new jersey department of transportation, in-house lecture series, trenton, september 24, 2008...

TRANSCRIPT

New Jersey Department of Transportation, In-House New Jersey Department of Transportation, In-House Lecture Series, Trenton, September 24, 2008Lecture Series, Trenton, September 24, 2008

Transportation and Oil Prices: Transportation and Oil Prices: From Modal Shift to Supply Chain From Modal Shift to Supply Chain PropagationPropagation

Jean-Paul RodrigueAssociate ProfessorDept. of Global Studies & GeographyHofstra UniversityNew York, USA

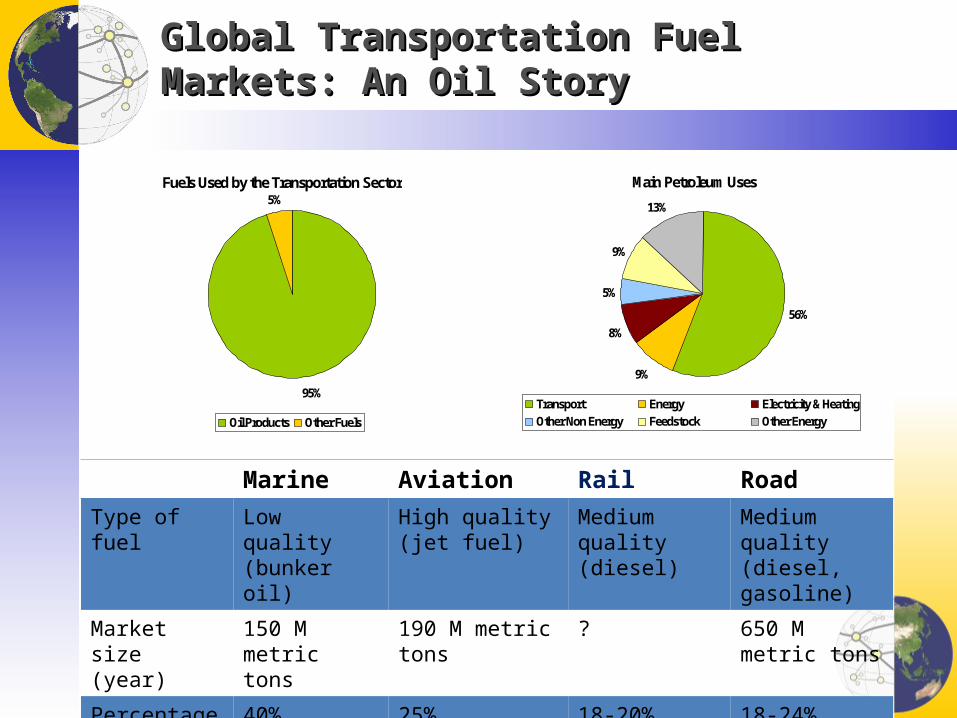

Global Transportation Fuel Markets: An Oil StoryGlobal Transportation Fuel Markets: An Oil Story

Fuels Used by the Transportation Sector

95%

5%

Oil Products Other Fuels

Main Petroleum Uses

56%

9%

8%

5%

9%

13%

Transport Energy Electricity & Heating

Other Non Energy Feedstock Other Energy

Marine Aviation Rail Road

Type of fuel Low quality (bunker oil)

High quality (jet fuel) Medium quality (diesel)

Medium quality (diesel, gasoline)

Market size (year)

150 M metric tons

190 M metric tons ? 650 M metric tons

Percentage of operating costs

40% 25% 18-20% 18-24%

The Peak Oil Debate: Doomsayers and NutjobsThe Peak Oil Debate: Doomsayers and Nutjobs

■ Doomsayers• Often the firsts to anticipate a paradigm shift.• Understand the trend and its potential consequences.• Exaggerate the outcome, often through linear inference.• Fail (or refuse) to consider positive feedback effects (e.g.

technology and conservation) and the complexity of economic systems.

■ Nutjobs• Blow things out of proportion, often taking advantage of an

event to seek media attention.• Dogmatism (conspiracies) over analysis.• Almost always make the wrong assessment.• Short shelf life (but keep coming back…).

Demystifying Conspiracy TheoriesDemystifying Conspiracy Theories

■ We are running out of oil• We are running out of cheap oil options.

■ OPEC fixes oil prices• A dysfunctional cartel that can do little.• Each member does mostly want it wants.• Statements should be viewed as comic relief (e.g. Chavez).

■ Speculation drives oil prices• Somewhat (short term), but many can also lose their shirts.

■ High oil prices paralyze transportation• Not really.• Low oil prices promotes wasteful practices.• High oil prices force a reconsideration and a default in

unsustainable practices.

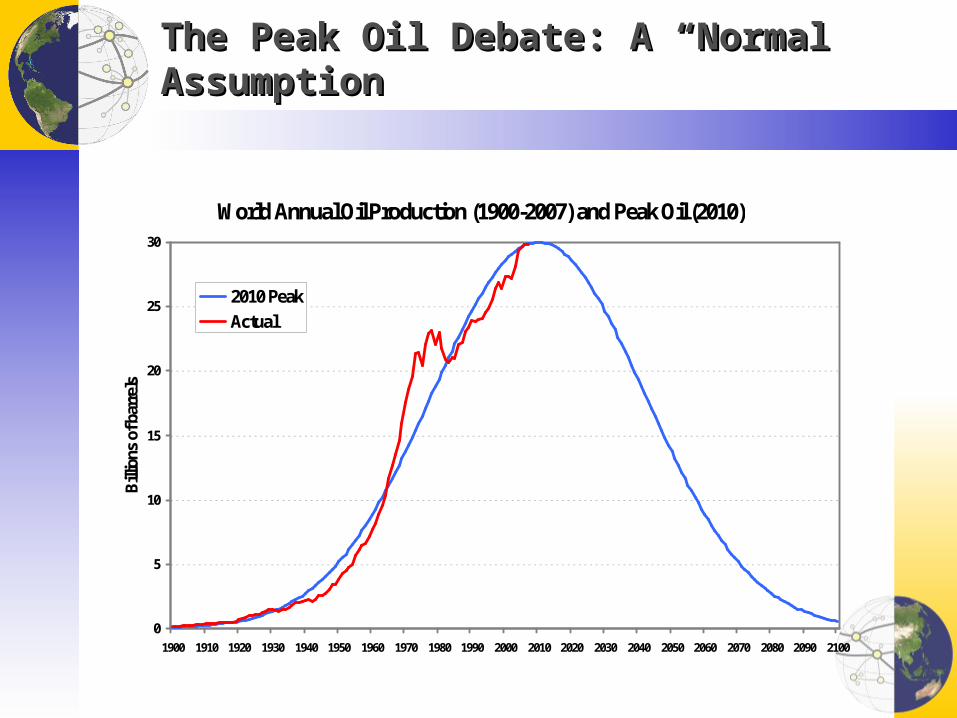

The Peak Oil Debate: A “Normal” AssumptionThe Peak Oil Debate: A “Normal” Assumption

World Annual Oil Production (1900-2007) and Peak Oil (2010)

0

5

10

15

20

25

30

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

Bill

ions

of b

arre

ls

2010 Peak

Actual

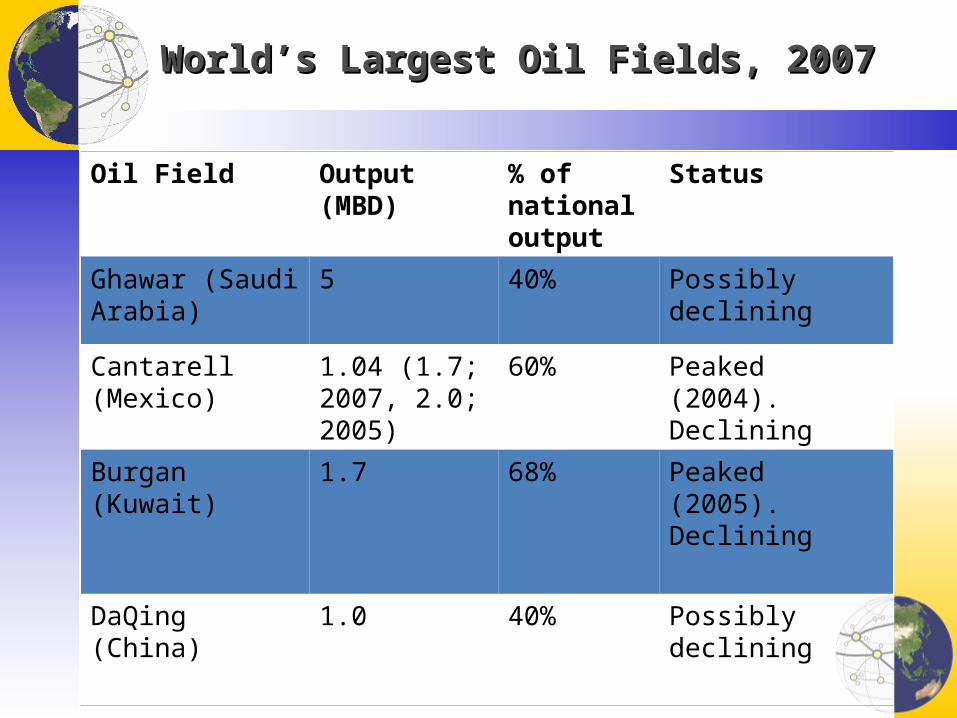

World’s Largest Oil Fields, 2007World’s Largest Oil Fields, 2007

Oil Field Output (MBD) % of national output

Status

Ghawar (Saudi Arabia)

5 40% Possibly declining

Cantarell (Mexico) 1.04 (1.7; 2007, 2.0; 2005)

