news european views - citibankicg.citi.com/transactionservices/home/sa/2009/investorservices... ·...

TRANSCRIPT

first edition 2008

news & viewsNews from:

Across Europe

Italy allows domestic pensionfunds to appoint an EU bank asa depositary bank

Sophisticated UCITS and leverage assessment: are regulatory approaches converging?

Germany

Ireland

Jersey

Luxembourg

United Kingdom

•

•

european

EuropeanStefano PierantozziEuropean Head of Fiduciary Oversight & Research [email protected]: +352 451 414 370

Valeria CarusoProduct ManagerGlobal Transaction Services [email protected] Tel: +39 02 8647 4081

Teresa ExtanceEuropean Fiduciary Risk [email protected]: +44 (0) 20 7500 9957

European News & Views

Contributors

GermanyMarco SperlichFiduciary Oversight & [email protected]: +49 69 1366 1179

IrelandShane BailyHead of Fiduciary Services, [email protected]: +353 1 622 6297

JerseyAnn-Marie RoddieFiduciary [email protected]: +44 (0) 1534 608 201

Simon PascoePartnerBedell [email protected]: +44 (0) 1534 814 856

LuxembourgPatrick WateletHead of Fiduciary Services, [email protected]: +352 451 414 231

Laurent DenayerSenior ManagerErnst & Young Business and Advisory [email protected]: +352 42 124 8372

United KingdomTony WrightHead of Fiduciary Oversight & Research, [email protected]: +44 (0) 20 7500 1598

Michaela WalkerPartnerEversheds LLP

Amanda HaleAssociateFinancial Services Authority

Since contributing her article, Amanda Hale has joined Citi, working with European Fiduciary Services.

European News & Views — First Edition 2008

Introduction

By Sean Quinn .................................................................................................................................................................. 1

Across Europe

Italy allows domestic pension funds to appoint an EU bank as a depositary bank .............................2

Sophisticated UCITS and leverage assessment: are regulatory approaches converging? ...............4

Germany

Amendments to the German Investment Act .....................................................................................................7

Ireland

Physical short selling under UCITS: time to reconsider? ............................................................................. 10

Jersey

Recent developments in Jersey funds .................................................................................................................13

Luxembourg

Fair valuation in the UCITS risk-management world ..................................................................................... 15

United Kingdom

Protected cell investment companies: UK developments ............................................................................ 16

Stock lending: developments following FSA CP 06/18 ................................................................................20

Glossary ......................................................................................................................................................................... 22

European News & Views

Contents

European News & Views — First Edition 2008

European News & Views — First Edition 2008

Welcome to 2008 and to our fi rst edition of European News & Views this year. In 2007, from the funds-industry perspective, we followed a number of signifi cant and interesting developments across Europe, some of which were proposed in 2007, such as short selling in Undertaking for Collective Investments in Transferable Securities (UCITS) funds in Ireland, and others that we were — and still are — eager to follow the evolution of in 2008, such as the European Commission’s developments on the possible adjustments to the UCITS Directive (85/611/EEC).

European News & Views — First Edition 2008 1

Sean QuinnEMEA Head of Fiduciary Services

Introduction

We would like to share with you a number of these developments across Europe, in addition to which we are delighted to be able to include an article on the recent developments in Jersey funds, for which we thank Simon Pascoe of Bedell Group.

In Germany, key developments came into force in January 2008, relating to the amendments to the original modernisation of the Germany Investment Act in January 2004, which the German parliament passed in November 2007. These amendments aim to strengthen the fund market in Germany and possibly stimulate the development of investments there.

In the United Kingdom, we thank Michaela Walker at Eversheds LLP for an update to the FSA's COLL sourcebook, contained in COLL 5.4, relating to stock lending, following the FSA Consultation Paper 06/18 of October 2006.

We also thank Amanda Hale for an interesting article written in a personal capacity while at the FSA, on “Protected Cell Investment Companies: UK Developments”, topical in the UK after Her Majesty’s Treasury's consultation on outline proposals to develop a protected cell regime for UK OEICs.

For Ireland, we summarise recent developments on short selling on UCITS funds.

In Luxembourg, we thank Laurent Denayer of Ernst & Young’s Business and

Advisory Services for contributing the article, “Fair Valuation in the UCITS Risk-Management World”.

We continue to follow up on developments relating to the risk-management process for UCITS, comparing the regulatory approaches adopted in different countries in our article entitled “Sophisticated UCITS and Leverage Assessment: Are Regulatory Approaches Converging?”

Finally, our article entitled “Italy Allows Domestic Pension Funds to Appoint an EU Bank as a Depositary Bank” provides a brief insight into the European Directive 2003/41/EC (otherwise known as the “Pension Funds Directive”) and the recent adoption, in 2007, of article 19.2 of the Pension Funds Directive by the Italian legislature, permitting institutions for occupational retirement provisions to appoint depositary banks established in another Member State.

This edition of European News & Views also features some stylistic improvements, one of which includes a short glossary of abbreviations and acronyms that are commonly referred to in this edition, but not necessarily defi ned, in the articles. We hope you will fi nd this useful and the articles interesting.

We welcome and look forward to your invaluable feedback in 2008.

European News & Views

Across Europe

2 European News & Views — First Edition 2008

Italy allows domestic pension funds to appoint an EU bank as a depositary bank

European Directive 2003/41/EC of 3 June 2003 (referenced in the UK as the “Occupational Pensions Directive” and in the rest of Europe as the “Pension Funds Directive”), disciplining the activities and the supervision of institutions for occupational retirement provisions, has fi nally been transposed into Italian law with the Law Decree n. 28 of 2007 (the 2007 Decree). The Italian legislature has adopted article 19(2) of the Pension Funds Directive in its entirety. This allows institutions for occupational retirement provisions to appoint depositary banks established in another Member State.

The Pension Funds Directive was subject to a long debate before becoming European law. The issuance of the Pension Funds Directive was particularly arduous because matters related to occupational pension schemes or pension funds have been traditionally the preserve of each EU Member State. Under the EU Treaty, decisions related to the structure of pension arrangements have been classifi ed as a matter for Member States.

The Pension Funds Directive was designed around two key principles of the prudent person and of transparency, with the aim of providing economic effi ciency and security. It is not introducing any change to national state pension schemes, nor is it forcing Member States to introduce specifi c types of pension arrangements. Rather, it aims to introduce a certain degree of harmonisation on the retirement provisions not belonging to the fi rst pillar of the EU.

Among other things, the Pension Funds Directive aims to:

Increase security for pension schemes’ members and benefi ciaries;

•

Create a common approach to registration or authorisation of institutions approved for the purpose of occupational pension provisions;

Facilitate rules to discipline investments in the assets of the pension schemes and to require suffi cient assets to cover the liabilities; and

Introduce the possibility for institutions to operate on a cross-border basis.

The last point in particular has been fully transposed into Italian law with the 2007 Decree. It represents an interesting step forward in the discipline of passporting rights in Italy, and has immediately raised a number of comments.

The 2007 DecreeIn conjunction with the recent reform of Italian pensions, which in the fi rst six months of 2007 has obliged private-sector employees to adhere to complementary pension schemes, it appears that the Italian legislature has also decided to take a more innovative approach than in the past in the regulation of cross-border service provision.

In this article, we would like to examine the wording of article 3 of the 2007 Decree, which amends the previous legislation stating that Italian pension funds are now allowed to appoint as a depositary bank not only an Italian bank or an Italian branch of a European bank, but even a “bank established in another Member State”, provided that it has been “duly authorised according to Directive 93/22/CEE or Directive 2000/12/CE, or it is acting as a depositary bank on the application of Directive 85/611/CEE”.

•

•

•

The wording of article 3 of the 2007 Decree is an extremely signifi cant step forward compared to the rules applicable to investment funds and UCITS in particular. The Bank of Italy Regulations issued on April 2005 (implementing the UCITS III Directives and disciplining all collective investment funds with the exception of pension funds) are less fl exible in this respect.

