new regulatory framework of the mexican financial system jaime gonzález aguadé chairman cnbv 1

TRANSCRIPT

New regulatory framework of the Mexican Financial System

Jaime González AguadéChairman CNBV

1

2

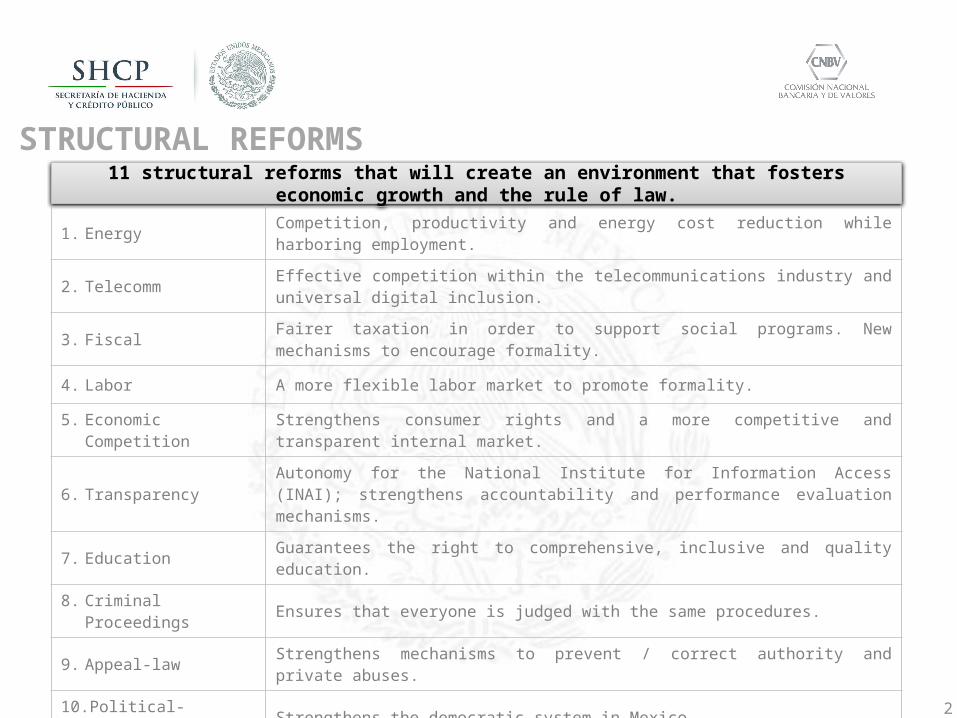

11 structural reforms that will create an environment that fosters economic growth and the rule of law.

1. Energy Competition, productivity and energy cost reduction while harboring employment.

2. Telecomm Effective competition within the telecommunications industry and universal digital inclusion.

3. Fiscal Fairer taxation in order to support social programs. New mechanisms to encourage formality.

4. Labor A more flexible labor market to promote formality.

5. Economic Competition Strengthens consumer rights and a more competitive and transparent internal market.

6. Transparency Autonomy for the National Institute for Information Access (INAI); strengthens accountability and performance evaluation mechanisms.