60% Peaked (2004). Declining

Burgan (Kuwait) 1.7 68% Peaked (2005). Declining

DaQing (China) 1.0 40% Possibly declining

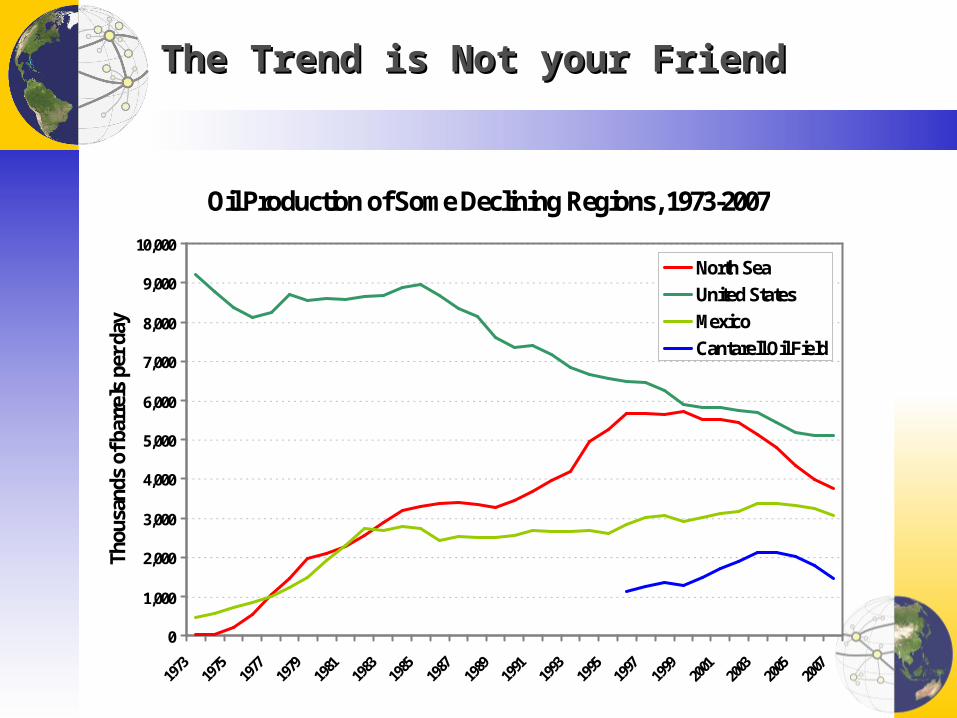

The Trend is Not your FriendThe Trend is Not your Friend

Oil Production of Some Declining Regions, 1973-2007

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Thou

sand

s of

bar

rels

per

day

North Sea

United States

Mexico

Cantarell Oil Field

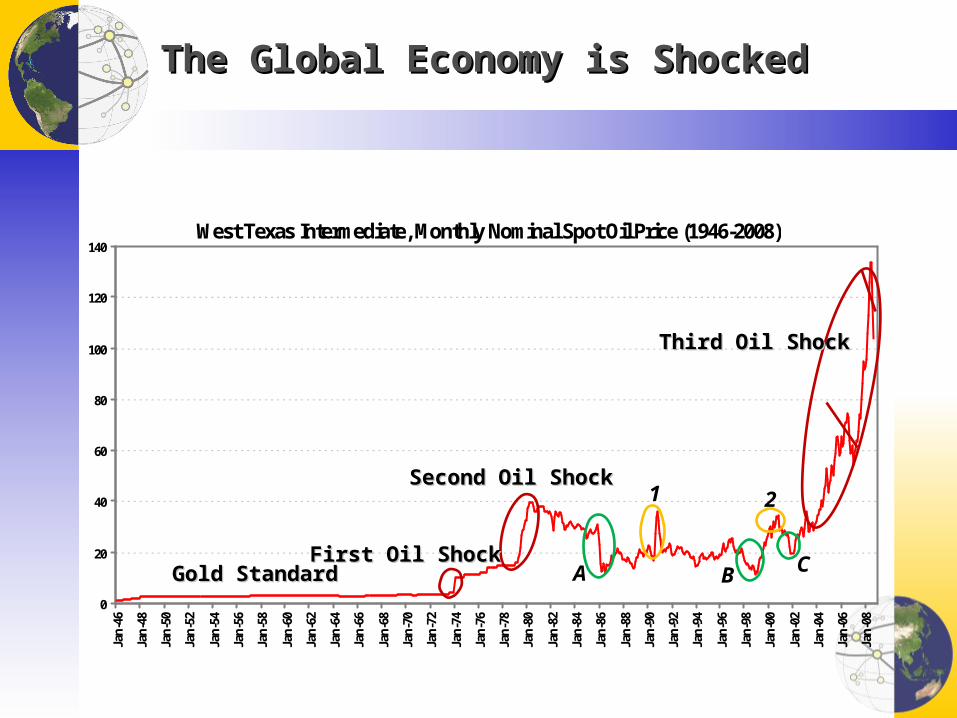

The Global Economy is ShockedThe Global Economy is Shocked

West Texas Intermediate, Monthly Nominal Spot Oil Price (1946-2008)

0

20

40

60

80

100

120

140

Jan-

46

Jan-

48

Jan-

50

Jan-

52

Jan-

54

Jan-

56

Jan-

58

Jan-

60

Jan-

62

Jan-

64

Jan-

66

Jan-

68

Jan-

70

Jan-

72

Jan-

74

Jan-

76

Jan-

78

Jan-

80

Jan-

82

Jan-

84

Jan-

86

Jan-

88

Jan-

90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Jan-

04

Jan-

06

Jan-

08

Gold StandardGold StandardFirst Oil ShockFirst Oil Shock

Second Oil ShockSecond Oil Shock

Third Oil ShockThird Oil Shock

A B C

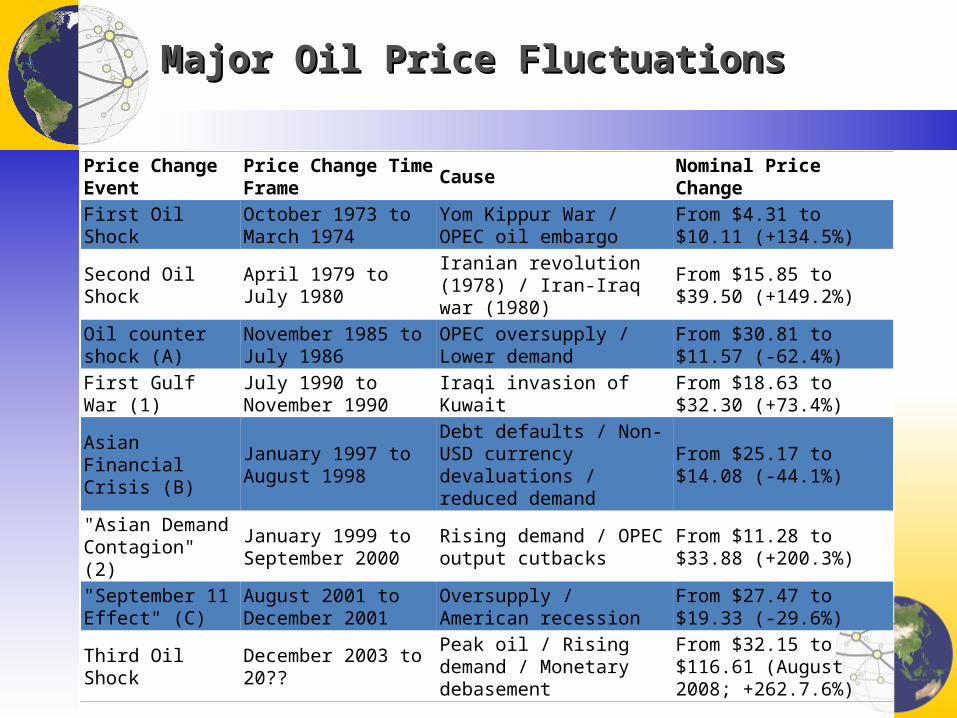

21

Major Oil Price FluctuationsMajor Oil Price Fluctuations

Price Change Event Price Change Time Frame Cause Nominal Price Change

First Oil Shock October 1973 to March 1974

Yom Kippur War / OPEC oil embargo

From $4.31 to $10.11 (+134.5%)

Second Oil Shock April 1979 to July 1980 Iranian revolution (1978) / Iran-Iraq war (1980)

From $15.85 to $39.50 (+149.2%)

Oil counter shock (A) November 1985 to July 1986

OPEC oversupply / Lower demand

From $30.81 to $11.57 (-62.4%)

First Gulf War (1) July 1990 to November 1990 Iraqi invasion of Kuwait From $18.63 to $32.30

(+73.4%)

Asian Financial Crisis (B)

January 1997 to August 1998

Debt defaults / Non-USD currency devaluations / reduced demand

From $25.17 to $14.08 (-44.1%)

"Asian Demand Contagion" (2)

January 1999 to September 2000

Rising demand / OPEC output cutbacks

From $11.28 to $33.88 (+200.3%)

"September 11 Effect" (C)

August 2001 to December 2001 Oversupply / American recession From $27.47 to $19.33 (-

29.6%)

Third Oil Shock December 2003 to 20?? Peak oil / Rising demand / Monetary debasement

From $32.15 to $116.61 (August 2008; +262.7.6%)

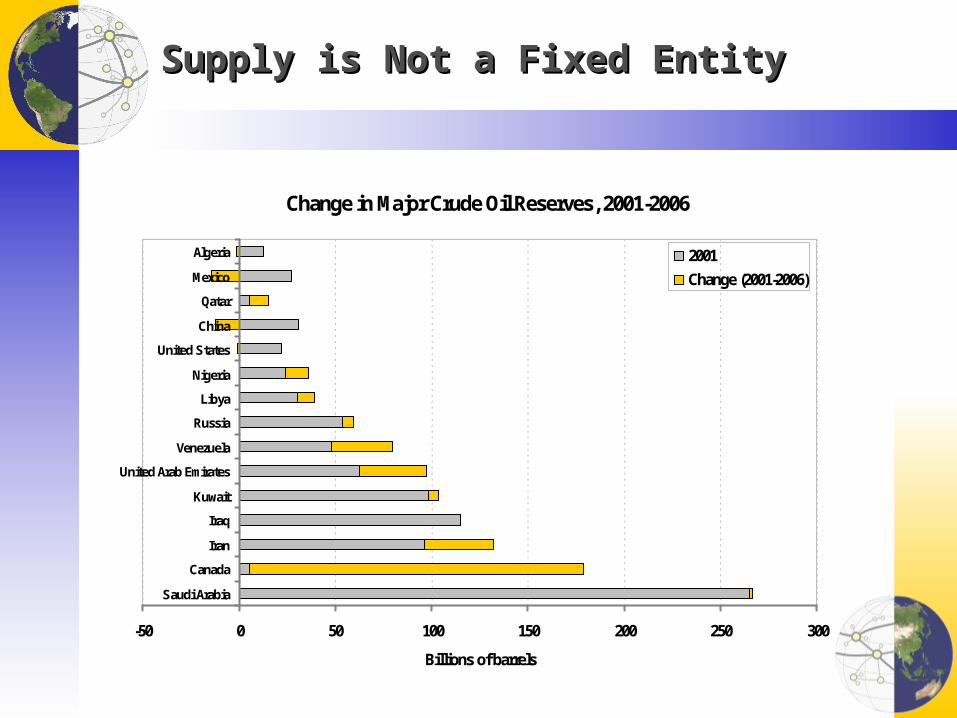

Supply is Not a Fixed EntitySupply is Not a Fixed Entity

Change in Major Crude Oil Reserves, 2001-2006

-50 0 50 100 150 200 250 300

Saudi Arabia

Canada

Iran

Iraq

Kuwait

United Arab Emirates

Venezuela

Russia

Libya

Nigeria

United States

China

Qatar

Mexico

Algeria

Billions of barrels

2001

Change (2001-2006)