Historically, Italian regulators considered the depositary bank function as the most important for the protection of the investors’ interests. Under Italian rules relating to depositary banks, the focus of regulation was essentially on the fi duciary or trustee and reporting activities.

The Italian fi nancial

sector was surprised by

the provisions of the

2007 Decree and its

possible impact.

However, foreign players have often seen the existing rules as a source of major concern for the establishment of depositary-bank services in Italy. Similarly, the fact that most asset-management companies belong to Italian banking groups and that most of the fund business is primarily captive have historically limited the appetite of foreign banking groups in providing depositary activities in the local market.

The Italian fi nancial sector was surprised by the provisions of the 2007 Decree and its possible impact. As of now, however, we are not aware of any existing or new pension funds having chosen to appoint a non-Italian depositary bank.

The Italian Banking Association (ABI) is drafting (with the cooperation of a restricted members’ working group) best-practice guidelines that are usually applied and complied by not just Italian banks, but also by foreign banks operating in Italy. It will be interesting to see how these guidelines will seek to limit or regulate, in any way, the extent of the 2007 Decree provisions.

Under all circumstances, the provisions of the 2007 Decree will require further analysis and clarifi cation. The areas we anticipate most of the debate will focus on are the following:

(i) Under Italian law, depositary banksof UCITS have been (since 2005) authorised to calculate the NAV. The 2007 Decree (and so the Pension Funds Directive itself) does not mention this possibility for pension funds.

(ii) The fl exibility introduced under the 2007 Decree brings a degree of disparity between pension funds and UCITS funds investors. This may not only lead to different investor protection regimes being applied (depending upon the country of establishment of the depositary bank), but it may also lead to a disparity in terms of cost structures as it is likely that competition between Italian and foreign depositary banks will result in lower costs being applied to pension funds.

Final considerationsThe establishment of a real passport for fi nancial products and services has become one of the main items in the agenda of the European Commission (EC), and this is starting to have its impact on Member States. The increased fl exibility in the appointment of a depositary, which the 2007 Decree has introduced, is only an initial step in the right direction.

While we wait for increased passporting rights to be extended to UCITS depositaries, we consider that the EC may be interested in looking into establishing rules allowing stricter segregation between banking groups and their own asset-management arms — as far as depositary services are concerned.

Reshaping the European investment fund industry to allow more competition on a cross-border basis may allow the emergence of EU centres of excellence for the provision of support services. The challenge is how to ensure that the benefi ts of such changes are evenly distributed among all EU investors.

European News & Views — First Edition 2008 3

Across Europe

4 European News & Views — First Edition 2008

Across Europe

In the March 2007 edition of European News and Views, we referenced the key features of an RMP for UCITS that hold FDIs. While the obligation to have a robust RMP has been consistently implemented in all the EU jurisdictions, can we be sure that the features of the RMP are always the same?

In the last few months, we have seen an increase in the number of UCITS that have decided to convert to the status of “sophisticated”. Often this decision is driven by the promoter and/or manager’s interest in using more advanced investment techniques; however, as of now there is still little guidance as to what a sophisticated UCITS is — and how to recognise one when you see it.

Sophisticated or not?The distinction between “sophisticated” and “non-sophisticated” UCITS was introduced by the EC Recommendation of 27 April 2004, 2004/383 on the use of fi nancial derivative instruments for UCITS.1

The introduction of two separate categories of UCITS is dictated by the need to ensure that those UCITS

adopting more advanced investment techniques also adopt more advanced risk-management techniques.

The EC Recommendation therefore suggests that sophisticated UCITS should use advanced risk-management techniques to measure market risk (in particular, the use of VaR is recommended), while non-sophisticated UCITS should use the commitment approach.

The EC Recommendation does not provide detailed guidance to help assess the degree of sophistication of a UCITS. Although it does make reference to the fact that non-sophisticated UCITS are those “which have overall less and simpler derivative positions”, it does not provide for a formal defi nition of sophisticated UCITS, which may be interpreted as defi ned by exclusion.

It should be noted, however, that the EC Recommendation considers that the adoption of the commitment approach by a UCITS should be done by taking into account:

1. The nature of the FDIs used;

2. The aim to be achieved by the use of FDIs;

3. The number of FDIs used;

4. The frequency of the FDI contractsentered; and

5. The management techniques adopted.

Therefore the assessment of a UCITS’ degree of sophistication should be made on the basis of these fi ve criteria.

The EC Recommendation also recommends Member States’ competent authorities to undertake further work and thus develop a “convergent Community-wide approach” for defi ning criteria to identify sophisticated and non-sophisticated UCITS. However, as of now no organised work has been carried out to ensure the desired convergence of regulatory approaches.

Figure 1 below provides a snapshot of the approaches taken by the regulators in some countries, comparing them to the EC’s initial defi nition.

Sophisticated UCITS and leverage assessment: are regulatory approaches converging?

Source Sophisticated Non-sophisticated

EC Defi ned by exclusion.UCITS that have overall less and simpler derivative positions.

FSA (UK) Refers to the EC defi nition. Refers to the EC defi nition.

Financial Regulator (Ireland)

Defi ned by exclusion.Uses only a limited number of simple derivative instruments for non-complex hedging or investment strategies.

CSSF (Luxembourg)A UCITS making signifi cant recourse to FDIs and/or making use of more complex instruments or strategies.

A UCITS having less important or less complex positions in FDIs for hedging purposes only.

BaFin (Germany)Defi ned by exclusion (however, it is the default classifi cation).

A UCITS investing in an exhaustive list of basic derivative instruments, or combinations thereof, and mainly for hedging purposes.

Figure 1

Depending upon

its classifi cation as

sophisticated or non-

sophisticated, a UCITS

may adopt different

methodologies for

calculating market-risk

exposure.

There is no consistent or clear-cut defi nition of what a sophisticated or non-sophisticated UCITS is. The burden is on the promoter and/or manager to ensure that it considers adequately the characteristics of the UCITS and that the rationale for the decision taken is properly motivated and documented.

Leverage assessment and VaRIn line with the EC Recommendation, a UCITS’ market-risk exposure relating to FDIs may not exceed 100 per cent of the UCITS’ NAV. Therefore a UCITS’ overall market-risk exposure cannot exceed 200 per cent of its NAV on a permanent basis.

This limit can be temporarily increased, taking into account that a UCITS may occasionally borrow up to 10 per cent

of its NAV; hence, a UCITS’ overall maximum market-risk exposure is capped to 210 per cent of the NAV, on a temporary basis.

Depending upon its classifi cation as sophisticated or non-sophisticated, a UCITS may adopt different methodologies for calculating market-risk exposure.

A non-sophisticated UCITS may adopt the commitment approach, whereby fi nancial derivative positions are converted into equivalent positions in the underlying assets. Sophisticated UCITS are instead required to adopt a VaR methodology. For the commitment approach, the calculation of market-risk exposure is relatively straightforward, so that the 200 per cent (or 210 per cent if applicable) limit can be effectively calculated.

The same cannot be said for the VaR methodology. VaR values depend upon a number of factors such as:

The probability distribution chosen to approximate the UCITS’ portfolio’s expected returns;

The period of observation; and

The confi dence level.

•

•

•

The EC Recommendation has provided some guidelines in terms of the parameters for application of the VaR approach, namely:

A 99 per cent confi dence interval;

A holding period of one month; and

“Recent” volatilities, i.e. no more than one year from the calculation date.

However, the EC Recommendation has not provided criteria for defi ning which VaR values correspond to a 200 per cent market-risk exposure as calculated under the commitment approach, recommending EU Member States’ regulators to “take into account that the methods for assessing the leverage of UCITS need further refi nement, in particular with respect to a maximum VaR/stress-test value corresponding to a total exposure of 200 per cent of a UCITS’ NAV”.

