new relationships for health plans: accountable systems of care 1 michigan association of health...

TRANSCRIPT

1

NEW RELATIONSHIPS FOR HEALTH PLANS: ACCOUNTABLE SYSTEMS OF CARE

Michigan Association of Health Plans2015 Summer Conference

Nuyen, Tomtishen and Aoun, P.C.

HAVEN’T WE SEEN THIS ALL BEFORE?

1990s

Predominant focus: lower costs

Success under risk contracts driven by risk selection

Health IT just starting

HMO focused with robust UR and benefit designs requiring gatekeepers

Commercial payor focused

Today

Focus on both costs and quality

Risk adjustment seeks to equalize the playing field

Greater investment in health IT spurred by federal $$$; data analytics

Programs can operate in PPO or traditional FFS products; new focus on evidence-based care

Medicare is “in the game” 2

Nuyen, Tomtishen and Aoun, P.C.

MEDICARE ACOs Over 400 ACOs serving more than 7 million

Medicare beneficiaries Close to 20 in Michigan, including 1 Pioneer ACO

(DMC/Tenet) 3 received shared savings distributions with

respect to 2013 (collectively, $ 26.7M); 1 had a loss ($2.5M)

MedPAC analysis – Study of ACOs in 78 markets (1.7 million beneficiaries). ACOs performed comparable to Medicare FFS In high use areas, ACOs saved Medicare about 2%.

3

Nuyen, Tomtishen and Aoun, P.C.

MEDICARE ACOs Traditional options

Track 1 – upside only Track 2 – upside and downside risk (up to 60% share of

savings) – only 5 ACOs chose this Track Pioneer – higher levels of upside and downside risk (60-

75%); prospective assignment – currently 19 remain in the program (initially 32)

New Options Track 3 (new) – higher levels of upside and downside risk

(up to 75% share of savings) Next Generation – higher levels of upside and downside

risk (80-100%) with improvements in benchmarks, attribution and beneficiary engagement; flexibility in payment arrangements

Investment Model - incentives to foster ACOs in rural areas, e.g., advance payment for infrastructure

4

Nuyen, Tomtishen and Aoun, P.C.

MEDICARE P4P TRAIN Bundled Payments

Bronson, Borgess and DMC/Tenet in Phase 2 (risk bearing) Borgess and DMC (knee and hip replacement); Bronson (knee and hip replacement, neurosurgery

and cardiac) Numerous other Michigan hospitals (and physician

groups) are currently in Phase 1 (evaluation) Trinity Health Beaumont Health (Oakwood and Botsford) Marquette General Hospital Portage Health Lakeland Hospital

5

Nuyen, Tomtishen and Aoun, P.C.

MEDICARE P4P TRAIN Bundled Payments

Comprehensive Joint Replacement Model (proposed rule) Knee and Hip Replacement Mandatory participation in 75 areas

Flint and Saginaw are designated Hospitals must assume risk for admission

and 90 days post-acute care

6

Nuyen, Tomtishen and Aoun, P.C.

MEDICARE P4P TRAIN Hospital Value-Based Purchasing Measures performance across various

domains Outcomes (mortality, patient safety)

(30%) Patient Satisfaction (30%) Clinical Processes of Care (20%) Efficiency (20%)

FY 2015: 1.5% (by 2017, it will reach max of 2.0%) Multiplier effect (2.58 in FY 2015)

7

Nuyen, Tomtishen and Aoun, P.C.

MEDICARE P4P TRAIN Hospital Value-Based Purchasing Efficiency domain evaluates

Medicare Spending Per Beneficiary for admission and services rendered within 30 days following admission (even if such services are unrelated)

8

Nuyen, Tomtishen and Aoun, P.C.

MEDICARE P4P TRAIN Other Initiatives

Hospital and physician quality reporting Inpatient reporting to include episode

payment

Physician payment reform – Merit-based incentive payments (includes penalties) begins in 2019 Ability to opt out if participating in a

sufficient number of “alternative payment models”

9

Nuyen, Tomtishen and Aoun, P.C.