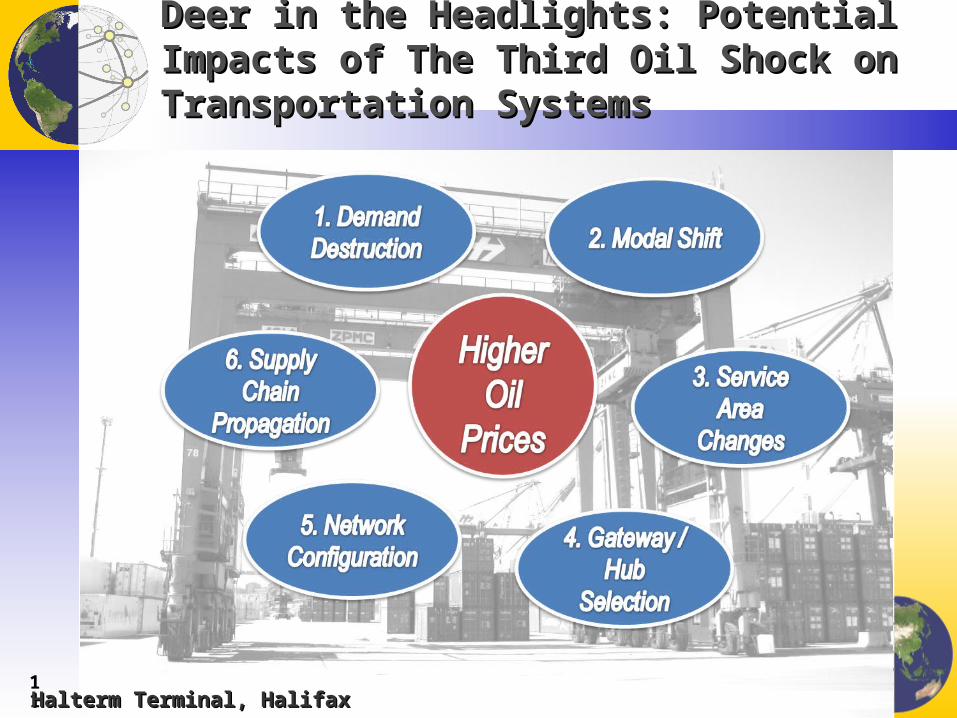

Deer in the Headlights: Potential Impacts of The Deer in the Headlights: Potential Impacts of The Third Oil Shock on Transportation SystemsThird Oil Shock on Transportation Systems

11Halterm Terminal, HalifaxHalterm Terminal, Halifax

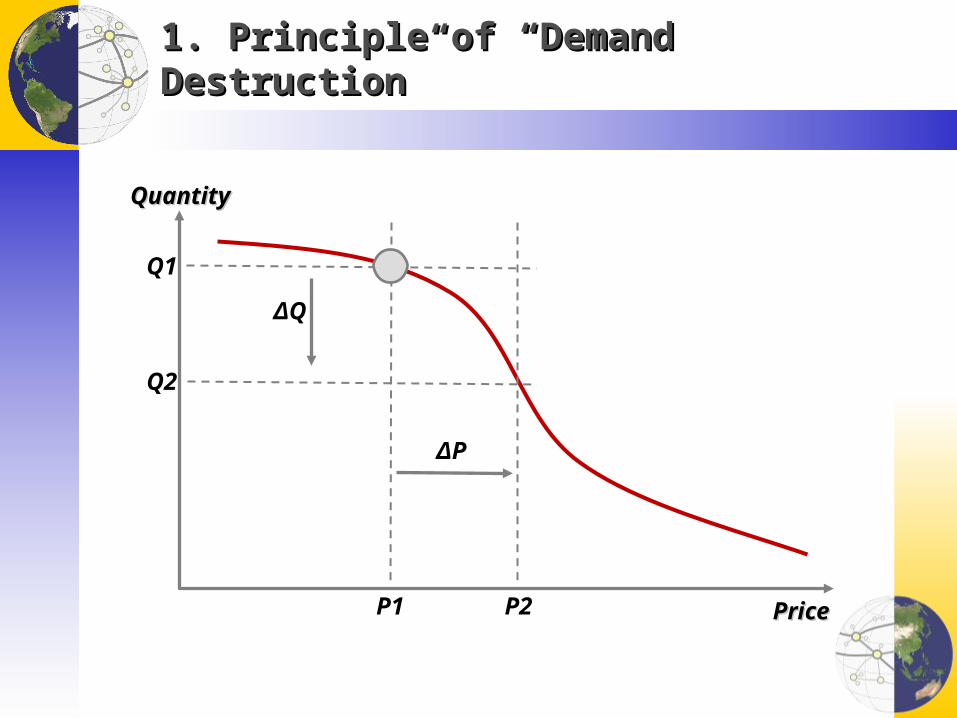

1. Principle of “Demand Destruction”1. Principle of “Demand Destruction”

PricePrice

QuantityQuantity

P1

ΔP

P2

Q1

ΔQ

Q2

Annual Vehicle-Miles Traveled and Year-over-Year Annual Vehicle-Miles Traveled and Year-over-Year Changes (Peak Mobility?)Changes (Peak Mobility?)

Recession

End of the motorization cycleSlow down of suburbanizationAging of the population

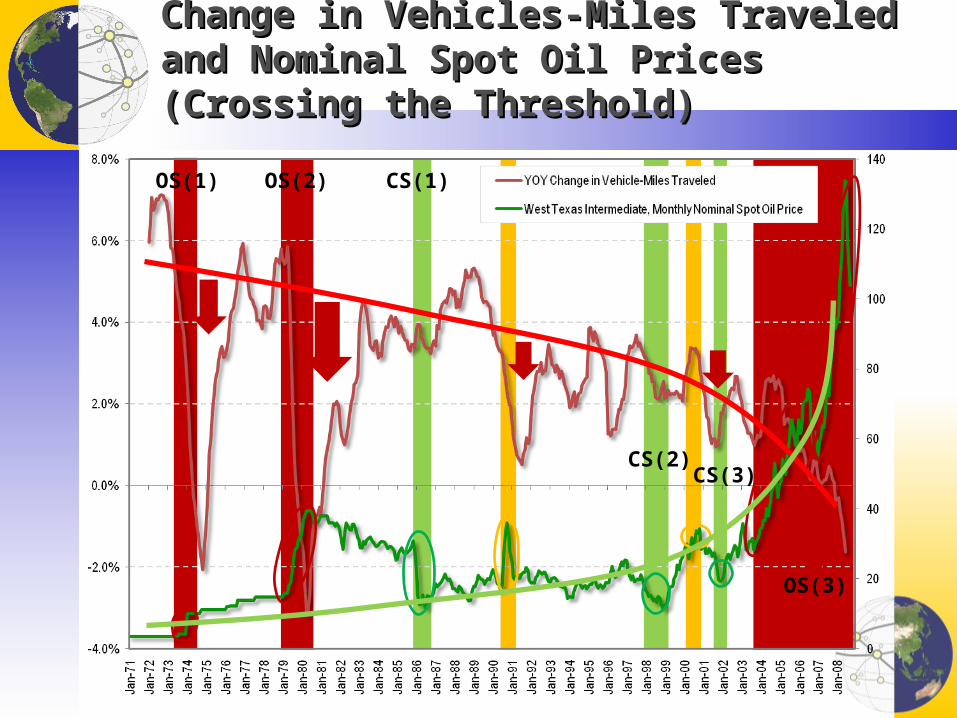

Change in Vehicles-Miles Traveled and Nominal Spot Change in Vehicles-Miles Traveled and Nominal Spot Oil Prices (Crossing the Threshold)Oil Prices (Crossing the Threshold)

OS(1) OS(2)

OS(3)

CS(1)

CS(2)CS(3)

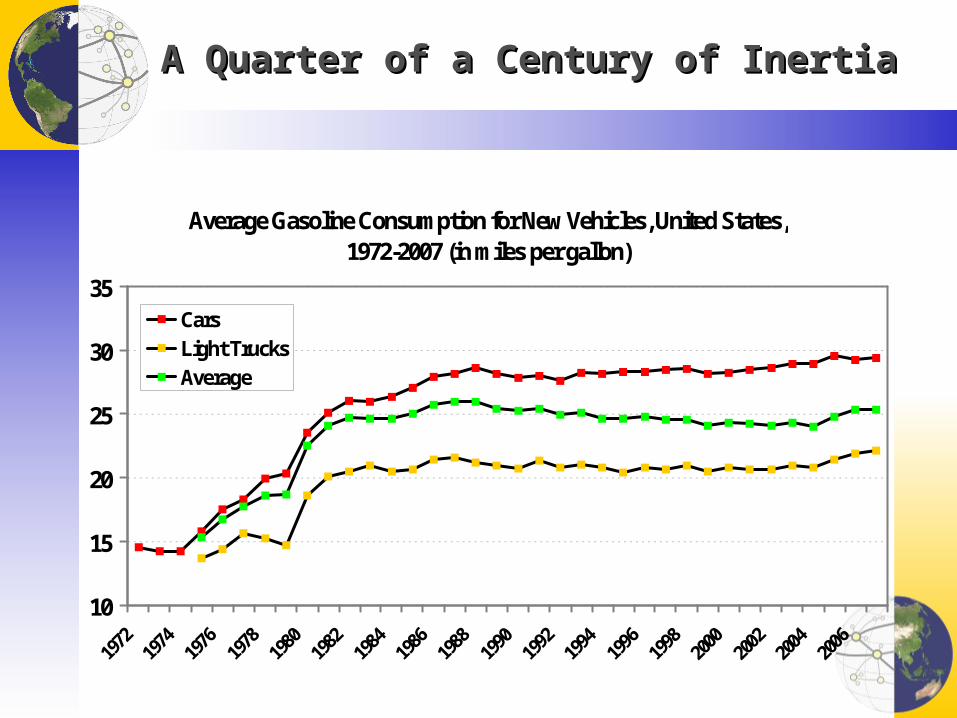

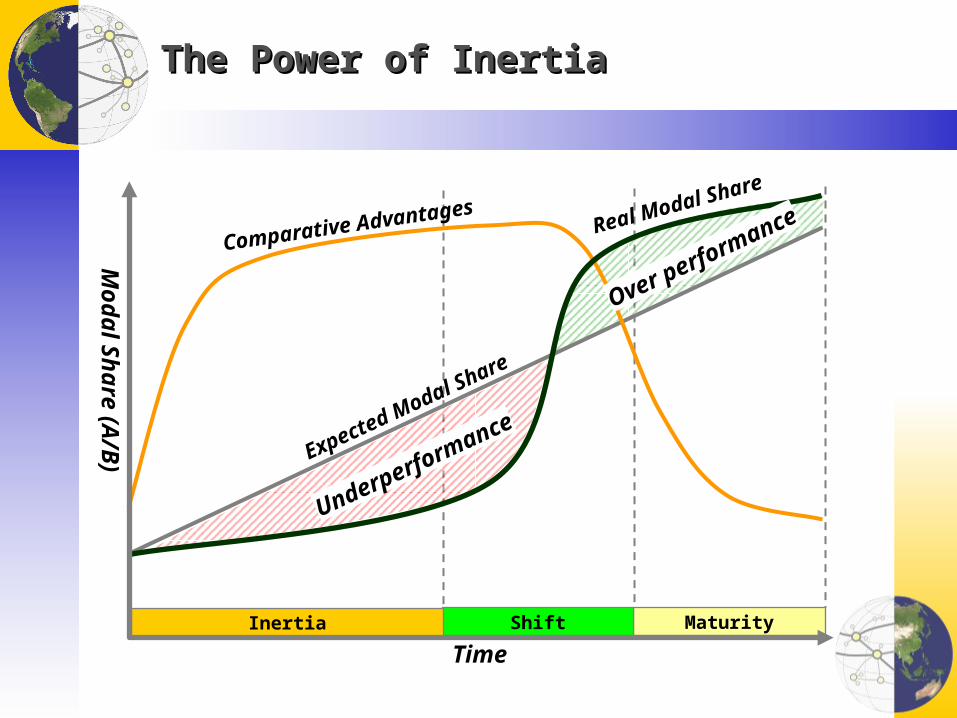

A Quarter of a Century of InertiaA Quarter of a Century of Inertia

Average Gasoline Consumption for New Vehicles, United States, 1972-2007 (in miles per gallon)