7. Education Guarantees the right to comprehensive, inclusive and quality education.

8. Criminal Proceedings Ensures that everyone is judged with the same procedures.

9. Appeal-law Strengthens mechanisms to prevent / correct authority and private abuses.

10. Political- Electoral Strengthens the democratic system in Mexico.

11. Financial Creates conditions for households and businesses in Mexico to access credit at cheaper cost.

STRUCTURAL REFORMS

3

3

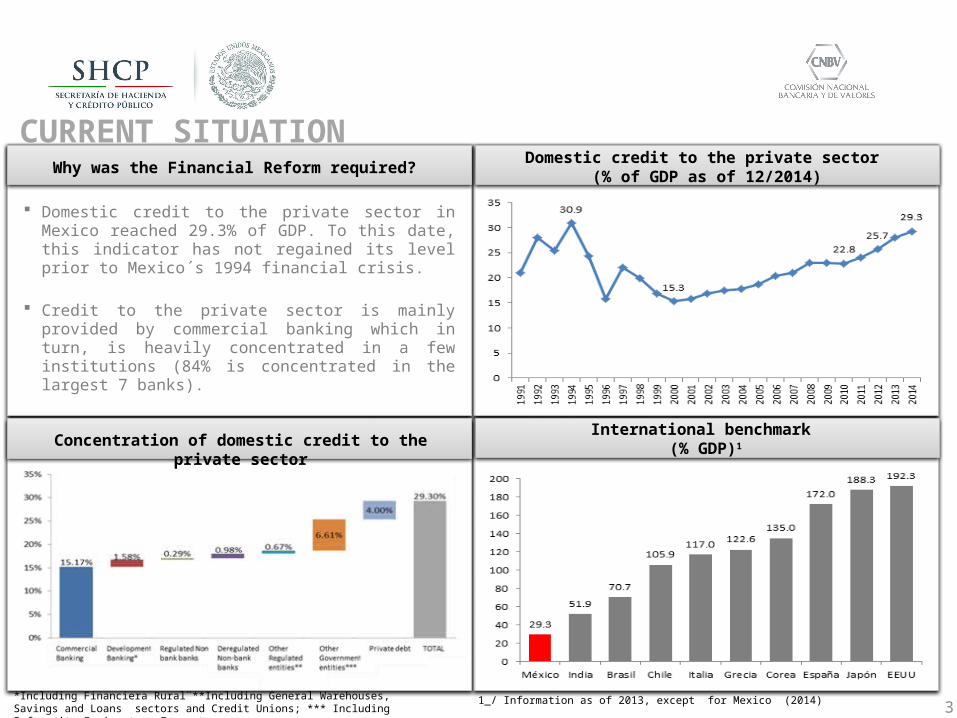

Domestic credit to the private sector (% of GDP as of 12/2014)

1_/ Information as of 2013, except for Mexico (2014)

CURRENT SITUATION

International benchmark (% GDP)1

*Including Financiera Rural¨**Including General Warehouses, Savings and Loans sectors and Credit Unions; *** Including Infonavit, Fovissste y Fonacot.

Why was the Financial Reform required?

Domestic credit to the private sector in Mexico reached 29.3% of GDP. To this date, this indicator has not regained its level prior to Mexico´s 1994 financial crisis.

Credit to the private sector is mainly provided by commercial banking which in turn, is heavily concentrated in a few institutions (84% is concentrated in the largest 7 banks).

Internationally, Mexico stands below peer countries (Chile, Brazil, India).

Concentration of domestic credit to the private sector

IPC in units

CURRENT SITUATION

Value and number of securities issued

Why was the financial reform required?

The IPC Index fluctuated between 37,500 and 46,000 units over the last 2 years.

The number of listed companies has remained virtually static, reaching 140.

In the last four years, 346 securities offerings are authorized on average, mainly concentrated in the debt market.

The value of the Mexican market capitalization to GDP is 44%, ranking below other peer economies.

Listed companies

35,000

37,000

39,000

41,000

43,000

45,000

47,000

2/1/13 2/4/13 2/7/13 2/10/13 2/1/14 2/4/14 2/7/14 2/10/14 2/1/15 2/4/15

2013 2014 2015

# Emisoras 134 140 140

Market Capitalization in million USD $508,856 $544,648 $485,045*

Traded value in million USD $143,030 $187,257 $40,828

Average daily trade in million USD $572 $749 $669

Includes CKDs, FIBRAS, securitizations, structured notes, medium and long term debt , stocks and derivatives.

* Peso depreciation of 5.5% vs USD.

