of the total payroll

― $500,000 or 25% of the total sales

• Ohio (as part of the CAT) and California (effective Jan. 1, 2011) have adopted a “factor presence nexus standard.”

36

What Are Limitations OfE i P N ?Economic Presence Nexus?

Sell in home state to a customer in Ohio or Michigan Customer comes into store to buy product and returns to home state Customer comes into store to buy product, and store arranges delivery to

customer in neighboring state Customer calls and orders product

• Advertising― Local newspaper with Internet site― National newspaperNational newspaper― Send flyers into a specific state― Send flyers in a nationwide mailing― Radio advertisement

Ad ti l l t l i i t ti― Advertise on a local television station― Nationwide television ad ― Does the type of advertising matter? Goodwill vs. product solicitation

• If you have advertising nexus, must the company refuse to sell to customers from economic presence states to avoid filing responsibility?

37

What Are Limitations Of EconomicP N ? (C )Presence Nexus? (Cont.)

• Call center in home state engages in nationwide solicitation

• 86-272 protected solicitation?

• Web page invites customers to sellers location in neighboring state

• Web page invites customers to call to place order

• Web page allows for online orders

• Web page provides access to database for a fee• Web page provides access to database for a fee

― Does it matter if you know location of customer?

― Mail out product vs. downloaded product paid via PayPal

l l l h d l dd l h h• E-mail sales solicitation to purchased e-mail address list, on which addresses are not state-specific

• Do Internet sellers have to screen customers for home state location d i h h ll h id fili ibili ?to determine whether to sell to them, to avoid filing responsibility?

38

Are There Limits To Economic Nexus?

• New Jersey economic nexus case• Quark, Inc. v. Director, Div. of Taxation, N.J. Tax Court Docket

No. 005744-2003 (Aug. 13, 2009) • New Jersey’s Taxation Department assessed its corporate • New Jersey s Taxation Department assessed its corporate

income tax on two software companies, citing Lanco (188 N.J. 380) as its authority.

• Both software companies had very modest sales in the state ( d th MTC’ $500 000 l th h ld)(under the MTC’s $500,000 sales threshold).

• N.J. Tax Court rejected the Taxation Department’s argument, finding this case is different than Lanco (intangible property vs. tangible copyrighted property).g py g p p y)

• No affiliation with an entity that had a physical presence in New Jersey; this was an operating entity, not a holding company created to generate a tax benefit.

39

P di IPending Issues

• How do the states react to the denial of certiorari by the Supreme Court in nexus cases?

• Will states become more creative in expanding what constitutes substantial nexus?

• Will states expand use of economic nexus to foreign commerce?

40

V l Di l AVoluntary Disclosure Agreements

Offers:

1. Limitation of exposure – Some states will agree to limit exposure to current and future years, and some may agree to limit prior year exposure to several years. There is generally no statute of limitations for non-filed returns.

2. Penalty (and sometimes full or partial interest) waiver – Penalty waiver is typical, but interest may also be eliminated or reduced.

3. Increased opportunity to manage audit activity – Returns may or may not be audited when filed. But, a voluntarily filed return is akin to a self-audit, and taxpayers generally do better on self-audit.

4. May also avoid possibility of prosecution

41

Voluntary Disclosure Agreements (Cont.)

Requirements:

1. No previous contact by state – Voluntary disclosure proposals are not considered voluntary if the state already has the are not considered voluntary if the state already has the taxpayer on its radar. Have returns ready to go in order to maintain the option when it is likely that the state will discover the non-filing businessdiscover the non filing business.

2. Made anonymously – Requires using a third-party professional (attorney/accountant) to approach the state

3. If accepted – The taxpayer must usually file the returns, pay the tax and any interest within a brief period of time from acceptance.