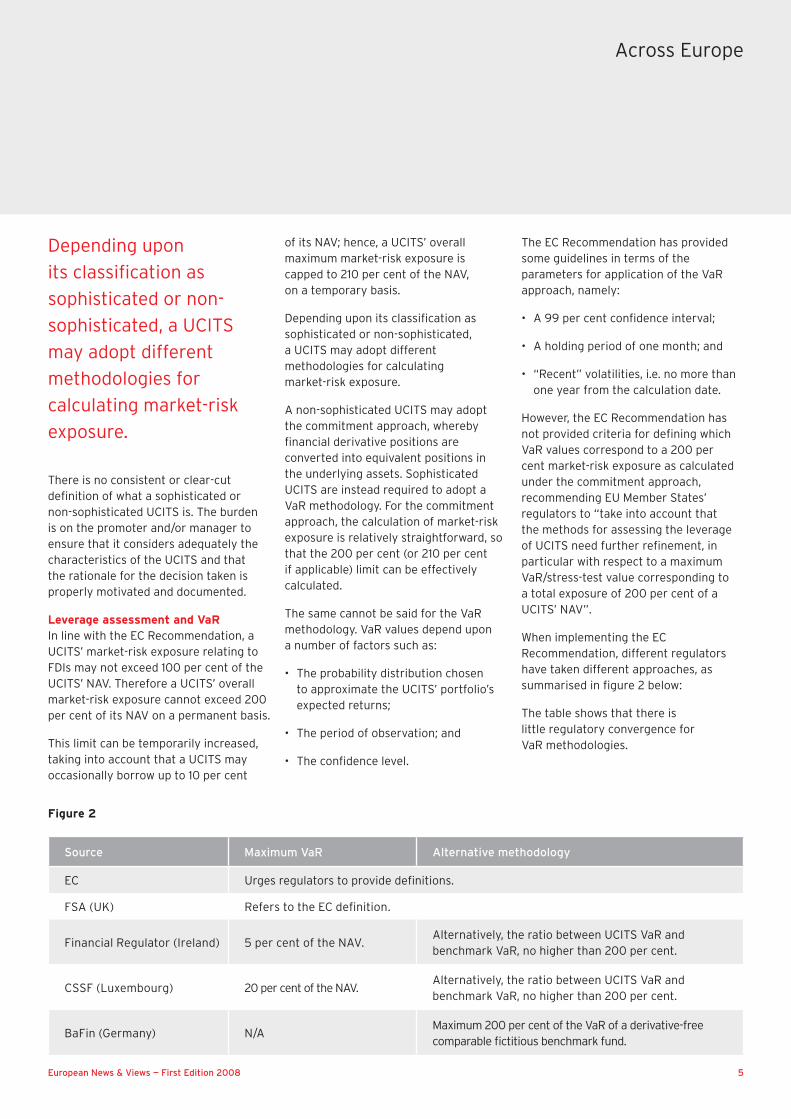

When implementing the EC Recommendation, different regulators have taken different approaches, as summarised in fi gure 2 below:

The table shows that there is little regulatory convergence for VaR methodologies.

•

•

•

Source Maximum VaR Alternative methodology

EC Urges regulators to provide defi nitions.

FSA (UK) Refers to the EC defi nition.

Financial Regulator (Ireland) 5 per cent of the NAV.Alternatively, the ratio between UCITS VaR and benchmark VaR, no higher than 200 per cent.

CSSF (Luxembourg) 20 per cent of the NAV.Alternatively, the ratio between UCITS VaR and benchmark VaR, no higher than 200 per cent.

BaFin (Germany) N/AMaximum 200 per cent of the VaR of a derivative-free comparable fi ctitious benchmark fund.

Figure 2

European News & Views — First Edition 2008 5

Across Europe

Across Europe

6 European News & Views — First Edition 2008

The Irish and Luxembourg regulators, in particular, have taken two different approaches to VaR (in Luxembourg the maximum limit is 300 per cent higher than in Ireland), but both countries introduced a “relative VaR” for those UCITS that aim to replicate a benchmark or for which a benchmark can be identifi ed.

Similarly, Germany has opted for the defi nition of a relative VaR, but has not, as of December 2007, set absolute VaR levels.

The “relative VaR” approach is a practical one; however, the following queries are open:

How is the 200 per cent limit for the relative VaR mathematically calculated to assess the 200 per cent limit for market risk under the commitment approach?

Should the benchmark of reference contain any derivative element or not? Interestingly the German regulators have considered this point in their provisions; but if the benchmark is a hedge-funds index, should some kind of transparency be applied?

Limits defi ned for absolute VaR are less consistent than those defi ned for relative VaR.

By way of example, while noting that both in Luxembourg and in Ireland the EC Recommendation parameters have been consistently implemented, a Luxembourg-regulated sophisticated UCITS is allowed on a statistical basis to risk, in 1 per cent of cases, losing up to 20 per cent of its assets within a month; while for an Irish-regulated UCITS, the limit is set to 5 per cent.

One could also rightfully argue that if the UCITS framework is built around the assumption that a UCITS’ maximum potential loss should be equal to its NAV, even higher levels (up to 100 per cent)

•

•

of VaR should be allowed, so it should not come as a surprise to see that regulatory approaches are not completely consistent.

For the UCITS framework

to demonstrate a

consistent application of

standard risk-spreading

rules, a more consistent

approach at country level

will be a key factor.

ConclusionsOver the last few years, the regulators, the industry and the EC have made considerable effort to achieve higher consistency in the UCITS framework. This was demonstrated, for instance, with the process for clarifying criteria for determining the eligibility of certain assets for UCITS investment, carried out by CESR.

However, for the UCITS framework to demonstrate a consistent application of standard risk-spreading rules, a more consistent approach at country level will be a key factor. As of now, there is little evidence of how market risk calculated under the commitment approach and market risk calculated under the VaR approach relate to each other. Time may help in defi ning the most meaningful VaR parameters and limits.

Notes1 Commission Recommendation COM 2004/383/EC (the EC Recommendation).

Germany

Amendments to the German Investment Act

Following the modernisation of the German Investment Act (InvG), which came into force in January 2004, the German parliament passed the German Investment Act Amendment Act (InvÄndG) on 8 November 2007. The aim of the InvÄndG is to further strengthen the German fund market and stimulate the development of investments in Germany. In this context, it also implements the UCITS Directives 85/611/EWG and 2007/16/EWG, subject to the harmonisation of the EU investment market.

As the InvÄndG came into force on 1 January 2008, we would like to take this opportunity to highlight the major changes for the German fund market.

Investment-management companiesAbolishment as a credit institutionFrom now, German investment-management companies (KAGs) are not defi ned as credit institutions anymore, but are regarded as an institution of “sui generis” based on the one-to-one implementation of the UCITS Directives.

As a result of this conversion, it is expected that KAGs will become more competitive as numerous provisions of the German Banking Act (KWG) no longer apply. For example, KAGs do not have to meet the capital requirements of the KWG anymore. Instead of the minimum initial capital requirements of EUR730 thousand (or EUR2.5 million for Real Estate Investment Companies), only EUR300 thousand will now be required. However, additional capital is required if the value of the managed fund assets exceeds EUR1.125 billion (formerly EUR3 billion). Furthermore, a KAG is no longer under the German Federal Bank’s (Bundesbank) supervision; it, however, remains under supervision of the German Federal Financial Supervisory Authority (BaFin).

The requirements of the German Banking Act, in particular regarding to licensure, cancellation or expiration of permission, organisational requirements, year-end audits and insolvency proceedings, are now (nearly “one-to-one”) refl ected in the InvÄndG.

Corporate governanceThe InvÄndG states that at least one member of the KAG supervisory board has to be a representative (professional) independent from the KAG shareholders, from the KAG’s affi liates and from the business partners of the KAG. This, however, does apply to KAGs that are exclusively managing special funds or special investment stock corporations.

The authority to appoint a custodian remains with the KAG. Custodians, KAGs and investment stock corporations are obliged to take all necessary organisational steps to ensure that no confl icts of interest arise, including the setting-up of confi dential areas by establishing “Chinese Walls”.

ReportingA key element of deregulation is the cancellation of the regulatory reporting requirements as used to be set forth in § 10 InvG, which have never actually come into practical use.