5

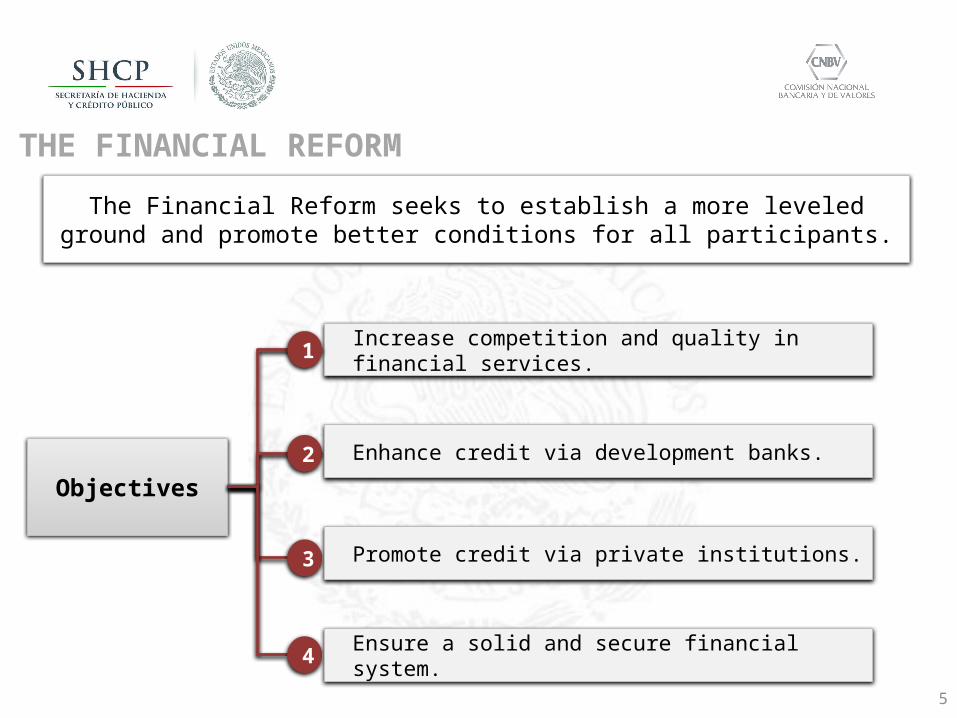

THE FINANCIAL REFORM

The Financial Reform seeks to establish a more leveled ground and promote better conditions for all participants.

Objectives

Increase competition and quality in financial services.1

2

3

4

Enhance credit via development banks.

Promote credit via private institutions.

Ensure a solid and secure financial system.

6

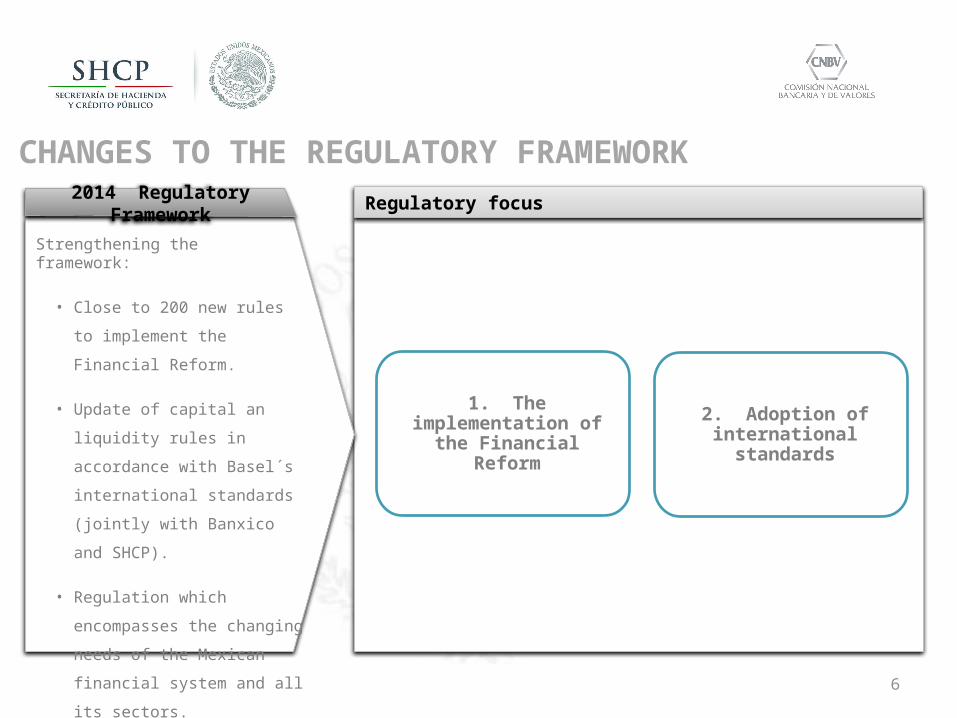

1. The implementation of the Financial Reform

2. Adoption of international standards

Regulatory focus

Strengthening the framework:

• Close to 200 new rules to

implement the Financial Reform.