STATE INNOVATION MODEL & MEDICAID

Payment for Value Increasing number of Patient Centered

Medical Homes Establishment of Accountable Systems of

Care Initially shared savings (level 1), but

ultimately downside risk assumption (level 2) Community Health Innovation Regions –

multi-stakeholder involvement to improve health, cost and satisfaction

Medicaid re-bid

10

Welcome

Detroit Medical Center2015

11

Welcome

12

DMC By the Numbers

Detroit Medical Center is proud to be part of Tenet Healthcare Corporation, a national, diversified healthcare services company, with:

80 Hospitals, including DMC210 Outpatient Centers105,000 Employees

7 Hospitals and 2 Institutes51 Outpatient Facilities1,811 Licensed Beds3,000 Affiliated Physicians13,323 Employees

2014 Patient StatsDischarges

Adult/Child: 77,275Newborn: 5,456

Outpatient Visits: 1,100,383ER Visits: 354,073Surgeries:Inpatient: 20,572Outpatient: 36,224

7 Children’s Hospital of Michigan Outpatient Facilities

1 Huron Valley-Sinai HospitalOutpatient Facility

32 Rehabilitation Institute of Michigan Outpatient Facilities

9 Sinai-Grace HospitalOutpatient Facilities

2 Sinai-Grace Hospital and Harper University Hospital Professional Buildings

Children’s Hospital of MichiganDetroit Receiving Hospital and University Health CenterHarper University HospitalHeart HospitalHutzel Women’s HospitalRehabilitation Institute of Michigan

Welcome

13

LeapFrogDMC Harper/Hutzel

DMC Huron Valley-SinaiDMC Detroit Receiving

DMC Sinai-Grace

Welcome

14

DMC Detroit ReceivingDMC Sinai-Grace

MPRO's 2014 Governor's Awards of Excellence

Detroit Receiving Hospital Harper University Hospital/Hutzel Women's Sinai-Grace Hospital and Huron Valley-Sinai Hospital

Environmental and Excellence Achievements

Nation’s leading health care community supporting environmental stewardship working to improve patient safety and care through tools, best practices and knowledge sharing.

Welcome

15

DMC Awarded CMS National Health Care $10 Million Innovation Award

DMC among few to receive $10 million grant from Centers for Medicare and Medicaid Services to test new primary care model in Detroit

• DMC Chief Medical Officer Dr. Suzanne White is one of only 39 recipients of about 3,000 applicants across the United States. The grant will enable the DMC to test an innovative primary care and preventative health model that reaches patients who use some of Detroit’s busiest emergency departments.

• The project, entitled Gateway to Health: An Innovative Model for Primary Care Expansion in Detroit, will make patient-centered medical care immediately accessible to individuals without existing primary care physicians, arriving to four DMC emergency departments at DMC Harper University Hospital, DMC Detroit Receiving Hospital, DMC Sinai-Grace Hospital and DMC Children’s Hospital of Michigan.

Welcome

16

2014 Most Wired HospitalFor the eighth consecutive year, Detroit Medical Center has been named to the nation’s MOST WIRED list, according to the results of the 2014 Most Wired Survey and Benchmarking Study released in the July issue of Hospitals & Health Networks magazine, which has named the Most Wired hospitals and health systems since 1999.

The Most Wired Survey is conducted annually by Hospitals & Health Networks magazine. It focuses on how the nation’s hospitals use information technologies for quality, customer service, public health and safety, business processes and workforce issues.

DMC EMR and IT Awards

Welcome

17

“The focus of the Michigan Pioneer ACO is not on cutting required care but rather on improving care transitions and care coordination,” said DMC Chief Medical Officer Dr. Suzanne White. “The efforts of the Michigan Pioneer ACO will continue to focus on improving quality and outcomes, while reducing unnecessary costs.”