In place of the auditing competencies of the BaFin, the custodian now has explicitly been made responsible for controlling compliance of the investment funds with regulatory and contractual investment restrictions.

Acceleration of permitsIn order to achieve quicker fund launches, the InvÄndG introduces a statutory approval period of no more than four weeks after application to grant approval of the fund rules. The BaFin must issue the permit within this time. If during this period the BaFin has not decided and has not expressed

objections against the fund rules, then the permit is deemed granted.

With respect to UCITS funds, it is possible to obtain a pre-approval by the BaFin. In any such case, the BaFin may approve a set of pre-formulated alternative template provisions for fund rules, which the KAG may then arrange to become the fund rules for a fund. Should the fund rules solely consist of such pre-approved provisions, no additional approval of the BaFin is required for launching the fund. However, prompt notifi cation to the BaFin of the creation of the funds is still required from the KAG, and the fund rules, together with both the simplifi ed and the full prospectus, must be submitted to the BaFin. It is also possible to obtain the BaFin’s pre-approval for custodians selected.

In addition, the notifi cation periods for changes in the contractual fund terms have been shortened to enable a quicker product alteration and to match fl exible market demands.

Private placementsThe legislator has addressed the problem that provisions in the former InvG were not suffi cient to determine whether or not certain sales activities were to be considered as “public distribution” within the meaning of the InvG. Therefore, the InvÄndG provides that the BaFin may publish ordinances to establish parameters for determining whether or not a sales activity qualifi es as “public distribution” under the InvÄndG.

The ordinance will apply to foreign investment, and also to domestic single hedge funds that are not permitted for distribution to the public, as they must be distributed by way of “private placements”. Furthermore, the distribution to several institutional investors will be defi ned as “Private Placement” as a standard.

European News & Views — First Edition 2008 7

Germany

8 European News & Views — First Edition 2008

CustodiansFollowing the reduced duties of KAGs and subject to the waiver of reporting obligations, the regulatory control functions of a German custodian are now, strengthened by the regulators. For the fi rst time, the InvÄndG clearly references that the custodian is expressly required to monitor compliance with the statutory and contractual investment limits for the investment funds. The reason to move these duties from the KAG to the custodian was the replacement of the § 10 reporting requirements and audit report ordinance, resulting in reasonable organisational provisions that have to be made by the custodian. In case of long-term unsolved compliance breaches, the custodian is required to escalate these breaches to the BaFin.

Apart from compliance monitoring, the following main duties remain a priority:

The control of investment funds’ NAV;

Subscriptions and redemptions;

Income;

Market conformity;

Settlements; and

Protection of the interests of investors.

Product-related changesUCITSOn 19 March 2007, the UCITS Implementing Directive was published. It serves the purpose of abolishing uncertainties with respect to defi ning certain types of fi nancial instruments under the UCITS regulations. Due to these uncertainties and different interpretations by the regulatory bodies, the European single market had shown signs of competitive distortion and supervisory arbitrage.

The BaFin has already taken into account the recommendations set by CESR and the UCITS Implementing Directive. The InvÄndG now provides the legal framework for, and paves the way to,

•

•

•

•

•

•

new and innovative products resulting in amendments or new asset classes.

Real estateReal-estate funds are now allowed to hold more than three real-estate assets, as well as stakes in real-estate companies, which hold equity participations in other real-estate companies. In case of indirect participation, there must be a 100 per cent shareholding in a second-level real-estate company or on any further level.

In addition to PPP funds,

another new fund class

(so-called “other funds”)

is being introduced, to

be used for investments

in innovative fi nancial

products.

In order to neutralise confl icts of interests between daily returns and long-term fund investors, the option to establish thresholds for redemptions has been introduced, meaning that the KAG will only have to accept redemption requests once a month and only if a notice period of up to 12 months has been complied with.

Internal real-estate expert committees shall no longer evaluate assets prior to a purchase. Valuation has to be carried out by an independent expert who is not a member of the KAG’s real-estate expert committee. Furthermore, the external professional must have appropriate personal and technical expertise relevant to properties in question.

Special funds The restriction of a maximum of 30 investors for special funds has now been changed to 100 investors.

Additionally, the investment restrictions that apply to special funds have been lightened to the effect that all assets in accordance with section 2 § 4 of the InvG can be acquired without having to comply with the various investment limits associated with different fund categories.

Also, the prohibition on contributions in kind has been lifted. Short-term borrowing of up to 30 per cent of the value of special fund assets is now possible in order to expand the investment opportunities of institutional funds.

Some restrictions remain in place, such as for loans to real-estate companies or limitations relating to market-risk potential allowed when derivatives are used for funds other than hedge funds.

Infrastructure fundsThe InvÄndG implements a new fund category that, among other investments, can invest in participations in project companies for public-private partnership (PPP). The intention is to provide private investors access to the PPP market, but only by allowing acquisition of fund-units after the completion of construction or renovation.

The rules of such funds have to provide that redemption requests will only be accepted at least once a year, but not more often than half a year. An investor may, however, only request redemption of their fund-units if the value of the units does not exceed EUR1 million.

Other fundsIn addition to PPP funds, another new fund class (so-called “other funds”) is being introduced, to be used for investments in innovative fi nancial products. Besides “classic” assets, such as securities and money-market instruments, “other funds” can acquire equity participations in non-listed

Germany

European News & Views — First Edition 2008 9

companies, precious metals and non-securitised receivables arising from cash loans.

In contrast to single hedge funds, “other funds” are not allowed to use the instruments of short selling or unrestricted leverage. Only short-term loans of up to 20 per cent of the fund value are allowed. “Other funds” have already been dubbed as German single hedge funds “light”.

Conclusion The effort to further strengthen the position of Germany as an investment market, as far as complying with the UCITS Directives is concerned, has taken almost one year from the fi rst drafted amendments to the fi nal InvÄndG passed by the German parliament and the German Federal Council. The amendments to the InvG will serve to simplify the distribution and notifi cation of foreign investment funds. It is our opinion that the implementation of new asset classes and the shortening of investment restrictions may generate more fl exibility in investment strategies and pension schemes.

Ireland

10 European News & Views — First Edition 2008

Physical short selling under UCITS: time to reconsider?

Historically physical short selling of securities has been considered not acceptable under the UCITS framework. Are we sure this is a correct interpretation, and is it now the right time to reconsider this approach?

With the implementation of UCITS III 1 and the expanded scope for the usage of derivatives, the divide between harmonised retail funds and hedge funds has become smaller and smaller.

Using derivatives for synthetic short sellingWhen the EC published its Recommendation of 27 April 2004 on the use of fi nancial derivative instruments for UCITS2 (the EC Recommendation), the investment fund industry realised the possibility of including synthetic short positions in a UCITS’ portfolio. In recent months, we have witnessed how these opportunities have been exploited to create so-called 130/30 UCITS that are, de facto, a replication of hedge funds’ long-short strategies.

Article 7.3 of the EC Recommendation, “Substitution with an Alternative Underlying Cover in the Case of Cash-Settlement”, allows synthetic short selling, as it states, “where the fi nancial derivative instrument is cash-settled automatically or at the UCITS discretion, Member States should consider allowing the UCITS not to hold the specifi c underlying instrument as cover”.

The fact that a UCITS may buy a put option on a stock without having to hold the underlying stock as a cover means that it can replicate a short-selling strategy.

In the case of 130/30 UCITS, a synthetic short position on a particular stock or on a basket of stocks is often created through an equity swap contract.

Synthetic short-selling techniques do not provide particular safeguards in comparison with physical short selling. When synthetic short selling is achieved via swap contracts, for instance, that in their most basic form do not provide for any element of protection, there is in theory no limit to the potential loss in extremely adverse market conditions. The presence of a cash or liquid cover may allow the UCITS to close the position in the case of a swap, but it is not a factor that may prevent potentially unlimited losses.

Borrowing and its implicationsArticle 2.2 “Limitation to Possible Temporary Borrowing” of the EC Recommendation states that “Member States are recommended to ensure that the UCITS’ overall risk exposure may not be increased by more than 10% by means of temporary borrowing, so that the UCITS' overall risk exposure may not exceed 210% of the NAV under any circumstances”.