42

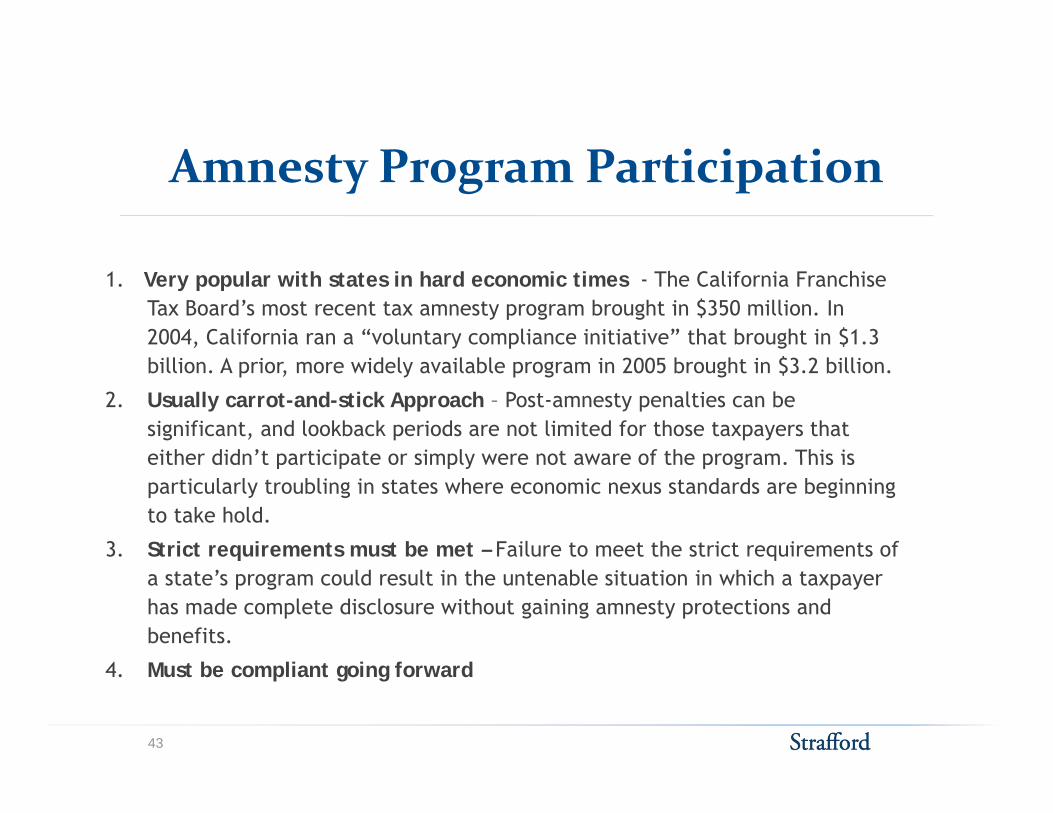

A P P i i iAmnesty Program Participation

1. Very popular with states in hard economic times - The California Franchise Tax Board’s most recent tax amnesty program brought in $350 million. In 2004, California ran a “voluntary compliance initiative” that brought in $1.3 billion. A prior, more widely available program in 2005 brought in $3.2 billion.

2. Usually carrot-and-stick Approach – Post-amnesty penalties can be significant, and lookback periods are not limited for those taxpayers that either didn’t participate or simply were not aware of the program This is either didn t participate or simply were not aware of the program. This is particularly troubling in states where economic nexus standards are beginning to take hold.

3. Strict requirements must be met – Failure to meet the strict requirements of q qa state’s program could result in the untenable situation in which a taxpayer has made complete disclosure without gaining amnesty protections and benefits.

4 M t b li t i f d4. Must be compliant going forward

43

A i S i /IApportionment Strategies/Issues

1. Single-sales-factor states – Economic nexus theories combined with single-sales-factor states create issues for non-residents.

2. Consider seeking the right to apportion within states in which the business already has a physical presencewhich the business already has a physical presence

3. Sales of services and intangibles – Market-sourcing states create opportunities/problems.

4. Property and payroll

44

DEVELOPMENTS ON THE Mike Shaikh, Reed Smith

DEVELOPMENTS ON THE HORIZON

D l O Th H iDevelopments On The Horizon• U S Business Activity Tax Simplification Act (BATSA) HR 1439• U.S. Business Activity Tax Simplification Act (BATSA), HR 1439

• Physical presence standard for all business activity taxes

• Applies P.L. 86-272 to all sellers, including sellers of intangible property

• Includes more qualitative de minimis activities beyond solicitation

• Defines physical presence (14-day rule)

• Recent developments

• House Judiciary Committee approved legislation on July 7, 2011.

• Now on House of Representatives floor

• Similar legislation is expected in the Senate.

46