10

15

20

25

30

35

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

CarsLight TrucksAverage

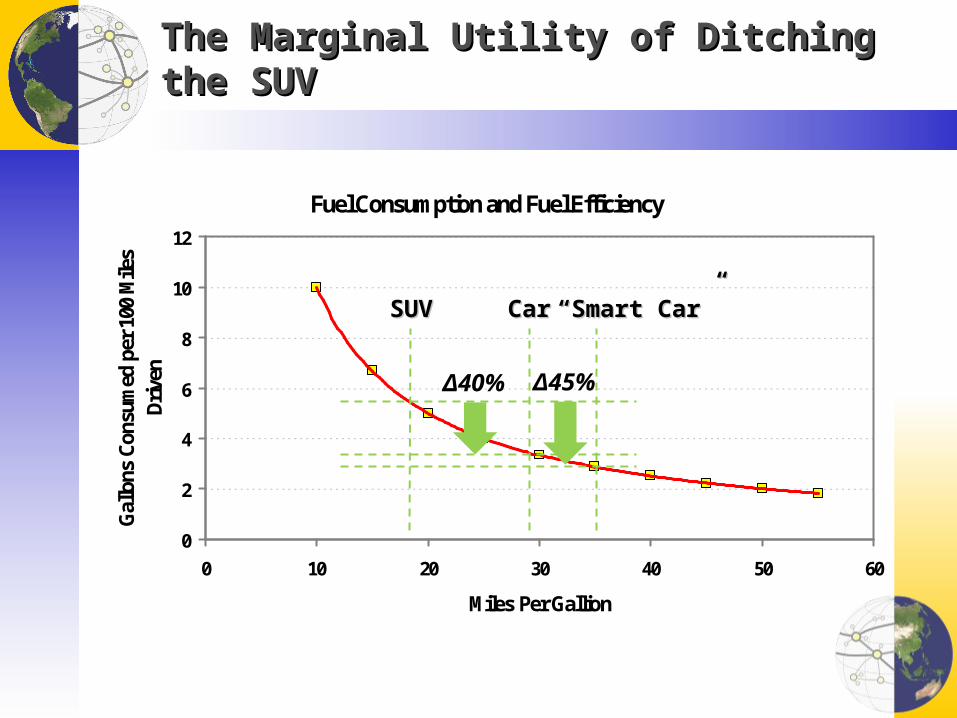

The Marginal Utility of Ditching the SUVThe Marginal Utility of Ditching the SUV

Fuel Consumption and Fuel Efficiency

0

2

4

6

8

10

12

0 10 20 30 40 50 60

Miles Per Gallion

Gal

lons

Con

sum

ed p

er 1

00 M

iles

Dri

ven

SUVSUV CarCar ““Smart Car”Smart Car”

Δ40% Δ45%

Air Transportation Has Some Room for SubstitutionAir Transportation Has Some Room for Substitution

Trend in Aircraft Fuel Efficiency (Fuel burned per Seat)

20

30

40

50

60

70

80

90

100

1955 1965 1975 1985 1995 2005

Year of Introduction

% o

f Bas

e (C

omet

4)

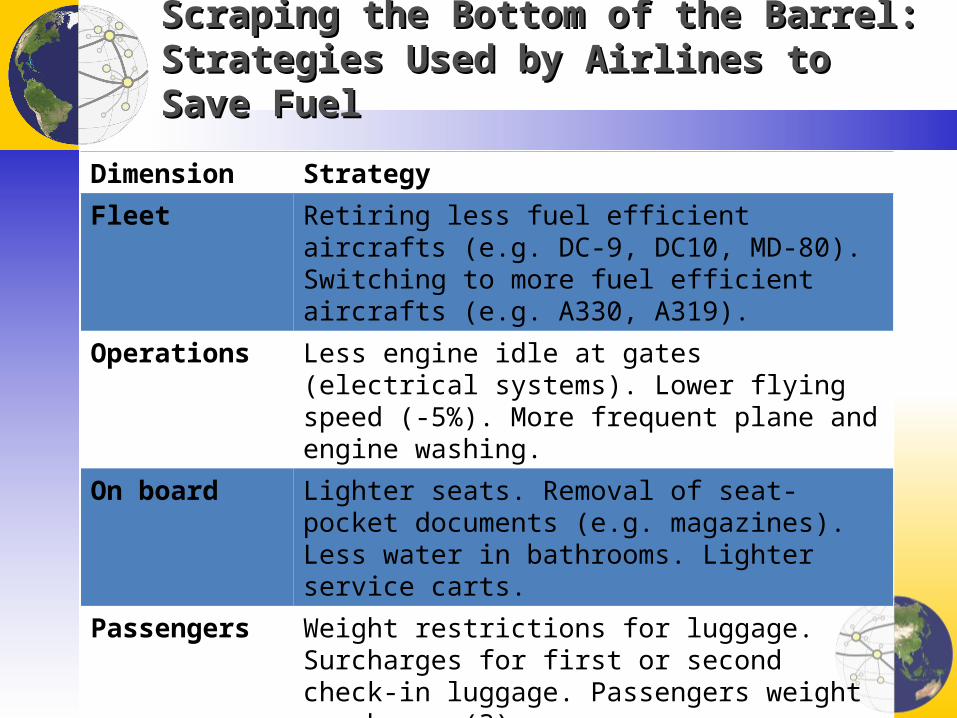

Scraping the Bottom of the Barrel: Strategies Used Scraping the Bottom of the Barrel: Strategies Used by Airlines to Save Fuelby Airlines to Save Fuel

Dimension Strategy

Fleet Retiring less fuel efficient aircrafts (e.g. DC-9, DC10, MD-80). Switching to more fuel efficient aircrafts (e.g. A330, A319).

Operations Less engine idle at gates (electrical systems). Lower flying speed (-5%). More frequent plane and engine washing.

On board Lighter seats. Removal of seat-pocket documents (e.g. magazines). Less water in bathrooms. Lighter service carts.

Passengers Weight restrictions for luggage. Surcharges for first or second check-in luggage. Passengers weight surcharges(?)

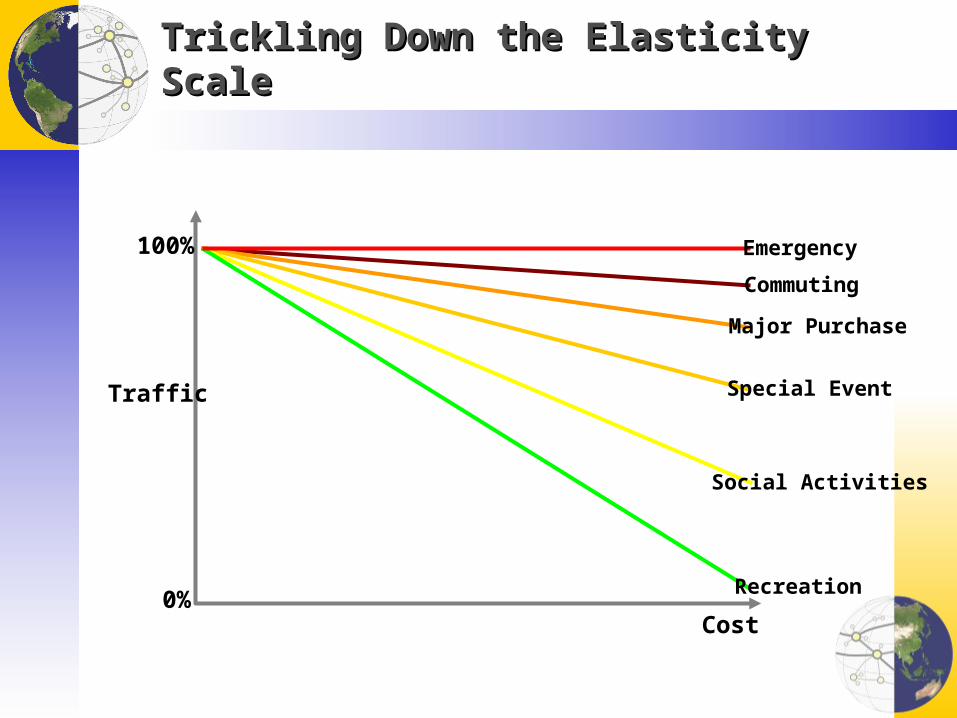

Trickling Down the Elasticity ScaleTrickling Down the Elasticity Scale

Traffic

Cost

100%

0%

Emergency

Commuting

Major Purchase

Special Event

Social Activities

Recreation

Differentials in Demand DestructionDifferentials in Demand Destruction

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10

Cost Level

Traf

fic

Shopping

Social / RecreationWork

Total trips

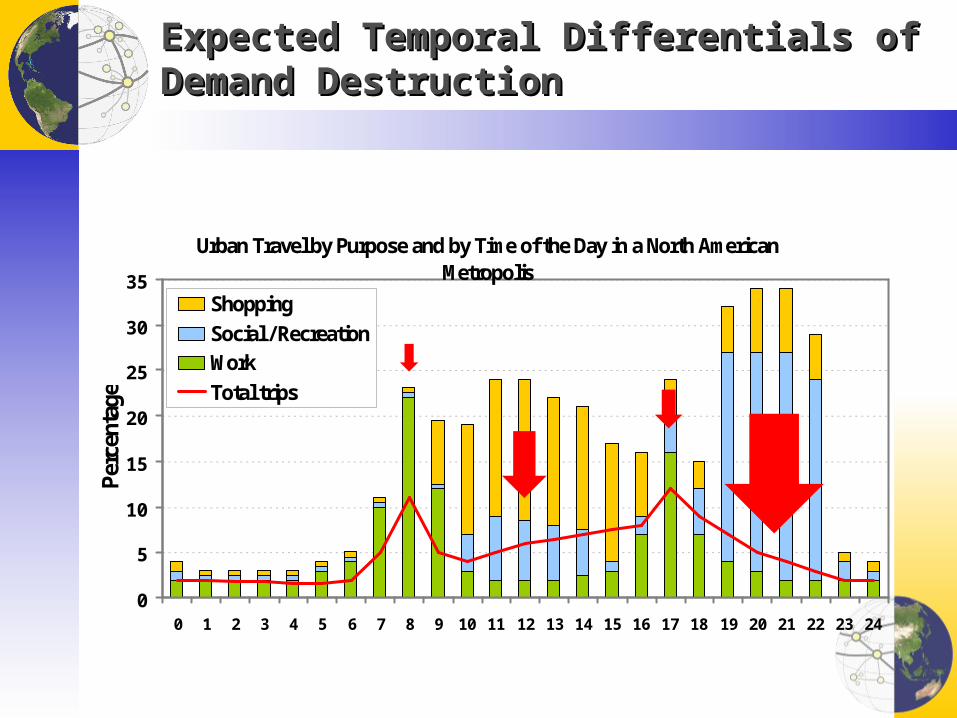

Expected Temporal Differentials of Demand Expected Temporal Differentials of Demand DestructionDestruction