In October 2007, the

Irish Financial Regulator

published policy changes

for CISs, with particular

regard to 130/30 UCITS.

This recommendation relates to article 36 of UCITS III, which states that a Member State may allow a UCITS to borrow up to 10 per cent of its assets (of its value) “provided that the borrowing is on a temporary basis”.

At the same time, article 42 of UCITS III states that a UCITS may not “carry out uncovered sales of transferable securities, money market instruments or other fi nancial instruments”.

So, UCITS III does not rule out the possibility of a physical short selling of a transferable security. It just states that two conditions apply:

1. The marked-to-market value of theshort-sold securities may not exceed 10 per cent of the UCITS’ NAV; and

2. Uncovered sales are not allowed.

Therefore, we believe it may be reasonable for a UCITS to borrow transferable securities from a third party (versus the deposit of adequate collateral), and sell them on the market — as long as the entire process happens “on a temporary basis”, but further consideration is required.

As the prohibition embedded in article 42 of UCITS III relates to “uncovered” sales in general, the key issue is then to defi ne what should be considered as being appropriate “cover”.

Regulators’ views and new initiativesThe EC Recommendation has by now been implemented in most Member States. The establishment in many EU jurisdictions of 130/30 UCITS is, as we noted before, a direct consequence of that.

Interestingly, in October 2007, the Irish Financial Regulator published policy changes for CISs, with particular regard to 130/30 UCITS.3

The Financial Regulator, with respect to 130/30 techniques (the policy change relates, however, to any UCITS), considers that, in light of the now permitted synthetic short-selling techniques, it is now appropriate to allow UCITS to enter into physical short-selling transactions, providing such transactions are covered by a stock-borrowing transaction.

Also, it suggests that a stock-borrowing arrangement “does not constitute borrowing under Regulation 70 . . . as long as the assets used to support the

European News & Views — First Edition 2008 11

stock borrow cannot be passed to the counterparty”. This means that neither the 10 per cent limit nor the concept of “temporary borrowing” applies.

Adequate coverAs we have already mentioned, the key regulatory issue to focus on is article 42 of UCITS III, stating that neither an investment company nor a management company or depositary acting on behalf of a unit trust may “carry out uncovered sales of transferable securities, money market instruments or other fi nancial instruments”.

The Financial Regulator has considered that securities borrowed constitute adequate cover.

We are not aware of any other EU jurisdictions where physical short selling is allowed under UCITS regulations; however, we think it may be of interest to identify possible alternative cover that regulators may consider in the future.

One consideration is that only the securities sold provide for a perfect cover; under any other circumstance, the UCITS would be performing a naked short sale. Alternative cover can be considered adequate, but only if the focus is limited to the economic profi le of the transaction.

Another consideration is whether or not the cover should also provide hedging against market risk. We do not believe there should be such an obligation, but it is fair to say that currently there are no guidelines available for reference.

To clarify these considerations, we think it is relevant to refer to the EC Recommendation, and in particular to the rules applicable to cover for FDIs that provide for physical delivery of the underlying fi nancial instrument on maturity or exercise. This is the case that most resembles physical short sales, where there is an obligation to deliver (or to buy back) the shorted securities.

Article 7.2 of the EC Recommendation, in particular, “exceptional substitution with an alternative underlying cover in the absence of cash settlement”, specifi es that “in case where the risks of the underlying fi nancial instrument of a derivative can be appropriately represented by another underlying fi nancial instrument and the underlying fi nancial instrument is highly liquid, Member States should consider allowing UCITS to hold exceptionally other liquid assets as cover provided that they can be used at any time to purchase the underlying fi nancial instrument to be delivered and that the additional market risk which is associated with that type of transaction is adequately measured.”

So it is possible that, should naked short selling be allowed in the future, cover could be provided by liquid assets — and cover requirements calculated on the basis of the marked-to-market value of the shorted securities.

Risk management, leverage and sophisticationThe Financial Regulator’s policy-change document also includes provisions in terms of risk-management process and disclosures.

We do not know whether

other European regulators

will follow the lead of the

Irish Financial Regulator.

In terms of risk management, the Financial Regulator requests that UCITS that want to avail themselves of the opportunity to short sell have to submit a risk-management process for approval, in particular in relation to the calculation of global exposure, and they also have to demonstrate expertise and experience in the use of short-selling strategies.

For the calculation of global exposure, additional exposure generated through short selling and reinvestment of the generated cash proceeds must be added to the exposure generated through the use of FDIs.

The Financial Regulator is silent on whether or not a UCITS engaged in physical short selling should be considered a sophisticated one, and hence whether the UCITS leverage should be calculated under the commitment approach or with a VaR methodology.

This is not a straightforward question to answer. Exposure generated via physical short selling is, prima facie, better measured with the commitment approach in consideration of the fact that the UCITS assumes an obligation to deliver assets whose value can be easily determined on the basis of market prices.

However, should a UCITS also make use of complex fi nancial derivative strategies, a VaR approach could be the preferred solution. We expect that concerned UCITS will enter into preliminary discussions with the Financial Regulator to clarify the matter.

Additional regulatory considerationsThe Financial Regulator considers that CESR’s guidelines concerning eligible assets for investment by UCITS (CESR/07-044) implicitly allow this short-selling technique when they state that UCITS are allowed “to use repurchase agreements or securities lending or security borrowing to generate leverage through the re-investment of collateral”.

We do not know whether other European regulators will follow the lead of the Financial Regulator, although we are aware a similar approach is currently being debated also in Luxembourg in different industry associations.

Ireland

Ireland

12 European News & Views — First Edition 2008

Some points may require further clarifi cation, such as the following:

It is not clear how collateral can be generated through securities borrowing. Also, CESR guidelines CESR/07-044 state that UCITS can generate leverage “re-investing collateral”, and in the case of physical short selling there does not seem to be a “re-investment”.

CESR guidelines state, with reference to Money Market Instruments (MMIs), that “article 42 of the UCITS Directive prohibits the short selling of MMIs by UCITS”. The Financial Regulator refers to “stocks” only but further clarifi cation would be welcome on this point, in particular if any inconsistency of treatment between different categories of assets were introduced.

The EC Recommendation provides for a defi nition of uncovered sale that does not refer to the absence/presence of cover, but rather to the risk to which a UCITS is exposed. Accordingly, “uncovered sales are all transactions in which the UCITS is exposed to the risk of having to buy securities at a higher price than the price at which the securities are delivered and thus making a loss and the risk of not being able to deliver the underlying fi nancial instrument for settlement at the time of the maturity of the transaction”. In the case of a physical short sale covered via borrowing, the UCITS still risks having to buy the security at a higher price, and still risks not being able to deliver the security — not to the market but to the lender.

UCITS that adopt synthetic short-selling techniques are likely to be considered as sophisticated UCITS, in consideration of the use they make of FDIs. However, UCITS that engage in physical short selling are not required to do so. Should these be

•

•

•

•

required as well to employ more sophisticated risk-management techniques such as VaR?

ConclusionDuring the past few years, CESR, various Member State regulators and the fund industry have harmonised the defi nitions of eligible assets for UCITS investment, and taken several initiatives to streamline the UCITS notifi cation process.

However, management techniques and risk-management processes have been left somehow untouched by the harmonisation effort despite the publication of the EC Recommendation, and they are now starting to diverge.

The changes implemented by the Financial Regulator are pioneering, and UCITS fund promoters have shown great interest in taking advantage of these measures by incorporating “covered” short sales in their strategies. But will these changes challenge regulatory approaches? And what will be their impact on current efforts to streamline the UCITS notifi cation procedures?

Notes1 Directive 85/611/EC of Council as amended by Directives of the European Parliament of Council.

2 Commission Recommendation COM 2004/383/EC.

3 “Collective Investment Schemes – Policy Changes and Related Matters – UCITS – Covered Short Sales”.