“The focus of the Michigan Pioneer ACO is not on cutting required care but rather on improving care transitions and care coordination,” said DMC Chief Medical Officer Dr. Suzanne White. “The efforts of the Michigan Pioneer ACO will continue to focus on improving quality and outcomes, while reducing unnecessary costs.”

Welcome

18

Payer Provider relationships• Guaranteed failure• Unbalanced deal• Lack of timely data• Too much faith on

abilities to manage everything

• Lack of focus and attention

• Lack of statistical validity

• Guaranteed success• Balanced and fair

agreement• Timely and accurate

data• Real involvement of

physicians• Using process

improvement techniques

Welcome

19

Recent Examples in the Market

• Getting the incentive deal in June – without data by doctor – “…well, that’s coming.”

• Not getting first of year data until May.• Plan authorizing an admit to “not upset the member”

over Med. Dir objections.• Call 24 HH agencies – none will take patient.• Payer and DME Co. arguing over payment for DME –

patient sits in hospital Fri-Mon.• DRG audit – request records – downgrade before getting

records.

Welcome

20

Questions

• How do we eliminate redundancy between plans and providers– auths, UM, etc.?

• How can collaboration happen on a higher level?

• When will there be national standards for health plans to adhere for provider service? See next slide – Trust?

Welcome

21

Trust Toward PayorsComposite Trust Measures*

• The average score for all payor was 51.8; the average change from 2014 was -0.7.• Cigna, Blue Cross / Blue Shield, and Aetna all were above-average performers.• Humana, Bluecard, Wellpoint / Anthem, and UnitedHealthcare were all below-average performers.• BCBS, Humana, and Bluecard improved on their scores from 2014; Cigna, Aetna, Anthem, and United all declined in trust from 2014. The largest decrease was by Anthem with a drop of nearly 4 points.

*Composite Trust Index Score values are calculated as an equally-weighted mean of all three individual Trust measures.

Welcome

22

23

24

Who Is MidMichigan?

Non-profit health system affiliated with the University of Michigan Health System

More than 5,000 employees and physicians

4 Hospitals 17 Locations with Medical

Offices 6 Health Parks 7 Urgent Cares 8 Continuing Care

Locations

25

Population Health InitiativesCurrent Strategies and Accomplishments• ConnectCare Self-funded PPO Product• Accountable Care Organization (ACO) • Medicare Shared Savings Program• Narrow Network Development• Merger and Acquisition Activity• Partnerships with Health Plans• Board Approved Population Health Strategy• State Innovation Model (SIM)• Patient-centered Medical Home / Neighborhood• Patient Registry / Health Information Exchange / Data Warehouse

26

Overarching Population Health Strategy

Enhance the patient experience to strengthen patient engagement and loyalty

Continue to develop value-based payment strategies with payors and increase covered lives

Collaborate and align efforts with physicians and community/state agencies to transform care in meaningful ways

Invest in tools and personnel to create a team-based care management approach and effectively coordinate patient care

27

Matching Services to Health Status

5%

15-35%

60-80%

High Risk

Dedicated, individualized care plan, avoid (re)admissions, care

coordination

High risk care management, navigators, care planning,

palliative care, behavioral health

Avoid duplication, overutilization & higher acuity

sites, enhance access & patient engagement

Moderate care management, patient portal, patient engagement & self

management

Patient engagement, self management; convenient, affordable, accessible care

Patient portal, telehealth & e-visits, retail clinics, hybrid/concierge model

Moderate Risk

Low Risk

Patient Needs Tailored Services

Con

sum

ptio

n o

f H

ealth

Car

e S

ervi

ces

28

Health Factors Affecting Health Outcomes1

Health Factors

Health Behaviors 30%

Tobacco use

Diet & Exercise

Alcohol use

Clinical Care 20%Access to care

Quality of care

Social & Economic Factors 40%

Education

Employment

Income

Family & Social Support

Community Safety

Physical Environment 10%

Environmental Quality

Built Environment

1http://www.countyhealthrankings.org/our-approach

Health Plan Barriers

Hindering Forward Progress

o Misaligned incentives• Less than 2% of revenue is from value based purchasing

arrangements• Significant majority of revenue continues to be fee-for-service

o Time gap between implementation and incentive realization• Benefits are being captured now, primarily benefiting health plans and