Urban Travel by Purpose and by Time of the Day in a North American Metropolis

0

5

10

15

20

25

30

35

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Perc

enta

ge

Shopping

Social / RecreationWork

Total trips

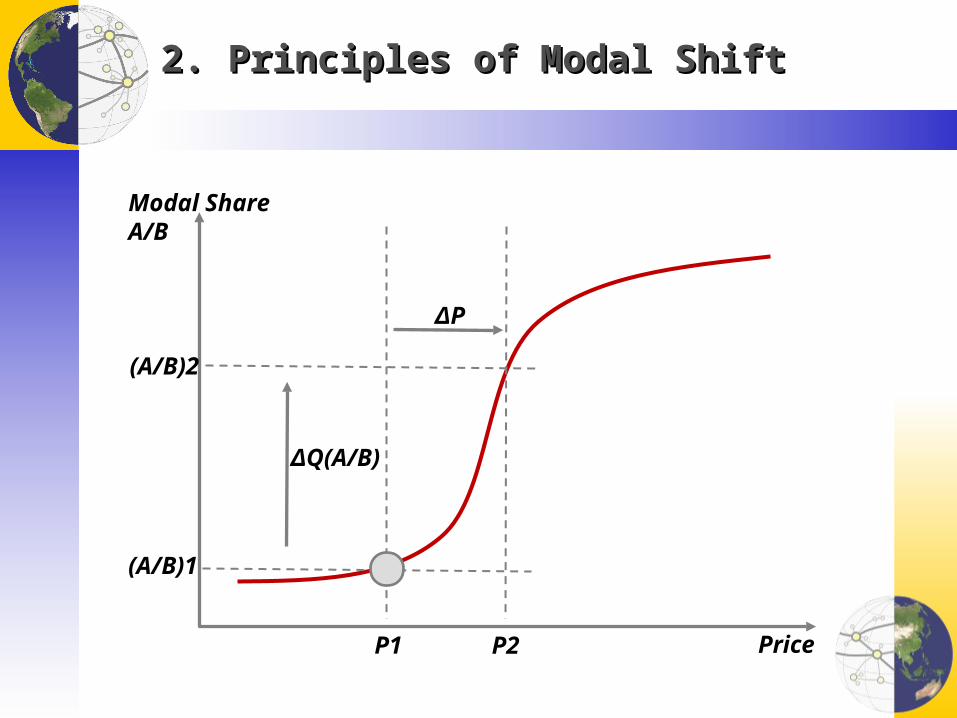

2. Principles of Modal Shift2. Principles of Modal Shift

Price

Modal ShareA/B

P1

ΔP

P2

(A/B)1

ΔQ(A/B)

(A/B)2

MaturityShiftInertia

The Power of InertiaThe Power of Inertia

Modal Share (A

/B)

Time

Comparative Advantages Real Modal Share

Expected Modal Share

Underperformance

Over performance

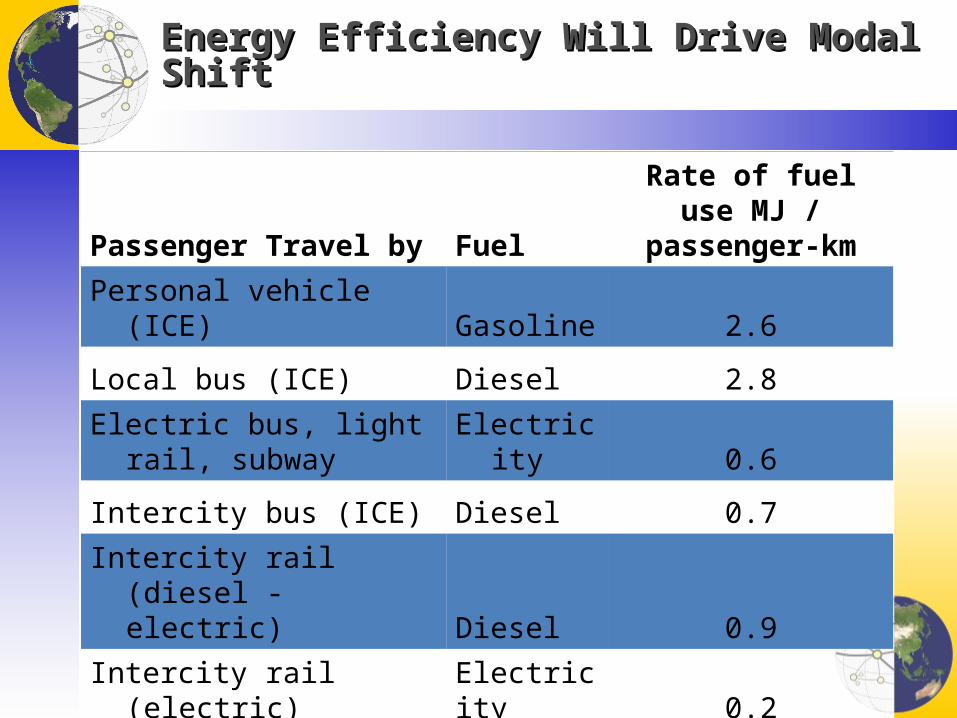

Energy Efficiency Will Drive Modal ShiftEnergy Efficiency Will Drive Modal Shift

Passenger Travel by FuelRate of fuel use MJ /

passenger-km

Personal vehicle (ICE) Gasoline 2.6

Local bus (ICE) Diesel 2.8

Electric bus, light rail, subway Electricity 0.6

Intercity bus (ICE) Diesel 0.7

Intercity rail (diesel - electric) Diesel 0.9

Intercity rail (electric) Electricity 0.2

High-speed rail (electric) Electricity 0.3

Aircraft (domestic) Kerosene 2.0

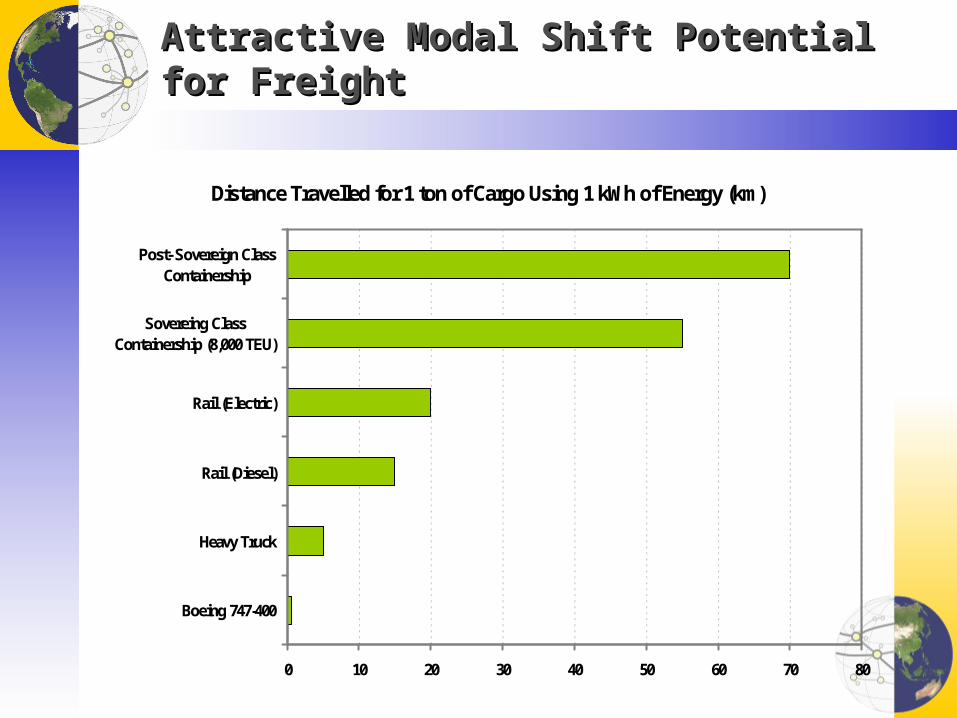

Attractive Modal Shift Potential for FreightAttractive Modal Shift Potential for Freight

Distance Travelled for 1 ton of Cargo Using 1 kWh of Energy (km)

0 10 20 30 40 50 60 70 80

Boeing 747-400

Heavy Truck

Rail (Diesel)

Rail (Electric)

Sovereing ClassContainership (8,000 TEU)

Post- Sovereign ClassContainership

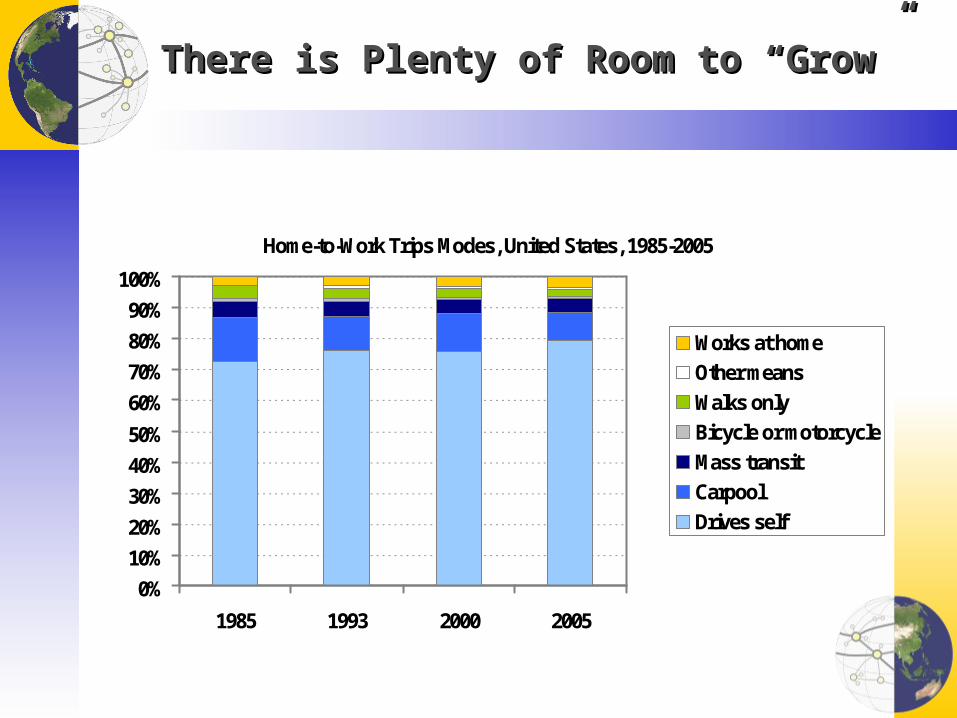

There is Plenty of Room to “Grow”There is Plenty of Room to “Grow”