Jersey

European News & Views — First Edition 2008 13

Revisions to the Jersey Expert Fund GuideA key part of the recent efforts to promote Jersey’s funds industry was the introduction of the Jersey Expert Fund Guide in 2005, which offers both speed and regulatory fl exibility for those wishing to domicile funds in Jersey for “expert” investors.

In summary, the key features of an expert fund are:

Suitability for “expert investors”. Investors must satisfy certain qualifi cations, which, for example, include a minimum investment of USD100 thousand.

Fast-track authorisation process. Expert funds can essentially self-certify compliance with the policy requirements of the Jersey Financial Services Commission (JFSC) rather than be subjected to detailed scrutiny, which generally leads to establishment in a matter of days.

Promoter policy relaxed. The criteria as to who may act as investment manager of an expert fund are easier to satisfy.

Risk-warning notices. Investors must sign an acknowledgement in respect of the prescribed investment warning.

Flexibility. The JFSC takes a more relaxed approach with regard to permits issued and ongoing conditions, with no mandatory investment restrictions.

Limited need for Jersey-based functionaries. The minimum requirements are for a Jersey-based manager/administrator and two Jersey-resident directors.

The regime has been very successful, and has contributed to a period of accelerated growth in the Jersey funds sector.

•

•

•

•

•

•

Late last year, the JFSC produced an updated Jersey Expert Fund Guide, which made a number of minor enhancements to further improve the expert fund regime. These enhancements included the clarifi cation that expert funds may be listed on a stock exchange, subject to certain safeguards regarding the introduction of new investors through the stock exchange; and the extension of permissible jurisdictions in which the investment management of an expert fund may take place, so as to include, as well as any OECD Member State, any other state or jurisdiction with which the JFSC has entered into a Memorandum of Understanding on investment business.

The Non-Jersey Domiciled Fund GuideThe Expert Fund Guide was closely followed by the introduction of the Non-Domiciled Fund Guide designed to make the administration of funds from Jersey simpler and more effi cient.

In February 2007, the JFSC issued the revised Non-Jersey Domiciled Fund Guide which, again, made a number of enhancements as regards the regime applying in Jersey for administration of non-Jersey-domiciled funds. In general, several important clarifi cations were introduced, including the removal of the requirement for a non-Jersey-domiciled fund to hold a permit under the Collective Investment Funds (Jersey) Law 1988 (the Collective Law), provided that it does not have an established place of business in Jersey. The established-place-of-business test was also clarifi ed by an amending order under the Collective Law, meaning that a foreign company should not have an established place of business in Jersey by reason only that the directors meet in Jersey, or a manager, director or administrator of the company is ordinarily resident in Jersey.

Jersey regulatory requirements for non-domiciled funds are expected to be further relaxed, following the

consolidation in regulations described below (see “Future Regulation of Funds and Functionaries of Funds”).

The Jersey Listed Fund GuideA new guide, “The Jersey Listed Fund Guide” on Jersey incorporated funds, which are intended to be listed on a stock exchange, was introduced in January 2007. The guide introduces a fast-track procedure for the establishment of closed-end collective investment funds, which are to be listed on certain well regulated stock exchanges or markets. The main advantage of the listed-fund procedure is speed, in that such funds should be approved by the JFSC within three working days. Also, such funds are not restricted only to expert investors.

The investment manager of a listed fund must be of good standing and established in an OECD Member State or in a jurisdiction with which the JFSC has entered into a Memorandum of Understanding, and all listed funds must have at least two Jersey-resident directors and a Jersey-based monitoring functionary to ensure due diligence and compliance with the Jersey Listed Fund Guide.

Future regulation of funds and functionaries of fundsIn November 2007, a change of regulation resulted in all fund functionaries being licensed under the Financial Services Law, rather than under the Collective Law. This new method of regulating “fund services business” is important and should simplify the procedure required when setting up a new fund in Jersey. In particular, once a Jersey monitoring functionary has been licensed under the Financial Services Law as a fund services business, it will be allowed to take on new fund administration business without the need for additional licences/permits (as is currently the case) under the Collective Law.

Recent developments in Jersey funds

Jersey

14 European News & Views — First Edition 2008

The JFSC is set to introduce

the Unregulated Eligible

Investor Exemption,

which will permit the

establishment of an

unregulated fund that

is exempt from the

requirements of the

Collective Law.

Although the fund itself will continue to require a regulatory permit under the Collective Law, the majority of the requirements imposed by the JFSC will be placed on the Jersey monitoring functionary, rather than on the fund itself. It is expected that those who currently carry on fund services businesses in Jersey will be “grandfathered” into such regime. There will then be a new Code of Practice for fund services business and, thus, in some instances, there will need to be compliance with higher regulatory standards in the conduct of all fund services business in Jersey.

However, the JFSC has recognised that certain fund functionaries, in particular managed entities without a physical presence on the Island, should have the opportunity to be exempt from the Codes of Practice and, in which case, continue to comply with their existing permit conditions. As a consequence, the areas of the Codes of Practice, which currently provide a lighter, easier regime for what are termed “managed managers”, are expected to remain.

These changes will also result in the Non-Domiciled Fund Guide (see above) having a more limited application. In most cases, a Jersey-based entity acting for a non-domiciled fund will be able to

do so by virtue of its registration under the Financial Services Law.

International cooperationThe JFSC is seeking bilateral agreement with other jurisdictions for regulatory purposes. In this respect, during the past year Memoranda of Understanding have been entered into with the Netherlands and Cyprus, establishing a formal framework for mutual assistance and exchange of information between regulators and to facilitate the enforcement and compliance with laws in each jurisdiction so as to protect investors and depositors in such jurisdictions.

In the case of the Netherlands, this is an important development, as it permits Jersey-listed funds to be recognised as an appropriate vehicle for listing on EURONEXT I Amsterdam. The use of a EURONEXT listing for permanent capital vehicles in connection with property funds, private-equity funds and hedge funds has been an area of growth in the past 12 months for the Channel Islands.

Unregulated fundsIn the early part of 2008, the JFSC is set to introduce the Unregulated Eligible Investor Exemption, which will permit the establishment of an unregulated fund that is exempt from the requirements of the Collective Law. Unlike the position with regular collective investment funds in Jersey, there will be no approval process conducted by the JFSC for such unregulated funds and any offering document will be required to include a prescribed form of investment warning and state clearly that the fund is not regulated by the JFSC.

An eligible investor in an unregulated fund is expected to be required to make a minimum initial investment of USD1 million or otherwise satisfy “expert investor” type criteria as described in the term sheet issued by the JFSC. Unregulated funds may be open- or

closed-end funds, listed or unlisted, and will have no set restrictions on investments, borrowing or gearing. It is also anticipated that unlike the position with Jersey expert funds, there will be no requirement for Jersey-domiciled directors and/or administrators. The Jersey unregulated fund should prove particularly attractive to European-based promoters and managers looking to establish offshore hedge funds.

Simon PascoePartnerBedell Group

Luxembourg

European News & Views — First Edition 2008 15

Fair valuation of illiquid securities remains a challenging issue in the UCITS world. While standard industry fair-valuation practices are still lacking, a new CSSF Circular has provided more clarity on how fair valuation should be implemented for Luxembourg UCITS.

UCITS III funds use actual trading market prices to value their portfolio investments. When actual market prices are not readily available, fair values need to be assessed.

“Fair value” refers to the price at which an asset would trade if a liquid market existed in such an asset. A key concept is, of course, the defi nition of “liquid market” that indicates that there will be both buyers and sellers of the security. Furthermore, the appropriate price will be the one at which there is a balance between buyers and sellers (market equilibrium).

There is not as such a “right” or “correct” price for a fair-valued security. There exists, however, a reasoned process for making informed valuation decisions.

The methods used to fair-value portfolios can be questionable in non-liquid markets, and they have revealed signifi cant problems, especially in the light of the recent sub-prime crisis, in the ways valuation methods are conducted. Despite the importance of the issue to investors, and inconsistencies in practices adopted among funds, there is no generally accepted means to conduct fair valuations, and little disclosure by funds as to the methods by which fair valuations are conducted, who conducts them, when they are conducted or how much fair valuation affects portfolio or unit valuations.