negatively impacting the potential for future rewards to providerso Focus on “rules” (technical denials) rather than rewarding overall

performance and positive trendso Lack of consistent guidelines, benchmarks and regulations across all

payors

29

Health Plan Barriers

Future Opportunities

o Identify and implement strategies to address the 80% of health factors that affect health outcomes

o Make room for and encourage provider self-management• Transition care management responsibilities along with the

delegated risk to decrease cost• Share savings with healthcare providers

o Reduce overhead costs (consistent with your expectations of healthcare providers)

30

©2014 Trinity Health. All Rights Reserved. 3131

Hospitals in 21 States85*

Home Health &

Hospice Agencies44

Continuing Care Facilities70

Employed Physicians

3,300

PACE Center Locations14

Affiliated Physicians

22,890

Other Continuing Care Facility

Employed Physicians

Affiliated Physicians

Hospital

Home Care Agency

PACE Center

Introduction to Trinity Health: Our 21-State Diversified Network

128 Long-term care, assisted, independent living and affordable housing communities

©2014 Trinity Health. All Rights Reserved. 32

Stein’s Law

32

“If something cannot go on forever it will stop”

©2014 Trinity Health - Livonia, MI 33

Accenture Research shows: By 2017, nearly 1 in

5 Americans will purchase benefits from a health

insurance exchange (30 mil in private exchange

and another 30 mil in public exchange)

33

RETIREES:

IBM moves 110,000 retirees to Towers Watson’s

Medicare exchange for 2014

PART-TIMERS:

Target discontinues coverage for

part-time employees and shifts them to

public exchanges (via a private model)

ACTIVE EMPLOYEES:Walgreens will offer its 160,000 employees subsidies to buy insurance on Aon Hewitt’s private exchange in 2014

©2014 Trinity Health. All Rights Reserved. 34

Transition from Fee For Service to Risk

34

• Quality Reporting• Gaps in Care• QI Program

• Hospitalist Program• SNFist Program• Discharge Program• Home Care

Program• Actuarial Services

• High Risk Clinic• Enrollment Clinic• Claims Payment• Network Mgmt• Customer Service

• Care Management

Pay for Performance

Gain Sharing/ACO Model

SymmetricRisk

HealthPlan

% Premium

Competencies

30%

Full RiskCapitation

• Quality Reporting• Gaps in Care• QI Program

• Quality Reporting• Gaps in Care• QI Program

• Hospitalist Program• SNFist Program• Discharge Program• Home Care

Program• Actuarial Services

• Care Management

• Quality Reporting• Gaps in Care• QI Program

• Care Management

• High Risk Clinic• Enrollment Clinic• Claims Payment• Network Mgmt• Customer Service

• Hospitalist Program• SNFist Program• Discharge Program• Home Care

Program• Actuarial Services

• Care Management

• Quality Reporting• Gaps in Care• QI Program

5%

50%90% 100%

Model

• Marketing and Sales• Licensing

©2014 Trinity Health. All Rights Reserved. 35

Insights that will drive strategy

35

• Lowest cost silver plans (top 3 to 5) players captured > 90% market share (out of pocket cost also, important)

Lowest cost premiums drive market share

• ~70%+ renewed with the same insurance company as the last year

Inertia is strong and barriers to switch are high

• Narrow network can be traded off with lower monthly $ premium.