Home-to-Work Trips Modes, United States, 1985-2005

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1985 1993 2000 2005

Works at home

Other means

Walks only

Bicycle or motorcycle

Mass transit

Carpool

Drives self

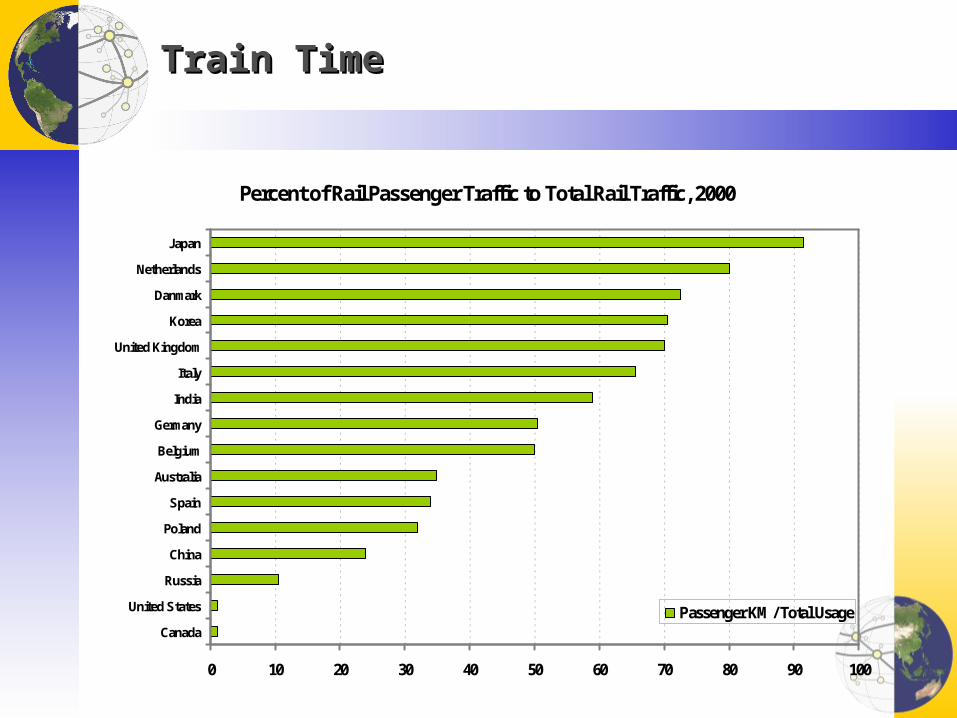

Train TimeTrain Time

Percent of Rail Passenger Traffic to Total Rail Traffic, 2000

0 10 20 30 40 50 60 70 80 90 100

Canada

United States

Russia

China

Poland

Spain

Australia

Belgium

Germany

India

Italy

United Kingdom

Korea

Danmark

Netherlands

Japan

Passenger KM / Total Usage

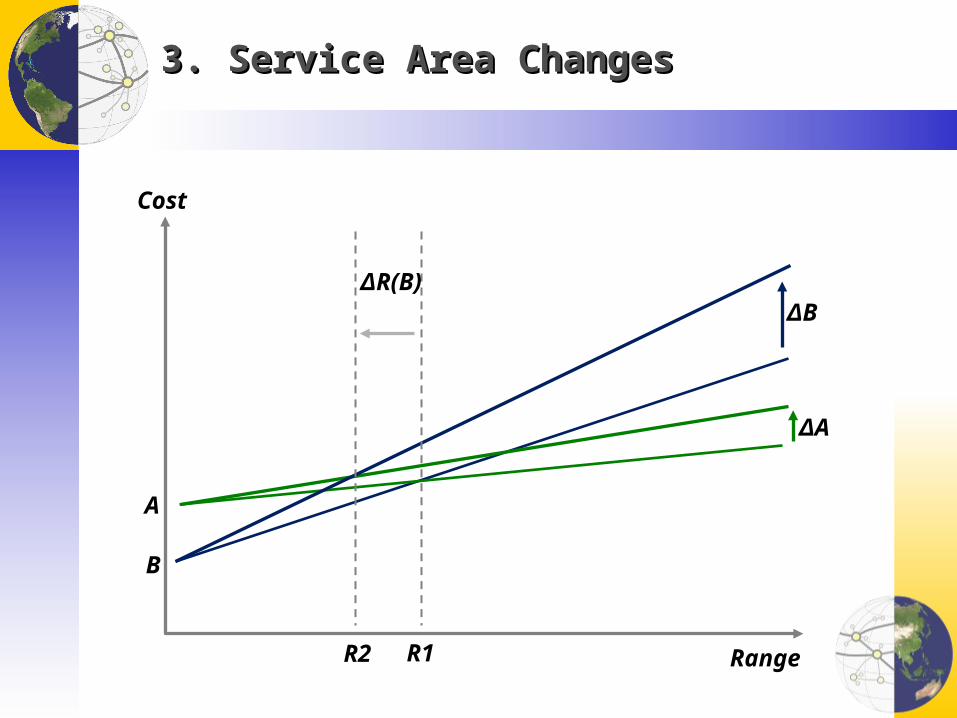

3. Service Area Changes3. Service Area Changes

Range

ΔA

ΔB

R1

Cost

ΔR(B)

R2

A

B

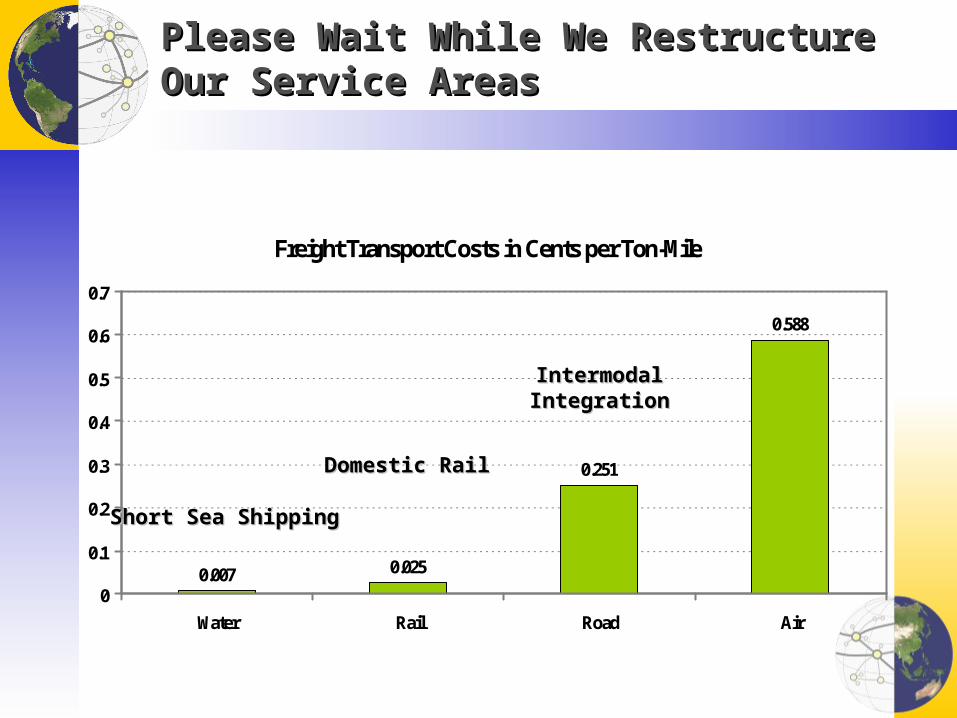

Please Wait While We Restructure Our Service AreasPlease Wait While We Restructure Our Service Areas

Freight Transport Costs in Cents per Ton-Mile

0.007 0.025

0.251

0.588

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Water Rail Road Air

Short Sea ShippingShort Sea Shipping

Domestic RailDomestic Rail

IntermodalIntermodalIntegrationIntegration

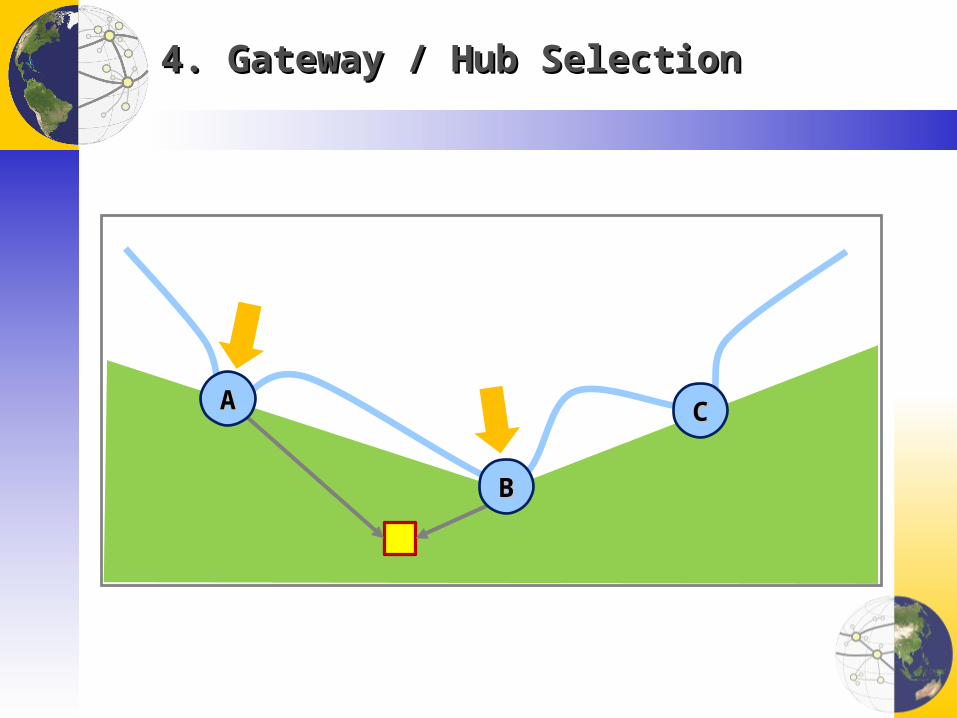

4. Gateway / Hub Selection4. Gateway / Hub Selection

BB

AA CC

Going Down the FunnelGoing Down the Funnel

Container Traffic Handled by Montreal and Halifax, 1981-2007 (TEU)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2007

2005

2003

2001

1999

1997

1995

1993

1991

1989

1987

1985

1983

1981

Halifax

Montreal

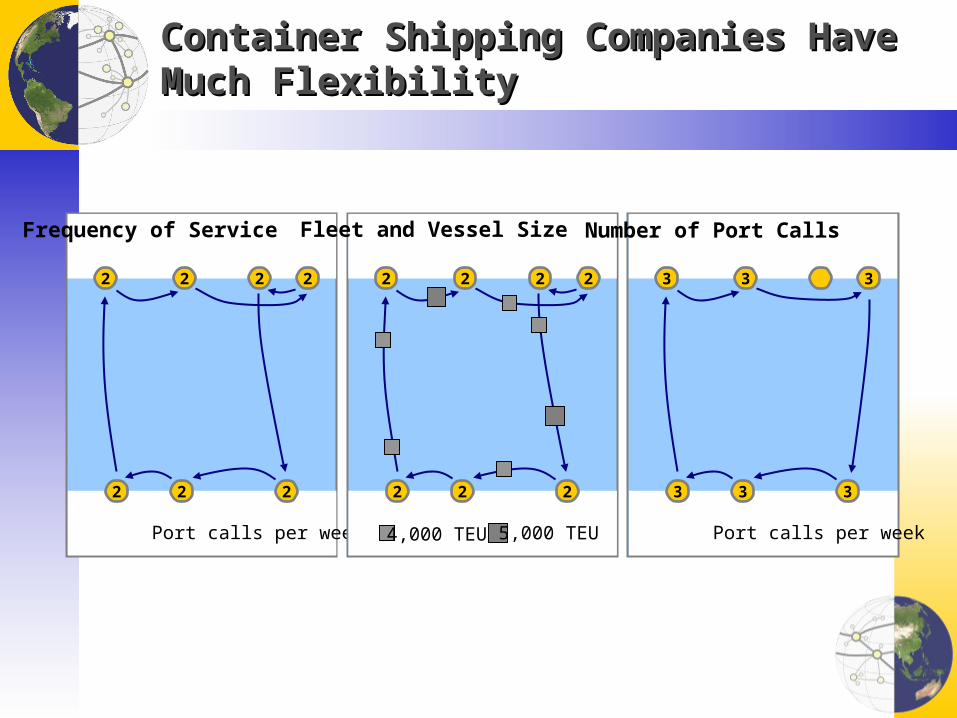

Container Shipping Companies Have Much Container Shipping Companies Have Much FlexibilityFlexibility