Fair valuation is, however, a domain in which regulatory expectations rapidly evolve.

The new CSSF Circular 07/308 on UCITS risk management states that OTC fi nancial derivative instruments in UCITS III must be valued daily, accurately and verifi ably, and independently of the UCITS. The UCITS must be able to determine with reasonable precision their fair value throughout their life.

A reliable and verifi able valuation must meet the following criteria:

The valuation must be based on a current market value or, if it is not available, on a valuation model that used a recognised and accepted methodology; and

The control of the valuation must be performed either by:

a. An independent third party,suffi ciently frequently and following a process that can be monitored by the UCITS; or

b. A unit independent of the portfolio management of the UCITS. The UCITS can use third-party valuation tools or market data but must verify their adequacy. Models used by a party linked to the UCITS (such as a trading room that executes the UCITS transactions) are expressly prohibited if they have not been reviewed by the UCITS.

The UCITS also needs to communicate the valuation process to the CSSF, including a description of the unit in charge, methods used, type of controls, etc.

The responsibility for fair-value determination is assigned to the Board of the fund as a whole, as the valuation of fund assets and liabilities determines a fund NAV. Fair-valuation issues need to be addressed in valuation policies and procedures. This includes:

•

•

Escalation procedures that will be triggered by the nature of a specifi c event;

The size of the position being fair-valued; and

The valuation material impact on the fund’s NAV.

The Board also needs to establish criteria for determining when market quotations are not reliable for a particular security. It has to establish methodologies to determine the current value of securities and, fi nally, to regularly review the appropriateness and accuracy of the methods used in valuing security.

Independent control of pricing can be done in several ways. Complete and independent revaluation of the security can enable the identifi cation of any signifi cant bias in the valuation methodology as well as the evaluation of market data reasonableness. The objective is not to assess the accuracy of the valuation, but to test the appropriateness of the approach and to check that it was applied consistently over time. Independent control should use its own set of data, use its own valuation methodology and decide on the necessary thresholds it wants to set before escalating the issue.

SEC Division of Investment Management Director Paul F. Roye summed up the fair-valuation process well in April 2004: “Fair valuation procedures must continuously be . . . critiqued, and refi ned in order to maximize their effectiveness for the benefi t of shareholders. Fair valuation, therefore, must be a dynamic process.”

Laurent DenayerSenior ManagerErnst & Young Business and Advisory Services

•

•

•

Fair valuation in the UCITS risk-management world

United Kingdom

16 European News & Views — First Edition 2008

Many European jurisdictions have already incorporated the ability to establish or convert to a protected cell investment company within their legislation. Such companies can be found in Ireland, France, Luxembourg, Isle of Man, Guernsey and Jersey, to name but a few.

In the United Kingdom, while the UK legislation does not currently permit for the provision of protected cells within an umbrella OEIC, in the summer 2007 HM Treasury consulted on outline proposals to develop a protected cell regime for UK OEICS in a paper entitled “Consultation on Better Regulation Measures for the Asset Management Sector”, dated May 2007.

The term “protected cell” may not be very familiar to everyone, especially as the ability to operate protected cells within umbrella investment companies is not possible in all European jurisdictions. It might be useful to start off with an explanation as to how the “cells” operate and what benefi ts they might offer, especially from an investor’s perspective. We can then go on to compare how the other jurisdictions operate in more detail.

The main feature of a protected cell investment company is that, although the investment company remains a single legal entity, it consists of separate and distinct cells. The assets and liabilities of each cell are protected from those of the other cells.

The overall objective is to ensure that the assets of one cell are: only available to those creditors of the investment company who are creditors in respect of that cell; protected from the creditors of the company who are not creditors in respect of it; and protected from the creditors who are not entitled to have recourse to its assets. A protected cell enables the assets to be ring-fenced

within the investment company’s individual cells.

Establishing protected cell investment companies — implications for investors To help understand this, it is useful to look at the development of funds under the Undertakings for Collective Investment in Transferable Securities (UCITS) Directive 85/611/EEC, otherwise known as UCITS. Following changes to the UCITS rules, known as UCITS III, we are seeing schemes investing in increasingly complex instruments and adopting riskier strategies. For example, the same investment company might have one sub-fund investing in UK equities, another in derivatives or structured products and another in overseas investments. These sub-funds might also employ borrowing (a form of leverage).

In the summer 2007

HM Treasury consulted

on outline proposals to

develop a protected cell

regime for UK OEICS.

Recent developmentsThe Irish Financial Regulator has proposed amendments to Notice UCITS 12 and Guidance Note 3/03. It says that a UCITS scheme in Ireland would be allowed to create short positions and then use the cash proceeds to invest in additional long positions. This means that the scheme can potentially have a maximum leveraged global exposure of 300 per cent, while the market exposure of the total portfolio remains at a net 100 per cent. (See the Financial Regulator’s “Collective investment schemes — policy changes and related matters — October 2007” under the heading of UCITS-

Covered short sales). This will assist with the development of short extension policies such as 130/30 funds.

While they say the rules may allow for this, they have not discussed in detail the practical application.

Comparison of different protected cell regimesLuxembourg Multiple compartment UCIs are recognised under article 133 of the 2002 Law on UCIs. In brief, this states that the assets of a compartment are only subject to the liabilities of that compartment, unless the constitutional documents of the UCI stipulate the contrary.

This is similar in concept to the protected cell regime in Ireland, but in Luxembourg protected cells amount to legally separate funds. UCIs may be constituted with multiple compartments, each compartment corresponding to a distinct part of the assets and liabilities of the UCI.

The constitutional documents of the UCI must expressly provide for that possibility and the applicable operational rules. The issue prospectus must describe the specifi c investment policy of each compartment. The rights of investors and of creditors concerning a compartment or which have arisen in connection with the creation, operation or liquidation of a compartment are limited to the assets of that compartment, unless a clause included in the constitutional documents provides otherwise.

The assets of a compartment are exclusively available to satisfy the rights of investors in relation to that compartment and the rights of creditors whose claims have arisen in connection with the creation, the operation or the liquidation of that compartment, unless

Protected cell investment companies: UK developments

United Kingdom

European News & Views — First Edition 2008 17

a clause included in the constitutional documents provides otherwise.

Each compartment of an undertaking may be separately liquidated without such separate liquidation resulting in the liquidation of another compartment. Only the liquidation of the last remaining compartment of the UCI will result in the liquidation of the UCI as referred to in article 106 (1) of the Law of 20 December 2002 relating to the undertakings for collective investment.

Article 106 (1) states, “In the event of a non-judicial liquidation of an UCI, the liquidator(s) must be approved by the Commission for the Supervision of the Financial Sector (CSSF). The liquidator(s) must provide all guarantees of honourability and professional skill.”

France In France, in 1989, a legal framework for collective investment schemes (SICAVs) was established in accordance with European Directive 85/611/EEC relating to UCITS III.

A SICAV is a limited company (Société Anonyme) that can only manage its own portfolio and is subject to special regulations. The company's capital is at all times equal to its net assets. Various types of SICAVs exist, but for the purposes of protected cells, the one that we are most concerned with is the umbrella SICAV, which consists of a single structure, composed of different compartments, each compartment having its own distinct investment policy.

Traditionally, French UCITS were always considered, even though consisting of several compartments, as single legal structures. It was not possible to structure “watertight” compartments. As a result, compartments or protected cells were introduced in France in August 2003. (Details of the provisions can be

found in article L214-33 of the Monetary and Financial Code.)

A UCITS may have two or more compartments if its articles of association provide for this. Each compartment gives rise to the issue of a category of shares or units that represent the assets of the UCITS that are allocated to it.

In summary the French regulator introduced a new concept into French law whereby “Notwithstanding Article 2093 of the Civil Code and unless otherwise stipulated in the undertaking for collective investment in transferable securities, articles of association, the assets of a given compartment may only be used to meet the compartment’s debts, commitments and obligations and only benefi t from that compartment's receivables.” (Article L214-33).