• Update of capital an liquidity rules

in accordance with Basel´s

international standards (jointly

with Banxico and SHCP).

• Regulation which encompasses the

changing needs of the Mexican

financial system and all its sectors.

This effort resulted in 300 changes to the

regulatory framework during 2014.

2014 Regulatory Framework

CHANGES TO THE REGULATORY FRAMEWORK

7

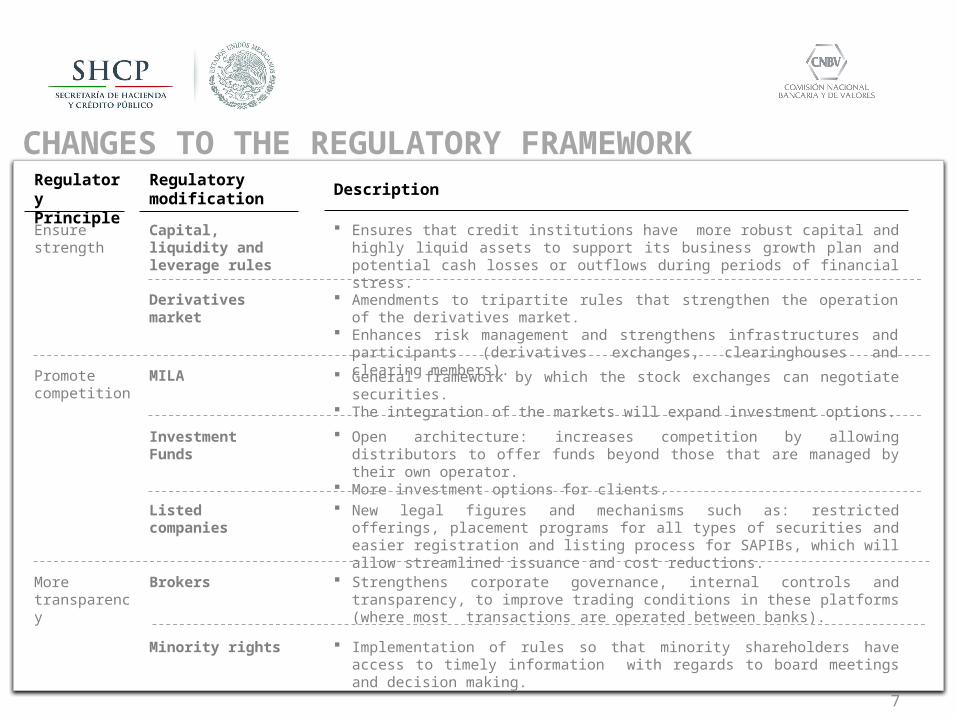

CHANGES TO THE REGULATORY FRAMEWORKRegulatory Principle

Regulatory modification Description

Ensure strength

Capital, liquidity and leverage rules

Ensures that credit institutions have more robust capital and highly liquid assets to support its business growth plan and potential cash losses or outflows during periods of financial stress.

Promote competition

Listed companies New legal figures and mechanisms such as: restricted offerings, placement programs for all types of securities and easier registration and listing process for SAPIBs, which will allow streamlined issuance and cost reductions.

Investment Funds Open architecture: increases competition by allowing distributors to offer funds beyond those that are managed by their own operator.

More investment options for clients.

Derivatives market Amendments to tripartite rules that strengthen the operation of the derivatives market. Enhances risk management and strengthens infrastructures and participants (derivatives

exchanges, clearinghouses and clearing members).