• Broad physician network is more important than a broad hospital network

Network is important after cost

• Trust is important for consumers. New entrants/less familiar brand names would be less preferred

Trust in Insurance company

• Strategic growth dictates that we be precise in the discounts we accept in order to capture lives

Commercial-like rates

are necessary

1

2

3

4

5

©2014 Trinity Health. All Rights Reserved. 36

Trinity Health is investing in capabilities to deploy a proactive population health management model nationally

36

… which employs comprehensive medical management infrastructure programs…

‘Virtuous Cycle’ of

Improved care

… and yields superior outcomes

Designed to address patient needs at all points of care before and including the hospital

Improved accessImproved coordination and

ownership of careImproved disease stabilizationImproved patient and physician

satisfactionImproved quality and utilization

measurements

Hospitalist programHigh-risk clinicHome care programFacility case mgmt. Behavioral HealthDiabetes Disease mgmt.COPD complex care mgmt.CHF complex care mgmt.ESRD programUrgent care centersHealth educationPalliative care programHospice programChest pain care mgmt. program

©2014 Trinity Health. All Rights Reserved. 37

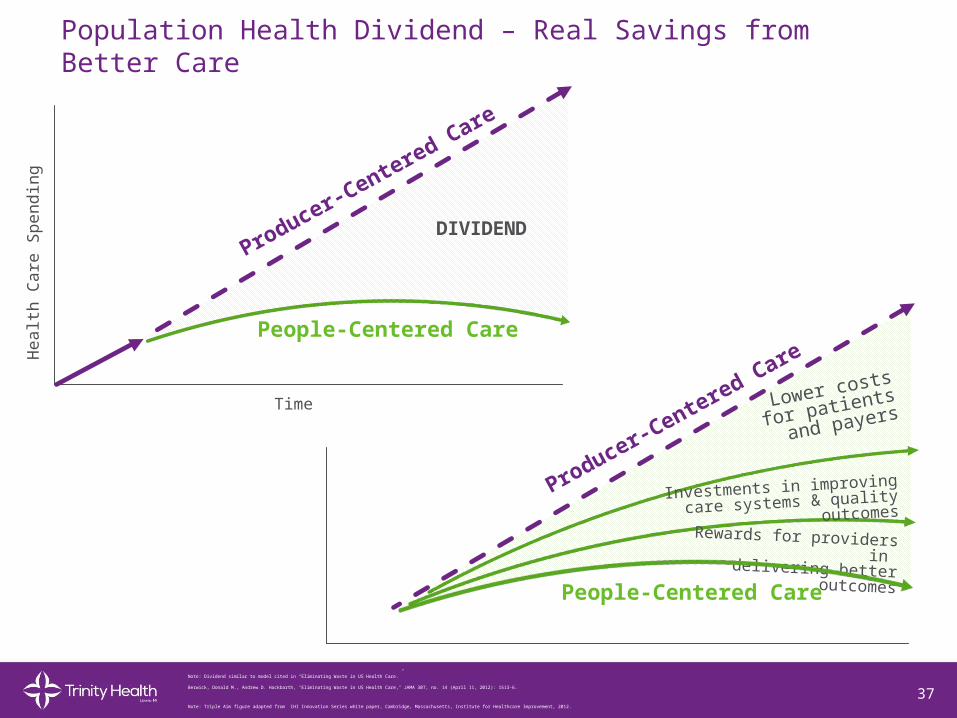

Population Health Dividend – Real Savings from Better Care

37

Producer-Centered Care

People-Centered Care

Time

He

alth

Ca

re S

pe

nd

ing

DIVIDEND

Note: Dividend similar to model cited in “Eliminating Waste in US Health Care.”

Berwick, Donald M., Andrew D. Hackbarth, "Eliminating Waste in US Health Care," JAMA 307, no. 14 (April 11, 2012): 1513-6.

Investments in improving

care systems & quality outcomes

Rewards for providers in delivering better outcomes

Producer-Centered Care

People-Centered Care

Lower costs for

patients and

payers

Note: Triple Aim figure adapted from IHI Innovation Series white paper, Cambridge, Massachusetts, Institute for Healthcare Improvement, 2012.

©2014 Trinity Health. All Rights Reserved. 38

2016 2018 2020

30% ? 50% ? 75%

75% of contracts to be value-based by 2020

Trinity Health Goal

©2015 Trinity Health - Livonia, MI 38