Perceived benefi ts to fund accounting, from this introduction, have been in the areas of information and marketing. For example, if an investor holds shares in a compartment and they have already received a copy of the full prospectus, the fund manager is authorised to sell units in another one of the compartments of the umbrella by presentation of that compartment’s simplifi ed prospectus.

Isle of ManPart 1 of the Financial Supervision Act 1988 established a new statutory framework in the Isle of Man for the promotion and regulation of collective investment schemes.

Under the heading of International Collective Investment Schemes (ICIS) section 1.3.5, it makes reference to ICIS formed as protected cell companies.

The Protected Cell Companies (Prescribed Class of Business) (Collective Investment Schemes) Regulations 2004

enable certain collective investment schemes (International Schemes) in corporate form to be “prescribed class of business” for the purposes of the Protected Cell Companies Act 2004. It states that International schemes have been prescribed and may be formed as a protected cell company.

IrelandThe Companies Act 1990 was amended to provide for segregated liability and cross-investments for investment funds. The changes were achieved through amendment of Part XIII of the Companies Act 1990. Legislation brought in during 2005, “Investment Funds, Companies and Miscellaneous Provisions Act” introduced segregated liability between sub-funds of the same umbrella. This became law on 30 June 2005.

The 2005 Act provided for complete segregation of liability between sub-funds of an umbrella fund company. Any liability incurred on behalf of or attributable to any sub-fund will be discharged out of the assets of that sub-fund and the assets of any other sub-fund shall not be applied to satisfy that liability. All umbrella fund companies established after 30 June 2005 must provide for segregated liability, and many established prior to that date are electing to convert to segregated liability status.

To adopt segregated liability, a company’s memorandum and articles of association must be amended by resolution of the shareholders in a general meeting.

Once the segregation of liability between sub-funds has been adopted, the 2005 Act requires that the words “an umbrella fund with segregated liability between sub-funds” be included in the company's letterhead. Also, in any written or oral contracts, the 2005 Act requires that the status of the company as an umbrella

United Kingdom

18 European News & Views — First Edition 2008

fund with segregated liability between sub-funds must be disclosed. In order to protect potential investors of such funds, a strict disclosure is required of all material matters.

Guernsey and JerseyProtected cell companies (PCCs) were fi rst developed in Guernsey in the late 1990s. Initially this was to attract captive insurance work to Guernsey; but, proving popular, they were seen to be a useful vehicle for collective investment fund structures.

In July 2005, the States of Jersey approved the Companies (Jersey) Law (Amendment No. 8). The amendment came into force early in 2006 and a key purpose of the amendment was to introduce cell companies into Jersey law.

There were two new vehicles introduced: the Jersey PCC and the Incorporated Cell Company (ICC). The purpose was to provide a vehicle that could create cells and to, separate parts — within which assets and liabilities may be segregated. The key principle here is that the assets of a cell should only be available to the creditors and shareholders of that cell.

A framework can be established which includes all the participants in the structure such as administrators, managers, investment managers and custodians. When particular transactions are envisaged, such as adding a new fund to invest in a specifi c country or sector, a cell can be created specifi cally to act in that defi ned role. A new cell can therefore be added at a fraction of the cost and time that would be required were the structure to be established from scratch.

Some of the advantages of Jersey cell companies over other jurisdictions are that they allow for stronger ring-fencing of assets and liabilities, reduced risk

of the cell company itself becoming insolvent and rights of cells to invest directly in each other.

United KingdomUK legislation does not currently allow for the provision of protected cells within an umbrella OEIC.

To allow a UK umbrella

OEIC to be set up as a

protected cell company,

or to convert an existing

one to have protected

cells, will require an

amendment to the OEIC

Regulations 2001.

It seems that umbrella schemes constituted as AUTs, in the event of default, would be wound up in accordance with the provisions of its constituent trust deed. It is unlikely that trust law would allow contagion between sub-funds, although this currently remains unsubstantiated as there are no real-life examples of an insolvency of an umbrella scheme constituted as an AUT.

UK OEICs can be established in the legal form of umbrella funds, under which a number of sub-funds are created. These are all within the same legal entity. Generally, this makes the investment company legally liable for all the debts of the investment company, including any debts occurring at sub-fund level.

This risk between sub-funds is often described as cross-contagion, as the umbrella OEIC is able to draw on the assets of each of its sub-funds if one was to become insolvent.

To allow a UK umbrella OEIC to be set up as a protected cell company, or to convert an existing one to have protected cells, will require an amendment to the OEIC Regulations 2001.

One of the FSA’s concerns in undertaking work with HM Treasury is protection for the investor. The investor may not be aware that investing in a “safe”, less risk-adverse sub-fund will actually make them liable (in the case of a failure to meet liabilities) for the losses of a much riskier sub-fund within the same umbrella investment company.

It is important to keep things in perspective from a UK viewpoint, as in practice the probability of an umbrella sub-fund collapsing is small. They must comply with FSA-imposed borrowing requirements that allow a maximum of 10 per cent borrowing for non-UCITS retail schemes on a non-temporary basis and a 10 per cent limit on borrowing for UCITS schemes that can only be on a temporary basis, imposed by the UCITS Directive.

In addition to borrowing facilities, investment companies may also use derivatives to gain additional exposure. Although there are no maximum limits imposed for investment purposes, any exposure generated must be fully covered by the schemes property. In conjunction with the borrowing facility, a scheme can achieve a maximum exposure of 110 per cent.

The aim would be to

reduce contagion risk for

investors and to bring the

UK into line with other

leading EU fund domiciles.

European News & Views — First Edition 2008 19

Notes1 Disclaimer: Amanda Hale writes in a personal capacity. The views expressed herein are those of the author, and do not necessarily refl ect the views of the Financial Services Authority. The text does not constitute guidance for the purposes of section 157 of the Financial Services and Markets Act 2000.

Since writing this article, Amanda Hale has joined Citi, working with European Fiduciary Services.

To assist investors in accessing this risk, the FSA also require the contagion risk to be disclosed in the fund prospectus and in periodic reports. There is still a chance, though, that investors may not fully understand the implications of this risk.

Recognising the risks associated with non-segregated liability in umbrella funds, HM Treasury consulted on the outline proposals to develop a protected cell regime for UK OEICs in its paper, “Consultation on Better Regulation Measures for the Asset Management Sector”.

The aim would be to reduce contagion risk for investors and to bring the UK into line with other leading EU fund domiciles. HM Treasury is currently considering responses and will announce what the next steps will be shortly.

Amanda HaleAssociateFinancial Services Authority1

United Kingdom

20 European News & Views — First Edition 2008

United Kingdom

Stock lending is an increasingly well-used method in the investment manager’s toolkit, and the FSA in the UK has made some recent changes and clarifi cations to the rules in this area. For authorised funds, stock lending is becoming a more attractive investment technique as an extension of effi cient portfolio management (EPM), by generating additional income for the benefi t of a fund.

Stock lending involves the temporary transfer of securities by a lender to a borrower, with an agreement from the borrower to return equivalent securities to the lender at a pre-agreed time. For a fund, collateral equal to the value of the securities transferred (plus a margin or haircut) is required to be given to the depositary to set against the risk of default.

In its CP 06/18 of October 2006, the FSA proposed that the rules on stock lending be made more fl exible for UCITS investment funds (funds that can be authorised for sale in any of the EU Member States) and non-UCITS retail schemes. Further consultation was carried out, and the results were published in Handbook Notice 63, February 2007. The rule changes were introduced to the COLL sourcebook (the rule book that applies to all UCITS and non-UCITS retail schemes under the FSA) on 6 March 2007, and they are contained in COLL 5.4.

The rule changes are as follows:

Repurchase and reverse repurchase agreements are allowed within the scope of permitted stock lending. Many funds had been using repos, but it was not clear from the rules that this was permitted and so clarifi cation on this has been provided.

The list of permitted counterparties with whom stock-lending transactions may be undertaken now includes US

•

•