MILA General framework by which the stock exchanges can negotiate securities. The integration of the markets will expand investment options.

More transparency

Brokers Strengthens corporate governance, internal controls and transparency, to improve trading conditions in these platforms (where most transactions are operated between banks).

Minority rights Implementation of rules so that minority shareholders have access to timely information with regards to board meetings and decision making.

7

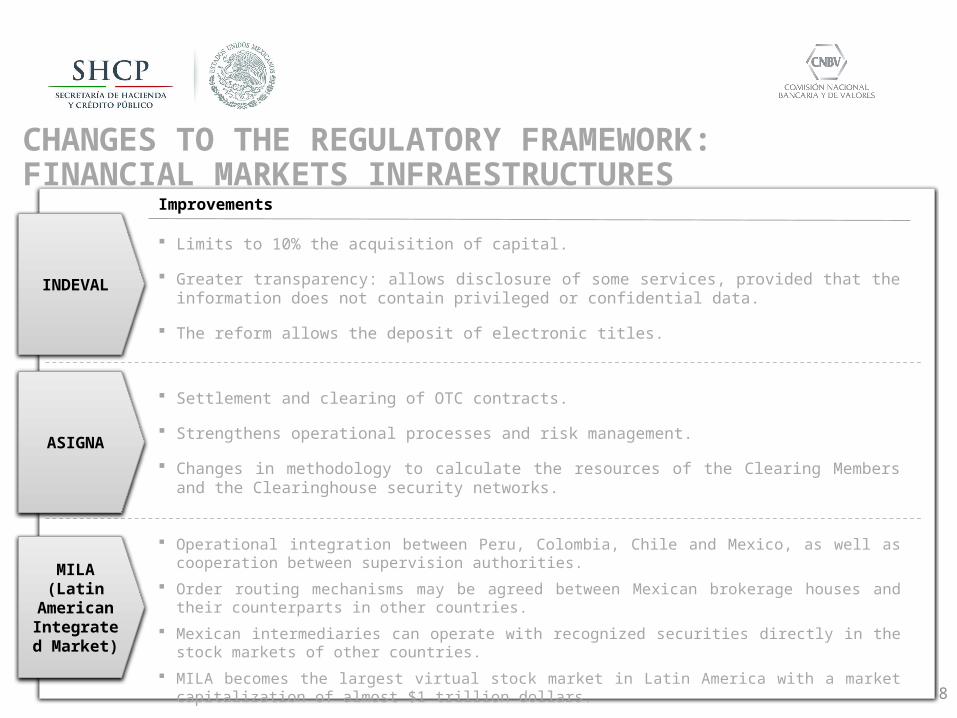

Limits to 10% the acquisition of capital.

Greater transparency: allows disclosure of some services, provided that the information does not contain privileged or confidential data.

The reform allows the deposit of electronic titles.

Improvements

INDEVAL

ASIGNA

MILA (Latin American Integrated

Market)

Settlement and clearing of OTC contracts.

Strengthens operational processes and risk management.

Changes in methodology to calculate the resources of the Clearing Members and the Clearinghouse security networks.

Operational integration between Peru, Colombia, Chile and Mexico, as well as cooperation between supervision authorities.

Order routing mechanisms may be agreed between Mexican brokerage houses and their counterparts in other countries.

Mexican intermediaries can operate with recognized securities directly in the stock markets of other countries.

MILA becomes the largest virtual stock market in Latin America with a market capitalization of almost $1 trillion dollars.

CHANGES TO THE REGULATORY FRAMEWORK: FINANCIAL MARKETS INFRAESTRUCTURES

8

9

1. In recent years, Mexico has adopted the best international practices that will lay the grounds for the development of the financial system.

2. In particular, the Financial Reform has established flexible mechanisms for securities registration and trade, aimed to reduce the complexity and cost of such processes.

3. The challenge ahead is to ensure that intermediaries properly adopt the new regulation so that the results are achieved in the markets.

4. We will continue working on the modernization of the regulatory framework to provide depth and soundness to the market.

CLOSING REMARKS