2 2 2 2

2 2 2

Port calls per week

2 2 2 2

2 2 2

4,000 TEU 5,000 TEU

3 3 3

3 3 3

Port calls per week

Frequency of Service Fleet and Vessel Size Number of Port Calls

Equa

tor

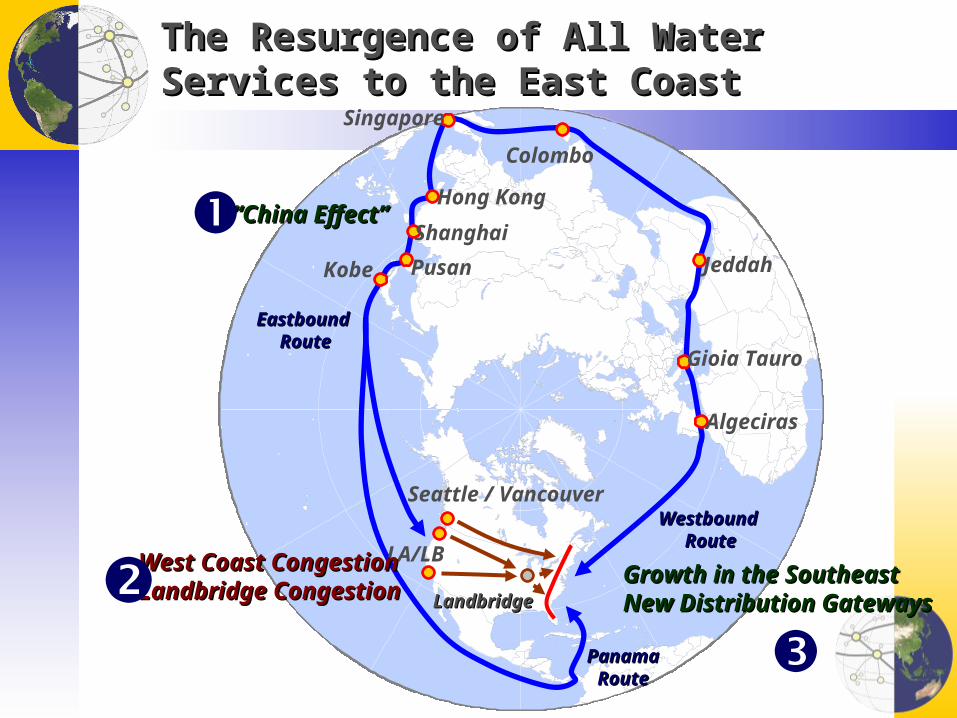

The Resurgence of All Water Services to the East The Resurgence of All Water Services to the East CoastCoast

LandbridgeLandbridge

Westbound Westbound RouteRoute

Eastbound Eastbound RouteRoute

Algeciras

Gioia Tauro

Jeddah

Colombo

Singapore

Hong Kong

Shanghai

PusanKobe

LA/LB

Seattle / Vancouver

PanamaPanamaRouteRoute

““China Effect”China Effect”

West Coast CongestionWest Coast CongestionLandbridge CongestionLandbridge Congestion

Growth in the SoutheastGrowth in the SoutheastNew Distribution GatewaysNew Distribution Gateways

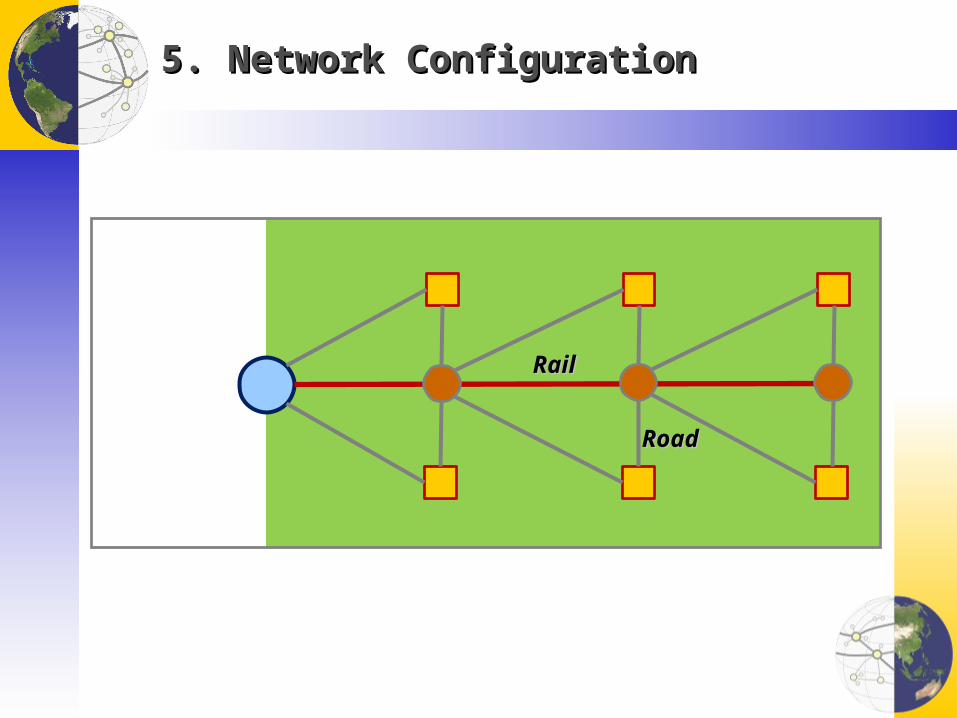

5. Network Configuration5. Network Configuration

RailRail

RoadRoad

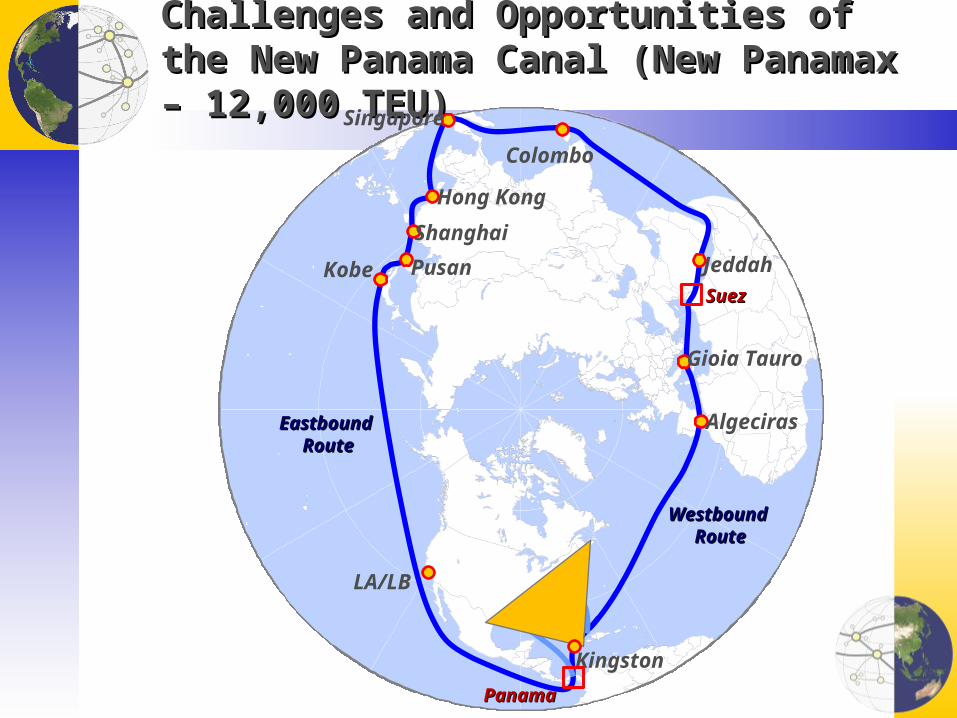

Challenges and Opportunities of the New Panama Challenges and Opportunities of the New Panama Canal (New Panamax – 12,000 TEU) Canal (New Panamax – 12,000 TEU)

Equa

tor

Westbound Westbound RouteRoute

Eastbound Eastbound RouteRoute

Algeciras

Gioia Tauro

Jeddah

Colombo

Singapore

Hong Kong

Shanghai

PusanKobe

LA/LB

Kingston

PanamaPanama

SuezSuez

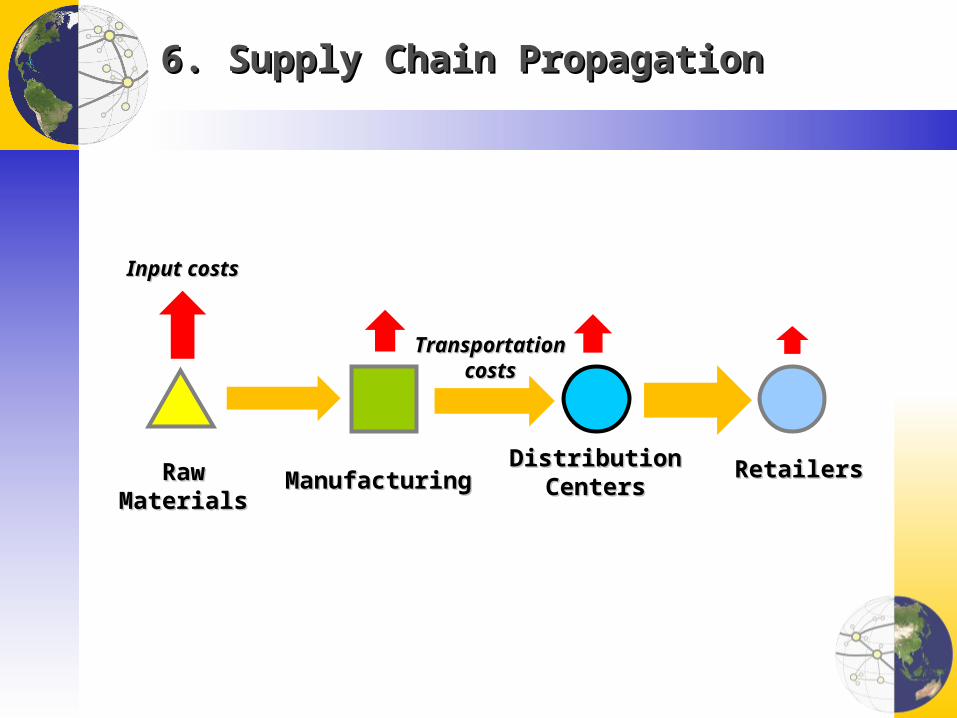

6. Supply Chain Propagation6. Supply Chain Propagation

RawRawMaterialsMaterials

DistributionDistributionCentersCenters

RetailersRetailersManufacturingManufacturing

Input costsInput costs

TransportationTransportationcostscosts

Swallowing the PillSwallowing the Pill

0

1

2

3

4

5

6

7

8

World Oil Expenditures as % of GPD, 1972-2008

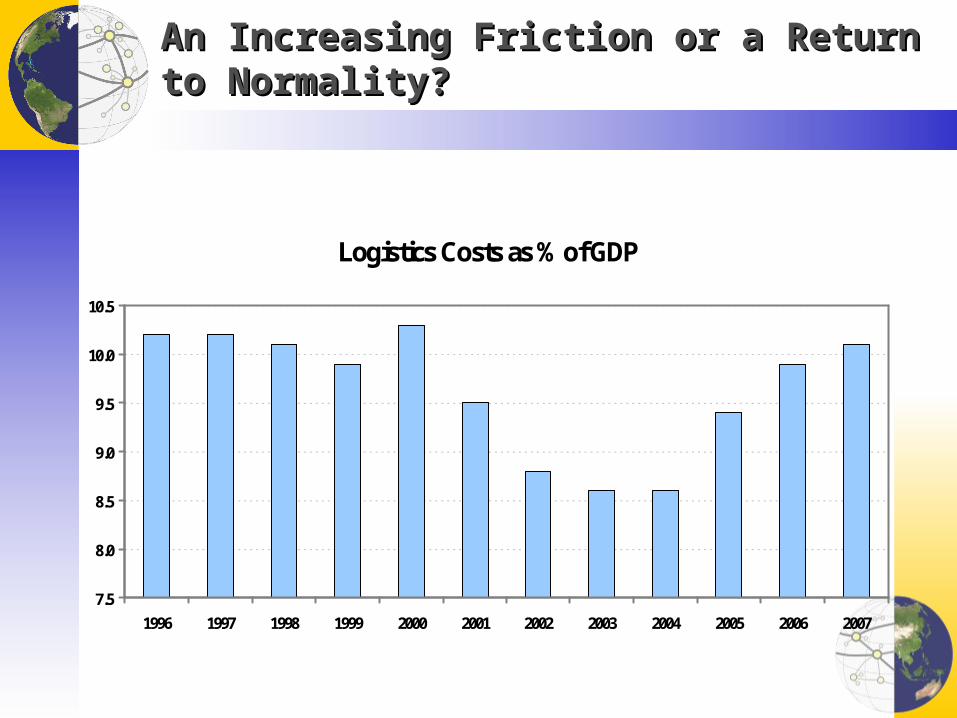

An Increasing Friction or a Return to Normality?An Increasing Friction or a Return to Normality?

Logistics Costs as % of GDP

7.5

8.0

8.5

9.0

9.5

10.0

10.5

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Breaking the Comparative Advantages ThresholdBreaking the Comparative Advantages Threshold

Costs of Shipping a 40 foot Container From China to the American East Coast

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

2000 ($30barrel)

2005 ($56barrel)

2008 ($135barrel)

($150 barrel) ($200 barrel)

From China

From Mexico

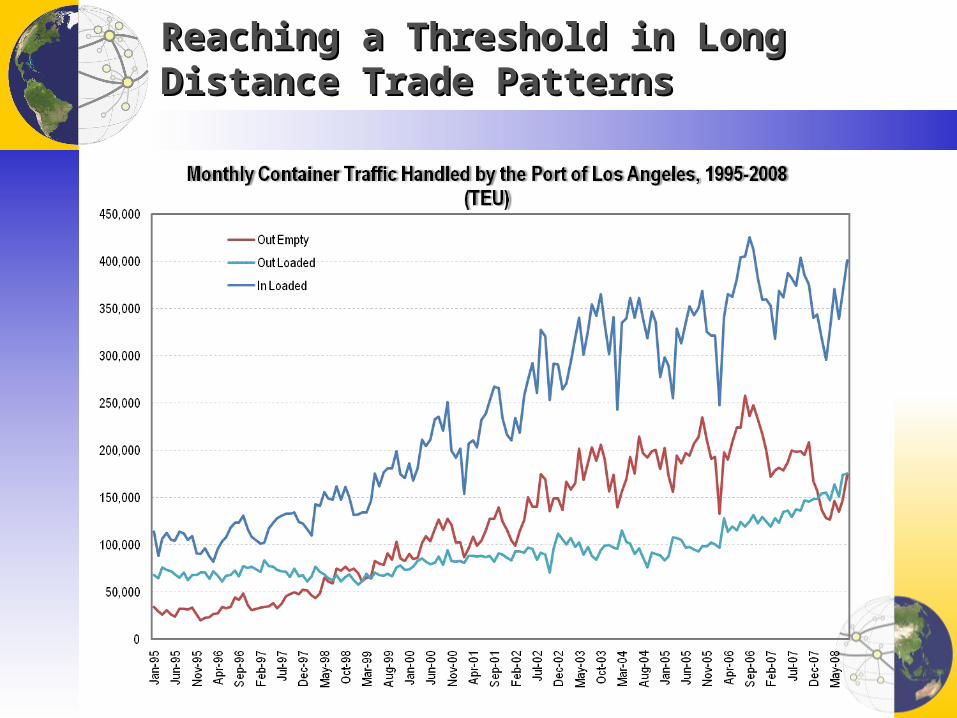

Reaching a Threshold in Long Distance Trade Reaching a Threshold in Long Distance Trade PatternsPatterns

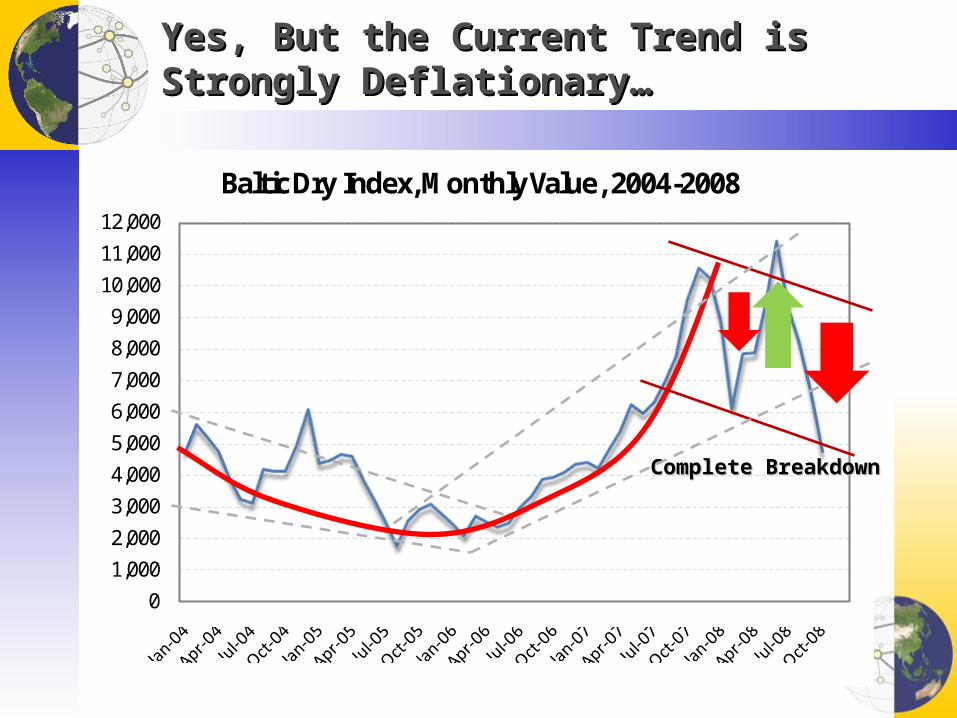

Yes, But the Current Trend is Strongly Deflationary…Yes, But the Current Trend is Strongly Deflationary…

01,0002,0003,0004,0005,0006,0007,0008,0009,00010,00011,00012,000

Baltic Dry Index, Monthly Value, 2004-2008

Complete BreakdownComplete Breakdown

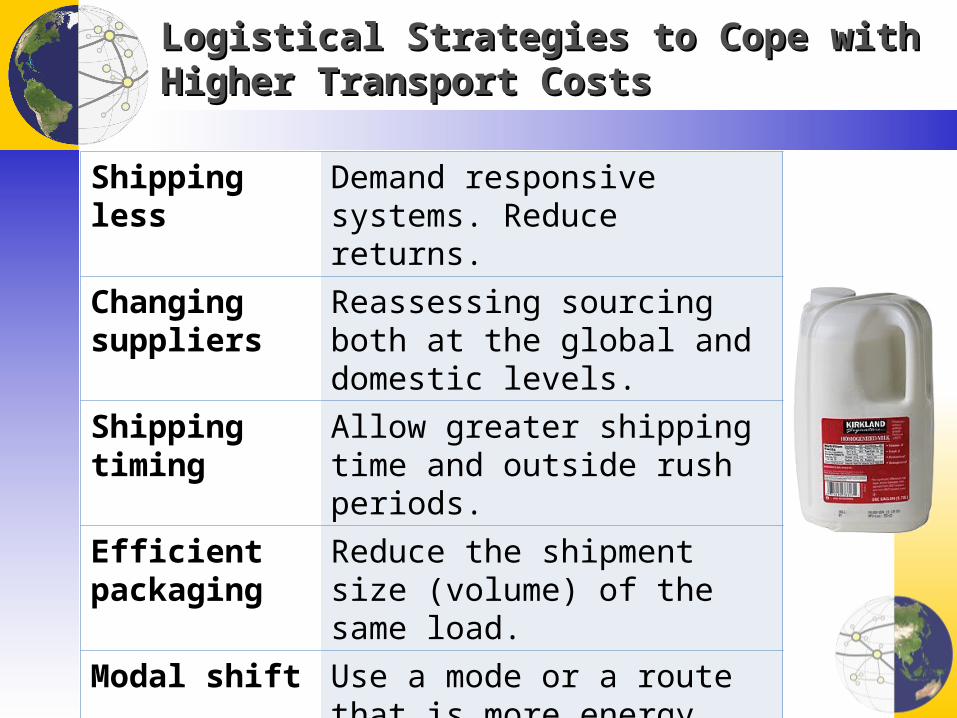

Logistical Strategies to Cope with Higher Transport Logistical Strategies to Cope with Higher Transport CostsCosts

Shipping less Demand responsive systems. Reduce returns.

Changing suppliers

Reassessing sourcing both at the global and domestic levels.

Shipping timing Allow greater shipping time and outside rush periods.

Efficient packaging

Reduce the shipment size (volume) of the same load.

Modal shift Use a mode or a route that is more energy efficient.

Conclusion: A Phase of Creative DestructionConclusion: A Phase of Creative Destruction

■ Impacts complex to assess• Many factors, processes and consequences.• As usual, analyzing the transition is prone to understatements

and exaggerations.• High energy prices have positive consequences … to a limit:

• Force a reconsideration of practices and conservation.• Better allocation of resources.

RealityRealityRealityReality